personal finance

Auto Added by WPeMatico

Auto Added by WPeMatico

FinanZero, a Brazilian online credit marketplace, announced today that it has closed a $7 million round of funding — its fourth since it launched in 2016. It has raised a total of $22.85 million to date.

The real-time online loan broker allows people to apply for a personal loan, a car equity loan or a home equity loan for free and receive an answer in minutes. A key to FinanZero’s success is that it doesn’t offer the loans itself, but has instead partnered with about 51 banks and fintechs who back the loans.

FinanZero is based in Brazil’s financial capital, São Paulo, and has 52 employees.

“From day one we said, ‘We only work with a success fee,’ so we only get paid when the customer signs the loan contract,” said Olle Widen, the company’s co-founder and CEO.

Instead of charging the customer, FinanZero gets a commission from one of its partners, and with a growing volume of credit applications — an average of 750,000 applications per month — the company has seen 61% revenue growth from 2019-2020.

Olle Widen, co-founder and CEO of FinanZero. Image Credits: FinanZero

The Brazilian finance and banking market has been ripe for disruption, as it has traditionally favored the rich.

Those with low incomes — the vast majority of Brazilian citizens — are then left with few options when it comes to financing, and which in turn forces them into compounding debt from which they’ll likely never escape. Traditionally, young Brazilians have lived with their families until they got married, and while there is a cultural aspect to it, the bottom line is that mortgages were infinitely hard to get approved.

With products like FinanZero and Nubank — Latin America’s largest digital bank — Brazilians are starting to see more economic mobility and independence from the legacy institutions that dictated their lives for so long.

Widen, who is Swedish, moved to Brazil about 10 years ago for personal reasons, and while there, was pitched the idea of FinanZero by Webrock Ventures, an investment company focused on bringing Nordic innovation to Brazil.

At the time, Swedish startup Lendo — a precursor to FinanZero — was making waves in Sweden, and the team felt that a similar model would succeed in Brazil, a country known for its bureaucracy and red tape, and thus primed for a streamlined and hassle-free approach to loans.

The original idea was to just copy Lendo, Widen said, but as others have discovered, along the way the team needed to “tropicalize” the product and the experience, meaning they had to build a custom solution for the Brazilian market and its people.

“The founder of Lendo was a childhood friend of mine,” said Widen, of his close ties to the Swedish fintech.

To apply for a loan on FinanZero you don’t need to provide your credit score. Instead, all you need is a utility bill (proof of address), proof of income and your government ID. The process is so simple, Widen said, that 92% of loan applications are initiated from a smartphone.

“Our business model is very based on the bank’s risk appetite and we saw 60% growth from 2019-2020. We are close to 3 million visits per month, about 1.5 are unique and in March of 2021, we had 800,000 people fill out the entire loan form. We have about a 10% approval rating across all products,” Widen said.

The round was led by the Swedish investors VEF, Dunross & Co, and Atlant Fonder, which are all previous investors in the company. The funding will go toward marketing — most of which will be on T.V. — product development, and talent acquisition.

Powered by WPeMatico

Founders, entrepreneurs, and tech executives in the know realize they may be able to avoid paying tax on all or part of the gain from the sale of stock in their companies — assuming they qualify.

If you’re a founder who’s interested in exploring this opportunity, put careful consideration put into the formation, operation and selling of your company.

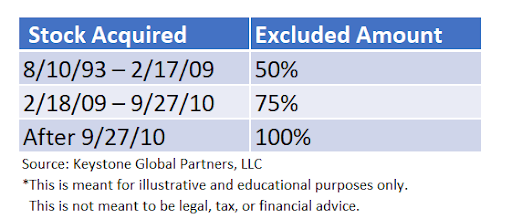

Qualified Small Business Stock (QSBS) presents a significant tax savings opportunity for people who create and invest in small businesses. It allows you to potentially exclude up to $10 million, or 10 times your tax basis, whichever is greater, from taxation. For example, if you invested $2 million in QSBS in 2012, and sell that stock after five years for $20 million (10x basis) you could pay zero federal capital gains tax on that gain.

These tax savings can be so significant, that it’s one of a handful of high-priority items we’ll first discuss, when working with a founder or tech executive client. Surprisingly, most people in general either:

Founders who are scaling their companies usually have a lot on their minds, and tax savings and personal finance usually falls to the bottom of the list. For example, I recently met with someone who will walk away from their upcoming liquidity event with between $30-40 million. He qualifies for QSBS, but until our conversation, he hadn’t even considered leveraging it.

Instead of paying long-term capital gains taxes, how does 0% sound? That’s right — you may be able to exclude up to 100% of your federal capital gains taxes from selling the stake in your company. If your company is a venture-backed tech startup (or was at one point), there’s a good chance you could qualify.

In this guide I speak specifically to QSBS on a federal tax level, however it’s important to note that many states such as New York follow the federal treatment of QSBS, while states such as California and Pennsylvania completely disallow the exclusion. There is a third group of states, including Massachusetts and New Jersey, that have their own modifications to the exclusion. Like everything else I speak about here, this should be reviewed with your legal and tax advisors.

My team and I recently spoke with a founder whose company was being acquired. She wanted to do some financial planning to understand how her personal balance sheet would look post-acquisition, which is a savvy move.

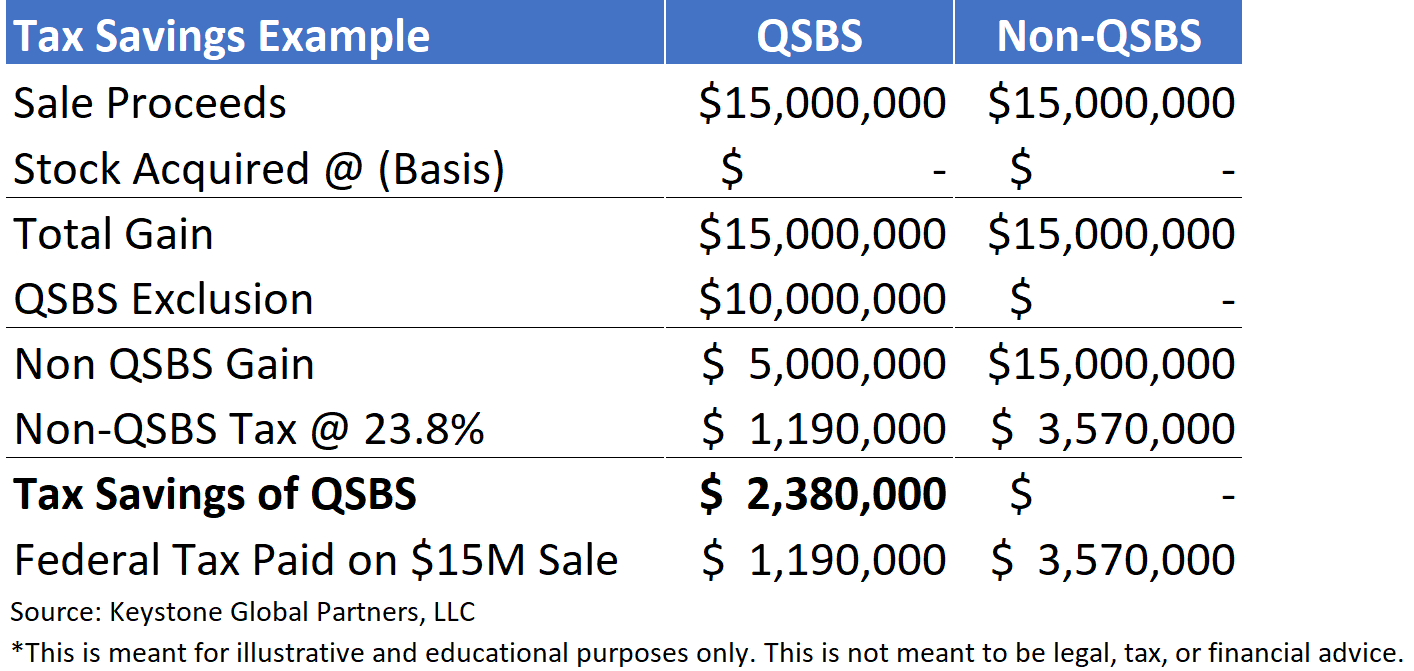

We worked with her corporate counsel and accountant to obtain a QSBS representation from the company and modeled out the founder’s effective tax rate. She owned equity in the form of company shares, which met the criteria for qualifying as Section 1202 stock (QSBS). When she acquired the shares in 2012, her cost basis was basically zero.

A few months after satisfying the five-year holding period, a public company acquired her business. Her company shares, first acquired for basically zero, were now worth $15 million. When she was able to sell her shares, the first $10 million of her capital gains were completely excluded from federal taxation — the remainder of her gain was taxed at long-term capital gains.

This founder saved millions of dollars in capital gains taxes after her liquidity event, and she’s not the exception! Most founders who run a venture-backed C Corporation tech company can qualify for QSBS if they acquire their stock early on. There are some exceptions.

A frequently asked question as we start to discuss QSBS with our clients is: how do I know if I qualify? In general, you need to meet the following requirements:

When in doubt, follow this flowchart to see if you qualify:

Powered by WPeMatico

Home ownership has long been touted as the American dream. But rising rates of mortgage debt and student loan debt are making the pursuit of home ownership a nightmare. Debt-burdened individuals or those with inconsistent or tight cash flow can not only struggle to get credit loan approval when buying a home but also struggle to satisfy monthly mortgage payments even after purchase.

Patch Homes is hoping to keep the proverbial American dream alive. Patch looks to provide homeowners with cash flow and liquidity by allowing them to monetize their homes without taking on debt, interest or burdensome monthly payments.

Today, Patch took another big step in making its vision a far-reaching reality. The company has announced it has raised a $5 million Series A round led by Union Square Ventures (USV), with participation by from Tribe Capital and previous investors Techstars Ventures, Breega Capital and Greg Schroy.

Patch Home looks to partner with homeowners by investing up to $250,000 (with an average investment of ~$100,000) for an equity stake in the home’s value, generally in the 5% to 20% range. Homeowners aren’t subject to any interest or recurring payments and have 10 years to pay back Patch’s investment. Upon doing so, the only incremental money Patch receives is its portion of the change in the home’s value over the course of the 10-year period. If the value of the home goes down in value, Patch willingly takes a loss on its investment.

According to Patch Homes CEO and co-founder Sahil Gupta, one of the major motivations behind the company’s model is to align Patch’s incentives with the homeowners’, allowing both parties to think of each other as trusted partners even after financing. After Patch’s investment, the company provides a number of ancillary services to homeowners, such as credit score monitoring, as well as home value and property tax tracking.

In one instance recounted by Gupta in an interview with TechCrunch, Patch even covered three months of an owner’s mortgage during a liquidity crunch for his small business, allowing him to maintain his home and credit score. Patch is incentivized to provide all services that can help ensure an increase in home value, benefiting both Patch and the homeowner, with the homeowner earning the majority of the asset’s appreciated value.

Additionally, since Patch’s model isn’t focused on a homeowner’s ability to pay back a loan, interest or periodic payments, Patch is able to provide financing to more people. Patch is able to help those with more variable qualifications that struggle to get traditional loans — such as a 1099 contracted worker — monetize their illiquid assets with less harsh or restrictive terms and without increasing their debt burden. Gupta described this as solving the core problem of providing liquidity to asset-rich but cash-flow sensitive people.

Patch is not only looking to provide easier liquidity to more homeowners, but they’re trying to do so faster than traditional lenders. Interested customers can first receive a free estimate of whether Patch will invest in their home or not, how much it’s willing to invest and what percentage equity it will take — primarily based on Patch’s machine learning models that focus on asset, market and location-level attributes.

After the initial estimate, a Patch home advisor will educate the customer on the product and start a formal application process, which includes your standard income and credit score verification, which takes 5-10 days. All-in, homeowners have the ability to get money in as little as 14 days, a significantly shorter timeline than your standard home credit process. Once the investment is made, owners have full freedom with how they use the money.

According to Patch, while its customers come from a diverse set of backgrounds, many either with accumulated debt have to pay down the net or may struggle making monthly payments. The average Patch homeowner uses 40% of the investment to eliminate debt, adds 40% to their savings account or passive income and invests 20% into home improvements.

To date, Patch has raised a total of $6 million and believes the latest round of funding will help scale its operations as they team up with advisors like USV that have experience scaling fintech companies (such as a Lending Club or Carta). The funds will be used to invest in product and Patch’s clearing technology in order to further expedite Patch’s lending process.

Patch also hopes to use the investment to help them gradually expand their footprint, with the goal of eventually having a presence all 50 states. (Patch is currently available in 11 regional markets within California and Washington and expects to be in 18 regional markets by the end of the year including those in Utah, Colorado and Oregon.)

and Sahil Gupta (R)")

Image via Patch Homes

What makes home ownership so galvanizing for the Patch team? Patch CEO Sahil Gupta spent years putting his Carnegie Mellon financial engineering degree to work in banking and finance, as well as in financial products and strategy positions at fintech startups backed by heavy hitters such as YC and Goldman Sachs.

After realizing the majority of the U.S. population are homeowners, but were struggling to make monthly payments or save for the future, Sahil wanted to figure out to take an illiquid asset like a home and make it easily accessible.

Around the same time, Sahil’s co-founder Sundeep Ambati was working as a contractor on a new business venture of his and was struggling to get a home equity loan. While these circumstances ultimately led Sahil and Sundeep to found Patch Homes in 2016 out of the Techstars New York accelerator program, the deeper motivation behind Patch can be traced back nearly 30 years when Sahil’s father made an equity-sharing agreement with his brother as they were building his family’s home in India.

With a growing family and a pregnant wife, Sunil’s father was adamant about living debt-free, so his brother provided an investment in exchange for an equity stake in the house. According to Sahil, the home is still in the family and has appreciated substantially in value to the benefit of both Sahil’s father and his brother. Longer-term, Patch wants to be the preferred partner for home ownership, helping reduce cash-tight owners’ financial anxiety without the debilitating weight of debt.

“Some companies want to help people buy or sell homes, but home ownership really begins after that point. Patch is built to be inside the home with you and everything that comes thereafter,” Gupta told TechCrunch.

“Patch was created to partner with homeowners to help them unlock their home equity so they can achieve their financial goals along every step of their home ownership journey.

Powered by WPeMatico

When Stackin’ initially pitched itself as part of the Techstars Los Angeles accelerator program two years ago, the company was a video platform for financial advice targeting a millennial audience too savvy for traditional advisory services.

Now, nearly two years later, the company has pivoted from video to text-based financial advice for its millennial audience and is offering a new spin on lead generation for digital banks.

The company has launched a new, no-fee, checking and savings account feature in partnership with Radius Bank, which offers users a 1% annual percentage yield on deposits.

And Stackin’ has raised $4 million in new cash from Experian Ventures, Dig Ventures and Cherry Tree Investments, along with supplemental commitments from new and previous investors including Social Leverage, Wavemaker Partners and Mucker Capital.

“Stackin’ has a unique and highly effective approach to connect and communicate with an entire generation of younger consumers around finance,” said Ty Taylor, group president of Global Consumer Services at Experian, in a statement.

Founded two years ago by Scott Grimes, the former founder of Uproxx Media, and Kyle Arbaugh, who served as a senior vice president at Uproxx, Stackin’ initially billed itself as the Uproxx of personal finance.

It turns out that consumers didn’t want another video platform.

“Stackin’ is fundamentally changing the shape and context of what a financial relationship means by creating a fun, inclusive and judgement free environment that empowers our users to learn and take action through messaging,” said Scott Grimes, CEO and co-founder of Stackin’, in a statement. “This funding allows us to build out new features around banking and investing that will enhance the relationship with our customers.”

Later this fall the company said it would launch a new investment feature that will encourage Stackin’ users to participate in the stock market. It’s likely that this feature will look something like the Acorns model, which encourages users to invest in diversified financial vehicles to get them acquainted with the stock market before enabling individual trades on stocks.

According to Grimes, the company made the switch from video to text in March 2018 and built a custom messaging platform on Twilio to service the company’s 500,000 users.

“In a short time, we have built a large customer base with a demographic that is typically hard to reach. Having financial institutions like Experian come on board as an investor is a testament that this model is working,” Grimes wrote in an email.

Powered by WPeMatico

With an IPO on the horizon, subprime lender Elevate will have an additional $545 million credit faculty to support its growing customers. Elevate’s niche right now is providing loans to borrowers with creditscores between 575 and 625. As the company expands, it wants to provide loans to customers with even lower credit-scores. Ken Rees, CEO of Elevate, is quick to note that 65 percent… Read More

With an IPO on the horizon, subprime lender Elevate will have an additional $545 million credit faculty to support its growing customers. Elevate’s niche right now is providing loans to borrowers with creditscores between 575 and 625. As the company expands, it wants to provide loans to customers with even lower credit-scores. Ken Rees, CEO of Elevate, is quick to note that 65 percent… Read More

Powered by WPeMatico

Penny, a personal finance bot we reviewed last fall, has raised $1.2 million in seed funding from Social Capital. As a refresher, the app offers a chat-based interface that offers advice tailored to your personal finances. This advice includes things like how much you spend on food each week, how this month’s spending compares to last month’s and even income graphs. One unique… Read More

Penny, a personal finance bot we reviewed last fall, has raised $1.2 million in seed funding from Social Capital. As a refresher, the app offers a chat-based interface that offers advice tailored to your personal finances. This advice includes things like how much you spend on food each week, how this month’s spending compares to last month’s and even income graphs. One unique… Read More

Powered by WPeMatico

Netflix, Hulu, Amazon Prime, Birchbox, Spotify, HBO NOW, newspapers, box of the month clubs, meal services, and more: The rise of subscription-based commerce means consumers now pay for a number of items on a recurring basis. But even a few dollars spent here and there have a way of adding up, and eating into your household’s budget. A new startup called Trim wants to help you… Read More

Netflix, Hulu, Amazon Prime, Birchbox, Spotify, HBO NOW, newspapers, box of the month clubs, meal services, and more: The rise of subscription-based commerce means consumers now pay for a number of items on a recurring basis. But even a few dollars spent here and there have a way of adding up, and eating into your household’s budget. A new startup called Trim wants to help you… Read More

Powered by WPeMatico

Honeydue is a mobile app that aims to reduce money-related arguments between couples by offering tools to share information on respective account balances and spending.

Honeydue is a mobile app that aims to reduce money-related arguments between couples by offering tools to share information on respective account balances and spending.