Peloton

Auto Added by WPeMatico

Auto Added by WPeMatico

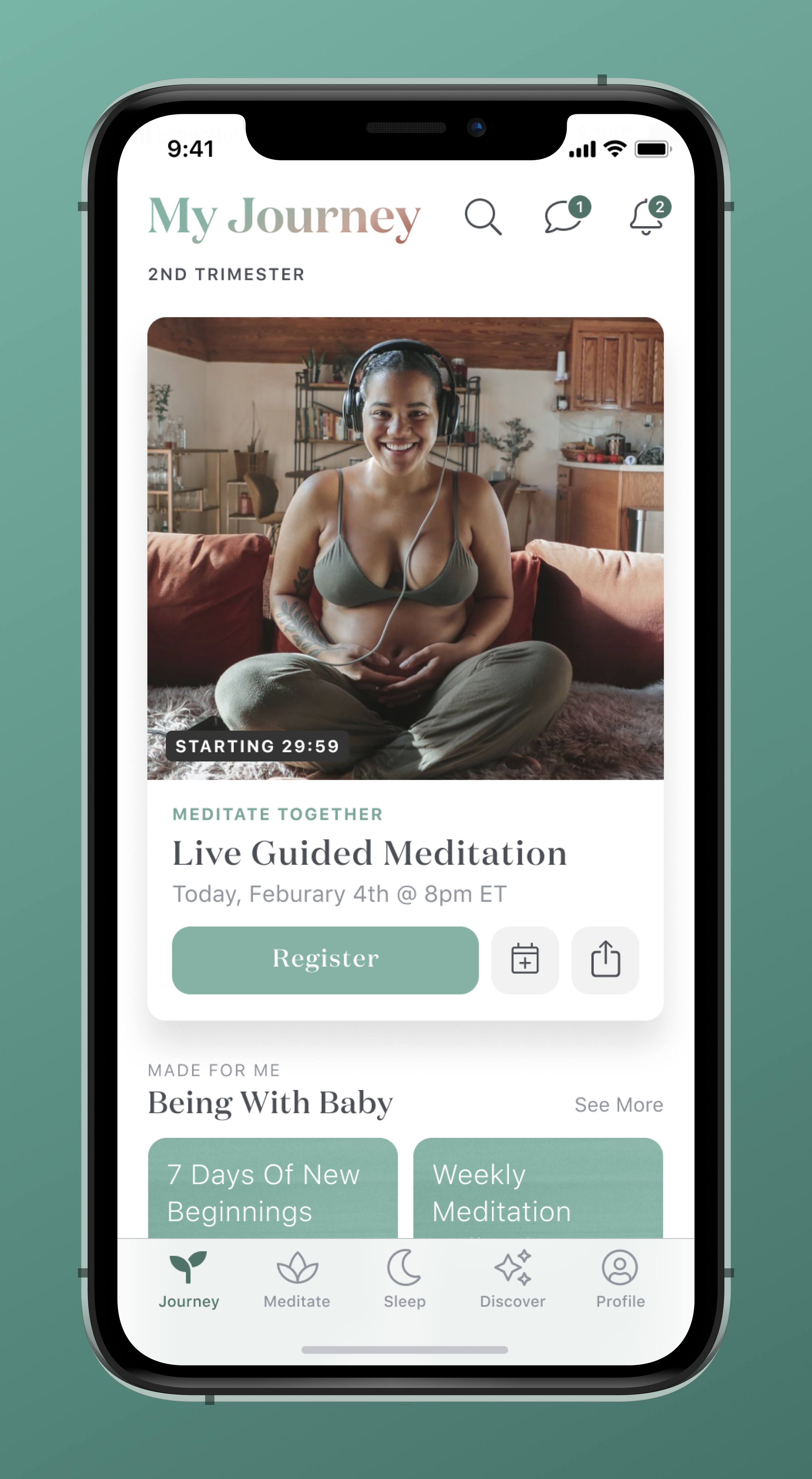

Nathalie Walton almost didn’t become a mother. Her risky pregnancy caused her placenta to burst during childbirth, almost killing her and her son last year. Walton, who feels lucky to have survived, says the haunting experience made her an example of a reality she had long known: To be a pregnant Black woman is to be at risk, regardless of economic background.

The stress of her pregnancy led Walton to download Expectful, a meditation and sleep app for new mothers. She recalls stabilizing, emotionally and physically, within a week, bringing an otherwise “soft landing” to a volatile pregnancy.

Weeks after delivering her son, Everett, Walton just so happened to hear of an advisory role opening at Expectful. Even though she was mid-maternity leave from her managerial role at Airbnb, she jumped at the opportunity.

“I definitely had a full-time job, I had a newborn baby,” Walton said. But, she says, it was an opportunity to be entrepreneurial in a sector she cared about. Even if it was just for a few months.

And now, Walton is the chief executive of the company. The business is pivoting its product strategy to grow beyond recorded meditations. Walton helped it raise its first millions in venture capital, making her one of the few dozen Black female founders to do so. New financing and the boom of the mental health focus amid the coronavirus pandemic puts Expectful in a coveted spot. And it puts Walton, who is at the helm of a company for the first time, in a pressure-cooker spotlight.

Even in the world of startups, going from user to chief executive in less than a year is a remarkable feat. But it’s not one that she rushed.

Walton graduated from Georgetown and immediately joined the New York banking world. After a few years as an analyst at JP Morgan, though, she became unsatisfied with the work.

“I think I had a quarter-life crisis,” Walton said. Searching for new opportunities, she ended up at a prospective students day at Stanford University in what would become a pivotal moment in her life.

“For the first time, I met entrepreneurs and saw an actual concept that you can pursue a career you like, be successful and make a difference in the world,” she said. Walton eventually applied, and got accepted, to Stanford Graduate School of Business (GSB), a prestigious program that produces founders and top executives. It was then that she realized she wanted to be a chief executive one day.

“I admired them, but I just didn’t see the pathway for me to get there,” she said, of the entrepreneurs she met, who were then largely white and male. “I didn’t have the confidence.”

So, she set that hope aside and pursued intrapreneurship, which would let her join a stable organization and act as a mini-founder within it. Employees in this role are tasked with building a startup within a startup, whether that is rooting an innovative idea or leading an experiential team. Corporations have long embraced this idea to bring momentum to otherwise red-tapey processes.

Walton joined eBay and soon rose to work as the head of business operations and development. Her work helped the company break into 3D printing.

Over the years, this has been the defining characteristic of Walton: join an organization, build a scrappy idea from scratch, and then do it all over again. She has held roles in Airbnb and Google that all required her to have the agility of a founder convincing people on a moonshot vision, and the rigor of a manager who can get a deal done.

She had the same vision heading into an advisory role at Expectful. But when Walton landed a key Expectful partnership with Johnson & Johnson, then-CEO and founder Mark Krassner had an idea.

Before starting Expectful, Krassner experienced the benefits of meditation firsthand. He also saw his mother face depression, which made him realize how meditation could have a positive impact on others. After seeing research that showed how meditation could positively impact a pregnancy, he began thinking of a solution in this cross-section. He eventually started a course on Teachable, a startup that lets anyone create and monetize an online class, with 15 moms and a guided meditation.

Over time, the idea stuck. Krassner eventually turned his course into a 12-person startup. Under his leadership, Expectful grew to profitability and over 13,000 paid users. Its conversion rate from free to paid users was five times higher than industry standards, the company claims.

That said, from the moment Mark Krassner started Expectful, he knew he was an unlikely founder. He doesn’t have any children, so leading a meditation and sleep app for new mothers comes with its own hurdles.

“As a male founder with no kids, it was on my mind from day No. 1,” Krassner said. He eventually wanted to put a female at the head of the company, he says. Walton was the obvious choice.

Walton returned to Airbnb after her maternity leave right as Airbnb had aggressive COVID-19 layoffs. While her job was saved, her team disappeared as part of the cuts. She started looking for jobs, and received lucrative offers from Facebook, Apple, Google and Amazon. When she told Krassner she was leaning toward a lead product manager position at Amazon, he replied with an offer to take over Expectful’s entire business.

“I think it caught her off guard,” Krassner said, who is still a board member at the company. “Usually you don’t think a CEO is looking for [a new CEO] unless things are going to hell in a handbasket.”

Expectful began as a guided meditation library, which will continue to be its core. But now, Walton wants to take advantage of that momentum and evolve the company into a “go-to wellness resource for hopeful, expecting and new parents.”

The language suggests that the startup is evolving in how it markets itself. Right now, the site has a number of references to “motherhood” and women. But Walton says Expectful defines a mother by anyone who identifies themselves as one. While the startup primarily has content geared toward the gestational parent, or the one who gives birth to the child, Walton says they have a “a partner’s library for non-gestational parents that identify as non-gestational mothers, fathers, or however they choose to identify.”

Walton plans to pivot the startup in three phases: content, marketplace and community.

For content, Expectful wants to organize pregnancy-related information. Currently, a lot of information or advice around pregnancy lives in books or in-person classes. But the learning experience, which Walton says is similar to middle school-style lectures, doesn’t feel built for this century.

The next step in her plan is digitizing the service providers that help women through pregnancy. In simpler words, replace the disorganized recommendations in Facebook groups for parents.

“When I went to ask my OB-GYN for recommendations for a doula, she gave me a sheet of paper with the names of 10 doulas,” she said. “You have to text the doula, ask them questions and if they want to meet up — it all feels yucky.” Expectful wants to put all that information in one platform so moms can access tips and recommendations from the ease of their homes.

The end-product here would be a peer-reviewed platform that can help a mom find everything from a therapist to a live-in nanny, with reviews built-in.

Finally, Walton wants to invest in the community. Expectful recently launched Mother Circles, which connects postpartum mothers into support cohorts led by a doula facilitator. The circles include six weekly video calls, a group chat and 500 hours of on-demand doula support.

Image Credits: Expectful

Part of Walton’s focus through all of these priorities is to invest in Black maternal health outcomes. Her own experience, she says, showed her how even a “Stanford-educated wellness junkie” such as herself can be at a high-risk for pregnancy because of her skin color.

It’s a lofty goal, even with the promising growth and strong library of guided meditations. The competition is steep. One of Expectful’s closest competitors is Peanut, a social network for moms used by over 1.2 million people. Mahmee, a digital support network for postpartum mothers, has raised $3 million and views itself as complementary to Expectful. Headspace has launched its own motherhood meditation series, but it is not as comprehensive as Expectful’s.

“I think we’re able to connect with women in a way that some of these other companies aren’t,” Walton said. “People are paying for the service, so they clearly need it.”

While Walton declined to share new user metrics, she said that the company’s revenue has grown 100% since March 2020.

Long-term, Expectful wants to mimic Peloton’s playbook in terms of getting premium content and community to the right audience. Still, growing from a startup to a venture business requires more than just ambition and market fit. It requires the ability to exponentially grow and keep growing.

A handful of investors believe that Walton’s Expectful can do it. Expectful raised $3 million in a seed financing round led by Harlem Capital. Indicator Ventures, Sequoia Scout Fund, Joyance Partners, Break Trail Ventures, Chinagona Ventures, Powerhouse Capital, AVG Basecamp Fund and Babylist also participated. Angel investors included Ellen Pao, Mike Smith and Ashley Mayer. The round also included $1.2 million in convertible SAFE notes, making the financing round a total of $4.2 million.

“Historically when I look at what black women raise fundraising, I feel fortunate that I’ve been able to raise this round,” Walton said.

Harlem Capital founding partner Henri Pierre-Jacques said that “obviously, given our focus we weren’t going to invest in a white male.” Walton’s “founder-market fit” is what made the firm invest, even with the hairy dynamic of an exiting CEO.

Mayer, head of communications at Glossier, was the one who introduced Walton to the woman who told her about the advisory role of Expectful. She says that Nathalie’s “path to entrepreneurship feels inevitable.

“It was always just a question of finding the space where her passions collided,” Mayer said.

As a new mother and new founder, Walton has had a busy balancing act of a year.

“I’m working more now than I have really in the last decade,” she said. “But I’ve never been more fulfilled because, as someone who went through this, and I’m still going through this, I feel so personally the level of pain that so many women suffer through.”

Powered by WPeMatico

So much can change in a day.

This morning, news that a trial COVID-19 vaccine candidate had an effective rate of more than 90% shook the financial world. The Pfizer vaccine is reportedly so effective, the company “will have manufactured enough doses to immunize 15 to 20 million people” by the end of the year, according to the New York Times, appears to have given investors the green light to pile back into companies harmed by the pandemic.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

The shift of money from shares that proved popular during the summer is massive and abrupt. Zoom and Peloton are down sharply this morning, while Uber and Lyft are soaring. Indeed, the Dow Jones Industrial Average and S&P 500 indices are up around 4.8% and 3.3% respectively, while SaaS and cloud share are off 3.5%.

Investors are taking money out of companies that were expected to do well thanks to the pandemic and moving that capital into firms that were weakened by the pandemic.

Our question for this morning: what do these changes mean for the economic forces that have broadly favored venture-backed startups? What happens to high-flying startups if the pandemic trade flips? What’s next for insurtech, edtech, fintech and SaaS? Let’s discuss.

Our question for this morning: what do these changes mean for the economic forces that have broadly favored venture-backed startups? What happens to high-flying startups if the pandemic trade flips? What’s next for insurtech, edtech, fintech and SaaS? Let’s discuss.

Short-term market movements do not always predict the future accurately, so we should not treat today’s trading as gospel.

That said, it’s not hard to draw some basic conclusions from the trading activity. Here’s what I think we can deduce from today’s stock market activity:

Powered by WPeMatico

During the most recent quarter, only a few earnings reports stood out from the rest. Zoom’s set of results were one of them, with the video-communications company showing enormous acceleration as the world replaced in-person contact with remote chat.

Another was Peloton’s earnings from the fourth quarter of its fiscal 2020, which it reported September 10th. The company’s revenue and profitability spiked as folks stuck at home turned to the connected fitness company’s wares.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Shares of Peloton have rallied around 4x since March, roughly the start of when the COVID-19 pandemic began to impact life in the United States, driving demand for the company’s at-home workout equipment. In late June, the leisure company Lululemon bought Mirror, another connected fitness company aimed at the home market for around $500 million.

With Peloton’s 2019 IPO and its growth along with Mirror’s exit in 2020, connected fitness is demonstrably hot, and private-market investors are taking notice. A recent Tweet from fitness tech watcher Joe Vennare detailing a host of recent funding rounds raised by “digital fitness” companies made the point last week, piquing our curiosity at the same time.

Is there really some sort of Peloton effect driving private investment into lots of connected fitness startups? How hot is the more nascent side of connected fitness?

This morning let’s take a look through some recent funding rounds in the space to get a feel for what’s going on. (If you’re a VC who cares about the sector, feel free to email in your own notes, subject line “connected fitness” please.) We’ll then execute the same search for Q3 2019 and see how the data compares.

To start with the current market I pulled a Crunchbase query for all Q3 funding rounds for companies tagged as “fitness” and then filtered out the cruft to get a look at the most pertinent funding events.

Here’s what I came up for for Q3 2020, to date:

Powered by WPeMatico

Matteo Franceschetti, CEO of Eight Sleep, would prefer that you don’t call his startup a mattress company.

Eight Sleep does sell mattresses, albeit smart ones packed with sensors and temperature regulation controls. The company has raised north of $70 million from backers including Founders Fund and Khosla Ventures. A great deal of this funding surrounds the idea that there is more untapped potential in the sleep economy than existing players in the space have been able to imagine.

While Franceschetti says he intends for his company to remain private for the “foreseeable future,” Eight Sleep is in a less-than-comfortable spot following Casper’s botched IPO last week. Though Casper’s stock popped on its first day of trading, the process of pricing its shares ended up leaving its private investors a bit less than ecstatic. Casper debuted trading at a value of $575 million, a far cry from the $1.1 billion private market valuation it had previously achieved.

Franceschetti has been aiming to transform Eight Sleep into a company more focused on a robust tech platform than your average bed-in-a-box company. The startup’s initial effort, a smart sleep cover for your existing mattress, evolved into a mattress with a layer of sensors that then transformed into a sensor-laden mattress with a heating and cooling unit, called “The Pod.” The company’s product development has aimed to build out a more end-to-end platform for sleep, something Franceschetti says has made him reticent to compare his company to other direct-to-consumer mattress companies.

Powered by WPeMatico

Now that the final technology IPOs of 2019 have touched down, it’s a good time to start looking back at what happened during the year. We’re hunting for trends as the clock winds down. Here’s one that’s obvious: Hardware startups are still struggling.

It’s cliché to note in startupland that hardware is hard. Everyone knows it. Making hardware is difficult by itself, but as all tech hardware requires software, hardware shops wind up needing wider domain expertise than pure-software startups. And that’s hard.

But even if a nuts-and-bolts tech company hits scale, it seems difficult to keep that momentum up.

This year we saw Peloton, a hybrid hardware and digital services company, go public and struggle. Despite a recent public market resurgence, the company is slipping back toward its IPO price. Today its equity is trading down about 6% to around $30 per share. The company’s IPO price of $29 is uncomfortably close to its current value.

2019’s IPO crop also included EHang, a late entry to the market (more here on its debut) that quickly began to lose altitude after it started to float. EHang traded up today, but the firm is still worth less than its IPO valuation, a reduced figure that was dinged during the China-based drone company’s march toward the public markets.

So, Peloton is about flat and EHang is down. That’s not a great mix of results for a year’s IPO class of hardware companies. Looking back in time, things don’t get much better.

NIO, a China-based electric car company (despite making this thing of beauty), has deleted about two-thirds of its value since its late-2018 U.S.-listed IPO. After going public at $6.25, shares of NIO are worth just $2.70 today.

Sonos also went public in the United States in 2018. It traded above its IPO price of $15 at first. Then it fell under $10 per share as 2018 came to a close. The smart speaker and stereo company spent 2019 recovering. It’s now worth its IPO price again, closing trading today worth about $14.80 per share.

If you go back to 2017, however, Roku has kicked ass. After pricing at $14 per share, the TV hardware and digital services firm is trading for $137 per share, a nearly 10x gain. But Roku was moving away from hardware at the time of its IPO, making it a somewhat poor example. Hardware revenues for Roku were just 31% of revenue in its most recent quarter, for example. That figure was 42% in the year-ago quarter. It will continue to fall.

We don’t need to go over what happened to Fitbit and GoPro, I don’t think.

Hardware can make a lot of money. Samsung and Apple make oceans of money from their hardware. Microsoft has managed to make Surface into a real business, with billions of dollars in yearly revenue. Amazon has a big hardware business with both consumer reading gadgets and consumer surveillance devices. Even Google is taking its new phone seriously enough to buy out a chunk of the NBA’s ad slots (I think it’s this one), according to my extensive in-market testing. Facebook is the laggard of the group.

But for smaller hardware companies going public, unless I’m missing a number of recent of IPOs — and I don’t think that I am — it’s a tough world out there.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

As with yesterday, Kate and Alex were both on-site at TechCrunch’s San Francisco headquarters to chat over the latest. Unlike yesterday, however, Equity brought along a guest: Sean Dempsey from Merus Capital. (Merus writes seed and Series A checks, with a focus on enterprise companies.)

And thus the three dove into the news. Early-stage first, to shake things up.

Kate wrote a story this week about a startup you might have forgotten about but who’s name probably rings a bell. Bodega! The company now goes by Stockwell, actually, and they’ve raised a whopping total of $45 million in VC funding. But what’s in a name after all? We debate.

Next we turned to an interesting company called Kapwing. What’s that you ask? “It’s a laymen’s Adobe Creative Suite built for what people actually do on the internet: make memes and remix media,” says TechCrunch’s Josh Constine. We’re intrigued.

This week Peloton priced and went public. The firm’s $29 per-share IPO price was top of its proposed range ($26 to $29). The public markets, however, decided that the unicorn had reached too high.

So, shares of the high-end exercise company dropped, wrapping the day down about 11%. A good IPO first day this was not, though the company did manage to raise more capital than it might have with more conservative pricing. (Peloton has a yucky multi-class share structure that we touched on as well; it seems that all the big companies these days are opposed to regular governance.)

Next we turned to the Vox-NYMag merger. It’s a bit out of our territory but it’s a digital media deal, so we were interested. After all, the two of us have spent our entire careers in digital media and we have a vested interest in these companies surviving.

We honestly tried to get all the WeWork out of our system yesterday. We wanted to include zero WeWork content on this episode. But WeWork keeps doing things, so here we are.

Keeping things as brief as we can, WeWork is going to divest some companies that it bought (more on what we thought it was up to, here) including its jet, and the firm is looking to take on more capital. Unsurprisingly.

All that and we’re done for this week. Chat you all at Disrupt!

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Spotify, Pocket Casts, Downcast and all the casts.

Powered by WPeMatico

This morning, Peloton (NASDAQ: PTON), the tech-enabled stationary bicycle and fitness content streaming company, raised $1.2 billion in its NASDAQ initial public offering. Despite dropping more than 10% in its first day of trading — ultimately closing down 11% at $25.84 per share — the IPO was a bona fide success. Peloton, once denied (over and over again) by VC skeptics, now has hundreds of millions of dollars to take its business into a new era. One in which, the media, hardware, software, logistics and social company attempts to become a generation-defining company akin to Apple.

Founded in 2012 — six years after Soul Cycle opened its first cycling studio in New York’s Upper East Side and two years before a Soul Cycle founder, Ruth Zukerman, jumped ship to launch her own indoor cycling business, Flywheel Sports — a man by the name of John Foley made the ambitious, some might say foolish, decision to start a company that would sell these exercise bikes direct-to-consumer. That way, you could take a Soul Cycle class, in essence, in the comfort of your own home. Even better, technology would improve the experience.

As my colleague Josh Constine recently described it, these bikes come outfitted with a 22-inch Android screen, transforming an outdated exercising experience and bringing it into 2019: “It makes lazy people like me work out. That’s the genius of the Peloton bicycle. All you have to do is Velcro on the shoes and you’re trapped. You’ve eliminated choice and you will exercise,” Constine writes.

Peloton’s ability to get people exercise — a feature driven by its talented instructors (some of whom were poached from competitor Flywheel Sports) — ultimately had venture capital investors funneling $1 billion, roughly, into the business. Today, Peloton operates dozens of showrooms across the U.S., counts 1.4 million total community members — defined as any individual who has a Peloton account — and over 500,000 paying subscribers. Why? Because the company, as stated in its IPO prospectus, “sells happiness.”

“Peloton is so much more than a Bike — we believe we have the opportunity to create one of the most innovative global technology platforms of our time,” writes Foley. “It is an opportunity to create one of the most important and influential interactive media companies in the world; a media company that changes lives, inspires greatness, and unites people.”

Peloton’s flagship product, a tech-enabled stationary bike.

Peloton’s community coupled with the high margins on sales of its $2,245 bikes had the company reporting $915 million in total revenue for the year ending June 30, 2019, an increase of 110% from $435 million in fiscal 2018 and $218.6 million in 2017. Its losses, meanwhile, hit $245.7 million in 2019, up significantly from a reported net loss of $47.9 million last year.

What’s next for Peloton? The opportunities are endless, given the company’s firm seat at the intersection of hardware, software, media content and more. A third product may be in the works, expansion to international markets or new instructors. Peloton is going after a massive market ripe for disruption. What’s certain is that we’ll see a whole lot of cash flowing into fitness tech copycats in the next couple of years.

Peloton, following a number of lukewarm consumer IPOs (Uber), nearly doubled its valuation to $8.1 billion this morning after pricing its IPO at the top of its range, $29 per share. To answer some of our most burning questions, we chatted with Peloton’s president William Lynch, the former CEO of Barnes & Noble, about the float.

The following conversation has been edited for length and clarity.

Peloton president and former Barnes & Noble CEO William Lynch.

Kate Clark: What’s next for Peloton?

William Lynch: We now have over a billion in capital to fuel more growth, especially in the area of product innovation.

Powered by WPeMatico

It makes lazy people like me work out. That’s the genius of the Peloton bicycle. All you have to do is velcro on the shoes and you’re trapped. You’ve eliminated choice and you will exercise. Through a succession of savvy product design choice I’ll break down here, Peloton removes the friction to getting fit. It’s the leader in a movement I call “pushbutton health”. And this is why I think Peloton will be a big succes no matter what short-term investors do when it IPOs this week after raising $994 million in venture capital.

The bike

Basically, Peloton is a $2300 stationary bike with an iPad stuck to the front. The $40 per month subscription unlocks thousands of live and on-demand video cycling classes where instructors positively yell at you. When you think you’re tired already, they look into your eyes, tell you “you got this”, the soundtrack crescendos, you crank up the resistance, and you pedal harder at home. The resulting endorphin rush is addictive, and you find yourself persuading friends they need a Peloton too.

That viral loop which adds to its 500,000 subscribers is how Peloton plans to raise ~$1.16 billion going public this week at an ~$8 billion valuation. Its revenue doubled this year as it began to dominate the connected exercise equipment market, though losses quadrupled as it burned cash to become a household name. But after riding 110 of 150 days I’ve been home since buying its bike, I’m confident in the company. Whatever it invests now to build its lead will likely be paid back handsomely by its increasingly handsome customers who can’t bear to clip out. Here’s why.

Peloton classes are recorded in front of a live studio audience of riders

The Shoes – Usually the activation energy to start a workout requires dragging yourself to the gym or suiting up to face the elements outside. That can be daunting enough that you rarely do. But once you slip into the Peloton bike shoes, you can hardly walk normally which means you can hardly procrastinate. You’re home so you don’t even need clothes. Just a few velcro straps and you’re over the hump and resigned to exercise.

The Clips – Home gym equipments reduces the barrier to entry but also the barrier to exit. You can tell yourself you’ll keep doing push-up sets or squats jumping rope, but you can stop any time. Yet after you’re clipped into the Peloton bike, you’re almost assured to keep pedaling until the instructor gives you that end-of-ride congratulations.

Just put the shoes on and you’ll exercise

The Schedule – You can get a sweat in just 10 or 20 minutes going hard on a Peloton. Combined with zero commute, that means you’ll practically always be able fit in a ride regardless of how busy you are. No more “I don’t have time to make it to the gym so I’ll just skip out”. When my calendar gets crunched or I dawdle a little before deciding to ride, classes as short as 5 minutes ensure there’s no weaseling out.

The Instructors – I wish I had these coaches to motivate me through sorting email. Peloton’s 20+ instructors range from hippie-dippie gurus to no-nonsense trainers that fit your personality type. You find yourself craving your favorite’s special brand of relentless positivity. I burn far more calories in a shorter time than exercising solo because they inspire me to push a little harder or they slow their countdown to add a couple all-out seconds to the end of a sprint. They’re even becoming celebrities, with bankers lining up for selfies during Peloton’s IPO road show. Sick of them? You can always Scenic Ride through video of some of the world’s prettiest bike paths.

Peloton instructors (from left): Alex Toussaint, Emma Lovewell, Ben Alldis, and Leane Hainsby

The Intimacy – You’re eye-to-eye with those instructors as they stare into the camera and out of the giant screen bolted to your handlebars. That generates intimacy despite them broadcasting to thousands. Even in person, a SoulCycle coach across the room can feel further away. You’re mostly guided by audio cues, but their gaze compels you to perform. Peloton almost feels like FaceTime, and that’s a sense of connection many long for more of these days.

The Pavlovian Response – Your brain quickly begins to associate the sounds of Peloton with the glowing feeling of finishing a workout. The rip of the velcro shoe straps, the click of clipping into the bike, but most of all the instructor catch-phrases. You get hooked on hear the bubbling British accent of “I’mmmm Leeaannne Haaaaainsby” as she introduces herself, Ben Alldis’ infectious “You got 5, you got 4…” countdowns, or Emma Lovewell reminding you to “Live, learn, love well”. That final ‘namaste’ followed by wiping down the bike and jumping in a cold shower forms a ritual you’re inclined to repeat.

Eye-contact with the instructors creates an intimate bond

The Soundtrack – Popular songs are more than just a pump-up accompaniment to Peloton classes. Your pedaling pace is often pegged to the tempo, with sprints starting when the beat drops. As your legs tire, you feel obliged to maintain your speed so you don’t fall behind the drums. You can even search classes by music genre and preview each’s playlist. Peloton has paid out $50 million in royalties for its music, and faces $300 million-plus in lawsuits for copyright infringement. But having the best tunes to bike to might end up worth the penalty since it helped Peloton race ahead in a lucrative market.

The Bike As Decor – Most home exercise equipment ends up in a closet or as a clothing rack. By designing its bicycles for beauty, Peloton coerces you to place them conspicuously in your home. You might have seen the hysterical Twitter thread parodying this practice, but it’s funny because it’s true. You’re a lot more likely to ride it if it’s central to your home (ours is between our bed and the doors to the veranda), and you’ll be embarassed if visitors ask about it and you haven’t hopped on recently.

“A good place for your Peloton bike is between your kitchen and your living room facing the cactus garden so you always remember virtual spin class” –ClueHeywood on Twitter

The Network Effect – Many of these smart product design moves could be copied by competitors. But by amassing a community of 1.4 million members to date, Peloton benefits from social features and economies of scale. You can ride together with pals over video chat, send each other digital high fives, or race and compare achievements. Each friend that joins Peloton is one more reason not to sign up for a competitor. The whole concept virtual personal training is being legitimized. And the cost of producing more classes gets spread wider as membership grows.

The Shared Accounts – Peloton has even built in a way to feel noble about your sanctimonious prosyletizing about how it “jumpstarted your metabolism”. Each $39 on-bike subscription allows unlimited accounts on up to three devices, so you can hook up some friends if you convince them to buy the big-budget gadget.

High-five fellow riders as you virtuall pass them

The Growth Hacks – Peloton streaks are for adults what Snapchat streaks are to kids: a clever way to reward consistent usage. But beyond the achievement badges displayed on your profile, you’ll get in-ride leaderboards full of people to proudly pass, progress bars to fill by pedaling, and kilojoule output high scores to beat. Peloton makes exercise a game you want to win.

The Shoutouts – Yet Peloton’s most explicit levering of our psychology comes from the in-class name-drop shoutouts instructors give. Whether mentioning the screen names of a few participants at the start of a session or congratulating users hitting their 50th, 200th, or 500th ride, the recognition pushes people to join the dozen live-streamed classes each day that add urgency to the on-demand catalog. Proof it works? People strategize to ensure their 100th ride is a long live class to maximize the chance of a shout-out.

A free cult shirt after your 100th ride

The ‘Transcendence’ – Peloton minimizes the isolation from working out at home. In fact, its whole product enables people to feel ‘glamorous’ and ‘manifested’ yet nonchalant in ways going to a sweaty gym or using a personal trainer can’t. It’s like being able to buy a little piece of the smug satisfaction and in-group affiliation of going to Burning Man. That’s why the company even sends you a free “Century Club” t-shirt when you hit your 100th ride. You’re meant to feel cool sharing that you “Peloton”, using the startup’s name as a verb.

—

Conspicuous Self-Actualization

Still, Peloton has plenty left to optimize. There’s room to expand use of its camera to offer premium one-on-one coaching, head-to-head racing, group video chat with friends, and augmented reality filters to make people feel comfortable on screen and take shareable selfies. A wider range of intense but short classes could appeal to overworked professionals who picked Peloton precisely because they don’t have an hour for the gym.

Novelty could come from celebrity guest instructors, or themed classes for pre-gaming for a night out, fans of a particular artist, or songs about a certain topic. And it should definitely have some iconic sounds like an om or singing bowl chime that play before each class to center you and after to release you.

Most excitingly, the Peloton screen has the potential to be a platform for exercise-controlled gaming and apps. Whether pedaling to escape zombies chasing you or piece together a puzzle, maintaining an output level to keep your cross-hairs locked on an enemy plane as you dogfight, or making a garden bloom by growing each flower during a different interval, Peloton could evolve riding to be much more interactive. Apps could offer training simulators for different sports focused on sprints for basketball or marathons for soccer. Or just put Netflix on it! By opening up to outside developers, Peloton could build a moat of extra experiences competitors can’t match.

With the strengths and opportunities of its core product, Peloton is poised to absorb more of your fitness time and money. It’s already branching out with yoga, meditation, lifting, bootcamp, and jazzercise classes you can do standing next to your bike or without one on its $19 per month app. Its second gadget is a $4300 treadmill.

From there it could break into more of the “pushbutton health” business. I categorize these as wellness products and services that rely on convenience instead of your will power. Think delivery health food instead calorie-counting apps that are a chore. My pushbutton regimen includes Peloton, six salads per week dropped off in batches by Thistle, monthly packages of Nomiku vacuum-sealed meals that RFID scan into its sous vide machine, and a Future remote personal trainer who nags me by text message.

It’s easy to get hooked on the positivity

Peloton could easily dive into selling meal kits, personal training, or a wider range of workout clothes to compete with Lulu Lemon. If it’s the center of your fitness routine, the company could become a gateway to new health products it owns or partners with.

I’m bullish on Peloton because I’m betting people are going to stay busy, lazy, and competitive. It offers the effectiveness of a spin class but with scheduling flexibility. It removes every excuse for staying on the couch. And in an age of visual communication where many seek to share both the journey to and the destination of an Instagrammable body and the discipline to ge there, Peloton provides conspicuous self-actualization through consumerism. Plus, finishing a ride feels damn good.

Powered by WPeMatico

At TechCrunch Disrupt, the original tech startup conference, venture capitalists remain amongst the premier guests.

VCs are responsible for helping startups — the focus of the three-day event — get off the ground, and, as such, they are often the most familiar with trends in the startup ecosystem, ready to deliver insights, anecdotes and advice to our audience of entrepreneurs, investors, operators, managers and more.

In the first half of 2019, VCs spent $66 billion purchasing equity in promising upstarts, according to the latest data from PitchBook. At that pace, VC spending could surpass $100 billion for the second year in a row. We plan to welcome a slew of investors to TechCrunch Disrupt to discuss this major feat and the investing trends that have paved the way for recording funding.

Mega-funds and the promise of unicorn initial public offerings continue to drive investment. SoftBank, of course, began raising its second Vision Fund this year, a vehicle expected to exceed $100 billion. Meanwhile, more traditional VC outfits revisited limited partners to stay competitive with the Japanese telecom giant. Andreessen Horowitz, for example, collected $2.75 billion for two new funds earlier this year. We’ll have a16z general partners Chris Dixon, Angela Strange and Andrew Chen at Disrupt for insight into the firm’s latest activity.

At the early-stage, the fight for seed deals continued, with larger funds moving downstream to muscle their way into seed and Series A financings. Pre-seed has risen to prominence, with new funds from Afore Capital and Bee Partners helping to legitimize the stage. Bolstering the early-stage further, Y Combinator admitted more than 400 companies across its two most recent batches,

We’ll welcome pre-seed and seed investor Charles Hudson of Precursor Ventures and Redpoint Ventures general partner Annie Kadavy to give founders tips on how to raise VC. Plus, Y Combinator CEO Michael Seibel and Ali Rowghani, the CEO of YC’s Continuity Fund, which invests in and advises growth-stage startups, will join us on the Disrupt Extra Crunch stage ready with tips on how to get accepted to the respected accelerator.

Moreover, activity in high-growth sectors, particularly enterprise SaaS, has permitted a series of outsized rounds across all stages of financing. Speaking on this trend, we’ll have AppDynamics founder and Unusual Ventures co-founder Jyoti Bansal and Battery Ventures general partner Neeraj Agrawal in conversation with TechCrunch’s enterprise reporter Ron Miller.

We would be remiss not to analyze activity on Wall Street in 2019, too. As top venture funds refueled with new capital, Silicon Valley’s favorite unicorns completed highly anticipated IPOs, a critical step toward bringing a much needed bout of liquidity to their investors. Uber, Lyft, Pinterest, Zoom, PagerDuty, Slack and several others went public this year, and other well-financed companies, including Peloton, Postmates and WeWork, have completed paperwork for upcoming public listings. To detail this year’s venture activity and IPO extravaganza, David Krane, CEO and managing partner of Uber and Slack investor GV, will be on deck, as will Sequoia general partner Jess Lee, Floodgate’s Ann Miura-Ko and Aspect Ventures’ Theresia Gouw.

There’s more where that came from. In addition to the VCs already named, Disrupt attendees can expect to hear from Bessemer Venture Partners’ Tess Hatch, who will provide her expertise on the growing “space economy.” Forerunner Ventures’ Eurie Kim will give the Extra Crunch Stage audience tips on building a subscription product, Mithril Capital’s Ajay Royan will explore opportunities in the medical robotics field and SOSV’s Arvind Gupta will dive deep into the cutting-edge world of health tech and more.

Disrupt SF runs October 2-4 at the Moscone Center in the heart of San Francisco. Passes are available here.

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week, I wrote about Stripe’s grand plans. Before that, I noted Peloton’s secret weapons.

Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets. If you don’t subscribe to Startups Weekly yet, you can do that here.

The best companies are built by people who have personally experienced the problem they’re attempting to solve. Lauren Jonas, the founder and chief executive officer of Part & Parcel, is intimately familiar with the struggles faced by the women she’s building for.

San Francisco-based Part & Parcel is a plus-sized clothing and shoe startup providing dimensional sizing to women across the U.S. The company operates a bit differently than your standard direct-to-consumer business by seeking to include the women who wear and evangelize the Part & Parcel designs by giving them a cut of their sales.

Here’s how it works: Ambassadors sign up to receive signature styles from Part & Parcel, which they then share and sell to women in their network. Ultimately, the sellers are eligible to receive up to 30% of the profit per sale. The out-of-the-box model, which might remind you somewhat of Mary Kay or Tupperware’s business strategy, is meant to encourage a sense of community and usher in a new era in which plus-sized women can facilitate other plus-sized women’s access to great clothes.

“I bought a brown men’s polyester suit and wore it to an interview,” Jonas, an early employee at Poshmark and the long-time author of the popular blog, ‘The Pear Shape,’ tells TechCrunch. “I was that kid wearing a men’s suit.”

Clothing tailored to plus-sized women has long been missing from the retail market. Increasingly, however, new brands are building thriving businesses by catering precisely to the historically forgotten demographic. Dia&Co., for example, raised another $70 million in venture capital funding last fall from Sequoia and USV. And Walmart recently acquired another brand in the space, ELOQUII, for an undisclosed amount. Part & Parcel, for its part, has raised $4 million in seed funding in a round led by Lightspeed Venture Partners’ Jeremy Liew.

The startup launched earlier this year in Anchorage, “a clothing desert,” and has since grown its network to include women in several other underserved markets. Given her own history struggling to find a fitted woman’s suit, Jonas launched her line with structured pieces, including suits and blouses — though the startup’s biggest success yet, she says, has been its boots, which come in three different calf width options.

“Seventy percent of women in this country are plus-sized,” Jonas said. “I’m bringing plus out of the dark corner of the department store.”

Image: Bryce Durbin / TechCrunch

TechCrunch’s Megan Rose Dickey published a highly anticipated deep dive on the state of sex tech this week. The piece provides new data on funding in sex tech and wellness companies, analysis on sex tech startup’s battle for public advertising and responses from industry leaders on how we can destigmatize sex with technology. Here’s a short passage from the story:

Cindy Gallop sees a market opportunity in every type of business obstacle she encounters. That’s why All The Sky will also seek to invest in startups that tackle the infrastructural tools needed to fuel sextech, like payments, hosting providers and e-commerce sites.

“I want to fund the sextech ecosystem to maintain and sustain a portfolio for All the Skies, to create a bloody huge sextech ecosystem and three, to monopolistically build out the ecosystem to be a multi-trillion-dollar market,” Gallop says.

I swung by Contrary Capital‘s Demo Day this week, in which a number of startups gave a 4- to 5-minute pitch. Next on my list is Alchemist‘s Demo Day in Menlo Park. The accelerator welcomes enterprise startups for a six-month program focused on early customer adoption, company development and mentorship.

Also on my radar is Females To The Front. The event began this week in Palm Springs and if I were based in SoCal, I would have swung by. Led by Amy Margolis, the event is said to be the largest gathering of female cannabis founders and funders to date. Here’s how the group describes the event: “Females to the Front Retreat will mix immersive and hands-on workshops, pitch training, investment deck preparation and business skill set education with investor meetings and plenty of shared meals, pool time, yoga, connections, rest and rejuvenation. Every workshop is built to directly engage attendees instead of powerpoint and panels. Be prepared to return home inspired, engaged and with so many more tools in your toolbox.”

For the record, I don’t advertise events in my newsletter just wanted to give props to this one because it’s a great development for the cannabis tech ecosystem.

We are just weeks away from our flagship conference, TechCrunch Disrupt San Francisco. We have dozens of amazing speakers lined up. In addition to taking in the great line-up of speakers, ticket holders can roam around Startup Alley to catch the more than 1,000 companies showcasing their products and technologies. And, of course, you’ll get the opportunity to watch the Startup Battlefield competition live. Past competitors include Dropbox, Cloudflare and Mint… You never know which future unicorn will compete next.

You can take a look at the full agenda here. And if you still need convincing, here’s five reasons to attend this year’s conference from our COO himself.

This week, the lovely Alex Wilhelm, editor-in-chief of Crunchbase News, and I gathered to discuss a number of topics including WeWork’s IPO and Uber’s attempts to bypass a new law meant to protect gig workers. Listen here.

Powered by WPeMatico