payment processing

Auto Added by WPeMatico

Auto Added by WPeMatico

Sunday was a big day in fintech: Afterpay has agreed to merge with Square. This agreement sets two of the most admired financial technology companies in recent history on a path to becoming one.

Afterpay and Square have the potential to build one of the world’s most important payments networks. Square has built a very significant merchant payment network, and, via Cash App, a thriving high-growth consumer payment service. However, these two lines of business have historically not been integrated. Together, Square and Afterpay will be able to weave all of these services together into a single integrated experience.

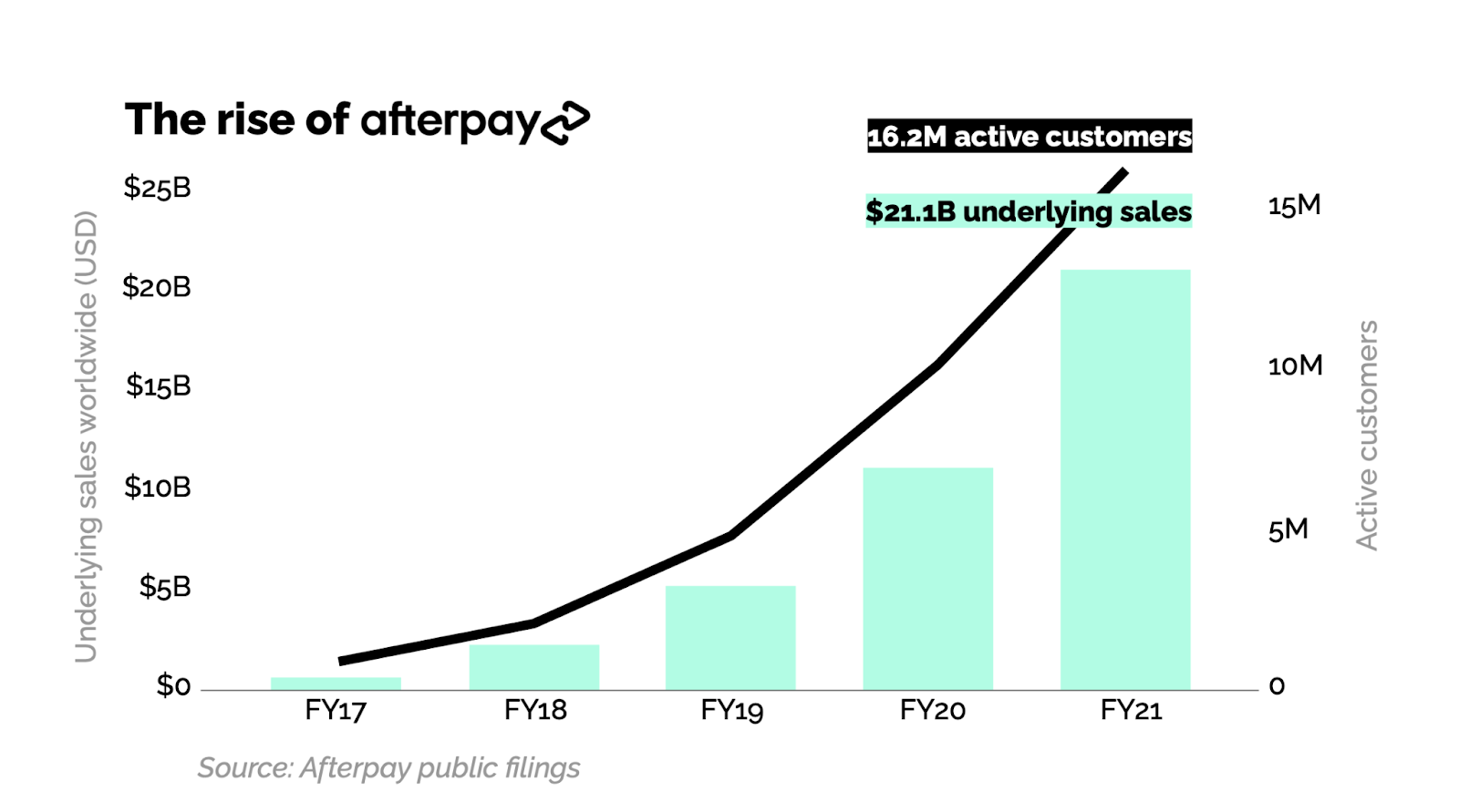

Afterpay and Cash App each have double-digit millions of consumers, and Square’s seller ecosystem and Afterpay’s merchant network both record double-digit billions of payment volume per year. From the offline register and the online checkout flow to sending money in just a few taps, Square and Afterpay will tell a complete story of next-generation economic empowerment.

As Afterpay’s only institutional venture investor, I wanted to share some perspective on how we got here and what this merger means for the future of consumer finance and the payments industry.

Afterpay and Square have the potential to build one of the world’s most important payments networks.

Every five to 10 years, the global payments industry undergoes a critical innovation cycle that determines the winners and losers for the next several decades. The last major transition was the shift to NFC-based mobile payments, which I wrote about in 2015. The major mobile OS vendors (Apple and Google) cemented their position in the global payments stack by deftly bridging the needs of the networks (Visa, Mastercard, etc.) and consumers by way of the mobile devices in their pockets.

Afterpay sparked the latest critical innovation cycle. Conceived in a living room in Sydney by a millennial, Nick Molnar, for millennials, Afterpay had a key insight: Millennials don’t like credit.

Millennials came of age during the global mortgage crisis of 2008. As young adults, they watched their friends and family lose their homes by overextending on mortgage debt, bolstering their already lower trust for banks. They also have record levels of student debt. Therefore, it’s no surprise that millennials (and Gen Z right behind them) strongly prefer debit cards over credit cards.

But it’s one thing to recognize the paradigm shift and quite another to do something about it. Nick Molnar and Anthony Eisen did something, ultimately building one of the fastest-growing payments startups in history on their core product: Buy now, pay later … and never any interest.

Afterpay’s product is simple. If you have $100 in your cart and choose to pay with Afterpay, it will charge your bank card (typically a debit card) $25 every two weeks in four installments. No interest, no revolving debt and no fees with on-time payments. For the millennial consumer, this meant they could get the primary benefit of a credit card (the ability to pay later) with their debit card, without the need to worry about all the bad things that come with credit cards — high interest rates and revolving debt.

All upside, no downside. Who could resist? For the early merchants, virtually all of whom relied on millennials as their key growth segment, they got a fair trade: Pay a small fee above payment processing to Afterpay, get significantly higher average order values and conversions to purchase. It was a win-win proposition and, with lots of execution, a new payment network was born.

Image Credits: Matrix Partners

Afterpay went somewhat unnoticed outside Australia in 2016 and 2017, but once it came to the U.S. in 2018 and built a business there that broke $100 million net revenues in only its second year, it got attention.

Klarna, which had struggled with product-market fit in the U.S., pivoted their business to emulate Afterpay. And Affirm, which had always been about traditional credit — generating a significant portion of their revenue from consumer interest — also noticed and introduced their own BNPL offering. Then came PayPal with “Pay in 4,” and just a few weeks ago, there has been news that Apple is expected to enter the space.

Afterpay created a global phenomenon that has now become a category embraced by mainstream players across the industry — a category that is on track to take a meaningful share of global retail payments over the next 10 years.

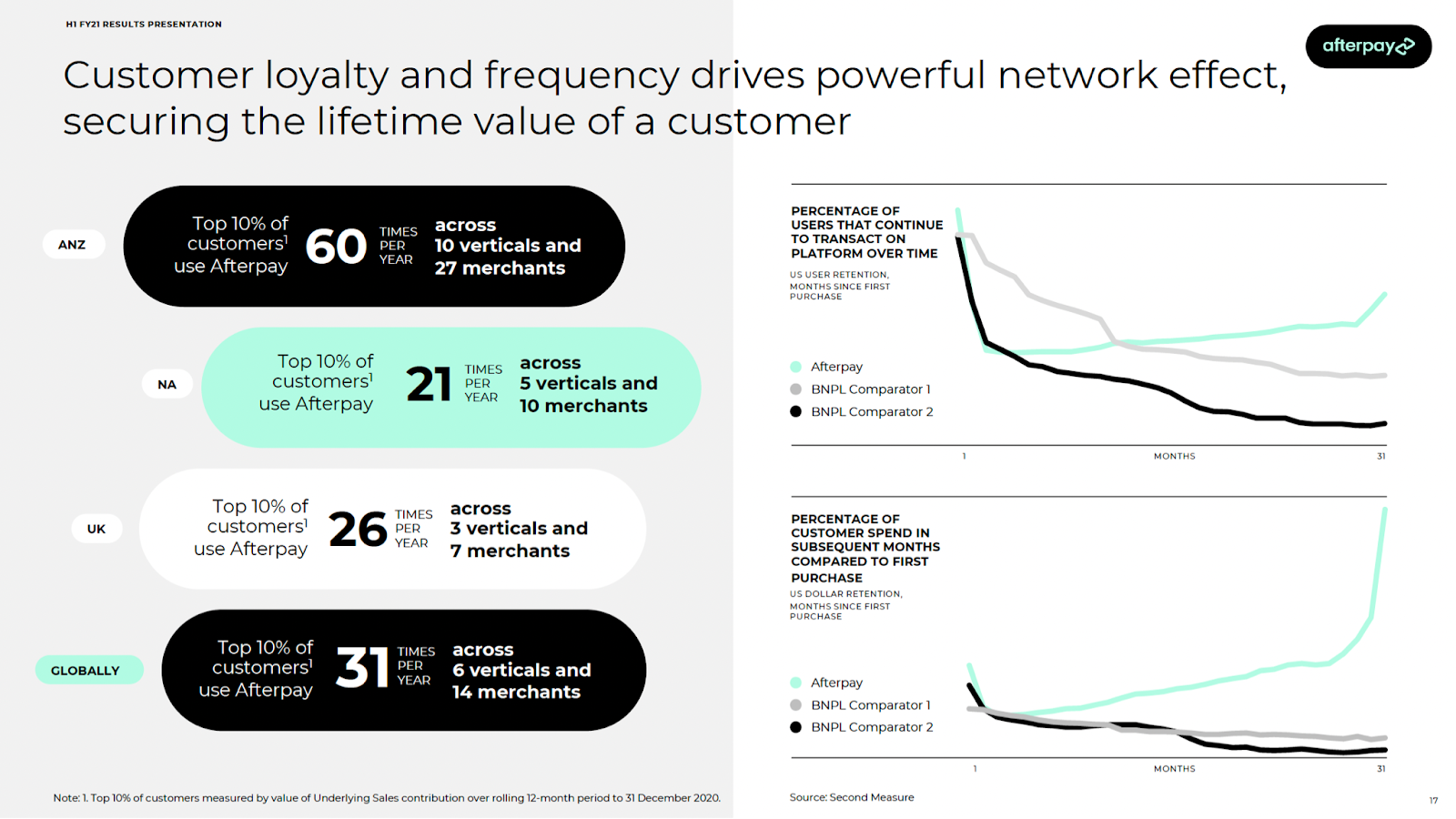

Afterpay stands apart. It has always been the BNPL leader by virtually every measure, and it has done it by staying true to their customers’ needs. The company is great at understanding the millennial and Gen Z consumer. It’s evident in the voice, tone and lifestyle brand you experience as an Afterpay user, and in the merchant network it continues to build strategically. It’s also evident in the simple fact that it doesn’t try to cross-sell users revolving debt products.

Most importantly, it’s evident in the usage metrics relative to competition. This is a product that people love, use and have come to rely on, all with better, fairer terms than were ever available to them than with traditional consumer credit.

Image Credits: Afterpay H1 FY21 results presentation

I’ve been building payment companies for over 15 years now, initially in the early days of PayPal and more recently as a venture investor at Matrix Partners. I’ve never seen a combination that has such potential to deliver extraordinary value to consumers and merchants. Even more so than eBay + PayPal.

Beyond the clear product and network complementarity, what’s most exciting to me and my partners is the alignment of values and culture. Square and Afterpay share a vision of a future with more opportunity and fewer economic hurdles for all. As they build toward that future together, I’m confident that this combination is a winner. Square and Afterpay together will become the world’s next generation payment provider.

Powered by WPeMatico

Paystone, a payments and integrated software company, secured another strategic investment this year, this time $23.8 million ($30 million CAD) from Crédit Mutuel Equity, the private equity arm of Crédit Mutuel Alliance Fédérale.

The Canada-based company got its start in 2008 as the payment processing company Zomaron, and rebranded itself as Paystone in 2019. Today it provides electronic payments and customer engagement technology to businesses, particularly those that provide services, CEO Tarique Al-Ansari told TechCrunch.

“Paystone is on a mission to help businesses grow, and we were enthralled by their commitment to that mission and their focus on service-oriented verticals,” said Léa Perge, investor at Crédit Mutuel Equity in Canada, via email.

While most of the company’s peers focus on product companies, Al-Ansari saw how underserved the service side was: their needs are different, and unlike retail, aren’t looking to sell online. Rather, they need an online presence and digital marketing to engage with customers, but their focus is being findable and having content that tells people why they should do business with them.

Paystone provides the marketing through content, help with reviews and with loyalty and rewards programs. However, rather than reward for spending, Paystone rewards for behavior. Refer a friend, get a reward. Write a review, get a reward. Al-Ansari calls it “payments as a benefit.” Referrals and reviews are how businesses become more findable, and the more content that’s out there, the more it helps people consider the business trustworthy, he added.

The new funding gives Canada-based Paystone total funds raised in 2021 of $78.8 million in a mix of debt and equity. It raised $54.9 million in January, funds that were barely touched as of yet, Al-Ansari said.

Though he wasn’t actively seeking new funds, Al-Ansari had been speaking with Crédit Mutuel Equity, which used to be CIC Capital Canada, prior to the pandemic, and their deal was put on hold.

Crédit Mutuel Equity came back with similar interest, and taking into account the kind of talent Paystone wanted to go after and its acquisition strategy — the company has already acquired five companies — Al-Ansari decided to take the additional funds. He said it gives the company options to hire more and double down on building the company, as well as enough capital to look for more acquisitions.

This year, Paystone entered the U.S. market for the first time and will do a proper launch later this year. The company has over 30,000 merchant locations on its platform throughout North America, and Al-Ansari expects that to grow by 5,000 this year. The company has 150 employees currently, and another 50 are expected to come on board by the end of the year.

In addition, Al-Ansari expects growth to accelerate for the rest of the year. The company processes around $6 billion in credit card payments and is on track to bring in $55.7 million in revenue this year. It is cash flow positive, residuals from the company’s origins of being bootstrapped, he said.

“We want to become the go-to destination for service businesses to set up a digital presence to accept payments and provide loyalty and rewards,” Al-Ansari said. “We will do this by solidifying our market position and growing our platform with the tools that customers want.”

Powered by WPeMatico

The COVID-19 pandemic has forced businesses to rethink how they accept and make payments. Paper invoices, checks and point-of-sale payments have given way to “corona-free payments” through mobile apps, electronic invoicing and ACH. Although significant, this is the sideshow to a more significant reshuffling of the payments industry.

Nearly $150 trillion in worldwide B2B and B2C transactions take place every year, but only a tiny portion are digital. A lot of technology companies want their piece of that massive pie. Until recently, though, only payment facilitators (aka, “payfacs”), gateways, banks and credit card companies had access to it.

That’s changing. Whether they know it yet or not, B2B tech platforms are becoming payments companies. Payfacs are competing to integrate their technology into these platforms, which drive an ever-growing number of transactions. Revenue-sharing deals are on the table, and payfacs are pushing the competitive advantages they can offer to the clients of these B2B platforms. Capabilities like cross-border payments, seamless customer onboarding, fraud protection, marketplace payments and B2B invoicing influence, which payfacs win in “integrated payments” (the jargon for this space) and which don’t.

B2B companies that use to leave the choice of gateway to their clients need to become savvy in payment technology, both to control the user experience and to tap this new business. There’s a massive amount of revenue on the table, and it’s just too easy to blow this opportunity and alienate clients in the process.

A decade ago, the revolution in cloud computing led to a wave of B2B tech platforms promising to “disrupt” every industry. Gyms got gym management platforms. Hospitals got clinic management platforms. Retailers got commerce management platforms. Media companies got subscription management platforms. Many of these fill-in-the-blank management platforms — all independent software vendors (ISVs) — helped clients manage their operations and interactions with consumers or other businesses.

But ISVs didn’t get involved in payments, which was odd, given how complementary payments were to their platforms and how much money was at stake. Mastercard says there is about $120 trillion annually in B2B payments worldwide, and paper checks still dominate about half of the U.S.’s $25 trillion payment volume. Meanwhile, retail e-commerce sales account for $4.2 trillion out of $26 trillion in total retail, or about 16.1%, according to eMarketer. Less than 8% of global commerce is thought to occur online.

You’d think B2B software companies would find a way to generate revenue on some of that $146 trillion in transactions, but most did not. Payment processing is its own, messy, complicated niche. Payfacs go through a grueling underwriting process to provision a merchant account, which includes know-your-customer (KYC) and anti-money laundering (AML) checks. If a merchant defaults, the payfac is next in line to make good on the transactions.

When you run a venture-backed B2B platform, you have enough to worry about already.

So, B2B platforms stayed clear. They formed integrations with a basket of payfacs (Stripe, PayPal, Square, my company BlueSnap, etc.) and then let their clients choose which one to use. That’s a lot of integrations to maintain.

Powered by WPeMatico

Since moving to the United States, I’ve come to appreciate and admire the United States Postal Service as a symbol of American ingenuity and resilience.

Like electricity, telephones and the freeway system, it’s part of our greater story and what binds the United States together. But it’s also something that’s easy to take for granted. USPS delivers 181.9 million pieces of First Class mail each day without charging an arm and a leg to do so. If you have an address, you are being served by the USPS — and no one’s asking you for cash up front.

As CEO of Shippo, an e-commerce technology platform that helps businesses optimize their shipping, I have a unique vantage point into the USPS and its impact on e-commerce. The USPS has been a key partner since the early days of Shippo in making shipping more accessible for growing businesses. As a result of our work with the USPS, along with several other emerging technologies (like site builders, e-commerce platforms and payment processing), e-commerce is more accessible than ever for small businesses.

And while my opinion on the importance of the USPS is not based on my company’s business relationship with the Postal Service, I want to be upfront about the fact that Shippo generates part of its revenue from the purchase of shipping labels through our platform from the USPS along with several other carriers. If the USPS were to stop operations, it would have an impact on Shippo’s revenue. That said, the negative impact would be far greater for many thousands of small businesses.

I know this because at Shippo, we see firsthand how over 35,000 online businesses operate and how they reach their customers. We see and support everything from what options merchants show their customers at checkout through how they handle returns — and everything in between. And while each and every business is unique with different products, customers operations and strategies, they all need to ship.

In the United States, the majority of this shipping is facilitated by the USPS, especially for small and medium businesses. For context, the USPS handles almost half of the world’s total mail and delivers more than the top private carriers do in aggregate, annually, in just 16 days. And, it does all of this without tax dollars, while offering healthcare and pension benefits to its employees.

As has been the case for many organizations, COVID-19 has significantly impacted the USPS. While e-commerce package shipments continue to rise (+30% since early March based on Shippo data), it has not been enough to overcome the drastic drop in letter mail. With this, I’ve heard opinions of supposed “inefficiency,” calls for privatization, pushes for significant pricing and structural changes, and even indifference to the possibility of the USPS shutting down.

Amid this crisis, we all need the USPS and its vital services now more than ever. In a world with a diminished or dismantled USPS, it won’t be Amazon, other major enterprises, or even Shippo that suffer. If we let the USPS die, we’ll be killing small businesses along with it.

Quite often, opinions on the efficiency (or lack thereof) of the USPS are very narrow in scope. Yes, the USPS could pivot to improve its balance sheet and turn operating losses into profits by axing cumbersome routes, increasing prices and being more selective in who they serve.

However, this omits the bigger picture and the true value of the USPS. What some have dubbed inefficient operations are actually key catalysts to small business growth in the United States. The USPS gives businesses across the country, regardless of size, location or financial resources, the ability to reach their customers.

We shouldn’t evaluate the USPS strictly on balance sheet efficiency, or even as a “public good” in the abstract. We should look at how many thousands of small businesses have been able to get started thanks to the USPS, how hundreds of billions of dollars of commerce is made possible by the USPS annually and how many millions of customers, who otherwise may not have access to goods, have been served by the USPS.

In the U.S., e-commerce accounts for over half a trillion dollars in sales annually, and is growing at double-digit rates each year. When I hear people talk about the growth of e-commerce, Amazon is often the first thing that comes up. What doesn’t shine through as often is the massive growth of small business — which is essential to the health of commerce in general (no one needs a monopoly!). In fact, the SMB segment has been growing steadily alongside Amazon. And with the challenges that traditional businesses face with COVID-19, more small businesses than ever are moving online.

USPS Priority Mail gets packages almost anywhere in the U.S. in two to three days (average transit time is 2.5 days based on Shippo data) and starts at around $7 per shipment, with full service: tracking, insurance, free pickups and even free packaging that they will bring to you.

In a time when we as consumers have become accustomed to free and fast shipping on all of our online purchases, the USPS is essential for small businesses to keep up. As consumers we rarely see behind the curtain, so to speak, when we interact with e-commerce businesses. We don’t see the small business owner fulfilling orders out of their home or out of a small storefront, we just see an e-commerce website. Without the USPS’ support, it would be even harder, in some cases near impossible, for small business owners to live up to these sky-high expectations. For context, 89% of U.S.-based SMBs (under $10,000 in monthly volume) on the Shippo platform rely on the USPS.

I’ve seen a lot of talk about the USPS’s partnership with Amazon, how it is to blame for the current situation, and how under a private model, things would improve. While we have our own strong opinions on Amazon and its impact on the e-commerce market, Amazon is not the driver of USPS’s challenges. In fact, Amazon is a major contributor in the continued growth of the USPS’s most profitable revenue stream: package delivery.

While I don’t know the exact economics of the deal between the USPS and Amazon, significant discounting for volume and efficiency is common in e-commerce shipping. Part of Amazon’s pricing is a result of it actually being cheaper and easier for the USPS to fulfill Amazon orders, compared to the average shipper. For this process, Amazon delivers shipments to USPS distribution centers in bulk, which significantly cuts costs and logistical challenges for the USPS.

Without the USPS, Amazon would be able to negotiate similar processes and efficiencies with private carriers — small businesses would not. Given the drastic differences in daily operations and infrastructure between the USPS and private carriers, small businesses would see shipping costs increase significantly, in some cases by more than double. On top of this, small businesses would see a new operational burden when it comes to getting their packages into the carriers’ systems in the absence of daily routes by the USPS.

Overall, I would expect to see the level of entrepreneurship in e-commerce slow in the United States without the USPS or with a private version of the USPS that operates with a profit-first mindset. The barriers to entry would be higher, with greater costs and larger infrastructure investments required up-front for new businesses. For Shippo, I’d expect to see a much greater diversity of carriers used by our customers. Our technology that allows businesses to optimize across several carriers would become even more critical for businesses. Though, even with optimization, small businesses would still be the group that suffers the most.

Today, most SMB e-commerce brands, based on Shippo data, spend between 10-15% of their revenue on shipping, which is already a large expense. This could rise well north of 20%, especially when you take into account surcharges and pick-up fees, creating an additional burden for businesses in an already challenging space.

I urge our lawmakers and leaders to see the full picture: that the USPS is a critical service that enables small businesses to survive and thrive in tough times, and gives citizens access to essential services, no matter where they reside.

This also means providing government support — both financially and in spirit — as we all navigate the COVID-19 crisis. This will allow the USPS to continue to serve both small businesses and citizens while protecting and keeping their employees safe — which includes ensuring that they are equipped to handle their front-line duties with proper safety and protective gear.

In the end, if we continue to view the USPS as simply a balance sheet and optimize for profitability in a vacuum, we ultimately stand to lose far more than we gain.

Powered by WPeMatico

The last few decades have produced many successful marketplaces. We went from goods marketplace pioneers such as eBay and Amazon to simple service marketplaces such as Uber, Lyft, Doordash, Upwork, Thumbtack, TaskRabbit, and Fiverr. But why haven’t we seen many successful B2B service marketplaces?

Some would argue that companies such as Upwork, Thumbtack, Fiverr, or TaskRabbit are horizontal B2B marketplaces in the sense that they provide access to suppliers of different services. But while businesses do indeed transact with freelancers on such “horizontal” marketplaces, for most service verticals these are limited-value, one-off transactions. They fail to enable long-term business collaborations.

So, such marketplaces haven’t delivered more valuable services nor introduced a new paradigm for how businesses buy specific services at scale and on an on-going basis. Why is that?

Horizontal services marketplaces don’t provide much value beyond matching clients with quality service providers. In other words, they don’t facilitate collaboration between buyers and suppliers, never mind provide ways for the two parties to collaborate more efficiently over time as they engage in follow-on projects.

In essence, the model these marketplaces were built around is not much different from the likes of Craigslist, which put a convenient UX on traditional classified advertisements.

In their article “What’s Next for Marketplace Startups?,” Andrew Chen and Li Jin found that there aren’t many successful service marketplaces because those offerings are complex, diverse, and difficult to evaluate. It’s challenging to define a successful transaction in a service marketplace because it’s harder to quantify success.

One reason is that several service providers must often work together to complete a single job for a buyer, requiring a complex workflow from end to end. As a result, it’s difficult for marketplaces to not only mediate service delivery but also make it significantly more efficient for buyers and suppliers. If both the buyer and suppliers don’t see a significant efficiency gain other than being initially matched, why would they continue using the marketplace?

(Image via Getty Images / Lidiia Moor)

The $50 billion translation industry is a prime example of complex B2B services marketplaces. On the supply side are roughly 50,000 small agencies around the globe responsible for more than 85% of this $50 billion industry. (Note we are referring to agencies here as suppliers, though they play on both sides.)

On the demand side are businesses that need to translate text from one language into another. Plus about 1,500,000 freelance linguists work in this industry, many of whom are more specialized than professionals in other industries.

Anyone can find and hire a translator on Fiverr or Upwork. Both provide a vast selection of language translators. However, the quality and cost of the translation depends on the translation tools available to the translator as well as their subject expertise.

Neither Fiverr nor Upwork provide computer-aided translation (CAT) and collaborative workflow solutions for users of their platforms. Additionally, neither provides an effective way for all parties to collaborate and continuously improve the efficiency and quality.

But the problem with traditional marketplaces goes even further: Multiple translators and reviewers are usually needed to complete a single job for a customer. Multi-language translation projects are even more complicated. Such projects require multiple service providers and cost estimates, in addition to project management tools.

This is why building a B2B service marketplace is difficult. Service marketplaces must not only connect buyers and suppliers, but also provide tools to enable an efficient and collaborative workflow that reduces wasted time and effort.

In addition to the problems already outlined, traditional marketplaces experience another issue that prevents them from growing and retaining market participants: Buyer and supplier attrition.

Many business services are based on regularly recurring engagements. In some cases, a buyer and a service provider interact daily, requiring a different workflow than gig-marketplaces are built around.

Buyers and suppliers have little motivation to continue interacting on a platform with no workflow automation solutions. They lack a way to improve service efficiency and quality, automate collaboration, payment, paperwork, and other basic processes required for a business.

This is why many traditional marketplaces suffer from slow network effects and high attrition. (A network effect is what happens when a platform, product, or service delivers more value the more it is used.

Think Facebook, eBay, WhatsApp.) Why wouldn’t companies work directly with service providers outside of a marketplace after they were introduced? What incentives keep the service transaction on the marketplace? These are critical questions to answer when building a marketplace.

Traditional marketplaces target broad services, making it nearly impossible to provide workflow solutions for buyers and suppliers. Going forward, successful service marketplaces will be developed relying on an industry-specific SaaS workflow. This will focus buyers and suppliers on longer-term projects and interactions that serve the unique needs of collaborations and transactions in a specific vertical.

Image via Getty Images / OstapenkoOlena

In “The next 10 Years Will Be About Market Networks,” James Currier, Managing Partner at NFX Ventures, defines a new era of service marketplaces, which he calls market networks.

A market network is a platform that combines elements of an n-sided marketplace, a network, and workflow solutions. An n-sided marketplace is one that requires coordination of multiple supply-side parties to provide a complex service for a single buyer.

Market networks enable multiple buyers and suppliers to interact, collaborate, and transact on the same platform. They provide users with industry-specific workflow solutions that enable efficient, ongoing collaboration on long-term projects. This reduces costs and leads to a higher quality of services and increased overall value for all users.

But how do you actually build a successful market-network platform? While the answer to that varies from company to company, here is our approach. We were able to build a market network for the translation industry that combines the components: network, marketplace, and workflow solution.

The first step to building an effective complex market network is to develop a workflow that is easy for users to embrace. It might not seem like much, but this increases productivity by enabling teams to perform tasks that were previously impossible.

Powered by WPeMatico