Patreon

Auto Added by WPeMatico

Auto Added by WPeMatico

Millions.co, a social commerce platform geared toward professional and semi-professional athletes wanting help to monetize their fanbase by selling merch and/or on-demand video, has grabbed $10 million in funding led by Boston-based Volition Capital.

The round is being loosely pegged as a Series A as the seasoned team behind Millions self-funded the first wave of development to get the platform launched.

The founding team includes CEO Matt Whitteker, a boxing gym owner who co-founded the supply chain data management unicorn Assent Compliance and NoNotes.com; CMO Brandon Austin, co-founder of Go-Fish Cam; and, in advisor roles, Adrian Salamunovic, co-founder of DNA 11 and CanvasPop; Scott Whitteker (Fight for the Cure) and Bruce Buffer (a veteran sports announcer).

Millions launched its fan engagement social commerce platform in April — with an initial three products for pro/semi-pro athletes to pitch at their followers: Namely custom merchandize (including a free design service); ask-me-anything personalized videos; and a pay-per-view streaming offering that lets fans pay to tune into a livestream of their favorite sportsperson.

The startup’s initial plan had been to build just an e-commerce and merchandising platform but, having built that component, Salamunovic says the team decided to bundle in video products — such as personalized videos and “democratising” pay-per-view (PPV).

“Our biggest advantage and differentiator is that we are strictly focused on the sports world and fan engagement,” he tells TechCrunch. “The obvious indirect competitors are Twitch (heavily focused on e-sports/gaming), Patreon (focused on creators), Represent.com (focused on merch drops for ‘influencers’), and even OnlyFans (we know who they focus on) but we’re laser-focused on the multibillion-dollar sports market.”

“Cameo has a very similar product to our video ‘Ask Me Anything’ platform — but we don’t focus on birthday shout-outs we focus on allowing fans to ask their favorite athletes questions around their training, their success, predictions (we’ve seen a lot of gamblers use our platform to get tips) and less on things like shout-outs,” he adds. “We love Cameo, but we’re really different and focused on sports.”

“Instagram, TikTok, Snapchat, Facebook are all great social media platforms that allow athletes to engage and interact with their fans but it’s not a great place to monetize your audience,” Salamunovic also argues. “We help athletes create a brand, build a merch line, sell video content (personalized videos and watch parties all on a single platform). We’re not trying to replace any of these platforms, we’re complementing them by allowing the athletes to provide a single link and landing page for deeper interaction and monetization. The fans seem to love it too.”

At this stage, Millions only has around 300 athlete profiles live but says it has “thousands” who’ve registered interest across a variety of sports categories.

Its first focus — including for partnerships with agencies and sports leagues — has been on “combat sports and gyms”. But the platform has a long list of sports types in the search filter — from lacrosse to water polo to baseball or gymnastics — so the ambition is to go after a very broad funnel of pro/semi sportspeople.

And for every Michael Jordan or Cristiano Ronaldo — aka, those top-tier athletes who can command hundreds of millions in sponsorship fees by inking partnerships with top brands to promote their products and who you certainly won’t find selling hats on Millions — there are scores of athletes who aren’t able to cut such sweet deals and who will have far more modest fanbases.

It’s that broad field of players and performers who Millions hopes will flock to its platform — and take up its dedicated offer of social commerce tools and tech to engage with and monetize their followers.

Commenting on the funding in a statement, Sean Cantwell, managing partner at Volition Capital, suggested: “Athletes are always looking for ways to connect on a deeper level with fans, generate additional revenue streams and build their personal brands and Millions offers all of this on a single platform. We think that Millions is the future of fan engagement.”

To help grease the funnel of sportspeople it needs to drive eyeballs to its platform, Millions is offering athletes a “signing bonus” when they join and start selling — with a variety of tiers of bonus (of up to $5K) per sportsperson.

“We initially wanted to stay hyper-focused on combat sports and not try to ‘boil the ocean’. Now we’re releasing new athletes’ profiles daily and introducing new sports like football, volleyball, golf and more,” notes Salamunovic. “Really, this platform is designed for any athlete who wants to reach their fans and create new monetization channels without having to put a ton of effort into things like page design, technology, design or logistics… we take care of all that so they can focus on engaging with their fans and most importantly on their sport and training.”

“We’re looking to build the most important sports tech company in history,” he adds. “We’re going to be the Etsy ($21 billion market cap) of sports. That’s an ambitious statement but it’s true; 98% of athletes NEED our product/platform.”

Chasing that scale is why Millions is raising now. And while the early focus has been on North America — where about 90% of the onboarded sportspeople hail from currently — it reckons there’s “huge growth potential” in Europe and Asia so is very much gunning to build a global business.

It says it’ll be splashing Series A cash on growing its product engineering team and recruiting to expand its team generally, as well as spending on marketing to get the word out to athletes and get more signed up to build their own brands and sell direct to fans.

“I believe a powerful thing we’re doing, past just the product offering, is enabling athletes to have a team,” adds Austin. “With Millions, athletes get a marketing team, a personal account manager, and a design team that they can use to build their brand and product line, and to promote to, and further build, their fan base. We allow the athlete to focus on training, playing/fighting, and winning while we help take care of everything else, and coach them on how to brand and market themselves.”

Millions’ business model is to take a 20% cut of all sales athletes make via the platform — with the split remaining the same for merchandise or video sales.

For the former, Millions is using a global network of print-on-demand suppliers to do the fulfilment.

While products the platform can customize for athletes to sell as their own brand merch include t-shirts, caps and hoodies.

Powered by WPeMatico

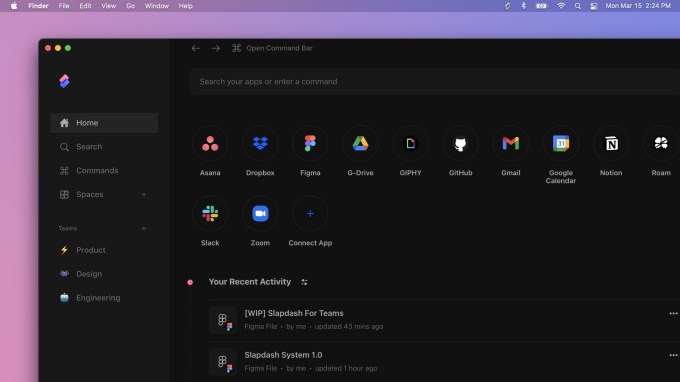

The explosion in productivity software amid a broader remote work boom has been one of the pandemic’s clearest tech impacts. But learning to use a dozen new programs while having to decipher which data is hosted where can sometimes seem to have an adverse effect on worker productivity. It’s all time that users can take for granted, even when carrying out common tasks like navigating to the calendar to view more info to click a link to open the browser to redirect to the native app to open a Zoom call.

Slapdash is aiming to carve a new niche out for itself among workplace software tools, pushing a desire for peak performance to the forefront with a product that shaves seconds off each instance where a user needs to find data hosted in a cloud app or carry out an action. While most of the integration-heavy software suites to emerge during the remote work boom have focused on promoting visibility or re-skinning workflows across the tangled weave of SaaS apps, Slapdash founder Ivan Kanevski hopes that the company’s efforts to engineer a quicker path to information will push tech workers to integrate another tool into their workflow.

The team tells TechCrunch that they’ve raised $3.7 million in seed funding from investors that include S28 Capital, Quiet Capital, Quarry Ventures, UP2398 and Twenty Two Ventures. Angels participating in the round include co-founders at companies like Patreon, Docker and Zynga.

Image Credits: Slapdash

Kanevski says the team sought to emulate the success of popular apps like Superhuman, which have pushed low-latency command line interface navigation while emulating some of the sleek internal tools used at companies like Facebook, where he spent nearly six years as a software engineer.

Slapdash’s command line widget can be pulled up anywhere, once installed, with a quick keyboard shortcut. From there, users can search through a laundry list of indexable apps including Slack, Zoom, Jira and about 20 others. Beyond command line access, users can create folders of files and actions inside the full desktop app or create their own keyboard shortcuts to quickly hammer out a task. The app is available on Mac, Windows, Linux and the web.

“We’re not trying to displace the applications that you connect to Slapdash,” he says. “You won’t see us, for example, building document editing, you won’t see us building project management, just because our sort of philosophy is that we’re a neutral platform.”

The company offers a free tier for users indexing up to five apps and creating 10 commands and spaces; any more than that and you level up into a $12 per month paid plan. Things look more customized for enterprise-wide pricing. As the team hopes to make the tool essential to startups, Kanevski sees the app’s hefty utility for individual users as a clear asset in scaling up.

“If you anticipate rolling this out to larger organizations, you would want the people that are using the software to have a blast with it,” he says. “We have quite a lot of confidence that even at this sort of individual atomic level, we built something pretty joyful and helpful.”

Powered by WPeMatico

Buzzy live voice chat app Clubhouse has confirmed that it has raised new funding – without revealing how much – in a Series B round led by Andreessen Horowitz through the firm’s partner Andrew Chen. The app was reported to be raising at a $1 billion valuation in a report from The Information that landed just before this confirmation. While we try to track down the actual value of this round and the subsequent valuation of the company, what we do know is that Clubhouse has confirmed it will be introducing products to help creators on the platform get played, including subscriptions, tipping and ticket sales.

This funding round will also support a ‘Creator Grant Program’ being set up by Clubhouse, which will be used to “support emerging Clubhouse creators” according to the startup’s blog post. While the app has done a remarkable job attracting creator talent, including high-profile celebrity and political users, directing revenue towards creators will definitely help spur sustained interest, as well as more time and investment from new creators who are potentially looking to make a name for themselves on the platform, similar to YouTube and TikTok influencers before them.

Of course, adding monetization for users also introduces a method for Clubhouse itself to monetize. The platform is free to all users, and doesn’t yet offer any kind of premium plan or method of charging users, nor is it ad-supported. Adding ways for users to pay other users provides an opportunity for Clubhouse to retain a cut for its services.

The plans around monetization routes for creators appear to be relatively open-ended at this point, with Clubhouse saying it’ll be launching “first tests” around each of the three areas it mentions (tipping, tickets and subscriptions) over the “next few months.” It sounds like these could be similar to something like a Patreon built right into the platform. Tickets are a unique option that would go well with Clubhouse’s more formal roundtable discussions, and could also be a way that more organizations make use of the platform for hosting virtual events.

The startup also announced that it will be starting work on its Android app (it’s been iOS only for now) and that it will also invest in more backend scaling to keep up with demand, as well as support team growth and tools for detecting and prevuing abuse. Clubhouse has come under fire for its failure in regards to moderation and prevention of abuse in the past, so this aspect of its product development will likely be closely watched. The platform will also see changes to discovery aimed at surfacing relevant users, groups (‘clubs’ in the app’s parlance) and rooms.

During a regular virtual town hall the app’s founders host on the platform, CEO Paul Davison revealed that Clubhouse now has 2 million weekly active users. It’s also worth noting that Clubhouse says it now has “over 180 investors” in the company, which is a lot for a Series B – though many of those are likely small, independent investors with very little stake.

Powered by WPeMatico

Sex, despite being one of the most fundamental human experiences, is still one of those businesses that some advertisers reject, banks are hesitant to financially support and some investors don’t want to fund.

Given how sex is such a huge part of our lives, it’s no surprise founders are looking to capitalize on the space. But the idea of pleasure versus function, plus the stigma still associated with all-things sex, is at the root of the barriers some startup founders face.

Just last month, Samsung was forced to apologize to sextech startup Lioness after it wrongfully asked the company to take down its booth at an event it was co-hosting. Lioness is a smart vibrator that aims to improve orgasms through biofeedback data.

Sextech companies that relate to the ability to reproduce or, the ability to not reproduce, don’t always face the same problems when it comes to everything from social acceptance to advertising to raising venture funding. It seems to come down to the distinction between pleasure and function, stigma and the patriarchy.

This is where the trajectories for sextech startups can diverge. Some startups have raised hundreds of millions from traditional investors in Silicon Valley while others have struggled to raise any funding at all. As one startup founder tells me, “Sand Hill Road was a big no.”

Powered by WPeMatico

Meme creators have never gotten their fair share. Remixed and reshared across the web, their jokes prop up social networks like Instagram and Twitter that pay back none of their ad revenue to artists and comedians. But 300 million monthly user meme and storytelling app Imgur wants to pioneer a way to pay creators per second that people view their content.

Today Imgur announces that it’s raised a $20 million venture equity round from Coil, a micropayment tool for creators that Imgur has agreed to build into its service. Imgur will eventually launch a premium membership with exclusive features and content reserved for Coil subscribers.

Users pay Coil a fixed monthly fee, install its browser extension, the Interledger protocol is used to route assets around, and then Coil pays creators dollars or XRP tokens per second that the subscriber spends consuming their content at a rate of 36 cents per hour. Imgur and Coil will earn a cut too, diversifying the meme network’s revenue beyond ads.

“Imgur began in 2009 as a gift to the internet. Over the last 10 years we’ve built one of the largest, most positive online communities, based on our core value to ‘give more than we take’” says Alan Schaaf, founder and CEO of Imgur. The startup bootstrapped for its first five years before raising a $40 million Series A from Andreessen Horowitz and Reddit. It’s grown into the premier place to browse ‘meme dumps’ of 50+ funny images and GIFs, as well as art, science, and inspirational tales. With the same unpersonalized homepage for everyone, it’s fostered a positive community unified by esoteric inside jokes.

While the new round brings in fewer dollars, Schaaf explains that Imgur raised at a valuation that’s “higher than last time. Our investors are happy with the valuation. This is a really exciting strategic partnership.” Coil founder and CEO Stefan Thomas who was formerly the CTO of cryptocurrency company Ripple Labs will join Imgur’s board. Coil received the money it’s investing in Imgur from Ripple Labs’ Xpring Initiative, which aims to fund proliferation of the Ripple XRP ecosystem, though Imgur received US dollars in the funding deal.

Thomas tells me that “There’s no built in business model” as part of the web. Publishers and platforms “either make money with ads or with subscriptions. The problem is that only works when you have huge scale” that can bring along societal problems as we’ve seen with Facebook. Coil will “hopefully offer a third potential business model for the internet and offer a way for creators to get paid.”

Founded last year, Coil’s $5 per month subscription is now in open beta, and it provides extensions for Chrome and Firefox as it tries to get baked into browsers natively. Unlike Patreon where you pick a few creators and choose how much to pay each every month, Coil lets you browse content from as many creators as you want and it pays them appropriately. Sites like Imgur can code in tags to their pages that tell Coil’s Web Monetization API who to send money to.

The challenge for Imgur will be avoiding the cannibalization of its existing content to the detriment of its non-paying users who’ve always known it to be free. “We’re in the business of making the internet better. We do not plan on taking anything away for the community” Schaaf insists. That means it will have to recruit new creators and add bonus features that are reserved for Coil subscribers without making the rest of its 300 million users feel deprived.

It’s surprising thT meme culture hasn’t spawned more dedicated apps. Decade-old Imgur precedes the explosion in popularity of bite-sized internet content. But rather than just host memes like Instagram, Imgur has built its own meme creation tools. If Imgur and Coil can prove users are willing to pay for quick hits of entertainment and creators can be fairly compensated, they could inspire more apps to help content makers turn their passion into a profession…or at least a nice side hustle.

Powered by WPeMatico

The popular TechCrunch podcast Equity this week launched a new series called Equity Dive, wherein a host interviews the writer of the latest edition of the Extra Crunch EC-1.

If you’ve ever wanted to know everything there is to know about Patreon, the platform that connects creators with fans and their wallets, then this is the show for you. TechCrunch Silicon Valley editor Connie Loizos speaks with Eric Peckham who spent hours upon hours meeting with the Patreon team to learn its origin story and the ins and outs of its business practices to get the company to where it is today.

As Eric says:

The way to think about how Patreon has evolved is I see it in kind of three stages, which was this initial crowd funding platform, and then evolving beyond that to try and be a destination platform for consumers where there would be great content that you just go to Patreon to find and you go to discover creators, kind of a marketplace model. They moved away from that. That was somewhat of a gradual shift and essentially the decision was it’s not good to be stuck in this game of trying to be yet another destination platform for consumers competing with YouTube and Instagram and every single media site out there. Really the opportunity and mission underlies our work is about helping creators and enabling all these independent creators to sustain themselves and to build thriving businesses.

They shifted, they now describe themselves as a SaaS company actually, which is very different from framing yourself as kind of a consumer destination. The long and short of it is they see this opportunity, which is a growing market of independent creators around the world who are building fan bases, and for that particular type of SMB they want to provide essentially the full suite of tools and services that they need to run their businesses.

For access to the full transcription, become a member of Extra Crunch. Learn more and try it for free.

Connie Loizos: Hi, I’m Connie Loizos and I’d like to welcome you to our first Equity Dive. Once a month we’re going to be dedicating an entire episode to a deep dive into the life of one company. This month I’m joined by Eric Peckham, who has reported extensively on the crowd funding membership platform Patreon. Hi Eric.

Eric Peckham: Hey Connie, excited to be here for the first Equity Dive.

Connie Loizos: Same, so Eric you and I ran into each other first in Berlin but we don’t know each other very well. I’d love to hear more about you. You’re based in LA, and from what I understand you are a media industry analyst. Is that correct?

Eric Peckham: Yes, so I cover through both my own newsletter Monetizing Media, the happenings of the global media and entertainment industry. It’s kind of a very business minded lens on media and entertainment.

Connie Loizos: Well I read your extensive coverage on Patreon and it was really impressive, and I wondered considering how much you wrote, is this sort of a long interest of yours this company or how did you decide to settle on this for your first deep dive for TechCrunch?

Eric Peckham: Yes, it was an exciting process digging into this. We made a short list of exciting companies, a lot of unicorn companies or late stage startups we thought were about to become unicorns, and Patreon jumped out for a number of reasons. One is as someone who runs his own newsletter I have had subscribers to that newsletter suggest creating a Patreon. I’ve looked into it before, so I had a little bit of a creator perspective of just wanting to better understand Patreon and other options in the market. I think from a bigger picture, more of a Silicon Valley perspective, Patreon’s a really fascinating company. They’ve raised over $100 million from top PC firms like Index, CRV, they’re the dominant player in this space they’re targeting, but it’s kind of them versus just the big social media platforms. There isn’t the startup that’s comparable in size to it and it’s really trying to own this whole territory of independent content creators, surveying them with different business tools or services.

Connie Loizos: It is really interesting to think the David and Goliath story involves a $100 million venture backed startup versus, as you say, I know these big players Facebook, YouTube. Let’s start at the beginning, so you decided on Patreon for reasons that I can certainly understand now. How did you set about pitching them on this idea? Because obviously you were going to need a lot of access to them, a lot of their time.

Powered by WPeMatico

The Los Angeles-based video gaming clipping service Medal has made its first acquisition as it rolls out new features to its user base.

The company has acquired the Discord -based donations and payments service Donate Bot to enable direct payments and other types of transactions directly on its site.

Now, the company is rolling out a service to any Medal user with more than 100 followers, allowing them to accept donations, subscriptions and payments directly from their clips on mobile, web, desktop and through embedded clips, according to a blog post from company founder Pim De Witte.

For now, and for at least the next year, the service will be free to Medal users — meaning the company won’t take a dime of any users’ revenue made through payments on the platform.

For users who already have a storefront up with Patreon, Shopify, Paypal.me, Streamlabs or ko-fi, Medal won’t wreck the channel — integrating with those and other payment processing systems.

Through the Donate Bot service any user with a discord server can generate a donation link, which can be customized to become more of a customer acquisition funnel for teams or gamers that sell their own merchandise.

A Webhooks API gives users a way to add donors to various list or subscription services or stream overlays, and the Donate Bot is directly linked with Discord Bot List and Discord Server List as well, so you can accept donations without having to set up a website.

In addition, the company updated its social features, so clips made on Medal can ultimately be shared on social media platforms like Twitter and Discord — and the company is also integrated with Discord, Twitter and Steam in a way to encourage easier signups.

Powered by WPeMatico

Greetings from Chittorgarh, one of my stops on a two-week excursion through Goa and Rajasthan, India. I’ve been a little too busy exploring, photographing cows and monkeys and eating a lot of delicious food to keep up with *all* the tech news, but I’ve still got the highlights.

For starters, if you haven’t heard yet, TechCrunch launched Extra Crunch, a paid premium subscription offering full of amazing content. As part of Extra Crunch, we’ll be doing deep dives on select businesses, beginning with Patreon. Read Patreon’s founding story here and learn how two college roommates built the world’s leading creator platform. Plus, we’ve got insights on Patreon’s product, business strategy, competitors and more.

Sign up for Extra Crunch membership here.

On to other news…

Y Combinator’s latest batch of startups is huge

So huge the Silicon Valley accelerator had to move locations and set up two stages at its upcoming demo days (March 18-19) to accommodate the more than 200 startups ready to pitch investors (who will have to hop between stages at the event). There will also be a virtual demo day live-streamed for some investors to watch “because there are so few seats.” Here’s what I’m wondering… At what point is a YC cohort too big? If investors aren’t even able to view all the companies at Demo Day, what exactly is the point? Send me your thoughts.

Another week, another SoftBank deal. The Vision Fund’s latest bet is autonomous delivery. The Japanese telecom giant has invested $940 million in Nuro, the developer of a custom unmanned vehicle designed for last-mile delivery of local goods and services. The startup, also backed by Greylock and Gaorong Capital, will use the cash to expand its delivery service, add new partners, hire employees and scale up its fleet of self-driving bots. And while we’re on the subject of autonomous, TuSimple, a self-driving truck startup, has raised a $95 million Series D at a unicorn valuation.

Mamoon Hamid and Ilya Fushman

TechCrunch’s Connie Loizos spoke with Mamoon Hamid and Ilya Fushman, who joined Kleiner Perkins from Social Capital and Index Ventures, respectively. The pair talked about Kleiner Perkins, touching on people who’ve left the firm, how its decision-making process now works, why there are no senior women in its ranks and what they make of SoftBank’s Vision Fund.

Here’s your weekly reminder to send me tips, suggestions and more to kate.clark@techcrunch.com or @KateClarkTweets.

Facebook CEO Mark Zuckerberg considered a multi-billion-dollar purchase of Unity, a game development platform. This is according to a new book coming out next week, “The History of the Future,” by Blake Harris, which digs deep into the founding story of Oculus and the drama surrounding the Facebook acquisition, subsequent lawsuits and personal politics of founder Palmer Luckey. Here’s more on the acquisition-that-could-have-been from TechCrunch’s Lucas Matney.

Indonesia-focused Intudo Ventures raised a new $50 million fund this week to invest in the world’s fourth most populated country; InReach Ventures, the “AI-powered” European VC, closed a new €53 million early-stage vehicle; and btov Partners closed an €80 million fund aimed at industrial tech startups.

Xiaomi-backed electric toothbrush startup Soocas raises $30M

Jobvite raises $200M+ and acquires three recruitment startups to expand its platform play

Opendoor files to raise another $200M

DriveNets emerges from stealth with $110M for its cloud-based alternative to network routers

Figma gets $40M Series C to put design tools in the cloud

Xiaomi-backed electric toothbrush Soocas raises $30 million Series C

Malt raises $28.6 million for its freelancer platform

Elevate Security announces $8M Series A to alter employee security behavior

Massless raises $2M to build an Apple Pencil for virtual reality

Just when you thought the scooter boom and the subscription-boom wouldn’t intersect, Grover arrived to prove you wrong. The startup is launching an e-scooter monthly subscription service in Germany. Their big idea is that instead of purchasing an e-scooter outright, GroverGo customers can enjoy unlimited e-scooter rides without the upfront costs or commitment of owning an e-scooter.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and General Catalyst’s Niko Bonatsos chat startups.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico

We are experimenting with new content forms at TechCrunch. This is a rough draft of something new — provide your feedback directly to the authors: Danny at danny@techcrunch.com or Arman at Arman.Tabatabai@techcrunch.com if you like or hate something here.

Ignoring the midterm hysteria, we continue our obsession with SoftBank today by looking at the group’s IPO of its telecom unit. But first, some thoughts about Form Ds.

Recently, I was looking up the investment history of Patreon (Note: I was an investor in the company through my previous venture firm CRV). I did what I normally do: I went straight to the SEC’s EDGAR system and started searching for the company and its filings. And came up with nothing. Full-text search, office address searches and founder name searches — nothing was returned.

And yet, the company has publicly raised more than $100 million in venture capital according to Crunchbase, and to my knowledge, is not incorporated outside of the United States.

There should be a whole spate of filings, and yet none exist. What’s up with that?

After some investigation, my working hypothesis is that startups are (increasingly?) not filing disclosures with the SEC as a specific strategy to avoid scrutiny.

To take a step back, when companies take money from investors, they sell those investors securities. Under American laws, all securities need to be registered with the Securities and Exchange Commission using pre-defined templates (such as an S-1 registration form) to ensure that all investors know exactly what they are buying.

However, registration is expensive and time-consuming, and so U.S. law also provides a set of exemptions from registration for companies where that process is impractical. Startups take advantage of these exemptions and stay private, until they eventually want to become public through a registration with the SEC.

One mandated component of taking advantage of these registration exemptions is that the startup needs to file a Form D with the SEC. The Form D is free to file and relatively simple, requiring basic information such as the amount of capital fundraised and who the investors were in the round. It’s required to be filed 15 days after the first sale of securities, and, conveniently, the form preempts most state securities laws so that startups don’t have to file in state jurisdictions.

There are theoretically large penalties for failing to file — a company could open itself to investor lawsuits, and there are various financial felonies available that could be applied, as well.

But that’s legal theory, and the practicalities are that almost nothing bad happens to startups that fail to file a Form D. American courts, along with the SEC, have upheld that a startup does not lose its covered security exemption by failing to file the form. The only additional requirement is generally to file state security forms in lieu of the federal form.

A bigger question is why go through this when filing is easy and free? The obvious answer is that startups don’t want to put their round’s information out in the public eye where the good people at TechCrunch will see it and report on it. Of course, the whole point of Form D disclosure is to provide the public a modicum of information about what is happening in the economy.

But actually, the motivations go far beyond that. One reader, Paul David Shrader, saw our note yesterday that we were investigating Form Ds and offered this list of reasons on why companies in general (and to be clear, not specific to any company he has advised) choose to forgo filing:

As for the “why,” there are a few reasons why management, the board of directors, or even investors may be sensitive to fundraising disclosures:

1. The company doesn’t want the increased scrutiny internally that comes along with a new funding round. This can come from employees demanding different levels of compensation.

2. The company doesn’t want increased regulatory scrutiny. Many startups operate in regulatory gray areas, and increased attention from regulators before they are ready can be a Bad Thing.

3. The company has security concerns. For startups that operate in certain environments internationally, raising a monster round can place a target on the backs of its employees. This has been an issue in Latin America from time to time.

4. The company has competitive concerns. Raising a big round may attract new entrants to the market or heighten attention from existing competitors before a startup has solidified its position in the market.

5. Investors don’t want disclosure. Some investors want to disclose new investments on their own timeframe, and they make this a condition of their investment. Publicly-traded investors or sovereign wealth funds may only want to disclose at the time of their quarterly reports.

6. Flat rounds or down rounds can suck away any positive momentum. When founders are trying to convince customers and employees to join the rocket ship that is their company, a flatlining fundraise can look like… well, a flatlining company.

7. The round may not be closed yet. Companies sometimes have optimistic goals about the size of a round (“We’re raising $4 million!”), but only have a smaller amount committed at the outset of the round. Sometimes a single round can take 18+ months to close, even though a sizable (or not so sizable) percentage closed at the outset.

Some of these are obvious, but others, such as internal compensation concerns or international security concerns, were more surprising to me. Thanks Paul David for the thoughts.

Now, I said at the outset that my hypothesis is that startups are increasingly foregoing Form D disclosure. Arman and I are still doing work on this (the SEC has some data sets), but to be frank, it is very hard to operationalize and prove. Form D filings are up or steady, which makes sense given that the number of startups in areas like San Francisco have skyrocketed over the past decade. We are trying to prove something that doesn’t exist, and Karl Popper has helpfully explained that that is impossible.

Nonetheless, we are still interested in whether the legal norms have shifted here, and will hopefully report back on this again. If you are a startup attorney with an opinion here, please email Danny@techcrunch.com or Arman.tabatabai@techcrunch.com with your thoughts.

Photo by Alessandro Di Ciommo/NurPhoto via Getty Images

Talking about filings, one of the most complicated filings in the world is underway. While we were digging into SoftBank’s financing strategies yesterday, all the activity around the looming IPO of its telco business caught our attention.

As we analyzed yesterday, though SoftBank’s debt balance continues to balloon, the company’s balance sheet has rarely prevented it from pursuing investments in the past.

SoftBank continues to dole out multi-billion-dollar checks with stunning regularity, having invested around one-third of its $90+ billion Vision Fund. And we know SoftBank has no intention of slowing its torrid pace, with chairman and CEO Masayoshi Son previously stating he plans to raise $100 billion funds that would spend around $50 billion annually, every two or three years.

One way SoftBank is looking to access additional funding to pour into the next batch of unicorns is by taking a portion of its Japanese mobile business public. For some context, SoftBank is generally considered to be the third largest telco in Japan behind NTT DoCoMo and KDDI.

Even though initial estimates expect SoftBank to only sell around 30-40 percent of the company’s shares, the offering is widely expected to be one of the largest listings ever at potentially more than $25 billion, which would value the overall business at $90 billion on the high end. Reuters recently reported via a Japanese news service that the Tokyo Stock Exchange is expected to give SoftBank approval to list shares next Monday, with a likely listing date of December 19th.

But the progression of the IPO has been oddly complex and unique from the beginning.

First, there was an issue with a set of bonds SoftBank had issued in 2013, which were guaranteed by the telecom business and had covenants requiring that the company hold investment-grade credit ratings before pursuing a sale of any sort. However, SoftBank’s bonds hold junk status from major credit ratings agencies. To fix that roadblock, SoftBank issued a new set of bonds with better terms to buy back the bonds with the prohibitive covenants, undercutting and aggravating some investors of the initial bonds.

Then, it was reported that while lining up the underwriting banks for the IPO, SoftBank reportedly asked banks to commit to loans to the Vision Fund that total around $9 billion, a claim SoftBank has not commented on. As reported by Bloomberg:

The IPO’s top underwriters, which include Nomura Holdings Inc. and Goldman Sachs Group Inc., have given non-binding assurances while they finalize terms of the loan to the Vision Fund, the people said. Stakes in around five of the investment fund’s holdings will be used as collateral, according to the people, who asked not to be identified because the information is private.

Deutsche Bank AG, Mizuho Financial Group Inc. and Sumitomo Mitsui Financial Group Inc. were also among banks chosen to lead SoftBank’s wireless unit IPO, Bloomberg News reported last week. Details of the loan are still being worked out, and terms could change, the people said. Meanwhile, Deutsche Bank and Goldman Sachs committed about $1 billion each, they said.

While the fund’s holdings (perhaps Uber or WeWork or others) would be set as collateral, Bloomberg also reported in the same article that the loans were non-recourse, meaning that if for some reason SoftBank were unable to repay the loan, the lenders would have no claim to any assets outside of the company stakes set as collateral. The loan terms become more concerning with the Vision Fund since it invests in many unlisted and, in many cases, unprofitable companies. As we noted yesterday, at least one potential lender, Bank of America, decided not to participate due to concerns that the terms were too risky.

Such sausage-making isn’t usually visible to the public, which would seem to indicate that at least some of the banks are grousing to reporters about terms they find egregious. As always, feel free to grouse to us as well.

What we are reading (or at least, trying to read)

Powered by WPeMatico

Patreon is forming a patronage empire. Today it acquired white-labeled subscription membership platform Memberful, which lets creators sell exclusive access to content through their own site instead of a centralized platform like Patreon. Rather than being folded into a Patreon feature, Memberful will run as an independent brand, maintaining its tiered pricing structure, though new sign-ups will get a rate closer to Patreon’s low 5 percent rake.

Terms weren’t disclosed for the deal that brings Memberful’s whole seven-person team and 500 paying clients aboard. But Patreon clearly sees rolling up competitors and complements in the patronage space as a worthy use of its $60 million raise at a $450 million valuation late last year that brought it to $105 million in funding. In June, Patreon bought Kit to let creators bundle in merchandise with their perks for paying monthly subscribers. It also bought out competitor Subbable back in 2015.

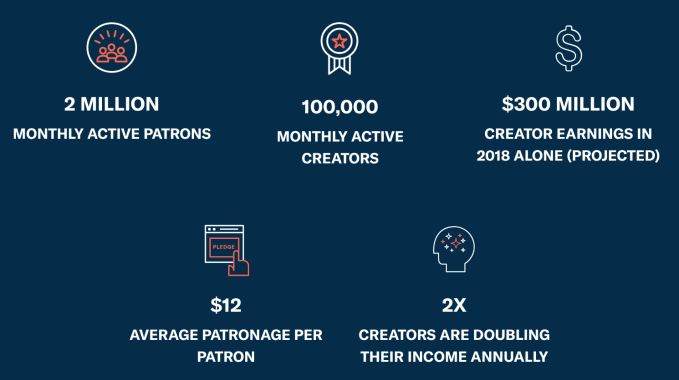

By teaming up, Patreon and Memberful will be able to provide subscription patronage services for creators, whether they want their fan community to live on Patreon, or through Memberful on their own WordPress or website with integrations of Stripe and MailChimp. Patreon already has 2 million patrons paying an average of $12 each to a total of 100,000 creators, and it expects to pay out $300 million in 2018 alone. The acquisition could let Patreon move up market, recruiting comedians, illustrators, game developers and vloggers that already have an established audience elsewhere.

“I think membership is on the up and is going to grow for the next decade,” says Patreon VP of Product Wyatt Jenkins. “Our strategy is to be an open, neutral platform,” as opposed to focusing on one type of content like YouTube with videos or Twitch with streaming where you’re locked into that platform’s tools. Memberful, launched in 2013, has bootstrapped the creation of its white-labeled tools without the need for venture funding.

Memberful gives creators like Stratechery’s Ben Thompson (who has an interview with Patreon CEO Jack Conte about the acquisition) and podcast producer Gimlet Media full control over branding, with no Patreon chrome. But it’s more expensive and also requires more work as creators have to manage their own site, customer service and payment processing. Memberful takes a 10 percent cut with no monthly fee for its limited basic tier, or $25 per month plus 4.9 percent for the full-featured pro version, though it also offers enterprise pricing. That pricing will remain for existing users, but “new customers will see a transaction fee closer to Patreon’s,” which is a flat 5 percent, a Patreon spokesperson tells me. Patreon does basically everything for a creator, but it also ropes them into the Patreon-branded ecosystem that also promotes other content makers.

Sometimes Patreon handling everything can be a problem, though. Last week it experienced a higher-than-normal volume of declines from banks of charges to patrons. That left some creators without their expected income, and required patrons to deal with the chore of calling their bank to tell them paying $1, $5 or $20 per month to their favorite creator wasn’t fraud. Patreon now tells me that “as of Friday, we let everyone know that we were back to normal decline rates, and were going to continue retrying the rest of the cards like we normally do.”

It makes sense for Patreon to race to consolidate the patronage industry as it’s being invaded by giant incumbents. Twitch, YouTube and Facebook all offer their own versions of paid subscriptions to creators that get patrons extra perks like exclusive content or badges so they stick out in chat rooms full of fans. While those platforms are all focused on video streamers, they still pose a threat to Patreon, which needs to maximize the number of successful creators it hosts in order to earn enough from its tiny cut of payments. Facebook especially could muscle in, as many creators already run their own Facebook Pages.

Asked about competition from those platforms, Jenkins said, “I think there’s a strong chance it’s a tailwind. The concept of membership is pretty new. If those big companies are going to drop millions of dollars into marketing the concept of membership I think that’s great.” He stressed the question of “Do you want to own your fan base? On YouTube, those aren’t your fans, they’re YouTube users. YouTube is incentivized to keep them watching videos so it can show ads.”

That might lead fans to unsubscribe from a creator as YouTube promotes other similar ones they could watch instead. “You don’t own the relationship.” Facebook Page admins have found that out the hard way as algorithm changes prioritize friends over public figures, making it tough to reach the followers they spent years begging to like them. If Patreon can offer creators audience growth through discovery on its interconnected network without cannibalizing anyone’s member counts, its neutrality and focus could make it a leader in this new wing of the digital economy.

Powered by WPeMatico