paris

Auto Added by WPeMatico

Auto Added by WPeMatico

When Shomik Dutta and Betsy Hoover first met in 2007, he was coordinating fundraising and get-out-the-vote efforts for Barack Obama’s first presidential campaign and she was a deputy field director for the campaign.

Over the next two election cycles the two would become part of an organizing and fundraising team that transformed the business of politics through its use of technology — supposedly laying the groundwork for years of Democratic dominance in organizing, fundraising, polling and grassroots advocacy.

Then came Donald J. Trump and the 2016 election.

For both Dutta and Hoover, the 2016 outcome was a wake-up call against complacency. What had worked for the Democratic party in 2008 and 2012 wasn’t going to be effective in future election cycles, so they created the investment firm Higher Ground Labs to provide financing and a launching pad for new companies serving Democratic campaigns and progressive organizations.

“As the political world shifts from analog to digital, we need a lot more tools to capture that spend,” says Dutta. “Democrats are spending on average 70 cents of every dollar raised on television ads. We are addicted to old ways of campaigning. If we want to activate and engage an enduring majority of voters we have to go where they are (and that’s increasingly online) and we have to adapt to be able to have these conversations wherever they are.”

While the Obama campaign effectively used the internet as a mobilization tool in its two campaigns, the lessons of social media and mobile technologies that offer a “direct-to-consumer” politics circumventing traditional norms have, in the ensuing years, been harnessed most effectively by conservative organizations, according to some scholars and activists.

“The internet is a tool and in that sense it’s neutral, but just like other communication tools from the past, people with more power, with more resources, with more organization, have been able to take advantage of it,” Jen Schradie, an assistant professor at the Observatoire sociologique du changement at Sciences Po in Paris, told Vox in an interview earlier this month.

Schradie is a scholar whose recent book, “The Revolution That Wasn’t,” contends that the internet’s early application as a progressive organizing tool has been overtaken by more conservative elements. “The idea of neutrality seems more true of the internet because the costs of distributing information are dramatically lower than with something like television or radio or other communication tools,” she said. “However, to make full use of the internet, you still need substantial resources and time and motivation. The people who can afford to do this, who can fund the right digital strategy, create a major imbalance in their favor.”

Schradie contends that a web of privately funded think tanks, media organizations, talk radio and — increasingly — mobile applications have woven a conservative stitch into the fabric of social media. The medium’s own tendency to promote polarizing and fringe viewpoints also served to amplify the views of pundits who were previously believed to be political outliers.

Essentially, these sites have enabled commentators and personalities to create a patchwork of “grassroots” organizations and media operations dedicated to reaching an audience receptive to their particular political message that’s funded by billionaire donors and apolitical corporate ad dollars.

Then there’s the technology companies, like Cambridge Analytica, which improperly used access to Facebook data for targeting purposes — also financed by these same billionaires.

“The last six years have witnessed millions and millions of dollars of private Koch money and Mercer money that have gone to pretty sophisticated data and media efforts to advance the Republican agenda,” says Dutta. “I want to even the scale.”

Dutta is referring to Charles and David Koch and Robert Mercer, the scions and founder (respectively) of two family dynasties worth billions. The Koch brothers support a web of political advocacy groups, while Mercer and his daughter were large backers of Breitbart News and Cambridge Analytica, two organizations that arguably provided much of the policy underpinnings and online political machinery for the Trump presidential campaign.

But there’s also the simple fact that Donald Trump’s digital strategy director, Brad Parscale, was able to effectively and inexpensively leverage the social media tools and data troves amassed by the Republican National Committee that were already available to the candidate who won the Republican primary. In fact, in the wake of Romney’s loss, Republicans spent years building up profiles of 200 million Americans for targeted messaging in the 2016 election.

“Who controls Facebook controls the 2016 election,” Parscale said during a speaking engagement at the Romanian Academy of Sciences, according to a report in Forbes.

Parscale, now the campaign manager for the president’s 2020 reelection campaign recalled, “These guys from Facebook walked into my office and said: ‘we have a beta … it’s a new onboarding tool … you can onboard audiences straight into Facebook and we will match them to their Facebook accounts,’ ” according to Forbes .

During the 2016 campaign, Hillary Clinton’s team made 66,000 visual ads, according to Parscale, while the Trump campaign made 5.9 million ads by leveraging social media networks and the language of memes. And in the run-up to the 2020 election, Parscale intends to go back to the same well. The Trump campaign has already spent more than $5 million on Facebook ads in the current election cycle, according to The New York Times — outspending every single Democratic candidate in the field and roughly all of the Democrats combined.

Dutta and Hoover are working to offset this movement with investments of their own. Back in 2017, the two launched Higher Ground Labs, an early-stage company accelerator and investment firm dedicated to financing technology companies that could support progressive causes.

The firm has $15 million committed from investors, including Reid Hoffman, the co-founder of LinkedIn and a partner at Greylock; Ron Conway, the founder of SV Angel and an early backer of Google, Facebook and Twitter; Chris Sacca, an early investor in Uber; and Elizabeth Cutler, the founder of SoulCycle. Already, Higher Ground has invested in more than 30 companies focused on services like advocacy outreach, polling and campaign organizing — among others.

The latest cohort of companies to receive backing Higher Ground Labs

“It is vitally important that Democrats learn to do their campaigns online,” says Dutta. “The way you recruit volunteers; the way you poll sentiment; the way you target and mobilize voters has to be done with online tools and has to improve in the progressive movement and that’s the job of Higher Ground Labs to fix.”

For-profit companies have a critical role to play in election organizing and mobilization, Dutta says. Thanks to government regulation, only private companies are allowed to trade data across organizations and causes (provided they do it at fair market value). That means advocacy groups, unions and others can tap the information these companies collect — for a fee.

The Democratic Party already has one highly valued private company that it uses for its technology services. Formed from the merger of NGP Software and Voter Activation Network, two companies that got their start in the late 1990s and early 2000s, NGP VAN is the largest software and technology services provider for Democratic campaigns. It’s also a highly valued company, which received roughly $100 million in financing last year from the private equity firm Insight Venture Partners, according to people familiar with the investment. Terms of the deal were not disclosed.

“Our vision has been to build a platform that would break down the painful data silos that exist in the campaigns and nonprofit space, and to offer truly best-in-class digital, fundraising and organizing features that could serve both the largest and the smallest nonprofits and campaigns, all with one unified CRM,” wrote Stu Trevelyan, the chief executive of NGP VAN + EveryAction, in an August blogpost announcing the investment. “We’re so excited that others, like our new partners at Insight, share that vision, and we can’t wait to continue innovating and growing together in the coming years.”

Even as private equity dollars boost the firepower of organizations like NGP VAN, venture capitalists are financing several companies from the Higher Ground Labs portfolio.

Civis Analytics, a startup founded by the former chief analytics officer of Barack Obama’s 2012 reelection campaign, raised $22 million from outside investors, and counts Higher Ground Labs among its backers. Qriously, another Higher Ground Labs portfolio company, was acquired by Brandwatch, as was GroundBase, a messaging platform acquired by the nonprofit progressive advocacy organization ACRONYM.

Other companies in the portfolio are also attracting serious attention from investors. Standouts like Civis Analytics and Hustle, which raised $30 million last May, show that investors are buying into the proposition that these companies can build lasting businesses serving Democratic and progressive political campaigns and corporate businesses that would also like to rally employees or personalize a marketing pitch to customers.

These are companies like Change Research, an earlier-stage company that just launched from Higher Ground Labs accelerator last year. That company, founded by Mike Greenfield, a serial Silicon Valley entrepreneur who was the first data scientist working on the problem of fraud detection at PayPal, and Pat Reilly, a communications professional who worked with state and local Democratic politicians, is slashing the cost of political polling.

“I wanted to do something for American democracy to try and improve the state of things,” Greenfield said in an interview last year.

For Greenfield, that meant increasing access to polling information. He cited the test case of a Kansas special election in a district that Donald Trump had won by 27 points. Using his own proprietary polling data, Greenfield predicted that the Democratic challenger, James Thompson, would pose a significant threat to his Republican opponent, Mike Estes.

Estes went on to a 7% victory at the ballot, but Thompson’s campaign did not have access to polling data that could have helped inform his messaging and — potentially — sway the election, said Greenfield.

“Public opinion is used to ween out who can be most successful based on how much money they’re able to raise for a poll,” says Reilly. It’s another way that electoral politics is skewed in favor of the people with disposable income to spend what is a not-insignificant amount of money on campaigns.

Polls alone can cost between $20,000 to $30,000 — and Change Research has been able to cut that by 80% to 90%, according to the company’s founders.

“It’s safe to say that most of the world was stunned by the outcome [of the presidential election] because most polls predicted the opposite,” says Greenfield. “Being a good American and as a parent of a 10-year-old and a 12-year-old, providing forward-thinking candidates and causes with the kind of insight they needed to win up and down the ballot could not only be a good business, but really help us save our democracy.”

Change Research isn’t just polling for politicians. Last year, the company conducted roughly 500 polls for political candidates and advocacy groups.

“The way that I’ve described Change Research to investors is that we want to simultaneously move the world in a better direction and having a positive impact while building a substantial business,” says Greenfield. “We’re only going to work with candidates and causes that we’re aligned with.”

Being exclusively focused on progressive causes isn’t the liability that many in the broader business community would think, says Dutta. Many Democratic organizations won’t work with companies that sell services to both sides of the aisle.

For Higher Ground Labs, a stipulation for receiving their money is a commitment not to work with any Republican candidate. Corporations are okay, but conservative causes and organizations are forbidden.

“We’re in a moment of existential crisis in America and this Republican party is deeply toxic to the health and future of our country,” says Dutta. “The only path out of this mess is to vote Republicans out of office and to do that we need to make it easier for good candidates to run for office and to engage a broader electorate into voting regularly.”

Powered by WPeMatico

When SeedLegals launched in 2017 in the U.K., I’d say many of us thought, “why has that not been done before?” After all, two things have happened that make this an obvious idea for a startup: startup funding rounds are now so common that there is no reason large amounts of automation could not be done. If you can buy a divorce online, surely you can organise funding rounds?

The second trend is the sheer level of automation happening in legal software today. After all, we now have “Uber for Lawyers” (Lexoo, Linkilaw, Lawbite) and AI-driven legaltech (KIRA, Luminance, ThoughtRiver). (Eventually, we will have blockchain smart contracts do ALL the work, but that’s for another time…).

So it’s not surprising that today SeedLegals announces it has closed a $4 million Series A led by venture capital firm Index Ventures (London/SF/etc.) with participation from Kima Ventures (Paris/TelAviv), The Family (Paris) and existing investor Seedcamp (London).

SeedLegals says it now has 7,000 startups — capturing, it claims, 8% of all early-stage U.K. funding rounds — using its platform to manage the entire fundraising process and all related legal documents. The platform helps companies build and negotiate term sheets, shareholder agreements, cap tables, stock option allocations, EIS approvals, hiring agreements, NDAs and more.

It also has two new products: SeedFAST and Instant Investment, which enable startups to quickly top up investment between funding rounds.

If U.K. companies created more than 27,000 contracts on SeedLegals last year, the start-up reckons that saved them an estimated £4.5 million in legal costs. Normally, lawyers create custom documents for each transaction. That means 18 weeks, on average, to complete a funding round, with legal fees starting at £3,000 for a simple seed round to £20,000 and up for each side for later-stage rounds.

The platform replaces spreadsheets and Word docs with a database-driven platform. You enter data once and the system uses pre-built knowledge, deal data and document automation to dynamically build all the outputs.

Anthony Rose, co-founder and CEO at SeedLegals, says they have removed the “complexity, unnecessary middlemen, standardized and automated the processes, and that has really resonated with both founders and investors.”

Hannah Seal from Index Ventures, who joins the board with this round, commented: “SeedLegals

is making the complex process of fundraising straightforward for everyone involved.

“We closed this round on SeedLegals and have been impressed with the speed and ease of use. For startups who spend thousands on legal fees on agreements that vary little from company to company, this is an absolute no-brainer.”

SeedLegals was created by serial entrepreneur Anthony Rose, known in the tech industry for his work launching BBC iPlayer, and VC and angel investor Laurent Laffy, whose own portfolio includes consumer brands such as Graze and Secret Escapes .

Powered by WPeMatico

DNA Script has raised $38.5 million in new financing to commercialize a process that it claims is the first big leap forward in manufacturing genetic material.

The revolution in synthetic biology that’s reshaping industries from medicine to agriculture rests on three, equally important pillars.

They include: analytics — the ability to map the genome and understand the function of different genes; synthesis — the ability to manufacture DNA to achieve certain functions; and gene editing — the CRISPR-based technologies that allow for the addition or subtraction of genetic code.

New technologies have already been introduced to transform the analytics and editing of genomes, but little progress has been made over the past 50 years in the ways in which genetic material is manufactured. That’s exactly the problem that DNA Script is trying to solve.

Traditionally, making DNA involved the use of chemical compounds to synthesize (or write) DNA in chains that were limited to around 200 nucleotide bases. Those synthetic pieces of genetic code are then assembled to make a gene.

DNA Script’s technology holds the promise of making longer chains of nucleotides by mirroring the enzymatic process through which DNA is assembled within cells — with fewer errors and no chemical waste material. The enzymatic process can accelerate commercial applications in healthcare, chemical manufacturing and agriculture.

“Any technology that can make that faster is going to be very valuable,” says Christopher Voigt, a synthetic biologist at the Massachusetts Institute of Technology in Cambridge, told the journal Nature.

DNA Script isn’t the only company in the market that’s looking to make the leap forward in enzymatic DNA production. Nuclear, a startup working with Harvard University’s famed geneticist, George Church, and Ansa Bio, a startup affiliated with Jay Keasling’s Berkeley lab at the University of California, are also moving forward with the technology.

But the Paris-based company has achieved some milestones that would make its technology potentially the first to come to market with a commercially viable approach.

At least, that’s what new investors LSP and Bpifrance, through its Large Venture fund, are hoping. They’re joined by previous investors Illumina Ventures, M. Ventures, Sofinnova Partners, Kurma Partners and Idinvest Partners in backing the company’s latest funding.

The company said the money would be used to accelerate the development of its first products and establish a presence in the United States.

“As we announced earlier this year at the AGBT General Meeting, DNA Script was the first company to enzymatically synthesize a 200mer oligo de novo with an average coupling efficiency that rivals the best organic chemical processes in use today,” said Thomas Ybert, chief executive and co-founder of DNA Script. “Our technology is now reliable enough for its first commercial applications, which we believe will deliver the promise of same-day results to researchers everywhere, with DNA synthesis that can be completed in just a few hours.”

Powered by WPeMatico

Activision Blizzard said it has lined up five franchises for a new, city-based Call of Duty esports league.

Atlanta, Dallas, New York, Paris and Toronto will all play host to franchise teams that will compete in a professional league based on what is perhaps Activision Blizzard’s most successful title, the company announced after its earnings call earlier today.

Each city is partnering with existing Overwatch League team owners to leverage the existing framework that Activision has labored over for the past few years to lay the groundwork for a global, city-based Call of Duty league, the company said.

The first teams are Atlanta Esports Ventures, the joint venture owned by Cox Enterprises and Province Inc.; the Envy Gaming esports team, which has been active in Call of Duty competitive play since 2007 and with the Dallas Fuel Overwatch league team; New York’s Sterling.VC, a sports media company backed by Sterling Equities (owners of the New York Mets); c0ntact Gaming, which owns the Overwatch League team Paris Eternal and the Paris-based Call of Duty team; and Toronto’s OverActive Media.

“The upcoming launch of our new Call of Duty esports league reaffirms our leadership role in the development of professional esports. We have already sold Call of Duty teams in Atlanta, Dallas, New York, Paris and Toronto to existing Overwatch League team owners, and we will announce additional owners and markets later this year,” said Bobby Kotick, chief executive of Activision Blizzard. “Our owners value our professional, global city-based model, the success we have had with broadcast partners, sponsors and licensees, and the passion with which our players have responded to our events.”

The announcement came on the heels of an earnings announcement that saw the company report earnings of $1.825 billion for the quarter, beating its outlook of $1.715 billion but down slightly from the year ago period when the company brought in almost $2 billion.

The company credited esports and its Overwatch League and the newly announced Call of Duty city-based league (including selling its first five teams to cities) for contributing to the better-than-expected numbers.

Powered by WPeMatico

In the nine years since private equity and venture capital investments into sustainable technologies last crossed the $6 billion threshold, the problems caused by global carbon emissions have only intensified.

Now, as the world confronts the reality that there’s not much time left to reverse course on carbon emissions and the impact they will have on life on earth, both corporate and private investors are once again stepping up their commitments to startups in the space.

In 2018, global venture capital investment into startups focused on sustainability jumped 127 percent, to $9.2 billion, the highest since 2010, according to a January report from Bloomberg New Energy Finance. Powering that boost was a $1.1 billion investment in the smart window maker, View, and another $795 million for Chinese electric vehicle firm Youxia Motors. In fact, there were no fewer than eight VC/PE financings of Chinese EV specialist companies in 2018, totaling some $3.3 billion.

That stark assessment is coming from more corners of the scientific community, and the reality of the danger is being emphasized by politicians and concerned citizens around the globe.

The simple truth is that things are getting worse. And for the past two years, emissions have been increasing as countries continue to use oil and gas and coal to fuel economic growth, even as the global community realizes that carbon emissions are an increasing threat.

A recent assessment by the U.S. government put the cost of climate change caused by carbon emissions at $500 billion annually by the end of the century. And the financial toll doesn’t begin to assess the cost to the quality of human life and the potential lives that will be lost because of climate-related disasters.

This isn’t the first time the world has realized the threat climate change poses. It’s not even the second. Back in 1979 — and throughout the next decade — the U.S. grappled with how to craft an appropriate response to the coming climate-related crisis. Perhaps unsurprisingly, the government failed, and the issue of imminent climate disaster was set aside.

Former Vice President Al Gore picked up the thread in the mid-2000s in the wake of his defeat to the Connecticut Yankee turned Texas oilman George W. Bush in the contested 2000 presidential election. Through advocacy work and the popular climate-focused documentary “An Inconvenient Truth,” Gore was able to proselytize among a group of technocrats looking for the next big thing in the wake of the internet explosion that had transformed professional and personal lives.

Venture capital investors flocked to invest in renewable technologies — from biofuels to new solar energy generating technologies to new battery chemistries and beyond.

Over the next seven years billion-dollar companies would rise and fall on the back of speculative investment in the promise of a cleaner energy future that would disrupt the oil industry and turn billionaires into multi-billionaires — all while saving the world.

It didn’t work out.

Problems with scaling technologies beyond a controlled laboratory setting; global economic pressures wrought by an explosion of manufacturing capacity in countries like China; and the hubris of investors who thought that their investment acumen in picking winners of the information age could work just as well in centuries-old industries like oil and gas, or electricity, found themselves floundering in complicated, regulated markets with deep-pocketed incumbents and entrenched interests in promoting the status quo.

In the process, investors lost hundreds of millions of dollars in the U.S. alone, and destabilized some of the oldest firms in the investment industry.

Now, companies and investors are returning to the market in a major way. Some of the largest businesses in the food and agriculture industry are investing in new companies that are developing protein replacements and novel cultivation technologies; utilities are investing more heavily in smart grid technologies as electrification and microgrids become more real; automakers and battery manufacturers are backing new energy storage technologies; and frontier investors are backing companies tackling everything from biologically based chemical manufacturing to new construction technologies for smart homes and cities, to new kinds of nuclear power that could transform how the world conceives of energy abundance (along with geo-engineering tech to remove carbon from the atmosphere).

“In the last few years, the number of technologies ripe for investment has expanded dramatically,” Ravi Manghani, research director for energy storage at Wood Mackenzie, an energy research and consultancy firm, told CNBC in March. “It’s no longer just three or four technology verticals.”

While none of these technological advancements are a guaranteed solution to the threats carbon emissions pose, or are surefire commercially viable businesses, the fact that investors are once again looking at sustainability as a viable investment thesis — capable of producing multiple billion-dollar businesses — is a good step forward.

Any plan to address decarbonization has to confront industries as diverse as agriculture, construction, transportation, chemicals and consumer goods from clothes to chemicals.

Failure to confront these challenges would be catastrophic. Even if global warming is restricted to just the 2 degree Celsius target set at the Paris climate agreement, that could mean the extinction of the world’s tropical reefs and several meters of sea-level rise, as The New York Times reported last August. Already the impacts of climate change have meant tens of billions of dollars in damage for the U.S. in 2018 alone.

“The era of incrementalism on climate change is over,” said Massachusetts Senator Ed Markey, one of the architects of the “Green New Deal” legislation, in an interview with Vox. “We are now in the era of the Green New Deal. It’s not going away. It is creating an incentive for governors to do more, for mayors to do more, for companies to do more. The polling says it has political legs that will drive it right into the election of 2020, and when that cycle is done, I think we’re going to see a much greater capacity for us to take the kind of action that we need.”

Powered by WPeMatico

We were promised flying cars but, as it turns out, flying boats were easier to build.

SeaBubbles, a “flying” boat startup that uses electric power instead of gas, hit Miami this weekend to show off one of its five prototype boats — or six, if you count an early, windowless white boat they’ve lovingly dubbed the “soapdish.” This innovative boat design combines technology from nautical industries and aviation and intelligent software to raise the hull of the boat out of the water using foils, which helps it consume less energy by allowing it to travel on rougher waters with reduced drag, while also keeping the passenger cabin relatively comfortable.

When raised, the boat is “flying” above the water, so to speak.

Founded only three years ago in Paris, the idea for SeaBubbles was dreamed up by Alain Thébault, a sailor who previously designed and piloted the Hydroptère, an experimental hydrofoil trimaran, using a similar system that lifts the boat in order to reduce drag. That boat went on to break the world record for sailing speed twice, at 50.17 knots. Meanwhile, SeaBubbles’ co-founder Anders Bringdal is a four-time windsurfing world champion, who also set a windsurfing world record at 51.45 knots.

Together, the two have envisioned SeaBubbles as a way for cities to reduce traffic congestion and help the environment by taking advantage of the area’s waterways to move people around in fast water taxis.

“The cities today have one thing in common: pollution and congestion,” explains Bringdal. “Every city has waterways — ones that are fairly unused. Think about having a giant freeway that goes straight down the center of the city, and no one uses it… why is that?,” Bringdal continues.

“You could do this with a normal boat,” he admits. “But with a normal boat with a normal combustion engine, the fuel price you’re paying is between $70 and $130 per hour. With us, it’s $2,” he says.

The cost savings come from an all-electric design, which means the boat charges at a power station — preferably one that’s solar charged, of course — instead of guzzling gas.

The company experimented with all sorts of designs and models before settling on its first-to-market SeaBubbles water taxi: a smaller, 4.5-meter version that seats four in addition to the pilot. However, the technology itself is scalable to larger boats or even ferries.

According to SeaBubbles’ U.S. partner, Daniel Berrebi, whose company Baja Ferries has made a “small” investment in SeaBubbles, even larger boats like his could eventually benefit from the technology.

Beyond his obvious business interest on that front, Berrebi is also working with SeaBubbles to help the company make its first U.S. sales. He says he’s sold four boats to private individuals in the area — yes, sold as in “checks in hand, and signed on the dotted line.” These buyers don’t want to be named, but may include well-known names in music and sports. (Of course one has to wonder how much anonymity they will really have when tooling about Miami waterways in one of only a handful of these flying boats currently in existence?)

SeaBubbles has been able to come to market with its technology so soon because it’s not building everything in-house.

The boats’ engines are from Torqeedo, for example, while the fly-by-wire software to control the boat comes from foiling and flight control systems engineer Ricardo Bencatel’s company, 4DC Tech. His software solution also powered America’s Cup teams’ boats, like those from Artemis Racing and Oracle. But the version running on SeaBubbles has customized components to control the boat’s unique features.

“The [SeaBubbles] boat has three main sensors — it has two high-altitude sensors to measure the height of the water, then it has a gyroscope — like the one in cell phones,” explains Bencatel.

“The computer combines those measurements from the sensors, then it knows the angles of the boat, the height and the speed,” he says. The software then uses this information to control the flaps on the boat to make adjustments. “For example, the lift — if you want to go higher,” Bencatel says. “Or if it’s rolling to one of the sides, it uses the flaps to turn it to the other side. Or if it’s pitching — bow down or bow up — it uses the front or the rear flaps,” he adds.

And all of these adjustments are being made automatically, by way of software, meaning the boat operator only really has to turn the wheel and drive. They don’t have to think about when to raise or lower the boat — it just happens when the boat reaches a certain speed. Under six knots, the boat is experiencing 100 percent drag, while above eight knots, the boat is “flying” and the drag is reduced to 60 percent. This makes the ride less bumpy, too.

The lithium-ion batteries used by SeaBubbles are IP67 waterproof, and, over time, the boat could make up for its high sticker price — $200,000 at its suggested retail price — with savings on gasoline and reduced maintenance costs.

The prototype version of the SeaBubbles boat has only 1.5 hours autonomy and a five-hour battery recharge to show off the technology. But the company claims the versions going into production have 2.5 hours autonomy and a 35-minute recharge. These are the ones they expect to ship this summer to the first purchasers.

In addition to Miami, SeaBubbles also has customers in Russia — a luxury hotel in Moscow and a deal in St. Petersburg — as well as in Rotterdam and Amsterdam. It plans to start building boats for these markets, and hopes to reach Paris by this summer or the next. In Paris, the prototype boats run slower — take-off speed is six knots, and cruising speed tops out at 15 knots. The production version is faster due to bigger engines, with an average cruising speed of 16 knots and a top speed of 20 knots.

The company is in Miami this week to show off its boat to more buyers, and take meetings with local officials.

Bringdal admits that some of the company’s earlier statements may have been overly ambitious — like having boats in 50 cities by 2024. ”I think, in reality, it’s step by step,” he says. “We’re very happy to be seeing something here in the U.S.”

SeaBubbles, which has seven staff full-time and 25 people, including contractors, has raised $14 million to date from investors, including the founder of drone maker Parrot, Henri Seydoux; Partech Ventures; the French government-backed BPI fund; MAIF, a French insurance group; as well as friends, family and other angels.

The company is preparing to raise a Series A.

(Photo credits: Alain Thébault and Sarah Perez)

Powered by WPeMatico

The City of Paris first warned Airbnb, and it is now taking action. The mayor of Paris, Anne Hidalgo, told the JDD that the city is suing the company for 1,010 illegal listings. The fine could be worth as much as $14.2 million (€12.625 million).

Based on current legislation, you can’t rent an apartment more than 120 days a year. If you want to rent an apartment on Airbnb in Paris, you first must register your apartment with the city. The city then gives you an ID number so they can track how many nights you’re listing your apartment on Airbnb.

And yet, many listings still don’t have that ID number. The mayor’s office flagged around 1,000 apartments back in December 2017 and said Airbnb was dragging its feet. The company had little incentive to comply, as hosts were responsible for their own listings.

Thanks to a new law, the responsibility is now shared between the hosts and the platform. The City of Paris can now fine Airbnb for all those illegal listings, up to €12,500 per listing.

According to Hidalgo, Airbnb has been putting too much pressure on the housing market. She thinks that 65,000 apartments are now reserved for Airbnb in Paris alone. In some areas, it has become quite hard to find an apartment because of that. Local shops also suffer because tourists have different needs. In addition to better monitoring, Hidalgo is also in favor of restricting listings to 30 nights per year.

Airbnb told the JDD that it has complied with regulations and informed all Airbnb hosts about the new rules. The company also says that regulation in Paris doesn’t comply with European regulation. It’s clear that this fight is not over.

Powered by WPeMatico

First it was the notch, now the hole-punch has emerged as the latest tech for concealing selfie cameras whilst keeping our smartphones as free of bezel as possible to maximize the screen space.

This week, Samsung and Huawei both unveiled new phones that dispense with the iconic “notch” — pioneered by Apple but popularized by everyone — in favor of positioning the front-facing camera in a small “Infinity-O” hole located on the top-left side of the screen.

Dubbed hole-punch, the approach is part of Samsung’s new Galaxy A8s and Huawei’s View 20, which were unveiled hours apart on Tuesday. Huawei was first by just hours, although Samsung has been pretty public with its intention to explore a number notch alternatives, including the hole-punch, which makes sense given that it has persistently mocked Apple for the feature.

The Samsung Galaxy S8a will debut in China with a hole-punch spot for the camera [Image via Samsung]

Don’t expect to see any hole-punches just yet though.

The Samsung A8s is just for China right now, while the View 20 isn’t being fully unveiled until December 26 in China and, for global audiences, January 22 in Paris. We also don’t have a price for either, but they do represent a new trend that could become widely adopted across phones from other OEMs in 2019.

That’s certainly Samsung’s plan. The Korea firm is rolling out the hole-punch on the A8s, but it has plans to expand its adoption into other devices and series. The A8s itself is pretty mid-range, but that makes it an ideal candidate to test the potential appeal of a more subtle selfie camera since Samsung’s market share has fallen in China where local rivals have pushed it hard. It starts there, but it could yet be adopted in higher-end devices with global availability.

As for the View 20, Huawei has also been pretty global with its ambitions, except in the U.S., where it hasn’t managed to strike a carrier deal despite reports that it has been close before. The current crisis with its CFO — the daughter of the company’s founder who was arrested during a trip to Canada — is another stark reminder that Huawei’s business is unlikely to ever get a break in the U.S. market: so expect the View 20 to be a model for Europe and Asia.

Huawei previewed its View 20 with a punch-hole selfie camera lens this week [Image via Huawei]

Samsung hasn’t said a tonne about the hole-punch design, but our sister publication Engadget — which attended the View 20’s early launch event in Hong Kong — said it was mounted below the display “like a diamond” to maintain the structure.

“This hole is not a traditional hole,” Huawei told Engadget.

Huawei will no doubt also talk up the fact that its hole is 4.5mm versus an apparent 6mm from Samsung.

Small details aside, one important upcoming trend from these new devices is the birth of the “mega” megapixel smartphone camera.

The View 20 packs a whopping 48-megapixel lens for a rear camera, which is something that we’re going to see a lot more of in 2019. Xiaomi, for one, is preparing a January launch for a device that’ll have the 48-megapixel camera, according to a message on Sina Weibo from company co-founder Bin Lin. There’s no word on which camera enclosure that device will have, though.

Xiaomi teased an upcoming smartphone that’ll sport a 48-megapixel camera [Image via Bin Lin/Weibo]

Powered by WPeMatico

The dream of a startup founder can often be summarized by the following well-intentioned, and mostly delusional, quote: “We’ll raise a few rounds and in a few years we’ll IPO on Nasdaq.”

But a more likely scenario looks something like this:

You invest a few years of hard work to build something of value. One day you receive an acquisition offer out of the blue. You’re elated. And you’re not prepared. You drop everything to focus on this opportunity. Exclusive due diligence starts. Your company is a mess (IP, contracts, burn). Days become weeks; weeks become months. You’ve neglected business and fundraising. You’re running out of money. M&A is now your one and only option. The buyer says they found a bunch of cockroaches in the walls and drops the price. Now what?

Sound unlikely?

This is still a favorable situation: You had an offer! Think about how much time you invested in your various funding rounds. The hundreds of names and Google spreadsheet or Streak-powered quasi-CRM process.

Have you spent even a fraction of that on understanding exit paths? If you’d rather not live the situation described above, read along.

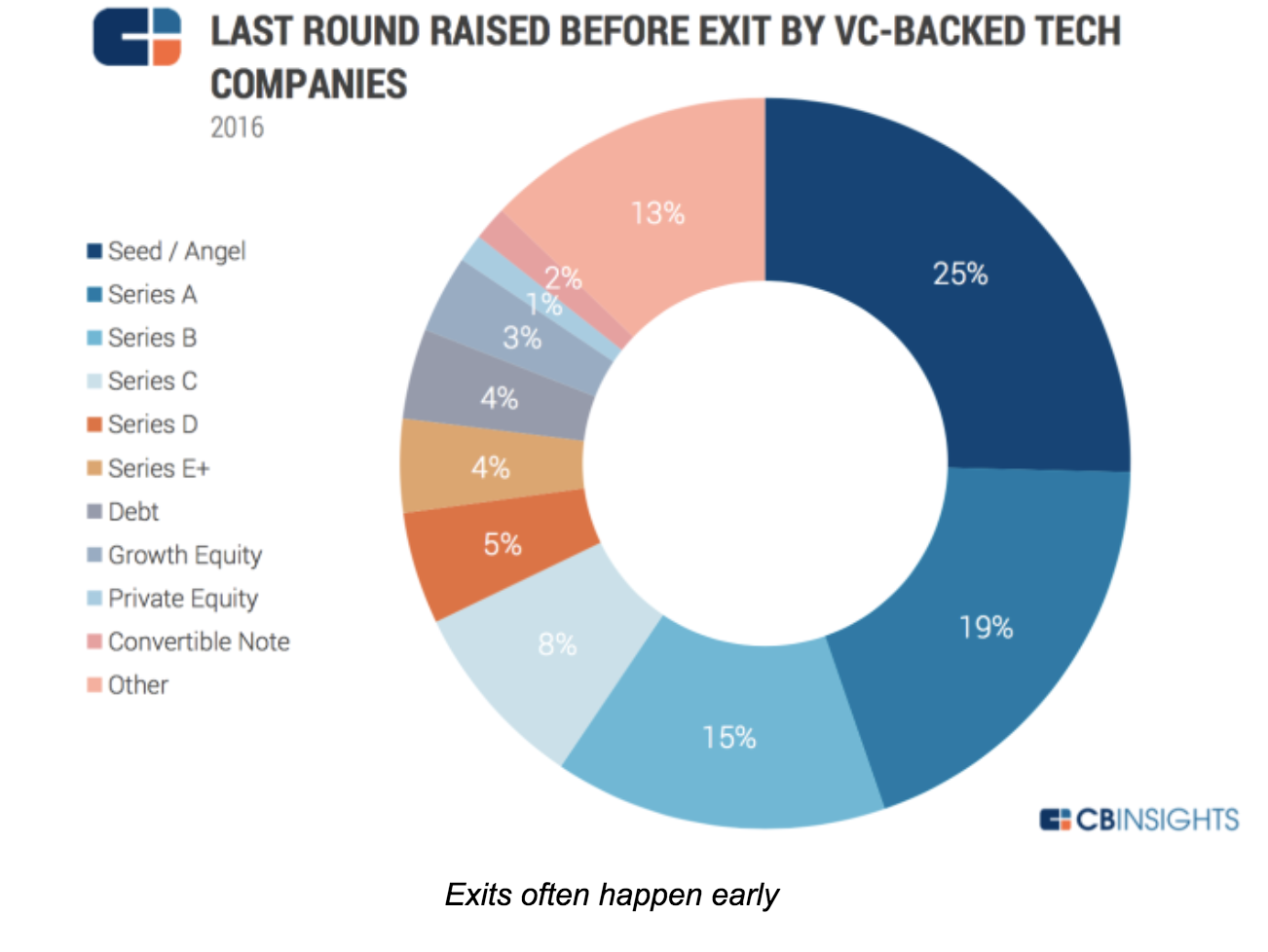

Investors live by exits, but many founders keep dreaming of unicornization and avoid the “E-word” until it’s too late. Yet, in 2016, 97 percent of exits were M&As. And most happened before Series B.

Exits matter because that’s when you, your team and your investors get paid. Oddly enough, and to use a chess metaphor, we hear a lot about the “opening game” (lean startup) and the “mid-game” (growth), but very little about this “end game.”

As a result, founders miss opportunities or leave money on the table. This is a shame. Our fund has more than 700 companies in portfolio. We want the best possible exit for each of them. And fortune favors the prepared! Now, how to get 700 exits (and counting)?

To explore the topic, we organized a series of Master Classes tapping corporate buyers, bankers, investors, lawyers and startup CEOs with M&A or IPO experience in San Francisco. It was a group that included the founders of Guitar Hero — bought by Activision; JUMP Bikes — a SOSV portfolio company bought by Uber, Ubiquisys — bought by Cisco and Withings — bought by Nokia. Each one for hundreds of millions.

Their observations can be summarized below.

“Founders must be aware of what contributes to an exit. This means understanding partnerships and how they are formed in the business space the entrepreneur is working in,” said one Master Class participant.

As founders, you build your product, your company and… optionality. You need to understand the options open to your company, and take steps to enable them.

The most likely one is an acquisition, but there are others like IPO (including small cap), RTO, SBO, LBO, Equity Crowdfunding and even ICO.

“Exit is not a goal per se, but as a CEO it is something you should think about as early in your cycle as possible, while being business-focused,” said the London-based investor Frederic Rombaut, of Seraphim Capital.

Indeed, most participants said that exits should always be on the chief executive’s agenda, no matter how early in the process. “Exits should be on the CEO agenda. Not front and center, but on the agenda. M&A is a by-product of a great business and targeted BD. IPOs are always an option once you’ve built significant cashflow forecasting.”

It’s important to ask questions like: How many “strategic engagements” with potential buyers have you had this month? Is your message and value clear in their eyes? Have you considered an acquisition track in parallel to a fundraise?

It doesn’t stop there:

One thing is sure: The time to exit is not when you’re running out of money.

Unicorn or not, the most likely exit is an acquisition.

As George Patterson, managing director at HSBC in New York said, “Good tech companies are bought, not sold. The question is thus: how to get bought?”

Patterson says it’s important to understand how mergers and acquisitions actually work; how to prepare a startup for an exit; and how to develop a “feel” for the market you’re exiting through and into.

Hearing from corp dev veterans from Cisco, Logitech, Dassault and IBM, a few key ideas emerged:

Motivations vary

It could be from least to most expensive, or as a mix, as listed by Mark Suster, managing partner at Upfront Ventures:

How corporates find you

Corporates find deals via the development of partnerships, investment (CVC), their business units, corp dev research, media and investor connections.

Asked about the best approach, Todd Neville, manager of Corporate Business Development and Strategy at IBM (who gave the most detailed description of the corp dev process), said, “Do something cool to one of the IBM customers. If they rave about even a POC, we’re interested.”

In other words, business development is corporate development.

Get the house in order

Buyers typically want to know three things:

For IP, they will check your contracts (staff and contractors), and run some automated code analysis for proprietary code and open source use. They will evaluate potential IP infringement. No point buying you if you end up costing more in lawsuits!

For your team skills: Sitting down with your engineers will tell them plenty enough without understanding the details of this or that algorithm. The last thing a corporate wants is to be accused of stealing!

Lawyers engaged early can help. The later the clean-up, the more costly and painful.

Develop a feel for your “market”

Develop relationships and create champions within corporates. It will help promote your deal when the time comes, and will let you keep your finger on the pulse of corporate strategy to time your moves.

Do you read the earning calls of Cisco or IBM (or others relevant to you)? This is where strategies are presented. Are your keywords coming up there or in their press releases?

Chris Gilbert, former CEO of Ubiquisys (sold to Cisco for more than $300 million) was very deliberate in planning his exit.

“Selling starts on day one and is a leadership-only function — work out who will be your buyer. Only the CEO can do this. Constantly articulate why a company should buy you,” Gilbert said. Bring clear messages into the acquiring company so it can be presented upwards: give them the presentation you would like them to show their boss! When the time is right, force decisions through competition. If you know they have to buy you, your starting position is strong.”

The dark art of price discovery

There are dozens of formulas (from DCF to comparables) to evaluate a deal — which also means none is “correct.” What matters is: How much would you sell for, and how much is the buyer ready to pay?

Gilbert, at Ubiquisys, described how close interactions with his banker helped drive the price up among the bidders assembled.

Just like buyers, we meet bankers and lawyers too rarely at startup events, but there is much to learn with them. They make deals happen, avoid value erosion and optimize price. They often also make introductions before you engage them, to build goodwill and earn your business.

And if you worry about fees, the right banker handsomely pays for itself by finding more bidders and playing “bad cop” for you, avoiding direct confrontation with your future employer. Do you want a slice of the watermelon or the whole grape?

When asked about what happens after an M&A or IPO, buyers said they generally hoped the founders would stay with them for many years. Often using re-vesting, earn-outs or shares of the acquiring company to incentivize them. Neville, from IBM, mentioned a security company they acquired whose founder is now the head of one of the largest IBM divisions.

In the case of IPOs, supposedly the ultimate “exit,” any block of shares sold by founders would face extreme scrutiny and might cause a price drop.

So who’s exiting during those deals? Investors (and not always).

Eventually, if the average age of a startup at exit is 8-10 years, the active duty period of founders (if not replaced in the meantime) extends even more. Better love the problem you’re solving, and your customers!

Thanks to speakers, participants and supporters of this Master Class series:

London: Frederic Rombaut (Seraphim Capital), Joe Tabberer (FirstBank), Chris Gilbert (Ubiquisys), Jonathan Keeling (Crowdcube), Fred Destin, Tony Fish (AMF Ventures, James Clark (London Stock Exchange), Denise Law (SGCIB).

Paris: Frederic Rombaut (Seraphim Capital), Manuel Gruson (Dassault Systemes), Pierre-Henri Chappaz (Rothschild Global Advisory), Christine Lambert-Goue (All Invest), Olivier Younes (EXPEN), Eric Carreel (Withings), Fabien Bardinet (Balyo), Xavier Lazarus (Elaia Partners), Pierre-Eric Leibovici(Daphni). Jean de La Rochebrochard (Kima Ventures), Jeremy Sartre (SmartAngels), Gwen Regina Tan (Entrepreneur First).

San Francisco: Natasha Ligai (Logitech), Matt Cutler (Cisco),Will Hawthorne, (CODE Advisors), Ryan Rzepecki (JUMP Bikes), Charles Huang (Guitar Hero), Jeff Thomas (Nasdaq), Shahin Farshchi (Lux Capital), Ammar Hanafi (Moment Ventures), Adam J. Epstein (Third Creek Advisors), Nathan Harding (EKSO Bionics), Kate Whitcomb, Anthony Marino and Ethan Haigh (SOSV).

New York: Todd Neville (IBM), George Patterson (HSBC), Ryan Rzepecki (JUMP Bikes), Aaron Kellner (SeedInvest), Jeremy Levine (Bessemer Venture Partners), Taylor Greene (Collaborative Fund), Adam Rothenberg (BoxGroup), Eli Curi (Fenwick & West), Ian Engstrand and Salil Gandhi (Goodwin), Warren Spar(Sparring Partners Capital), Duncan Turner, Vivian Law and Sheng Ge (SOSV).

Powered by WPeMatico

It’s been hard to miss the scooter startup wars opening fresh, techno-fueled rifts in Valley society in recent months. Another flavor of ride-sharing steed which sprouted seemingly overnight to clutter up sidewalks — drawing rapid-fire ire from city regulators apparently far more forgiving of traffic congestion if it’s delivered in the traditional, car-shaped capsule.

Even in their best, most-groomed PR shots, the dockless carelessness of these slimline electrified scooters hums with an air of insouciance and privilege. As if to say: Why yes, we turned a kids’ toy into a battery-powered kidult transporter — what u gonna do about it?

An earlier batch of electric scooter sharing startups — offering full-fat, on-road mopeds that most definitely do need a license to ride (and, unless you’re crazy, a helmet for your head) — just can’t compete with that. Last mile does not haul.

But a short-walk replacement tool that’s so seamlessly manhandled is also of course easily vandalized. Or misappropriated. Or both. And there have been a plethora of scooter dismemberment/kidnap horror stories coming out of California, judging by reports from the scooter wars front line. Hanging scooters in trees is presumably a protest thing.

Scooter brand Lime struck an especially tone-deaf tech note trying to fix this problem after an update added a security alarm that bellowed robotic threats to call the cops on anyone who fumbled to unlock them. Safe to say, littering abusive scooters in public spaces isn’t a way to win friends and influence people.

Even when functioning ‘correctly’, i.e. as intended, scooter rides can ooze a kind of brash entitlement. The sweatless convenience looks like it might be mostly enabling another advance in tech-fueled douche behavior as a t-shirt wearing alpha nerd zips past barking into AirPods and inhaling a takeaway latte while cutting up the patience of pedestrians.

None of this fast-seeded societal friction has put the brakes on e-scooter startup momentum, though. Au contraire. They’ve been raising massive amounts of investment on rapidly inflating valuations ($2BN is the latest valuation for Bird).

But buying lots of e-scooters and leaving them at the mercy of human whim is an expensive business to try scaling. Hence big funding rounds are necessary if you’re going to replace all the canal-dunked duds and keep scooting fast enough for the competition.

At the same time, there isn’t a great deal to differentiate one e-scooter experience over another — beyond price and proximity. Branding might do it but then you have to scramble even harder and faster to create a slick experience and inflate a brand that sticks. (And it goes without saying that a scooter sticky with fecal-matter is absolutely not that.)

The still fledgling startups are certainly scrambling to scale, with some also already pushing into international markets. Lime just scattered ~200 e-scooters in Paris, for example. It’s also been testing the waters more quietly in Zurich. While Bird has its beady eye on European territory too.

The idea underpinning some very obese valuations for these fledgling startups is that scooters will be a key piece of a reworked, multi-modal transport mix for urban mobility, fueled by app-based convenience and city buy-in to greener transport options with emissions-free benefits. (Albeit scooters’ greenness depends on what they’re displacing; Great if it’s gas-guzzling cars, less compelling if it’s people walking or peddling.)

And while investors are buying in to the vision that lots of city dwellers are going to be scooting the last mile in future, and betting big on sizable value being captured by a few plucky scooter startups — more than half a billion dollars has been funneled into just two of these slimline scooter brands, Bird and Lime, since February — there are skeptical notes being sounded too.

Asking whether the scooter model really justifies such huge raises and heady valuations. Wondering if it isn’t a bit crazy for a fledgling Bird to be 2x a unicorn already.

Shared bike and scooter fleets are paving the way to a revolution in urban mobility but will only capture little value in the long term. Investors are highly overestimating the virtue of these businesses.

— Thibaud Elziere (@tiboel) June 18, 2018

The bear case for these slimline e-scooters says they’re really only fixing a pretty limited urban mobility problem. Too spindly and unsafe to go the distance, too sedate of pace (and challenged for sidewalk space) to feel worthwhile if you don’t have far to go anyway. And of course you’re not going to be able to cart your kids and/or much baggage on a stand-up two wheeler. So they’re useless for families.

Meanwhile scooter invasions are illegal in some places and, where they are possible, are fast inviting public and regulatory frisson and friction — by contributing to congestion and peril on already crowded pavements.

After taking one of Lime’s just-landed e-scooters for a spin in Paris this week, Willy Braun, VC at early stage European fund Daphni, came away unimpressed. “I didn’t feel I was really saving time in a short distance, since there is always many people in our narrow sidewalks,” he tells us. “And it isn’t comfortable enough for me to imagine a longer distance. Also it’s quite expensive ($1 per use and $.15/min).

“Lastly: Before renting it I read two news media that told me I had to use it only on the sidewalks and they tell us that we should only use it on the road during the onboarding — and that wearing an helmet is mandatory without providing it). As a comparison, I’d rather use e-bikes (or emoto-bikes) for longer journey without hesitation.”

“Give us Jump instead of Lime!” he adds, namechecking the electric bike startup that’s been lodged under Uber’s umbrella since April, adding a greener string to its urban mobility bow — and which is also heading over to Europe as part of the ride-hailing giant’s ongoing efforts to revitalize its regionally battered brand.

“Uber stands ready to help address some of the biggest challenges facing German cities: tackling air pollution, reducing congestion and increasing access to cleaner transportation solutions,” said CEO Dara Khosrowshahi wheeling a bright red Jump bike on stage at the Noah conference in Berlin earlier this month. Uber’s Jump e-bikes will launch in Germany this summer.

E-bikes do seem to offer more urban mobility versatility than e-scooters. Though a scooter is arguably a more accessible type of wheeled steed vs a bike, given you can just stand on it and be moved.

But in Europe’s dense and dynamic urban environments — which, unlike the US, tend to be replete with public transit options (typically at a spectrum of price-points) — individual transport choices tend to be based firstly on economics. After which it’s essentially a matter of personal taste and/or the weather.

Urban transport horses for courses — depending on your risk, convenience and comfort thresholds, thanks to a publicly funded luxury of choice. So scooters have loads of already embedded competition.

TechCrunch’s resident Parisienne, Romain Dillet — a regular user of on-demand bike services in the city (of which there are many), and prior to that the city’s own dock-based bike rental scheme — also went for a test spin on a Lime scooter this week. And also came away feeling underwhelmed.

“This is bad,” he said after his ride. “It’s slow and you need to brake constantly. BUT the worst part is that it feels waaaaaay more dangerous than a bike. Basically you can’t brake abruptly because you’re just standing there.”

Index Venture’s Martin Mignot was also in Paris this week and he took the chance to take a Lime scooter for a spin too — checking out the competition in his case, given the European VC firm is a Bird backer. So what did he think?

“The experience is pretty cool. It’s slightly faster than a bike, there’s no sweating. The weather was just amazing and very hot in Paris so it was pretty amazing in terms of speed and lack of effort,” he says, rolling out the positively spun, vested view on scooter sharing. “Especially going up hill to go to Gare du Nord.

“And the lack of friction — just to get on board and get started. So in general I think it’s a great experience and I think it feels a really interesting niche between walking and on-demand bikes… In Paris you’ve also got the mopeds. So that kind of ‘in between offering’. I think there’s a big market there. I think it’s going to work pretty well in Paris.”

Mignot is a tad disparaging about the quality of Lime’s scooters vs the model being deployed by Bird — a scooter model he also personally owns. But again, as you’d expect given his vested interests.

“Obviously I’m biased but I would say that the Xiaomi scooter/Ninebot scooter is higher quality than the one that Lime are using,” he tells us. “I thought that the Lime one, the handlebar is a little bit too high. The braking is a little bit too soft. Maybe it was the one I used, I don’t know.”

Talking generally about scooter startups, he says investors’ excitement boils down to trip frequency — thanks exactly to journeys being these itty-bitty last mile links.

But it’s also then about the potential for all that last mile hopping to be a shortcut for winning a prized slot on smartphone users’ homescreens — and thus the underlying game being played looks like a jockeying for prime position in the urban mobility race.

Lime, for example, started out with bike rentals before jumping into scooters and going multi-modal. So scooter sharing starts to look like a strategy for mobility startups to scoot to the top of the attention foodchain — where they’re then positioned to offer a full mix and capture more value.

So really scooters might mostly be a tool for catching people’s app attention. Think of that next time you see one lying on a sidewalk.

“What’s very interesting if you look at the trip distribution, most of the trips are short. So the vast majority of trips if you’re walking, obviously, are less than three miles. So that’s actually where the bulk of the mobility happens. And scooters play really well in that field. So in terms of sheer number of trips I think it’s going to dwarf any other type of transportation. And especially ride-hailing,” says Mignot.

“If you look at how often do people use Uber or Lyft or Taxify… it’s going to be much less frequent than the scooter users. And I think that’s what makes it such an interesting asset… The frequency will be much higher — and so the apps that power the scooters will tend to be on the homescreen. And kind of on top of the foodchain, so to speak. So I think that’s what makes it super interesting.”

Scooters also get a big investor tick on merit of the lack of friction standing in the way of riding vs other available urban options such as bikes (or, well, non-electric scooters, skateboards, roller blades, public transport, and so on and on) — in both onboarding (getting going) and propulsion (i.e. the lack of sweat required to ride) terms.

“That’s what’s so brilliant with these devices, you just snap the QR code and off you go,” he says. “The difference with bikes is that you don’t have to produce any effort. I think there are cases where obviously bikes are better. But I think there are a lot of cases where people will want something where you don’t sweat.

“Where you don’t wrinkle your clothes. Which goes a little bit faster. Without going all the way to the moped experience where you need to put the helmet, which is a bit more dangerous, which a lot of people, especially women, are not super familiar with. So I think what’s exciting with scooters as a form factor is it’s actually very mainstream.

“Anyone can ride them. It’s very simple to manoeuvre. It’s not super fast, it’s not too dangerous. It doesn’t require any muscular effort — so for older people or for people who just don’t want to sweat because they’re going to a meeting or something. It’s just a fantastic option.”

Index has also invested in an e-bike startup (Cowboy) and the firm is fully signed up to the notion that urban mobility will be multimodal. So if e-scooters valuations are a bit overcooked Index is not going to be too concerned. People in cities are clearly going to be riding something. And backing a mix is a smart way to hedge the risk of any one option ending up more passing fad than staple urban steed.

Mostly Index is betting that people will keep on riding robotic horses for urban courses. And whatever they ride it’s a fairly safe bet that an app is going to be involved in the process of finding (docklessness is therefore another attention play) or unlocking (scan that QR code!) the mobility device — opening up the possibility that a single app could house multiple mobility options and thus capture more overall value.

“It’s not a one-size fits all. They’re all complementing each other,” says Mignot of the urban mobility options in play. “I would say e-bikes are probably a little bit more great for little bit longer trips because you’re sitting down. But again it takes a little bit longer, because you have to adjust the saddle, you need to start peddling. There’s a bit more friction both on the onboading and on the riding. But they’re a bit better for slightly longer distances. I would say for shorter distances there’s nothing better than the scooter.”

He also points out that scooters are both cheaper and less bulky than e-bikes. And because they take up less street space they can — at least in theory — be more densely stacked, thereby generating the claimed convenience by having them sitting near enough to convince someone not to bother walking 10 minutes to the café or gym — and just scoot instead. So scooters’ slimline physique is also especially exciting to investors. (Even if, ironically, it’s being deployed to urge people to walk less.)

“I think we will end up with more density of scooters. Which is super important,” he continues. “People will, in the end, tend to take the vehicle that they can find where they are. And I think it’s more likely, eventually, that they will get a scooter than an e-bike. Just simply because they take less space and they are less expensive.”

But why wouldn’t people who do get won over to the sweatless perks of last mile scooting just buy and own their own ride — rather than shelling out on an ongoing basis to share?

Unlike bikes, scooters are mobile enough to be picked up and moved around fairly easily. Which means they can go with you into your home, office, even a restaurant — disruptively reducing theft risk. Whereas talk to any bike owner and they’ll almost invariably have at least one tale of theft woe, which is a key part of what makes bike sharing so attractive: It erases theft worry.

Add to that, you can find e-scooters on sale in European electronics shops for as little as €140. So if you’re going to be a regular scooterer, the purely economic argument to just own your own looks pretty compelling.

And people zipping around on e-scooters is a pretty common sight in another dense European city, Barcelona, which has very scooter-friendly weather but no scooter startups (yet). But unless it’s a tourist weaving along the seafront most of these riders are not shared: People just popped into their local electronics shop and walked out with a scooter in a box.

So the rides aren’t generating repeat revenue for anyone except the electricity companies.

Asked why people who do want to scoot won’t just buy, rather than rent Mignot talks up the hassle of ownership — undermined slightly by the fact he is also a scooter owner (despite the claimed faff from problems such as frequent flat tires and the chore of the nightly charge).

“The thing you notice very rapidly: There are two things, one is the maintenance,” he says. “The models that exist today are not super robust. Maybe in a very flat, very smooth roads, maybe Santa Monica, maybe it’s a little bit less true but I would say in Europe the maintenance that is required is fairly high… I have to do something on mine every week.

“The other thing is it takes a little bit of space. If you have to bring it to a restaurant or whatever type of crowded place, a movie theatre or wherever you’re going, to an office, to a meeting room, it’s a little bit on the heavy side, and it’s a little bit inconvenient. So certainly some people will buy them… But I also think that there are a lot of cases where you’d rather have it just on-demand.”

Unlike Mignot and Index, Tom Bradley, of UK focused VC firm Oxford Capital, is not so convinced by the on-demand scooter craze.

The firm has not made any e-scooter investments itself, though mobility is a “core theme”, with the portfolio including an on-demand coach travel startup (Sn-ap), and technology plays such as Morpheus Labs (machine learning for driverless cars) and UltraSoc (complex circuits for automotive parts, which sells to the likes of Tesla).

But it’s just not been sold on scooter startups. Bradley describes it as an “open question” whether scooters end up being “an important part of how people move around the cities of the future”. He also points to theft problems with dockless bike share schemes that have not played out well in the UK.

“We’re not convinced that this is a fundamental part of the picture,” he says of scooter sharing. “It may be a part of the picture but I personally am not yet convinced that it’s as big a part of the picture that people seem to be prepared to pay for.”

“I keep thinking of the Segway example,” he adds. “It’s an absolutely delightful product. It’s brilliant. It’s absolutely brilliant. In a way that these electric scooters are not. But obviously it was much more expensive. And it made people feel a bit weird. But it was supposed to be the answer — and it’s not the answer. Before its time, perhaps.”

Of course he also accepts that capital is “being used as a weapon”, as he puts it, to scoot full-pelt towards a future where shared electric scooters are the norm on city streets by waging a “marketing war” to get there.

“Venture capital valuations are what someone is prepared to pay. And in this case people are valuing potential rather than valuing the business… so the valuations [of Bird and Lime] are being driven more than anything by the amount of money being raised,” he says. “So you decide a rule of thumb about what is acceptable dilution, and if you’re going to raise $400M or whatever then the valuation’s got to be somewhere between $1.6BN and $2BN to make that sort of raise make sense — and leave enough equity for the previous investors and founders. So there’s an element of this where the valuations are being driven by the amount of capital being raised.”

Oxford Capital’s bearish view on scooter sharing is also bounded by the fund only investing in UK-based startups. And while Bradley says it sees lots of local mobility strengths — especially in the automotive market — he admits it’s more of a mental leap to imagine a world leading scooter startup sprouting from the country’s green and pleasant lands. Not least because it’s not legal to use them on UK public roads or pavements.

“If you look at places like Amsterdam, Berlin, they’re sort of built for bikes. London’s getting towards being built for bikes… Cycling’s been one of the big success stories in London. Is [scooter sharing] going to replace cycling? I don’t know. Not so convinced… It’s obviously easy for anyone to get on and off these things, young and old. So that’s good, it’s inclusive. But it feels a little bit like a solution looking for a problem, the sorts of journeys people talk about for these things — on campus, short urban journeys. A lot of these are walkable or cycle journeys in a lot of cities. So is there a mass need?

“Is this Segway 2 or is this bike hire 2… it’s hard to tell. And we’re coming down on the former. We’re not convinced this is going to be a fundamental part of the transport space. It will be a feature but not a huge part.”

But for Mignot the early days of the urban mobility attention wars mean there’s much to play for — and much that can be favorably reshaped to fit scooters into the mix.

“The whole thing, even on-demand bikes, it’s a two year old phenomenon really,” he says. “So I think everyone is just trying to learn and figure out and adapt to this new reality, whether it’s users or companies or cities. I think it’s very similar to when cars were first introduced. There were no parking spaces at the time and there were no rules on the road. And fast forward 100 years and it looks very different.

“If you look at the amount of infrastructure and effort and spend that has been put into making — and I would argue way more than should have — into making a city car-friendly, if you only do a 100th of the same amount of effort and spend into making some space for bicycles and light two-wheel vehicles I think we’ll be fine.

“That’s the beauty of this model. If you compare the space of the tech and if you look at the efficiency of moving people around vs the space, the scooters are simply the most efficient because their footprint on the ground is just so small.”

He even makes the case for scooters working well in London — arguing the sprawl of the city amps up the utility because there are so many tedious last mile trips that people have to make.

Even more so than in denser European cities like Paris, where he admits that hopping on a scooter might just be more of a “nice to have”, given shorter distances and all the other available options. So, really, where urban mobility is concerned, it can actually be courses for horses.

Yet, the reality is London is off-limits to the likes of Bird and Lime for now — thanks to UK laws barring this type of unlicensed personal electric vehicle from public roads and spaces.

You can buy e-scooters for use on private land in the UK but any scooter startups that tried their usual playbook in London would be scooting straight for legal hot water.

It’s not just the British weather that’s inclement.

“I’m really hoping that TfL [Transport for London] and the Department for Transport are going to make it possible,” says Mignot on that. “I think any city should welcome this with open arms. Some cities are, by the way. And I think over time once they see the success stories in other parts of the world I think they all will. But I wish London was one of those cutting edge cities that would welcome new innovation with open arms. I think right now, unfortunately, it’s not there.

“There’s a lot of talk about air quality, and so on, but actually, when push comes to shove… you have a lot of resistance and a lot of pushback… So it’s a little bit disappointing. But, you know, we’ll get there eventually.”

Powered by WPeMatico