paga

Auto Added by WPeMatico

Auto Added by WPeMatico

In African fintech, the fourth quarter of 2019 brought big money to new entrants.

Chinese investors put $220 million into OPay and PalmPay — two fledgling startups with plans to scale in Nigeria and the broader continent. Several sources told me the big bucks had created anxiety for more than few payments ventures in Nigeria with similar strategies and smaller coffers. They may not need to fret just yet, however: lessons from Africa’s most successful mobile-money case study, M-Pesa, suggest that VC alone won’t buy scale in digital finance.

Over the last decade, Africa has been in the midst of a startup boom accompanied by big growth in VC and improvements in internet and mobile penetration.

Some definitive country centers for company formation, tech hubs and investment have emerged; Nigeria, South Africa and Kenya lead the continent in numbers for all those categories. Additional strong and emerging points for innovation and startups across Africa’s 54 countries and 1.2 billion people include Ghana, Tanzania, Ethiopia, and Senegal.

The continent surpassed $1 billion in VC to startups in 2018 and per research done by Partech and WeeTracker, fintech is the focus of the bulk of capital and deal-flow.

By several estimates, Africa is home to the largest share of the world’s unbanked and underbanked population.

This runs parallel to the region’s off-the-grid SME’s and economic activity — on display and in commercial motion through the street traders, roadside kiosks and open-air markets common from Nairobi to Lagos.

IMF estimates have pegged Africa’s informal economy as one of the largest in the world. Thousands of fintech startups have descended onto this large pool of unbanked and underbranked citizens and SMEs looking to grow digital finance products and market share.

In this race, the West African nation of Nigeria — home to Africa’s largest economy and population — is becoming an epicenter for VC. Many fintech-related companies are adopting a strategy of scaling there first before expanding outward.

That includes new entrants OPay and PalmPay, which raised so much capital in fourth quarter 2019. It’s notable that both were founded in 2019 and largely incubated by Chinese actors.

PalmPay, a consumer-oriented payments product, went live in November with a $40 million seed-round (one of the largest in Africa in 2019) led by Africa’s biggest mobile-phones seller — China’s Transsion. The startup was upfront about its ambitions, stating its goals to become “Africa’s largest financial services platform,” in a company statement.

![]() To that end, PalmPay conveniently entered a strategic partnership with its lead investor. The startup’s payment app will come pre-installed on Transsion’s mobile device brands, such as Tecno, in Africa — for an estimated reach of 20 million phones in 2020.

To that end, PalmPay conveniently entered a strategic partnership with its lead investor. The startup’s payment app will come pre-installed on Transsion’s mobile device brands, such as Tecno, in Africa — for an estimated reach of 20 million phones in 2020.

PalmPay also launched in Ghana in November and its U.K. and Africa-based CEO, Greg Reeve, confirmed plans to expand to additional African countries in 2020.

If PalmPay’s $40 million seed round got founders’ attention, OPay’s $120 million Series B created shock-waves, coming just months after the mobile-based fintech venture raised $50 million — making OPay’s $170 million capital haul equivalent to roughly a fifth of all VC raised in Africa in 2018.

Founded by Chinese owned consumer internet company Opera — and backed by 9 Chinese investors — OPay is the payment utility for a suite of Opera -developed internet based commercial products in Nigeria that include ride-hail apps ORide and OCar and food delivery service OFood.

With its latest Series A, OPay announced it would expand in Kenya, South Africa, and Ghana.

In Nigeria, OPay’s $170 million Series A and B announced in the span of months dwarfs just about anything raised by new and existing fintech players, with the exception of Interswitch.

The homegrown payments processing company — which pioneered much of Nigeria’s digital finance infrastructure — reached unicorn status in November when Visa took a reported $200 million minority stake in the venture.

A sampling of more common funding amounts for payments ventures in Nigeria includes established fintech company Paga’s $10 million Series B. Recent market entrant Chipper Cash’s May 2019 seed-round was $2.4 million.

There is a large disparity between fintech startups in Nigeria with capital raises in ones and tens of millions vs. OPay and PalmPay’s $40 and $120 million rounds. Conventional wisdom could be that the big-capital, big spending firms have an unmistakable advantage in scaling digital payments in Nigeria and other markets.

A look at Kenya’s M-Pesa may prove otherwise.

Powered by WPeMatico

November 2019 could mark when Nigeria (arguably) became Africa’s unofficial capital for fintech investment and digital finance startups.

The month saw $360 million invested in Nigerian-focused payment ventures. That is equivalent to roughly one-third of all the startup VC raised for the entire continent in 2018, according to Partech stats.

A notable trend-within-the-trend is that more than half — or $170 million — of the funding to Nigerian fintech ventures in November came from Chinese investors. This marks a pivot (to tech) in China’s engagement with Africa. We’ll get to that.

Before the big Chinese-backed rounds, one of Nigeria’s earliest fintech companies, Interswitch, confirmed its $1 billion valuation after Visa took a minority stake in the company. Interswitch would not disclose the amount to TechCrunch, but Sky News reporting pegged it at $200 million for 20%.

Founded in 2002 by Mitchell Elegbe, Interswitch pioneered the infrastructure to digitize Nigeria’s then predominantly paper-ledger and cash-based economy.

The company now provides much of the tech-wiring for Nigeria’s online banking system that serves Africa’s largest economy and population. Interswitch offers a number of personal and business finance products, including its Verve payment cards and Quickteller payment app.

The financial services firm has expanded its physical presence to Uganda, Gambia and Kenya . The Nigerian company also sells its products in 23 African countries and launched a partnership in August for Verve cardholders to make payments on Discover’s global network.

Visa and Interswitch touted the equity investment as a strategic collaboration between the two companies, without a lot of detail on what that will mean.

One point TechCrunch did lock down is Interswitch’s (long-awaited) and imminent IPO. A source close to the matter said the company will list on a major exchange by mid-2020.

For the near to medium-term, Interswitch could stand as Africa’s sole tech-unicorn, as e-commerce venture Jumia’s volatile share-price and declining market-cap — since an April IPO — have dropped the company’s valuation below $1 billion.

Circling back to China, November was the month that signaled Chinese actors are all in on African tech.

In two separate rounds, Chinese investors put $220 million into OPay and PalmPay — two fledgling startups with plans to scale in Nigeria and the broader continent.

PalmPay, a consumer-oriented payments product, went live last month with a $40 million seed round (one of the largest in Africa in 2019) led by Africa’s biggest mobile-phone seller — China’s Transsion.

The startup was upfront about its ambitions, stating in a company release its goals to become “Africa’s largest financial services platform.”

To that end, PalmPay conveniently entered a strategic partnership with its lead investor. The startup’s payment app will come pre-installed on Transsion’s mobile device brands, such as Tecno, in Africa — for an estimated reach of 20 million phones.

PalmPay also launched in Ghana in November and its U.K. and Africa-based CEO, Greg Reeve, confirmed plans to expand to additional African countries in 2020.

![]()

OPay’s $120 million Series B was announced several days after the PalmPay news and came only months after the mobile-based fintech venture raised $50 million.

Founded by Chinese-owned consumer internet company Opera — and backed by nine Chinese investors — OPay is the payment utility for a suite of Opera -developed internet-based commercial products in Nigeria. These include ride-hail apps ORide and OCar and food delivery service OFood.

With its latest Series A, OPay announced it would expand in Kenya, South Africa and Ghana.

Though it wasn’t fintech, Chinese investors also backed a (reported) $30 million Series B for East African trucking logistics company Lori Systems in November.

With OPay, PalmPay and Lori Systems, startups in Africa have raised a combined $240 million from 15 Chinese investors in a span of months.

There are a number of things to note and watch out for here, as TechCrunch reporting has illuminated (and will continue to do in follow-on coverage).

These moves mark a next chapter in China’s engagement in Africa and could raise some new issues. Hereto, the country’s interaction with Africa’s tech ecosystem has been relatively light compared to China’s deal-making on infrastructure and commodities.

There continues to be plenty of debate (and critique) of China’s role in Africa. This new digital phase will certainly add a fresh component to all that. One thing to track will be data-privacy and national-security concerns that may emerge around Chinese actors investing heavily in African mobile consumer platforms.

We’ve seen lines (allegedly) blur on these matters between Chinese state and private-sector actors with companies such as Huawei.

As OPay and PalmPay expand, they may need to do some reassuring of African regulators as countries (such as Kenya) establish more formal consumer protection protocols for digital platforms.

One more thing to follow on OPay’s funding and planned expansion is the extent to which it puts Opera (and its entire suite of consumer internet products) in competition with multiple actors in Africa’s startup ecosystem. Opera’s Africa ventures could go head to head with Uber, Jumia and M-Pesa — the mobile money-product that put Kenya out front on digital finance in Africa before Nigeria.

Shifting back to American engagement in African tech, Twitter and Square CEO Jack Dorsey was on the continent in November. No sooner than he’d finished his first trip, Dorsey announced plans to move to Africa in 2020, for three to six months, saying on Twitter, “Africa will define the future (especially the bitcoin one!).”

We still don’t know much about what this last trip — or his future foray — mean in terms of concrete partnerships, investment or market moves in Africa from Dorsey and his companies.

He visited Nigeria, Ghana, South Africa and Ethiopia and met with leaders at Nigeria’s CcHub (Bosun Tijani), Ethiopia’s Ice Addis (Markos Lemma) and did some meetings with fintech founders in Lagos (Paga’s Tayo Oviosu).

He visited Nigeria, Ghana, South Africa and Ethiopia and met with leaders at Nigeria’s CcHub (Bosun Tijani), Ethiopia’s Ice Addis (Markos Lemma) and did some meetings with fintech founders in Lagos (Paga’s Tayo Oviosu).

I know pretty well most of the organizations and people Dorsey talked to and nothing has shaken out yet in terms of partnership or investment news from his recent trip.

On what could come out of Dorsey’s 2020 move to Africa, per his tweet and news highlighted in this roundup, a good bet would be it will have something to do with fintech and Square.

More Africa-related stories @TechCrunch

African tech around the ‘net

Powered by WPeMatico

Jumia may be the first startup you’ve heard of from Africa. But the e-commerce venture that recently listed on the NYSE is definitely not the first or last word in African tech.

The continent has an expansive digital innovation scene, the components of which are intersecting rapidly across Africa’s 54 countries and 1.2 billion people.

When measured by monetary values, Africa’s tech ecosystem is tiny by Shenzen or Silicon Valley standards.

But when you look at volumes and year over year expansion in VC, startup formation, and tech hubs, it’s one of the fastest growing tech markets in the world. In 2017, the continent also saw the largest global increase in internet users—20 percent.

If you’re a VC or founder in London, Bangalore, or San Francisco, you’ll likely interact with some part of Africa’s tech landscape for the first time—or more—in the near future.

That’s why TechCrunch put together this Extra-Crunch deep-dive on Africa’s technology sector.

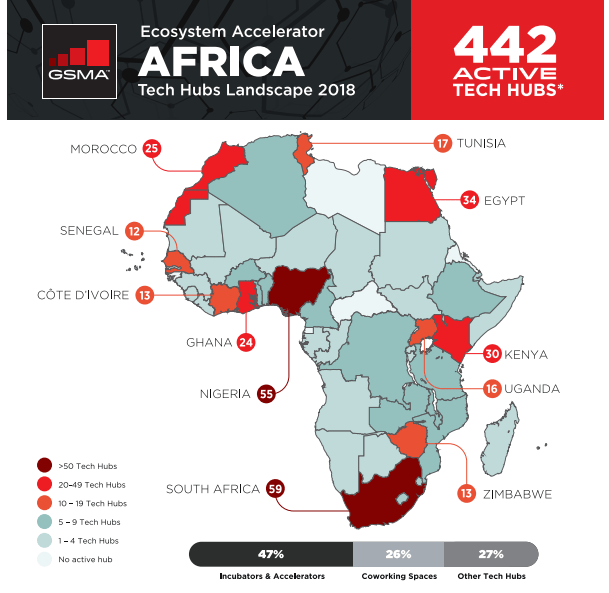

A foundation for African tech is the continent’s 442 active hubs, accelerators, and incubators (as tallied by GSMA). These spaces have become focal points for startup formation, digital skills building, events, and IT activity on the continent.

Prominent tech hubs in Africa include CcHub in Nigeria, Pan-African incubator MEST, and Kenya’s iHub, with over 200 resident members. More of these organizations are receiving funds from DFIs, such as the World Bank, and aid agencies, including France’s $76 million African tech fund.

Prominent tech hubs in Africa include CcHub in Nigeria, Pan-African incubator MEST, and Kenya’s iHub, with over 200 resident members. More of these organizations are receiving funds from DFIs, such as the World Bank, and aid agencies, including France’s $76 million African tech fund.

Blue-chip companies such as Google and Microsoft are also providing money and support. In 2018 Facebook opened its own Hub_NG in Lagos with partner CcHub, to foster startups using AI and machine learning.

Powered by WPeMatico

WorldCover, a New York and Africa-based climate insurance provider to smallholder farmers, has raised a $6 million Series A round led by MS&AD Ventures.

Y Combinator, Western Technology Investment and EchoVC also participated in the round.

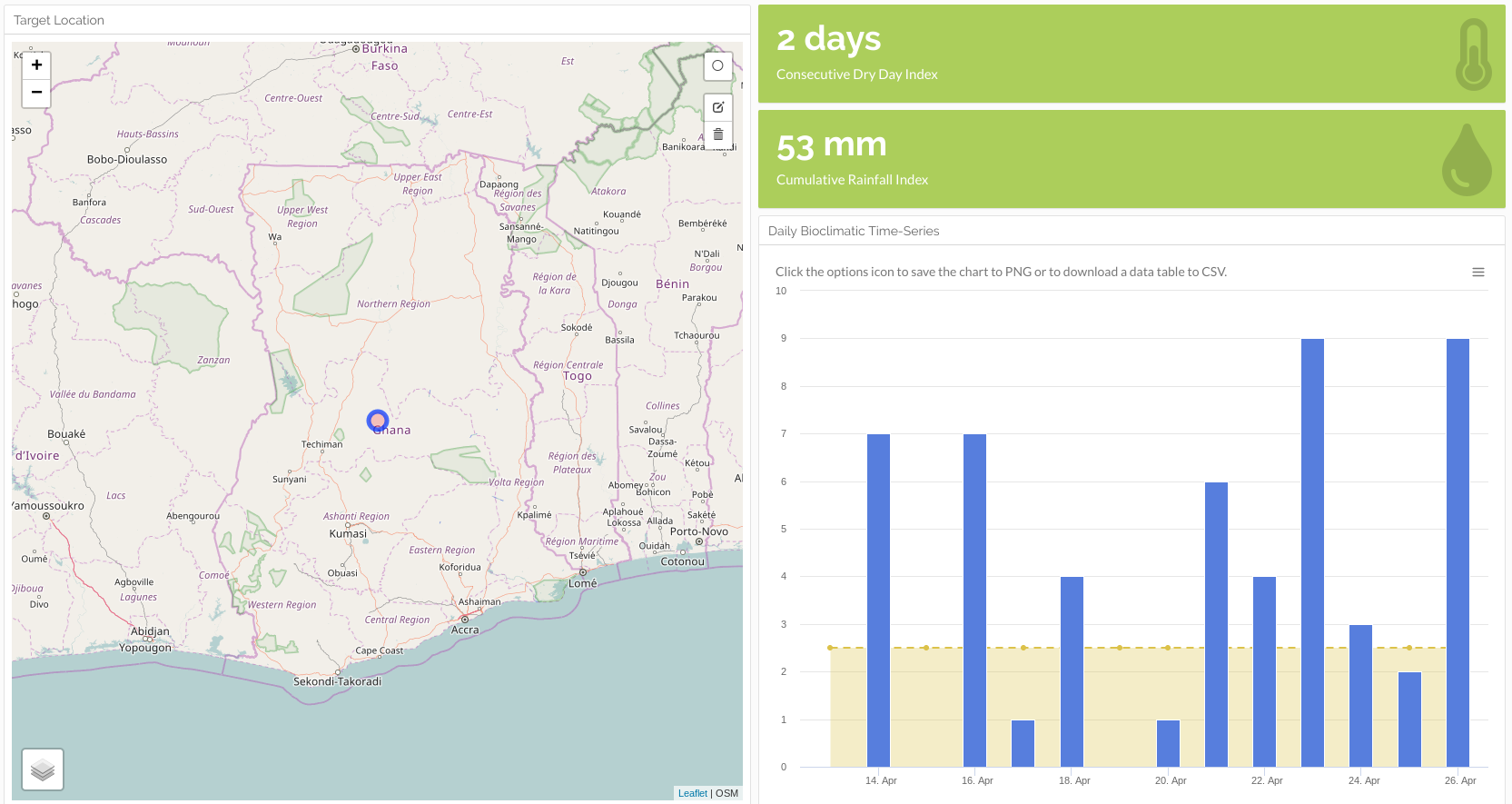

WorldCover’s platform uses satellite imagery, on-ground sensors, mobile phones and data analytics to create insurance options for farmers whose crop yields are affected adversely by weather events — primarily lack of rain.

The startup currently operates in Ghana, Uganda and Kenya . With the new funding, WorldCover aims to expand its insurance offerings to more emerging market countries.

“We’re looking at India, Mexico, Brazil, Indonesia. India could be first on an 18-month timeline for a launch,” WorldCover co-founder and chief executive Chris Sheehan said in an interview.

The company has served more than 30,000 farmers across its Africa operations. Smallholder farmers are those earning all or nearly all of their income from agriculture, farming on 10-20 acres of land and earning around $500 to $5,000, according to Sheehan.

Farmers connect to WorldCover by creating an account on its USSD mobile app. From there they can input their region and crop type and determine how much insurance they would like to buy and use mobile money to purchase a plan. WorldCover works with payments providers such as M-Pesa in Kenya and MTN Mobile Money in Ghana.

The service works on a sliding scale, where a customer can receive anywhere from 5x to 15x the amount of premium they have paid. If there is an adverse weather event, namely lack of rain, the farmer can file a claim via mobile phone. WorldCover then uses its data-analytics metrics to assess it, and, if approved, the farmer will receive an insurance payment via mobile money.

Common crops farmed by WorldCover clients include maize, rice and peanuts. It looks to add coffee, cocoa and cashews to its coverage list.

For the moment, WorldCover only insures for events such as rainfall risk, but in the future it will look to include other weather events, such as tropical storms, in its insurance programs and platform data analytics.

For the moment, WorldCover only insures for events such as rainfall risk, but in the future it will look to include other weather events, such as tropical storms, in its insurance programs and platform data analytics.

The startup’s founder clarified that WorldCover’s model does not assess or provide insurance payouts specifically for climate change, though it does directly connect to the company’s business.

“We insure for adverse weather events that we believe climate change factors are exacerbating,” Sheehan explained. WorldCover also resells the risk of its policyholders to global reinsurers, such as Swiss Re and Nephila.

On the potential market size for WorldCover’s business, he highlights a 2018 Lloyd’s study that identified $163 billion of assets at risk, including agriculture, in emerging markets from negative, climate change-related events.

“That’s what WorldCover wants to go after…These are the kind of micro-systemic risks we think we can model and then create a micro product for a smallholder farmer that they can understand and will give them protection,” he said.

With the round, the startup will look to possibilities to update its platform to offer farming advice to smallholder farmers, in addition to insurance coverage.

WorldCover investor and EchoVC founder Eghosa Omoigui believes the startup’s insurance offerings can actually help farmers improve yield. “Weather-risk drives a lot of decisions with these farmers on what to plant, when to plant, and how much to plant,” he said. “With the crop insurance option, the farmer says, ‘Instead of one hector, I can now plant two or three, because I’m covered.’ ”

Insurance technology is another sector in Africa’s tech landscape filling up with venture-backed startups. Other insurance startups focusing on agriculture include Accion Venture Lab-backed Pula and South Africa based Mobbisurance.

With its new round and plans for global expansion, WorldCover joins a growing list of startups that have developed business models in Africa before raising rounds toward entering new markets abroad.

In 2018, Nigerian payment startup Paga announced plans to move into Asia and Latin America after raising $10 million. In 2019, South African tech-transit startup FlexClub partnered with Uber Mexico after a seed raise. And Lagos-based fintech startup TeamAPT announced in Q1 it was looking to expand globally after a $5 million Series A round.

Powered by WPeMatico

The San Francisco-based startup Branch International, which makes small personal loans in emerging markets, has raised $170 million and announced a partnership with Visa to offer virtual, pre-paid debit cards to Branch client networks in Africa, South-Asia and Latin America.

Branch — which has 150 employees in San Francisco, Lagos, Nairobi, Mexico City and Mumbai — makes loans starting at $2 to individuals in emerging and frontier markets. The company also uses an algorithmic model to determine credit worthiness, build credit profiles and offer liquidity via mobile phones.

“We’ll use [the money] to deepen existing business in Africa. Later this year we’ll announce high-yield savings accounts…in Africa,” says Branch co-founder and chief executive Matt Flannery.

The $170 million round from Foundation Capital and its new debit card partner, Visa, will support Branch’s international expansion, which could include Brazil and Indonesia, according to Flannery. Branch launched in Mexico and India within the last year. In Africa, it offers its services in Kenya, Nigeria and Tanzania.

A potential Branch customer

The Branch-Visa partnership will allow individuals to obtain virtual Visa accounts with which to create accounts on Branch’s app. This gives Branch larger reach in countries such as Nigeria — Africa’s most populous country with 190 million people — where cards have factored more prominently than mobile money in connecting unbanked and underbanked populations to finance.

Founded in 2015, Branch started operating in Kenya, where mobile money payment products such as Safaricom’s M-Pesa (which does not require a card or bank account to use) have scaled significantly. M-Pesa now has 25 million users, according to sector stats released by the Communications Authority of Kenya. Branch has more than 3 million customers and has processed 13 million loans and disbursed more than $350 million, according to company stats.

Branch has one of the most downloaded fintech apps in Africa, per Google Play app numbers combined for Nigeria and Kenya, according to Flannery.

Already profitable, Branch International expects to reach $100 million in revenues this year, with roughly 70 percent of that generated in Africa, according to Flannery.

In addition to Visa and Foundation Capital, the $170 Series C round included participation from Branch’s existing investors Andreessen Horowitz, Trinity Ventures, Formation 8, the IFC, CreditEase and Victory Park, while adding new investors Greenspring, Foxhaven and B Capital.

Branch last raised $70 million in 2018. The company’s overall VC haul and $100 million revenue peg register as pretty big numbers for a startup focused primarily on Africa. Pan-African e-commerce startup Jumia, which also announced its NYSE IPO last month, generated $140 million in revenue (without profitability) in 2018.

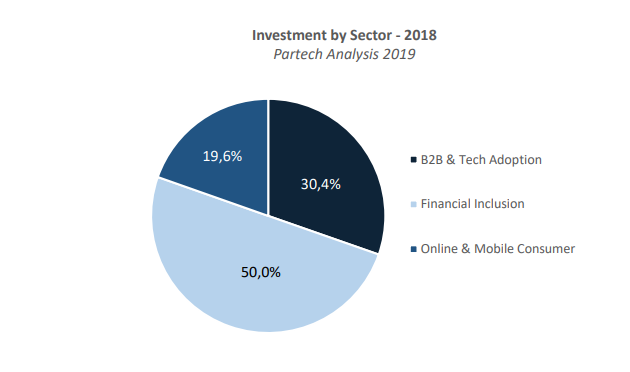

Startups building financial technologies for Africa’s 1.2 billion population have gained the attention of investors. As a sector, fintech (or financial inclusion) attracted 50 percent of the estimated $1.1 billion funding to African startups in 2018, according to Partech.

Startups building financial technologies for Africa’s 1.2 billion population have gained the attention of investors. As a sector, fintech (or financial inclusion) attracted 50 percent of the estimated $1.1 billion funding to African startups in 2018, according to Partech.

Branch’s recent round and plans to add countries internationally also tracks a trend of fintech-related products growing in Africa, then expanding outward. This includes M-Pesa, which generated big numbers in Kenya before operating in 10 countries around the world. Nigerian payments startup Paga announced its pending expansion in Asia and Mexico late last year. And payment services such as Kenya’s SimbaPay have also connected to global networks like China’s WeChat.

Powered by WPeMatico