Opinion

Auto Added by WPeMatico

Auto Added by WPeMatico

The speed at which gaming has proliferated is matched only by the pace of new buzzwords inundating the ecosystem. Marketers and decision-makers, already suffering from FOMO about opportunities within gaming, have latched onto buzzy trends like the applications of blockchain in gaming and the “metaverse” in an effort to get ahead of the trend rather than constantly play catch-up.

The allure is obvious, as the relationship between the blockchain, metaverse and gaming makes sense. Gaming has always been on the forefront of digital ownership (one can credit gaming platform Steam for normalizing the concept for games, and arguably other media such as movies), and most agreed upon visions of the metaverse rely upon virtual environments common in games with decentralized digital ownership.

Whatever your opinion of either, I believe they both have an interrelated future in gaming. However, the success or relevance of either of these buzzy topics is dependent upon a crucial step that is being skipped at this point.

Let’s start with the example of blockchain and, more specifically, NFTs. Collecting items of varying rarities and often random distribution form some of the core “loops” in many games (e.g., kill monster, get better weapon, kill tougher monster, get even better weapon, etc.), and collecting “skins” (i.e., different outfits/permutation of game character) is one of the most embraced paradigms of microtransactions in games.

The way NFTs are currently being discussed in relation to gaming are very much in danger of falling into this very trap: Killing the core gameplay loop via a financial fast track.

Now, NFTs are positioned to be a natural fit with various rare items having permanent, trackable and open value. Recent releases such as “Loot (for Adventurers)” have introduced a novel approach wherein the NFTs are simply descriptions of fantasy-inspired gear and offered in a way that other creators can use them as tools to build worlds around. It’s not hard to imagine a game built around NFT items, à la Loot.

But that’s been done before … kind of. Developers of games with a “loot loop” like the one described above have long had a problem with “farmers,” who acquire game currencies and items to sell to players for real money, against the terms of service of the game. The solution was to implement in-game “auction houses” where players could instead use real money to purchase items from one another.

Unfortunately, this had an unwanted side effect. As noted by renowned game psychologist Jamie Madigan, our brains are evolved to pay special attention to rewards that are both unexpected and beneficial. When much of the joy in some games comes from an unexpected or randomized reward, being able to easily acquire a known reward with real money robbed the game of what made it fun.

The way NFTs are currently being discussed in relation to gaming are very much in danger of falling into this very trap: Killing the core gameplay loop via a financial fast track. The most extreme examples of this phenomena commit the biggest cardinal sin in gaming — a game that is “pay to win,” where a player with a big bankroll can acquire a material advantage in a competitive game.

Blockchain games such as Axie Infinity have rapidly increased enthusiasm around the concept of “play to earn,” where players can potentially earn money by selling tokenized resources or characters earned within a blockchain game environment. If this sounds like a scenario that can come dangerously close to “pay to win,” that’s because it is.

What is less clear is whether it matters in this context. Does anyone care enough about the core game itself rather than the potential market value of NFTs or earning potential through playing? More fundamentally, if real-world earnings are the point, is it truly a game or just a gamified micro-economy, where “farming” as described above is not an illicit activity, but rather the core game mechanic?

The technology culture around blockchain has elevated solving for very hard problems that very few people care about. The solution (like many problems in tech) involves reevaluation from a more humanist approach. In the case of gaming, there are some fundamental gameplay and game psychology issues to be tackled before these technologies can gain mainstream traction.

We can turn to the metaverse for a related example. Even if you aren’t particularly interested in gaming, you’ve almost certainly heard of the concept after Mark Zuckerberg staked the future of Facebook upon it. For all the excitement, the fundamental issue is that it simply doesn’t exist, and the closest analogs are massive digital game spaces (such as Fortnite) or sandboxes (such as Roblox). Yet, many brands and marketers who haven’t really done the work to understand gaming are trying to fast-track to an opportunity that isn’t likely to materialize for a long time.

Gaming can be seen as the training wheels for the metaverse — the ways we communicate within, navigate and think about virtual spaces are all based upon mechanics and systems with foundations in gaming. I’d go so far as to predict the first adopters of any “metaverse” will indeed be gamers who have honed these skills and find themselves comfortable within virtual environments.

By now, you might be seeing a pattern: We’re far more interested in the “future” applications of gaming without having much of a perspective on the “now” of gaming. Game scholarship has proliferated since the early aughts due to a recognition of how games were influencing thought in fields ranging from sociology to medicine, and yet the business world hasn’t paid it much attention until recently.

The result is that marketers and decision-makers are doing what they do best (chasing the next big thing) without the usual history of why said thing should be big, or what to do with it when they get there. The growth of gaming has yielded an immense opportunity, but the sophistication of the conversations around these possibilities remains stunted, due in part to our misdirected attention.

There is no “pay to win” fast track out of this blind spot. We have to put in the work to win.

Powered by WPeMatico

Social media has served as a launchpad to success almost as long as it has been around. The stories of going viral from a self-produced YouTube video and then securing a record deal established the mythology of social media platforms. Ever since, social media has consistently gravitated away from text-based formats and toward visual mediums like video sharing.

For most people, a video on social media won’t be a ticket to stardom, but in recent months, there have been a growing number of stories of people getting hired based on videos posted to TikTok. Even LinkedIn has embraced video assets on user profiles with the recent addition of the “Cover Story” feature, which allows workers to supplement their profiles with a video about themselves.

As technology continues to evolve, is there room for a world where your primary resume is a video on TikTok? And if so, what kinds of unintended consequences and implications might this have on the workforce?

In recent months, U.S. job openings have risen to an all-time high of 10.1 million. For the first time since the pandemic began, available jobs have exceeded available workers. Employers are struggling to attract qualified candidates to fill positions, and in that light, it makes sense that many recruiters are turning to social platforms like TikTok and video resumes to find talent.

But the scarcity of workers does not negate the importance of finding the right employee for a role. Especially important for recruiters is finding candidates with the skills that align with their business’ goals and strategy. For example, as more organizations embrace a data-driven approach to operating their business, they need more people with skills in analytics and machine learning to help them make sense of the data they collect.

Recruiters have proven to be open to innovation where it helps them find these new candidates. Recruiting is no longer the manual process it used to be, with HR teams sorting through stacks of paper resumes and formal cover letters to find the right candidate. They embraced the power of online connections as LinkedIn rose to prominence and even figured out how to use third-party job sites like GlassDoor to help them draw in promising candidates. On the back end, many recruiters use advanced cloud software to sort through incoming resumes to find the candidates that best match their job descriptions. But all of these methods still rely on the traditional text-based resume or profile as the core of any application.

Videos on social media provide the ability for candidates to demonstrate soft skills that may not be immediately apparent in written documents, such as verbal communication and presentation skills. They are also a way for recruiters to learn more about the personality of the candidate to determine how they’d fit into the culture of the company. While this may be appealing for many, are we ready for the consequences?

While innovation in recruiting is a big part of the future of work, the hype around TikTok and video resumes may actually take us backward. Despite offering a new way for candidates to market themselves for opportunities, it also carries potential pitfalls that candidates, recruiters and business leaders need to be aware of.

The very element that gives video resumes their potential also presents the biggest problems. Video inescapably highlights the person behind the skills and achievements. As recruiters form their first opinions about a candidate, they will be confronted with information they do not usually see until much later in the process, including whether they belong to protected classes because of their race, disability or gender.

Diversity, equity and inclusion (DE&I) concerns have had a major surge in attention over the last couple of years amid heightened awareness and scrutiny around how employers are — or are not — prioritizing diversity in the workplace.

But evaluating candidates through video could erase any progress made by introducing more opportunities for unconscious, or even conscious, bias. This could create a dangerous situation for businesses if they do not act carefully because it could open them up to consequences such as damage to their reputation or even something as severe as discrimination lawsuits.

A company with a poor track record for diversity may have the fact that they reviewed videos from candidates used against them in court. Recruiters reviewing the videos may not even be aware of how the race or gender of candidates are impacting their decisions. For that reason, many of the businesses I have seen implement an option for video in their recruiting flow do not allow their recruiters to watch the video until late in the recruiting process.

But even if businesses address the most pressing issues of DE&I by managing bias against those protected classes, by accepting videos there are still issues of diversity in less protected classes such as neurodiversity and socioeconomic status. A candidate with exemplary skills and a strong track record may not present themselves well through a video, coming across as awkward to the recruiter watching the video. Even if that impression is irrelevant to the job, it could still influence the recruiter’s stance on hiring.

Furthermore, candidates from affluent backgrounds may have access to better equipment and software to record and edit a compelling video resume. Other candidates may not, resulting in videos that may not look as polished or professional in the eyes of the recruiter. This creates yet another barrier to the opportunities they can access.

As we sit at an important crossroads in how we handle DE&I in the workplace, it is important for employers and recruiters to find ways to reduce bias in the processes they use to find and hire employees. While innovation is key to moving our industry forward, we have to ensure top priorities are not being compromised.

Despite all of these concerns, social media platforms — especially those based on video — have created new opportunities for users to expand their personal brands and connect with potential job opportunities. There is potential to use these new systems to benefit both job seekers and employers.

The first step is to ensure that there is always a place for a traditional text-based resume or profile in the recruiting process. Even if recruiters can get all the information they need about a candidate’s capabilities from video, some people will just naturally feel more comfortable staying off camera. Hiring processes need to be about letting people put their best foot forward, whether that is in writing or on video. And that includes accepting that the best foot to put forward may not be your own.

Instead, candidates and businesses should consider using videos as a place for past co-workers or managers to endorse the candidate. An outside endorsement can do a lot more good for an application than simply stating your own strengths because it shows that someone else believes in your capabilities, too.

Video resumes are hot right now because they are easier to make and share than ever and because businesses are in desperate need of strong talent. But before we get caught up in the novelty of this new way of sharing our credentials, we need to make sure that we are setting ourselves up for success.

The goal of any new recruiting technology should be to make it easier for candidates to find opportunities where they can shine without creating new barriers. There are some serious kinks to work out before video resumes can achieve that, and it is important for employers to consider the repercussions before they damage the success of their DE&I efforts.

Powered by WPeMatico

Funding for Black entrepreneurs in the U.S. hit nearly $1.8 billion in the first half of 2021 — a fourfold increase from the previous year. But most venture-backed startups are “still overwhelmingly white, male, Ivy-League-educated and based in Silicon Valley,” according to a study conducted by RateMyInvestor and Diversity VC.

With venture investors committing to funding Black and minority founders, alongside the growing availability of government-backed proposals, such as New Jersey allocating $10 million to a seed fund for Black and Latinx startups, can we expect to see fundamental change? Or will we have to repeat the same conversations about representation failings within VC funds?

Crunchbase examined the access to capital in the venture-backed startup ecosystem and proved that many industry leaders still worry that nothing will drastically shift. As a Black fintech founder, I believe that venture investors are making safe bets and investing in late-stage founders instead of early or even pre-seed stages.

But what about those minority founders who don’t have family, friends or connections to lean on for the first $250,000? Venture funding does remain elusive, but here are some tricks for startup founders to hack the system.

Getting your foot in the door with new venture capitalist partners is challenging, and it is often easy for minority founders to be naive at first. I thought that reading TechCrunch and analyzing other VC deals I saw in the news would help me land multiple responses and speak the language of those who managed to score million-dollar deals for their startups. However, I didn’t receive a single response while other founders received VC investment for basic ideas.

This is something I had to learn the hard way: What you hear in the media or read on a company blog post often simplifies the process, and sometimes fails to cover the trajectory that minority founders, in particular, must follow to secure funding.

I experienced hundreds of rejections before raising $2 million to start a mobile payment platform, Bleu, using beacon technology to drive simple and secure payments. It is a huge mountain to climb and a full-time job to continuously pitch your vision and yourself to reach the first meeting with a VC fund — and that’s still miles away from a funding discussion.

These discussions then bring further biases to the surface. If you sat in the conference rooms or on those Zoom calls and heard the types of deals proposed to minority founders, you’d see how offensive they can be. Often, these founders are offered all the money they have requested — but don’t be fooled. It is usually not given all at once due to what I consider to be a lack of trust. Essentially, interval funding equates to being babysat.

Therefore, as a minority founder, you have to realize that it will be a long ride, and you will face rejections because you are at a disadvantage before even opening your mouth to pitch your idea. It is all possible, but patience is key.

Once I figured out how complicated the funding process was, my coping mechanism was to figure out how to capitalize on the business ideas I already had in place in case I never received any VC funding.

Think: How could you make money without an institutional investor, friends, family or internal networks? You’ll be surprised by your entrepreneurial thirst for success when you’ve experienced 100 rejections. This is why minority businesses caught in these testing situations can quickly gain the upper hand, whether through ancillary and side businesses or crowdfunding over GoFundMe and Kickstarter.

Although generally considered non-essential, ancillary companies do provide a regular flow of income and services to assist your core business idea. Most importantly, a recurring revenue stream outside your core business demonstrates to investors that you can create valuable products and acquire loyal customers.

Make sure to find a niche market and carry out surveys with potential clients to find out what specific needs they have. Then, build a product with their feedback in mind and launch it to beta clients. When you publicly release the product, find resellers to keep internal headcount low and generate recurring revenue.

Don’t take ancillaries lightly, though; they are not just a side business. There can be payment issues if you get hooked on them for revenue, distractions from clients or partners wanting custom requests, and supply chain problems.

In my case, I built a point-of-sale (POS) software platform to sell to merchants, which gave me a different revenue stream that could integrate with Bleu’s payment technology. These ancillary businesses can help fund your core business until you manage to plan how to launch fully or source further funding.

In 2019, The New York Times published an article headlined “More Start-Ups Have an Unfamiliar Message for Venture Capitalists: Get Lost.” It highlights how more and more entrepreneurs shunned by the VC funding route are turning to alternatives and forming counter-movements. There are always alternatives to look at if the fundraising process is proving to be too arduous.

Accelerators allow ventures to define their products or services, quickly build networks and, most importantly, sit at tables they wouldn’t be able to on their own. Applying to accelerators as a minority founder was the real turning point for me because I met a crucial investor who allowed us to build credibility and open up to new networks, investors and clients.

I would suggest looking out for accelerators explicitly searching for minority founders by using platforms such as F6S. They match you with accelerators and early growth programs committed to innovation in various global industries, like financial technology. That’s how I found the VC FinTech Accelerator in 2016, where one-third of founders were from minority backgrounds.

Then, Bleu earned a spot in the 2020 class of the IBM Hyper Protect Accelerator dedicated to supporting innovative startups in fintech and health tech industries. These types of accelerators offer startups workshops, technical and business mentorship, and access to a network of partners, customers and stakeholders.

You can impress accelerators by creating a pitch deck and a company video less than two minutes long that shows your founder and the product, and engaging with the fintech community to spread the news.

The other alternative to accelerators is government funds, but they have had little success investing in startups for myriad reasons. It tends to be a more hands-off approach as government funds are not under significant pressure from limited partners (LPs, either institutional or individual investors) to perform.

What you need as a minority founder is an investor who is an active partner but, with government-backed funds, there is less demand to return the capital. We have to ask ourselves whether governments are really searching for the best minority-owned startups to help them get sufficient returns.

There are many unconscious social stigmas, stereotypes and unseen biases that exist in the U.S. And you’ll find those cultural dynamics are radically different in other countries that don’t have the same history of discrimination, especially when looking at a team or assessing founders.

I also noticed that, as well as reduced bias, investors out of Southeast Asia, Nordic countries and Australia seemed far more likely to take risks on new contactless payment technology as cash use decreased across their regions. Take Klarna and Afterpay as examples of fintech success stories.

First, I engaged in market research and pored over annual reports to decide whether I should look abroad for funding, instead of applying to funds closer to home. I looked at Nielsen reports, payment publications, PaymentSource and numerous government documents or white papers to figure out the cash usage globally.

My investigations revealed that fintech in Australia was far ahead of the curve, with four-fifths of the population using contactless payments. The financial services sector is also the largest contributor to the national economy, contributing around $140 billion to GDP a year. Therefore, I spoke to the Australian Department of Foreign Affairs and Trade in the U.S., and they recommended some regulatory payment groups.

I immediately flew to Australia to meet with the banking community, and I was able to find an Australian investor by word of mouth who was surrounded by the demand for mobile payment solutions.

In contrast, an investor in the U.S. still using cash and card had no interest in what I had to say. This highlights the importance of market research and seeking out investors rather than waiting for them to come to you. There is no science to it; leverage your network and reach out to people over LinkedIn, too.

VC funding needs to become more inclusive for women and minority groups by tackling the pipeline problem and addressing the level of diversity within VC funds. All of the networks that VCs reach out to first tend to come from university programs at Stanford, MIT and Harvard. These more privileged and wealthy students are able to easily leverage the traditional and outdated networks built to benefit them.

The number of venture dollars flowing to Black and Latinx founders is dismally low partly due to this knowledge gap; many female and minority founders don’t even know that VC funding is an option for them. Therefore, if you do receive seed funding, spread the news about it within your networks to help others.

Inclusion starts at the educational level but, when the percentage of Black and minority students at these elite colleges are still low, you can see why minority representation is needed in the VC ranks. Even if representation rises by a percent, that would be a significant change.

There are increasing numbers of VC funds announcing initiatives and interest in investing in minority businesses, and I would recommend looking at these in-depth. But what about the demographics of the VC firms? How many ethnicities are present in the executive ranks?

To change the venture-backed startup ecosystem, we need to start at the top and diversify those signing the checks. Looking toward the future, it is Black-led funds, like Sequoia, or others that focus on diversity, like Women’s Venture Fund, BackStage Capital and Elevate Capital Inclusive Fund, that are lighting the way to solutions that will reflect the diversity of the U.S.

It’s up to the investor community at large to be intentional about building relationships with, and ultimately providing funding to, more women and minority-led startups.

Despite the barriers and hurdles minority founders face when searching for VC funding, more and more avenues for acquiring funding are appearing as the disparities are brought to the media’s attention.

As the outdated system adjusts, the key is to continue preparing yourself for rejections and searching for appropriate accelerators to build vital networks. Then, if you aren’t having any luck, consider what you could do with your business idea without the VC funding or turn to foreign markets, which may have a different setup and varied opportunities.

Powered by WPeMatico

The quest to make fusion power a reality recently took a massive step forward. The National Ignition Facility (NIF) at Lawrence Livermore National Laboratory announced the results of an experiment with an unprecedented high fusion yield. A single laser shot initiated reactions that released 1.3 megajoules of fusion yield energy with signatures of propagating nuclear burn.

Reaching this milestone indicates just how close fusion actually is to achieving power production. The latest results demonstrate the rapid pace of progress — especially as lasers are evolving at breathtaking speed.

Indeed, the laser is one of the most impactful technological inventions since the end of World War II. Finding widespread use in an incredibly diverse range of applications — including machining, precision surgery and consumer electronics — lasers are an essential part of everyday life. Few know, however, that lasers are also heralding an exciting and entirely new chapter in physics: enabling controlled nuclear fusion with positive energy gain.

After six decades of innovation, lasers are now assisting us in the urgent process of developing clean, dense and efficient fuels, which, in turn, are needed to help solve the world’s energy crisis through large-scale decarbonized energy production. The peak power attainable in a laser pulse has increased every decade by a factor of 1,000.

Physicists recently conducted a fusion experiment that produced 1,500 terawatts of power. For a short period of time, this generated four to five times more energy than what the whole world consumes at a given moment. In other words, we are already able to produce vast amounts of power. Now we also need to produce vast amounts of energy so as to offset the energy expended to drive the igniting lasers.

Beyond lasers, there are also considerable advances on the target side. The recent use of nanostructure targets allows for more efficient absorption of laser energies and ignition of the fuel. This has only been possible for a few years, but here, too, technological innovation is on a steep incline with tremendous advancement from year to year.

In the face of such progress, you may wonder what is still holding us back from making commercial fusion a reality.

There remain two significant challenges: First, we need to bring the pieces together and create an integrated process that satisfies all the physical and technoeconomic requirements. Second, we require sustainable levels of investment from private and public sources to do so. Generally speaking, the field of fusion is woefully underfunded. This is shocking given the potential of fusion, especially in comparison to other energy technologies.

Investments in clean energy amounted to more than $500 billion in 2020. The funds that go into fusion research and development are only a fraction of that. There are countless brilliant scientists working in the sector already, as well as eager students wishing to enter the field. And, of course, we have excellent government research labs. Collectively, researchers and students believe in the power and potential of controlled nuclear fusion. We should ensure financial support for their work to make this vision a reality.

What we need now is an expansion of public and private investment that does justice to the opportunity at hand. Such investments may have a longer time horizon, but their eventual impact is without parallel. I believe that net-energy gain is within reach in the next decade; commercialization, based on early prototypes, will follow in very short order.

But such timelines are heavily dependent on funding and the availability of resources. Considerable investment is being allocated to alternative energy sources — wind, solar, etc. — but fusion must have a place in the global energy equation. This is especially true as we approach the critical breakthrough moment.

If laser-driven nuclear fusion is perfected and commercialized, it has the potential to become the energy source of choice, displacing the many existing, less ideal energy sources. This is because fusion, if done correctly, offers energy that is in equal parts clean, safe and affordable. I am convinced that fusion power plants will eventually replace most conventional power plants and related large-scale energy infrastructure that are still so dominant today. There will be no need for coal or gas.

The ongoing optimization of the fusion process, which results in higher yields and lower costs, promises energy production at much below the current price point. At the limit, this corresponds to a source of unlimited energy. If you have unlimited energy, then you also have unlimited possibilities. What can you do with it? I foresee reversing climate change by taking out the carbon dioxide we have put into the atmosphere over the last 150 years.

With a future empowered by fusion technology, you would also be able to use energy to desalinate water, creating unlimited water resources that would have an enormous impact in arid and desert regions. All in all, fusion enables better societies, keeping them sustainable and clean rather than dependent on destructive, dirty energy sources and related infrastructures.

Through years of dedicated research at the SLAC National Accelerator Laboratory, the Lawrence Livermore National Laboratory and the National Ignition Facility, I was privileged to witness and lead the first inertial confinement fusion experiments. I saw the seed of something remarkable being planted and taking root. I have never been more excited than I am now to see the fruits of laser technology harvested for the empowerment and advancement of humankind.

My fellow scientists and students are committed to moving fusion from the realm of tangibility into that of reality, but this will require a level of trust and help. A small investment today will have a big impact toward providing a much needed, more welcome energy alternative in the global arena.

I am betting on the side of optimism and science, and I hope that others will have the courage to do so, too.

Powered by WPeMatico

Startups devoted to reproductive and women’s health are on the rise. However, most of them deal with women’s fertility: birth control, ovulation and the inability to conceive. The broader field of women’s health remains neglected.

Historically, most of our understanding of ailments comes from the perspective of men and is overwhelmingly based on studies using male patients. Until the early 1990s, women of childbearing age were kept out of drug trial studies, and the resulting bias has been an ongoing issue in healthcare. Other issues include underrepresentation of women in health studies, trivialization of women’s physical complaints (which is relevant to the misdiagnosis of endometriosis, among other conditions), and gender bias in the funding of research, especially in research grants.

For example, several studies have shown that when we look at National Institutes of Health funding, a disproportionate share of its resources goes to diseases that primarily affect men — at the expense of those that primarily affect women. In 2019, studies of NIH funding based on disease burden (as estimated by the number of years lost due to an illness) showed that male-favored diseases were funded at twice the rate of female-favored diseases.

Let’s take endometriosis as an example. Endometriosis is a disease where endometrial-like tissue (‘‘lesions’’) can be found outside the uterus. Endometriosis is a condition that only occurs in individuals with uteruses and has been less funded and less studied than many other conditions. It can cause chronic pain, fatigue, painful intercourse and infertility. Although the disease may affect one out of 10 women, diagnosis is still very slow, and the disease is confirmed only by surgery.

There is no non-invasive test available. In many cases, a woman is diagnosed only due to her infertility, and the diagnosis can take up to 10 years. Even after diagnosis, the understanding of disease biology and progression is poor, as well as the understanding of the relationships to other lesion diseases, such as adenomyosis. Current treatments include surgical removal of lesions and drugs that suppress ovarian hormone (mainly estrogen) production.

However, there are changes in the works. The NIH created the women’s health research category in 1994 for annual budgeting purposes and, in 2019, it was updated to include research that is relevant to women only. In acknowledging the widespread male bias in both human and animal studies, the NIH mandated in 2016 that grant applicants would be required to recruit male and female participants in their protocols. These changes are slow, and if we look at endometriosis, it received just $7 million in NIH funding in the fiscal year 2018, putting it near the very bottom of NIH’s 285 disease/research areas.

It is interesting to note that critical changes are coming from other sources, and not so much from the funding agencies or the pharmaceutical industry. The push is coming from patients and physicians themselves that meet the diseases regularly. We see pharmaceutical companies (such as Eli Lilly and AbbVie) in the women’s healthcare space following the lead of their patients and slowly expanding their R&D base and doubling efforts to expand beyond reproductive health into other key women’s health areas.

New technological innovations targeting endometriosis are being funded via private sources. In 2020, women’s health finally emerged as one of the most promising areas of investment. These include (not an exhaustive list by any means) diagnostics companies such as NextGen Jane, which raised a $9 million Series A in April 2021 for its “smart tampon,” and DotLab, a non-invasive endometriosis testing startup, which raised $10 million from investors last July. Other notable advances include the research-study app Phendo that tracks endometriosis, and Gynica, a company focused on cannabis-based treatments for gynecological issues.

The complexity of endometriosis is such that any single biotech startup may find it challenging to go it alone. One approach to tackle this is through collaborations. Two companies, Polaris Quantum Biotech and Auransa, have teamed up to tackle the endometriosis challenge and other women’s specific diseases.

Using data, algorithms and quantum computing, this collaboration between two female-led AI companies integrates the understanding of disease biology with chemistry. Moreover, they are not stopping at in silico; rather, this collaboration aims to bring therapeutics to patients.

New partnerships can majorly impact how fast a field like women’s health can advance. Without such concerted efforts, women-centric diseases such as endometriosis, triple-negative breast cancer and ovarian cancer, to name a few, may remain neglected and result in much-needed therapeutics not moving into clinics promptly.

Using state-of-the-art technologies on complex women’s diseases will allow the field to advance much faster and can put drug candidates into clinics in a few short years, especially with the help of patient advocacy groups, research organizations, physicians and out-of-the-box funding approaches such as crowdfunding from the patients themselves.

We believe that going after the women’s health market is a win-win for the patients as well as from the business perspective, as the global market for endometriosis drugs alone is expected to reach $2.2 billion in the next six years.

Powered by WPeMatico

Facebook is a monopoly. Right?

Mark Zuckerberg appeared on national TV today to make a “special announcement.” The timing could not be more curious: Today is the day Lina Khan’s FTC refiled its case to dismantle Facebook’s monopoly.

To the average person, Facebook’s monopoly seems obvious. “After all,” as James E. Boasberg of the U.S. District Court for the District of Columbia put it in his recent decision, “No one who hears the title of the 2010 film ‘The Social Network’ wonders which company it is about.” But obviousness is not an antitrust standard. Monopoly has a clear legal meaning, and thus far Lina Khan’s FTC has failed to meet it. Today’s refiling is much more substantive than the FTC’s first foray. But it’s still lacking some critical arguments. Here are some ideas from the front lines.

To the average person, Facebook’s monopoly seems obvious. But obviousness is not an antitrust standard.

First, the FTC must define the market correctly: personal social networking, which includes messaging. Second, the FTC must establish that Facebook controls over 60% of the market — the correct metric to establish this is revenue.

Though consumer harm is a well-known test of monopoly determination, our courts do not require the FTC to prove that Facebook harms consumers to win the case. As an alternative pleading, though, the government can present a compelling case that Facebook harms consumers by suppressing wages in the creator economy. If the creator economy is real, then the value of ads on Facebook’s services is generated through the fruits of creators’ labor; no one would watch the ads before videos or in between posts if the user-generated content was not there. Facebook has harmed consumers by suppressing creator wages.

A note: This is the first of a series on the Facebook monopoly. I am inspired by Cloudflare’s recent post explaining the impact of Amazon’s monopoly in their industry. Perhaps it was a competitive tactic, but I genuinely believe it more a patriotic duty: guideposts for legislators and regulators on a complex issue. My generation has watched with a combination of sadness and trepidation as legislators who barely use email question the leading technologists of our time about products that have long pervaded our lives in ways we don’t yet understand. I, personally, and my company both stand to gain little from this — but as a participant in the latest generation of social media upstarts, and as an American concerned for the future of our democracy, I feel a duty to try.

According to the court, the FTC must meet a two-part test: First, the FTC must define the market in which Facebook has monopoly power, established by the D.C. Circuit in Neumann v. Reinforced Earth Co. (1986). This is the market for personal social networking services, which includes messaging.

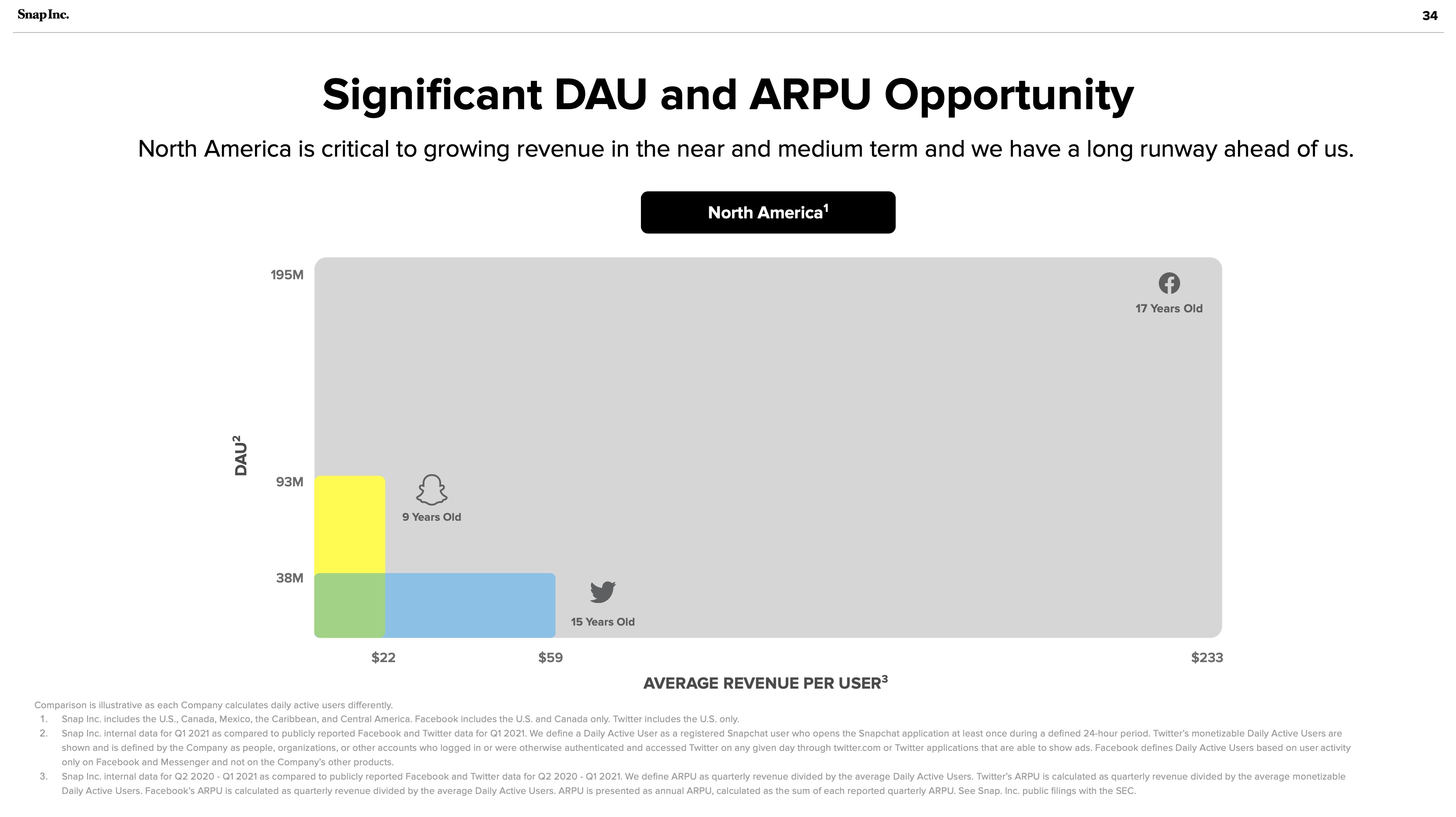

Second, the FTC must establish that Facebook controls a dominant share of that market, which courts have defined as 60% or above, established by the 3rd U.S. Circuit Court of Appeals in FTC v. AbbVie (2020). The right metric for this market share analysis is unequivocally revenue — daily active users (DAU) x average revenue per user (ARPU). And Facebook controls over 90%.

The answer to the FTC’s problem is hiding in plain sight: Snapchat’s investor presentations:

Snapchat July 2021 investor presentation: Significant DAU and ARPU Opportunity. Image Credits: Snapchat

This is a chart of Facebook’s monopoly — 91% of the personal social networking market. The gray blob looks awfully like a vast oil deposit, successfully drilled by Facebook’s Standard Oil operations. Snapchat and Twitter are the small wildcatters, nearly irrelevant compared to Facebook’s scale. It should not be lost on any market observers that Facebook once tried to acquire both companies.

The FTC initially claimed that Facebook has a monopoly of the “personal social networking services” market. The complaint excluded “mobile messaging” from Facebook’s market “because [messaging apps] (i) lack a ‘shared social space’ for interaction and (ii) do not employ a social graph to facilitate users’ finding and ‘friending’ other users they may know.”

This is incorrect because messaging is inextricable from Facebook’s power. Facebook demonstrated this with its WhatsApp acquisition, promotion of Messenger and prior attempts to buy Snapchat and Twitter. Any personal social networking service can expand its features — and Facebook’s moat is contingent on its control of messaging.

The more time in an ecosystem the more valuable it becomes. Value in social networks is calculated, depending on whom you ask, algorithmically (Metcalfe’s law) or logarithmically (Zipf’s law). Either way, in social networks, 1+1 is much more than 2.

Social networks become valuable based on the ever-increasing number of nodes, upon which companies can build more features. Zuckerberg coined the “social graph” to describe this relationship. The monopolies of Line, Kakao and WeChat in Japan, Korea and China prove this clearly. They began with messaging and expanded outward to become dominant personal social networking behemoths.

In today’s refiling, the FTC explains that Facebook, Instagram and Snapchat are all personal social networking services built on three key features:

Unfortunately, this is only partially right. In social media’s treacherous waters, as the FTC has struggled to articulate, feature sets are routinely copied and cross-promoted. How can we forget Instagram’s copying of Snapchat’s stories? Facebook has ruthlessly copied features from the most successful apps on the market from inception. Its launch of a Clubhouse competitor called Live Audio Rooms is only the most recent example. Twitter and Snapchat are absolutely competitors to Facebook.

Messaging must be included to demonstrate Facebook’s breadth and voracious appetite to copy and destroy. WhatsApp and Messenger have over 2 billion and 1.3 billion users respectively. Given the ease of feature copying, a messaging service of WhatsApp’s scale could become a full-scale social network in a matter of months. This is precisely why Facebook acquired the company. Facebook’s breadth in social media services is remarkable. But the FTC needs to understand that messaging is a part of the market. And this acknowledgement would not hurt their case.

Boasberg believes revenue is not an apt metric to calculate personal networking: “The overall revenues earned by PSN services cannot be the right metric for measuring market share here, as those revenues are all earned in a separate market — viz., the market for advertising.” He is confusing business model with market. Not all advertising is cut from the same cloth. In today’s refiling, the FTC correctly identifies “social advertising” as distinct from the “display advertising.”

But it goes off the deep end trying to avoid naming revenue as the distinguishing market share metric. Instead the FTC cites “time spent, daily active users (DAU), and monthly active users (MAU).” In a world where Facebook Blue and Instagram compete only with Snapchat, these metrics might bring Facebook Blue and Instagram combined over the 60% monopoly hurdle. But the FTC does not make a sufficiently convincing market definition argument to justify the choice of these metrics. Facebook should be compared to other personal social networking services such as Discord and Twitter — and their correct inclusion in the market would undermine the FTC’s choice of time spent or DAU/MAU.

Ultimately, cash is king. Revenue is what counts and what the FTC should emphasize. As Snapchat shows above, revenue in the personal social media industry is calculated by ARPU x DAU. The personal social media market is a different market from the entertainment social media market (where Facebook competes with YouTube, TikTok and Pinterest, among others). And this too is a separate market from the display search advertising market (Google). Not all advertising-based consumer technology is built the same. Again, advertising is a business model, not a market.

In the media world, for example, Netflix’s subscription revenue clearly competes in the same market as CBS’ advertising model. News Corp.’s acquisition of Facebook’s early competitor MySpace spoke volumes on the internet’s potential to disrupt and destroy traditional media advertising markets. Snapchat has chosen to pursue advertising, but incipient competitors like Discord are successfully growing using subscriptions. But their market share remains a pittance compared to Facebook.

The FTC has correctly argued for the smallest possible market for their monopoly definition. Personal social networking, of which Facebook controls at least 80%, should not (in their strongest argument) include entertainment. This is the narrowest argument to make with the highest chance of success.

But they could choose to make a broader argument in the alternative, one that takes a bigger swing. As Lina Khan famously noted about Amazon in her 2017 note that began the New Brandeis movement, the traditional economic consumer harm test does not adequately address the harms posed by Big Tech. The harms are too abstract. As White House advisor Tim Wu argues in “The Curse of Bigness,” and Judge Boasberg acknowledges in his opinion, antitrust law does not hinge solely upon price effects. Facebook can be broken up without proving the negative impact of price effects.

However, Facebook has hurt consumers. Consumers are the workers whose labor constitutes Facebook’s value, and they’ve been underpaid. If you define personal networking to include entertainment, then YouTube is an instructive example. On both YouTube and Facebook properties, influencers can capture value by charging brands directly. That’s not what we’re talking about here; what matters is the percent of advertising revenue that is paid out to creators.

YouTube’s traditional percentage is 55%. YouTube announced it has paid $30 billion to creators and rights holders over the last three years. Let’s conservatively say that half of the money goes to rights holders; that means creators on average have earned $15 billion, which would mean $5 billion annually, a meaningful slice of YouTube’s $46 billion in revenue over that time. So in other words, YouTube paid creators a third of its revenue (this admittedly ignores YouTube’s non-advertising revenue).

Facebook, by comparison, announced just weeks ago a paltry $1 billion program over a year and change. Sure, creators may make some money from interstitial ads, but Facebook does not announce the percentage of revenue they hand to creators because it would be insulting. Over the equivalent three-year period of YouTube’s declaration, Facebook has generated $210 billion in revenue. one-third of this revenue paid to creators would represent $70 billion, or $23 billion a year.

Why hasn’t Facebook paid creators before? Because it hasn’t needed to do so. Facebook’s social graph is so large that creators must post there anyway — the scale afforded by success on Facebook Blue and Instagram allows creators to monetize through directly selling to brands. Facebooks ads have value because of creators’ labor; if the users did not generate content, the social graph would not exist. Creators deserve more than the scraps they generate on their own. Facebook suppresses creators’ wages because it can. This is what monopolies do.

Facebook has long been the Standard Oil of social media, using its core monopoly to begin its march upstream and down. Zuckerberg announced in July and renewed his focus today on the metaverse, a market Roblox has pioneered. After achieving a monopoly in personal social media and competing ably in entertainment social media and virtual reality, Facebook’s drilling continues. Yes, Facebook may be free, but its monopoly harms Americans by stifling creator wages. The antitrust laws dictate that consumer harm is not a necessary condition for proving a monopoly under the Sherman Act; monopolies in and of themselves are illegal. By refiling the correct market definition and marketshare, the FTC stands more than a chance. It should win.

A prior version of this article originally appeared on Substack.

Powered by WPeMatico

The Pareto principle, also known as the 80-20 rule, asserts that 80% of consequences come from 20% of causes, rendering the remainder way less impactful.

Those working with data may have heard a different rendition of the 80-20 rule: A data scientist spends 80% of their time at work cleaning up messy data as opposed to doing actual analysis or generating insights. Imagine a 30-minute drive expanded to two-and-a-half hours by traffic jams, and you’ll get the picture.

As tempting as it may be to think of a future where there is a machine learning model for every business process, we do not need to tread that far right now.

While most data scientists spend more than 20% of their time at work on actual analysis, they still have to waste countless hours turning a trove of messy data into a tidy dataset ready for analysis. This process can include removing duplicate data, making sure all entries are formatted correctly and doing other preparatory work.

On average, this workflow stage takes up about 45% of the total time, a recent Anaconda survey found. An earlier poll by CrowdFlower put the estimate at 60%, and many other surveys cite figures in this range.

None of this is to say data preparation is not important. “Garbage in, garbage out” is a well-known rule in computer science circles, and it applies to data science, too. In the best-case scenario, the script will just return an error, warning that it cannot calculate the average spending per client, because the entry for customer #1527 is formatted as text, not as a numeral. In the worst case, the company will act on insights that have little to do with reality.

The real question to ask here is whether re-formatting the data for customer #1527 is really the best way to use the time of a well-paid expert. The average data scientist is paid between $95,000 and $120,000 per year, according to various estimates. Having the employee on such pay focus on mind-numbing, non-expert tasks is a waste both of their time and the company’s money. Besides, real-world data has a lifespan, and if a dataset for a time-sensitive project takes too long to collect and process, it can be outdated before any analysis is done.

What’s more, companies’ quests for data often include wasting the time of non-data-focused personnel, with employees asked to help fetch or produce data instead of working on their regular responsibilities. More than half of the data being collected by companies is often not used at all, suggesting that the time of everyone involved in the collection has been wasted to produce nothing but operational delay and the associated losses.

The data that has been collected, on the other hand, is often only used by a designated data science team that is too overworked to go through everything that is available.

The issues outlined here all play into the fact that save for the data pioneers like Google and Facebook, companies are still wrapping their heads around how to re-imagine themselves for the data-driven era. Data is pulled into huge databases and data scientists are left with a lot of cleaning to do, while others, whose time was wasted on helping fetch the data, do not benefit from it too often.

The truth is, we are still early when it comes to data transformation. The success of tech giants that put data at the core of their business models set off a spark that is only starting to take off. And even though the results are mixed for now, this is a sign that companies have yet to master thinking with data.

Data holds much value, and businesses are very much aware of it, as showcased by the appetite for AI experts in non-tech companies. Companies just have to do it right, and one of the key tasks in this respect is to start focusing on people as much as we do on AIs.

Data can enhance the operations of virtually any component within the organizational structure of any business. As tempting as it may be to think of a future where there is a machine learning model for every business process, we do not need to tread that far right now. The goal for any company looking to tap data today comes down to getting it from point A to point B. Point A is the part in the workflow where data is being collected, and point B is the person who needs this data for decision-making.

Importantly, point B does not have to be a data scientist. It could be a manager trying to figure out the optimal workflow design, an engineer looking for flaws in a manufacturing process or a UI designer doing A/B testing on a specific feature. All of these people must have the data they need at hand all the time, ready to be processed for insights.

People can thrive with data just as well as models, especially if the company invests in them and makes sure to equip them with basic analysis skills. In this approach, accessibility must be the name of the game.

Skeptics may claim that big data is nothing but an overused corporate buzzword, but advanced analytics capacities can enhance the bottom line for any company as long as it comes with a clear plan and appropriate expectations. The first step is to focus on making data accessible and easy to use and not on hauling in as much data as possible.

In other words, an all-around data culture is just as important for an enterprise as the data infrastructure.

Powered by WPeMatico

The future of technology is determined by a handful of venture capitalists. The world’s 10 leading venture capital firms have, together, invested over $150 billion in technology startups. The venture capitalists who run these firms decide which startups today will develop the new platforms and technologies that will shape our lives tomorrow.

There is a startling lack of diversity within the venture capital sector. This means that a small group of men — mostly white men — make decisions that affect all of us. Unsurprisingly, they all too often ignore the broader societal and human rights implications of these investment decisions.

We all live in a world shaped by venture capital. As of 2019, 81% of all venture capital funds worldwide are clustered in just a handful of countries, primarily in the U.S., Europe and China, which in turn are shaping the future of technology. If you spend time on Facebook or Twitter, use Google, travel in an Uber or stay in an Airbnb, then you’ve experienced firsthand the impact of venture capital funding.

Venture capital firms, which provide equity financing for early- and growth-stage startups, play a critical gatekeeper role, deciding which new technologies and technology companies will receive funding.

Venture capital firms need to institute human rights due diligence processes that meet the standards set forth in the UN Guiding Principles on Business and Human Rights.

All businesses — including venture capital — have a responsibility to respect human rights. In order to ensure that their investments are not undermining our human rights, it is therefore critical for venture capital firms to conduct due diligence processes before making investments.

Amnesty International recently surveyed the world’s largest venture capital firms and startup accelerators. Of the world’s 10 largest venture capital firms, not a single one had an adequate human rights due diligence process that met the standards set forth in the UN Guiding Principles on Business and Human Rights.

Unfortunately, this is true of the broader venture capital sector as well. Overall, of the 50 VC firms and three startup accelerators analyzed by Amnesty International, we found that almost all of them lacked adequate human rights due diligence policies and processes.

This failure to carry out adequate due diligence means that a vast majority of VC firms are failing in their responsibility to respect human rights.

This almost complete lack of respect for human rights among the world’s largest venture capital firms has three key impacts. First, and most immediately, it means that venture capital firms invest in companies whose products and services have been implicated in ongoing human rights abuses, such as companies that provide support to the Chinese government’s repression of the Uyghur population in Xinjiang and across China.

Second, it means that venture capital firms continue to fund companies whose business models have a significant negative impact on human rights, including our privacy and labor rights. For instance, leading venture capital firms continue to support companies that rely on app-based or “gig” workers, who often face exploitative or otherwise abusive work conditions, as well as companies whose “surveillance capitalism” business model undermines our right to privacy.

Third, the lack of human rights due diligence by venture capital firms dramatically increases the risk that they fund new and “frontier” technologies without ensuring that adequate human rights safeguards are in place.

For instance, the application of increasingly powerful artificial intelligence/machine learning (AI/ML) tools across a wide variety of sectors risks amplifying existing societal biases and discrimination. Seemingly objective algorithms can be biased by reliance on incomplete or unrepresentative training data, and/or by replicating the unconscious bias of those who developed the algorithms.

This is a critical blind spot, especially as VC-funded startups seek to disrupt such fundamental parts of our lives as education, finance and health.

The negative impacts of the VC firms’ lack of human rights due diligence — especially regarding issues like algorithmic bias — are magnified by these firms’ own lack of gender and racial diversity. For instance, women comprise only 23% of venture capital investment professionals (i.e., those involved in deciding which startups to fund).

The numbers are even worse when it comes to racial diversity — just 4% of investment professionals at VC firms in the U.S. are Latinx, and only 4% are Black. Groups like Blck VC, Diversity VC and digitalundivided have been calling attention to this issue for years, but venture capitalists have been slow to respond so far.

This lack of diversity is mirrored in the gender and racial composition of founders who receive VC funding. In 2018, all-female founding teams received just 2.2% of all U.S.-based venture funding. At the same time, Black and Latinx founders received less than 2.3% of all U.S.-based venture capital funding in 2019.

With power comes responsibility. Venture capital firms need to institute human rights due diligence processes that meet the standards set forth in the UN Guiding Principles on Business and Human Rights.

Further, they should provide support to their portfolio companies to ensure that they comply with human rights standards. Venture capital firms should also publicly commit to hiring more diverse teams, especially in investment-related positions. Finally, they should publicly commit to funding more diverse startup founders as part of their flagship funds.

VC firms have a responsibility to ensure that their investments are not causing harm. A responsibility that they have, to date, largely ignored.

Powered by WPeMatico

One of the big reasons you’re giving 110% of your talent and effort to your private company is because you’re hoping to eventually cash in on all those vested incentive stock options (ISOs) that have been sitting in some account, waiting for the day your company goes public.

There’s nothing wrong with that. Who doesn’t dream of reaping an options windfall and using it to retire early, buy a house, pay off their college loans, travel around the world or become a full-time philanthropist?

Unfortunately, when it comes to figuring out how to cash in their stock awards, most employees are on their own.

Their employers can’t always provide the answers they need — especially when the questions relate to personal finances. Most companies admit they need to be better at explaining how ISOs work in general, but they can’t legally work one-on-one with employees to help them exercise and sell shares the right way.

Most companies admit they need to be better at explaining how ISOs work in general, but they can’t legally work one-on-one with employees to help them exercise and sell shares the right way.

That’s why, when the time is right, many employees actively look for help from a qualified fiduciary financial adviser who can walk these could-be “options millionaires” through various cash-in scenarios.

Here’s a real-life example (using a pseudonym).

Kurt is a 50-year-old VP of product management at a healthcare startup that just went public. Over his three years with the company, Kurt had amassed 350,000 ISOs worth approximately $6 million. Unlike many options millionaires, he didn’t intend to cash in everything and retire early. He planned to stay with the firm but wanted to liquidate enough ISOs to pay for a vacation home and add greater diversification to his investment portfolio. This presented significant tax risks that Kurt wasn’t aware of.

If Kurt exercised his ISOs and sold the shares before a year had passed, his profits would be characterized as short-term capital gains, which are taxed as ordinary income.

To illustrate the potential tax implications of this action, we created a hypothetical scenario that showed if Kurt exercised all of his ISOs and sold the shares immediately, he would incur approximately $6 million in ordinary income, which would push him into the top tax bracket and put him on the hook for almost $3 million in combined federal and state taxes.

Powered by WPeMatico

Sunday was a big day in fintech: Afterpay has agreed to merge with Square. This agreement sets two of the most admired financial technology companies in recent history on a path to becoming one.

Afterpay and Square have the potential to build one of the world’s most important payments networks. Square has built a very significant merchant payment network, and, via Cash App, a thriving high-growth consumer payment service. However, these two lines of business have historically not been integrated. Together, Square and Afterpay will be able to weave all of these services together into a single integrated experience.

Afterpay and Cash App each have double-digit millions of consumers, and Square’s seller ecosystem and Afterpay’s merchant network both record double-digit billions of payment volume per year. From the offline register and the online checkout flow to sending money in just a few taps, Square and Afterpay will tell a complete story of next-generation economic empowerment.

As Afterpay’s only institutional venture investor, I wanted to share some perspective on how we got here and what this merger means for the future of consumer finance and the payments industry.

Afterpay and Square have the potential to build one of the world’s most important payments networks.

Every five to 10 years, the global payments industry undergoes a critical innovation cycle that determines the winners and losers for the next several decades. The last major transition was the shift to NFC-based mobile payments, which I wrote about in 2015. The major mobile OS vendors (Apple and Google) cemented their position in the global payments stack by deftly bridging the needs of the networks (Visa, Mastercard, etc.) and consumers by way of the mobile devices in their pockets.

Afterpay sparked the latest critical innovation cycle. Conceived in a living room in Sydney by a millennial, Nick Molnar, for millennials, Afterpay had a key insight: Millennials don’t like credit.

Millennials came of age during the global mortgage crisis of 2008. As young adults, they watched their friends and family lose their homes by overextending on mortgage debt, bolstering their already lower trust for banks. They also have record levels of student debt. Therefore, it’s no surprise that millennials (and Gen Z right behind them) strongly prefer debit cards over credit cards.

But it’s one thing to recognize the paradigm shift and quite another to do something about it. Nick Molnar and Anthony Eisen did something, ultimately building one of the fastest-growing payments startups in history on their core product: Buy now, pay later … and never any interest.

Afterpay’s product is simple. If you have $100 in your cart and choose to pay with Afterpay, it will charge your bank card (typically a debit card) $25 every two weeks in four installments. No interest, no revolving debt and no fees with on-time payments. For the millennial consumer, this meant they could get the primary benefit of a credit card (the ability to pay later) with their debit card, without the need to worry about all the bad things that come with credit cards — high interest rates and revolving debt.

All upside, no downside. Who could resist? For the early merchants, virtually all of whom relied on millennials as their key growth segment, they got a fair trade: Pay a small fee above payment processing to Afterpay, get significantly higher average order values and conversions to purchase. It was a win-win proposition and, with lots of execution, a new payment network was born.

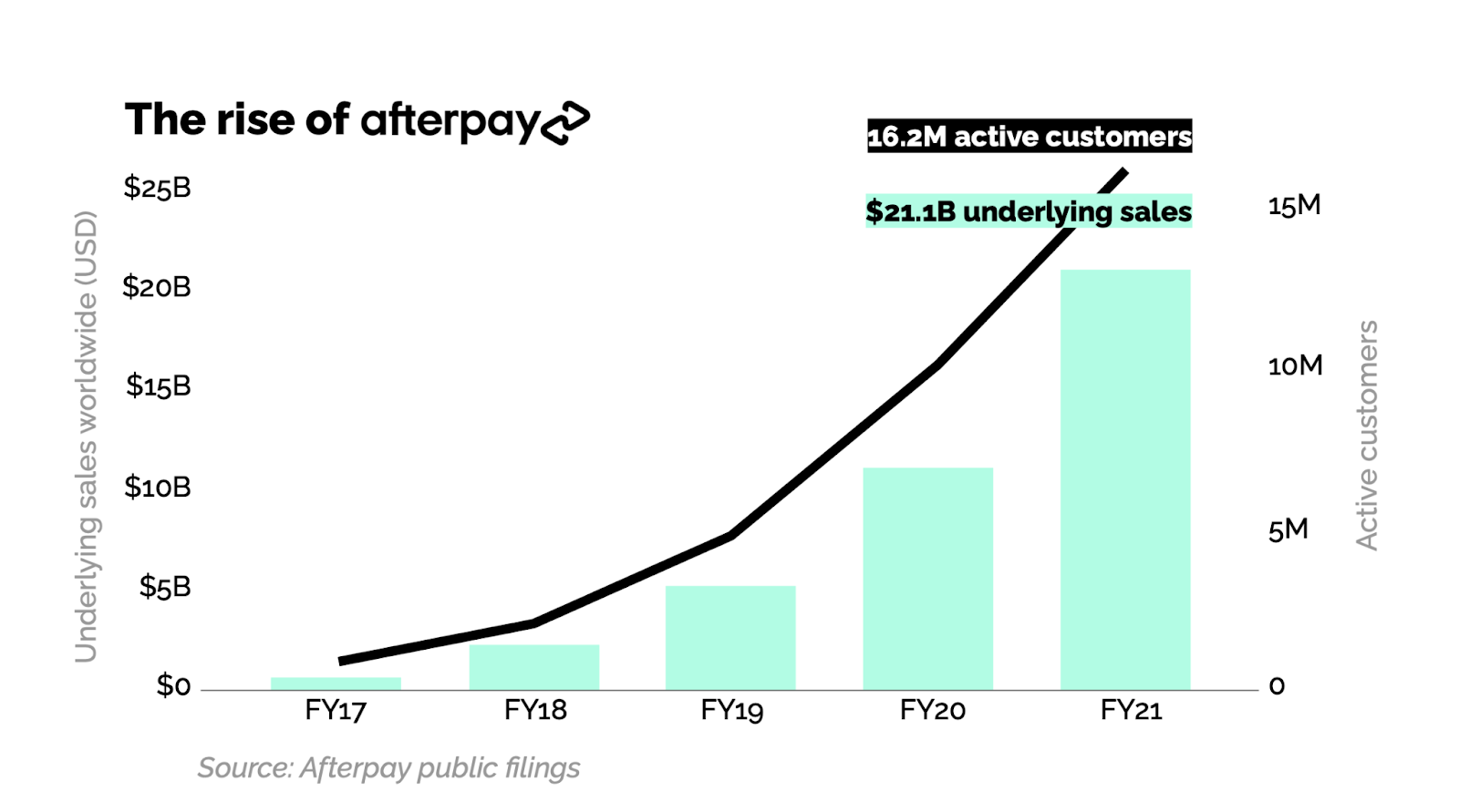

Image Credits: Matrix Partners

Afterpay went somewhat unnoticed outside Australia in 2016 and 2017, but once it came to the U.S. in 2018 and built a business there that broke $100 million net revenues in only its second year, it got attention.

Klarna, which had struggled with product-market fit in the U.S., pivoted their business to emulate Afterpay. And Affirm, which had always been about traditional credit — generating a significant portion of their revenue from consumer interest — also noticed and introduced their own BNPL offering. Then came PayPal with “Pay in 4,” and just a few weeks ago, there has been news that Apple is expected to enter the space.

Afterpay created a global phenomenon that has now become a category embraced by mainstream players across the industry — a category that is on track to take a meaningful share of global retail payments over the next 10 years.

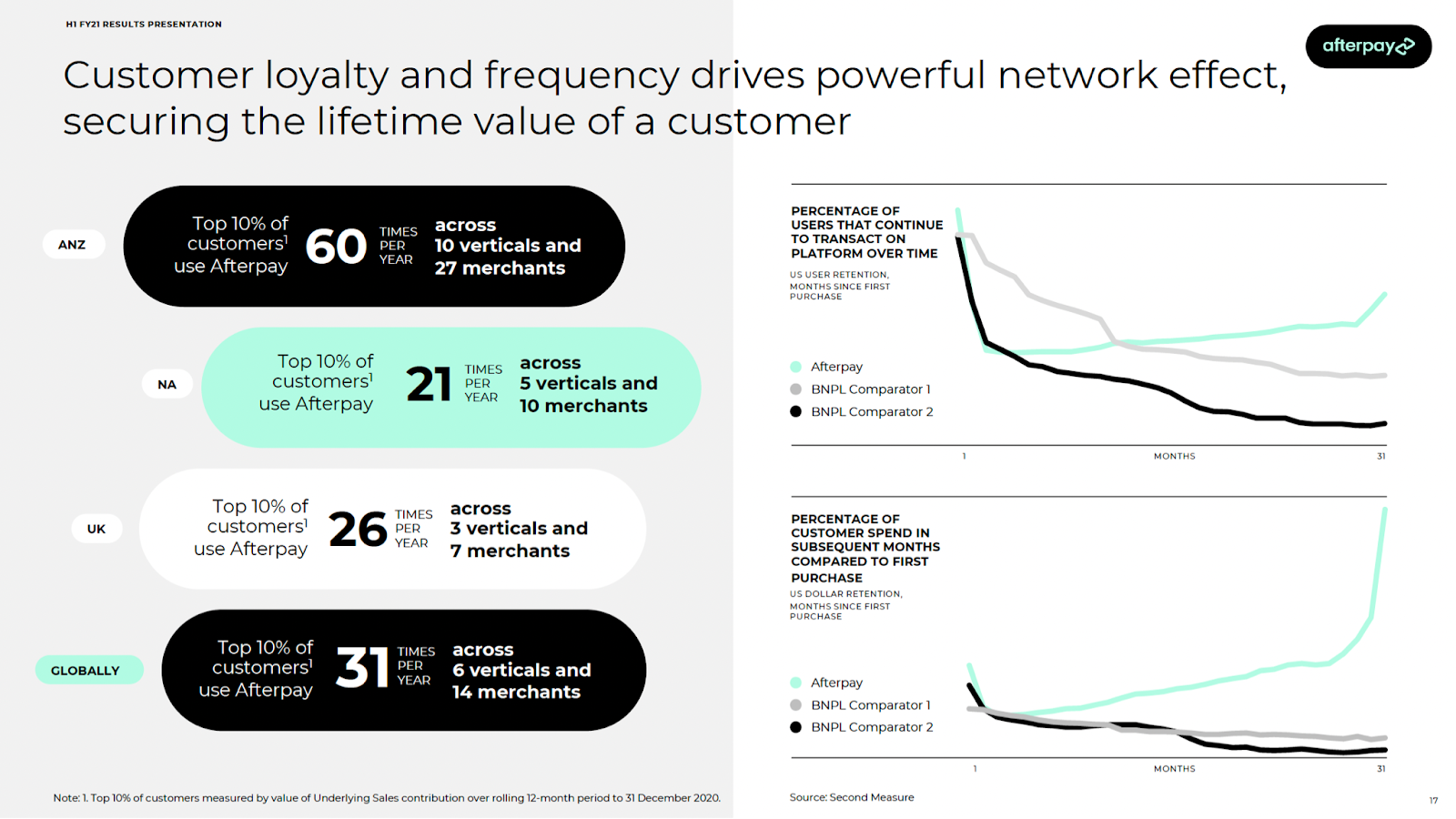

Afterpay stands apart. It has always been the BNPL leader by virtually every measure, and it has done it by staying true to their customers’ needs. The company is great at understanding the millennial and Gen Z consumer. It’s evident in the voice, tone and lifestyle brand you experience as an Afterpay user, and in the merchant network it continues to build strategically. It’s also evident in the simple fact that it doesn’t try to cross-sell users revolving debt products.

Most importantly, it’s evident in the usage metrics relative to competition. This is a product that people love, use and have come to rely on, all with better, fairer terms than were ever available to them than with traditional consumer credit.

Image Credits: Afterpay H1 FY21 results presentation

I’ve been building payment companies for over 15 years now, initially in the early days of PayPal and more recently as a venture investor at Matrix Partners. I’ve never seen a combination that has such potential to deliver extraordinary value to consumers and merchants. Even more so than eBay + PayPal.

Beyond the clear product and network complementarity, what’s most exciting to me and my partners is the alignment of values and culture. Square and Afterpay share a vision of a future with more opportunity and fewer economic hurdles for all. As they build toward that future together, I’m confident that this combination is a winner. Square and Afterpay together will become the world’s next generation payment provider.

Powered by WPeMatico