online retail

Auto Added by WPeMatico

Auto Added by WPeMatico

Flippa, an online marketplace to buy and sell online businesses and digital assets, announced its first venture-backed round, an $11 million Series A, as it sees over 600,000 monthly searches from investors looking to connect with business owners.

OneVentures led the round and was joined by existing investors Andrew Walsh (former Hitwise CEO), Flippa co-founders Mark Harbottle and Matt Mickiewicz, 99designs, as well as new investors Catch.com.au founders Gabby and Hezi Leibovich; RetailMeNot.com founders Guy King and Bevan Clarke; and Reactive Media founders Tim O’Neill and Tim Fouhy.

The company, with bases in both Austin and Australia, was started in 2009 and facilitates exits for millions of online business owners, some that operate on e-commerce marketplaces, blogs, SaaS and apps, the newest data integration being for Shopify, Blake Hutchison, CEO of Flippa, told TechCrunch.

He considers Flippa to be “the investment bank for the 99%,” of small businesses, providing an end-to end platform that includes a proprietary valuation product for businesses — processing over 4,000 valuations each month — and a matching algorithm to connect with qualified buyers.

Business owners can sell their companies directly through the platform and have the option to bring in a business broker or advisor. The company also offers due diligence and acquisition financing from Thrasio-owned Yardline Capital and a new service called Flippa Legal.

“Our strategy is verification at the source, i.e. data,” Hutchison said. “Users can currently connect to Stripe, QuickBooks Online, WooCommerce, Google Analytics and Admob for apps, which means they can expose their online business performance with one-click, and buyers can seamlessly assess financial and operational performance.”

Online retail, as a share of total retail sales, grew to 19.6% in 2020, up from 15.8% in 2019, driven largely by the global pandemic as sales shifted online while brick-and-mortar stores closed.

Meanwhile, Amazon has 6 million sellers, and Shopify sellers run over 1 million businesses. This has led to an emergence of e-commerce aggregators, backed by venture capital dollars, that are scooping up successful businesses to grow, finding many through Flippa’s marketplace, Hutchison said.

Flippa has over 3 million registered users and added 300,000 new registered users in the past 12 months. Overall transaction volume grows 100% year over year. Though being bootstrapped for over a decade, the company’s growth and opportunity drove Hutchison to go after venture capital dollars.

“There is a huge movement toward this being recognized as an asset class,” he said. “At the moment, the asset class is undervalued and driving a massive swarm as investors snap up businesses and aggregate them together. We see the future of these aggregators becoming ‘X company for apps’ or ‘X for blogs.’ ”

As such, the new funding will be used to double the company’s headcount to more than 100 people as it builds out its offices globally, as well as establishing outposts in Melbourne, San Francisco and Austin. The company will also invest in marketing and product development to scale its business valuation tool that Hutchison likens to the “Zillow Zestimate,” but for online businesses.

Nigel Dews, operating partner at OneVentures, has been following Flippa since it started. His firm is one of the oldest venture capital firms in Australia and has 30 companies in its portfolio focused on healthcare and technology.

He believes the company will create meaningful change for small businesses. The team combined with Flippa’s ability to connect buyers and sellers puts the company in a strong leadership position to take advantage of the marketplace effect.

“Flippa is an incredible opportunity for us,” he added. “You don’t often get a world-leading business in a brand new category with incredible tailwinds. We also liked that the company is based in Australia, but half of its revenue comes from the U.S.”

Powered by WPeMatico

Pan-African e-commerce company Jumia filed for an IPO on the New York Stock Exchange today, per SEC documents and confirmation from CEO Sacha Poignonnec to TechCrunch.

The valuation, share price and timeline for public stock sales will be determined over the coming weeks for the Nigeria-headquartered company.

With a smooth filing process, Jumia will become the first African tech startup to list on a major global exchange.

Poignonnec would not pinpoint a date for the actual IPO, but noted the minimum SEC timeline for beginning sales activities (such as road shows) is 15 days after submitting first documents. Lead adviser on the listing is Morgan Stanley .

There have been numerous press reports on an anticipated Jumia IPO, but none of them confirmed by Jumia execs or an actual SEC, S-1 filing until today.

Jumia’s move to go public comes as several notable consumer digital sales startups have faltered in Nigeria — Africa’s most populous nation, largest economy and unofficial bellwether for e-commerce startup development on the continent. Konga.com, an early Jumia competitor in the race to wire African online retail, was sold in a distressed acquisition in 2018.

With the imminent IPO capital, Jumia will double down on its current strategy and regional focus.

“You’ll see in the prospectus that last year Jumia had 4 million consumers in countries that cover the vast majority of Africa. We’re really focused on growing our existing business, leadership position, number of sellers and consumer adoption in those markets,” Poignonnec said.

The pending IPO creates another milestone for Jumia. The venture became the first African startup unicorn in 2016, achieving a $1 billion valuation after a $326 funding round that included Goldman Sachs, AXA and MTN.

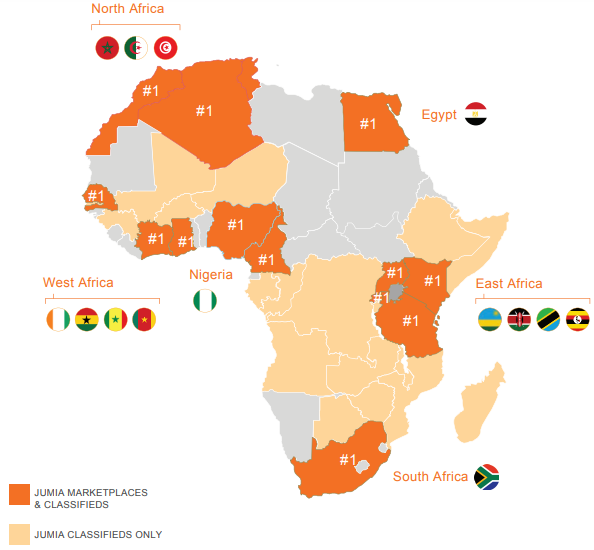

Founded in Lagos in 2012 with Rocket Internet backing, Jumia now operates multiple online verticals in 14 African countries, spanning Ghana, Kenya, Ivory Coast, Morocco and Egypt. Goods and services lines include Jumia Food (an online takeout service), Jumia Flights (for travel bookings) and Jumia Deals (for classifieds). Jumia processed more than 13 million packages in 2018, according to company data.

Starting in Nigeria, the company created many of the components for its digital sales operations. This includes its JumiaPay payment platform and a delivery service of trucks and motorbikes that have become ubiquitous with the Lagos landscape.

Starting in Nigeria, the company created many of the components for its digital sales operations. This includes its JumiaPay payment platform and a delivery service of trucks and motorbikes that have become ubiquitous with the Lagos landscape.

Jumia has also opened itself up to traders and SMEs by allowing local merchants to harness Jumia to sell online. “There are over 81,000 active sellers on our platform. There’s a dedicated sellers page where they can sign-up and have access to our payment and delivery network, data, and analytic services,” Jumia Nigeria CEO Juliet Anammah told TechCrunch.

The most popular goods on Jumia’s shopping mall site include smartphones (priced in the $80 to $100 range), washing machines, fashion items, women’s hair care products and 32-inch TVs, according to Anammah.

E-commerce ventures, particularly in Nigeria, have captured the attention of VC investors looking to tap into Africa’s growing consumer markets. McKinsey & Company projects consumer spending on the continent to reach $2.1 trillion by 2025, with African e-commerce accounting for up to 10 percent of retail sales.

Jumia has not yet turned a profit, but a snapshot of the company’s performance from shareholder Rocket Internet’s latest annual report shows an improving revenue profile. The company generated €93.8 million in revenues in 2017, up 11 percent from 2016, though its losses widened (with a negative EBITDA of €120 million). Rocket Internet is set to release full 2018 results (with updated Jumia figures) April 4, 2019.

Jumia’s move to list on the NYSE comes during an up and down period for B2C digital commerce in Nigeria. The distressed acquisition of Konga.com, backed by roughly $100 million in VC, created losses for investors, such as South African media, internet and investment company Naspers .

In late 2018, Nigerian online sales platform DealDey shut down. And TechCrunch reported this week that consumer-focused venture Gloo.ng has dropped B2C e-commerce altogether to pivot to e-procurement. The CEO cited better unit economics from B2B sales.

In late 2018, Nigerian online sales platform DealDey shut down. And TechCrunch reported this week that consumer-focused venture Gloo.ng has dropped B2C e-commerce altogether to pivot to e-procurement. The CEO cited better unit economics from B2B sales.

As demonstrated in other global startup markets, consumer-focused online retail can be a game of capital attrition to outpace competitors and reach critical mass before turning a profit. With its unicorn status and pending windfall from an NYSE listing, Jumia could be better positioned than any venture to win on e-commerce at scale in Africa.

Powered by WPeMatico

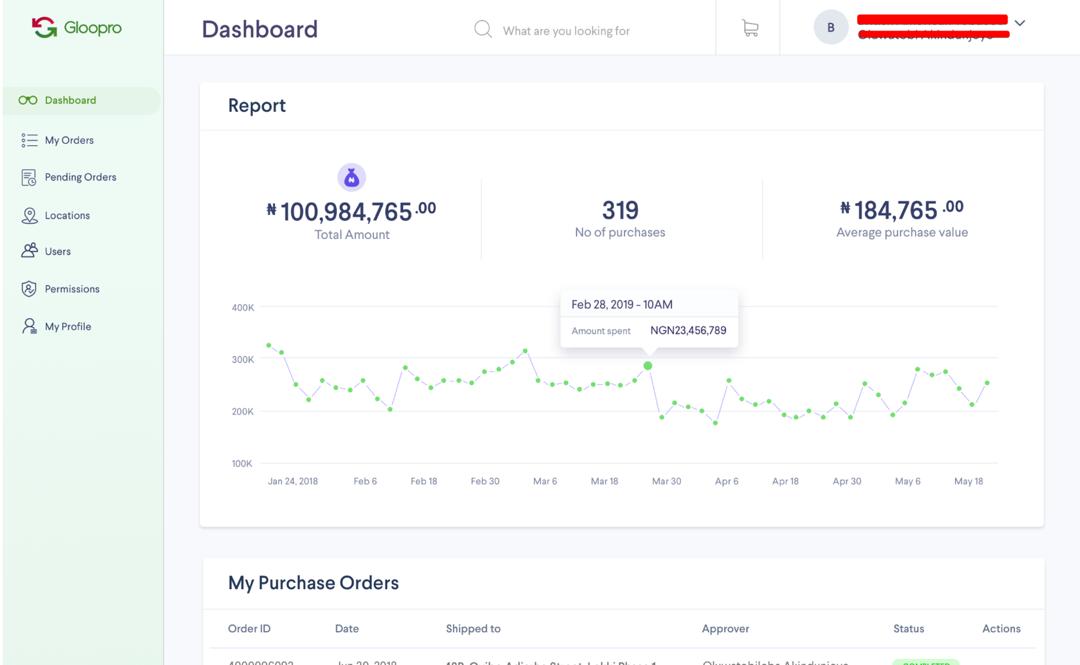

Nigerian startup Gloo.ng is dropping consumer online retail and pivoting to B2B e-procurement with Gloopro as its new name.

The Lagos-based venture has called it quits on e-commerce grocery services, shifting to a product that supplies large and medium corporates with everything from desks to toilet paper.

Gloopro’s new platform will generate revenues on a monthly fee structure and a percentage on goods delivered, according to Gloopro CEO D.O. Olusanya.

Gloopro, which raised around $1 million in seed capital as Gloo.ng, is also in the process of raising its Series A round. The startup looks to expand outside of Nigeria on that raise, “before the end of next year,” Olusanya told TechCrunch.

Gloopro’s move away from B2C comes as several notable consumer digital sales startups have failed to launch in Nigeria — Africa’s most populous nation with the continent’s highest number of online shoppers, per a recent UNCTAD report.

The country is home to the continent’s first e-commerce startup unicorn, Jumia, and serves as an unofficial bellwether for e-commerce startup activity in Africa.

Gloo.ng’s shift to B2B electronic commerce was prompted by Nigeria’s 2016 economic slump and a customer request, according Olusanya.

“When the recession hit it affected all consumer e-commerce negatively. We saw it was going to take a longer time to get to sustainability and profitability,” he told TechCrunch.

Then an existing client, Unilever, requested an e-procurement solution in 2017. “We observed that the unit economics of that business was far better than consumer e-commerce,” said Olusanya.

Gloopro dubs itself as a “secure cloud based enterprise e-procurement and commerce platform…[for]…corporate purchasing,” per a company description.

“The old brand Gloo.ng, is going to be rested and shut down completely. The corporate name will be PayMente Limited with the brand name Gloopro,” Olusanya said.

From the Gloopro interface customers can order, pay for and coordinate delivery of office supplies across multiple locations. The product also produces procurement analytics and allows companies to designate users and permissions.

Olusanya touts the product’s benefits at improving transparency and efficiency in the purchasing process.

“It makes procurement transparent and secure. A lot of companies in Nigeria still use paper invoices and there are some shenanigans,” he said.

Gloopro began offering the service in beta and building a customer base prior to winding down its Gloo.ng grocery service.

In addition to Unilever, Gloopro clients include Uber Nigeria, Cars45 and industrial equipment company LaFarge. Cars45 CEO Etop Ikpe and a spokesperson for Uber Nigeria confirmed their client status to TechCrunch.

Olusanya believes the company can compete with other global e-procurement providers, such as SAP Ariba and GT-Nexus, by “leveraging our sourcing and last-mile delivery experience in Nigeria” and expertise working around local requirements in Africa.

Gloopro expects to hit $4 million in revenue by the end of the year and the company could reach $100 million over the course of its international expansion into countries like South Africa, Kenya, Morocco, Egypt and the Ivory Coast, according to Olusanya. A seed investor briefed on Gloo.ng’s estimates confirmed the company’s revenue expectations with TechCrunch.

Gloo.ng’s pivot to Gloopro and e-procurement comes during an up and down period for B2C online retail in Nigeria, home of Africa’s largest economy.

Last year, e-commerce startup Konga.com, backed by roughly $100 million in VC, was sold in a distressed acquisition, at a loss to investors, including Naspers. In late 2018, Nigerian online sales platform DealDey shut down.

On the possible upside, several outlets reported this year that Jumia — Africa’s largest e-commerce site and first unicorn headquartered in Nigeria — is pursuing an IPO. But that information is unconfirmed based on a February 8, Bloomberg story without named sources. Jumia has declined to comment.

Powered by WPeMatico

Amazon this morning announced the launch of Amazon Cash, a new service that allows consumers to add cash to their Amazon.com balance by showing a barcode at a participating retailer, then having the cash applied immediately to their online Amazon account. The service will support adding any amount between $15 and $500 in a single transaction, Amazon says.

Amazon this morning announced the launch of Amazon Cash, a new service that allows consumers to add cash to their Amazon.com balance by showing a barcode at a participating retailer, then having the cash applied immediately to their online Amazon account. The service will support adding any amount between $15 and $500 in a single transaction, Amazon says.

Amazon Cash will be available at… Read More

Powered by WPeMatico

A key tenet of e-commerce is the recommendation engine. If implemented correctly, it can be a major sales driver for online retailers. However, most sites normally just implement a basic engine that guesses what shoppers want, without any input from the shoppers themselves. Shopping Quizzes has created a recommendation engine that actually asks shoppers what they’re looking… Read More

A key tenet of e-commerce is the recommendation engine. If implemented correctly, it can be a major sales driver for online retailers. However, most sites normally just implement a basic engine that guesses what shoppers want, without any input from the shoppers themselves. Shopping Quizzes has created a recommendation engine that actually asks shoppers what they’re looking… Read More

Powered by WPeMatico

Alongside co-founder and longtime partner Stephan Ango, Jesse Genet has built a business with Lumi that’s already been profitable, and has just raised $9 million in venture funding to boost its growth.

Alongside co-founder and longtime partner Stephan Ango, Jesse Genet has built a business with Lumi that’s already been profitable, and has just raised $9 million in venture funding to boost its growth.