online payments

Auto Added by WPeMatico

Auto Added by WPeMatico

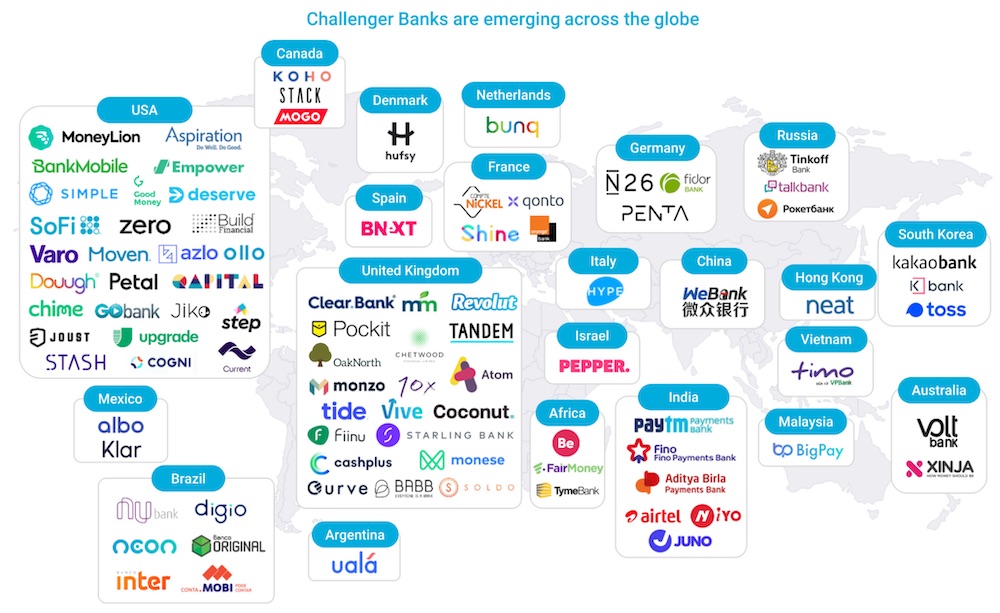

The neobank, or digital bank, phenomenon continues to take the world by storm, with global winners, from Brazil’s Nubank valued at $10 billion and Berlin’s N26 valued at $3.5 billion, to Chime, now valued at $14.5 billion as the most valuable consumer fintech in the United States.

Neobanks have led the charge of the $3.6 billion in venture capital funding for consumer fintech startups this year. And as the coronavirus-fueled acceleration of digital transformation continues, it seems the digital bank is here to stay, with some estimates pointing to neobanks reaching 60 million customers in North America and Europe by the end of 2020, and surpassing 145 million by 2024.

The space is also becoming more crowded, a trend which will only accelerate with fintech eating the world and creating greater infrastructure that enables any company to include a bank account as a product extension.

FT Partners Fintech Industry Research, January 2020

As a result, neobanks are not a monolithic model and not all are created equal. Looking underneath the hood of business models across the globe reveals remarkable operational differences and highlights specific features that are more likely to succeed in the long-term.

Today there are five distinct models that are leading globally:

Interchange-led: Relies on payments revenue, sourced through interchange as the revenue driver. Every time a customer uses the neobank’s card as a payment method they get paid [e.g. Chime / US; Neon (hybrid of 1 & 2) / Brazil].

Credit-led: Leverages a credit-first model, starting off with a credit card or similar offering, and later providing a bank account [e.g. Nubank, Neon (hybrid of 1 & 2) / Brazil].

Powered by WPeMatico

Cryptocurrency exchange Coinbase is adding a new way to withdraw funds from your Coinbase account. If you’ve added a compatible debit card to your account, you can transfer USD, EUR or GBP to your bank account nearly instantly.

There are some drawbacks, and the main one is that you’ll pay a lot of fees. In the U.S., Coinbase deducts 1.5% from the transaction, or a minimum $0.55 if it’s a small transaction. In the U.K. and Europe, you pay 2% in fees or a minimum fee of £0.45/€0.52, respectively.

You also need to have a compatible card. Not all debit cards support incoming transfers. You need to have a Visa card that supports Visa Fast Funds. In the U.S., you can also use a Mastercard card with Mastercard Send.

It’s hard to know whether your bank or card issuer support those features. The best way to figure it out is probably by adding your card to Coinbase and seeing what Coinbase says.

Coinbase isn’t removing other withdrawal methods. For instance, if you’re looking for a cheaper way to withdraw your funds in Europe, a SEPA bank transfer costs €0.15 per transfer. And Coinbase supports instant SEPA transfers if your bank has enabled that.

The company also lets you link your PayPal account with your Coinbase account. Your funds should hit your PayPal account within a few seconds, and there are no fees on Coinbase’s side.

As you can see, there are many ways to move money from your bank account to your Coinbase account. Some of them are slower than others, some of them are more expensive than others. Crypto-to-crypto transactions are a bit simpler by comparison, as you only need your recipient’s wallet address to send tokens.

Image Credits: Coinbase

Powered by WPeMatico

Stripe has led a $12 million Series A round in Manila-based online payment platform PayMongo, the startup announced today.

PayMongo, which offers an online payments API for businesses in the Philippines, was the first Filipino-owned financial tech startup to take part in Y Combinator’s accelerator program. Y Combinator and Global Founders Capital, another previous investor, both returned for the Series A, which also included participation from new backer BedRock Capital.

PayMongo partners with financial institutions, and its products include a payments API that can be integrated into websites and apps, allowing them to accept payments from bank cards and digital wallets like GrabPay and GCash. For social commerce sellers and other people who sell mostly through messaging apps, the startup offers PayMongo Links, which buyers can click on to send money. PayMongo’s platform also includes features like a fraud and risk detection system.

In a statement, Stripe’s APAC business lead Noah Pepper said it invested in PayMongo because “we’ve been impressed with the PayMongo team and the speed at which they’ve made digital payments more accessible to so many businesses across the Philippines.”

The startup launched in June 2019 with $2.7 million in seed funding, which the founders said was one of the largest seed rounds ever raised by a Philippines-based fintech startup. PayMongo has now raised a total of almost $15 million in funding.

Co-founder and chief executive Francis Plaza said PayMongo has processed a total of almost $20 million in payments since launching, and grown at an average of 60% since the start of the year, with a surge after lockdowns began in March.

He added that the company originally planned to start raising its Series A in in the first half of next year, but the growth in demand for its services during COVID-19 prompted it to start the round earlier so it could hire for its product, design and engineering teams and speed up the release of new features. These will include more online payment options; features for invoicing and marketplaces; support for business models like subscriptions; and faster payout cycles.

PayMongo also plans to add more partnerships with financial service providers, improve its fraud and risk detection systems and secure more licenses from the central bank so it can start working on other types of financial products.

The startup is among fintech companies in Southeast Asia that have seen accelerated growth as the COVID-19 pandemic prompted many businesses to digitize more of their operations. Plaza said that overall digital transactions in the Philippines grew 42% between January and April because of the country’s lockdowns.

PayMongo is currently the only payments company in the Philippines with an onboarding process that was developed to be completely online, he added, which makes it attractive to merchants who are accepting online payments for the first time. “We have a more efficient review of compliance requirements for the expeditious approval of applications so that our merchants can use our platform right away and we make sure we have a fast payout to our merchants,” said Plaza.

If the momentum continues even as lockdowns are lifted in different cities, that means the Philippine’s central bank is on track to reach its goal of increasing the volume of e-payment transactions to 20% of total transactions in the country this year. The government began setting policies in 2015 to encourage more online payments, in a bid to bolster economic growth and financial inclusion, since smartphone penetration in the Philippines is high, but many people don’t have a traditional bank account, which often charge high fees.

Though lockdown restrictions in the Philippines have eased, Plaza said PayMongo is still seeing strong traction. “We believe the digital shift by Filipino businesses will continue, largely because both merchants and customers continue to practice safety measures such as staying at home and choosing online shopping despite the more lenient quarantine levels. Online will be the new normal for commerce.”

Powered by WPeMatico

In Indonesia, about half of adults are “underbanked,” meaning they don’t have access to bank accounts, credit cards and other traditional financial services. A growing list of tech companies are working on solutions, from Payfazz, which operates a network of financial agents in small towns, to digital payment services from GoJek and Grab. As a result, financial inclusion is increasing for consumers and small businesses in Southeast Asia’s largest country, but one group remains underserved: schools.

InfraDigital was founded in 2018 by chief executive officer Ian McKenna and chief operating officer Indah Maryani. Both have backgrounds in financial tech, and their platform enables parents to pay school tuition with the same digital services they use for electricity bills or online shopping. The startup currently serves about 400 schools and recently raised a Series A led by AppWorks.

Many Indonesian schools still rely on cash payments, which are often delivered by kids to their teachers.

“My kid had just started school, and one day I spotted my wife giving him an envelope full of cash for tuition. He was only three years old,” McKenna said. “That triggered my curiosity about how these financial systems work.”

To give parents an easier alternative, InfraDigital, which is registered with Indonesia’s central bank, partners with banks, convenience store chains like Indomaret, online wallets and digital payment services like GoPay to allow them to send tuition money online.

“The way you pay your electricity bill, it’s likely that your school is already there, regardless of whether you have a bank account or live in a really remote place” where many people make cash payments for services at convenience stores, McKenna said. The startup is now working on a system for schools in areas that don’t have access to convenience store chains and banks.

Before building InfraDigital’s network, McKenna and Maryani had to understand why many schools still rely on cash payments and paper ledgers to manage tuition.

“Banks have been trying to tap into the education market for a long time, 12 to 15 years probably, but no one has become the biggest bank for schools,” said Maryani. “The reason behind that is because they come in with their own products and they don’t try to resolve the issues schools are facing. Since they are focused on the consumer side, they don’t really see schools or other offline businesses as their customers, and there is a lot of customization that they need to do.”

For example, a school might have 2,000 students and charge each of them about USD $10 a month in school fees. But they also collect separate payments for books, uniforms, and building fees. InfraDigital’s founders say schools typically send out an average of about 2.5 invoices a month.

Digitizing payments also makes it easier for schools to track their finances. InfraDigital provides its clients with a backend application for accounting and enrollment management. It automatically tracks tuition payments as they come in.

“People don’t get paid that much and they are ridiculously busy taking care of thousands of kids. It’s really, really tough,” McKenna said. “When you’re giving them a solution, it’s not about features, it’s not about tools, it’s about the practicalities of their day-to-day life and how we are going to assist them with it. So you remove that burden from them.”

During the COVID-19 pandemic, which resulted in movement restriction orders in different areas of Indonesia, InfraDigital’s founders say the platform was able to forecast trends even before schools officially closed. They started surveying schools in their client base, and sent back data to help them forecast how school closures would affect their income.

“From the school’s perspective, it’s a really damaging situation, with 30% to 60% income drops. Teachers don’t get paid. If the economy goes down, parents at lower-income schools, which are a big part of our client base, won’t be able to pay,” McKenna said. “It’s built into the model, and we’ll continue seeing that however long the economic impact of COVID-19 lasts.”

Powered by WPeMatico

Meet Alma, a French startup that helps you offer a new payment option for your expensive goods. Like Klarna, clients can choose to pay over three or four installments. But the comparison stops here, as Klarna isn’t available in France. Alma just raised a $14.1 million (€12.5 million) funding round.

Idinvest, ISAI and Picus Capital are investing in today’s funding round. Additionally, Alma has opened a $19.2 million (€17 million) credit line to finance merchant payments.

As a merchant, when you integrate Alma in your payment flow, your customers can choose Alma to make it less intimidating. Instead of getting charged when you pay, you can choose to buy now and pay over three or four installments. Merchants get paid instantly.

“We handle risk and cash advance in house,” co-founder and CEO Louis Chatriot told me. “When it comes to the risk of non-payment, we have implemented a series of verifications, filters and algorithms in order to detect fraud and high-risk profiles.”

The company creates multiple categories depending on your profile. It can ask for more information if Alma has some doubts, such as API access to your bank statement. Assessing risk is particularly difficult in France, as there’s no central credit scoring system.

Merchants can choose to pay the processing fees in full — 3.8% of the transaction for a payment in three intallments, 4.2% for a payment in four installments. But they also can share the processing fees with the end customer.

Alma is compatible with most e-commerce platforms, such as Shopify, Magento and Prestashop. Merchants can also offer Alma as a payment option in retail stores.

Over 1,000 merchants are using Alma already — the startup processes tens of millions of euros of transactions per year. Clients include Bobbies, Asphalte, Cowboy, Weebot, The Cool Republic and The Socialite Family.

With today’s funding round, the company wants to attract more merchants and launch two new payment options — pay later and a more traditional option to pay now. In addition to that, Alma currently redirects customers to its own checkout page. The startup wants to integrate its payment widget directly on e-commerce websites.

Powered by WPeMatico

It didn’t take much for the founders of Cora, Brazil’s newest startup to tackle some aspect of the broken financial services industry in the country, to raise their first $10 million.

Igor Senra and Leo Mendes had worked together before — founding their first online payments company, MOIP, in 2005. That company sold to WireCard in 2016 and after three years the founders were able to strike out again.

They built their initial business servicing the small and medium-sized businesses that make up roughly two-thirds of the Brazilian economy and represent some trillion dollars’ worth of transactions. But at WireCard, they increasingly were told to approach larger customers that didn’t have the same kind of demand for their services, according to Mendes.

So they built Cora — a technology-enabled lender to the small and medium-sized businesses that they knew so well.

The round was led by Kaszek Ventures, one of Latin America’s largest and most successful investment funds, with participation from Ribbit Capital — one of the most influential early-stage fintech investment firms globally.

“We created Cora to pursue our life purpose, which is to solve the financial problems faced by small and medium businesses. These businesses

The company is currently operating in closed beta and plans to launch its first product, a free SME-only mobile account, in the first half of 2020, according to the statement. Cora will later release a portfolio of payments, credit-related products and financial management tools that are currently being developed.

“So far, large financial institutions have mainly built products that focus either on individuals or on large corporate clients and have totally ignored small and medium sized enterprises, who are the most relevant creators of value in our economies,” said Mendes in a statement. “We want to offer a high-quality, customer-centric suite of financial products that addres

Powered by WPeMatico

Flipkart, the largest e-commerce platform in India, said Tuesday it has concluded the roll-out of a range of features to its shopping app in what is its biggest update in recent years.

Chief among these new features is access to Flipkart in Hindi language. Prior to the revamp of the app, Flipkart was available only in English, a language spoken by 10% of India’s 1.3 billion population.

Flipkart says it is hoping that the new features, which includes a video streaming service, would help it reach the next 200 million users in India.

The major bet on Hindi, a language spoken by more than 500 million people in India, illustrates a growing push from local and international companies operating in the country as they adapt their services and business models to go beyond the urban cities.

And that’s where much of the opportunity, which countless startups and companies have trumpeted to investors to successfully raise hundreds of millions of dollars in debt and venture capital in recent years, lies in the nation.

Powered by WPeMatico

The latest pairing between a tech upstart and a financial titan is a digital prepaid card targeted at Southeast Asia’s 430 million-plus unbanked and underserved population.

On Monday, Razer, the Singapore-based company best known for its gaming laptops and peripherals, announced a partnership with Visa to develop a Visa prepaid solution. The service, which allows unbanked users to top up and cash out easily, will be available as a mini program embedded in Razer Pay, the gaming company’s mobile payments app. That means Razer’s 60 million registered users will be able to pay at any of the 54 million merchant locations around the world that take Visa.

Going virtual is the natural step given the region’s fast-growing digital population, but the pair does not rule out the possibility to introduce a physical prepaid card down the road, Razer’s chief strategy officer Li Meng Lee told TechCrunch over a phone interview.

Both parties have something to gain from this marriage. Hong Kong-listed Razer has in recent years been doubling down on fintech to prove it’s more than a hardware company. Payment services seem like an inevitable development for Razer whose users in the region are accustomed to buying in-game credits at convenience stores.

“For many years, the people who have been making digital payments before it became a sexy word in the last couple of years… [many of them] are the gamers who go to a 7-Eleven, pay in cash, and get a pin code to buy virtual skins for the games,” noted Lee. “Because of that, we’ve been able to build up more than a million service points across Southeast Asia.”

The key differentiator of Razer’s prepaid service, Lee said, is that customers paying at Visa merchants don’t have to already own a bank account, whereas that prerequisite is common for many other e-wallet services.

Razer’s fintech arm Pay is handling transactions for a slew of internet services like Lazada and Grab and has made a big offline push, boasting a network of more than one million touchpoints through retailers including 7-Eleven and Starbucks where it’s accepted.

All in all, Razer claimed it processed over $1.4 billion in payment value last year — but that includes its “merchant services” business, covering on and offline payments, as well as Razer Pay.

The payment app first launched in Malaysia in mid-2018 and recently branched into Singapore as its second market. Lee said the service plans to roll out in the rest of Southeast Asia soon, upon which the Visa prepaid mini app will also be available in those markets.

For Visa, the tie-up with an internet firm could be a potential boost to its reach in the mobile-first Southeast Asia where some 213 million millennials and youths live.

“This is a great opportunity for us to be working with Razer in addressing how we work to bring the unbanked and underserved population into the financial system,” Chris Clark, Visa’s regional president for the Asia Pacific, told TechCrunch. “We will be doing some work with Razer on financial literacy and financial planning to bring that education to the population across the region.”

Razer’s fintech ambition has been evident since it announced to gobble up MOL, a company that offers online and offline payments in Southeast Asia, in April 2018. Besides payments, Lee said other microfinance services such as lending and insurance are also on the cards as part of an effort to ramp up user stickiness for Razer’s fintech arm.

Note: The original version of this article has been updated to correct that Razer’s $1.4 billion in GMV includes merchant services as well as Razer Pay.

Powered by WPeMatico

One of China’s most ambitious artificial intelligence startups, Megvii, more commonly known for its facial recognition brand Face++, announced Wednesday that it has raised $750 million in a Series E funding round.

Founded by three graduates from the prestigious Tsinghua University in China, the eight-year-old company specializes in applying its computer vision solutions to a range of use cases such as public security and mobile payment. It competes with its fast-growing Chinese peers, including the world’s most valuable AI startup, SenseTime — also funded by Alibaba — and Sequoia-backed Yitu.

Bloomberg reported in January that Megvii was mulling to raise up to $1 billion through an initial public offering in Hong Kong. The new capital injection lifts the company’s valuation to just north of $4 billion as it gears up for its IPO later this year, sources told Reuters.

China is on track to overtake the United States in AI on various fronts. Buoyed by a handful of mega-rounds, Chinese AI startups accounted for 48 percent of all AI fundings in 2017, surpassing those in the U.S. for the first time, shows data collected by CB Insights. An analysis released in March by the Allen Institute for Artificial Intelligence found that China is rapidly closing in on the U.S. by the amount of AI research papers published and the influence thereof.

A critical caveat to China’s flourishing AI landscape is, as The New York Times and other publications have pointed out, the government’s use of the technology. While facial recognition has helped the police trace missing children and capture suspects, there have been concerns around its use as a surveillance tool.

Megvii’s new funding round arrives just days after a Human Rights Watch report listed it as a technology provider to the Integrated Joint Operations Platform, a police app allegedly used to collect detailed data from a largely Muslim minority group in China’s far west province of Xinjiang. Megvii denied any links to the IJOP database per a Bloomberg report.

Kai-Fu Lee, a world-renowned AI expert and investor who was Google’s former China head, warned that any country in the world has the capacity to abuse AI, adding that China also uses the technology to transform retail, education and urban traffic among other sectors.

Megvii has attracted a rank of big-name investors in and outside China to date. Participants in its Series E include Bank of China Group Investment Limited, the central bank’s wholly owned subsidiary focused on investments, and ICBC Asset Management (Global), the offshore investment subsidiary of the Industrial and Commercial Bank of China.

Foreign backers in the round include a wholly owned subsidiary of the Abu Dhabi Investment Authority, one of the world’s largest sovereign wealth funds, and Australian investment bank Macquarie Group.

Megvii says its fresh proceeds will go toward the commercialization of its AI services, recruitment and global expansion.

China has been exporting its advanced AI technologies to countries around the world. Megvii, according to a report by the South China Morning Post from last June, was in talks to bring its software to Thailand and Malaysia. Last year, Yitu opened its first overseas office in Singapore to deploy its intelligence solutions to partners in Southeast Asia. In a similar fashion, SenseTime landed in Japan by opening an autonomous driving test park this January.

“Megvii is a global AI technology leader and innovator with cutting-edge technologies, a scalable business model and a proven track record of monetization,” read a statement from Andrew Downe, Asia regional head of commodities and global markets at Macquarie Group. “We believe the commercialization of artificial intelligence is a long-term focus and is of great importance.”

Powered by WPeMatico

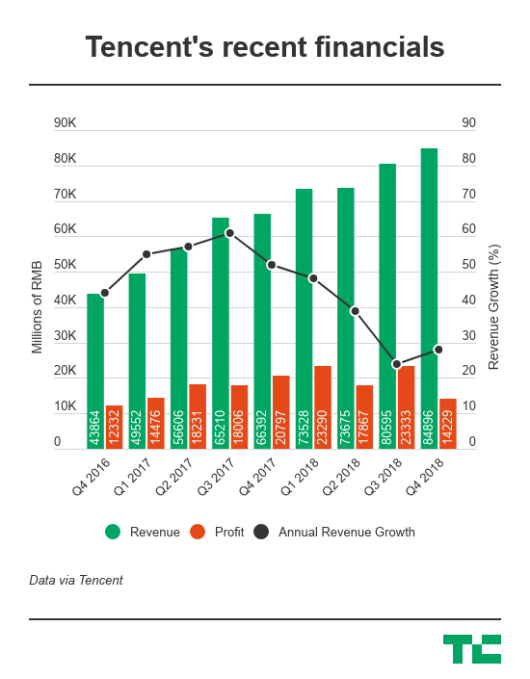

China’s Tencent reported disappointing profits in the fourth quarter on the back of surging costs but saw emerging businesses pick up steam as it plots to diversify amid slackening gaming revenues.

Net profit for the quarter slid 32 percent to 14.2 billion yuan ($2.1 billion), behind analysts’ forecast of 18.3 billion yuan. The decrease was due to one-off expenses related to its portfolio companies and investments in non-gaming segments like video content and financial technology.

Excluding non-cash items and M&A deals, Tencent’s net profit from the period rose 13 percent to 19.7 billion yuan ($2.88 billion). The company has to date invested in more than 700 companies, 100 of which are valued over $1 billion each and 60 of which have gone public.

Quarterly revenue edged up 28 percent to 84.9 billion yuan ($12.4 billion) beating expectations.

The Hong Kong-listed company is best known for its billion-user WeChat messenger but had for years relied heavily on a high-margin gaming business. That was until a months-long freeze on games approvals last year that delayed monetization for new titles, spurring a major reorg in the firm to put more focus on enterprise services, including cloud computing and financial technology.

Tencent has received approvals for eight games since China resumed the licensing process, although its blockbusters PlayerUnknown Battlegrounds and Fortnite have yet to get the green light. The firm also warned of a “sizeable backlog” for license applications in the industry, which means its “scheduled game releases will initially be slower than in some prior years.”

Video games for the quarter contributed 28.5 percent of Tencent’s total revenues, compared to 36.7 percent in the year-earlier period. Despite the domestic fiasco, Tencent remains as the world’s largest games publisher by revenue, according to data compiled by NewZoo. The firm has also gotten more aggressive in taking its titles global.

Social network revenues rose 25 percent on account of growth in live streaming and video subscriptions. The segment made up 22.9 percent of total revenues. Tencent has in recent years spent heavily on making original content and licensing programs as it competes with Baidu’s iQiyi video streaming site. Tencent claimed 89 million subscribers in the latest quarter, compared with iQiyi’s 87.4 million.

Tencent has been relatively slow to monetize WeChat in contrast to its western counterpart Facebook, though it’s under more pressure to step up its game. Tencent’s advertising revenue from the quarter grew 38 percent thanks to expanding advertising inventory on WeChat. Ads accounted for 20 percent of the firm’s quarterly revenues.

All told, WeChat and its local version Weixin reached nearly 1.1 billion monthly active users; 750 million of them checked their friends’ WeChat feeds, and Tencent recently introduced a Snap Story-like feature to lock users in as it vies for eyeball time with challenger TikTok.

The “others” category, composed of financial technology and cloud computing, grew 71.8 percent to generate 28.5 percent of total revenues. WeChat’s e-wallet, which is going neck-and-neck with Alibaba affiliate Alipay, saw daily transaction volume exceed 1 billion last year. During the fourth quarter, merchants who used WeChat Pay monthly grew more than 80 percent year-over-year.

Meanwhile, cloud revenues doubled to 9.1 billion yuan in 2018, thanks to Tencent’s dominance in the gaming sector as its cloud infrastructure now powers over half of the China-based games companies and is following these clients overseas. Tencent meets Alibaba head-on again in the cloud sector. For comparison, Alibaba’s most recent quarterly cloud revenue was 6.6 billion yuan. Just yesterday, the e-commerce leader claimed that its cloud business is larger than the second to eight players in China combined.

Powered by WPeMatico