online marketplace

Auto Added by WPeMatico

Auto Added by WPeMatico

VertoFX, an Africa and emerging markets-focused currency trading and payment startup, has raised a $2.1 million seed round, led by Accelerated Digital Ventures.

The London-based company, with a subsidiary in Lagos, Nigeria, has created a platform that allows businesses and banks to exchange and make payments in exotic foreign currencies that don’t often convert or trade conveniently across businesses or banks.

For example, South Africa’s Rand is Africa’s most convertible and traded currency — with lower spreads and transaction costs — while currencies of countries such as Ethiopia or Egypt may be difficult or expensive to trade or transact B2B payments.

“That’s the reason we are utilizing technology to create a marketplace model and price discovery to create liquidity for these currencies,” VertoFX founder Ola Oyetayo told TechCrunch.

There are around 40 global currencies that are considered exotic or illiquid, most of them in frontier markets in Asia, Africa and the Middle-East, according to Oyetayo.

And there’s a revenue opportunity to creating a convenient online marketplace for trading and payments in these currencies.

And there’s a revenue opportunity to creating a convenient online marketplace for trading and payments in these currencies.

“Our research says there’s about $400 billion being done by small and medium-scale businesses in Africa alone in transactional volume on an annual basis. If we take 1% of that as a commission or transaction fee, that’s a $4 billion addressable market, just in the continent,” said Oyetayo.

VertoFX was founded in 2017 by Oyetayo and Anthony Oduwole — both ex-global bankers born in Nigeria. The company was part of Y Combinator’s 2019 winter cohort and processed around $7 million in transaction volume last month, according to Oyetayo.

VertoFX was founded in 2017 by Oyetayo and Anthony Oduwole — both ex-global bankers born in Nigeria. The company was part of Y Combinator’s 2019 winter cohort and processed around $7 million in transaction volume last month, according to Oyetayo.

VertoFX is registered as a payment services provider with the U.K.’s Financial Conduct Authority. Current clients include several undisclosed banks and San Francisco-based payment venture Flutterwave.

VertoFX doesn’t release revenue figures, but confirmed it earns a commission, or spread, on each transaction processed on its platform. There are currently 19 currencies on the platform and the ability to settle in 120 countries, including China and the U.S.

VertoFX is also moving into offering market research — toward potential subscription services — on the currencies it trades, according to Oyetayo.

The startup will use the round for platform development, expanding the currencies and gaining licenses in new countries. “We’ll also use the round for hiring, primarily in compliance and regulator type roles,” said Oyetayo. VertoFX already has a developer team in India and is looking at local developer talent for its Africa offices.

ADV’s Ryan Proctor confirmed the VC firm’s lead on the investment round, which also included participation from YC and several local angel investors in Africa, Oyetayo told TechCrunch.

On the possibility of becoming acquired by a big bank, VertoFX isn’t so interested, according to Oyetayo.

“We both come from big banks and if we’d wanted to go down that route we’d have developed this more as a software as a service platform,” he said.

“We’re playing the long game here, and I don’t think acquisition is the end game,” he said.

Powered by WPeMatico

The RealReal, an online retailer for authenticated luxury consignment, has authorized the sale of up to $70 million in new shares, per a Delaware stock authorization filing discovered by the Prime Unicorn Index. If the company raises the entire amount, it would reach a valuation of $1.06 billion, cementing its status as the newest e-commerce unicorn.

The filing doesn’t guarantee The RealReal will sell the full amount of authorized shares. The company declined to comment on its fundraising plans.

The RealReal is led by founder and chief executive officer Julie Wainwright (pictured), the former CEO of Pets.com, a company now synonymous with the dot-com bust. It has raised quite a bit of capital to date — a total of $288 million from venture capital and private equity backers, including Great Hill Partners, Sandbridge Capital, PWP Growth Equity, Industry Ventures, Greycroft Partners and Canaan Partners. Most recently, The RealReal closed a Series G financing of $115 million in July 2018 that valued the business at $745 million, per PitchBook.

The RealReal has recently expanded its brick-and-mortar footprint and added additional e-commerce fulfillment centers as demand increased for its supply of second-hand luxury items. Founded in 2011, the company operates eight luxury consignment offices, where customers can receive free valuations of their luxury items. The RealReal is headquartered in San Francisco.

In a conversation with TechCrunch in 2017, Wainwright confirmed the company’s intent to go public at some point. With this upcoming round, The RealReal would be well placed for a 2020 initial public offering.

“That’s the goal,” Wainwright said during the interview. “We really aren’t in the mood to sell the business, we’re in the mood to go public at some point in the future.”

The RealReal competes with fellow second-hand e-tailers ThredUp and Poshmark . The latter is gearing up for a fall IPO, according to The Wall Street Journal. The online marketplace has tapped Morgan Stanley and Goldman Sachs to lead its offering after closing in on $150 million in revenue in 2018. ThredUp, another major player in the fashion retail market, hasn’t raised capital since 2015, but did begin opening physical stores in 2017 as part of its greater effort to compete with fellow venture-backed second-hand e-tailers.

The RealReal would also be the latest in a series of high-profile female-founded companies to gain unicorn status. Glossier tripled its valuation to $1.2 billion with a $100 million round earlier this year, followed by Rent the Runway, which attracted a $125 million investment at a $1 billion valuation, to name a few.

Powered by WPeMatico

SoftBank’s Vision Fund is taking a bet on China’s auto market after it agreed to pour $1.5 billion into online car trading group Chehaoduo, which literally means “many cars” in Chinese.

The Beijing-based company operates two main sites — peer-to-peer online marketplace Guazi for used vehicles, and Maodou, which retails new sedans through direct sales and financial leasing. (These sub-brands are more subtly named; they translate to “sunflower seeds” and “edamame,” respectively.)

Chehaoduo said it will deploy the proceeds on technology investments as well as the development of new products and services. It also plans to ramp up its marketing efforts and continue to open brick-and-mortar stores, an omnichannel move it believes can enhance trust in consumers used to meeting dealers in person and differentiate it from peers with an exclusively online focus. Chehaoduo currently runs 600 offline stores nationwide supporting new and used car dealing along with after-sales services.

The sizable funding round arrived at a time when China’s softening economy is sapping consumer confidence, but the company’s two-pronged strategy makes sure it covers a broad range of consumer demands. New passenger car sales in China — the world’s largest auto market — fell for the first time since the 1990s to 23.7 million units last year, according to a report by China’s Association of Automobile Manufacturers, the country’s top auto association.

On the other hand, used cars became a more economical choice in a consumer culture that, unlike many countries in the west, has been slow to embrace second-hand goods. But that mindset is shifting as people feel the heat of the Chinese economic downturn: Secondhand car sales were up 13 percent during the first 11 months of 2018, data from China’s Automobile Dealers Association show.

“China’s used car market is growing rapidly but online penetration remains low and auto financing is underutilized compared to developed markets. In just three years, Chehaoduo Group, through the Guazi brand, has leveraged the latest innovations in data-driven technology to establish China’s leading car trading platform,” says Eric Chen, partner at SoftBank’s Investment Advisers, in a statement.

The Japanese investment group has been a prolific backer in the mobility industry through a variety of affiliated companies with Vision Fund being one. SoftBank’s massive portfolio includes the likes of Uber, Didi Chuxing and Grab .

Chehaoduo counts Uxin and Renrenche as its most serious rivals. Uxin raised $225 million from a U.S. initial public offering last June while Renrenche lured Goldman Sachs in a $300 million funding round last year that also saw participation from Didi and Tencent.

Powered by WPeMatico

Despite its “unsexy” reputation, the logistics industry is attracting massive investment from venture capitalists.

With a fresh $97 million in Series C funding, NEXT joins a fleet of heavily funded logistics platforms, including Flexport, Huochebang and Convoy. The company, which connects shippers and carriers through an online marketplace, raised the capital from Brookfield Ventures, with participation from Sequoia Capital and logistics solutions provider GLP. NEXT declined to disclose the valuation or whether its latest financing included debt.

In 2018, global logistics startups collected more than $6 billion in VC funding, nearly double the $3.2 billion invested in the space the year prior, according to PitchBook. A significant portion of the 2018 capital went to Chinese ventures at about 40 percent. U.S. logistics businesses raised 19 percent, or about $1.2 billion, across 114 deals.

“The logistics space is under more pressure than ever before — with more shipments coming into our ports than drivers and warehouses have the capacity to manage,” NEXT co-founder and chief executive officer Lidia Yan said in a statement.

NEXT was founded in 2015 by Yan and her husband Elton Chung. The round brings the business’s total raised to $125 million, including a $21 million round in January 2018.

Headquartered in Lynwood, California, NEXT plans to use the investment to fill 150 positions in 2019, as well as complete the launch of Relay, a new service targeting the “systemic congestion” at shipping ports.

“NEXT continues to address the critical issues that face logistics management in the U.S. — from the nationwide driver shortage to congestion and operations at our busiest ports,” Sequoia partner Omar Hamoui said in a statement. “We’ve been impressed with NEXT’s ability to execute, and the introduction of Relay proves they have the team and expertise to continue innovating in ways that will ease the pain points of carriers and shippers.”

Powered by WPeMatico

CAVU Venture Partners has led the $20 million Series B for Once Upon a Farm, which sells organic, cold-pressed baby food in 8,500 grocery stores in the U.S.

The Berkeley-based startup was originally founded in 2015 by serial entrepreneurs Cassandra Curtis and Ari Raz. Today, it lists actress Jennifer Garner and former General Mills president John Foraker as co-founders, too.

Both Garner and Foraker — who was the chief executive officer of the popular organic mac & cheese brand Annie’s Homegrown for more than a decade — joined the company in September 2017. Foraker had been an angel investor in Once Upon a Farm and, after conversations with Garner, decided to accept the role of CEO. Garner, widely known for her roles in Alias, 13 Going on 30 and the upcoming HBO original series Camping, was already somewhat of a Once Upon a Farm evangelist when she signed on as chief brand officer a little over a year ago.

“I am proud of the innovative business that we have built,” Garner said in a statement. “It is incredibly exciting to see so many families embracing our products. This latest round of funding allows us to continue to help busy parents give their children the most nutritious foods possible and make life a little bit easier for families across the country.”

Foraker told TechCrunch that since he and Garner joined, the business has grown 10x. Last fall, the company’s products were for sale in 300 stores; today, as mentioned, they are available in more than 8,000.

“Because she has global celebrity, the power of that, she can really help us get the message out and help lots of moms and dads find [Once Upon a Farm],” Foraker said.

Once Upon a Farm sells smoothies and applesauce for kids up to age 12 directly to consumers through its online marketplace and in stores. Pouches of its signature baby food, smoothies and applesauce are $2.99 each.

As part of the deal, CAVU’s co-founder and managing partner Brett Thomas, along with CAVU investor Jared Jacobs, will join the company’s board. S2G Ventures and Beechwood Capital also participated in the round for the startup, which raised a $4 million Series A in June 2017.

The company plans to use the funds to expand its direct to consumer business, partner with more U.S. grocers and build out a wider assortment of baby products.

“You can buy fresh pet food now in almost 20,000 stores in the U.S.,” Foraker said. “We think fresh baby food has a long way to go.”

Powered by WPeMatico

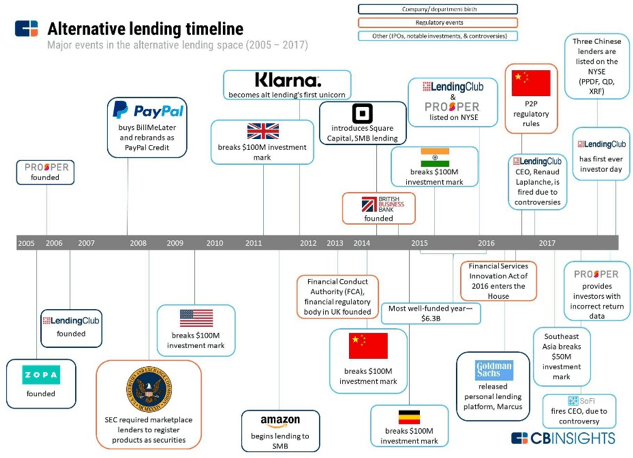

Renaud Laplanche spent ten years building LendingClub. In the process, he created an industry from scratch. Circumventing conventional banking channels for consumer credit began in 1996 when Chris Larsen started E-LOAN, which ultimately led to Prosper Marketplace. But LendingClub, which Laplanche founded in 2007, was and remains the poster child for the business of marketplace lending. The industry’s short history has been volatile, characterized by both triumphant hype and utter lack of confidence.

History of the Marketplace Lending Industry, CB Insights

While LendingClub has struggled in the public markets since their late 2014 IPO, they have managed to propel their industry into significance, while rapidly expanding their share of the personal loan market to 10%.

After his well-publicized departure in May 2016, Laplanche got started on his next venture in a hurry. Just a few months later he started Credify, ultimately renamed to Upgrade, a company that bears a striking resemblance to LendingClub. In just two years Upgrade has raised $142 million in funding, while originating more than $1 billion in loans since August 2017.

With Upgrade, Laplanche has the opportunity to start fresh with the benefit of hindsight. The initial promise of LendingClub and their competitors was unbundling the banks. Now, to persist and grow, marketplace lenders have realized they need to rebundle, providing an array of bank-like services to better serve their end customers. This post explores what Laplanche is doing differently this time with Upgrade.

There has been a general recognition across many fintech businesses that marketplace business models aren’t enough. The mutually-beneficial arrangement of marketplace lending is a perfect example. Superior customer experience, expedited loan decision, quick receipt of funds, and lower operational costs without legacy infrastructure were the selling points. Charles Moldow famously called it a “trillion-dollar opportunity” in 2014.

He may still be right, but in order to realize the opportunity, marketplace lenders need to capture a larger, more regular share of borrower’s attention. Loans may be high-volume purchases, but they’re not high-frequency transactions. So when a platform like LendingClub facilitates a loan so someone can refinance their outstanding credit card debt, is there really a relationship with the customer there? Capital is provided, customer service is available, and monthly payments are made. That’s all there is to it.

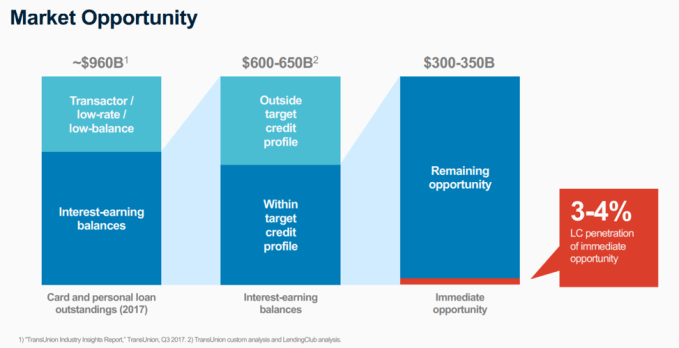

Total addressable market (TAM) is frequently used to assess opportunity. A critical part of the TAM estimation process might have been overlooked in the early assessments of the alternative lending industry. The large numbers in the figure below reflect an alluring market that LendingClub, Prosper, Avant, Upstart, OneMain, Best Egg and others have attempted to capitalize upon.

The notion of a replacement cycle, which I’ll borrow from Michael Mauboussin, is an important consideration here, particularly in a high volume, low frequency transaction relationship such as consumer lending. Just because a borrower refinances their credit card debt with a loan from LendingClub, there’s little guarantee that all of the money spent on acquiring that customer will lead to future transactions with that customer. Yet, in order for these companies to succeed, the average revenue per user (ARPU) is going to have to rise through some combination of repeat customers and complementary services to deepen the relationship and create new revenue channels.

The market opportunity for marketplace Lenders, LendingClub Investor Day 2017

With this realization in mind, fintech players across the board have focused on deepening relationships with customers to drive sales and lower SG&A costs. Customer acquisition is a major component of the income statement for these companies. The more engagement a lender has with their end customer, the greater the chance they stand to not only be called upon when a borrower needs to borrow again, but ultimately pinpoint opportunities for product recommendations.

And that’s exactly what Upgrade is doing. In many ways, they’re quite similar to LendingClub. Upgrade offers personal loans between $1,000 and $50,000 over three-to-five-year repayment periods at rates competitive with major banks. LendingClub varies a bit in the principal amount offerings and APRs, but they essentially do the same thing. Loans are originated through WebBank, the partner bank that also works with LendingClub. Operationally, there’s a blockchain component for data remediation and security purposes. However, the extent and value of this application are unclear.

The notion of financial wellness is increasingly popular among consumer fintech companies, as well as incumbent financial institutions. It reflects a transition away from a purely transactional relationship to a fiduciary one, as we’ve also seen in the wealth management industry. The tricky thing about this is that although it may be the right thing to do, late fees and overdraft penalties make up a sizeable portion of traditional bank revenue.

Where Upgrade differs from LendingClub is in their customer engagement model. Upgrade provides several features to customers that resemble a conventional personal financial management (PFM) app. Their Credit Health service offers free advice and monitoring tools, personalized recommendations, and customized updates for individual credit scores and underlying rationale. Additionally, they offer a financial education tool open to the public called Credit Health Insights, which offers tips and tricks for debt management and financial wellness. At the surface, there’s little differentiation here. A free credit score is becoming table stakes for any financial institution, and personalized insights are to be expected.

Upgrade’s borrower value proposition, LendIt 2018 Conference

In Upgrade’s case, however, the framing of the dual service is compelling. Typically, online lenders only approve 10-15% of applicants. While the credit underwriting models are looking for the most compelling borrower profiles who will pay back their loans, the majority of interested borrowers are sent back to the drawing board.

A major focus of Upgrade is to build the credit of the other 85-90% of applicants who are typically rejected so that they improve their profile and obtain a loan in the future. Credit repair and financial wellness are underserved markets today, although companies like Bloom Credit are working to change the record. This product combination helps to unify the interests of Upgrade and borrowers, both approved and rejected.

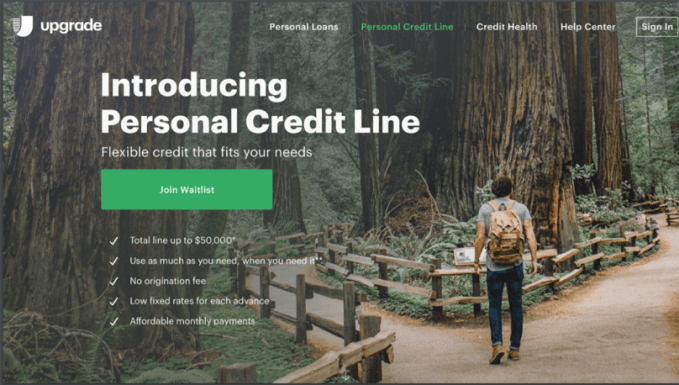

At the LendIt Conference in 2017, Laplanche concluded his presentation with a reference to the Wright Brothers. He discussed how he was enamored with their ability to combine two things to create something entirely new, which in their case was “wheeling and flying.” A year later, he returned to LendIt with a new product release that borrowed from the innovation strategy of Orville and Wilbur.

Upgrade launched a first of its kind product, a Personal Credit Line, a hybrid of a credit card and an unsecured loan. Here’s how it works: customers get approved for up to $50,000 in credit, from which they can draw down as needed. They only pay interest on what’s borrowed, over the course of a 12-60-month timeframe. The interest rate is also fixed over the term of the loan.

Upgrade’s Personal Credit Line, a hybrid of a personal loan and a credit card, Upgrade

The product is built on the premise that the level of innovation in the origination of consumer credit has been somewhat limited. Laplanche attempted to reinvent it once with the creation of LendingClub. In some ways, it worked. Personal loans originated by fintech lenders account for roughly a third of outstanding consumer loans according to Transunion. Now he’s trying to do it again.

When I first read the press release for the Personal Credit Line, I thought it was a very compelling way to expand the menu of options to qualified consumers. It puts more control in the hands of the borrower, so they can avoid the vicious cycle of consumer debt. I was also reminded of a comment made by Josh Brown, CEO of Ritholtz Wealth Management, after Wealthfront released their “Portfolio Line of Credit” product in April 2017. He said that while it might sound flashy, there’s nothing holding Schwab or Fidelity back from offering the same product tomorrow.

What’s so challenging about consumer-facing fintech companies is that customers are expensive to acquire, they’re difficult to keep, and products are easy to replicate. Providing a free credit score is easily accessible through a partnership with Equifax or Experian. It’s commoditized. The situation is similar with personal financial management tools. This Personal Credit Line seems awfully similar. What’s to stop Chase or Goldman’s Marcus from offering an identical product, perhaps with even better rates? U.S. Bank just launched a similar product, albeit for a different use case, called Simple Loan. It’s a $100 to $1,000 loan marketed as a payday lending alternative, with a roughly 20% lower interest rate than typical payday lender offers.

There is something to be said for being first to market, but ease of replication limits the defensibility of that position. There is a clear interest in an expansion into new products, which will continue to help Upgrade to differentiate the value proposition to consumers, and maybe one day small businesses. The unfortunate reality is that bigger players with an existing customer base and a lower cost of capital are on their tail.

Renaud Laplanche rings the bell with his team at LendingClub (DON EMMERT/AFP/Getty Images)

The real insight that distinguishes Upgrade from LendingClub is the profile of the users. On the supply side of the marketplace, Upgrade only welcomes institutional investors. LendingClub was, and still is, marketed to individuals and institutions.

The peer-to-peer model turned out to be a little too idealistic to serve as the foundation for a business. The concept of a marketplace is really attractive – the ability to invest in others, as cliché as that may sound, has a philanthropic twist to it that even implies a social good. Or, at the very least, an alignment of interests. Except interests aren’t aligned because of the mercurial nature of retail investors, which makes for unstable sources of capital.

LendingClub’s original business model, in the pure P2P form, was reliant on the ability to create a new asset class. The notion of investing in consumer credit may sound compelling, and return prospects may be even more appealing. But, you can’t bootstrap an asset class and base a business model around retail adoption. LendingClub had to solve for distribution of their service, as well as the dissemination of the broader concept of unsecured consumer lending as an asset class.

On Laplanche’s second go around with Upgrade, there’s no more promise of democratization of a new asset class. Instead, large multi-billion-dollar credit investors own the supply side of the marketplace. As a result, there’s a more stable capital base of institutional investors who know what they’re investing in and the reason why they’re investing in it.

What Laplanche did this time around was base his business model around stability. In this market it can pay to be a follower. LendingClub touts the notion that they have “brought a new asset class to investors,” but that education campaign came at a serious cost. It also invited boiler room-like sales behavior from competitors. Upgrade is stepping in after a decade of marketing to scale an untested industry to the masses. Fortunately, a lot of the work has already been done for them.

Upgrade is led by as experienced and forward-thinking of a leader as they come in the marketplace lending industry. They expect to originate over $2 billion loans in 2018 and hit profitability by year-end as well. They’re redefining convention when it comes to consumer credit products.

The question, however, remains: how long can the novelty last? Consumer fintech is fiercely competitive. It’s also increasingly occupied by incumbents with far lower costs of capital, large existing customer bases, and the ability to experiment in a way that a startup cannot. The unsecured consumer lending space has attracted mountains of capital in the past five years, but the opportunity is clearly defined. The number of lenders issuing more than 10,000 personal loans per year has more than doubled since 2011.

There’s a network effect component to marketplace lending businesses, particularly as lenders are able to maintain more connected relationships with consumers. But when it comes to standing apart from the rest of the pack, a differentiated product offering isn’t a very wide moat.

Powered by WPeMatico