nubank

Auto Added by WPeMatico

Auto Added by WPeMatico

With nearly half a million customers across Mexico and a network of 30,000 retail locations where representatives can take deposits, the challenger bank albo is already on its way to becoming a dominant player in Mexico’s emerging fintech industry.

And the company has recently raised another $45 million to consolidate its position.

“When your mission is to build the biggest bank in Mexico, you will need a ton of money,” said albo founder Angel Sahagún.

The company received its license to operate as a full depository bank in Mexico, and is slowly working toward being the premier internet-based financial services provider for Mexico’s large and growing middle class, Sahagún said.

“We are targeting a similar target market to Chime,” the albo founder and chief executive said. “We are targeting people who are underbanked and don’t have access to all the financial products in the market.”

Sahagún said the money will be used to expand into lending and insurance products the range of services albo offers. That’s a path that has already produced one multi-billion-dollar business in Nubank, Brazil’s wildly successful fintech company, which planted a flag for a new generation of Latin American startups.

While many challenger banks in the region pursued a strategy targeting upper-class and upper-middle-class consumers, Sahagún said his service had chosen a different path.

The company is trying to bring the middle and low-income Mexican consumers into the banking system by making it easy for them to move from a cash-based world to a digital one. “Where 90% of transactions are cash-based you need a value proposition that fits very well on that cash-based society,” Sahagún said.

It’s why the company set up a network of 30,000 locations, including convenience stores and drug stores, so that it can accept deposits at the places where its customers frequent.

That growth, and the company’s 40% share of the digital banking market in Mexico, according to data from Apptopia cited by the company, is why investors like Valar Ventures, Greyhound Capital, Mountain Nazca and Flourish Ventures were willing to invest as part of the $45 million round.

“albo has proven its ability to drive sustainable growth and is leading the market. This is the team that is going to transform banking in the region and we are proud to be supporting them in that,” said James Fitzgerald of Valar Ventures, in a statement.

Powered by WPeMatico

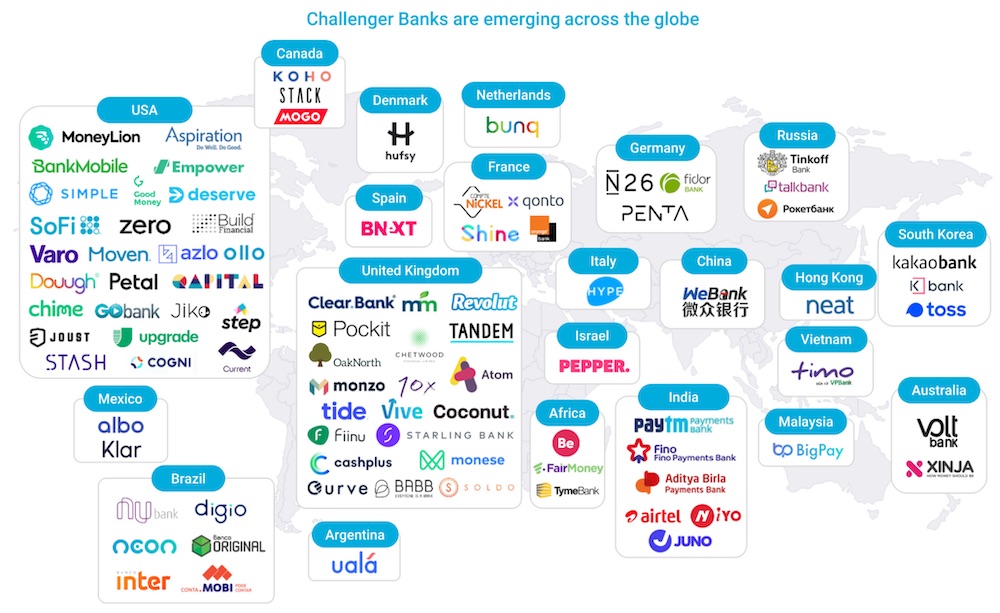

The neobank, or digital bank, phenomenon continues to take the world by storm, with global winners, from Brazil’s Nubank valued at $10 billion and Berlin’s N26 valued at $3.5 billion, to Chime, now valued at $14.5 billion as the most valuable consumer fintech in the United States.

Neobanks have led the charge of the $3.6 billion in venture capital funding for consumer fintech startups this year. And as the coronavirus-fueled acceleration of digital transformation continues, it seems the digital bank is here to stay, with some estimates pointing to neobanks reaching 60 million customers in North America and Europe by the end of 2020, and surpassing 145 million by 2024.

The space is also becoming more crowded, a trend which will only accelerate with fintech eating the world and creating greater infrastructure that enables any company to include a bank account as a product extension.

FT Partners Fintech Industry Research, January 2020

As a result, neobanks are not a monolithic model and not all are created equal. Looking underneath the hood of business models across the globe reveals remarkable operational differences and highlights specific features that are more likely to succeed in the long-term.

Today there are five distinct models that are leading globally:

Interchange-led: Relies on payments revenue, sourced through interchange as the revenue driver. Every time a customer uses the neobank’s card as a payment method they get paid [e.g. Chime / US; Neon (hybrid of 1 & 2) / Brazil].

Credit-led: Leverages a credit-first model, starting off with a credit card or similar offering, and later providing a bank account [e.g. Nubank, Neon (hybrid of 1 & 2) / Brazil].

Powered by WPeMatico

Lana, a new startup based in Madrid, is looking to be the next big thing in Latin American fintech.

Founded by serial entrepreneur Pablo Muniz, whose last business was backed by one of Spain’s largest financial services institutions, BBVA, Lana is looking to be the all-in-one financial services provider for Latin America’s gig economy workers.

Muniz’s last company, Denizen, was designed to provide expats in foreign and domestic markets with the financial services they would need as they began their new lives in a different country. While the target customer for Lana may not be the same middle to upper-middle-class international traveler that he had previously hoped to serve, the challenges gig economy workers face in Latin America are much the same.

Muniz actually had two revelations from his work at Denizen. The first — he would never try to launch a fintech company in conjunction with a big bank. And the second was that fintechs or neobanks that focus on a very niche segment will be successful — so long as they can find the right niche.

The biggest niche that Muniz saw that was underserved was actually in the gig economy space in Latin America. “I knew several people who worked at gig economy companies and I knew that their businesses were booming and the industry was growing,” he said. “[But] I was concerned about the inequalities.”

Workers in gig economy marketplaces in Latin America often don’t have bank accounts and are paid through the apps on which they list their services in siloed wallets that are exclusive to that particular app. What Lana is hoping to do is become the wallet of wallets for all of the different companies on which laborers list their services. Frequently, drivers will work for Uber or Cabify and deliver food for Rappi. Those workers have wallets for each service.

(Photo by Cris Faga/Pacific Press/LightRocket via Getty Images)

Lana wants to unify all of those disparate wallets into a single account that would operate like a payment account. These accounts can be opened at local merchant shops and, once opened, workers will have access to a debit card that they can use at other locations.

The Lana service also has a bill pay feature that it’s rolling out to users, in the first evolution of the product into a marketplace for financial services that would appeal to gig workers, Muniz said.

“We want to become that account in which they receive funds,” he said. “We are still iterating the value proposition to gig economy companies.”

Working with companies like Cabify, and other, undisclosed companies, Lana has plans to roll out in Mexico, Chile, Peru and, eventually, Colombia and Argentina.

Eventually, Lana hopes to move beyond basic banking services like deposits and payments and into credit services. Already hundreds of customers are using the company’s service through the distribution partnership with Cabify, which ran the initial pilot to determine the viability of the company’s offering.

“The idea of creating Lana was initially tested as an internal project at Cabify,” Muniz wrote in an email. “Soon Cabify and some potential investors saw that Lana could have a greater impact as an independent company, being able to serve gig economy workers from any industry and decided to start over a new entrepreneurial project.”

Through those connections with Cabify, Lana was able to bring in other investors like the Silicon Valley-based investment firm Base 10.

“One of the things we’ve been interested in is in inclusion generally and in fintech specifically,” said Adeyemi Ajao, the firm’s co-founder. “We had gotten very close to investing in a couple of fintech companies in Latin America and that is because the opportunity is huge. There are several million people going from unbanked to banked in the region.”

Along with a few other investors, Base 10 put in $12.5 million to finance Lana as it looks to expand. It’s a market that has few real competitors. Nubank, Latin America’s biggest fintech company, is offering credit services across the continent, but most of their end users already have an established financial history.

“Most of their end users are not unbanked,” said Ajao. “With Lana it is truly gig workers… They can start by being a wallet of wallets and then give customers products that help them finance their cars or their scooters.”

The ultimate idea is to get workers paid faster and provide a window into their financial history that can give them more opportunities at other gig economy companies, said Ajao. “The vision would be that someone can plug in their financial information for services. If they’re working for Rappi and have never been an Uber driver and they want to be an Uber driver, Lana can use their financial history with Rappi to offer a loan on a car,” he said.

That financial history is completely inaccessible to a traditional bank, and those established financial services don’t care about the history built in wallets that they can’t control or track. “Today if you’ve been a gig worker and you go to a bank, that’s worth nothing,” said Ajao.

Powered by WPeMatico

The alchemy for a successful startup can be hard to parse. Sometimes, it’s who you know. Sometimes it’s where you go to school. And sometimes it’s what you do. In the case of La Haus, a startup that wants to bring U.S. tech-enabled real estate services to the Latin American real estate market, it’s all three.

The company was founded by Jerónimo Uribe and Rodrigo Sánchez Ríos, both graduates of Stanford University who previously founded and ran Jaguar Capital, a Colombian real estate development firm that had built over $350 million worth of retail and residential projects in the country.

Uribe, the son of the controversial Colombian President Daniel Uribe (who has been accused of financing paramilitary forces during Colombia’s long-running civil war and wire-tapping journalists and negotiators during the peace talks to end the conflict) and Sánchez Ríos, a former private equity professional at the multi-billion-dollar firm Lindsay Goldberg, were exposed to the perils and promise of real estate development with their former firm.

Now the two entrepreneurs are using their know-how, connections and a new technology stack to streamline the home-buying process.

It’s that ambition that caught the attention of Pete Flint, the founder of Trulia and now an investor at the venture capital firm NFX. Flint, an early investor in La Haus, saw the potential in La Haus to help the Latin American real estate market leapfrog the services available in the U.S. Spencer Rascoff, the co-founder of Zillow, also invested in the company.

“Latin America is very early on in its infancy of having really professional agents and really professional brokerages,” said Flint.

La Haus guides home buyers through every stage of the process, with its own agents and salespeople selling properties sourced from the company’s developer connections.

“The average home in the U.S. sells in six weeks or less,” said La Haus chief financial officer Sánchez Ríos in an interview. “That timing in Latin America is 14 months. That’s the dramatic difference. There is no infrastructure in Latin America as a whole.”

La Haus began by reaching out to the founders’ old colleagues in the real estate development industry and started listing new developments on its service. Now the company has a mix of existing and new properties for sale on its site and an expanded geographic footprint in both Colombia and Mexico.

“We have a portal… that acts as a lead-generating machine,” said Sánchez Ríos. “We aggregate listings, we vet them. We focus on new developers.”

The company has about 500 developers using the service to list properties in Colombia and another 200 in Mexico. So far, the company has facilitated more than 2,000 transactions through its platform in three years.

“Real estate now is turning fully digital and also in this market professionalizing,” said Flint. “The publicly traded online real estate companies are approaching all-time highs. People are just prizing the space that they spend their time in… the technologies from VR and digital walkthroughs to digital closes become not just a nice to have but a necessity. “

Capitalizing on the open field in the market, La Haus recently closed on $10 million in financing led by Kaszek Ventures, one of the leading funds in Latin America. That funding will be used to accelerate the company’s geographic expansion in response to increasing demand for digital solutions in response to the COVID-19 epidemic.

“Because of Covid-19, consumers’ willingness to conduct real estate transactions online has gone through the roof,” said Sánchez Ríos, in a statement. “Fortunately we were in the position to enable that, and we expect to see a permanent shift online in how people conduct all, or at least most, of the home-buying process. This funding gives us ample runway to build the end-to-end real estate experience for the post-Covid Latin America.”

Joining NFX, Rascoff, and Kaszek Ventures are a slew of investors, including Acrew Capital, IMO Ventures and Beresford Ventures. Entrepreneurs like Nubank founder David Velez; Brian Requarth, the founder of Vivareal (now GrupoZap); and Hadi Partovi, CEO and founder of Code.org, also participated in the financing.

“We backed La Haus because we saw many of the same ingredients that resulted in a fantastic outcome for many of our successful companies: A world-class team with complementary skills; a huge addressable market; and an almost religious zeal by the founders to solve a big problem with technology,” said Hernan Kazah, co-founder and managing partner of Kaszek Ventures.

Powered by WPeMatico

Consumer fintech startups were massively successful in 2019, attracting millions of new users and disrupting traditional retail banks and financial services with mobile-first, consumer-oriented products. Despite the economic downturn in public markets and the massive wave of cuts at public and private companies in recent weeks, fintech startups have been raising a ton of money.

It feels like they’re all building a war chest to survive the economic winter as traditional banks continue to iterate so they can catch up and offer more user-friendly services. This is not the time to raise fees, slow down on product development or plans to acquire new users.

Back in January, I looked at challenger banks and their growth trajectories, but since then, they have managed to attract even more customers. According to the most recent figures:

And that’s without mentioning Starling Bank, Atom Bank, Bunq, Bnext, Paysend, etc. At some point, there will be as many challenger banks as non-challenger banks — perhaps we shouldn’t call them challenger banks anymore.

Beyond these startups, trading app Robinhood recently reached 13 million users, international payments startup TransferWise has 7 million customers and cryptocurrency exchange Coinbase has 30 million users.

Powered by WPeMatico

Another afternoon, another round of funding for a mobile banking app. This time, it’s Empower Finance, a San Francisco-based company that’s headed up by former Sequoia Capital partner Warren Hogarth and which just closed on $20 million in Series A funding from Icon Ventures and Defy Ventures.

David Velez, who is the founder and CEO of Nubank, the largest fintech in Latin America, also joined the round.

We’d first written about the company in 2017, when Hogarth was just getting the business off the ground. Fast-forward a bit and Empower now employs 35 people and has attracted more than 600,000 active users to its platform, says Hogarth. What has drawn them in: the company’s promise of combining AI and actual human financial planners to help millennials in particular accrue some wealth, including, more newly, through its own checking account product and through a savings account that’s currently promising 1.60% in annual percentage yield with no minimums, no overdraft fees and unlimited withdrawals.

It’s all part of an overall offering that crunches through account holders’ bank and credit card accounts, and recommends how much they save into which account, how much they should spend given their overall picture, various ways they can cut costs and where and when they’ve surpassed their pre-configured budgets.

Of course, the company has so much competition it’s dizzying, but like the various upstarts against which it’s battling for mindshare, the opportunity that Empower is chasing is enormous, too. Though companies like Chime can seem overpriced given how fast investors have marked up their rounds — Chime’s newest financing, announced in December, was done at a $5.8 billion post-money valuation, which was four times more than the company was worth at the outset of 2019 — digital banks are still tiny fish in an ocean of institutional financial services, representing something like 3% of the market.

They’re gaining more market share by the day, too, including by charging far lower fees for much more.

In Empower’s case, users pay $6 a month, but Hogarth says they also save $300 a year in additional fees they would pay a brick-and-mortar bank. He insists that on average, it also helps them save $1,300 more annually, too.

As for all those other companies — Mint, Acorns, the list goes on — Hogarth sounds surprisingly sanguine. “If you look at it from the outside, it looks crowded. But the consumer financial services in the U.S. is a $2 trillion business, and we haven’t had a fundamental shift since maybe Schwab came along 30 years ago.”

Indeed, says Hogarth, because Empower and its rivals are mobile and branchless and don’t have legacy software to contend with, they’re able to take 60 to 70% of the cost structure out of the business.

What that means on an individual company level is that even if each upstart can attract 2 to 3 million customers, they can get to a multibillion-dollar market cap. At least, that kind of math is “why there’s so much interest in this space,” says Hogarth.

It’s also why people like Nubank’s Velez, who have seen this story play out in Europe and Latin America and who are seeing the early phases of it in the U.S., are apparently keeping the money spigot open for now.

Empower had earlier raised an undisclosed amount of seed funding from Sequoia, followed by a $4.5 million round led by Initialized Capital.

Powered by WPeMatico

Two co-founders of Google Pay in India are building a neo-banking platform in the country — and they have already secured backing from three top VC funds.

Sujith Narayanan, a veteran payments executive who co-founded Google Pay in India (formerly known as Google Tez), said on Monday that his startup, epiFi, has raised $13.2 million in its Seed financial round led by Sequoia India and Ribbit Capital. The round valued epiFi at about $50 million.

David Velez, the founder of Brazil-based neo-banking giant Nubank, Kunal Shah, who is building his second payments startup CRED in India, and VC fund Hillhouse Capital also participated in the round.

The eight-month-old startup is working on a neo-banking platform that will focus on serving millennials in India, said Narayanan, in an interview with TechCrunch.

“When we were building Google Tez, we realized that a consumer’s financial journey extends beyond digital payments. They want insurance, lending, investment opportunities and multiple products,” he explained.

The idea, in part, is to also help users better understand how they are spending money, and guide them to make better investments and increase their savings, he said.

At this moment, it is unclear what the convergence of all of these features would look like. But Narayanan said epiFi will release an app in a few months.

Working with Narayanan on epiFi is Sumit Gwalani, who serves as the startup’s co-founder and chief product and technology officer. Gwalani previously worked as a director of product management at Google India and helped conceptualize Google Tez. In a joint interview, Gwalani said the startup currently has about two-dozen employees, some of whom have joined from Netflix, Flipkart, and PayPal.

Shailesh Lakhani, Managing Director of Sequoia Capital India, said some of the fundamental consumer banking products such as savings accounts haven’t seen true innovation in many years. “Their vision to reimagine consumer banking, by providing a modern banking product with epiFi, has the potential to bring a step function change in experience for digitally savvy consumers,” he said.

Cash dominates transactions in India today. But New Delhi’s move to invalidate most paper bills in circulation in late 2016 pushed tens of millions of Indians to explore payments app for the first time.

In recent years, scores of startups and Silicon Valley firms have stepped to help Indians pay digitally and secure a range of financial services. And all signs suggest that a significant number of people are now comfortable with mobile payments: More than 100 million users together made over 1 billion digital payments transaction in October last year — a milestone the nation has sustained in the months since.

A handful of startups are also attempting to address some of the challenges that small and medium sized businesses face. Bangalore-based Open, NiYo, and RazorPay provide a range of features such as corporate credit cards, a single dashboard to manage transactions and the ability to automate recurring payouts that traditional banks don’t currently offer. These platforms are also known as neo-bank or challenger banks or alternative banks. Interestingly, most neo-banking platforms in South Asia today serve startups and businesses — not individuals.

Powered by WPeMatico

Over the past year, startup banks have proven that they have a shot at disrupting retail banking. These challengers have amassed a war chest of funding, announced some ambitious international expansion plans and attracted millions of customers.

And yet, building a bank has proven to be even harder than building a startup in general. Retail banks aren’t willing to sit back and watch startups eat their lunch. Here’s a look back at the biggest moves of the year from challenger banks, some trends you should keep an eye on and the upcoming challenges for those startups.

Due to the regulatory framework and the size of the market, it is much easier to launch a challenger bank in Europe compared to anywhere else in the world. That’s why challenger banks have been thriving in Europe.

When a company gets a full banking license from the central bank of a EU country, the startup can passport its license across all EU countries and operate across the continent.

N26 raised a ton of money in 2019: last January, the Berlin-based startup announced a $300 million funding round, raising another $170 million in July. The company is now valued at $3.5 billion.

With more than 3.5 million customers in Europe, N26 announced some ambitious expansion plans. N26 is now live in the U.S. and is already planning a launch in Brazil.

Revolut has also been aggressively expanding in order to beat its competitors to new markets. In addition to its home market in the U.K., Revolut is available across Europe. In 2019, the company expanded to Singapore and Australia and currently has at least 8 million users.

While Revolut announced that it should launch in the U.S. and Canada by the end of last year, the clock ran out on that prediction. The startup has been very transparent about its expansion plans, even though it sometimes means that you have to wait months or even years before a full rollout.

For instance, Revolut announced in September 2018 that it would launch in New Zealand, Hong Kong and Japan “in the coming months.” It later became “early 2019,” then “2019.” India, Brazil, South Africa, Mexico and the UAE have also all been mentioned at some point. In other words: launching a banking product in a new country is hard.

The U.S. is a tedious market as you have to get a license in all 50 states to operate across the country

Monzo has been doing well at home in the U.K. It has attracted 3 million customers and raised £113 million (~$144m) in funding last year from Y Combinator’s Continuity fund. It is expanding to the U.S., but the rollout has been slow.

Nubank is another well-funded challenger bank. Backed by Tencent, the startup has raised a $400 million Series F round from TCV. According to the WSJ, the startup has a valuation above $10 billion.

Originally from Brazil, Nubank expanded to Mexico and has plans to expand to Argentina.

Chime is increasingly looking like the bigger player in the U.S., recently raising a $500 million funding round and reached a valuation of $5.8 billion. It only operates in the U.S.

Starling Bank and Atom Bank only operate in the U.K. Bunq is based in Amsterdam with a product tailor-made for the Netherlands, but it accepts customers across Europe.

This isn’t meant to be an exhaustive list as it’s becoming increasingly hard to cover all challenger banks.

There are a few basic features that separate challenger banks from legacy retail banks. Signing up is extremely simple and only requires a mobile app. The mobile app itself is usually much more polished than traditional banking apps.

Users receive a Mastercard or Visa debit card that communicates with the company’s server for each transaction. This way, users can receive instant notifications, block and unblock their cards and turn off some features, such as foreign payments, ATM withdrawals and online transactions.

Challenger banks usually customers promise no markup fees on transactions in foreign currencies, but there are sometimes some limits on this feature.

So how do these companies make money? When you pay with your card, banks generate a tiny, tiny interchange fee of money on each transaction. It’s really small, but it could become serious revenue at scale with tens of millions or hundreds of millions of users.

Challenger banks also offer other financial services like insurance products, foreign exchange or consumer credit. Some challenger banks develop those features in house, but many of those features are actually managed by external fintech partners. Challenger banks generate a commission on those products.

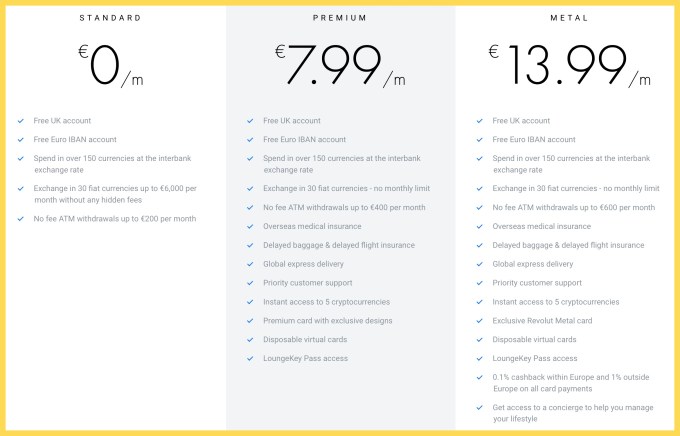

But the most promising product is premium subscriptions. While challenger banks started with free accounts and low, transparent fees, they have been selling premium subscriptions for a fixed monthly fee.

Challenger banks have become a software-as-a-service industry with a freemium component

For example, Revolut offers premium accounts for €7.99 per month with higher limits, some insurance benefits that you’d expect from a premium card and access to advanced features, such as cryptocurrencies and disposable virtual cards. There’s a super premium product for €13.99 called Metal with a metal card design, cashback on card payments and access to a concierge feature.

This seems a bit counterintuitive, but premium subscriptions have been performing well, according to discussions with people working in the industry. You pay a lot in subscription fees in order to avoid small transactional fees. (And you also get a cool card.)

Challenger banks have become a software-as-a-service industry with a freemium component. It leads to a premium positioning and high expectations from customers.

Revolut’s fees top out at €13.99/month.

Powered by WPeMatico

Although the 2008 global financial crisis sparked the fintech movement, in Latin America, the rise of ecommerce was responsible for the first wave of fintech startups.

Because digital payments were key to enabling the growth of ecommerce, investors funded companies like Braspag, PagSeguro, PayU, Mercado Pago and Moip in the early 2000s to take advantage of this opportunity.

Payment is still the most relevant segment, with successful cases like Stone and PagSeguro, but after the financial crisis, we started to see the rise of financial technology in lending and neobanking, generating impressive cases like Nubank, Neon, Creditas, Credijusto and Ualá.

As the ecosystem evolves and expands, let’s take a closer look at emerging trends in Latin America that might give us a hint about where to expect its next fintech unicorns.

Latin America has seen explosive growth in ride-hailing and food delivery platforms such as Uber, Didi, Rappi and iFood, creating a totally new market opportunity — many gig economy workers can’t access basic financial services such as bank accounts, personal loans and insurance. Even those who have access often struggle with financial products that that don’t suit their needs because they were designed for full-time workers.

Spotting this opportunity, Uber Money launched at Money 2020, focusing on providing drivers with financial services. As 50% of the population in Latin America is unbanked where Uber has more than 1 million drivers, the region is definitely a ripe market. Cabify is going even farther by spinning off Lana, its company that provides financial services, so it can expand its market beyond Cabify drivers to include other gig economy professionals.

Although established players in this sector have a clear advantage, they aren’t the only ones looking to explore this opportunity; Brazilian YC alumni Zippi is offering personal loans to ride-hailing drivers based on their driving earnings. As the gig economy tends to keep growing in the region, I believe we will start to see more solutions for those professionals.

As the banking world has been shaken by fintechs, insurance companies are growing aware that high regulatory barriers won’t protect their industry from disruption.

Insurance penetration in Latin America has been historically low compared to developed markets — 3.1%, compared to 8% — but the insurance market is growing well and tends to close this gap. Adding this to bad services and complex products that insurances provide, insurtech has an immense opportunity to grow.

Because purchasing insurance is historically a complicated and painful experience, the first insurtechs in the region focused on providing a better experience by digitizing the process and using online channels to acquire customers. Those insurtechs worked together with the insurance companies and operating as online broker, but now, we’re starting to see startups providing new insurance products, as well as traditional insurances in different models.

Some are partnering with insurance companies while others are competing directly with them; Think Seg and Miituo partnered with larger players to provide a pay-as-you-go model for car insurance, while Mango Life and Kakau are offering a better purchasing experience. On the other end, Crabi and Pier are rethinking the insurance model from the ground up.

As insurtechs emerge as a potential threat, incumbents are more willing to work with startups that can improve their services to enable them to compete on better grounds, which is exactly what companies such as Bdeo, Lisa, and HelloZum are doing.

Although penetrating the insurance industry is more complicated than other financial services due to high regulatory demands and steep initial operating costs, insurtechs fueled by VC investment will without any doubt try to do it. And, if we’ve learned anything from other fintech segments, it’s that entrepreneurs will find ways to overcome initial challenges.

Powered by WPeMatico

With roughly one million customers across Brazil and a new round of financing, the mobile phone insurance provider Pitzi now finds itself with a $100 million valuation.

The size of its latest round, which was led by QED Investors and included commitments from existing investors like Thrive Capital and Valiant Partners, was undisclosed.

PItzi acts as a reseller for insurance companies to offer products around mobile phone insurance across Brazil. Founded in 2012, the company’s mobile handset insurance offerings were a service that was in the right place at the right time, as low-cost handsets caused the market in Latin America’s most populous country to explode.

Pitzi previously raised $20 million from investors, including Thrive, Kaszek Ventures, Flybridge and DCM. Even with the company’s success, cell phone insurance in Brazil stands at 4%, compared with global standards of more than 40%. This despite the fact that there are more than 200 million phones in Brazil alone.

“Today, only 4% of smartphones here are protected but we’re driving that towards 90% in the coming years and using those phones to unlock even more transformation in the space,” said Daniel Hatkoff, founder and CEO of Pitzi, in a statement.

The investment by QED Investors puts Pitzi in some pretty good company when it comes to Latin American financial technology startups. Other Latin American investments in the firm’s portfolio include the multibillion-dollar credit card startup, Nubank; the personal finance lender, Creditas; the business lender, Konfio; and the rental financing company Quinto Andar.

As a result of the investment, Bill Cilluffo, a former president of Capital One International and a general partner with QED, will take a seat on the company’s board of directors, according to a statement.

For Hatkoff, the cell phone is a window into other products and services in the insurance industry thanks to the ways the device has transformed so many experiences for the emerging Brazilian middle class.

“The smartphone will be profoundly transformational in Brazil, allowing the emerging middle class to finally emerge and do things it never imagined possible,” said Hatkoff. “As market leaders, we at Pitzi are obsessed with unlocking the Brazilian consumer’s ability to use their phones in ever more powerful ways. Cell phone protection is just the beginning.”

Powered by WPeMatico