norwest venture partners

Auto Added by WPeMatico

Auto Added by WPeMatico

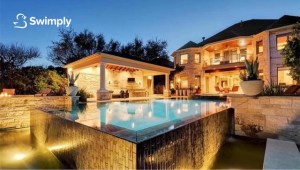

As the oldest of 12 children, Bunim Laskin spent much of his teen years looking for ways to help keep his siblings entertained. Noticing that a neighbor’s pool was often empty, Laskin reached out to ask if his family could use her pool. To make it worth her while, he suggested that they could help cover her expenses for maintaining the pool.

Soon after, five other families had made the same arrangement with her and the pool owner had six families covering 25% of her expenses. This meant that the neighbor was actually making money off her pool. The arrangement sparked a business idea in Laskin’s mind. At the age of 20, he founded Swimply, a marketplace for homeowners to rent out their underutilized pools to local swimmers, with Asher Weinberger.

The Cedarhurst, New York-based company launched a beta in 2018, starting with four pools in the New Jersey area.

“We used Google Earth to find houses, and then knocked on 80 doors with a pool,” CEO Laskin recalls. “We got to 100 pools organically. Word of mouth really helped us grow.” The site was pretty bare bones, he admits, with potential customers only able to view photos of the pools and connect with the pool owner by phone.

That year, Swimply did around 400 reservations and raised $1.2 million from friends and family.

In 2019, Swimply launched what he describes as a “proper” website and app with an automated platform. It grew “four to five times” that year, again mostly organically. In an episode that aired in March 2020, the company appeared on Shark Tank but went home without a deal.

Then the COVID-19 pandemic hit. Swimply, Laskin said, pivoted right into the pandemic.

“We were the perfect solution for people when the world was falling on its head,” he said. The company restructured its offering to ensure that pool owners did not have to interact with guests. “It was the perfect, contact-free, self-serve experience to hang out and be with people you quarantined with.”

The CDC then came out to say that it was safe to swim because chlorine could help kill the virus, and that proved to be a big boon to its business.

“On one end, it was a way for people to have a normal day and on the other, it helped give owners a way to earn an income, at a time when many people were being affected financially,” Laskin told TechCrunch.

Business took off in 2020 with revenue growing 4,000% and now Swimply is announcing a $10 million Series A round. Norwest Venture Partners led the financing, which also included participation from Trust Ventures and a number of angel investors such as Poshmark founder and CEO Manish Chandra; Rob Chesnut, former general counsel and chief ethics officer at Airbnb; Ancestry.com CEO Deborah Liu and Michael Curtis.

Swimply is now operating in a total of 125 U.S. markets, two markets in Canada and five markets in Australia. It plans to use its new capital in part to expand into new markets and toward product development.

Image Credits: Swimply

The way it works is pretty straightforward. Swimply simply connects homeowners that have underutilized backyard spaces and pools with those seeking a way to gather, cool off or exercise, for example. People or families can rent pools by the hour, ranging in price from $15 to $60 per hour (at an average of $45/hour) depending on the amenities. New markets that Swimply has recently expanded to include Portland, Oregon; Raleigh, North Carolina and the California cities of Oakland, San Luis Obispo and Los Gatos.

“The shifting mindset from younger generations about ownership is a huge contributor to increased growth of the Swimply marketplace,” said co-founder Weinberger, who serves as Swimply’s COO. “Swimming is the third most popular activity for adults and number one for children, and yet no other company has tackled the aquatic space to make swimming more affordable and accessible…until now.”

While the company declined to provide hard revenue figures, Laskin said Swimply was seeing “seven digits a month in revenue” and 15,000 to 20,000 reservations a month. Families represent the most popular reservation.

“People can book and pay through our platform, and only 20% of hosts ever meet their guests,” Laskin said. “We’re enabling a new kind of consumer behavior with what we’re doing.”

The company is planning to use its new capital to also rebuild much of its tech infrastructure and boost its customer support team to be more “readily available.”

It is also now offering a complimentary up to $1 million worth of insurance per booking for liability as well as $10,000 for property damage.

Swimply has a little over 20 employees, up 10 times from two people in December of 2020. It plans to double that number over the next few months.

The company’s model has proven quite lucrative for some owners, according to Laskin.

“Last year, there were some owners who earned $10,000 a month. One owner in Denver earned $50,000 last year and he had signed up toward the end of the summer. He should make over $100,000 this year,” Lasken projects.

Its only criteria is that owners offer a clean pool. Eighty-five percent of hosts offer restrooms as well. If they don’t, they are limited to one-hour reservations with a max of five guests. Swimply has also partnered with local pool companies, and if they pay one of its owners a visit and certify that pool, that owner gets a badge on the site “so guests get an additional level of security,” Laskin said.

Ed Yip of Norwest Venture Partners admits that when he first heard of the concept of Swimply, he “didn’t know what to make of it.”

But the more he heard about it, the more excited he got.

“This is the Holy Grail for a consumer investor. We’re not changing consumer behavior, but rather [we] productize the experience and make it safer and easier on both sides,” Yip told TechCrunch.

What also gets the investor excited is the potential for Swimply beyond just swimming pools in the future.

“We’re seeing a ton of demand from hosts wanting to list hot tubs and tennis courts, for example,” Yip said. “So this can turn into a marketplace for shared outdoor resources and that’s a huge market opportunity that adds value on both sides.”

Indeed, the concept of monetizing underutilized space is a growing concept. Earlier this year, we reported on Neighbor, which operates a self-storage marketplace, raising $53 million in a Series B round of funding. Neighbor’s unique model aims to repurpose under-utilized or vacant space — whether it be a person’s basement or the empty floor of an office building — and turn it into storage.

Powered by WPeMatico

HoneyBook, which has built out a client experience and financial management platform for service-based small businesses and freelancers, announced today that it has raised $155 million in a Series D round led by Durable Capital Partners LP.

Tiger Global Management, Battery Ventures, Zeev Ventures, 01 Advisors as well as existing backers Norwest Venture Partners and Citi Ventures also participated in the financing, which brings the San Francisco-based company’s valuation to over $1 billion. With the latest round, HoneyBook has now raised $248 million since its 2013 inception. The Series D is a big jump from the $28 million that HoneyBook raised in March 2019.

When the COVID-19 pandemic hit last year, HoneyBook’s leadership team was concerned about the potential impact on their business and braced themselves for a drop in revenue.

Rather than lay off people, they instead asked everyone to take a pay cut, and that included the executive team, who cut theirs “by double” the rest of the staff.

“I remember it was terrifying. We knew that our customers’ businesses were going to be impacted dramatically, and would impact ours at the same time dramatically,” recalls CEO Oz Alon. “We had to make some hard decisions.”

But the resilience of HoneyBook’s customer base surprised even the company, who ended up reinstating those salaries just a few months later. And, as corporate layoffs driven by the COVID-19 pandemic led to more people deciding to start their own businesses, HoneyBook saw a big surge in demand.

“Our members who saw a hit in demand went out and found demand in another thing,” Oz said. As a result, HoneyBook ended up doubling its number of members on its SaaS platform and tripling its annual recurring revenue (ARR) over the past 12 months. Members booked more than $1 billion in business on the platform in the past nine months alone.

HoneyBook combines on its platform tools like billing, contracts and client communication, with the goal of helping business owners stay organized. Since its inception, service providers across the U.S. and Canada such as graphic designers, event planners, digital marketers and photographers have booked more than $3 billion in business on its platform. And as the pandemic had more people shift to doing more things online, HoneyBook prepared to help its members adapt by being armed with digital tools.

Image Credits: HoneyBook

“Clients now expect streamlined communication, seamless payments, and the same level of exceptional service online that they were used to receiving from business owners in person,” Alon said.

Oz co-founded HoneyBook with wife Naama and longtime friend Dror Shimoni. Oz and Naama were both small business owners themselves at one time, so they had firsthand insight on the pain points of running a service-based business.

HoneyBook’s software not only helps SMBs do more business, but helps them “convert potentials to actual clients,” Oz said.

“We help them communicate with potential clients so they can win their business, and then help them manage the relationship so they can keep them,” Naama said.

The company plans to use its new capital toward continued product development and to “dramatically” boost its 103-person headcount across its New York and Tel Aviv offices.

“We’re seeing so much demand for additional services and products, so we definitely want to invest and create better ways for our members to present themselves online,” Alon told TechCrunch. “We’re also seeing demand for financial products and the ability to access capital faster. So that’s just a few of the things we plan to invest in.”

The company also wants to make its platform “more customizable” for different categories and verticals.

Chelsea Stoner, general partner at Battery Ventures, said her firm recognized that the expansive market of productivity tools to serve small businesses and entrepreneurs was “a market of discrete and separate productivity tools.”

HoneyBook, she said, is a true platform for SMBs, “providing a huge array of functionality in one cohesive UX.”

“It unites and connects every task for the solopreneurs, from creating and distributing marketing collateral, to organizing and executing proposals, to sending invoices and collecting payments,” Stoner said. “The company is constantly innovating and iterating in response to its members; we also see a lot of opportunity with payments going forward…And, due to COVID-19 and other factors, the company is sitting on pent-up demand that will accelerate growth even more.”

Powered by WPeMatico

Xpressbees, an Indian logistics firm that works with several e-commerce firms in the country, said on Monday it has raised $110 million in a new financing round as online shopping booms in the world’s second largest internet market.

The Pune-headquartered startup’s Series E financing round was led by private equity firms Investcorp, Norwest Venture Partners and Gaja Capital, the five-year-old startup said. Xpressbees, which concluded its Series D round three years ago, has raised $175.8 million to date, according to research firm Tracxn. The new round valued the startup at more than $350 million.

Xpressbees helps more than 1,000 customers — including financial and e-commerce services giant Paytm, social commerce startup Meesho, eyewear seller Lenskart, phone maker Xiaomi, online pharmacy NetMeds and online marketplace Snapdeal — deliver their products across the country. It has presence in over 2,000 cities and towns, and it processes more than 2.5 million orders a day — up from about 600,000 daily orders last year.

“We have been truly impressed by their strong customer centricity and capital efficiency which has resulted in exceptional feedback from top players in the e-commerce sector!” said Niren Shah, managing director and head of Norwest Venture Partners in India, in a statement.

Xpressbees started its journey within FirstCry, an e-commerce for baby products, in 2012. But in 2015, it became an independent company with Amitava Saha, co-founder and chief operating officer of FirstCry, moving out of FirstCry to become chief executive of Xpressbees. Supam Maheshwari, who co-founded FirstCry and serves as its chief executive, is the other co-founder of Xpressbees.

The startup said it plans to deploy the fresh capital to further automate its hubs and sorting centres, and expand its delivery footprint to cover the entire country. “I am delighted to see the impact we are making in the logistics ecosystem in the country,” said Saha in a statement.

At stake is India’s growing logistics industry, which NVP’s Shah estimated to be worth $200 billion. “We continue to believe that new age technology led logistics players such as Xpressbees will continue to play a pivotal role both in the growth of the e-commerce sector in India,” he added.

E-commerce sales, which account for less than 5% of all retail sales in India, skyrocketed during the pandemic after New Delhi enforced a two-month nationwide lockdown. During their festival sales last month, Amazon India and Walmart-owned Flipkart reported a record surge in their sales. The firms have created more than 150,000 seasonal jobs to accommodate the growing demand of orders. Xpressbees works with over 30,000 delivery staff.

Xpressbees competes with a handful of established firms and startups, including SoftBank-backed Delhivery, which became a unicorn last year, and Ecom Express, which has presence in about 2,400 Indian cities and towns.

Powered by WPeMatico

Qualified, a startup co-founded by former Salesforce executives Kraig Swensrud and Sean Whiteley, has raised $12 million in Series A funding.

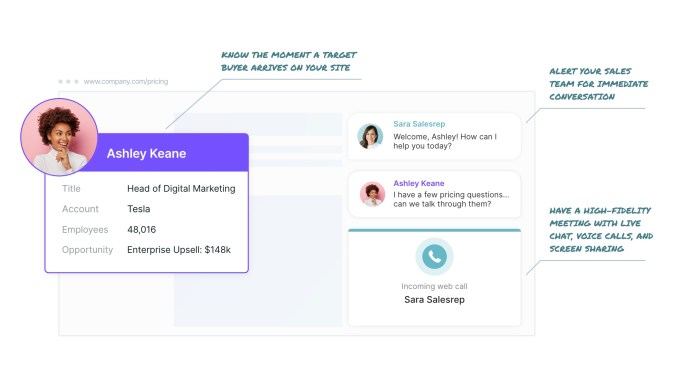

Swensrud (Qualified’s CEO) said the startup is meant to solve a problem that he faced when he was CMO at Salesforce. Apparently he’d complain about being “blind,” because he knew so little about who was visiting the Salesforce website.

“There could be 10 or 100 or 100,000 people on my website right now, and I don’t know who they are, I don’t know what they’re interested in, my sales team has no idea that they’re even there,” he said.

Apparently, this is a big problem in business-to-business sales, where waiting five minutes after a lead leaves your website can result in a 10x decrease in the odds of making contact. But the solution currently adopted by many websites is just a chatbot that treats every visitor similarly.

Qualified, meanwhile, connects real-time website visitor information with a company’s Salesforce customer database. That means it can identify visitors from high-value accounts and route them to the correct salesperson while they’re still on the website, turning into a full-on sales meeting that can also include a phone call and screensharing.

Image Credits: Qualified

Of course, the amount of data Qualified has access to will differ from visitor to visitor. Some visitors may be purely incognito, while in other cases, the platform might simply know your city or where you work. In still others (say if you click on a link from marketing email), it can identify you individually.

That’s something I experienced myself, when I decided to take a look at the Qualified website this morning and was quickly greeted with a message that read, “ Welcome TechCrunch! We’re excited about our funding announcement…” It was a little creepy, but also much more effective than my visits to other marketing technology websites, where someone usually sends me a generic sales message.

Welcome TechCrunch! We’re excited about our funding announcement…” It was a little creepy, but also much more effective than my visits to other marketing technology websites, where someone usually sends me a generic sales message.

Swensrud acknowledged that using Qualified represents “a change to people’s selling processes,” as it requires sales to respond in real time to website visitors (as a last resort, Qualified can also use chatbots and schedule future calls), but he argued that it’s a necessary change.

“If you email them later, some percentage of those people, they ghost you, they get bored, they moved on to the competition,” he said. “This real-time approach, it forces organizations to think differently in terms of their process.”

And it’s an approach that seems to be working. Among Qualified’s customers, the company says ThoughtSpot increased conversations with its target accounts by 10x, Bitly grew its enterprise sales pipeline by 6x and Gamma drove over $2.5 million in new business pipeline.

The Series A brings Qualified’s total funding to $17 million. It was led by Norwest Venture Partners, with participation from existing investors including Redpoint Ventures and Salesforce Ventures. Norwest’s Scott Beechuk is joining Qualified’s board of directors.

“The conversational model is simply a better way to connect with new customers,” Beechuk said in a statement. “Buyers love the real-time engagement, sellers love the instant connections, and marketers have the confidence that every dollar spent on demand generation is maximized. The multi-billion-dollar market for Salesforce automation software is going to adopt this new model, and Qualified is perfectly positioned to capture that demand.”

Powered by WPeMatico

Salt Lake City’s Spiff has announced a $10 million round of funding to expand the sales and marketing efforts for its service that automates commission payments for sales people.

Some of the biggest names in startup tech are using the service to pay their sales force, including Brex, Workfront, Algolia and the publicly traded startup Qualys.

The idea at Spiff is to create a new software category around sales compensation management, and it’s gotten buy-in from investors at Norwest Venture Partners, Next World Ventures and Epic Ventures. Seed investors, including Kickstart Album Ventures, Pipeline Capital and Peterson Ventures, returned to invest in the company as well.

“Commissions are a major cause of anxiety for teams who don’t understand or trust their incentive plan and many waste hours every month correcting mistakes or arguing with finance, which hits bottom lines,” said Spiff chief executive, Jeron Paul. “Norwest’s investment will help us automate commission calculations so sales teams have one less thing to worry about in these challenging times.”

Paul, a serial entrepreneur whose most recent business, Capshare, was sold to Solium in 2017, has spent the better part of his professional career developing services businesses for enterprises.

“The world of sales compensation software is long overdue for a revamp,” said Sean Jacobsohn, partner at Norwest Venture Partners, in a statement. “With 85 percent of companies still calculating sales commissions manually in Google Sheets or Excel, I’m excited to partner with Spiff to help transform the way people think about sales compensation and provide sales teams with a deeper level of visibility into their commissions.”

Powered by WPeMatico

An emergency room physician for the past 12 years, Dr. Robert Mittendorff joined Norwest Venture Partners eight years ago as a healthcare investor; the firm invests in a number of healthcare startups, including Talkspace, which raised a $50 million Series D last year, and TigerConnect.

As the COVID-19 pandemic spreads, Mittendorff is spending his weekdays with portfolio companies and weekends working with Kaiser Permanente in San Francisco. While he notes that his medical colleagues are “bearing the brunt” of the pandemic by working full time, we wanted to hear from someone who has a foot in both the investing and the healthcare world right now.

In this interview, he discusses what he’s learned from both roles, how it has influenced his healthcare investments, and offers his predictions regarding which companies will fare the best in the future.

This interview has been edited for length and clarity.

TechCrunch: How did you get to where you are today?

Dr. Robert Mittendorff: So, my journey to being a venture capitalist at Norwest and investing in healthcare companies as well as an emergency physician was really a parallel set of paths that overlapped and that cross every once in a while and now usually on a daily basis.

I started off life as a biomedical engineer really focused on wanting to be on the side of innovation and on the development of technologies to help human health. I knew early on that I wanted to be on the business side [of that], but it was important for me to understand and really be deeply in touch with what it was like to be a provider.

The journey started out going to engineering school, medical school, and then business school in the middle of medical school. I trained at Stanford, which really exposed me to county hospitals, which are probably going to be the more challenging situations as the weeks go on here, and then to Kaiser Permanente. And then, of course, Stanford, I was exposed to San Francisco General and then the Santa Clara Valley Hospital. I always practice part-time following up so it’s been 12 years as an attending, practicing part-time as an emergency physician.

In the venture space I saw an opportunity to really help select entrepreneurs and markets to grow them to a higher impact state.

Powered by WPeMatico

Customer engagement platform Leanplum today announced that it has raised a $27 million extension to its 2017 $47 million Series D round. This additional funding was led by previous investors Norwest Venture Partners and Shasta Ventures. Kleiner Perkins, Canaan and Launchub also participated in this round, which the company says it will use to bolster its product development and go-to-market efforts. With this, Leanplum has now raised a total of $125 million.

Maybe just as importantly, Leanplum also announced a major shakeup of its executive ranks. The company appointed George Garrick as president and CEO, and Sheri Huston as chief financial officer. Co-founder and former CEO Momchil Kyurkchiev will step into the chief product officer role.

Garrick brings a wealth of experience with him, having been the CEO of companies like Flycast, Placeware, Wine.com and Tapjoy . Huston, too, comes into the role with a lot of industry experience as the former CFO at Comscore and LiquiBox. The company is also adding Dynamic Signal founder Russ Fradin to its board of directors.

The company describes the changes in its executive ranks as a “transition.”

“Many if not most startups at some point in their growth realize that a management transition makes sense as the requirements for the CEO evolve from starting and proving a company, to running and scaling it,” Garrick told us in a statement. “Leanplum’s board and founders agreed that such a transition would be appropriate as Leanplum accelerates its growth phase.”

This was echoed by Kyurkchiev: “George is the right leader for Leanplum. His strong management experience with companies at our stage and in our domain will be essential for Leanplum as we continue to drive growth and expand globally.”

Leanplum says about 2 billion people used apps and websites that use its services in 2019.

As for the new funding, the company says it was simply easier to extend its Series D, which has the same investors as the original D round. “The board felt it was easier and more appropriate to just extend the D round rather than move into the next letter. Also, we wanted to minimize ‘letter creep,’ ” Garrick said.

Powered by WPeMatico

Two years after the Los Angeles-based fintech startup Dave launched with a suite of money management tools to save consumers from overdraft fees, the company is now worth $1 billion thanks to a nascent banking practice that had investors lining up.

The company used its overdraft protection service and money management display to shift customers’ focus away from the total balance that their account would show by giving them a sense of how much was actually left in their accounts once debits were included in their statements.

“What was cool about our financial management product was that we were trying to use Dave as a replacement for their current bank,” says Jason Wilk, Dave’s co-founder and chief executive.

Dave now counts over 4 million users for its financial management app and has roughly 800,000 people on the waiting list to use its banking services, Wilk says.

The company has taken a methodical approach to opening its doors as a digital bank, in part because it wants to have the necessary support infrastructure in place to service the demand that Wilk expects to see for its service.

“It’s one thing to help people with budgeting. It’s another to actually manage their money,” says Wilk.

")

Dave will use the $50 million raised from Norwest to significantly expand its product and engineering team within the next 12 months, in order to double down on the core business and ensure the success of the banking product.

“We can prove that Dave can be helpful by showing how we can help you manage your current account, and then Dave banking is the marketing lever from there,” says Wilk.

For now, customers need to have the financial management app installed to be able to access the company’s banking service.

Dave charges $1 per month for access to its financial management tools and that also gives customers the ability to use a cushion of between $50 to $75 to avoid being hit with overdraft fees from their current bank account. Dave asks for a tip every time a customer uses that cushion to cover expenses — something that Wilk says is still cheaper than having to worry about overdraft fees.

And, to add a bit of environmental spin, for every tip that Dave receives, the company plants a tree. “We plant millions and millions of trees,” says Wilk.

The company is FDIC insured through a partner bank, the Memphis-based Evolve Bank and Trust, which acts as a backstop for the company’s financial management activities.

“We already had a relationship with them for some payment processing stuff,” says Wilk. “We liked the team and liked the terms and went with them.”

Terms between financial services firms can vary, and, Wilk says, Evolve Bank was willing to give the company a good deal on splitting the interchange fee, which is a big source of revenue for upstart banks.

It’s possible that Dave could have received a bigger check at a potentially higher valuation, but Wilk says the startup is trying to stay lean.

“The company is growing so quickly, we didn’t want to get too diluted on this round,” he says. “We think the company is quite a bit more valuable than [$1 billion]. You don’t want to raise too much money too quickly if you really think the valuation is going to climb… Since we signed the term sheet the company has already grown another 40%.”

It was only four months ago that Dave was announcing a $110 million credit financing with Victory Park Capital and the launch of its banking product.

Dave’s products and services have a few advantages for customers that are just getting started on the path to financial security. The company monitors everyday monthly payments and reports them to credit agencies to improve customers’ credit ratings. The company also provides up to $100, interest-free, overdraft protection.

“Banks have failed their customers by building products that put their own interests ahead of the humans who use them. People don’t need predatory fees, they need tools that actually solve their challenges around credit building, finding work and getting access to their own money to cover immediate expenses. Dave is the banking product that works with its customers, not against them,” said Wilk, in a June statement announcing the funding and banking product launch.

While Dave is getting some hefty firepower and a generous valuation from Norwest, it’s also operating in a market where its core services that were a point of differentiation are quickly becoming table stakes.

Earlier in September, the new startup banking company Chime announced that it had hit 5 million banking customers and was offering its own overdraft protection service.

The San Francisco-based bank has also raised a lot more capital for a potential piggy bank to raid if it needs to acquire or spend on engineering talent to build out new products and services. Earlier this year, the company announced a $200 million round and said it had hit roughly 3 million customers. Clearly Chime is adding new banking customers at a torrid pace.

And they’re facing global competition as well. N26, the European startup bank with a $3.6 billion valuation and hundreds of millions in financing launched in the U.S. a few months ago as well.

The company sees a global opportunity to create new digital banking services in a world where large amounts of capital and an elite set of consumers move easily between international markets.

“We have an opportunity that we build a bank that has more than 50 million users around the globe. Today, we only have 3.5 million users but we’re accelerating,” said N26 chief executive, Valentin Self, in an interview with TechCrunch. “From a country perspective, we have agreed already that we go to Brazil. There’s no plan after Brazil yet. Now let’s focus on the U.S., then on Brazil, then next year we’ll find out what’s the feedback from these two markets.”

Powered by WPeMatico

Robin Healthcare, a new startup founded by serial entrepreneurs Noah Auerhahn and Emilio Galan, is hoping to harness the power of personal assistants to make the business of healthcare easier for the physicians who practice it.

The company’s technology, which works much the same way as a Google Home or Amazon Alexa or Echo, is placed in hospital rooms and transcribes and formats doctor interactions with patients to reduce paperwork and streamline the behind-the-scenes part of the process that can drive doctors to the point of distraction, the company’s co-founder said.

“I had a background doing claims data work in healthcare at UCSF finishing my clinical training,” says Galan. “And I was hearing lots of doctors telling me not to practice.”

The problem, says Galan, was the overabundance of paperwork. After school, Galan doubled down on his work in claims and billing, launching a company called HonestHealth, where he worked with institutions and companies, like The Robert Wood Johnson Foundation, Consumer Reports and the New York State Department of Health, to analyze healthcare claims data and develop consumer applications.

Galan met Auerhahn at the HLTH conference a few years ago just as Auerhahn was looking for his next challenge after the sale of his previous company, ExtraBux.

The two men saw the wave of smart devices coming and figured there must be a way to use the technology to build a fully billable clinical report from monitoring the conversations with patients.

The company currently has dozens of its smart devices installed in hospitals around the country, including a large surgical practice in Tennessee, the Campbell Clinic; Duke University Medical Center’s Private Diagnostic Clinic; the University of California San Francisco Medical Center; and Webster Orthopedics in Northern California.

Robin integrates with the major electronic health records companies, Epic and Cerner, through third-party integrations that are designed to make it easier to input data automatically as doctors are assessing a patient’s condition and delivering treatments.

“Part of why Robin exists is to avoid technology interrupting care,” says Auerhahn. “Having fewer interactions with EMR is a good way to do that.”

Robin’s service is human-assisted natural language processing to make sure that the data is input correctly.

The company’s early vision has been enough to attract investors like Norwest Venture Partners, which led the company’s $11.5 million Series A round.

In all, Robin Healthcare has raised $15 million in financing. The company’s other investors include Social Leverage, the early-stage investment firm founded by Howard Lindzon.

Powered by WPeMatico

William Hockey, co-founder, chief technology officer and president of the fast-growing fintech business Plaid, will step down next week, TechCrunch has learned.

The former Bain associate (pictured above left) co-founded the startup in 2012 alongside chief executive officer Zach Perret. Today, the San Francisco-based company employs 300 with additional offices in Salt Lake City and New York.

Plaid has confirmed the news, stating that Hockey will remain on the company’s board of directors.

“This conclusion was neither a rash nor a recent decision,” Hockey writes in a blog post shared with TechCrunch. “Over the past couple of years, I have known that there would come a point at which I would choose to move to a purely strategic and advisorial role.”

Most companies should be constantly running running at least one exec search. Post-product/market fit, the limiting factor to scale generally derives from some version of not having enough great leaders.

— Zachary Perret (@zachperret) June 18, 2019

Plaid builds infrastructure that allows consumers to interact with their bank account on the web, powering a number of third-party applications, like Venmo, Robinhood, Coinbase, Acorns and LendingClub. It rose to prominence recently, closing a $250 million Series C investment at a $2.65 billion valuation late last year. The deal was led by famed venture capitalist and author of the Internet Trends report Mary Meeker, who’s joined the startup’s board of directors.

In total, Plaid has secured $310 million in venture capital funding from Andreessen Horowitz, Index Ventures, Norwest Venture Partners, Coatue Management, Goldman Sachs, NEA, Spark Capital and others.

Plaid has integrated with 15,000 banks in the U.S. and Canada and says 25% of people living in those countries with bank accounts have linked with Plaid through at least one of the hundreds of apps that leverage Plaid’s application program interfaces (APIs) — an increase from 13% last year. Last month, the company launched its fintech platform in the U.K.

“As we’ve done in the U.S., Plaid will become the foundation for that growth by providing access to a financial network that allows developers to deliver the experience users expect from their financial apps,” the company wrote in a blog post.

TechCrunch participated in a panel discussion with Hockey and Brex CEO Henrique Dubugras last month, in which Hockey gave no indication of impending plans to leave the business. In fact, taking off just as Plaid amps up its global expansion efforts and accelerates growth is strange timing for a founder to depart.

Oftentimes, when a startup co-founder steps down from the C-suite, it’s to make room for a more experienced executive to lead the company through periods of fast growth. Recently, for example, Lime announced its co-founder Toby Sun would transition out of the CEO role to focus on company culture and R&D. Brad Bao, a Lime co-founder and longtime Tencent executive, assumed chief responsibilities.

Other times, it comes amid turmoil. Mike Cagney’s departure from SoFi, of course, is an example of this. One month after reports of a sexual harassment and wrongful termination lawsuit against the online lending business surfaced, SoFi announced Cagney would step down.

In Hockey’s case, the move was planned and calculated, he said. Plaid chief operating officer Eric Sager, who joined earlier this year, Perret and other executives will take over engineering and product reports, among Hockey’s other responsibilities.

“In tech, it has historically been taboo to talk about founders or executives transitioning to different roles inside companies,” Hockey writes. “Leadership transitions need to become a bedrock of any company that desires to endure across decades.”

Powered by WPeMatico