new enterprise associates

Auto Added by WPeMatico

Auto Added by WPeMatico

Finding the right learning platform can be difficult, especially as companies look to upskill and reskill their talent to meet demand for certain technological capabilities, like data science, machine learning and artificial intelligence roles.

Workera.ai’s approach is to personalize learning plans with targeted resources — both technical and nontechnical roles — based on the current level of a person’s proficiency, thereby closing the skills gap.

The Palo Alto-based company secured $16 million in Series A funding, led by New Enterprise Associates, and including existing investors Owl Ventures and AI Fund, as well as individual investors in the AI field like Richard Socher, Pieter Abbeel, Lake Dai and Mehran Sahami.

Kian Katanforoosh, Workera’s co-founder and CEO, says not every team is structured or feels supported in their learning journey, so the company comes at the solution from several angles with an assessment on technical skills, where the employee wants to go in their career and what skills they need for that, and then Workera will connect those dots from where the employee is in their skillset to where they want to go. Its library has more than 3,000 micro-skills and personalized learning plans.

“It is what we call precision upskilling,” he told TechCrunch. “The skills data then can go to the organization to determine who are the people that can work together best and have a complementary skill set.”

Workera was founded in 2020 by Katanforoosh and James Lee, COO, after working with Andrew Ng, Coursera co-founder and Workera’s chairman. When Lee first connected with Katanforoosh, he knew the company would be able to solve the problem around content and basic fundamentals of upskilling.

It raised a $5 million seed round last October to give the company a total of $21 million raised to date. This latest round was driven by the company’s go-to-market strategy and customer traction after having acquired over 30 customers in 12 countries.

Over the past few quarters, the company began working with Fortune 500 companies, including Siemens Energy, across industries like professional services, medical devices and energy, Lee said. As spending on AI skills is expected to exceed $79 billion by 2022, he says Workera will assist in closing the gap.

“We are seeing a need to measure skills,” he added. “The size of the engagements are a sign as is the interest for tech and non-tech teams to develop AI literacy, which is a more pressing need.”

As a result, it was time to increase the engineering and science teams, Katanforoosh said. He plans to use the new funding to invest in more talent in those areas and to build out new products. In addition, there are a lot of natural language processes going on behind the scenes, and he wants the company to better understand it at a granular level so that the company can assess people more precisely.

Carmen Chang, general partner and head of Asia at NEA, said she is a limited partner in Ng’s AI fund and in Coursera, and has looked at a lot of his companies.

She said she is “very excited” to lead the round and about Workera’s concept. The company has a good understanding of the employee skill set, and with the tailored learning program, will be able to grow with company needs, Chang added.

“You can go out and hire anyone, but investing in the people that you have, educating and training them, will give you a look at the totality of your employees,” Chang said. “Workera is able to go in and test with AI and machine learning and map out the skill sets within a company so they will be able to know what they have, and that is valuable, especially in this environment.”

Powered by WPeMatico

The podcasting world remains one of the most vibrant formats in media (and I am not just saying that since the Equity crew won a Webby yesterday for our not-that-humble podcast). Its openness, diversity, freedom and ease-of-authoring has broadened the medium to all sorts of hosts on every subject imaginable.

We experience that dynamism and verve in our own audio listening, but then we start to tune into our company’s internal communications, and, well, you certainly don’t need sleeping pills to zone out. Top-down, formal, banal — corporate comms remains mired in a 1950s way of speaking that is completely out-of-sync with the millennials and Gen Z majority of workers who expect something actually worth watching and listening to.

Spokn wants to make company-wide podcasting a must-listen event, not just for leaders to talk to their employees, but for every worker to have a voice and share their expertise and stories across their workplaces. Through its app, companies can deliver personalized podcast feeds on everything from a daily standup or weekly AMA to training and development content, all of which is secure and kept for internal use.

It’s an idea that has quickly attracted investor attention. The startup, which was part of Y Combinator’s most recent Winter 2021 batch, closed on a $4 million seed round two weeks before Demo Day led by Ann Bordetsky, a partner at NEA who joined earlier this year and previously served as COO of Rival. This is her first investment with the firm.

The company was founded by Fawzy Abu Seif, Mariel Davis and Mohammad Galal Eldeen. Abu Seif and Davis met each other in an Egyptian jazz club in November 2017, about a week after he had quit his job. They eventually came together not just as a couple — they got married in the fall of 2019 — but as business partners, linking up with Galal Eldeen and incorporating Spokn in April 2018.

Spokn’s Mohammad Galal Eldeen, Mariel Davis and Fawzy Abu Seif. Image Credits: Spokn

Spokn’s product evolved across three iterations. First, the team tried to create audio narrations of evergreen content at major publishers like The New York Times. The idea was to help publishers reuse their best content as a new revenue source while connecting more listeners into these brands. Getting publishers to commit was tough though. “The consumer app wasn’t doing that great, and we started hunting around the data to see if something was working,” Davis said.

What they found was that professional development podcasts were much more popular compared to other topics, and so they had an opportunity to re-jigger the product to focus on training and specifically target enterprises. The idea was “let’s empower companies with the same tools we had as a consumer company,” Abu Seif said.

Prior to Spokn, Davis had worked with an entrepreneur in the Middle East building out a social enterprise network focused on skills training, a role in which she handled internal communications. She saw just how little impact media like email made for employees, particularly in the distributed workforce she was attempting to engage. The new direction for Spokn was far more enticing.

The newly married couple moved to New York City from Egypt and signed an apartment lease in early March 2020 — just as the COVID-19 pandemic spread widely in the region. We “multiplied the living expenses by 8-10x while doing the same Zoom calls we could make from there,” Abu Seif joked.

Eventually, the company realized that it could do much more than just training, and expanded into broader internal comms. “Async audio is a lot more personal than email,” Abu Seif said. This latest product iteration launched in November 2020, and included push notifications, an app for streaming, personalization features and analytics to allow companies to track what was working and what was not for employees.

Spokn’s app offers a personalized feed of company podcasts. Image Credits: Spokn

Perhaps most importantly, companies can tailor the access lists for individual podcasts to particular groups of people, such as senior execs, people managers, sales employees or any other logical grouping. We “get a lot of inbound from companies that are trying to duct-tape solutions together,” Davis said. For Abu Seif, “all the tools that marketers have to engage consumers, we are empowering companies to engage with their employees.”

Despite the startup and product’s youth, it has attracted a quick following among companies, with customers including Podium, ShipBob, Cedar, Mixpanel, ServiceNow and Superhuman. Podium’s CEO, for example, records weekly podcasts that are shipping on Spokn, and apparently even installed a podcast studio near his office just to make it easier to produce his shows.

Podcasting inside companies fixes a lot of problems with traditional internal comms. First and foremost, it can create a deeper connection where email cannot. Audio can feel more personal than even video, and also can be played in the background. It’s also asynchronous, unlike live video, allowing employees in different time zones to connect with key stories at an appropriate time.

Plus, employees can avoid all the fatigue that comes from being onscreen. “No one wants Zoom zombies,” Bordetsky of NEA said. “We need intuitive and asynchronous communication tools like Spokn to build connection and community in the workplace.” Her thesis for the investment is that “flexible, distributed work is here to stay and employee communication is at the heart of building a modern, virtual-first employee experience.”

Buyers of Spokn range from heads of people to sales teams, and the company is also focused on recruiting and retention as well. “Companies are pretty freaked out about retaining their great talent,” Davis said. Some companies are now sharing “stories with prospects even before their first day at the company.”

While the product is mostly used by leaders today, Spokn wants to expand that remit to employees talking with their peer colleagues, helping to build community in hybrid offices where it is harder than ever to make a connection with others.

Of course, companies can screw up podcasting just as much as they have screwed up every other medium to communicate like humans, and Davis says it’s become her full-time job to help them think through storytelling and how to connect better with their own employees. We “work to find the right storytellers in the company,” she said.

Outside NEA, other investors in the seed round included Reach Capital, Funders Club, Liquid2, Share Capital, SOMA Capital, Scribble VC and Hack VC.

Powered by WPeMatico

After teasing the launch of their new startup last year, e-commerce veteran Julie Bornstein and her technical co-founder, Amit Aggarwal, are today launching The Yes, a women’s shopping platform that they’ve been quietly building for 18 months and they say will create tailor-made experiences for each user, courtesy of its sophisticated algorithms.

Bornstein’s experience and vision alone attracted $30 million in funding to the venture last year from Forerunner Ventures, New Enterprise Associates and True Ventures, among others. To learn more about how it breaks through in a world rife with e-commerce companies, we talked with Bornstein, who previously spent four years as COO of the styling service Stitch Fix and before that spent years as a C-level executive at Sephora. We wondered specifically how The Yes differs from Stitch Fix, given that both companies use data science to discover clothing for shoppers based on their size, budget and style.

Aside from the fact that The Yes is taking an app-only approach (unlike Stitch Fix), and doesn’t have a subscription model, Bornstein says that The Yes is very much focused on people “who want to shop” versus those who want their shopping done for them. Yet that’s just the start of what makes The Yes different than its other predecessors, said Bornstein in a conversation that follows below, edited lightly for length.

TC: You’re building what you call a store around each user, who downloads the app, answers questions that provide a lot of “signal” about that person’s style and brand preferences and size and budget, and that’s adaptive, meaning the algorithm is always re-ranking products as it learns better what a person likes. What demographic are you targeting?

JB: It’s women of a very broad age range, from 25 to 75, who care about fashion, whether they’re an in-the-know-on-everything fashionista or they just want to look great. And you can shop high/low, which is how most women shop these days. So it depends what you’re looking for.

TC: It sounds like you’re selling women’s apparel exclusively to start. Are you also selling handbags? Jewelry? Accessories?

JB: We’re focused on fashion and footwear, and we have accessories and handbags. A lot of our brands have great handbags. Then we will be expanding more to jewelry and other accessory categories over time.

TC: What brands can shoppers find on the platform?

JB: We have 145 brands at launch, ranging from Gucci, Prada and Erdem to contemporary brands like Vince and Theory to direct-to-consumer brands like Everlane and La Ligne to everyday brands like Levis. When a brand integrates with The Yes, the platform sells each brand’s full digital catalog.

TC: Why go app only?

Most of the e-commerce sites that have mobile presence really feel like a website converted to a small screen. We [thought if we] challenged ourselves to leverage the technology of the native app environment, [we] could build a much slicker experience for the user. We also know that mobile is growing. It’s about 50% of total purchases now in fashion and growing faster, so while we know that web will be important to add, we really felt like mobile and iOS were the places to start.

TC: Stitch Fix uses machine learning to analyze customer tastes, but it ultimately relies on human stylists to choose items. What new advances have been made in AI that can allow The Yes to actually pick products using artificial intelligence? Isn’t fashion, like music, a “noisy” problem, with consumers often not knowing what they want?

JB: It’s such a nuanced area and really hard to do in the form of recommendations, but there are a number of reasons that enable us to do it. One is we had to build the most extensive taxonomy that exists in fashion. We did think a lot about the music genome project that Pandora did and all the work that Spotify has done. Music is definitely one of our inspirations. And if you look at what they did, they had some human expertise in the beginning, creating these categories, and then the machine learned on top of it, and we have done the same in fashion. So we had fashion expertise build our initial taxonomy.

Then we leveraged both machine learning and computer vision to train models to understand how to absorb all pieces of data related to a product, as well as the image itself and how to read images. And it gave us a really strong understanding of 500 dimensions for every single item. [Meanwhile] to understand what the consumer cares about, we spent a lot of time testing and learning which questions [to ask] when it comes to brand and price and things like color and style and size and fit…

TC: Because of your background, comparisons are probably going to be made between The Yes and Stitch Fix. What was the impetus for this new business? Was it a matter of eliminating that personal touch?

JB: I had such a great experience at Stitch Fix, and I’m still a shareholder and a big fan of the company and the team. And I think what they’re doing, what they continue to do, is terrific in really pushing the boundary on this concept of shopping-as-a-service.

What I am working on, and our team is really focused on, is the actual consumer shopping experience for consumers who want to shop. There’s a strong percent of the population who really loves to shop and wants agency in their own selection, and that is really the consumer we’re going after.

TC: You’re launching with roughly 150 brands. What is your relationship with them? Are you taking a cut of a transaction? Are you ever taking possession of their products? Do you have a warehouse or warehouses?

There were two things coming into this business that I wanted to avoid based on my personal experience, which was one, owning inventory, and two, reshooting every item for its own new photographs on the site. Pinterest and Instagram and all these other visual sites have shown us that the brands spend a lot of money shooting images to look a certain way to help communicate what their brand is all about. So leveraging those assets has been terrific.

[Regarding inventory], there’s no reason to ship the product from the brand to another warehouse and then to the consumer. We’re cutting out that stuff and shipping it direct from the brand. From a consumer standpoint, you order on our app, and everything is one-click, and you are charged by [us]. But then the order is placed through the brand and is shipped from the brand to you. Then we will communicate to you when it’s shipped, when it’s arriving, and if you have any customer service issues, we take care of it.

And we take a flat commission [on sales].

TC: Returns are free. But isn’t that a huge cost center, and might it deter people from returning items if you charged something for returns?

JB: My feeling is that free shipping and free returns is a baseline requirement to offer a great service. And it’s our job to help match [shoppers] to product that you’re not going to return. We have an enormous goal to have the lowest return rate in the industry. It will obviously take us some time to get there. But we believe that by making sure that we understand what works for you and what doesn’t, we can get [there].

TC: You raised $30 million last year. Are you in the market for a Series B? What will you have to show investors toward that end?

JB: The logic behind the dollar amount that we raised was: how much do we need to build what we want to build, and then bring it to market and get traction? And so that is our goal that starts tomorrow. . .

TC: How has this current reality altered your plans? Launching during a pandemic isn’t what you were imagining, obviously.

JB: No, it is not. [Laughs.] I don’t know that any of us could have possibly. We did delay our launch; we were originally launching in March, and once COVID hit, we needed to make sure we could see straight and understand the impact. I think as time has passed, we have felt more and more compelled to get out there to help our brands, all of whom are feeling the impact of the retail stores closing, or orders being canceled by their retail partners. They’re all businesses and many of them small businesses, so we want to help them.

It’s also an interesting time because we all need a little bit of levity and escape. And the app really is a fun escape.

Powered by WPeMatico

David Renteln, the Los Angeles-based co-founder of Soylent and the co-founder and chief executive of new nicotine gum manufacturer Lucy Goods, thinks there should be a better-tasting, less-medicinal offering for people looking to quit smoking.

That’s why he founded Lucy Goods, and that’s why investors, including RRE Ventures, Vice Ventures and FundRX joined previous investors YCombinator and Greycroft in backing the company with $10 million in new funding.

“We reformulated nicotine gum and the improvements that we made were to the taste, the texture and the nicotine release speed,” said Renteln.

These days, any startup that’s working on smoking cessation or working with tobacco products can’t avoid comparisons to Juul — the multi-billion-dollar startup that’s at the center of the surge in teen nicotine consumption.

“The Juul comparison is something that’s obviously top of people’s minds,” Renteln said. “It’s important to note that there’s a huge difference in nicotine products.”

Renteln points to statements from former Food and Drug Administration chief, Scott Gottlieb (who’s now a partner at the venture firm New Enterprise Associates), which drew a distinction between combustible tobacco products on one end and nicotine gums and patches on the other.

“Nicotine isn’t the principle agent of harm associated with these tobacco products,” said Rentlen. “It’s addictive but not inherently bad for you.”

Lucy Goods also doesn’t release its nicotine dosage in a concentrated burst like vapes, which are designed to replicate the head rush associated with smoking a cigarette, said Renteln.

“It is a stimulant and they will get a sensation, but it’s not as intense as taking a very deep drag of a cigarette,” Renteln said.

The company’s website also doesn’t skew to young, lifestyle marketing images. Instead, there are testimonials from older, ex-smokers hawking the Lucy gum.

“I don’t want anyone underage using any nicotine product or any drug in general… [and] the flavors have been around for a long time.”

Joining Renteln in the quest to create a better nicotine gum is Samy Hamdouche, a former business development executive at several Southern California biotech startups and the previous vice president of research at Soylent.

For both men, the idea is to get a new product to market that can help people quit smoking — without a social stigma — Renteln said.

“Smoking is the leading cause of preventable death in the United States claiming over 480,000 lives every year and costing the U.S. an estimated $300 billion in direct health costs and lost productivity. Lucy is committed to bringing innovative nicotine products to the market to eliminate tobacco related harm and we’re proud to be part of their journey,” said RRE investor, Jason Black in a statement.

Powered by WPeMatico

In part two of a survey that asks top VCs about exciting opportunities in open source and dev tools, we dig into responses from 10 leading open-source-focused investors at firms that span early to growth stage across software-specific firms, corporate venture arms and prominent generalist firms.

In the conclusion to our survey, we’ll hear from:

These responses have been edited for clarity and length.

Powered by WPeMatico

E-commerce phenom and D2C bright light Casper has filed to go public.

The New York-based company that raised nearly $340 million while private, according to Crunchbase data, expects to trade on the New York Stock Exchange under the ticker symbol “CSPR.” Its S-1 filing includes a $100 million placeholder figure for its possible capital raise.

The company will need the money, as it loses money and burns cash. Let’s explore just how a mattress company does that.

In the full years of 2017 and 2018, Casper recorded revenue of $250.9 million (net of $45.7 million in “refunds, returns, and discounts”) and $357.9 million (net of $80.7 million in “refunds, returns, and discounts”). That worked out to growth of 42.6% in the year.

Over the same two periods, Casper lost $73.4 million and $92.1 million on a net basis, respectively.

In the first three quarters of 2019 versus 2018, Casper put up $312.3 million in top line (net of $80.1 million in “refunds, returns, and discounts”), up just over 20% from its year-ago three-quarter tally of $259.7 million in revenue (net of $57.7 million in “refunds, returns, and discounts”).

The company’s net loss during the three-quarter period rose from $64.2 million in 2018 to $67.4 million in 2019. The company’s net losses are generally rising (though slowly so far in 2019), while its growth decelerates.

In contrast, and to the company’s favor, its operating cash burn is slowing. From $84.0 million in 2017 to $72.3 million in calendar 2018, Casper slowed its operating cash consumption further in 2019, to just $29.7 million in the first three quarters of the year, compared to $44.9 million over the same period of the preceding year.

But the company’s slowing growth and stiff losses using regular accounting methods (GAAP) could strain its valuation. Casper was valued at $1.1 billion in its most recent funding round.

While the company’s gross margins aren’t bad for a non-software company (49.6% in the first nine months of 2019), the firm spent over 73% of its gross profit last year on sales and marketing costs. That figure indicates that Casper spent heavily to generate growth, growth that came in at about 20% so far in 2019, as reported.

That fact implies that growth will remain constrained, as the firm can’t afford to spend too much more on the line item. Which begs the question: What’s the value of a firm that is showing slowing growth, non-recurring revenue and sticky GAAP losses?

The company’s adjusted losses aren’t much better. Looking at its adjusted EBITDA, a profit metric so distorted to flatter that it’s nigh a funhouse mirror, Casper only marginally improved on its 2018 tally looking at the first three quarters of that year (-$57.5 million) in 2019 (-$53.8 million).

Casper has raised from IVP, Lerer Hippeau, Target and New Enterprise Associates. The firm raised seed capital back in 2014 along with a Series A. Lerer and NEA were most active back then, looking at its funding history.

The company raised $55 million more in 2015, and a far-larger $170 million in mid-2017. A $100 million round came in 2019 that set it up for its 2020 IPO.

This company’s IPO is a pricing question. And one that will impact a host of startups that both compete directly with Casper or operate in a different vertical with a similar business. Get hype.

Powered by WPeMatico

The Valley’s affinity for robotics shows no signs of cooling. Technical enhancements through innovations like AI/ML, compute power and big data utilization continue to drive new performance milestones, efficiencies and use cases.

Despite the old saying, “hardware is hard,” investment in the robotics space continues to expand. Money is pouring in across robotics’ billion-dollar sub verticals, including industrial and labor automation, drone delivery, machine vision and a wide range of others.

According to data from Pitchbook and Crunchbase, 2018 saw new highs for the number of venture deals and total invested capital in the space, with roughly $5 billion in investment coming from nearly 400 deals. With robotics well on its way to again set new investment peaks in 2019, we asked 13 leading VCs who work at firms spanning early to growth stages to share what’s exciting them most and where they see opportunity in the sector:

Participants discuss the compelling business models for robotics startups (such as “Robots as a Service”), current valuations, growth tactics and key robotics KPIs, while also diving into key trends in industrial automation, human replacement, transportation, climate change, and the evolving regulatory environment.

Which trends are you most excited in robotics from an investing perspective?

The opportunity to unlock human superpowers:

- Increase productivity to enhance creativity leading to new products and businesses.

- Automating dangerous tasks and eliminating undesirable, dangerous jobs in mining, manufacturing, and shipping/logistics.

- Making the most deadly mode of transport: driving, 100% safe.

How much time are you spending on robotics right now? Is the market under-heated, overheated, or just right?

- Three-quarters of the new opportunities I look at involve some sort of automation.

- The market for robot startups attempting direct human labor replacement, floor-sweeping, and dumb-waiter robots, and robotic lawnmowers and vacuums is OVER heated (too many startups).

- The market for robot startups that assist human workers, increase human productivity, and automate undesirable human tasks is UNDER heated (not enough startups).

Are there startups that you wish you would see in the industry but don’t? Plus any other thoughts you want to share with TechCrunch readers.

I want to see more founders that are building robotics startups that:

- Solve LATENT pain points in specific, well-understood industries (vs. building a cool robot that can do cool things).

- Focus on increasing HUMAN productivity (vs. trying to replace humans).

- Are solving for building interesting BUSINESSES (vs. emphasizing cool robots).

Three years ago, the most compelling companies to us in the industrial space were in software. We now spend significantly more time in verticalized AI and hardware. Robotic companies we find most exciting today are addressing key driver areas of (1) high labor turnover and shortage and (2) new research around generalization on the software side. For many years, we have seen some pretty impressive science projects out of labs, but once you take these into the real world, they fail. In these changing environmental conditions, it’s crucial that robots work effectively in-the-wild at speeds and economics that make sense. This is an extremely difficult combination of problems, and we’re now finally seeing it happen. A few verticals we believe will experience a significant overhaul in the next 5 years include logistics, waste, micro-fulfillment, and construction.

With this shift in robotic capability, we’re also seeing a shift in customer sentiment. Companies who are used to buying outright machines are now more willing to explore RaaS (Robot as a Service) models for compelling robotic solutions – and that repeat revenue model has opened the door for some formerly enterprise software-only investors. On the other hand, companies exploring robotics in place of tasks with high labor shortages, such as trucking or agriculture, are more willing to explore per hour or per unit pick models.

Adoption won’t be overnight, but in the medium term, we are very enthusiastic about the ways robotics will transform industries. We do believe investing in this space requires the right technical know-how and network to evaluate and support companies, so momentum investors looking to dip their hand into a hot space may be disappointed.

We’re entering the early stages of the golden age of robotics. Robotics is already a huge, multibillion-dollar market – but today that market is dominated by industrial robotics, such as welding and assembly robots found on automotive assembly lines around the world. These robots repeat basic tasks, over and over, and are usually separated by caged walls from humans for safety. However, this is rapidly changing. Advances in perception, driven by deep learning, machine vision and inexpensive, high-performance cameras allow robots to safely navigate the real world, escape the manufacturing cages, and closely interact with humans.

I think the biggest opportunities in robotics are those which attack enormous markets where it’s difficult to hire and retain labor. One great example is long-haul trucking. Highway driving represents one of the easiest problems for autonomous vehicles, since the lanes tend to be well-marked, the roads have gentle curves, and all traffic runs in the same direction. In the United States alone, long haul trucking is a multi-hundred billion dollar market every year. The customer set is remarkably scalable with standard trailer sizes and requirements for shipping freight. Yet at the same time, trucking companies have trouble hiring and retaining drivers. It’s the perfect recipe for robotic opportunity.

I’m intrigued by agricultural robots. I’ve seen dozens of companies attacking every part of the farming equation – from field clearing and preparation, to seeding, to weeding, applying fertilizer, and eventually harvesting. I think there’s a lot of value to be “harvested” here by robots, especially since seasonal field labor is becoming harder to find and increasingly expensive. One enormous challenge in this market, however, is that growing seasons mean that the robotic machinery has a lot of downtime and the cost of equipment isn’t as easily amortized in other markets with higher utilization. The other big challenge is that fields are very, very tough on hardware and electronics due to environmental conditions like rain, dust and mud.

There are a ton of important problems to be solved in robotics. The biggest open challenges in my mind are locomotion and grasping. Specifically, I think that for in-building applications, robots need to be able to do all the thing which humans can do – specifically opening and closing doors, climbing stairs, and picking items off of shelves and putting them down gently. Plenty of startups have tackled subsets of these problems, but to date no one has built a generalized solution. To be fair, to get to parity with humans on generalized locomotion and grasping, it’s probably going to take another several decades.

Overall, I feel like the funding environment for robotics is about right, with a handful of overfunded areas (like autonomous passenger vehicles). I think that the most overlooked near-term opportunity in robotics is teleoperation. Specifically, pairing fully automated robotic operations with occasional human remote operation of individual robots. Starship Technologies is a perfect example of this. Starship is actively deploying local delivery robots around the world today. Their first major deployment is at George Mason University in Virginia. They have nearly 50 active robots delivering food around the campus. They’re autonomous most of the time, but when they encounter a problem or obstacle they can’t solve, a human operator in a teleoperation center manually controls the robot remotely. At the same time. Starship tracks and prioritizes these problems for engineers to solve, and slowly incrementally reduces the number of problems the robots can’t solve on their own. I think people view robotics as a “zero or one” solution when in fact there’s a world where humans and robots work together for a long time.

Powered by WPeMatico

Before Tableau was the $15.7 billion key to Salesforce’s problems, it was a couple of founders arguing with a couple of venture capitalists over lunch about why its Series A valuation should be higher than $12 million pre-money.

Salesforce has generally been one to signify corporate strategy shifts through their acquisitions, so you can understand why the entire tech industry took notice when the cloud CRM giant announced its priciest acquisition ever last month.

The deal to acquire the Seattle-based data visualization powerhouse Tableau was substantial enough that Salesforce CEO Marc Benioff publicly announced it was turning Seattle into its second HQ. Tableau’s acquisition doesn’t just mean big things for Salesforce. With the deal taking place just days after Google announced it was paying $2.6 billion for Looker, the acquisition showcases just how intense the cloud wars are getting for the enterprise tech companies out to win it all.

The Exit is a new series at TechCrunch. It’s an exit interview of sorts with a VC who was in the right place at the right time but made the right call on an investment that paid off. [Have feedback? Shoot me an email at lucas@techcrunch.com]

Scott Sandell, a general partner at NEA (New Enterprise Associates) who has now been at the firm for 25 years, was one of those investors arguing with two of Tableau’s co-founders, Chris Stolte and Christian Chabot. Desperate to close the 2004 deal over their lunch meeting, he went on to agree to the Tableau founders’ demands of a higher $20 million valuation, though Sandell tells me it still feels like he got a pretty good deal.

NEA went on to invest further in subsequent rounds and went on to hold over 38% of the company at the time of its IPO in 2013 according to public financial docs.

I had a long chat with Sandell, who also invested in Salesforce, about the importance of the Tableau deal, his rise from associate to general partner at NEA, who he sees as the biggest challenger to Salesforce, and why he thinks scooter companies are “the worst business in the known universe.”

The interview has been edited for length and clarity.

Lucas Matney: You’ve been at this investing thing for quite a while, but taking a trip down memory lane, how did you get into VC in the first place?

Scott Sandell: The way I got into venture capital is a little bit of a circuitous route. I had an opportunity to get into venture capital coming out of Stanford Business School in 1992, but it wasn’t quite the right fit. And so I had an interest, but I didn’t have the right opportunity.

Powered by WPeMatico

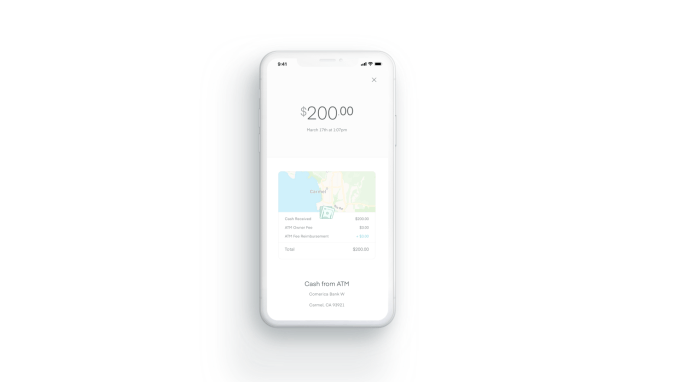

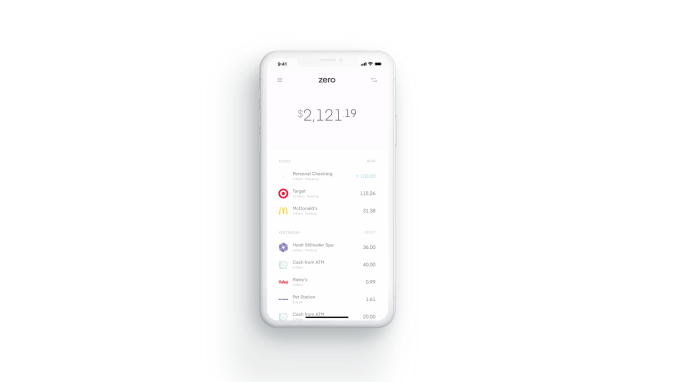

Just ahead of the launch of the Apple Card, a startup that has its own take on modernizing the credit card industry, Zero, is announcing the close of its $20 million Series A. The new round of funding was led by New Enterprise Associates (NEA), and brings Zero’s total raised to date to $35 million, including both equity and debt funding.

Other investors in the round include SignalFire, Eniac Ventures, Nyca Partners and some unnamed school endowments. Zero had previously announced an $8.5 million raise in fall 2017, led by Eniac, and had raised $7 million in venture debt from Silicon Valley Bank.

Zero has a clever idea that targets millennials’ hesitance to sign up for credit cards.

Today, only 33% of millennials have a major credit card, a Bankrate survey found — largely because they’re wary of falling into the vicious debt cycle. Instead, this younger demographic often only carries a debit card. But that also means they’re missing out on credit card benefits — like points, rewards and cash back.

Zero’s idea is to offer a rewards credit card that works like debit.

The Zerocard itself is a World Mastercard, so it earns credit card cash back. But unlike a traditional credit card, it’s combined with an FDIC-backed checking account called Zero Checking. That means Zerocard and Zero Checking work together in the app, allowing cardholders to see one net number they can spend from.

That way, they won’t make the mistake of accidentally going over budget, as is often the case with traditional credit cards, which then benefit from charging interest on the unpaid balance.

Zero co-founder and CEO Bryce Galen says he had always liked optimizing his personal finances, but didn’t see the value in overspending to chase rewards.

“People spend 10 to 15% more on average just because they’re putting it on a credit card, and not seeing where they stand all the time,” he says. “Spending 10 to 15% more to chase 1 to 2% in rewards doesn’t make sense.”

Plus, he adds, “half of all credit card points are never even redeemed.”

With Zerocard, the company does away with other credit card annoyances as well.

Zerocard doesn’t charge annual fees like many traditional credit cards do. And Zero Checking doesn’t add any additional ATM fees beyond what the ATM owner charges. It also does away with foreign transaction fees, minimum balance fees and overdraft fees — like many of today’s challenger banks.

Meanwhile, the Zero app is built with an eye toward what makes apps great.

Galen, who led product development for Zynga’s “Words with Friends” has experience in this department, while co-founder and COO Joel Washington previously co-founded car sales marketplace Shift. The executive team, combined, has backgrounds that include time at Affirm, Apple, Capital One, Dropbox, Google, Postmates, Silicon Valley Bank, Upgrade and Wells Fargo.

Overall, Zero’s design feels clean and simple, compared to the cluttered and dated apps from traditional banks. It has smart features, too, like a detailed transaction view that shows the vendor’s logo and location on a map to make it easier to recognize purchases.

“Zero creates an innovative debit-style experience, with an elegant design, and truly compelling rewards. It’s a fabulous banking experience,” said Hans Morris, managing partner of Nyca Partners and former president of Visa, Inc., in a statement. “Few people understand how complex it is to launch either a credit card or a checking account program, and I believe Zero is the first U.S. startup to launch both,” he said.

Zero launched in November 2018, but only to a small number of customers. Though officially open for business, it was functioning more like a public beta — though it didn’t call it that at the time. Meanwhile, its waitlist continued to grow.

Today, there are still 204,000 people waiting to be allowed in — something that Galen says is now going to happen.

“We haven’t launched to everyone on the waitlist yet, but we expect to within the next few weeks,” he says.

Another interesting twist on traditional credit cards is Zero’s path to card upgrades: it encourages but also rewards customers for telling their friends. By doing so, customers gain access to better-looking cards and higher cash-back percentages.

Zero customers start with a “Quartz” card offering 1% back on purchases. When a friend they refer joins, they receive a higher-level card called “Graphite” that offers 1.5% back. Two friends earns you the “Magnesium” card with 2% back and four friends gets you the “Carbon” card with 3% back. The Carbon card is also solid metal, capitalizing on the millennial trend of wanting their cards to look cool. And metal cards are in particular demand.

To receive the full cash-back rates, customers have to pay their balances in full by the due date, Zero says.

The company has partnered with Salt Lake City-based WebBank to issue the card, and deposits are held at Memphis-based Evolve Bank & Trust, an FDIC member. Zero makes money primarily on interchange and interest on deposits.

While some users may leave balances on the card that generate interest, Zero isn’t focused on that aspect of the business for revenue generation.

“Most companies in fintech today are launching undifferentiated debit cards as a feature or extension to their product for an additional engagement and monetization stream,” says Rick Yang, partner at NEA, as to why he invested.

“Zero is completely focused on their card programs and building a differentiated solution that actually provides a value proposition that resonates with consumers. We’ve also been fascinated by the growth of debit outpacing credit, and we think that our solution gives consumers the best of both worlds,” he adds.

Zero is currently iOS-only, but is working on an Android version that is expected to be ready in August.

Powered by WPeMatico

New Enterprise Associates, the 42-year-old venture capital firm, has invested in the $23 million Series B round for Mejuri, a startup capturing millennial women’s penchant for affordable and treat yo’ self type of jewelry rather than diamonds and precious stones for special occasions.

It’s the latest instance of startups drawing investor interest with their direct-to-customer retail model. Based in Toronto and Buenos Aires, four-year-old Mejuri designs, makes and sells jewelry directly to women online and through offline showrooms, bypassing middle-person costs. Besides striving for reasonable prices, Mejuri also wants to upend an entrenched practice in its industry.

Traditional jewelry, the startup points out, targets men for gifting and makes higher markups acceptable. With its D2C play, Mejuri believes it’s putting the purchasing decision back with women; indeed, it found 75 percent of its customers are buying for themselves. Its team of 120 employees is constantly on the watch for trends and consumer feedback, a strategy made possible by its online presence of more than 422,000 Instagram followers. Instead of releasing large batches of seasonal pieces, Mejuri adapts the so-called “drop” model that introduces only a small quantity of products each week, which allows it to timely translate customer sentiments into designs.

Photo source: Mejuri

Another enabling factor is the company’s female-led team: 80 percent of the staff are women, headed by founder Noura Sakkijha, a third-generation jeweler and a former industrial engineer who scored the company’s latest capital when she was seven months pregnant with two twins.

“Mejuri’s mission really hits home for me,” said NEA partner Vanessa Larco in a statement. “I noticed a shift in trends when none of my friends wanted to go to any of the traditional fine jewelry companies to purchase jewelry anymore, and I realized a lot of those big brands were in trouble.”

Natalie Massenet, founder of Net-a-Porter and partner at Imaginary, another venture fund that participated in Mejuri’s Series B, said the startup is set to “disrupt” the jewelry industry through supply chain standards that modern consumers demand, “like sourcing from conflict-free and socially responsible diamond suppliers and maintaining affordable prices to serve a consumer who is buying for herself and her friends.”

The user-centric focus has brought customer loyalty to Mejuri. The startup claims that 30 percent of its monthly transactions come from returning shoppers, and 70,000 customers are on the waitlist for its products. It’s accumulated a total of 20 million visitors to its website and released 1,500 designs since launch. Revenues have quadrupled year-over-year for the fourth consecutive year, and the company, one of TechCrunch’s favorite picks from 500 Startups’ Batch 15 Demo Day three years ago, said it’s on track to achieve the same level of traction in 2019.

The new proceeds bring Mejuri’s total funds raised to more than $29 million to date. Others in the new funding round include follow-on backers Felix Capital, BDC Capital, Incite Ventures and Dash Ventures. The company plans to spend its latest financial injection on offline expansion, overseas growth and investment in branding and customer experience.

Powered by WPeMatico