neologisms

Auto Added by WPeMatico

Auto Added by WPeMatico

Everyone at an organization should own growth, right? Turns out when everyone owns something, no one does. As a result, growth teams can cause an enormous amount of friction in an organization when introduced.

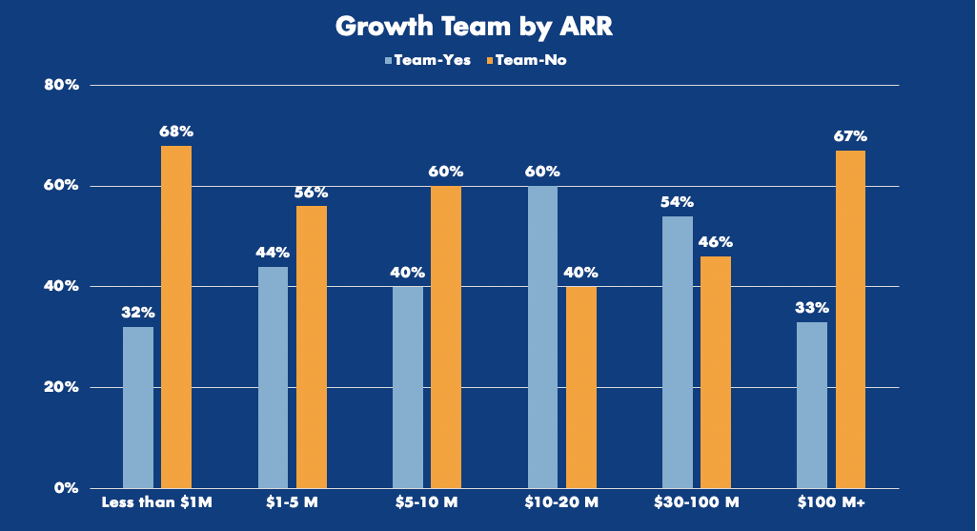

Growth teams are twice as likely to appear among businesses growing their ARR by 100% or more annually. What’s more, they also seem to be more common after product-market fit has been achieved — usually after a company has reached about $5 million to $10 million in revenue.

Image Credits: OpenView Partners

I’m not here to sell you on why you need a growth team, but I will point out that product-led businesses with a growth team see dramatic results — double the median free-to-paid conversion rate.

Image Credits: OpenView Partners

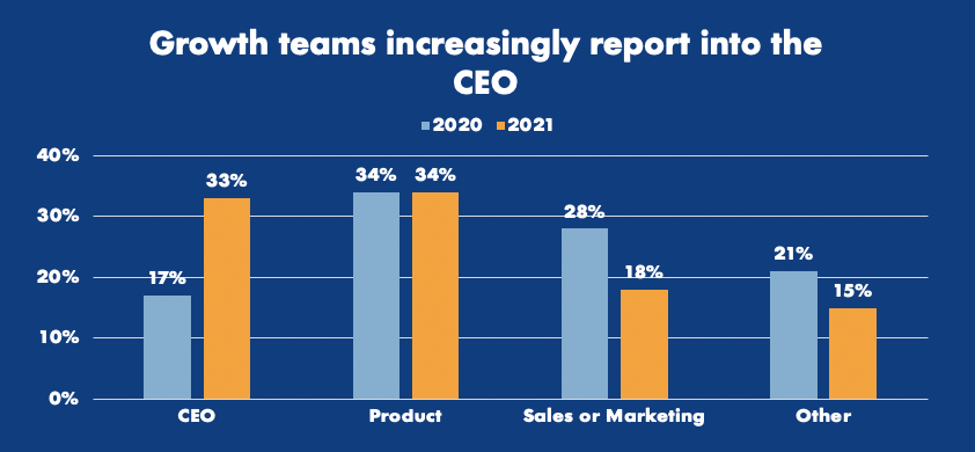

According to responses from product benchmarks surveys, growth teams have transitioned dramatically from reporting to marketing and sales to reporting directly to the CEO.

Some of the early writing on growth teams says that they can be structured individually as their own standalone team or as a SWAT model, where experts from various other departments in the organization converge on a regular cadence to solve for growth.

Image Credits: OpenView Partners

My experience, and the data I’ve collected from business-user focused software companies, has led me to the conclusion that growth teams in business software should not be structured as “SWAT” teams, with cross-functional leadership coming together to think critically about growth problems facing the business. I find that if problems don’t have a real owner, they’re not going to get solved. Growth issues are no different and are often deprioritized unless it’s someone’s job to think about them.

Becoming product-led isn’t something that happens overnight, and hiring someone will not be a silver bullet for your software.

I put early growth hires into a few simple buckets. You’ve got:

Product-minded growth experts: These folks are all about optimizing the user experience, reducing friction and expanding usage. They’re usually pretty analytical and might have product, data or MarketingOps backgrounds.

Powered by WPeMatico

Airbnb may be another overvalued “unicorn,” but it’s no WeWork.

The Information this morning reported new Airbnb financials — indicating a massive increase in operating losses — that immediately call Airbnb’s future into question. Precisely, Airbnb lost $306 million on operations on $839 million in revenue, namely as a result of marketing spend, in the first quarter of 2019. In total, Airbnb invested $367 million in sales and marketing, representing a 58% increase year-over-year, in Q1. The company is gearing up for a major liquidity event next year and is making a concerted effort to rake in new customers, as any soon-to-be-public business would.

Given WeWork’s sudden demise, coupled with Uber and Lyft’s lukewarm performances on the stock markets, many have wondered how Wall Street will respond to Airbnb’s eventual IPO prospectus. Will money managers have an appetite for another over-valued Silicon Valley darling? Or will the market compete like mad for shares in the massive home-sharing marketplace?

But Airbnb, again, is no WeWork, and I wager Wall Street will have a much friendlier approach to its offering. For one, Airbnb’s co-founder and chief executive officer Brian Chesky isn’t dropping $60 million on private jets — I don’t think. CEO behaviors aside, Airbnb has more capital in the bank than it has raised in its entire 11-year history, which is a whole lot of money. This is all according to a source who is familiar with Airbnb’s financials and shared this detail with TechCrunch following The Information’s Thursday morning report. As for Airbnb, the company told TechCrunch, “we can’t comment on the figures, but 2019 is a big investment year in support of our hosts and guests.”

")

Airbnb’s CEO Brian Chesky speaks at TechCrunch Disrupt SF 2014

Airbnb has attracted more than $3.5 billion in equity funding at a $31 billion valuation and has even more locked away in its bank account. Additionally, Airbnb has an untouched $1 billion credit line, the source said. Presumably, the referenced credit line is the 2016 $1 billion debt financing from JPMorgan, CitiGroup, Morgan Stanley and others.

Moreover, Airbnb has been “cumulatively” free cash flow positive for some time, meaning that it’s seen more money coming in than going out during recent quarters, according to our source. It has been reported that Airbnb surpassed $1 billion in revenue in the second quarter of 2019 and in the third quarter of 2018, but we’re guessing the business did not top $1 billion in Q4 of 2018 or Q1 of 2019 because it if had, that information would probably have been “leaked.”

Finally, Airbnb has been profitable on an EBITDA (earnings before interest, taxes, depreciation and amortization) basis for two consecutive years, the company announced in January. Gross bookings, meanwhile, are growing, as is Airbnb’s business offering and its experiences product.

Powered by WPeMatico

Federal authorities have announced its latest crackdown on illegal robocallers — taking close to a hundred actions against several companies and individuals blamed for the recent barrage of spam calls.

In the so-called “Operation Call It Quits,” the Federal Trade Commission brought four cases — two filed on its behalf by the Justice Department — and three settlements in cases said to be responsible for making more than a billion illegal robocalls.

Several state and local authorities also brought actions as part of the operation, officials said.

Each year, billions of automatically dialed or spoofed phone calls trick millions into picking up the phone. An annoyance at least, at worse it tricks unsuspecting victims into turning over cash or buying fake or misleading products. So far, the FTC has fined companies more than $200 million but only collected less than 0.01% of the fines because of the agency’s limited enforcement powers.

In this new wave of action, the FTC said it will send a strong signal to the robocalling industry.

Andrew Smith, director of the FTC’s Bureau of Consumer Protection, said Americans are “fed up” with the billions of robocalls received every year. “Today’s joint effort shows that combatting this scourge remains a top priority for law enforcement agencies around the nation,” he said.

It’s the second time the FTC has acted in as many months. In May, the agency also took action against four companies accused of making “billions” of robocalls.

The FTC said its latest action brings the number of robocall violators up to 145.

Several of the cases involved shuttering operations that offer consumers “bogus” credit card interest rate reduction services, which the FTC said specifically targeted seniors. Other cases involved the use of illegal robocalls to promote money-making schemes.

Another cases included actions against Lifewatch, a company pitching medical alert systems, which the FTC contended uses spoofed caller ID information to trick victims into picking up the phone. The company settled for $25.3 million. Meanwhile, Redwood Scientific settled for $18.2 million, suspended due to the inability for defendant Danielle Cadiz to pay, for “deceptively” marketing dentistry products, according to the FTC’s complaint.

The robocalling epidemic has caught the attention of the Federal Communications Commission, which regulates the telecoms and internet industries. Last month, its commissioners proposed a new rule that would make it easier for carriers to block robocalls.

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a newsletter published every Saturday that dives into the week’s noteworthy venture capital deals, funds and trends. Before I dive into this week’s topic, let’s catch up a bit. Last week, I wrote about the sudden uptick in beverage startup rounds. Before that, I noted an alternative to venture capital fundraising called revenue-based financing. Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets.

Here’s what I’ve been thinking about this week: Unicorn scarcity, or lack thereof. I’ve written about this concept before, as has my Equity co-host, Crunchbase News editor-in-chief Alex Wilhelm. I apologize if the two of us are broken records, but I think we’re equally perplexed by the pace at which companies are garnering $1 billion valuations.

Here’s the latest data, according to Crunchbase: “2018 outstripped all previous years in terms of the number of unicorns created and venture dollars invested. Indeed, 151 new unicorns joined the list in 2018 (compared to 96 in 2017), and investors poured more than $135 billion into those companies, a 52% increase year-over-year and the biggest sum invested in unicorns in any one year since unicorns became a thing.”

2019 has already coined 42 new unicorns, like Glossier, Calm and Hims, a number that grows each and every week. For context, a total of 19 companies joined the unicorn club in 2013 when Aileen Lee, an established investor, coined the term. Today, there are some 450 companies around the globe that qualify as unicorns, representing a cumulative valuation of $1.6 trillion.

We’ve clung to this fantastical terminology for so many years because it helps us classify startups, singling out those that boast valuations so high, they’ve gained entry to a special, elite club. In 2019, however, $100 million-plus rounds are the norm and billion-dollar-plus funds are standard. Unicorns aren’t rare anymore; it’s time to rethink the unicorn framework.

Petition to stop using the term “unicorn” unless the company is valued at more than $1 billion *and* profitable.

— Kate Clark (@KateClarkTweets) May 22, 2019

Last week, I suggested we only refer to profitable companies with a valuation larger than $1 billion as unicorns. Understandably, not everyone was too keen on that idea. Why? Because startups in different sectors face barriers of varying proportions. A SaaS company, for example, is likely to achieve profitability a lot quicker than a moonshot bet on autonomous vehicles or virtual reality. Refusing startups that aren’t yet profitable access to the unicorn club would unfairly favor certain industries.

So what can we do? Perhaps we increase the valuation minimum necessary to be called a unicorn to $10 billion? Initialized Capital’s Garry Tan’s idea was to require a startup have 50% annual growth to be considered a unicorn, though that would be near-impossible to get them to disclose…

While I’m here, let me share a few of the other eclectic responses I received following the above tweet. Joseph Flaherty said we should call profitable billion-dollar companies Pegasus “since [they’ve] taken flight.” Reagan Pollack thinks profitable startups oughta be referred to as leprechauns. Hmmmm.

The suggestions didn’t stop there. Though I’m not so sure adopting monikers like Pegasus and leprechaun will really solve the unicorn overpopulation problem. Let me know what you think. Onto other news.

Image by Rafael Henrique/SOPA Images/LightRocket via Getty Images

CrowdStrike has set its IPO terms. The company has inked plans to sell 18 million shares at between $19 and $23 apiece. At a midpoint price, CrowdStrike will raise $378 million at a valuation north of $4 billion.

Slack inches closer to direct listing. The company released updated first-quarter financials on Friday, posting revenues of $134.8 million on losses of $31.8 million. That represents a 67% increase in revenues from the same period last year when the company lost $24.8 million on $80.9 million in revenue.

Online lender SoFi has quietly raised $500M led by Qatar

Groupon co-founder Eric Lefkofsky just-raised another $200M for his new company Tempus

Less than 1 year after launching, Brex eyes $2B valuation

Password manager Dashlane raises $110M Series D

Enterprise cybersecurity startup BlueVoyant raises $82.5M at a $430M valuation

Talkspace picks up $50M Series D

TaniGroup raises $10M to help Indonesia’s farmers grow

Stripe and Precursor lead $4.5M seed into media CRM startup Pico

Maveron, a venture capital fund co-founded by Starbucks mastermind Howard Schultz, has closed on another $180 million to invest in early-stage consumer startups. The capital represents the firm’s seventh fundraise and largest since 2000. To keep the fund from reaching mammoth proportions, the firm’s general partners said they turned away more than $70 million amid high demand for the effort. There’s more where that came from, here’s a quick look at the other VCs to announce funds this week:

This week, I penned a deep dive on Slack, formerly known as Tiny Speck, for our premium subscription service Extra Crunch. The story kicks off in 2009 when Stewart Butterfield began building a startup called Tiny Speck that would later come out with Glitch, an online game that was neither fun nor successful. The story ends in 2019, weeks before Slack is set to begin trading on the NYSE. Come for the history lesson, stay for the investor drama. Here are the other standout EC pieces of the week.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I debate whether the tech press is too negative or too positive in its coverage of tech startups. Plus, we dive into Brex’s upcoming round, SoFi’s massive raise and CrowdStrike’s imminent IPO.

Powered by WPeMatico

The San Francisco Bay Area is a global powerhouse at launching startups that go on to dominate their industries. For locals, this has long been a blessing and a curse.

On the bright side, the tech startup machine produces well-paid tech jobs and dollars flowing into local economies. On the flip side, it also exacerbates housing scarcity and sky-high living costs.

These issues were top-of-mind long before the unicorn boom: After all, tech giants from Intel to Google to Facebook have been scaling up in Northern California for over four decades. Lately however, the question of how many tech giants the region can sustainably support is getting fresh attention, as Pinterest, Uber and other super-valuable local companies embark on the IPO path.

The worries of techie oversaturation led us at Crunchbase News to take a look at the question: To what extent do tech companies launched and based in the Bay Area continue to grow here? And what portion of employees work elsewhere?

For those agonizing about the inflationary impact of the local unicorn boom, the data offers a bit of reassurance. While companies founded in the Bay Area rarely move their headquarters, their workforces tend to become much more geographically dispersed as they grow.

Just because a company is based in Northern California doesn’t mean most workers are there also. Headquarters, our survey shows, does not always translate into headcount.

“Headquarters location can often be the wrong benchmark to use to identify where employees are located,” said Steve Cadigan, founder of Cadigan Talent Ventures, a Silicon Valley-based talent consultancy. That’s particularly the case for large tech companies.

Among the largest technology employers in Northern California, Crunchbase News found most have fewer than 25 percent of their full-time employees working in the city where they’re headquartered. We lay out the details for 10 of the most valuable regional tech companies in the chart below.

With the exception of Intel, all of these companies have a double-digit percentage of employees at headquarters, so it’s not as if they’re leaving town. However, if you’re a new hire at Silicon Valley’s most valuable companies, it appears chances are greater that you’ll be based outside of headquarters.

Tesla, meanwhile, is somewhat of a unique case. The company is based in Palo Alto, but doesn’t crack the city’s list of top 10 employers. In nearby Fremont, Calif., however, Tesla is the largest city employer, with roughly 10,000 reportedly working at its auto plant there.(Tesla has about 49,000 employees globally.)

High-valuation private and recently public tech companies can also be pretty dispersed.

Although they tend to have a larger percentage of employees at headquarters than more-established technology giants, the unicorn crowd does like to spread its wings.

Take Uber, the poster child for this trend. Although based in San Francisco, the ride-hailing giant has fewer than one-fourth of its employees there. Out of a global workforce of around 22,300, only about 5,000 are SF-based.

It’s unclear if that kind of breakdown is typical. We had trouble assembling similar geographic employee counts at other Bay Area unicorns, mainly because cities break out numbers only for their 10 largest employers. The lion’s share of regional unicorns are San Francisco-based, and of them only Uber made the Top 10.

That said, there is another, rougher methodology for assessing who works at headquarters: job postings. At a number of the most valuable Bay Area-based unicorns — including Airbnb, Juul, Lime, Instacart, Stripe and the now-public Lyft — a high number of open positions are far from the home office. And as we wrote last year, private companies have been actively seeking out cities to set up secondary hubs.

Even for earlier-stage startups, it’s not uncommon to set up headquarters in the San Francisco area for access to financing and networking, while doing the bulk of hiring in another location, Cadigan said. The evolution of collaborative work tools has also enabled more companies to add staff working remotely or in secondary offices.

Plus, of course, unicorn startups tend to be national or global in focus, and that necessitates hiring where their customers are located.

As we wrap up, it’s worth bringing up how unusual it once was for denizens of a metro area to oppose a big influx of high-skill jobs. In the past couple of years, however, these attitudes have become more common. Witness Queens residents’ mixed reactions to Amazon’s HQ2 plans. And in San Francisco, a potential surge of newly minted IPO millionaires is causing some consternation among locals, along with jubilation among the realtor crowd.

Just as college towns retain room for new students by graduating older ones, however, it seems reasonable that sustaining Northern California’s strength as a startup hub requires locating jobs out-of-area as companies scale. That could be good news for other cities, including Austin, Phoenix, Nashville, Portland and others, which have emerged as popular secondary locations for fast-growing unicorns.

That said, we’re not predicting near-term contraction in Bay Area tech employment, particularly of the startup variety. The region’s massive entrepreneurial and venture ecosystem keeps on producing valuable newcomers well-capitalized to keep hiring.

Methodology

We looked only at employment at company headquarters (except for Apple) . Companies on the list may have additional employees based in other Northern California cities. For Apple, we included all Silicon Valley employees, per estimates by the Silicon Valley Business Journal.

Numbers are rounded to the nearest hundred for the largest employers. Most of the data is for full-time employees only. Large tech employers hire predominantly full-time for staff positions, so part-time, whether included or not, is expected to reflect only a very small percentage of employment.

Cities list their 10 largest employers in annual reports. We used either the annual reports themselves or data excerpted in Wikipedia, using calendar year 2017 or 2018.

Powered by WPeMatico

It takes a lot more than a good idea and the right timing to build a billion-dollar company. Talent, focus, operational effectiveness and a healthy dose of luck are all components of a successful tech startup. Many of the most successful (or, at least, highest-valued) tech unicorns today didn’t get there alone.

Mergers and acquisitions (M&A) can be a major growth vector for rapidly scaling, highly valued technology companies. It’s a topic that we’ve covered off and on since the very first post on Crunchbase News in March 2017. Nearly two years later, we wanted to revisit that first post because things move quickly, and there is a new crop of companies in the unicorn spotlight these days. Which ones are the most active in the M&A market these days?

Before displaying the U.S. unicorns with the most acquisitions to date, we first have to answer the question, “What is a unicorn?” The term is generally applied to venture-backed technology companies that have earned a valuation of $1 billion or more. Crunchbase tracks these companies in its Unicorns hub. The original definition of the term, first applied in a VC setting by Aileen Lee of Cowboy Ventures back in late 2011, specifies that unicorns were founded in or after 2003, following the first tech bubble. That’s the working definition we’ll be using here.

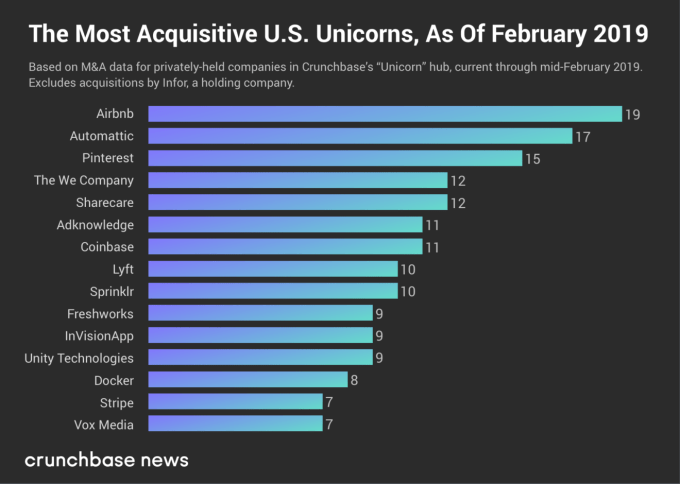

In the chart below, we display the number of known acquisitions made by U.S.-based unicorns that haven’t gone public or gotten acquired (yet). Keep in mind this is based on a snapshot of Crunchbase data, so the numbers and ranking may have changed by the time you read this. To maintain legibility and a reasonable size, we cut off the chart at companies that made seven or more acquisitions.

As one would expect, these rankings are somewhat different from the one we did two years ago. Several companies counted back in early March 2017 have since graduated to public markets or have been acquired.

Dropbox, which had acquired 23 companies at the time of our last analysis, went public weeks later and has since acquired two more companies (HelloSign for $230 million in late January 2019 and Verst for an undisclosed sum in November 2017) since doing so. SurveyMonkey, which went public in September 2018, made six known acquisitions before making its exit via IPO.

Which companies are still in the top ranks? Travel accommodations marketplace giant Airbnb jumped from number four to claim Dropbox’s vacancy as the most acquisitive private U.S. unicorn in the market. Airbnb made six more acquisitions since March 2017, most recently Danish event space and meeting venue marketplace Gaest.com. The still-pending deal was announced in January 2019.

WordPress developer and hosting company Automattic is still ranked number two. Automattic href=”https://www.crunchbase.com/acquisition/automattic-acquires-atavist–912abccd”>acquired one more company — digital publication platform Atavist — since we last profiled unicorn M&A. Open-source software containerization company Docker, photo-sharing and search site Pinterest, enterprise social media management company Sprinklr and venture-backed media company Vox Media remain, as well.

There are some notable newcomers in these rankings. We’ll focus on the most notable three: The We Company, Coinbase and Lyft. (Honorable mention goes to Stripe and Unity Technologies, which are also new to this list.)

The We Company (the holding entity for WeWork) has made 10 acquisitions over the past two years. Earlier this month, The We Company bought Euclid, a company that analyzes physical space utilization and tracks visitors using Wi-Fi fingerprinting. Other buyouts include Meetup (a story broken by Crunchbase News in November 2017) reportedly for $200 million. Also in late 2017, The We Company acquired coding and design training program Flatiron School, giving the company a permanent tenant in some of its commercial spaces.

In its bid to solidify its position as the dominant consumer cryptocurrency player, Coinbase has been on quite the M&A tear lately. The company recently announced its plans to acquire Neutrino, a blockchain analytics and intelligence platform company based in Italy. As we covered, Coinbase likely made the deal to improve its compliance efforts. In January, Coinbase acquired data analysis company Blockspring, also for an undisclosed sum. The crypto company’s other most notable deal to date was its April 2018 buyout of the bitcoin mining hardware turned cryptocurrency micro-transaction platform Earn.com, which Coinbase acquired for $120 million.

And finally, there’s Lyft, the more exclusively U.S.-focused ride-hailing and transportation service company. Lyft has made 10 known acquisitions since it was founded in 2012. Its latest M&A deal was urban bike service Motivate, which Lyft acquired in June 2018. Lyft’s principal rival, Uber, has acquired six companies at the time of writing. Uber bought a bike company of its own, JUMP Bikes, at a price of $200 million, a couple of months prior to Lyft’s Motivate purchase. Here too, the Lyft-Uber rivalry manifests in structural sameness. Fierce competition drove Uber and Lyft to raise money in lock-step with one another, and drove M&A strategy as well.

With long-term business success, it’s often a chicken-and-egg question. Is a company successful because of the startups it bought along the way? Or did it buy companies because it was successful and had an opening to expand? Oftentimes, it’s a little of both.

The unicorn companies that dominate the private funding landscape today (if not in the number of deals, then in dollar volume for sure) continue to raise money in the name of growth. Growth can come the old-fashioned way, by establishing a market position and expanding it. Or, in the name of rapid scaling and ostensibly maximizing investor returns, M&A provides a lateral route into new markets or a way to further entrench the status quo. We’ll see how that strategy pays off when these companies eventually find the exit door .

Powered by WPeMatico

Why has San Francisco’s startup scene generated so many hugely valuable companies over the past decade?

That’s the question we asked over the past few weeks while analyzing San Francisco startup funding, exit, and unicorn creation data. After all, it’s not as if founders of Uber, Airbnb, Lyft, Dropbox and Twitter had to get office space within a couple of miles of each other.

We hadn’t thought our data-centric approach would yield a clear recipe for success. San Francisco private and newly public unicorns are a diverse bunch, numbering more than 30, in areas ranging from ridesharing to online lending. Surely the path to billion-plus valuations would be equally varied.

But surprisingly, many of their secrets to success seem formulaic. The most valuable San Francisco companies to arise in the era of the smartphone have a number of shared traits, including a willingness and ability to post massive, sustained losses; high-powered investors; and a preponderance of easy-to-explain business models.

No, it’s not a recipe that’s likely replicable without talent, drive, connections and timing. But if you’ve got those ingredients, following the principles below might provide a good shot at unicorn status.

First, lose money until you’ve left your rivals in the dust. This is the most important rule. It is the collective glue that holds the narratives of San Francisco startup success stories together. And while companies in other places have thrived with the same practice, arguably San Franciscans do it best.

It’s no secret that a majority of the most valuable internet and technology companies citywide lose gobs of money or post tiny profits relative to valuations. Uber, called the world’s most valuable startup, reportedly lost $4.5 billion last year. Dropbox lost more than $100 million after losing more than $200 million the year before and more than $300 million the year before that. Even Airbnb, whose model of taking a share of homestay revenues sounds like an easy recipe for returns, took nine years to post its first annual profit.

Not making money can be the ultimate competitive advantage, if you can afford it.

Industry stalwarts lose money, too. Salesforce, with a market cap of $88 billion, has posted losses for the vast majority of its operating history. Square, valued at nearly $20 billion, has never been profitable on a GAAP basis. DocuSign, the 15-year-old newly public company that dominates the e-signature space, lost more than $50 million in its last fiscal year (and more than $100 million in each of the two preceding years). Of course, these companies, like their unicorn brethren, invest heavily in growing revenues, attracting investors who value this approach.

We could go on. But the basic takeaway is this: Losing money is not a bug. It’s a feature. One might even argue that entrepreneurs in metro areas with a more fiscally restrained investment culture are missing out.

What’s also noteworthy is the propensity of so many city startups to wreak havoc on existing, profitable industries without generating big profits themselves. Craigslist, a San Francisco nonprofit, may have started the trend in the 1990s by blowing up the newspaper classified business. Today, Uber and Lyft have decimated the value of taxi medallions.

Not making money can be the ultimate competitive advantage, if you can afford it, as it prevents others from entering the space or catching up as your startup gobbles up greater and greater market share. Then, when rivals are out of the picture, it’s possible to raise prices and start focusing on operating in the black.

You can’t lose money on your own. And you can’t lose any old money, either. To succeed as a San Francisco unicorn, it helps to lose money provided by one of a short list of prestigious investors who have previously backed valuable, unprofitable Northern California startups.

It’s not a mysterious list. Most of the names are well-known venture and seed investors who’ve been actively investing in local startups for many years and commonly feature on rankings like the Midas List. We’ve put together a few names here.

You might wonder why it’s so much better to lose money provided by Sequoia Capital than, say, a lower-profile but still wealthy investor. We could speculate that the following factors are at play: a firm’s reputation for selecting winning startups, a willingness of later investors to follow these VCs at higher valuations and these firms’ skill in shepherding portfolio companies through rapid growth cycles to an eventual exit.

Whatever the exact connection, the data speaks for itself. The vast majority of San Francisco’s most valuable private and recently public internet and technology companies have backing from investors on the short list, commonly beginning with early-stage rounds.

Generally speaking, you don’t need to know a lot about semiconductor technology or networking infrastructure to explain what a high-valuation San Francisco company does. Instead, it’s more along the lines of: “They have an app for getting rides from strangers,” or “They have an app for renting rooms in your house to strangers.” It may sound strange at first, but pretty soon it’s something everyone seems to be doing.

It’s not a recipe that’s likely replicable without talent, drive, connections and timing.

A list of 32 San Francisco-based unicorns and near-unicorns is populated mostly with companies that have widely understood brands, including Pinterest, Instacart and Slack, along with Uber, Lyft and Airbnb. While there are some lesser-known enterprise software names, they’re not among the largest investment recipients.

Part of the consumer-facing, high brand recognition qualities of San Francisco startups may be tied to the decision to locate in an urban center. If you were planning to manufacture semiconductor components, for instance, you would probably set up headquarters in a less space-constrained suburban setting.

While it can be frustrating to watch a company lurch from quarter to quarter without a profit in sight, there is ample evidence the approach can be wildly successful over time.

Seattle’s Amazon is probably the poster child for this strategy. Jeff Bezos, recently declared the world’s richest man, led the company for more than a decade before reporting the first annual profit.

These days, San Francisco seems to be ground central for this company-building technique. While it’s certainly not necessary to locate here, it does seem to be the single urban location most closely associated with massively scalable, money-losing consumer-facing startups.

Perhaps it’s just one of those things that after a while becomes status quo. If you want to be a movie star, you go to Hollywood. And if you want to make it on Wall Street, you go to Wall Street. Likewise, if you want to make it by launching an industry-altering business with a good shot at a multi-billion-dollar valuation, all while losing eye-popping sums of money, then you go to San Francisco.

Powered by WPeMatico