neobanks

Auto Added by WPeMatico

Auto Added by WPeMatico

The global venture capital bet on neobanks is massive. London-based Starling Bank has raised more than $900 million, per Crunchbase. The same data source indicates that Chime has raised $1.5 billion. Monzo has raised nearly $650 million. And the list goes on: E-commerce-focused neobank Juni raised $21.5 million last month. Novo, an SMB-focused neobank, raised $41 million in June. Nubank has raised $2.3 billion. And FairMoney has locked down more than $50 million.

On and on and on.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

But despite our general inclination to lump banking-focused fintech providers that serve consumers, business customers or both into a single bucket, there’s wide divergence in how the various neobank players are performing in the market.

Back in August 2020, The Exchange noted that many neobanks were racking up steep losses. Our read at the time was that the capital being poured into the fintech category was being invested aggressively in the name of growth. Based on recent results, that view is holding up.

But not all neobanks are the unprofitable enterprises that they once were. Chime indicated in September 2020 that it generates positive, unadjusted EBITDA. That’s a stricter profit metric than the one that Lyft used recently to claim its ascendance into the realm of profitable companies; Lyft posted positive adjusted EBITDA in its most recent quarter, but burned cash to fund its operations and posted a wide net loss in the period.

But not all neobanks are the unprofitable enterprises that they once were. Chime indicated in September 2020 that it generates positive, unadjusted EBITDA. That’s a stricter profit metric than the one that Lyft used recently to claim its ascendance into the realm of profitable companies; Lyft posted positive adjusted EBITDA in its most recent quarter, but burned cash to fund its operations and posted a wide net loss in the period.

And Starling Bank reached what it describes as profitable territory in October 2020. Things have changed since our first look into neobank results.

The trend of positive neobank news continued this June, when Revolut reported its recent financial performance. The company did post rather negative aggregate results for the 2020 period. But when we drilled down into its quarterly results, we saw the picture of a fintech company scaling its gross margins and revenues while nearly reaching adjusted net income neutrality by Q4 2020. We were impressed.

This morning, let’s add to our running dig into neobank results by parsing recently released data from Starling Bank and Monzo. As we’ll see, although some neobanks are managing to clean up their ledgers and work toward profits — or reach profitability — not all are in the black.

Powered by WPeMatico

How big is the market in India for a neobank aimed at teenagers? Scores of high-profile investors are backing a startup to find out.

Bangalore-based FamPay said on Wednesday it has raised $38 million in its Series A round led by Elevation Capital. General Catalyst, Rocketship VC, Greenoaks Capital and existing investors Sequoia Capital India, Y Combinator, Global Founders Capital and Venture Highway also participated in the new round, which brings FamPay’s to-date raise to $42.7 million.

TechCrunch reported early this month that FamPay was in talks with Elevation Capital to raise a new round.

Founded by Sambhav Jain and Kush Taneja (pictured above) — both of whom graduated from Indian Institute of Technology, Roorkee in 2019 — FamPay enables teenagers to make online and offline payments.

The thesis behind the startup, said Jain in an interview with TechCrunch, is to provide financial literacy to teenagers, who additionally have limited options to open a bank account in India at a young age. Through gamification, the startup said it’s making lessons about money fun for youngsters.

Unlike in the U.S., where it’s common for teenagers to get jobs at restaurants and other places and understand how to handle money at a young age, a similar tradition doesn’t exist in India.

After gathering the consent from parents, FamPay provides teenagers with an app to make online purchases, as well as plastic cards — the only numberless card of its kind in the country — for offline transactions. Parents credit money to their children’s FamPay accounts and get to keep track of high-ticket spendings.

In other markets, including the U.S., a number of startups including Greenlight, Step and Till Financial are chasing to serve the teenagers, but in India, there currently is no startup looking to solve the financial access problem for teenagers, said Mridul Arora, a partner at Elevation Capital, in an interview with TechCrunch.

It could prove to be a good issue to solve — India has the largest adolescent population in the world.

“If you’re able to serve them at a young age, over a course of time, you stand to become their go-to product for a lot of things,” Arora said. “FamPay is serving a population that is very attractive and at the same time underserved.”

The current offerings of FamPay are just the beginning, said Jain. Eventually the startup wishes to provide a range of services and serve as a neobank for youngsters to retain them with the platform forever, he said, though he didn’t wish to share currently what those services might be.

Image Credits: FamPay

Teens represent the “most tech-savvy generation, as they haven’t seen a world without the internet,” he said. “They adapt to technology faster than any other target audience and their first exposure with the internet comes from the likes of Instagram and Netflix. This leads to higher expectations from the products that they prefer to use. We are unique in approaching banking from a whole new lens with our recipe of community and gamification to match the Gen Z vibe.”

“I don’t look at FamPay just as a payments service. If the team is able to execute this, FamPay can become a very powerful gateway product to teenagers in India and their financial life. It can become a neobank, and it also has the opportunity to do something around social, community and commerce,” said Arora.

During their college life, Jain and Taneja collaborated and built an app and worked at a number of startups, including social network ShareChat, logistics firm Rivigo and video streaming service Hotstar. Jain said their work with startups in the early days paved the idea to explore a future in this ecosystem.

Prior to arriving at FamPay, Jain said the duo had thought about several more ideas for a startup. The early days of FamPay were uniquely challenging to the founders, who had to convince their parents about their decision to do a startup rather than joining firms or startups as had most of their peers from college. Until being selected by Y Combinator, Jain said he didn’t even fully understand a cap table and dilutions.

He credited entrepreneurs such as Kunal Shah (founder of CRED) and Amrish Rau (CEO of Pine Labs) for being generous with their time and guidance. They also wrote some of the earliest checks to the startup.

The startup, which has amassed over 2 million registered users, plans to deploy the fresh capital to expand its user base and product offerings, and hire engineers. It is also looking for people to join its leadership team, said Jain.

Powered by WPeMatico

Challenger banks continue to make significant advances in attracting customers away from the big incumbents by providing more modern, user-friendly tools to manage their money. Today, one of the trailblazers in this area, Kuda Technologies, is announcing funding to continue building out its specific ambition: to provide a modern banking service for Africans and the African diaspora, or as co-founder and CEO Babs Ogundeyi describes them, “every African on the planet, wherever you are in the world.”

The company, which currently offers mobile-first banking services in Nigeria, has picked up $25 million in a Series A being led by Valar Ventures, the firm co-founded and backed by Peter Thiel, with Target Global and other unnamed investors participating. This is the first time that Valar — which has invested in a number of fintech startups, including N26, TransferWise, Stash and, just in the last week, BlockFi and BitPanda — has backed an African startup.

Kuda currently provides services for consumers to save and spend money, and it has recently introduced overdrafts (essentially revolving credit for individuals). Ogundeyi said in an interview that the plan is to use these new funds to continue expanding its credit offerings, to build out services for businesses, to add in more integrations and to move into more markets.

The funding is coming on the heels of very strong growth for Kuda, which is co-headquartered in London and Lagos.

When we last wrote about the startup, four months ago, it had just closed a seed round of $10 million led by Target Global. That was, at the time — and I think still is — the largest-ever seed round raised by a startup out of Africa, and thus as much of a milestone for the tech industry there as it was for Kuda itself.

At the time of the seed round, Kuda had registered 300,000 customers: now, that figure has more than doubled to 650,000, and tellingly, that base is spending more money through the Kuda app.

“In November we were doing about $500 million in transactions per month,” Ogundeyi said, for services like bill payments, card transactions and phone top-ups. “We closed February at $2.2 billion.”

Image Credits: Kuda

Kuda, as we described in our profile of the company when covering its seed round, is following in the footsteps of a number of other so-called “neobanks”, building a suite of banking services with a more accessible user interface and a more modern approach: you interact with the bank using a mobile app, and in addition to basic banking services, it provides tools to help people manage their money more intelligently.

But Kuda is also different from many of these, specifically because it taps into some financial practices that are unique to its market.

As Ogundeyi describes it, most people who are employed by companies will have “salary accounts” at banks, where companies pay in a person’s wages on a regular basis. These will typically be at incumbent banks, but they do not offer the same ranges of services to customers. No mobile apps, no facilities to buy mobile top-ups or make other kinds of bill payments, no AI-based calculators to figure out your monthly spend and provide suggestions on how to manage your budget, and so on.

That has opened a gap in the market for others to provide those services in their place. Kuda’s deposits, Ogundeyi said, typically start as basic transfers that people make from those “salary accounts” elsewhere. These start out small, maybe 20% of a person’s wages, but as those users find themselves using Kuda’s payment and other tools more, they are increasing how much they transfer in each payment period.

“As the trust increases you’re naturally more comfortable having money with Kuda,” he said. The next stage from that will be people depositing money directly with Kuda. A small minority already do this, he added, although the startup “has a bit more work to do” to get more companies integrated into its platform. (This is one of the areas that will be developed with this latest round of funding.)

In turn, having more money in Kuda accounts is likely to spur another wave of services being turned on at the startup, such as loans with more competitive interest rates, because they will not just be based on how much money people have but also their spending histories on the platform. “We can offer loans to salaried customers instantly as long as their salary is with Kuda,” he said.

Much of this is being enabled because of how Kuda is built. A lot of challenger banks have tapped into a world of finance and banking APIs built by another wave of fintech startups, partnering with other banks to provide backend deposit and other services: their value-add is in building efficient customer service and tools to help people manage and borrow money in smarter ways.

Kuda, on the other hand, has its own microfinance banking license from the central bank of Nigeria. This means that on top of building those same money management services, Kuda can also issue debit cards (in partnership with Visa and Mastercard), manage payments and transfers, and build all of the services in the stack itself, including those salary account services and loans. (Kuda does have partnerships with incumbent banks, specifically Zenith Bank, Guaranteed Trust and Access Bank, for people to come in for physical deposits and withdrawals when needed.)

While the service is still only live in Nigeria, the “vision is still to serve all Africans in Africa as well as outside of it,” Ogundeyi said.

The first step of that will likely be Nigerians outside of Nigeria — most likely in the U.K., where Kuda already has a headquarters, and where it has a ready market: London alone has been estimated to be home to upwards of 1 million Nigerian immigrants and people of Nigerian descent (the number of U.K. residents actually born in Nigeria is considerably smaller, more like 200,000: that is the diaspora at work).

He added that the startup is also at work on preparing for the next countries on the continent to expand its service, another area where this funding will go: “It will let us fast-track teams, on-the-ground operational teams,” he said.

The bigger picture is that the market for financial services targeting Africans has been on a significant upswing and so we will be seeing a lot more activity coming out of the region, not just from home-grown startups, but also out of other tech companies increasingly doing more business in that part of the world.

Cases in point: In addition to Stripe acquiring Nigerian payments company Paystack last year, just earlier this week, PayPal announced a deal with Flutterwave to bring PayPal services to more merchants in the region — specifically so that PayPal customers can pay merchants in the region using PayPal rails. Square’s CEO, Jack Dorsey, meanwhile, never did make his intended move to the continent — COVID-19 has derailed many plans, as we all know — but it shows that the company is trying not to overlook opportunities there, either.

PayPal, to be clear, has been active in Nigeria since 2014, but partnering with a significant player in the region represents an important step for it: Flutterwave itself earlier this month raised $170 million and became Africa’s latest unicorn, in what is still a pretty small list.

The fact that there is so much more to be done with payments and more financial services leaves the door open wide for Kuda to move in a number of different directions if it chooses. Having customers in two countries, especially with one foot in the developed market and another in an emerging market, for example, gives the company an interesting window into the world of remittances.

Money transfer has been one of the very biggest, and most important financial services for African diasporas — alongside those from many other emerging markets.

Even in cases where people are “unbanked” and have no other financial footprints, they have been turning to remittance services to send money home to their families from abroad. Kuda, with its integrations into people’s salaries, could easily become an efficient, one-stop-shop conduit for that activity too. (That’s one reason, likely, that remittance startup, Remitly, has also moved into starting to offer accounts to its users in originating countries.)

All of this to say that Valar’s making a new kind of bet here, but one laden with possibilities and a differentiated approach compared to the rest of its investment activities.

“Nigeria is at a tipping point in the adoption of digital banking,” noted Andrew McCormack, a general partner and co-founder at Valar, who led its investment here. “With the rapidly growing, youthful population who are open to new financial alternatives, Kuda is well-positioned to benefit and will transform the landscape of African banking. We are excited to lead their Series A and continue on the journey alongside Kuda.”

Powered by WPeMatico

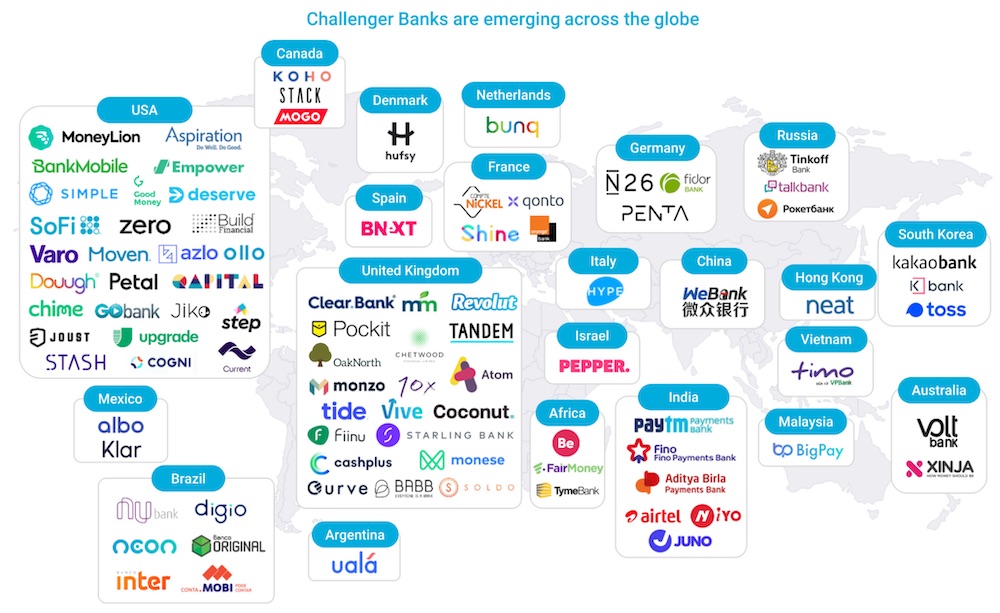

The neobank, or digital bank, phenomenon continues to take the world by storm, with global winners, from Brazil’s Nubank valued at $10 billion and Berlin’s N26 valued at $3.5 billion, to Chime, now valued at $14.5 billion as the most valuable consumer fintech in the United States.

Neobanks have led the charge of the $3.6 billion in venture capital funding for consumer fintech startups this year. And as the coronavirus-fueled acceleration of digital transformation continues, it seems the digital bank is here to stay, with some estimates pointing to neobanks reaching 60 million customers in North America and Europe by the end of 2020, and surpassing 145 million by 2024.

The space is also becoming more crowded, a trend which will only accelerate with fintech eating the world and creating greater infrastructure that enables any company to include a bank account as a product extension.

FT Partners Fintech Industry Research, January 2020

As a result, neobanks are not a monolithic model and not all are created equal. Looking underneath the hood of business models across the globe reveals remarkable operational differences and highlights specific features that are more likely to succeed in the long-term.

Today there are five distinct models that are leading globally:

Interchange-led: Relies on payments revenue, sourced through interchange as the revenue driver. Every time a customer uses the neobank’s card as a payment method they get paid [e.g. Chime / US; Neon (hybrid of 1 & 2) / Brazil].

Credit-led: Leverages a credit-first model, starting off with a credit card or similar offering, and later providing a bank account [e.g. Nubank, Neon (hybrid of 1 & 2) / Brazil].

Powered by WPeMatico

The world of consumer banking has seen a massive shift in the last ten years. Gone are the days where you could open an account, take out a loan, or discuss changing the terms of your banking only by visiting a physical branch. Now, you can do all this and more with a few quick taps on your phone screen — a shift that has accelerated with customers expecting and demanding even faster and more responsive banking services.

As one mark of that switch, today a startup called Thought Machine, which has built cloud-based technology that powers this new generation of services on behalf of both old and new banks, is announcing some significant funding — $83 million — a Series B that the company plans to use to continue investing in its platform and growing its customer base.

To date, Thought Machine’s customers are primarily in Europe and Asia — they include large, legacy outfits like Standard Chartered, Lloyds Banking Group, and Sweden’s SEB through to “challenger” (AKA neo-) banks like Atom Bank. Some of this financing will go towards boosting the startup’s activities in the US, including opening an office in the country later this year and moving ahead with commercial deals.

The funding is being led by Draper Esprit, with participation also from existing investors Lloyds Banking Group, IQ Capital, Backed and Playfair.

Thought Machine, which started in 2014 and now employs 300, is not disclosing its valuation but Paul Taylor, the CEO and founder, noted that the market cap is currently “increasing healthily.” In its last round, according to PitchBook estimates, the company was valued at around $143 million, which, at this stage of funding, puts this latest round potentially in the range of between $220 million and $320 million.

Thought Machine is not yet profitable, mainly because it is in growth mode, said Taylor. Of note, the startup has been through one major bankruptcy restructuring, although it appears that this was mainly for organisational purposes: all assets, employees and customers from one business controlled by Taylor were acquired by another.

Thought Machine’s primary product and technology is called Vault, a platform that contains a range of banking services: checking accounts, savings accounts, loans, credit cards and mortgages. Thought Machine does not sell directly to consumers, but sells by way of a B2B2C model.

The services are provisioned by way of smart contracts, which allows Thought Machine and its banking customers to personalise, vary and segment the terms for each bank — and potentially for each customer of the bank.

It’s a little odd to think that there is an active market for banking services that are not built and owned by the banks themselves. After all, aren’t these the core of what banks are supposed to do?

But one way to think about it is in the context of eating out. Restaurants’ kitchens will often make in-house what they sell and serve. But in some cases, when it makes sense, even the best places will buy in (and subsequently sell) food that was crafted elsewhere. For example, a restaurant will re-sell cheese or charcuterie, and the wine is likely to come from somewhere else, too.

The same is the case for banks, whose “Crown Jewels” are in fact not the mechanics of their banking services, but their customer service, their customer lists, and their deposits. Better banking services (which may not have been built “in-house”) are key to growing these other three.

“There are all sorts of banks, and they are all trying to find niches,” said Taylor. Indeed, the startup is not the only one chasing that business. Others include Mambu, Temenos and Italy’s Edera.

In the case of the legacy banks that work with the startup, the idea is that these behemoths can migrate into the next generation of consumer banking services and banking infrastructure by cherry-picking services from the VaultOS platform.

“Banks have not kept up and are marooned on their own tech, and as each year goes by, it comes more problematic,” noted Taylor.

In the case of neobanks, Thought Machine’s pitch is that it has already built the rails to run a banking service, so a startup — “new challengers like Monzo and Revolut that are creating quite a lot of disruption in the market” (and are growing very quickly as a result) — can integrate into these to get off the ground more quickly and handle scaling with less complexity (and lower costs).

Taylor was new to fintech when he founded Thought Machine, but he has a notable track record in the world of tech that you could argue played a big role in his subsequent foray into banking.

Formerly an academic specialising in linguistics and engineering, his first startup, Rhetorical Systems, commercialised some of his early speech-to-text research and was later sold to Nuance in 2004.

His second entrepreneurial effort, Phonetic Arts, was another speech startup, aimed at tech that could be used in gaming interactions. In 2010, Google approached the startup to see if it wanted to work on a new speech-to-text service it was building. It ended up acquiring Phonetic Arts, and Taylor took on the role of building and launching Google Now, with that voice tech eventually making its way to Google Maps, accessibility services, the Google Assistant and other places where you speech-based interaction makes an appearance in Google products.

While he was working for years in the field, the step changes that really accelerated voice recognition and speech technology, Taylor said, were the rapid increases in computing power and data networks that “took us over the edge” in terms of what a machine could do, specifically in the cloud.

And those are the same forces, in fact, that led to consumers being able to run our banking services from smartphone apps, and for us to want and expect more personalised services overall. Taylor’s move into building and offering a platform-based service to address the need for multiple third-party banking services follows from that, and also is the natural heir to the platform model you could argue Google and other tech companies have perfected over the years.

Draper Esprit has to date built up a strong portfolio of fintech startups that includes Revolut, N26, TransferWise and Freetrade. Thought Machine’s platform approach is an obvious complement to that list. (Taylor did not disclose if any of those companies are already customers of Thought Machine’s, but if they are not, this investment could be a good way of building inroads.)

“We are delighted to be partnering with Thought Machine in this phase of their growth,” said Vinoth Jayakumar, Investment Director, Draper Esprit, in a statement. “Our investments in Revolut and N26 demonstrate how banking is undergoing a once in a generation transformation in the technology it uses and the benefit it confers to the customers of the bank. We continue to invest in our thesis of the technology layer that forms the backbone of banking. Thought Machine stands out by way of the strength of its engineering capability, and is unique in being the only company in the banking technology space that has developed a platform capable of hosting and migrating international Tier 1 banks. This allows innovative banks to expand beyond digital retail propositions to being able to run every function and type of financial transaction in the cloud.”

“We first backed Thought Machine at seed stage in 2016 and have seen it grow from a startup to a 300-person strong global scale-up with a global customer base and potential to become one of the most valuable European fintech companies,” said Max Bautin, Founding Partner of IQ Capital, in a statement. “I am delighted to continue to support Paul and the team on this journey, with an additional £15 million investment from our £100 million Growth Fund, aimed at our venture portfolio outperformers.”

Powered by WPeMatico