neobank

Auto Added by WPeMatico

Auto Added by WPeMatico

Meet Vivid, a new challenger bank launching in Germany that promises low fees and an integrated cashback program. The two co-founders, Alexander Emeshev and Artem Yamanov, previously worked as executives for Russian bank Tinkoff Bank.

Vivid doesn’t try to reinvent the wheel and is building its product on top of well-established players. It relies on solarisBank for the banking infrastructure, a German company with a banking license that provides banking services as APIs to other fintech companies. As for debit cards, Vivid is working with Visa.

If you live in Germany and want to sign up to Vivid, you can expect a lot of features that you can find in other challenger banks, such as N26, but with a few additional features. Vivid users get a current account and a debit card. They can then manage their money from the mobile app.

The physical Vivid card doesn’t feature any identifiable details — there’s no card number, expiry date or CVV. Just like Apple’s credit card in the U.S., you have to check the mobile app to see those details. Every time you make a purchase, you receive a notification. You can lock and unlock your card from the app. The card works in Google Pay but not yet in Apple Pay.

In order to make money management easier, Vivid lets you create pockets. Those are sub-accounts presented in a grid view, like on Lydia or N26 Spaces. You can move money between pockets by swiping your finger from one pocket to another. Each pocket has its own IBAN.

You can associate your card with any pocket. Soon, you’ll also be able to share a pocket with another Vivid user. Like on Revolut, you can exchange money to another currency. The company adds a small markup fee but doesn’t share more details.

As for the cashback feature, the startup focuses on a handful of partnerships. You can earn 5% on purchases at REWE, Lieferando, BoFrost, Eismann, HelloFresh and Too Good To Go, and 10% on online subscriptions, such as Netflix, Prime Video, Disney+ and Nintendo Switch Online. While it’s generous, you’re limited to €20 maximum in cash back per month.

Interestingly, Vivid also wants to bring back Foursquare-style mayorship. If you often go to the same bar or café and you spend more than any other Vivid user over a two-week window, you become the mayor and receive 10% cashback.

Vivid has two plans — a free plan and a Vivid Prime subscription for €9.90 per month. Prime users receive a metal card, more cash back on everyday purchases and higher withdrawal limits.

The company plans to launch stock and ETF trading in the coming months. Vivid also plans to expand into other European countries this year.

Vivid is entering a crowded market, but already offers a solid product if everything works as expected. It’s going to be interesting to see how the product evolves and if they can attract a large user base.

Powered by WPeMatico

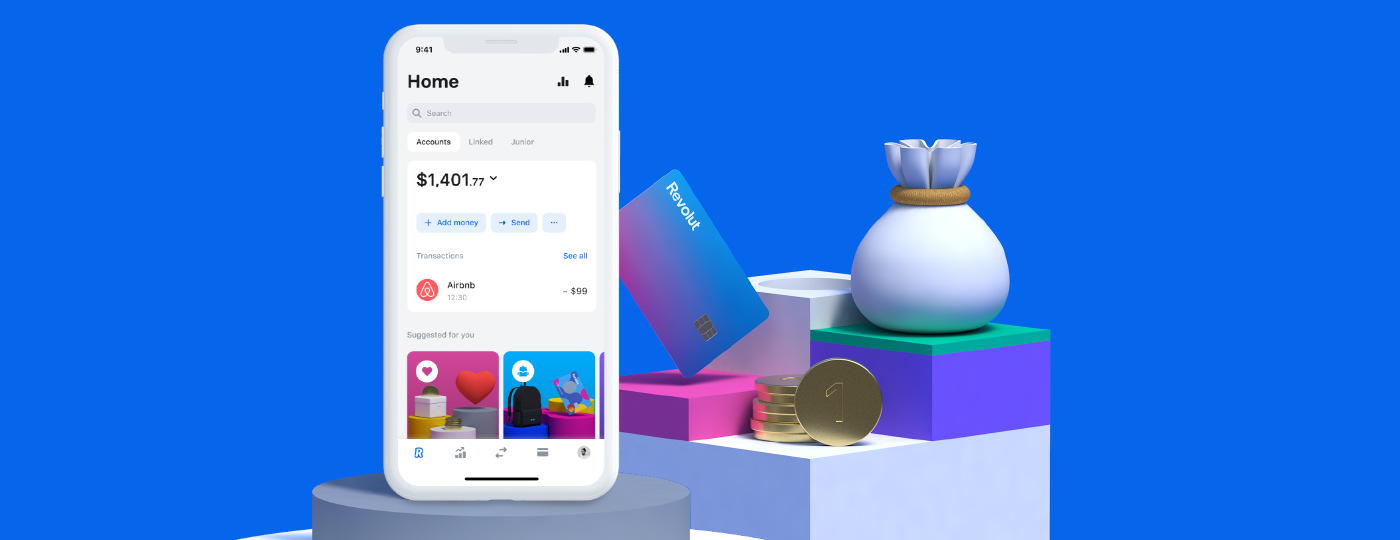

Fintech startup Revolut has expanded its open banking feature to Ireland. The feature first launched in the U.K. back in February. Once again, the startup is partnering with TrueLayer to let you add third-party bank accounts to your Revolut account.

The feature launch also marks the launch of TrueLayer in Ireland. For now, Revolut users can only link their Revolut account with AIB, Permanent TSB, Ulster Bank and Bank of Ireland. Revolut and TrueLayer will add support to other banks in the future. Revolut currently has 1 million customers in the Republic of Ireland.

The idea behind open banking is quite simple. Many online services rely on application programming interfaces (APIs) to talk to each other. You can connect with your Facebook account on many online services, you can interact with other services from Slack, etc.

Financial institutions have been lagging behind on this front, but it is changing thanks to new regulation and technical updates. With open banking, your bank account should work more like a traditional internet service.

When you connect your bank account with Revolut, you can view your balance and past transactions from a separate tab that lists all your linked accounts. Users can also take advantage of Revolut’s budgeting features with their bank accounts.

As TechCrunch’s Steve O’Hear noted when he first covered Revolut’s open banking feature, Revolut was originally authorized for Account Information Services (AIS) by the U.K. regulator, the Financial Conduct Authority. It lets you access and display information from other financial institutions.

But the startup now has permission to carry out Payment Initiation Services (PIS). It means that you’ll soon be able to initiate transfers from your bank account directly from Revolut. It should make it much easier to top up your Revolut balance, for instance.

While this feature might seem anecdotal, Revolut wants to build a comprehensive financial hub for all your financial needs — a sort of super app for everything related to money. With open banking, you theoretically no longer have to open your traditional banking app.

Image Credits: Revolut

Powered by WPeMatico

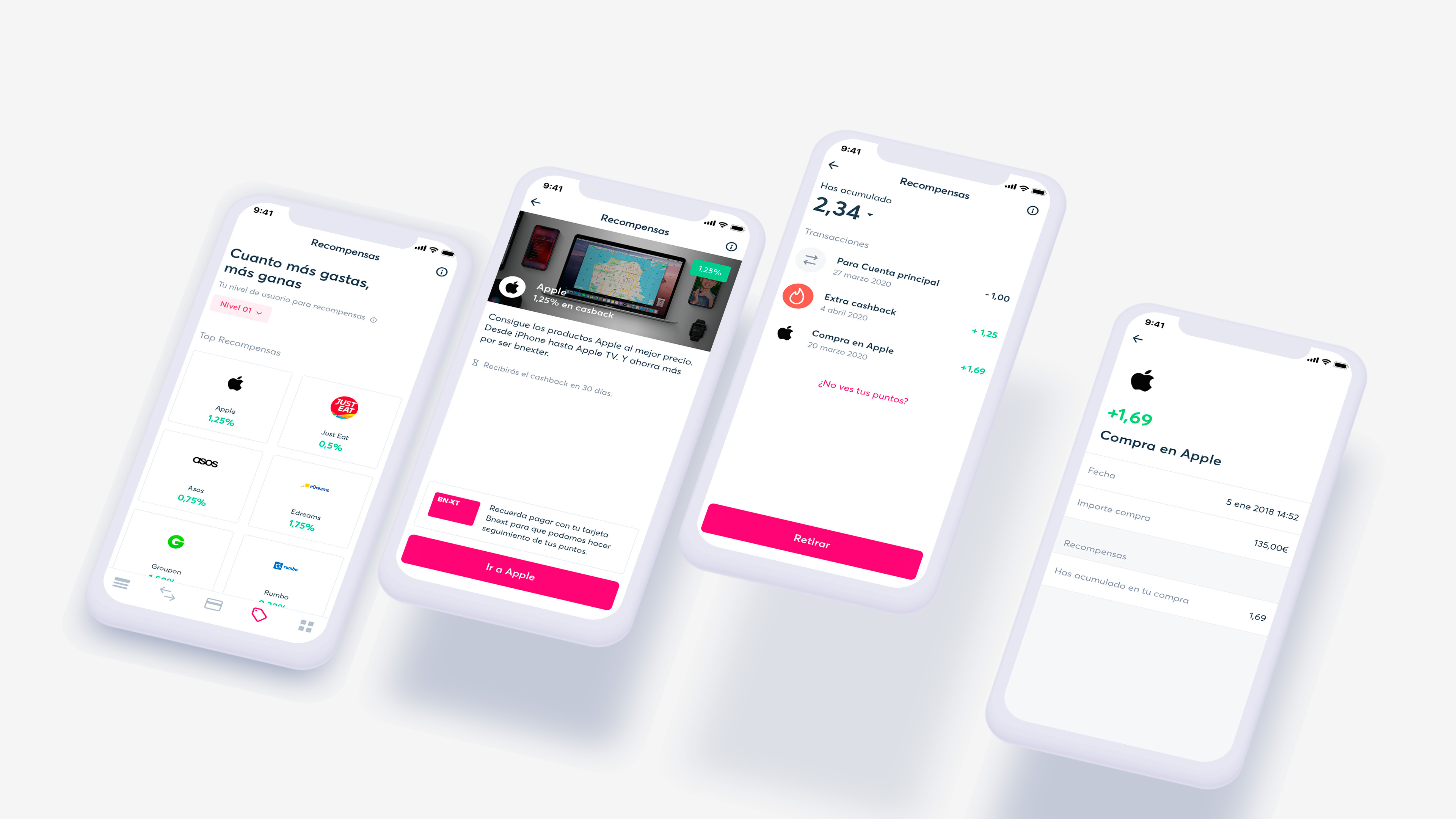

Spanish startup Bnext is revamping its cashback program so that you can buy from partner stores directly from the Bnext app and get some money back. The company has partnered with Button and the feature is available as an open beta.

Traditional cashback portals are a bit clunky. When you find an offer that gives you 2% of your money back, you click on the offer, get redirected to the partner site and hope that your purchase will be registered. A bit later, you get some money back on the cashback website, which you need to cash out to your bank account.

If you’re using Bnext as your bank account, you’ll be able to access rewards directly from your banking app. In addition to that, you don’t get redirected to another site as you purchase goods directly from the Bnext app.

There are multiple levels. If you’re making your first purchase through the feature, you get 1% in savings on average. If you’ve made more than three purchases over the past 30 days, you get 3% in savings on average. In order to reach level 3, you need a premium Bnext subscription. With that level, you get 5% in savings on average.

Partners include AliExpress, Booking.com, eDreams, Europcar, Nike, Just Eat and more. Eventually, the startup wants to let you earn rewards from in-store purchases as well. Bnext is creating a new revenue stream with this feature as the startup will keep a share of the revenue from each transaction.

Bnext provides current accounts and payment cards. You can receive notifications for each transaction with your card, and temporarily lock and unlock your card. You don’t pay any foreign transaction fee as long as you spend less than €2,000 per month with a standard account.

The company has also put together a marketplace of fintech products. You can earn interest by lending money to small companies on October, get a loan, an insurance product and more.

Earlier this year, the startup expanded to Mexico. The company plans to roll out rewards in Mexico soon. Bnext has managed to attract a bit less than 400,000 users.

Powered by WPeMatico

Challenger bank Bunq is adding a new feature that lets you donate to charities directly from the app. In addition to that, Bunq is also in the process of redesigning its app. The company is launching a public beta test to get feedback from its users.

Other fintech startups, such as Revolut and Lydia, have launched donation features in the past. But in those cases, startups have selected a handful of charities.

Bunq has chosen a different approach, as you can create your own donation campaigns in the app. As long your local charity has an IBAN number, you can add it to Bunq’s donation feature. You can even add a local business in case you want to help them stay in business.

You can then invite other people to donate to your charities. You can also track the total amount of your donations, as well as the total donations from the entire Bunq user base.

The company has also been working on the third major version of the app. In order to test it before the public release, Bunq is launching a public beta program. The first build will roll out in the coming weeks.

In order to simplify navigation, Bunq has tried to remove clutter by focusing on one main button on each page. The app will be divided in four main tabs.

The first tab, called “Me,” will feature all your personal information — personal bank accounts, savings goals, etc. On the second tab, called “Us,” you can see information about Bunq, such as total investments and total donations. The third tab features your profile information.

Finally, the fourth tab is a dedicated camera button. It lets you scan invoices and receipts, which could be particularly useful for business customers. I’m not sure a lot of people use that feature, but things could still change before the final release.

Powered by WPeMatico

Consumer fintech startups were massively successful in 2019, attracting millions of new users and disrupting traditional retail banks and financial services with mobile-first, consumer-oriented products. Despite the economic downturn in public markets and the massive wave of cuts at public and private companies in recent weeks, fintech startups have been raising a ton of money.

It feels like they’re all building a war chest to survive the economic winter as traditional banks continue to iterate so they can catch up and offer more user-friendly services. This is not the time to raise fees, slow down on product development or plans to acquire new users.

Back in January, I looked at challenger banks and their growth trajectories, but since then, they have managed to attract even more customers. According to the most recent figures:

And that’s without mentioning Starling Bank, Atom Bank, Bunq, Bnext, Paysend, etc. At some point, there will be as many challenger banks as non-challenger banks — perhaps we shouldn’t call them challenger banks anymore.

Beyond these startups, trading app Robinhood recently reached 13 million users, international payments startup TransferWise has 7 million customers and cryptocurrency exchange Coinbase has 30 million users.

Powered by WPeMatico

European fintech startup Revolut is launching its app and service in the U.S. Starting today, anybody can sign up and get a Revolut debit card. In the U.S., Revolut has partnered with Metropolitan Commercial Bank for the banking infrastructure — deposits are FDIC insured up to $250,000.

In just a few years, Revolut has managed to attract over 10 million customers by building a financial hub that lets you spend, send, receive and manage money from a single app. The company recently raised a $500 million funding round, valuing the company at $5.5 billion.

But the U.S. has been watching from the sidelines. Tens of thousands of customers have signed up to the waiting list and they’ll now be able to access all of Revolut’s core features.

Like competing challenger banks, such as Chime and N26, Revolut lets you open an account from your phone. After downloading the app, you enter personal details and send a few official documents to comply with know-your-customer regulation.

After that, you get U.S. account details and you can instantly top up your account with a bank transfer or a card transfer. A few days later, you also receive a physical debit card. You can also generate a virtual debit card from the app.

Revolut lets you control your debit card from the app directly. You can receive notifications every time you make a transaction. You can freeze and unfreeze your card, set some limits and restrict some feature, such as online payments or ATM withdrawals.

One of Revolut’s key features is that you can convert from one currency to another based on interbank rate with a low fee — sometimes without any markup for popular currencies and small transactions (more details on foreign exchange fees here). You can hold foreign currencies in your Revolut account or send money to another Revolut user or a bank account in another country.

In the U.S., Revolut offers the ability to receive your salary two days in advance if you share your Revolut banking details with your employer.

Revolut offers a ton of additional features in Europe, but the company is starting with this basic feature set in the U.S. You can expect more features in the future, such as the ability to purchase cryptocurrencies and invest on the stock market.

In Europe, Revolut also offers insurance products through premium monthly subscriptions, mobile phone insurance, savings accounts, credit, rewards and more. Many of those features require partnerships with third-party companies. But it gives you an idea of Revolut’s roadmap in the U.S.

Powered by WPeMatico

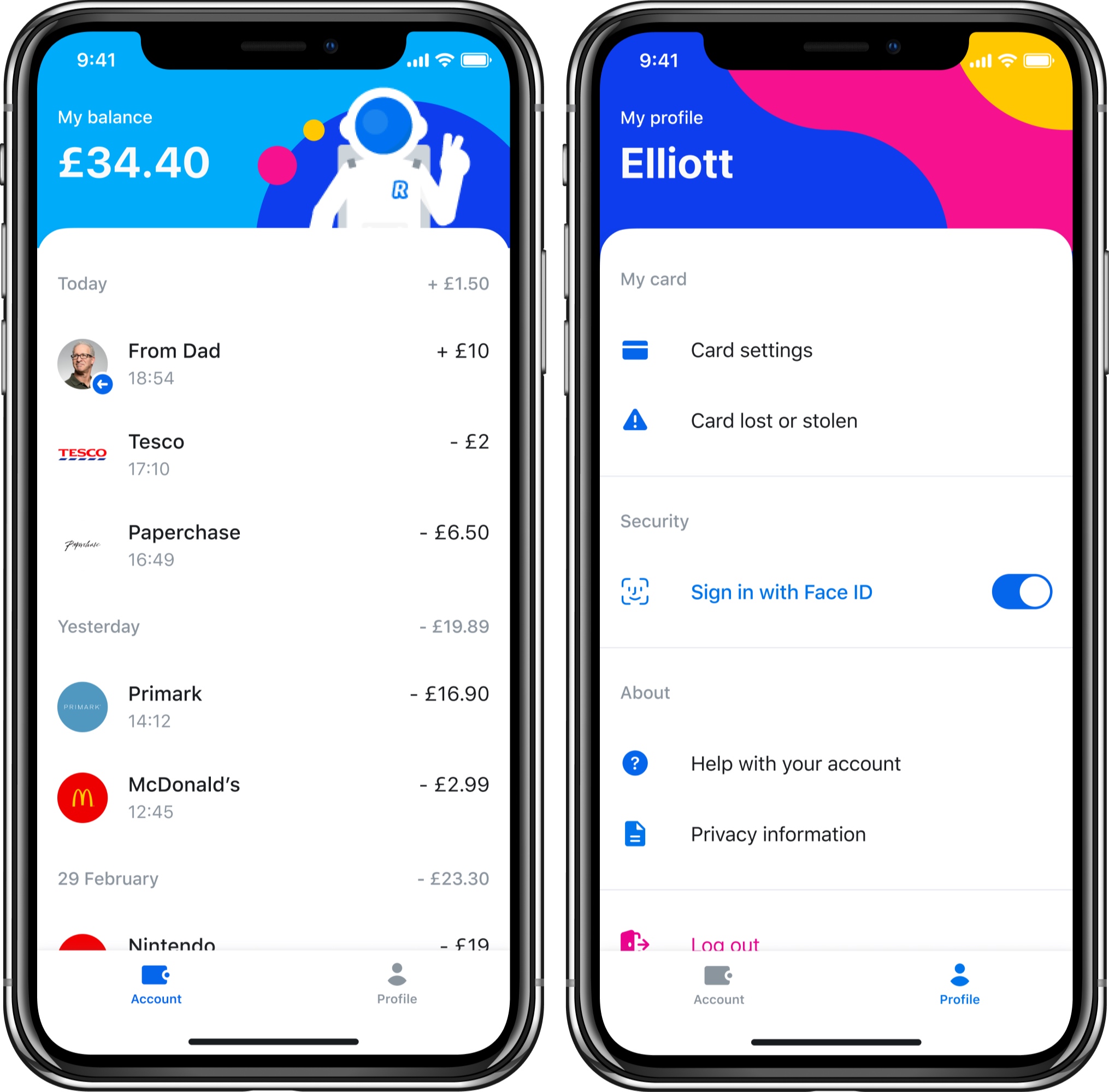

Revolut is introducing a new product specifically targeted toward kids aged 7-17 years old — Revolut Junior. Revolut Junior is a new app and service that integrates directly with the main Revolut app on the parent’s side.

Parents or legal gardians who are also Revolut users can create a Revolut Junior account for their kid. After that, your kid can download the Revolut Junior app and get a Revolut Junior card.

The new app offers a limited set of features with an interface divided in two tabs — Account and Profile. Kids can see a list of transactions in real time in the Account tab. They can configure card settings in the Profile tab. And that’s about it.

On the other end, parents can control their kids’ spending from Revolut. They can transfer money to a Revolut Junior account instantly. Parents can also access balances and transactions as well as disable some card features, such as online payments. They can also choose to receive notifications when a child is using their card.

The reason why Revolut Junior can attract a ton of users is that Revolut itself already has over 10 million users. It’s going to be easier to convince existing Revolut customers to use Revolut Junior over a custom-made challenger bank for teens, such as Kard or Step. Arguably, the biggest competitor of challenger banks for teens is still cash.

As kids grow up, chances are they’ll switch to a full-fledged Revolut account if they’ve been using Revolut Junior for years. Revolut Junior represents a great acquisition funnel as well.

Revolut Junior is only available to Premium and Metal customers in the U.K. for now. The company will eventually roll it out to more users and more countries.

Revolut plans to add more features to Revolut Junior in the future. For instance, parents will be able to set a regular allowance and financial goals. Kids will get savings options, spending reports, spending limits and more.

Powered by WPeMatico

Fintech startup Revolut has introduced a new trading feature for premium users. Starting today, Premium and Metal users can access gold exposure from the app.

Revolut works with a gold services partner (London Bullion Market Association) so that money you spend on gold exposure is backed by real gold held by this partner. In other words, you’re not going to receive gold coins in the mail. You can just invest money based on the price of gold.

The startup has been building a financial hub and already lets you purchase cryptocurrencies and buy public shares. Gold is part of a new feature called Commodities.

There are multiple ways to invest in gold. You can purchase gold exposure directly at market price, set a limit price to auto-exchange gold when it reaches a certain price or get cashback in gold for Metal customers.

At any time, you can convert your gold investment back into fiat currencies or cryptocurrencies. If you spend money with your Revolut card and you only have gold, Revolut will use your gold exposure automatically. You can also transfer gold exposure to another Revolut user.

According to the company’s website, Revolut charges a 0.25% markup when you trade gold during the week and a 1% markup from Saturday at midnight to Monday at midnight U.K. time.

It’s worth noting that gold isn’t protected through the Financial Services Compensation Scheme in the U.K. “However, in the unlikely event of Revolut’s insolvency, all Precious Metals holdings will be sold and proceeds will be credited to your e-money account,” Revolut says. You’ll have to trust their word.

Powered by WPeMatico

Fintech startup Revolut is raising a large Series D round of funding. TCV is leading the $500 million round, valuing the company at $5.5 billion. Over the past few years, Revolut has raised $836 million in total.

Some existing investors are also participating in today’s funding round, but Revolut isn’t sharing names. Previous investors include DST Global, Index Ventures, Balderton Capital and many others.

If you’re not familiar with Revolut, the company is building a financial service to replace traditional bank accounts. You can open an account from an app in just a few minutes. You can then receive, send and spend money from the app or using a debit card.

On top of that, Revolut has added a ton of features that it has built in-house or through partnerships. You can insure your phone, get a travel medical insurance package, buy cryptocurrencies, buy shares, donate to charities, save money and more.

Revolut currently has more than 10 million customers, mostly in Europe and the U.K. The company doesn’t share specific numbers when it comes to transaction volume and monthly active customers, but here are some percentage-based metrics:

With the new influx of cash, the company says that it’ll focus on improving its product for existing users as well as revenue. It’s all about making Revolut more useful and stickier going forward.

In particular, you can expect new lending services for both retail customers as well as companies using Revolut for Business. While Revolut provides a ton of services in the U.K., customers in other markets don’t have the same feature set. For instance, Revolut recently launched savings vaults in the U.K. — customers in other markets will be able to open savings sub-accounts in the future, as well.

Other than that, Revolut wants to double down on the core features. The company will improve its two subscription tiers (Premium and Metal) and improve banking operations across Europe — you can expect full bank accounts in Europe in the future.

There are currently 2,000 people working for Revolut. “We’re on a mission to build a global financial platform — a single app where our customers can manage all of their daily finances, and this investment demonstrates investor confidence in our business model. Going forward, our focus is on rolling-out banking operations in Europe, increasing the number of people who use Revolut as their daily account, and striving towards profitability,” Revolut co-founder and CEO Nik Storonsky said in the release.

Revolut is currently live in the U.K., Europe, Singapore and Australia (in beta). While the company has announced plans to expand to a handful of countries, the main focus is on launching in the U.S. and Japan in the coming months.

Powered by WPeMatico

German fintech startup N26 is shutting down its operations in the U.K. Customers who opened a bank account in the U.K. will have to transfer their deposits, spend everything with their card or withdraw money at an ATM, as all accounts will be automatically closed on April 15, 2020.

Many European fintech companies take advantage of a European process called passporting. It lets you apply for a license to operate as a bank or a financial service in an EU member state and then expand to all EU member states.

As you may have guessed, N26 has to exit from the U.K. banking market because it currently has a European banking license through the central bank of Germany. Passporting is going to change following Brexit.

In particular, European companies that operate in the U.K. using inward passporting have to follow a new application process in order to continue operating in the U.K.

“The timings and framework outlined in the EU Withdrawal Agreement mean that the company will in due course be unable to operate in the UK with its European banking licence,” N26 writes in a statement. N26 users in other markets won’t be affected by this change.

N26 also faces a ton of competition in the U.K. from Monzo, Starling and in some ways Revolut. It’s also possible that N26 didn’t want to invest a lot of time and money in order to set up a proper subsidiary company in the U.K. with its own banking license.

You can no longer sign up in the U.K. If you’re an existing customer, everything will work normally until April 15. You should empty your bank account, move your recurring payments to another bank, identify all your subscriptions, direct debits and deposits and move them to another bank.

On April 15, you won’t be able to access your account. Your card will be deactivated. Direct debits and deposits will bounce as well. If you have a premium subscription, N26 is going to stop charging you for your N26 You or N26 Metal subscription from March 14.

Powered by WPeMatico