N26

Auto Added by WPeMatico

Auto Added by WPeMatico

JoomPay, a startup with a similar product to PayPal-owned Venmo in the U.S., is set to launch in Europe shortly after being granted a Luxembourg Electronic Money Institution (EMI) license. The app allows people to send and receive money with anyone, instantly and for free. “Venmo me” has become a common phrase in the U.S., where people use it to split bills in restaurants or similar instances. Venmo is in common use in the U.S., but it’s not available in Europe, although dozens of other innovative mobile peer to peer transfer options exist, such as Revolut, N26, Monese and Monzo. The waitlist for the app’s beta is open now (iOS, Android).

Europe leads the world’s instant payments industry, with $18 trillion in worldwide volume predicted by 2025, up from $3 trillion in 2020 — a growth of more than 500%. Western Europe — and COVID-19 — is now driving that innovation and will account for 38% of instant payment transaction value by 2025. While Europe lacks simple peer-to-peer payments solutions such as Venmo or Square Cash App in the U.S., challenger banks have stepped up to provide similar kinds of services. JoomPay’s opportunity lies in being able to be a middle-man between these various banking systems.

Shopping app Joom, which has been downloaded 150 million times in Europe, has spun-off JoomPay to solve this problem. The app allows users to send and receive money from any person, regardless of whether they use JoomPay or not — and you only need to know their email or the phone number. JoomPay connects to any existing debit/credit card or a bank account. It also provides its users with a European IBAN and an optional free JoomPay card with cashback and bonuses.

Yuri Alekseev, CEO and co-founder of JoomPay, said: “Since COVID-19 started, we’ve seen a significant decline in cash usage. People can’t meet as easily as before but still need to send money, and we offer a viable alternative.”

JoomPay may have an uphill struggle. Its main competitors in Europe are the huge TransferWise, Paysend and, of course, PayPal itself.

Powered by WPeMatico

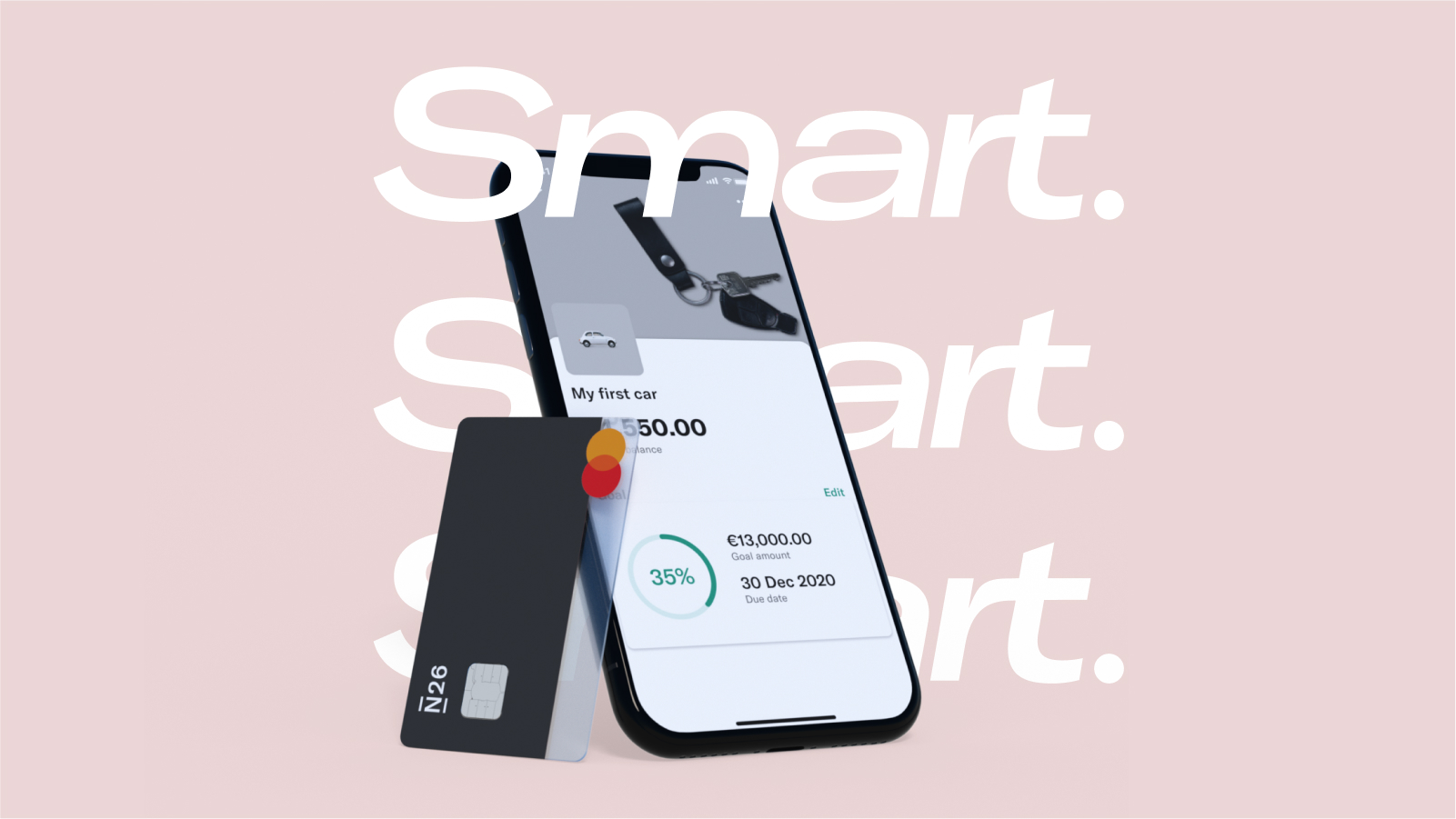

Challenger bank N26 is adding a third subscription product called N26 Smart. N26 Smart is designed to be a mid-tier subscription plan with advanced banking features but without a travel insurance package.

In Europe, in addition to the free plan, N26 already provides two subscription tiers, called N26 You and N26 Metal. N26 You costs €9.90 per month and comes with higher limits, such as five free ATM withdrawals instead of three and free withdrawals in foreign currencies.

With an N26 You account you can create sub-accounts (N26 Spaces), share them with other N26 users or use them to save money. As an N26 You subscriber, you also get a travel insurance package with medical travel insurance, trip and flight insurance and more. You can also access some partner offers.

N26 Metal is the most expensive plan and costs €16.90 per month. In addition to everything in N26 You, you get car rental insurance when you’re abroad and phone insurance. As the name suggests, you also get a metal card.

The new N26 Smart subscription costs €4.90 and works well for people who don’t need travel insurance. With an N26 Smart subscription, you can create up to 10 sub-accounts. You get five free ATM withdrawals per month. You can also call N26 support directly in addition to in-app support chat.

N26 is launching a new round-up feature for N26 Smart users. It lets you round each purchase up to the nearest Euro and save it in a separate sub-account. N26 Smart accounts also have access to colorful debit cards — the same colors as N26 You.

This is just a first step, as N26 plans to revamp its subscription products altogether. In the near future, N26 You will become N26 International. There will be more features focused on borderless banking. N26 Metal will become N26 Unlimited.

As for the free N26 Standard account, the company wants to focus on digital cards. Some users are going to switch to the N26 Smart plan to keep some of the features that they’ve been using with a free account. That move should help the company’s bottom line.

Image Credits: N26

Powered by WPeMatico

The neobank, or digital bank, phenomenon continues to take the world by storm, with global winners, from Brazil’s Nubank valued at $10 billion and Berlin’s N26 valued at $3.5 billion, to Chime, now valued at $14.5 billion as the most valuable consumer fintech in the United States.

Neobanks have led the charge of the $3.6 billion in venture capital funding for consumer fintech startups this year. And as the coronavirus-fueled acceleration of digital transformation continues, it seems the digital bank is here to stay, with some estimates pointing to neobanks reaching 60 million customers in North America and Europe by the end of 2020, and surpassing 145 million by 2024.

The space is also becoming more crowded, a trend which will only accelerate with fintech eating the world and creating greater infrastructure that enables any company to include a bank account as a product extension.

FT Partners Fintech Industry Research, January 2020

As a result, neobanks are not a monolithic model and not all are created equal. Looking underneath the hood of business models across the globe reveals remarkable operational differences and highlights specific features that are more likely to succeed in the long-term.

Today there are five distinct models that are leading globally:

Interchange-led: Relies on payments revenue, sourced through interchange as the revenue driver. Every time a customer uses the neobank’s card as a payment method they get paid [e.g. Chime / US; Neon (hybrid of 1 & 2) / Brazil].

Credit-led: Leverages a credit-first model, starting off with a credit card or similar offering, and later providing a bank account [e.g. Nubank, Neon (hybrid of 1 & 2) / Brazil].

Powered by WPeMatico

Fintech startup N26 is announcing some changes in the leadership team with two new C-Level hires. First, Adrienne Gormley, pictured above, is joining the company as chief operating officer, replacing Martin Schilling who left the company in March 2020. Second, Diana Styles, pictured below, will become N26’s chief people officer.

Gormley has spent the last six years working for Dropbox in Dublin. She was the VP of Global Customer Experience as well as the head of EMEA for Dropbox. Previously, she’s worked at Google and Transware.

At N26, she will be in charge of a large chunk of the company, from customer service, to business operations, service experience and workplace division.

Styles has many years of human resources experience. She was the senior vice president of Human Resources, Global Sales and Brands at Adidas. Similarly, as chief people officer, she will oversee important aspects of the company, such as employee retention, leadership development, talent acquisition and more.

Both will be based in Berlin and report to the company’s co-founder and chief financial officer Maximilian Tayenthal. N26 has grown quite a lot over the past few years as there are now 1,500 employees working for the company.

Image Credits: N26

Powered by WPeMatico

Venture capitalists and other investors have poured capital into fintech startups around the world in recent years, including a record number of rounds worth $100 million or more in the second quarter of 2020. In Q2 2020 venture-backed fintech startups raised 28 nine-figure rounds, underscoring the scale of the bet investors are making on fintech’s long-term success.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Inside that fintech wave are various hubs of activity, including payments tech, investing and banking. That last category has helped give rise to so-called neobanks, startup banking entities that offer mobile-first, consumer-friendly banking tools and services. Given the old-fashioned nature of banking in many countries (and how far out of reach banking remains for many) neobanks have seen strong uptake by users in recent years.

And the startup cohort has raised oceans of capital to help fuel its growth. In America, Chime was most recently valued at $5.8 billion after raising hundreds of millions in late 2019. More recently, neobank Revolut added $80 million to its Q1 2020 round worth $500 million. Revolut is also worth north of $5 billion. Monzo is well-funded (albeit at a recent valuation reduction), Latin America-focused NuBank is worth $10 billion, according to Crunchbase, Starling recently raised another £40 million, while Germany’s N26 is worth over $3 billion after its most recent nine-figure round.

From the fundraising perspective, then, neobanks are killing the game. And thanks to recent tailwinds from the COVID-19 pandemic that have bolstered interest in savings-related products, many of the same entities could be enjoying a strong year thus far. But recent self-reporting of some neobank’s 2019-era results details ample red ink — perhaps more than we might have anticipated.

From the fundraising perspective, then, neobanks are killing the game. And thanks to recent tailwinds from the COVID-19 pandemic that have bolstered interest in savings-related products, many of the same entities could be enjoying a strong year thus far. But recent self-reporting of some neobank’s 2019-era results details ample red ink — perhaps more than we might have anticipated.

Of course, startups don’t raise money for fun; they raise it to invest it in their operations and drive scale. So, we knew that these megafundraisers were losing money on purpose. All the same, let’s peek at the economics of several neobanks, as their now dated and thus not at all current results can provide useful context on two points: Why investors are excited to put their capital to work in neobanks, and why neobanks always seem to have another check to announce.

To prevent my receiving unhappy emails from irked fans of these companies, please bear in mind that we’re looking several quarters back when observing the following results.

It would be lovely to have more recent data, but with European neobanks reporting their — roughly — 2019 results in recent weeks, this is what we have. We are going to parse the numbers, but we will not conflate past performance with current results. We do not know much about 2020 neobank financial performance.

Anyhoo, to the numbers. You can read the full documents from Monzo here, Starling here (or here, if that link is struggling) and Revolut here.

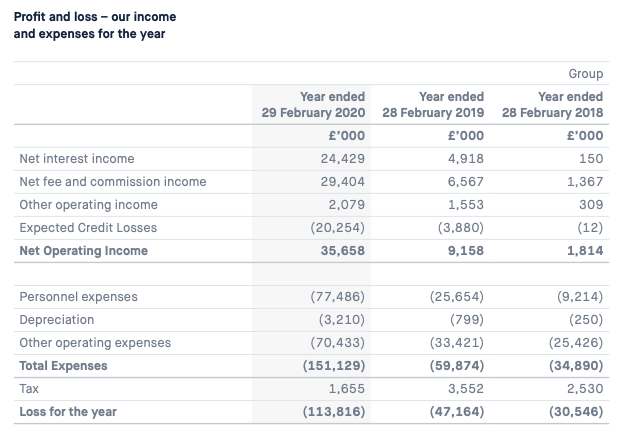

Let’s start with Monzo, which has a clear set of figures for us to peek at:

Image Credits: Monzo

Powered by WPeMatico

Consumer fintech startups were massively successful in 2019, attracting millions of new users and disrupting traditional retail banks and financial services with mobile-first, consumer-oriented products. Despite the economic downturn in public markets and the massive wave of cuts at public and private companies in recent weeks, fintech startups have been raising a ton of money.

It feels like they’re all building a war chest to survive the economic winter as traditional banks continue to iterate so they can catch up and offer more user-friendly services. This is not the time to raise fees, slow down on product development or plans to acquire new users.

Back in January, I looked at challenger banks and their growth trajectories, but since then, they have managed to attract even more customers. According to the most recent figures:

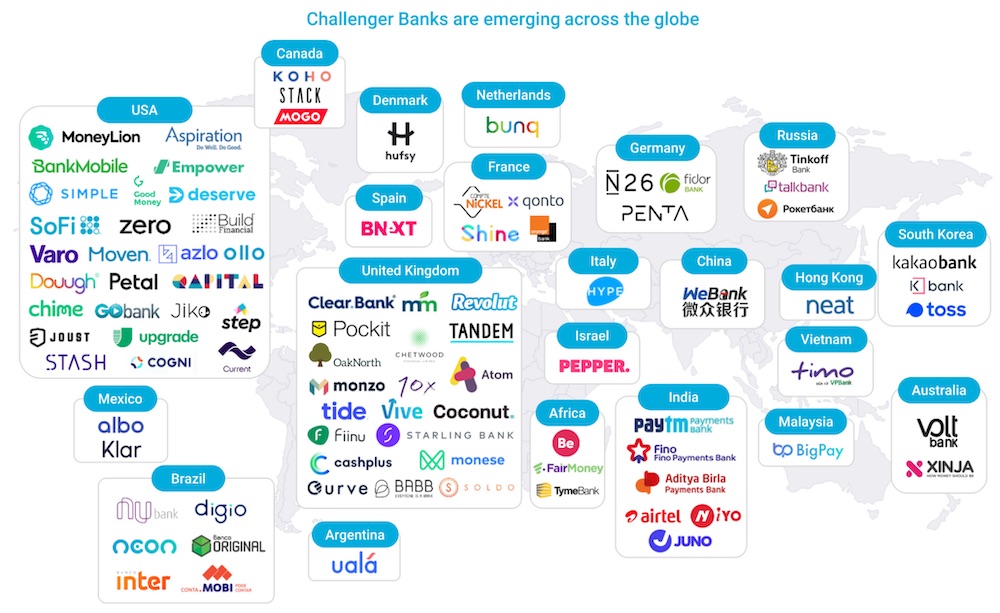

And that’s without mentioning Starling Bank, Atom Bank, Bunq, Bnext, Paysend, etc. At some point, there will be as many challenger banks as non-challenger banks — perhaps we shouldn’t call them challenger banks anymore.

Beyond these startups, trading app Robinhood recently reached 13 million users, international payments startup TransferWise has 7 million customers and cryptocurrency exchange Coinbase has 30 million users.

Powered by WPeMatico

German fintech startup N26 is shutting down its operations in the U.K. Customers who opened a bank account in the U.K. will have to transfer their deposits, spend everything with their card or withdraw money at an ATM, as all accounts will be automatically closed on April 15, 2020.

Many European fintech companies take advantage of a European process called passporting. It lets you apply for a license to operate as a bank or a financial service in an EU member state and then expand to all EU member states.

As you may have guessed, N26 has to exit from the U.K. banking market because it currently has a European banking license through the central bank of Germany. Passporting is going to change following Brexit.

In particular, European companies that operate in the U.K. using inward passporting have to follow a new application process in order to continue operating in the U.K.

“The timings and framework outlined in the EU Withdrawal Agreement mean that the company will in due course be unable to operate in the UK with its European banking licence,” N26 writes in a statement. N26 users in other markets won’t be affected by this change.

N26 also faces a ton of competition in the U.K. from Monzo, Starling and in some ways Revolut. It’s also possible that N26 didn’t want to invest a lot of time and money in order to set up a proper subsidiary company in the U.K. with its own banking license.

You can no longer sign up in the U.K. If you’re an existing customer, everything will work normally until April 15. You should empty your bank account, move your recurring payments to another bank, identify all your subscriptions, direct debits and deposits and move them to another bank.

On April 15, you won’t be able to access your account. Your card will be deactivated. Direct debits and deposits will bounce as well. If you have a premium subscription, N26 is going to stop charging you for your N26 You or N26 Metal subscription from March 14.

Powered by WPeMatico

Over the past year, startup banks have proven that they have a shot at disrupting retail banking. These challengers have amassed a war chest of funding, announced some ambitious international expansion plans and attracted millions of customers.

And yet, building a bank has proven to be even harder than building a startup in general. Retail banks aren’t willing to sit back and watch startups eat their lunch. Here’s a look back at the biggest moves of the year from challenger banks, some trends you should keep an eye on and the upcoming challenges for those startups.

Due to the regulatory framework and the size of the market, it is much easier to launch a challenger bank in Europe compared to anywhere else in the world. That’s why challenger banks have been thriving in Europe.

When a company gets a full banking license from the central bank of a EU country, the startup can passport its license across all EU countries and operate across the continent.

N26 raised a ton of money in 2019: last January, the Berlin-based startup announced a $300 million funding round, raising another $170 million in July. The company is now valued at $3.5 billion.

With more than 3.5 million customers in Europe, N26 announced some ambitious expansion plans. N26 is now live in the U.S. and is already planning a launch in Brazil.

Revolut has also been aggressively expanding in order to beat its competitors to new markets. In addition to its home market in the U.K., Revolut is available across Europe. In 2019, the company expanded to Singapore and Australia and currently has at least 8 million users.

While Revolut announced that it should launch in the U.S. and Canada by the end of last year, the clock ran out on that prediction. The startup has been very transparent about its expansion plans, even though it sometimes means that you have to wait months or even years before a full rollout.

For instance, Revolut announced in September 2018 that it would launch in New Zealand, Hong Kong and Japan “in the coming months.” It later became “early 2019,” then “2019.” India, Brazil, South Africa, Mexico and the UAE have also all been mentioned at some point. In other words: launching a banking product in a new country is hard.

The U.S. is a tedious market as you have to get a license in all 50 states to operate across the country

Monzo has been doing well at home in the U.K. It has attracted 3 million customers and raised £113 million (~$144m) in funding last year from Y Combinator’s Continuity fund. It is expanding to the U.S., but the rollout has been slow.

Nubank is another well-funded challenger bank. Backed by Tencent, the startup has raised a $400 million Series F round from TCV. According to the WSJ, the startup has a valuation above $10 billion.

Originally from Brazil, Nubank expanded to Mexico and has plans to expand to Argentina.

Chime is increasingly looking like the bigger player in the U.S., recently raising a $500 million funding round and reached a valuation of $5.8 billion. It only operates in the U.S.

Starling Bank and Atom Bank only operate in the U.K. Bunq is based in Amsterdam with a product tailor-made for the Netherlands, but it accepts customers across Europe.

This isn’t meant to be an exhaustive list as it’s becoming increasingly hard to cover all challenger banks.

There are a few basic features that separate challenger banks from legacy retail banks. Signing up is extremely simple and only requires a mobile app. The mobile app itself is usually much more polished than traditional banking apps.

Users receive a Mastercard or Visa debit card that communicates with the company’s server for each transaction. This way, users can receive instant notifications, block and unblock their cards and turn off some features, such as foreign payments, ATM withdrawals and online transactions.

Challenger banks usually customers promise no markup fees on transactions in foreign currencies, but there are sometimes some limits on this feature.

So how do these companies make money? When you pay with your card, banks generate a tiny, tiny interchange fee of money on each transaction. It’s really small, but it could become serious revenue at scale with tens of millions or hundreds of millions of users.

Challenger banks also offer other financial services like insurance products, foreign exchange or consumer credit. Some challenger banks develop those features in house, but many of those features are actually managed by external fintech partners. Challenger banks generate a commission on those products.

But the most promising product is premium subscriptions. While challenger banks started with free accounts and low, transparent fees, they have been selling premium subscriptions for a fixed monthly fee.

Challenger banks have become a software-as-a-service industry with a freemium component

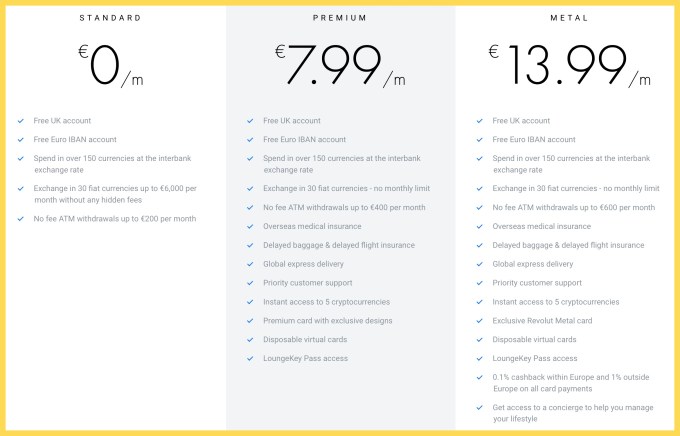

For example, Revolut offers premium accounts for €7.99 per month with higher limits, some insurance benefits that you’d expect from a premium card and access to advanced features, such as cryptocurrencies and disposable virtual cards. There’s a super premium product for €13.99 called Metal with a metal card design, cashback on card payments and access to a concierge feature.

This seems a bit counterintuitive, but premium subscriptions have been performing well, according to discussions with people working in the industry. You pay a lot in subscription fees in order to avoid small transactional fees. (And you also get a cool card.)

Challenger banks have become a software-as-a-service industry with a freemium component. It leads to a premium positioning and high expectations from customers.

Revolut’s fees top out at €13.99/month.

Powered by WPeMatico

Challenger bank N26 has unveiled a new premium plan called N26 You. This plan replaces N26 Black with the same benefits and a few tweaks.

N26 is keeping its three-tier system with a free basic bank account, a premium account (N26 You) and a super premium account (N26 Metal). With N26’s free plan, you can pay anywhere in the world without any foreign transaction fee, but there’s a 1.7% markup on ATM withdrawals in a foreign currency.

N26 You costs the same price as the previous premium plan N26 Black, €9.90 in the Eurozone and £4.90 in the U.K. In addition to a travel and purchase insurance package, you can withdraw money without any foreign transaction fee (€9.90 is roughly what you’d pay in fees if you withdraw the equivalent of €580 with a free N26 account).

You also can create up to 10 Spaces to organize your money with savings goals, separate sub-accounts and more — free accounts can only create two Spaces.

And, of course, you get a better-looking card. N26 is reusing its pastel color palette to give you more options. You can now choose between five colors — Aqua, Rhubarb, Sand, Slate and Ocean. The card has a minimal design with a tiny N26 logo in the top-left corner, a transparent line at the bottom of the card and a solid color background.

N26 also plans to add perks to the N26 You plan, such as discounts on Hotels.com, WeWork, GetYourGuide, Babbel, Blinkist and Bloom & Wild. Those perks were limited to N26 Metal customers in the past, so it’s going to be interesting to see how the lineup will work once those perks are added to N26 You. If you’re an existing N26 Black customer, you automatically become an N26 You customer.

Changing N26 Black to a premium plan with multiple card designs might seem like a small detail, but it potentially opens up a lot of possibilities. You’ll soon be able to order an additional card.

Eventually, you could imagine having a blue card associated with your main account and a yellow card associated with a shared Space sub-account, for instance. At least, that’s what I hope the company will do.

Powered by WPeMatico

European fintech startup N26 is now accepting customers in the U.S. The company is launching a bank account with a debit card that should provide a better experience compared to traditional retail banks.

If you’re familiar with N26, the product that is going live today won’t surprise you much. Customers in the U.S. can download a mobile app and create a bank account from their phone in just a few minutes. It’s a true bank account with ACH payments, routing and account numbers.

A few days later, you receive a debit card that you can control from the mobile app. Every time you make a transaction, you instantly receive a push notification telling you how much money you just paid. You can set up your PIN code, customize limits, turn on and off online payments, and make ATM withdrawals or payments abroad.

And that’s about all there is to know. But what about fees? Basic N26 accounts are free. There’s no monthly fee and no minimum balance. There’s no fee on transactions in a foreign currency and you get two free ATM withdrawals per month.

N26 is going to progressively roll out signups over the summer as a sort of beta program. If you’ve signed up to the waitlist, you’ll get an invitation over the coming hours, days and weeks. There are currently 100,000 people on the waitlist. N26 will then open signups to everyone later this summer.

When N26 rolls out its final product in a couple of months, the company says that it plans to automatically find and reimburse fees the ATM operators are charging. N26 cards in the U.S. work on the Visa network instead of Mastercard.

Just like Chime, N26 will also try to let you get paid up to two days early if you get paid via direct deposit. Instead of waiting a couple of days to clear those transactions, N26 will go ahead and top up your account.

Behind the scenes, there are a few differences between N26 in Europe and N26 in the U.S. While N26 has a full-fledged banking license in Europe, the company has partnered with Axos Bank, which is acting as a white-label partner in the U.S.

Axos Bank essentially manages your money for you, and N26 acts as the interface between customers and their bank accounts. As a result, you get an FDIC-insured account.

N26 first partnered with a third-party company in Europe, as well. But it was a costly deal that wasn’t meant to stick around. The startup got a banking license in Germany that was good for Europe at large. In the U.S., it’s a different story, as the market is not as unified as in Europe — it’s complicated to get a license to operate in all 50 states.

“We looked at 30 players, we did some due diligence and we’re happy to partner with Axos Bank. The deals that you get in the U.S. for white-label banks are much more favorable than in Europe,” N26 co-founder and CEO Valentin Stalf told me. “It’s a setup for the longer term. It’s good for a couple million customers,” Stalf added later in the conversation.

N26 is already planning more features for the U.S. The company plans to roll out two premium plans — N26 Metal and then N26 Black.

And it sounds like there will be some changes when it comes to perks for premium users. “We took that to a separate level,” Stalf said.

And shared Spaces are finally arriving in the coming months. Spaces are sub-accounts designed to put money aside. You can swipe money from one Space to another or you can set up automated rules.

Eventually, you’ll be able to share a Space with other people so that you can save money and spend money together. It’ll work “like a WhatsApp group,” Stalf said.

N26 currently has 3.5 million customers in Europe and has raised more than $500 million in total so far. There are now a thousand people working for N26 in Berlin, 60 employees in New York, 80 people in Barcelona and a small team of five to 10 people starting soon in Vienna.

“It went from being a small company to being an international company,” Stalf said.

Powered by WPeMatico