Mubadala Ventures

Auto Added by WPeMatico

Auto Added by WPeMatico

The rise of data breaches, along with an expanding raft of regulations (now numbering 80 different regional regimes, and growing) have thrust data protection — having legal and compliant ways of handling personal user information — to the top of the list of things that an organization needs to consider when building and operating their businesses. Now a startup called InCountry, which is building both the infrastructure for these companies to securely store that personal data in each jurisdiction, as well as a comprehensive policy framework for them to follow, has raised a Series A of $15 million. The funding is coming in just three months after closing its seed round — underscoring both the attention this area is getting and the opportunity ahead.

The funding is being led by three investors: Arbor Ventures of Singapore, Global Founders Capital of Berlin and Mubadala of Abu Dhabi. Previous investors Caffeinated Capital, Felicis Ventures, Charles River Ventures and Team Builder Ventures (along with others that are not being named) also participated. It brings the total raised to date to $21 million.

Peter Yared, the CEO and founder, pointed out in an interview the geographic diversity of the three lead backers: he described this as a strategic investment, which has resulted from InCountry already expanding its work in each region. (As one example, he pointed out a new law in the UAE requiring all health data of its citizens to be stored in the country — regardless of where it originated.)

As a result, the startup will be opening offices in each of the regions and launching a new product, InCountry Border, to focus on encryption and data handling that keep data inside specific jurisdictions. This will sit alongside the company’s compliance consultancy as well as its infrastructure business.

“We’re only 28 people and only six months old,” Yared said. “But the proposition we offer — requiring no code changes, but allowing companies to automatically pull out and store the personally identifiable information in a separate place, without anything needed on their own back end, has been a strong pull. We’re flabbergasted with the meetings we’ve been getting.” (The alternative, of companies storing this information themselves, has become massively unpalatable, given all the data breaches we’ve seen, he pointed out.)

In part because of the nature of data protection, in its short six months of life, InCountry has already come out of the gates with a global viewpoint and global remit.

It’s already active in 65 countries — which means it’s already equipped to store, process and regulate profile data in the country of origin in these markets — but that is actually just the tip of the iceberg. The company points out that more than 80 countries around the world have data sovereignty regulations, and that in the U.S., some 25 states already have data privacy laws. Violating these can have disastrous consequences for a company’s reputation, not to mention its bottom line: In Europe, the U.K. data regulator is now fining companies the equivalent of hundreds of millions of dollars when they violate GDPR rules.

This ironically is translating into a big business opportunity for startups that are building technology to help companies cope with this. Just last week, OneTrust raised a $200 million Series A to continue building out its technology and business funnel — the company is a “gateway” specialist, building the welcome screens that you encounter when you visit sites to accept or reject a set of cookies and other data requests.

Yared says that while InCountry is very young and is still working on its channel strategy — it’s mainly working directly with companies at this point — there is a clear opportunity both to partner with others within the ecosystem as well as integrators and others working on cloud services and security to build bigger customer networks.

That speaks to the complexity of the issue, and the different entry points that exist to solve it.

“The rapidly evolving and complex global regulatory landscape in our technology driven world is a growing challenge for companies,” said Melissa Guzy of Arbor Ventures, in a statement. Guzy is joining the board with this round. “InCountry is the first to provide a comprehensive solution in the cloud that enables companies to operate globally and address data sovereignty. We’re thrilled to partner and support the company’s mission to enable global data compliance for international businesses.”

Powered by WPeMatico

Wefox Group, the Berlin-based insurtech startup behind the consumer-facing insurance app and carrier One and the insurance platform Wefox, has raised $125 million in Series B funding. Notably, the round is led by Abu Dhabi government-owned Mubadala Ventures (which is also an LP in SoftBank’s Vision Fund) and is the first investment from Mubadala’s newly created European Investment Fund. Chinese investor Creditease also participated.

The investment, which Wefox Group says is the first tranche in the Series B round, will be used for expansion into the European broker market. The German company will also grow its product and engineering teams, specifically in relation to applying “advanced data analytics” to realise Wefox’s vision for an all-in-one insurance platform that places personalisation at the heart of how various insurance coverage is sold and delivered.

Wefox’s existing investors include Target Global, Salesforce Ventures, Seedcamp, Idinvest and Hollywood actor Ashton Kutcher’s investment vehicle Sound Ventures. The startup raised $28 million in Series A funding in late 2016.

In a call with Wefox Group co-founder and CEO Julian Teicke, he disclosed that Wefox has grown its revenues to around $40 million since being founded in 2014. The company now serves more than 1,500 brokers and more than 400,000 customers, making it “Europe’s number one insurtech platform.”

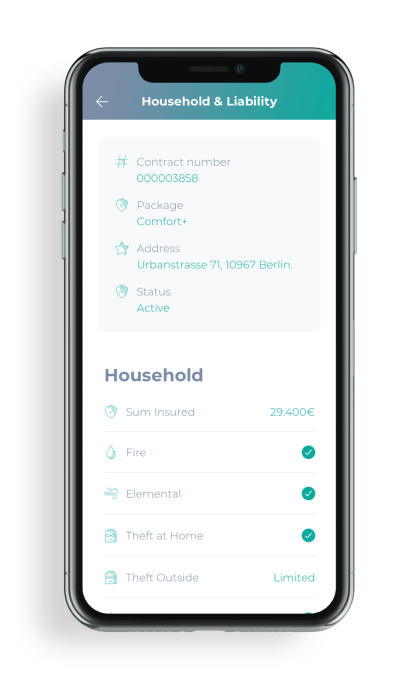

As it exists today, Wefox Group consists of two main products and subsidiaries: Wefox, and One.

Wefox is a platform that connects insurance providers, brokers and customers in an attempt to drag the insurance industry into the digital age. Rather than bypass human brokers entirely, Wefox lets independent brokers on-board their existing customers onto the platform to help deliver a better experience and more easily manage their clients’ coverage.

Efficiencies are achieved through a degree of automation, helping a broker scale the admin side of their business while also ensuring customers get the most appropriate coverage. From a consumer’s perspective, the Wefox app and website also acts as a “digital” wallet, where they can store details of the various insurance coverage to which they have subscribed.

Teicke says that about 80 percent of customers on the Wefox platform come via brokers. The remaining 20 percent sees customers sign-up direct. In this scenario, Wefox effectively acts as a lead generation or matching service for local brokers.

One is a direct-to-consumer fully digital insurance provider, offering various personal insurance coverage — and is only one of multiple insurance providers that reside on the Wefox platform and can be recommended by brokers. Teicke says it is also modular in design, letting customers select areas of coverage and essentially plugging in additional coverage based on their needs and appetite for risk at any given time. This includes pioneering the use of IoT and other data, customer permitting, to make insurance coverage proactive rather than reactive.

One is a direct-to-consumer fully digital insurance provider, offering various personal insurance coverage — and is only one of multiple insurance providers that reside on the Wefox platform and can be recommended by brokers. Teicke says it is also modular in design, letting customers select areas of coverage and essentially plugging in additional coverage based on their needs and appetite for risk at any given time. This includes pioneering the use of IoT and other data, customer permitting, to make insurance coverage proactive rather than reactive.

“The modular, timestamp and IoT triggered product design will be the role model for all insurance incumbents,” says Teicke. Related to this, Wefox Group plans to make the underlying technology of One available to other insurance providers so they too can plug proactive insurance provision into the Wefox platform, based on specific cohorts, scenarios and specialist coverage.

Ultimately, the grand vision and big bet — and no doubt what attracted such large amounts of capital into this Series B round — is that insurance will transition to a platform play, fueled by responsibly harnessing various types of data. The will see a platform exist to deliver the right coverage at the right time from a multitude of providers rather than the outdated and disparate model that exists today.

“Our hypothesis is that insurance will be massively impacted by the IoT data revolution,” says Teicke. “Insurers will have access to an exponentially grown number of real-time variables in order to price insurance products in real time. This trend will change insurance from a pure financial service to a service that offers proactive advice to reduce risk and consists of a financial service component only as an add-on to the core business model.”

Meanwhile, the new round of funding draws a line under a particularly tough period for Wefox Group after it was threatened with a lawsuit by New York-based insurance platform Lemon. The complaint, filed in the U.S. District Court Southern District of NY, alleged that Wefox reverse-engineered Lemonade to create One, and infringed Lemonade’s intellectual property. Ultimately, however, the dispute panned out to be a “much ado about nothing,” with Lemonade quietly dropping the lawsuit a few months later.

Powered by WPeMatico