mortgages

Auto Added by WPeMatico

Auto Added by WPeMatico

Housing is big money. The industry has trillions under management and hundreds of billions under development.

And investors have noticed the potential. Opendoor raised nearly $1.3 billion to help homeowners buy and sell houses more quickly. Katerra raised $1.2 billion to optimize building development and construction, and Compass raised the same amount to help brokers sell real estate better. Even Amazon and Airbnb have entered the fray with high-profile investments.

Amidst this frenetic growth is the seed of the next wave of innovation in the sector. The housing industry — and its affordability problem — is only likely to balloon. By 2030, 84% of the population of developed countries will live in cities.

Yet innovation in housing lags compared to other industries. In construction, a major aspect of housing development, players spend less than 1% of their revenues on research and development. Technology companies, like the Amazons of the world, spend nearly 10% on average.

Innovations in older, highly regulated industries, like housing and real estate, are part of what Steve Case calls the “third wave” of technology. VCs like Case’s Revolution Fund and the SoftBank Vision Fund are investing billions into what they believe is the future.

These innovations are far from silver bullets, especially if they lack involvement from underrepresented communities, avoid policy and ignore distributive questions about who gets to benefit from more housing.

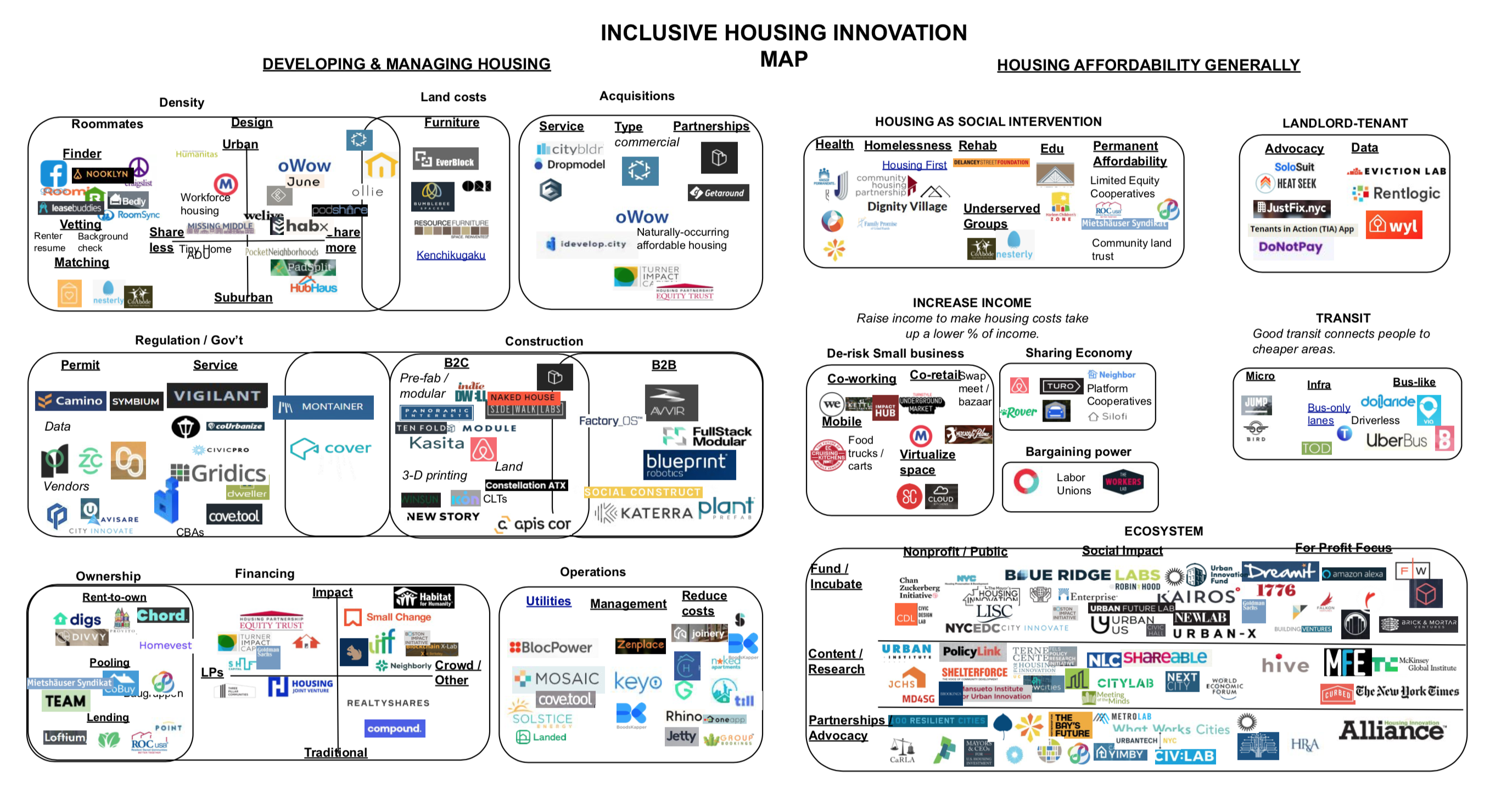

Yet there are hundreds of interventions reworking housing that cannot be ignored. To help entrepreneurs, investors and job seekers interested in creating better housing, I mapped these innovations in this package of articles.

To make sense of this broad field, I categorize innovations into two main groups, which I detail in two separate pieces on Extra Crunch. The first (Part 1) identifies the key phases of developing and managing housing. The second (Part 2) section identifies interventions that contribute to housing inclusion more generally, such as efforts to pair housing with transit, small business creation and mental rehabilitation.

Unfortunately, many of these tools don’t guarantee more affordability. Lowering acquisition costs, for instance, doesn’t mean that renters or homeowners will necessarily benefit from those savings. As a result, some tools likely need to be paired with others to ensure cost savings that benefit end users — and promote long-term affordability. I detail efforts here so that mission-driven advocates as well as startup founders can adopt them for their own efforts.

Today:

Coming Tomorrow:

Please feel free to let me know what else is exciting by adding a note to your LinkedIn invite here.

If you’re excited about this topic, feel free to subscribe to my future of inclusive housing newsletter by viewing a past issue here.

Powered by WPeMatico

San Francisco-based Blend is simplifying the process of mortgage applications for both borrowers and lenders, but is looking to expand into other lending products. To do that the company has raised $100 million in new funding led by Greylock, with participation from a bunch of existing investors. Read More

San Francisco-based Blend is simplifying the process of mortgage applications for both borrowers and lenders, but is looking to expand into other lending products. To do that the company has raised $100 million in new funding led by Greylock, with participation from a bunch of existing investors. Read More

Powered by WPeMatico

It’s difficult for tech workers and it’s even more difficult for those not touched by the modern gold rush. One mortgage originator, Opes Advisors, is incorporating restricted stock units (RSU) and private shares to make it easier for techies to move from incubator to nest egg. But what appears helpful to a population that sees housing prices moving out of reach could actually… Read More

It’s difficult for tech workers and it’s even more difficult for those not touched by the modern gold rush. One mortgage originator, Opes Advisors, is incorporating restricted stock units (RSU) and private shares to make it easier for techies to move from incubator to nest egg. But what appears helpful to a population that sees housing prices moving out of reach could actually… Read More

Powered by WPeMatico

Home loans are the Holy Grail of online lending. They come with high loan balances, steady returns and hefty fees. There also is a healthy liquid market for the securitized loans, and the debt is asset backed, which reduces risk and opens up the investor pool. On top of that, “establishment” mortgage lenders are not leading the pack with innovation, which means there is a lot of… Read More

Home loans are the Holy Grail of online lending. They come with high loan balances, steady returns and hefty fees. There also is a healthy liquid market for the securitized loans, and the debt is asset backed, which reduces risk and opens up the investor pool. On top of that, “establishment” mortgage lenders are not leading the pack with innovation, which means there is a lot of… Read More

Powered by WPeMatico

Habito, founded by Daniel Hegarty, pitches itself as the UK’s “first digital mortgage broker” — though Trussle may disagree — and offers an ‘fully automated’ brokering service to help you find the most suitable mortgage and make an application.

Habito, founded by Daniel Hegarty, pitches itself as the UK’s “first digital mortgage broker” — though Trussle may disagree — and offers an ‘fully automated’ brokering service to help you find the most suitable mortgage and make an application.