morgan stanley

Auto Added by WPeMatico

Auto Added by WPeMatico

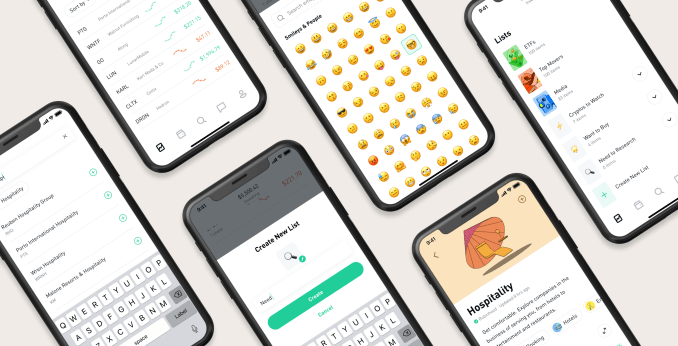

Yin Wu has co-founded several companies since graduating from Stanford in 2011, including a computer vision company called Double Labs that sold to Microsoft, where she stayed on for a couple of years as a software engineer. In fact, it was only after that sale she she says she “actually understood all of the nuances with a company’s cap table.”

Her newest company, Pulley, a 14-month-old, Mountain View, Ca.-based maker of cap table management software aims to solve that same problem and has so far raised $10 million toward that end led by the payments company Stripe, with participation from Caffeinated Capital, General Catalyst, 8VC and numerous angel investors.

Wu is going up against some pretty powerful competition. Carta was reportedly raising $200 million in fresh funding at a $3 billion valuation as of the spring (a round the company never official confirmed or announced). Last year, it raised $300 million. Morgan Stanley has meanwhile been beefing up its stock plan administration business, acquiring Solium Capital early last year and more recently purchasing Barclay’s stock plan business.

Of course, startups often manage to find a way to take down incumbents and a distraction for Carta, at least, in the form of a very public gender discrimination lawsuit by a former VP of marketing, could be the kind of opening that Pulley needs. We emailed with Yu yesterday to ask if that might be the case. She didn’t answer directly, but she did mention “values,” as well as sharing some more details about what she sees as different about the two products.

TC: Why start this company? Has Carta’s press of late created an opening for a new upstart in the space?

YW: I left Microsoft in 2018 and started Pulley a year later. We skipped the seed and raised the A because of overwhelming demand from investors. Many wanted a better product for their portfolio companies. Many founders are increasingly thinking about choosing with companies, like Pulley, that better align with their values.

TC: How many people are working for Pulley and are any folks you pulled out of Carta?

YW: We’re a team of seven and have four people on the team who are former Y Combinator founders. We attract founders to the team because they’ve experienced firsthand the difficulties of managing a cap table and want to build a better tool for other founders. We have not pulled anyone out of Carta yet.

TC: Carta has raised a lot of funding and it has long tentacles. What can Pulley offer startups that Carta cannot?

YW: We offer startups a better product compared to our competitors. We make every interaction on Pulley easier and faster. 409A valuations take five days instead of weeks, and onboarding is the same day rather than months. By analogy, this is similar to the difference between Stripe and Braintree when Stripe initially launched. There were many different payment processes when Stripe launched. They were able to capture a large portion of the market by building a better product that resonated with developers.

One of the features that stands out on Pulley is our modeling feature [which helps founders model dilution in future rounds and helps employees understand the value of their equity as the company grows]. Founders switch from our competitors to Pulley to use our modeling tool [and it works] with pre-money SAFEs, post-money SAFEs and factors in pro-ratas and discounts. To my knowledge, Pulley’s modeling tool is the most comprehensive product on the market.

TC: How does your pricing compare with Carta’s?

YW: Pulley is free for early-stage companies regardless of how much they raise. We’re price competitive with Carta on our paid plans. Part of the reason we started Pulley is because we had frustrations with other cap table management tools. When using other services, we had to regularly ping our accountants or lawyers to make edits, run reports or get data. Each time we involved the lawyers, it was an expensive legal fee. So there is easily a $2,000 hidden fee when using tools that aren’t self-serve for setting up and updating your cap table.

TC: Is there a business-to-business opportunity here, where maybe attorneys or accountants or wealth managers private label this service? Or are these industry professionals viewed as competitors?

YW: We think there are opportunities to white label the service for accountants and law firms. However, this is currently not our focus.

TC: How adaptable is the software? Can it deal with a complicated scenario, a corner case?

YW: We started Pulley one year ago and we’re launching today because we have invested in building an architecture that can support complex cap table scenarios as companies scale. There are two things that you have to get right with cap table systems, First, never lose the data and second, always make sure the numbers are correct. We haven’t lost data for any customer and we have a comprehensive system of tests that verifies the cap table numbers on Pulley remain accurate.

TC: At what stage does it make sense for a startup to work with Pulley, and do you have the tools to hang onto them and keep them from switching over to a competitor later?

YW: We work with companies past the Series A, like Fast and Clubhouse. Companies are not looking to change their cap table provider if Pulley has the tool to grow with them. We already have the features of our competitors, including electronic share issuance, ACH transfers for options, modeling tools for multiple rounds and more. We think we can win more startups because Pulley is also easier to use and faster to onboard.

TC: Regarding your paid plans, how much is Pulley charging and for what? How many tiers of service are there?

YW; Pulley is free for early-stage startups with less than 25 stakeholders. We charge $10 per stakeholder per month when companies scale beyond that. A stakeholder is any employee or investor on the cap table. Most companies upgrade to our premium plan after a seed round when they need a 409A valuation.

Cap table management is an area where companies don’t want a free product. Pulley takes our customers’ data privacy and security very seriously. We charge a flat fee for companies so they rest assured that their data will never be sold or used without their permission.

TC: What’s Pulley’s relationship to venture firms?

YW: We’re currently focused on founders rather than investors. We work with accelerators like Y Combinator to help their portfolio companies manage their cap table, but don’t have a formal relationship with any VC firms.

Powered by WPeMatico

TuSimple, the self-driving truck startup backed by Sina, Nvidia, UPS and Tier 1 supplier Mando Corporation, is headed back into the marketplace in search of new capital from investors. The company has hired investment bank Morgan Stanley to help it raise $250 million, according to multiple sources familiar with the effort.

Morgan Stanley recently sent potential investors an informational packet, viewed by TechCrunch, that provides a snapshot of the company and an overview of its business model, as well as a pitch on why the company is poised to succeed — all standard fare for companies seeking investors.

TuSimple declined to comment.

The search for new capital comes as TuSimple pushes to ramp up amid an increasingly crowded pool of potential rivals.

TuSimple is a unique animal in the niche category of self-driving trucks. It was founded in 2015 at a time when most of the attention and capital in the autonomous vehicle industry was focused on passenger cars, and more specifically robotaxis.

Autonomous trucking existed in relative obscurity until high-profile engineers from Google launched Otto, a self-driving truck startup that was quickly acquired by Uber in August 2016. Startups Embark and the now defunct Starsky Robotics also launched in 2016. Meanwhile, TuSimple quietly scaled. In late 2017, TuSimple raised $55 million with plans to use those funds to scale up testing to two full truck fleets in China and the U.S. By 2018, TuSimple started testing on public roads, beginning with a 120-mile highway stretch between Tucson and Phoenix in Arizona and another segment in Shanghai.

Others have emerged in the past two years, including Ike and Kodiak Robotics. Even Waymo is pursuing self-driving trucks. Waymo has talked about trucks since at least 2017, but its self-driving trucks division began noticeably ramping up operations after April 2019, when it hired more than a dozen engineers and the former CEO of failed consumer robotics startup Anki Robotics. More recently, Amazon-backed Aurora has stepped into trucks.

TuSimple stands out for a number of reasons. It has managed to raise $298 million with a valuation of more than $1 billion, putting it into unicorn status. It has a large workforce and well-known partners like UPS. It also has R&D centers and testing operations in China and the United States. TuSimple’s research and development occurs in Beijing and San Diego. It has test centers in Shanghai and Tucson, Arizona.

Its ties to, and operations in China can be viewed as a benefit or a potential risk due to the current tensions with the U.S. Some of TuSimple’s earliest investors are from China, as well as its founding team. Sina, operator of China’s biggest microblogging site Weibo, is one of TuSimple’s earliest investors. Composite Capital, a Hong Kong-based investment firm and previous investor, is also an investor.

In recent years, the company has worked to diversify its investor base, bringing in established North American players. UPS, which is a customer, took a minority stake in TuSimple in 2019. The company announced it added about $120 million to a Series D funding round led by Sina. The round included new participants, such as CDH Investments, Lavender Capital and Tier 1 supplier Mando Corporation.

TuSimple has continued to scale its operations. As of March 2020, the company was making about 20 autonomous trips between Arizona and Texas each week with a fleet of more than 40 autonomous trucks. All of the trucks have a human safety operator behind the wheel.

Powered by WPeMatico

The economic lockdown resulting from the coronavirus pandemic has had an immediate negative impact on renewable energy projects and electric vehicles sales, but the sustainable trends are still in place and may even be strengthened over the longer term.

For the first time in four decades, global installation of solar, wind and other renewable energy will be less than the previous year, according to the International Energy Agency, which is projecting a 13% reduction in installations in 2020 compared to 2019. Woods Mackenzie projects an 18% reduction for global solar installations in 2020. Morgan Stanley is projecting declines in U.S. solar PV installations from 48% in second quarter to 17% in the fourth quarter of 2020.

This is due to a combination of construction delays, supply chain disruptions and a capital crunch.

Installation of rooftop solar has been hit particularly hard. Access to homes and businesses was generally halted in March 2020 for several months. Installers have indicated that as much as half the workforce had to be furloughed. The supply chain was also disrupted as PV manufacturing in China was temporarily suspended. Installations and the supply chain will resume, and most contracts are still in place, but the robust projected growth in rooftop PV for 2020 will not be met, and it may take more than a year to catch up. Also, some businesses that planned installations may have higher priorities for cash and investment now as they reopen. Many of the small businesses planning solar installations may not return at all.

On the other hand, utility scale electricity generation from renewable energy continues to grow and take market share. In the first part of this year, renewable energy has produced more electricity than coal for the first time since the late 19th century, when hydropower started the power industry. Wind and solar are the cheapest alternatives for new electric generation in the U.S. The pandemic and collapse in oil prices will not change that. The closure of coal plants has been accelerating this year, and wind and solar will continue to be competitive with gas.

Furthermore, most solar and wind farms were already financed and construction underway in rural areas not affected by the lockdown. About 30 GW of new solar capacity have already been contracted, and as long as interest rates remain low, financing should not be a problem. In fact, many solar and wind projects in the U.S and China are rushing to completion this year to qualify for government incentives.

But supply chains for utility scale renewables were still disrupted. Solar panel manufacturing in China was halted during the first quarter and has now reopened, but facing reduced orders. At one point, 18 wind turbine manufacturing facilities in Spain and Italy were stopped while social distancing and sanitation measures were put in place. Mining operations in Africa and other countries were also temporarily halted and now face reduced demand.

The replacement of oil and gas electricity generation with renewables in developing countries is not going to seem as attractive as a few years ago. Emerging economies need to expand electricity as cheaply as possible, which means coal, gas and even diesel plants. New fossil fuel plants in developing nations could lock in carbon emissions for years.

Electric vehicle sales globally have also been severely impacted. The transition to electric vehicles takes place as people purchase new vehicles. The price of oil has collapsed, used-car prices are dropping and unemployment has soared to levels not seen since the Great Depression. Cheap gas, cheap cars and high unemployment will dramatically lower the expectations for multipassenger EV sales in 2020. Wood Mackenzie has projected a 43% global decline in EV sales in 2020 from 2019. Furthermore, many new electric models from the automakers are not expected until 2021.

However, the long-term transition to EVs will continue and may even accelerate. It still costs less to drive a mile on electricity compared to gasoline, and when the upfront cost of electric vehicles becomes competitive with internal combustion vehicles in a few years, the market should quickly move to EVs. Now that the battery range is adequate for the average driver, the last barrier seems to be the availability of fast charging stations between cities.

Before the collapse in oil demand this year, the oil majors were expecting peak oil demand to occur sometime during the 2040s. Now peak oil demand is expected earlier, perhaps in the mid-2020s. Some even think that 2019 might turn out to be the highest level of oil consumption historically. At any rate, it seems that it will be at least a few years until the 2019 levels are reached again, if ever.

However, the recent collapse in oil prices means the oil and gas industry will be able to supply fuel at very competitive prices for decades. This will at least make it more difficult for electric vehicles to take market share in the short term, and very difficult for alternative liquid fuels to be competitive. For biofuels and synthetic fuels, it seems to be a repeat of earlier decades when cheap oil crushed those industries. Replacing gas and diesel-powered cars is certainly going to be unattractive in the impoverished economies of developing nations.

But there are also bright spots for clean transportation alternatives emerging. Electric bicycles, for example, are a hot item. As people look for alternatives to mass transit and want something to move outdoors in the fresh air, electric-assisted bikes are a great solution and are no longer looked down upon as a vehicle for older (or lazy) cyclists.

Telecommuting struggled for years to take hold, but the pandemic seems to have finally changed that. The recent national lockdown has spurred many large businesses to set up their employees to work from home. They have found that it works fairly well, and many will not return to packed downtown offices.

Several experts have cited the potential for cleaner energy alternatives because the public is seeing cleaner air and the environmental benefits of a 30% reduction in daily oil consumption. Some consumer surveys have indicated a greater interest in electric vehicles.

There is certainly the hope that we will take the opportunity to revive the economy with cleaner technologies than before the lockdown. However, the reality is that workers and businesses need to start up again with the infrastructure they have, and investment in cleaner technology requires capital. Since many business operations are struggling to find cash and loans to just remain open, new clean technology may be delayed.

Yet the major infrastructure changes for a sustainable future are well underway. Solar and wind are rapidly replacing fossil fuels for electricity. Automakers and governments are committed to electrification of the transportation sector. The pandemic may be a near-term obstacle, but the transition to a sustainable economy is just delayed and may even be accelerated in the coming years.

Powered by WPeMatico

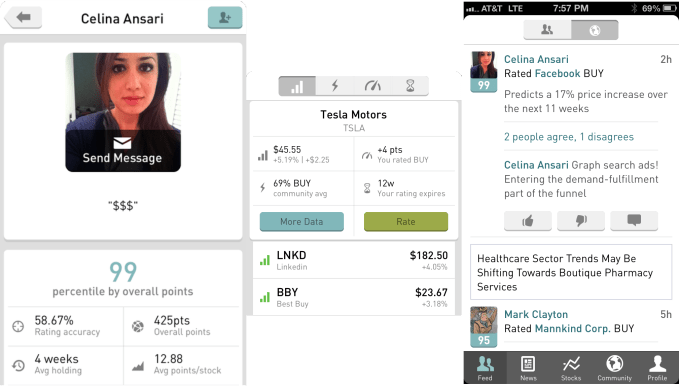

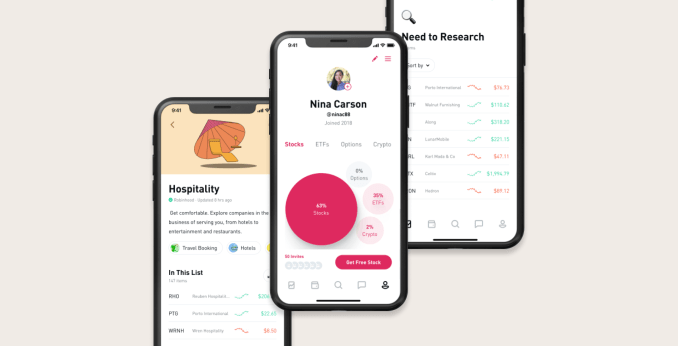

Before it was worth $7.6 billion, the original idea for Robinhood was a stock-trading social network. At my kitchen table in San Francisco in 2013, the founders envisioned an app for sharing hot tips to a feed complete with a leaderboard of whose predictions were most accurate. Once they had SEC approval, they pivoted toward the real money maker: letting people buy and sell stocks in the app, and pay to borrow cash to do so.

Now, seven years later, Robinhood is subtly taking the first steps back to its start. Today it’s launching Profiles. For now, they let users see analytics about their portfolio, like how concentrated they are in stocks versus options versus cryptocurrency, as well as across different business sectors. Complete with usernames and a photo, Profiles let you follow self-made or Robinhood-provided lists of stocks and other assets.

Profiles could give Robinhood’s customers the confidence to trade more, and create a sense of lock-in that stops them from straying to other brokerages that have dropped their per-trade fees to zero to match the startup, like Charles Schwab, Ameritrade and E-Trade, which was acquired for $13 billion today by Morgan Stanley, as reported by The Wall Street Journal.

The Profile features certainly sound helpful. They could reveal that your portfolio is too centered around tech, media and telecom stocks, or that you’re ignoring cryptocurrency or corporations from your home state. Lists also makes it easier to track specific business verticals, save stocks to buy when you have the cash or set aside some for deeper research. Robinhood pulls info from FactSet, Morningstar and other trusted sources to figure out which stocks and ETFs go into sector lists, or you can make and name your own. Profiles and lists begin to roll out to all users next week.

But what’s most interesting is how profiles lay the foundation for Robinhood as a social network. It’s easy to imagine letting users follow other accounts or lists they create. The original Robinhood app let users make predictions like “17% increase in Facebook share price over the next 11 weeks,” with comments to explain why. It showed users’ prediction accuracy, their average holding time for assets, a point score for smart foresight and community BUY or SELL ratings on stocks.

If Robinhood rebuilt some of these features, it might lessen the need for an expensive financial advisor or having enough cash to qualify for one with a different brokerage. Robinhood could let you crowdsource advice. “We understand the connotation of taking something from the rich and giving it to the poor. Robinhood is liberating information that’s locked up with professionals and giving it to the people,” Robinhood co-founder and co-CEO Vlad Tenev told me back in 2013.

Robinhood would certainly need to be careful about scammy tips going viral. Improper safeguards could lead to pump and dump schemes where those late to buy in get screwed when prices snap back to reality.

But embracing social could leverage some of its strongest assets: the youthfulness of its user base and the depth of connection to its users. The median age of a Robinhood customer is 30, and half say they’re first-time investors. Being able to turn to friends or experts within the app might convince them to pull the trigger on trades.

Most online brokerages are somewhat undifferentiated beyond differences in pricing, while their clunky, unstylized products don’t generate the same brand affinity as people have for Robinhood. Unsatisfied users could bail for a competitor at any time. Robinhood’s users are accustomed to social networking and the way it locks in users, because they don’t want to abandon their community.

When I asked Robinhood Profiles’ product manager Shanthi Shanmugam directly about whether this was the start of more social trading features, they suspiciously dodged the question, telling me, “When thinking about how to reflect who you are as an investor, we looked at how other apps represent you and it felt natural to leverage a design that felt more like a profile. When helping people group their investment ideas, it was easy to envision this as a playlist you might find on your favorite music app.”

That’s far from a denial. Offering social validation for trading could help Robinhood earn more from its customers despite their small total account balances. While Robinhood might have more than 10 million accounts versus E-Trade’s 5.2 million and Morgan Stanley’s 3 million, E-Trade’s average account size is $69,230 and Morgan Stanley’s is $900,000, while a survey found most of Robinhood’s held $1,000 to $5,000.

That all means that Robinhood earns less on interest sitting in users’ accounts than the old incumbents. But Robinhood earns the majority of its money on selling order flow and through its subscription Robinhood Gold feature that lets users pay monthly so they can borrow cash to trade with. Profiles and lists, and then eventually more social features, could get Robinhood’s users trading more so there’s more order flow to sell and more reason for them to buy subscriptions.

“Democratizing access is about lowering fees, minimums and other barriers people face — like confidence. Profiles and lists make finance easier to understand and more familiar for people,” says Shanmugam. More social features built safely, more reassurance, more trading, more revenue. Robinhood has raised $910 million. But to outgun larger competitors like the newly assembled Morgan Stanley/E-Trade that’s matched its zero-fee pricing, Robinhood will have to win with product.

Powered by WPeMatico

Airbnb may be another overvalued “unicorn,” but it’s no WeWork.

The Information this morning reported new Airbnb financials — indicating a massive increase in operating losses — that immediately call Airbnb’s future into question. Precisely, Airbnb lost $306 million on operations on $839 million in revenue, namely as a result of marketing spend, in the first quarter of 2019. In total, Airbnb invested $367 million in sales and marketing, representing a 58% increase year-over-year, in Q1. The company is gearing up for a major liquidity event next year and is making a concerted effort to rake in new customers, as any soon-to-be-public business would.

Given WeWork’s sudden demise, coupled with Uber and Lyft’s lukewarm performances on the stock markets, many have wondered how Wall Street will respond to Airbnb’s eventual IPO prospectus. Will money managers have an appetite for another over-valued Silicon Valley darling? Or will the market compete like mad for shares in the massive home-sharing marketplace?

But Airbnb, again, is no WeWork, and I wager Wall Street will have a much friendlier approach to its offering. For one, Airbnb’s co-founder and chief executive officer Brian Chesky isn’t dropping $60 million on private jets — I don’t think. CEO behaviors aside, Airbnb has more capital in the bank than it has raised in its entire 11-year history, which is a whole lot of money. This is all according to a source who is familiar with Airbnb’s financials and shared this detail with TechCrunch following The Information’s Thursday morning report. As for Airbnb, the company told TechCrunch, “we can’t comment on the figures, but 2019 is a big investment year in support of our hosts and guests.”

")

Airbnb’s CEO Brian Chesky speaks at TechCrunch Disrupt SF 2014

Airbnb has attracted more than $3.5 billion in equity funding at a $31 billion valuation and has even more locked away in its bank account. Additionally, Airbnb has an untouched $1 billion credit line, the source said. Presumably, the referenced credit line is the 2016 $1 billion debt financing from JPMorgan, CitiGroup, Morgan Stanley and others.

Moreover, Airbnb has been “cumulatively” free cash flow positive for some time, meaning that it’s seen more money coming in than going out during recent quarters, according to our source. It has been reported that Airbnb surpassed $1 billion in revenue in the second quarter of 2019 and in the third quarter of 2018, but we’re guessing the business did not top $1 billion in Q4 of 2018 or Q1 of 2019 because it if had, that information would probably have been “leaked.”

Finally, Airbnb has been profitable on an EBITDA (earnings before interest, taxes, depreciation and amortization) basis for two consecutive years, the company announced in January. Gross bookings, meanwhile, are growing, as is Airbnb’s business offering and its experiences product.

Powered by WPeMatico

Slack, the popular workplace messaging company, is expected to list on the New York Stock Exchange on Thursday in the second major direct listing in the U.S. after Spotify introduced the concept to investors in April of last year.

At this point, plenty of industry observers think it makes sound sense for Slack to embrace the direct listing approach, wherein a company places its stock on a public exchange without raising any money or using underwriters. Though the company warned last week that its operating losses are widening as it chases new customers, it has $800 million on its balance sheet, meaning it doesn’t need to raise more right now.

Slack also doesn’t need underwriters who typically discount a company’s shares in order to ensure that they appreciate in value when they begin trading. It’s a known brand in the tech world, and that universe is broadening by the day. Put another way, Slack doesn’t need to be “sold” for investors to want to snap up its shares.

Still, we wondered about some of the thinking that has gone into preparing Slack for its move into the world of publicly traded companies, so we talked with a couple of people who are familiar with what’s happening behind the scenes to find out more. They asked not to be named, but here’s what we learned:

1) Unlike with the popular streaming music platform Spotify, which has more than 100 million premium subscribers and roughly twice as many active monthly users, Slack wasn’t as well-known to Wall Street as Silicon Valley might imagine. In fact, we’re told the bankers that were selected to advise Slack on its offering — Morgan Stanley, Goldman Sachs and Allen & Co., which are the same three that advised Spotify — had to provide more education to analysts and institutional investors this time around.

2) There will (hopefully) be enough shares to go around, while also not a glut of them. The big concern in a direct offering — which does not feature a lock-up period — is that too many people will dump their shares on the market, crushing the company’s share price, or else that too few will part with their holdings, turning the buying and selling of the company’s shares into a financial game of chicken. We’ll see what happens here, but we’re told the banks have spent the last six months trying to ensure that many — but not all — of the company’s institutional shareholders will be selling some of their stakes at the offering, Also worth noting is that unlike with Spotify, some Slack employees have restricted stock units that will vest upon its public listing and so be part of the supply of shares on its first day.

3) In establishing guidance around how Spotify’s shares should be valued, the banks advising the company looked almost entirely to its private market trades, of which there were many. There has been less secondary activity with Slack’s shares, so the banks are likely to rely on these sales but also to use other inputs. We’ll learn soon enough what they settle on, but based on the latest prices at which its shares have traded in the private market, Slack’s presumed valued right now is at $16.7 billion, or 36 times trailing 12-month sales.

4) You might imagine that banks hate direct listings because of the rich underwriting fees they aren’t collecting, and they probably do. Still, even with a direct listing, they get paid pretty well, thanks to both advisory fees and also because investors often trade through the banks named as advisers in the prospectus. There are also fewer mouths to feed on a deal with a direct listing. In Slack’s case — as happened with Spotify — Morgan Stanley, Goldman Sachs and Allen & Co. will reportedly reap almost all of the spoils — or a reported 90% of the $22 million in fees earmarked for all the advisers involved in the deal. In a traditional IPO, a longer number of banks that promise research coverage are given shares to sell, which eats into lead underwriters’ allotment.

5) One risk that Slack shouldn’t necessarily run into but that may have adversely impacted Uber’s IPO is its investor base. According to Slack’s S-1, its biggest outside shareholders include Accel (it owns 24% sailing into the offering), Andreessen Horowitz (13.3%), Social Capital (10.2%) and SoftBank (7.3 %). Why it matters: Slack doesn’t have to worry about less traditional private company backers like mutual funds not wanting to buy up its shares because they’re too busy trying to offload some.

6) Direct listings may well become a more popular product for consumer companies because companies can avoid further dilution, and there’s no lock-up on their shares, creating a shorter path to liquidity for the company and its employees and its investors. Still, Slack is probably anomalous as an enterprise company with a high enough profile to pull one off. The listings are really for companies that don’t need money any time soon and whose shares are already of interest to investors, who don’t need inducements to pay attention.

7) This is the second direct listing of a highly valued privately held company and, for the second time, it’s happening on the NYSE, with the same market maker, Citadel Securities, charged with ensuring orderly trading; the same bank, Morgan Stanley, selected to advise Citadel; and even the same law firms that worked on Spotify’s direct listing pulled back into service.

It’s nice if you’re part of this particular club, and no one can blame Slack for not wanting to reinvent the wheel. But one wonders how nervous it makes Nasdaq, as well as other banks and law firms, to be shut out of this process a second time.

Powered by WPeMatico

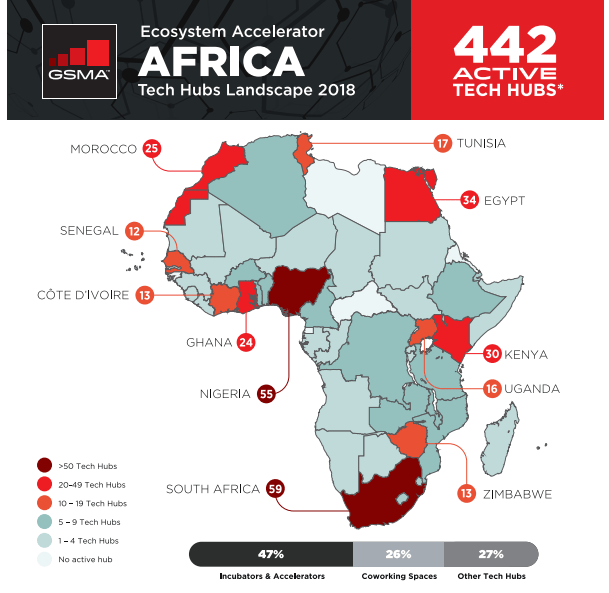

Jumia may be the first startup you’ve heard of from Africa. But the e-commerce venture that recently listed on the NYSE is definitely not the first or last word in African tech.

The continent has an expansive digital innovation scene, the components of which are intersecting rapidly across Africa’s 54 countries and 1.2 billion people.

When measured by monetary values, Africa’s tech ecosystem is tiny by Shenzen or Silicon Valley standards.

But when you look at volumes and year over year expansion in VC, startup formation, and tech hubs, it’s one of the fastest growing tech markets in the world. In 2017, the continent also saw the largest global increase in internet users—20 percent.

If you’re a VC or founder in London, Bangalore, or San Francisco, you’ll likely interact with some part of Africa’s tech landscape for the first time—or more—in the near future.

That’s why TechCrunch put together this Extra-Crunch deep-dive on Africa’s technology sector.

A foundation for African tech is the continent’s 442 active hubs, accelerators, and incubators (as tallied by GSMA). These spaces have become focal points for startup formation, digital skills building, events, and IT activity on the continent.

Prominent tech hubs in Africa include CcHub in Nigeria, Pan-African incubator MEST, and Kenya’s iHub, with over 200 resident members. More of these organizations are receiving funds from DFIs, such as the World Bank, and aid agencies, including France’s $76 million African tech fund.

Prominent tech hubs in Africa include CcHub in Nigeria, Pan-African incubator MEST, and Kenya’s iHub, with over 200 resident members. More of these organizations are receiving funds from DFIs, such as the World Bank, and aid agencies, including France’s $76 million African tech fund.

Blue-chip companies such as Google and Microsoft are also providing money and support. In 2018 Facebook opened its own Hub_NG in Lagos with partner CcHub, to foster startups using AI and machine learning.

Powered by WPeMatico

SoFi is one of the leading fintech startups to emerge from San Francisco and breach the financial markets. Originally started as a way to better finance student debt, it has since expanded to include products targeted at personal loans and home loans.

Today, the company announced a new exchange-traded fund (ETF) product focused on the gig economy. GIGE, which trades on Nasdaq, is an actively managed fund advised by Toroso Investments that allows investors to capitalize on this hot sector of the economy. Toroso offers a range of services around creating and managing ETFs.

The company also announced the creation of an ETF focused on high-growth stocks. That ETF, which trades as SFYF on the NYSE, is designed to identify and capture the growth of the top 50 of the 1,000 largest publicly traded issues.

It has formerly used that growth focus to create two ETFs, targeting 500 high-growth companies under the trading name SFY and a product it called “SoFi Next 500 ETF,” which trades under SFYX, both of which have no management fees.

SoFi’s SFYF fund is composed specifically of public companies that show the strongest growth on three key metrics: top-line revenue growth, net income growth and forward-looking consensus estimates of net income growth.

For its GIGE fund, SoFi defines the “gig economy” as a group of companies that “embrace and support the workforce in which employment is based around short-term engagements that allow for flexibility and personal freedom and temporary contracts.”

SoFi’s new funds add value to investors primarily through providing 1) access to industry disruptors at 2) an earlier-stage point in their growth cycle.

In recent years, more and more investors have been trying to get a piece of the hottest tech companies earlier with a growing number of traditional institutional investors now dipping their toes into startup and tech investing.

Furthermore, a number of platforms and funds were launched to support the high-demand for access to some of the top public and private companies and major disruptive trends, including funds focused on themes such as artificial intelligence, big data, cybersecurity or the next manufacturing revolution.

SoFi argues that its GIGE fund offers compelling value due to the speed at which it offers investors access to new equity issues, as the fund is structured so that most post-IPO companies can join the GIGE within 31 days of IPO, relative to the 60-90 days traditional passive funds that often have to wait to add a newly IPO’d company.

Additionally, because SoFi’s GIGE fund is actively managed, SoFi is also offering fund investors access to experienced asset managers and an alternative to algorithmic, machine-led passive funds that have increasingly dominated the capital markets.

“Our members are excited by high-growth and gig economy companies because these companies are in many cases part of their lives,” said SoFi CEO Anthony Noto in a press release. “We’re giving our members a way to get started investing by buying what they know and investing in themselves.”

The announcement is the company’s latest step in its attempt to further establish itself under the new guard of CEO Anthony Noto, formerly of Goldman Sachs, who replaced former head Michael Cagney in 2018, as the company looks to move further away from dark clouds in its past established by lawsuits, sexual harassment claims, FTC penalties and chunky rounds of layoffs. In the past week, the company also announced that CMO and former COO, Joanne Bradford, will be leaving the company at the end of May, though the split was reportedly long-planned and amicable.

The launch of SoFi’s new investment products also comes just weeks after the company was reportedly in discussions to raise $500 million from the Qatar Investment Authority.

To date, SoFi has raised roughly $2 billion in venture capital, according to data from Crunchbase, with backing from a number of Silicon Valley and Wall Street heavy hitters, including SoftBank, Silver Lake Partners, Morgan Stanley, Founders Fund and a host of others.

Already at a valuation of nearly $4.5 billion, according to PitchBook, SoFi appears well on its way to an eventual IPO. Noto, however, noted in a recent interview with Yahoo Finance that “an IPO is not a priority at this point” for SoFi as the company remains focused on executing on a high-quality sustainable growth path.

Powered by WPeMatico

The RealReal, an online retailer for authenticated luxury consignment, has authorized the sale of up to $70 million in new shares, per a Delaware stock authorization filing discovered by the Prime Unicorn Index. If the company raises the entire amount, it would reach a valuation of $1.06 billion, cementing its status as the newest e-commerce unicorn.

The filing doesn’t guarantee The RealReal will sell the full amount of authorized shares. The company declined to comment on its fundraising plans.

The RealReal is led by founder and chief executive officer Julie Wainwright (pictured), the former CEO of Pets.com, a company now synonymous with the dot-com bust. It has raised quite a bit of capital to date — a total of $288 million from venture capital and private equity backers, including Great Hill Partners, Sandbridge Capital, PWP Growth Equity, Industry Ventures, Greycroft Partners and Canaan Partners. Most recently, The RealReal closed a Series G financing of $115 million in July 2018 that valued the business at $745 million, per PitchBook.

The RealReal has recently expanded its brick-and-mortar footprint and added additional e-commerce fulfillment centers as demand increased for its supply of second-hand luxury items. Founded in 2011, the company operates eight luxury consignment offices, where customers can receive free valuations of their luxury items. The RealReal is headquartered in San Francisco.

In a conversation with TechCrunch in 2017, Wainwright confirmed the company’s intent to go public at some point. With this upcoming round, The RealReal would be well placed for a 2020 initial public offering.

“That’s the goal,” Wainwright said during the interview. “We really aren’t in the mood to sell the business, we’re in the mood to go public at some point in the future.”

The RealReal competes with fellow second-hand e-tailers ThredUp and Poshmark . The latter is gearing up for a fall IPO, according to The Wall Street Journal. The online marketplace has tapped Morgan Stanley and Goldman Sachs to lead its offering after closing in on $150 million in revenue in 2018. ThredUp, another major player in the fashion retail market, hasn’t raised capital since 2015, but did begin opening physical stores in 2017 as part of its greater effort to compete with fellow venture-backed second-hand e-tailers.

The RealReal would also be the latest in a series of high-profile female-founded companies to gain unicorn status. Glossier tripled its valuation to $1.2 billion with a $100 million round earlier this year, followed by Rent the Runway, which attracted a $125 million investment at a $1 billion valuation, to name a few.

Powered by WPeMatico

Zoom, the only profitable unicorn in line to go public, priced its initial public offering at between $28 and $32 per share Monday morning. The video conferencing business plans to trade on the Nasdaq under the ticker symbol “ZM.”

Zoom, valued at $1 billion in 2017, initially filed to go public in March. According to its amended IPO filing, the company will raise up to $348.1 million by selling 10.9 million Class A shares. The offering will grant Zoom a fully diluted market value of $8.7 billion, a more than 8x increase to its latest private market valuation.

Although the company has garnered praise for its stellar financials — Zoom posted $330 million in revenue in the year ending January 31, 2019, a remarkable 2x increase year-over-year, with a gross profit of $269.5 million — the road to IPO hasn’t been without hiccups.

The company’s founder and chief executive officer Eric Yuan last night published an open letter concerning the conduct of Zoom’s chief financial officer Kelly Steckelberg. According to the letter, Zoom was recently informed by an anonymous source that Steckelberg had an “undisclosed, consensual relationship” during her tenure at a previous employer.

Steckelberg was most recently the CEO of the online dating site Zoosk; before that, she was a senior director in consumer finance at Cisco . The letter does not specify where the relationship took place, when or with whom.

Losing a CFO mere days before an IPO would have been a major loss for Zoom. CFOs often become the face of the IPO, handling the grueling tasks associated with crafting an IPO prospectus, leading the roadshow and more, while also maintaining day-to-day financial operations.

Yuan writes that the Zoom’s board of directors conducted a full investigation into the matter and determined that Steckelberg would stay on as Zoom’s CFO: “Kelly expressed regret for what transpired at her former employer, took ownership for the situation, and made clear to us that she had learned valuable lessons from the experience,” he wrote.

“We appreciated Kelly’s openness and candor during this process,” he continued. “It is clear that this matter related only to circumstances at her former employer. During Kelly’s tenure at Zoom, she has been an incredible contributor, as well as a model steward of our culture, values, and high standards since joining the Company.”

We reached out to Zoosk for comment. Zoom declined to comment further.

Zoom, expected to make the final call on its IPO price next Wednesday, will likely price at the top of the range and see a clean pop on its first day on the markets given its clean track record and positive financials. The business was founded in 2011 by Eric Yuan, an early engineer at WebEx, which sold to Cisco for $3.2 billion in 2007. Before launching Zoom, he spent four years at Cisco as its vice president of engineering.

Zoom has raised $145 million to date from investors, including Emergence Capital, which owns a 12.2 percent pre-IPO stake; Sequoia Capital (11.1 percent pre-IPO stake); Digital Mobile Venture (8.5 percent), a fund affiliated with former Zoom board member Samuel Chen; and Bucantini Enterprises Limited (5.9 percent), a fund owned by Li Ka-shing, a Chinese billionaire and among the richest people in the world.

Morgan Stanley, JP Morgan and Goldman Sachs are leading its offering.

Powered by WPeMatico