money

Auto Added by WPeMatico

Auto Added by WPeMatico

Diem, a London, U.K.-based fintech startup, has raised a seed round of $5.5 million led by Fasanara Capital, and angel investor Chris Adelsbach, founder of Outrun Ventures. Additional investors include Andrea Molteni (early investor in Farfetch), Ben Demiri (co-chairman at fashion tech PlatformE) and Nicholas Kirkwood (founder of the eponymous brand).

Diem is a debit card with an app affording instant cash access, traditional banking service benefits (debit card, domestic and international bank transfers), but also allowing consumers to dispose of goods for eventual resale. The idea here is that this feeds into the so-called circular economy, making Diem attractive from an environmental point of view. Some estimates put the amount of worth of goods disposed of in the last 15 years at $6.9 trillion.

Here’s how it works: You have an old item of clothing, phone, book or bag, for instance. You load the item it into the app. The app makes you an offer for what the item is worth. If you accept, cash is loaded into your account immediately. You send the item to Diem, which is then resold. The incentive, therefore, is not to throw away the object and add to landfill, because you have now turned it into cash. Think “neo bank meets people who sell your stuff on eBay.”

Geri Cupi said in a statement: “Diem’s mission is to empower consumers to value, unlock, and enjoy wealth they never knew they had. All of this while fuelling the circular economy and supporting the commitment to sustainability as our key value proposition. DIEM makes it possible for capitalism and sustainability to co-exist.”

Lead Investor and CEO at Fasanara Capital, Francesco Filia, said: “Fasanara is excited to announce our partnership with DIEM and Geri Cupi… [it’s] a new generation fintech powered by principles of circular economy and look forward to support its growth.”

Powered by WPeMatico

One of the biggest gripes about investing apps is that they are not acting responsibly by not educating users properly and allegedly letting them fend for themselves. This can result in people losing a lot of money, as evidenced by the number of lawsuits against Robinhood.

Today, an eight-year-old company that has been focused on nothing but financial education is now offering trading and banking services in the U.S..

Over the years, London-based Invstr has built out an educational platform with features such as an investing academy. It’s created a Fantasy Finance game, which gives users the ability to manage a virtual $1 million portfolio so they can learn more about the markets before risking their own money for real. Via social gamification, Invstr has set out to make the educational process fun.

It has also built a community around users so they can learn from each other (something another Robinhood competitor Gatsby is also doing).

Over 1 million users have downloaded the platform globally.

Invstr, according to CEO and founder Kerim Derhalli, is taking a different approach from competitors by offering education and learning tools upfront. And in addition to giving users the ability to make commission-free stock trades, it’s also giving them a way to digitally bank and invest using their Invstr+ accounts “without ever needing to move money from one place to another.”

Invstr takes it all a step further for subscribers who have access to an “Invstr Score,” performance stats and behavioral analytics among other things.

Derhalli said moving in this direction with the company was part of his business plan from day one.

“I think the most powerful trend in the U.S. is self-directed investing,” Derhalli told TechCrunch. “Younger generations have grown up in an app world and they expect to be autonomous and do things for themselves. Many distrust the banking system, and they don’t want to follow in their parents’ footsteps when it comes to banking and finance. We think this is a massive opportunity.”

In the unveiling of its new offerings, Invstr also announced Wednesday that it has closed on a $20 million Series A in the form of a convertible offering. This builds upon $20 million it previously raised across two seed rounds from investors such as Ventura Capital, Finberg, European angel investor Jari Ovaskainen and Rick Haythornthwaite, former global chairman of Mastercard.

Derhalli said he felt compelled to found Invstr after seeing firsthand how a lack of knowledge and confidence can prevent individuals from starting to invest. He worked for three decades in senior leadership roles at Deutsche Bank, Lehman Brothers, Merrill Lynch and JPMorgan before founding Invstr “so that anyone, anywhere could learn how to invest.”

Invstr is offering its new investing services in partnership with Apex Clearing, which formerly provided execution and settlement services to Robinhood. Its digital banking services are being offered through a partnership with Vast Bank. To address the security piece, Invstr said its user data is also protected by technology from Okta.

The company, which also has offices in New York and Istanbul, plans to use the new capital to launch new brokerage and analytics tools and a portfolio builder.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion. Use code “TCARTICLE at checkout to get 20% off tickets right here.

Powered by WPeMatico

U.S. challenger bank Current, which has doubled its member base in less than six months, announced this morning it raised $131 million in Series C funding, led by Tiger Global Management. The additional financing brings Current to over $180 million in total funding to date, and gives the company a valuation of $750 million.

The round also brought in new investors Sapphire Ventures and Avenir. Existing investors returned for the Series C, as well, including Foundation Capital, Wellington Management Company and QED.

Current began as a teen debit card controlled by parents, but expanded to offer personal checking accounts last year, using the same underlying banking technology. The service today competes with a range of mobile banking apps, offering features like free overdrafts, no minimum balance requirements, faster direct deposits, instant spending notifications, banking insights, check deposits using your phone’s camera and other now-standard baseline features for challenger banks.

In August 2020, Current debuted a points rewards program in an effort to better differentiate its service from the competition, which as of this month now includes Google Pay.

When Current raised its Series B last fall, it had over 500,000 accounts on its service. Today, it touts over 2 million members. Revenue has also grown, increasing by 500% year-over-year, the company noted today.

“We have seen a demonstrated need for access to affordable banking with a best-in-class mobile solution that Current is uniquely suited to provide,” said Current founder and CEO Stuart Sopp, in a statement about the fundraise. “We are committed to building products specifically to improve the financial outcomes of the millions of hard-working Americans who live paycheck to paycheck, and whose needs are not being properly served by traditional banks. With this new round of funding we will continue to expand on our mission, growth and innovation to find more ways to get members their money faster, help them spend it smarter and help close the financial inequality gap,” he added.

The additional funds will be used to further develop and expand Current’s mobile banking offerings, the company says.

Powered by WPeMatico

While a handful of tech companies like Zoom and Shopify are enjoying massive gains as a result of COVID-19, that’s obviously not the case for most. Weaker demand, slower sales cycles, and customer insistence on pricing concessions and payment deferrals have conspired to cloud the outlook for many tech companies’ growth.

Compounding these challenges, a lot of tech companies are struggling to raise capital just when they need it most. The data so far suggests that investors, particularly those focused on earlier stage financings, are taking a more cautious approach to new deals and valuations while they wait to see how individual companies perform and which way the economy will go. With the outcome of their planned equity financings uncertain, some tech companies are revisiting their funding strategies and exploring alternative sources of capital to fuel their continued growth.

For certain businesses, COVID-19’s impact on revenue was immediate. For others, the effects of slower economic activity and tighter budgets surfaced more gradually with deals in the funnel before the pandemic closing in April and May. Either way, in the second half of 2020, technology CFOs face a common challenge: How do you accurately forecast sales when there’s very little consensus around key issues such as when business activity will return to pre-COVID levels and what the long-term effects of the crisis might be?

Unfortunately, navigating this uncertainty is just as daunting a challenge for investors. These days, equity investors’ assessment of a company’s growth potential, and the value they are willing to pay for that growth, aren’t just impacted by their view of the company itself. Equally important is their assumptions about when the economy will recover and what the new normal might look like. This uncertainty can lead to situations where companies and their potential investors have materially different views on valuation.

While the full impact of COVID was felt too late to have a material impact on Q1 deal volumes, recently released data from Pitchbook and the NVCA suggest that 2020 will see a significant decrease in the number of companies funded, possibly by as much 30 percent compared to 2019 among early stage companies. And, while it often takes several months to see evidence of broad trends in investment terms, anecdotal evidence indicates investors are seeking to mitigate risk by demanding additional protective provisions.

Powered by WPeMatico

If necessity is the mother of invention, then new business owners are getting very inventive in the ways in which they access cash. Relying on some long-tested and some new avenues to raise money, entrepreneurs are finding more ways to get public market cash faster than they would have in the past.

Whether it’s from Reg A crowdfunding dollars, Special Purpose Acquisition Companies (SPACs) or direct listings, these somewhat arcane and specialized financing vehicles are making a comeback alongside a rise in new funding mechanisms to get to market quickly and avoid the dilution that comes from private market rounds (especially since those rounds are likely to come at a reduced valuation given market conditions).

Some of these tools have existed for a while and are newly popular in an era where retail investors are driving much of the daily fluctuations of the public markets. Wall Street institutions are largely maintaining their conservative postures with regard to new offerings, so secondary market retail volume growth is outpacing institutional. Retail investors want into these new issues and are pouring into the markets, contributing to huge pops to new public offerings for companies like Lemonade this Thursday and creating an environment where SPACs and crowdfunding campaigns can flourish.

The rise of zero-commission brokerages and the popularization of fractional trading led by the startup Robinhood and adopted by every one of the major online brokers including Charles Schwab, TD Ameritrade, E-Trade and Interactive Brokers has created a stock market boom that defies the underlying market conditions in the U.S. and globally. For instance, daily trades on Robinhood are up 300% year-over-year as of March 2020.

According to data from the BATS exchange, the total trade count in the U.S. was up 71% and May trading was up more than 43% over 2019. Meanwhile, E-Trade daily average revenue trades posted a 244% increase in May over last year’s numbers.

The appetite for new issues is growing and if many of the largest venture-backed companies are holding off on going public, smaller names are using SPACs to access public capital and reach these new investors.

Powered by WPeMatico

Corporate venture capitalists (CVCs) are booming in the startup space as large companies look to take advantage of the fast-paced innovation and original thinking that entrepreneurs offer.

For startups, taking funding from CVCs can come with many benefits, including new opportunities for marketing, partnerships and sales channels. Still, no founder should consider a corporate investor “just another VC.” CVCs come with their own set of priorities, strategic objectives and rules.

When it comes to choosing a CVC with which to enter negotiations, the most important step is doing your own diligence beforehand. An entrepreneur’s goal is to find the perfect match to partner with and guide you as you grow your business. So before you start discussing terms, you’ll want to understand what’s driving the CVC’s interest in venture investing.

While traditional VCs are purely financially driven, CVCs can be in the venture game for a variety of reasons, including finding new technology that might generate marketplace demand for their products. An example is Amazon’s Alexa fund, which invested into emerging companies that drive use and adoption of Alexa. Alternatively, a CVC’s parent company may be looking to invest in tech that will help them operate their own products more efficiently, such as Comcast Ventures investing in DocuSign.

As a rule of thumb, the bigger CVC funds like GV and Comcast tend to be financially driven, meaning they’ll be approaching negotiations through a financial lens. As such, the negotiating process more closely resembles an institutional fund. You as a founder have to do the work to figure out what’s driving your CVC — is this a customer acquisition or distribution opportunity? Or are they seeking to find a source of knowledge transfer and/or bring new tech into their parent company?

“Before negotiating, always look at a CVC’s existing portfolio,” says Rick Prostko, managing director at Comcast Ventures. “Have they made a lot of investments, at what stage, and with whom? From this information you’ll see the strategic thinking of the CVC, and you can determine how best to position yourself when you begin negotiations.”

Powered by WPeMatico

Khatabook, a startup that is helping small businesses in India record financial transactions digitally and accept payments online with an app, has raised $60 million in a new financing round as it looks to gain more ground in the world’s second most populous nation.

The new financing round, Series B, was led by Facebook co-founder Eduardo Saverin’s B Capital. A range of other new and existing investors, including Sequoia India, Partners of DST Global, Tencent, GGV Capital, RTP Global, Hummingbird Ventures, Falcon Edge Capital, Rocketship.vc and Unilever Ventures, also participated in the round, as did Facebook’s Kevin Weil, Calm’s Alexander Will, CRED’s Kunal Shah and Snapdeal co-founders Kunal Bahl and Rohit Bansal.

The one-and-a-half-year-old startup, which closed its Series A financing round in October last year and has raised $87 million to date, is now valued between $275 million to $300 million, a person familiar with the matter told TechCrunch.

Hundreds of millions of Indians came online in the last decade, but most merchants — think of neighborhood stores — are still offline in the country. They continue to rely on long notebooks to keep a log of their financial transactions. The process is also time-consuming and prone to errors, which could result in substantial losses.

Khatabook, as well as a handful of young and established players in the country, is attempting to change that by using apps to allow merchants to digitize their bookkeeping and also accept payments.

Today more than 8 million merchants from over 700 districts actively use Khatabook, its co-founder and chief executive Ravish Naresh told TechCrunch in an interview.

“We spent most of last year growing our user base,” said Naresh. And that bet has worked for Khatabook, which today competes with Lightspeed -backed OkCredit, Ribbit Capital-backed BharatPe, Walmart’s PhonePe and Paytm, all of which have raised more money than Khatabook.

The Khatabook team poses for a picture (Khatabook)

According to mobile insight firm AppAnnie, Khatabook had more than 910,000 daily active users as of earlier this month, ahead of Paytm’s merchant app, which is used each day by about 520,000 users, OkCredit with 352,000 users, PhonePe with 231,000 users and BharatPe, with some 120,000 users.

All of these firms have seen a decline in their daily active users base in recent months as India enforced a stay-at-home order for all its citizens and shut most stores and public places. But most of the aforementioned firms have only seen about 10-20% decline in their usage, according to AppAnnie.

Because most of Khatabook’s merchants stay in smaller cities and towns that are away from large cities and operate in grocery stores or work in agritech — areas that are exempted from New Delhi’s stay-at-home orders, they have been less impacted by the coronavirus outbreak, said Naresh.

Naresh declined to comment on AppAnnie’s data, but said merchants on the platform were adding $200 million worth of transactions on the Khatabook app each day.

In a statement, Kabir Narang, a general partner at B Capital who also co-heads the firm’s Asia business, said, “we expect the number of digitally sophisticated MSMEs to double over the next three to five years. Small and medium-sized businesses will drive the Indian economy in the era of COVID-19 and they need digital tools to make their businesses efficient and to grow.”

Khatabook will deploy the new capital to expand the size of its technology team as it looks to build more products. One such product could be online lending for these merchants, Naresh said, with some others exploring to solve other challenges these small businesses face.

Amit Jain, former head of Uber in India and now a partner at Sequoia Capital, said more than 50% of these small businesses are yet to get online. According to government data, there are more than 60 million small and micro-sized businesses in India.

India’s payments market could reach $1 trillion by 2023, according to a report by Credit Suisse .

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re taking a look at a bit of data on the European venture capital scene in Q1. As with our looks at other locales like Silicon Valley and other bits of the United States, we’re taking stock of what happened in the first quarter. Q1 2020 includes pre-COVID-19 results, though as some European countries began to lock-down before the United States, there may be more pandemic-impact in the following results than we’ve seen domestically thus far.

Today’s grip of data is via the folks over at PitchBook, who compiled a venture-focused dig through the continent’s first three months of the year. Let’s parse the top numbers, make a comparison or two and then look to what’s next.

Despite COVID-19, China’s broad shuttering and an aged bull market deep, Europe’s venture capital activity in Q1 2020 was mostly fine. It wasn’t great, and there were some less-than-winsome results that could be chalked up to the pandemic, but the first quarter provided an alright start to the year.

Powered by WPeMatico

Frank, a New York-based student-facing startup, has raised $5 million in what the company described as an “interim strategic round” that Chegg, a public edtech company, took part in. According to Frank founder and CEO Charlie Javice, previous investors Aleph and Marc Rowan took part in the round alongside new investor GingerBread Capital.

The education funding-focused startup last raised known capital in December of 2017, when it closed a $10 million Series A. Frank raised a seed round earlier that same year worth $5.5 million.

According to Javice, her firm closed its round in early March, before the recent market carnage. Bearing in mind that there is always lag between when a funding round is closed and when it is announced, the new Frank round is on the fresher side of things. Most rounds are a bit more like Shippo’s recent investment (closed in December, announced in April) than Podium’s recent deal, which it started raising in mid-February of this year.

Timing aside, what Frank is doing is interesting, so let’s talk about its business, how it approached 2019 and how it’s faring in today’s changed market.

To help keep student debt low, Frank is a bit akin to TurboTax for college money, as TechCrunch wrote when covering its Series A, helping students get through a thicket of forms and aid to collect as much aid as possible while avoiding borrowing.

American higher education is too expensive, and applying for financial help is irksome and byzantine. I can safely report that sans quoting an expert, as I had to go through it as a student and only finished paying my student loans last July.

Frank wants to help make college more affordable, with the company noting in a call with TechCrunch that there’s been a good number of companies working to help students service debt in a less expensive way after they’ve hired the money; it wants to help students avoid taking on so much red ink in the first place.

According to Javice, lots of students fail to finish signing up for federal aid programs, and some students wind up dropping out of programs before finishing them, leaving them saddled with debt but no degree. That’s a hell of a trap to wind up in, as student loans are the barnacles of the financial world — incredibly hard to get rid of.

According to Javice, Frank was a little early to rethinking its own growth/profit trade-off than the rest of the startup world, which woke up when WeWork filed to go public and was quickly booed off Wall Street. In mid-2019, Frank slowed growth to get closer to the margins it wanted. (Thinking out loud, this is probably how the startup managed to survive so long off its December 2017 Series A.)

Indeed, according to Frank’s CEO, it was in a comfortable cash position before this round, which she described as more a vote of confidence than a round of necessity.

Which brings us to today, and the new, COVID-19 world. In an email to TechCrunch, Javice said that “like everyone else,” her company is “adjusting to the new realities.” She added that college and university attendance “has typically been countercyclical” and that her company is “seeing a large demand for higher education and specifically financial aid.”

If the new economy winds up creating a little tailwind for Frank, it won’t be the only startup to accrue help; Slack and Zoom and other remote work-friendly companies have also seen their fortunes turn for the better in recent weeks. And now with $5 million more on hand, it can certainly meet new demand.

Update: An earlier version of this article listed Chegg as the round’s lead investor; it did receive a board seat in the transaction but Frank does not consider it a lead investor. The post has been amended.

Powered by WPeMatico

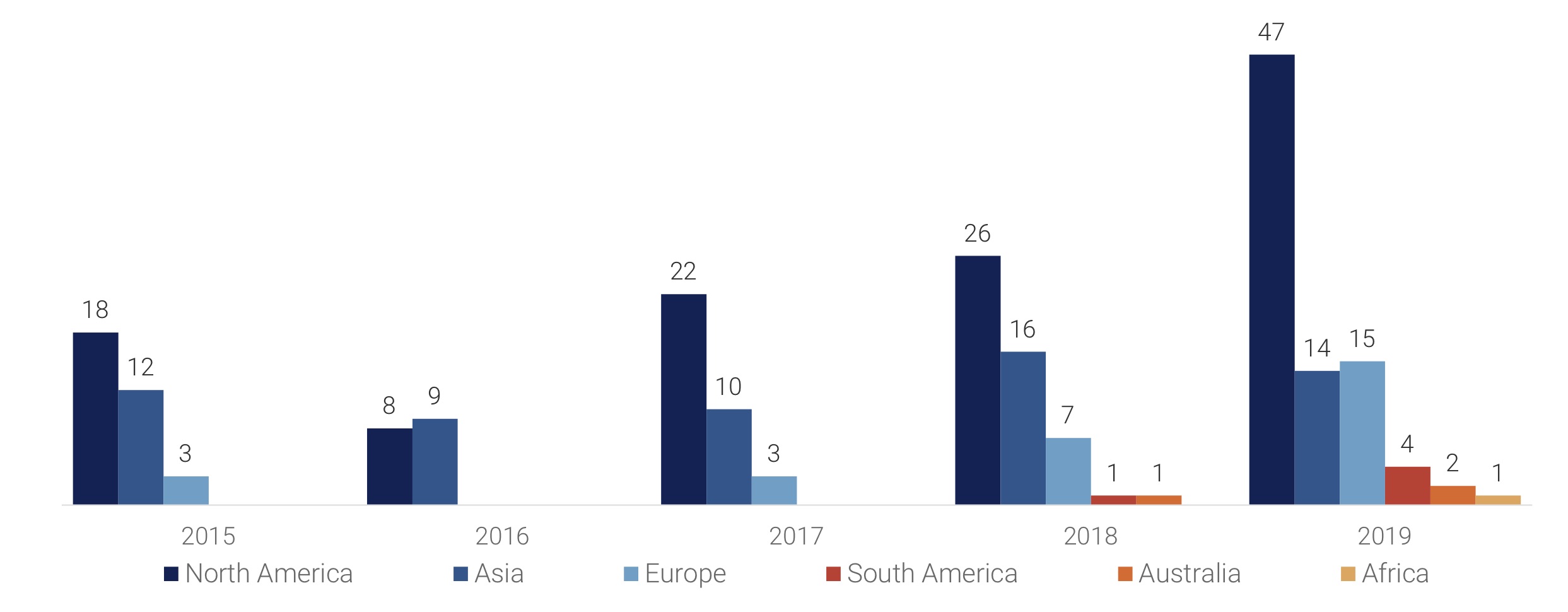

Financial services startups raised less money in 2019 than they did in 2018 as VC firms looked to back late stage firms and focused on developing markets, a new report has revealed.

According to research firm CB Insights’ annual report published this week, fintech startups across the world raised $33.9 billion* in total last year across 1,912 deals*, down from $40.8 billion they picked up by participating in 2,049 deals the year before.

It’s a comprehensive report, which we recommend you read in full here (your email is required to access it), but below are some of the key takeaways.

Early-stage deals dropped to a 12-quarter low as deal share globally shifts to mid- and late-stages (CB Insights)

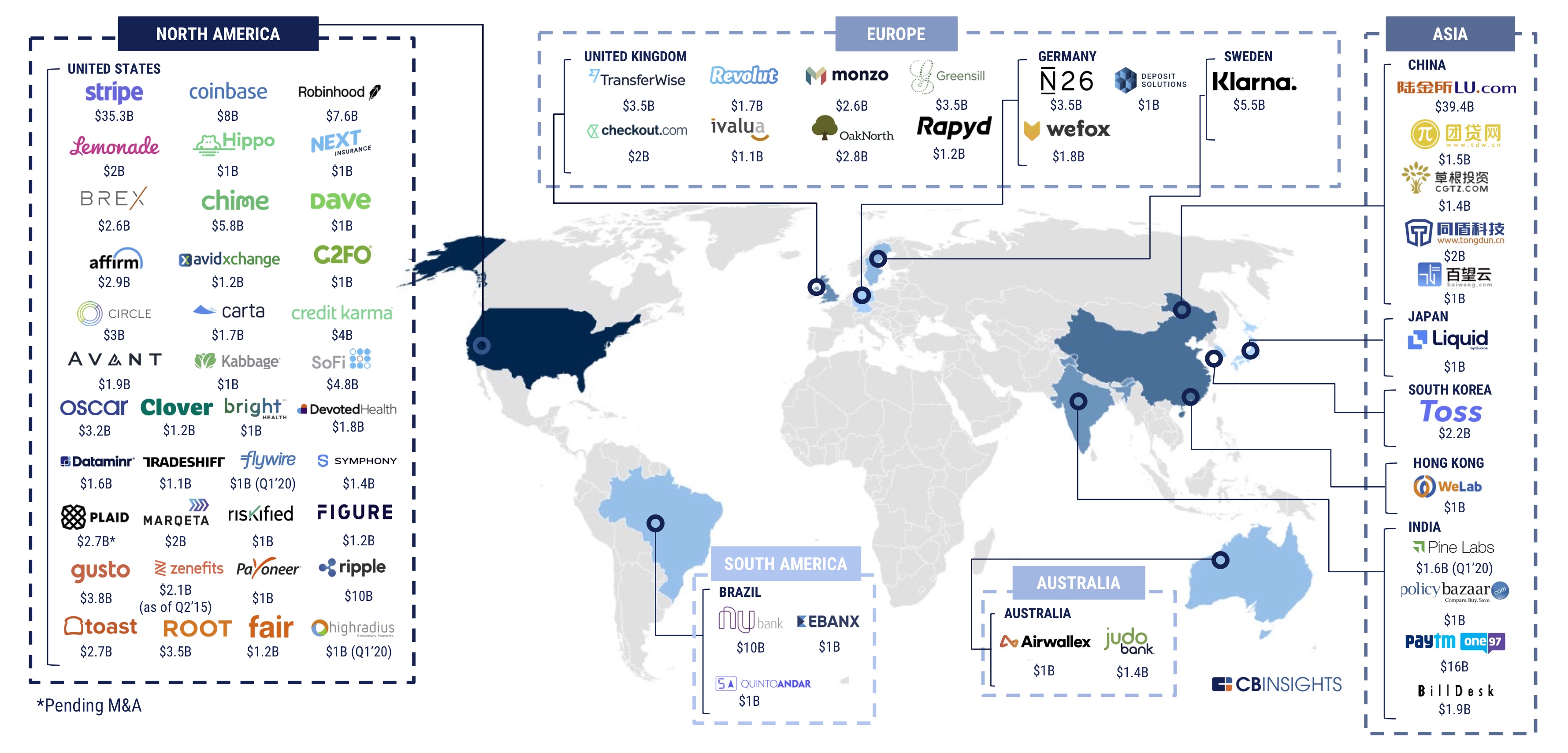

The fintech market globally today has 67 unicorns as of earlier this month (CB Insights)

2019 saw 83 mega-rounds totaling $17.2B, a record year in every market except Europe

*CB Insights report includes a $666 million financing round of Paytm . It was incorrectly reported by some news outlets and the $666 million raise was part of the $1 billion round the Indian startup had revealed weeks prior. We have adjusted the data accordingly.

Powered by WPeMatico