mobile banking

Auto Added by WPeMatico

Auto Added by WPeMatico

U.S.-based challenger bank Current, which has now grown to nearly 3 million users, announced this morning it has raised a $220 million round of Series D funding, led by new investor Andreessen Horowitz (a16z). The funding swiftly follows Current’s $131 million Series C at the end of last year, at which point the company had doubled its user base over just six months to more than 2 million users.

As a result of the new round, the fintech company has roughly tripled its valuation in five months, to $2.2 billion.

Other participants in the round include returning investors Tiger Global Management, TQ Ventures (the fund managed by media executive Scooter Braun), Avenir, Sapphire Ventures, Foundation Capital, Wellington Management and EXPA. David George, who led the round with a16z, will become a Current board member.

Current began its life as a teen debit card controlled by parents, but later expanded to offer personal checking accounts powered by the same underlying banking technology. Like a range of modern-day “neobanks,” or digital banks, the Current app offers a baseline of standard features like free overdrafts, no minimum balance requirements, faster direct deposits, instant spending notifications, banking insights, free ATMs, check deposits using your phone’s camera and more. It also last year launched a points rewards program in an effort to better differentiate its service from the growing number of competitors and became one of the first banks to transfer the early round of stimulus payments during the pandemic.

These days, Current is partnering with creators, like the recently announced MrBeast (aka Jimmy Donaldson), who said last week on his YouTube channel that he will personally send $1 to the first 100,000 people who sign up using his Creator code. MrBeast is also an investor.

Like other fintechs in its same space, Current has benefitted from the younger generation’s adoption of mobile banking apps instead of larger, traditional banks, which they feel don’t serve their interests. Its average customer age is 27, for example. Digital banks can keep costs down by not having to pay for the overhead of brick-and-mortar locations, allowing them to roll out benefits like reduced or zero account fees and other consumer-friendly protections.

Current today continues to offer teen banking, in a challenge to mobile banking app Step, which has also leveraged social media influencers to get the word out with a younger demographic. But Step today is appealing to the 13 to 18-year-old crowd directly, offering banking services and a secured card. Current, meanwhile, targets its service to the parents.

Its teen account costs $36 per year, while personal checking is available both as a free and premium ($4.99/mo) service. The company in the past has said its primary focus is the more than 130 million Americans who live paycheck to paycheck. This continues to be its main drive today, though the mission may attract a broader slice of the American population over time.

“We are still focused on onboarding people to the financial system, making sure that everyone has access to everything, and then democratizing — or going out and getting that value — in this new world that’s being rewritten and bringing it back to as many people as possible,” says Current CEO and founder Stuart Sopp. “Now, in that increase of scope and time. I think we’re going to pick up more and more people.”

Current says the new funds will be used to grow the company and its member base as it expands it range of banking products. One key area of new investment will be cryptocurrency, it says, which will involve a partnership and an educational component to help Current’s users better understand the crypto market.

As it turns out, Sopp’s background includes crypto, in addition to Wall Street trading. In fact, an early version of Current designed by Sopp and CTO Trevor Marshall involved crypto.

“A little-known fact is that Current started with Bitcoin wallet addresses and Ripple gateways,” he says. But the team realized the technology was a little too nascent at the time, and moved to mobile banking. “We have this background, and this knowledge of how it all works. Now do we need to build it ourselves? No, I don’t think we need to build it all ourselves. There’s lots of good companies out there,” he says.

Crypto fits into Current’s vision of democratizing access to financial systems to those in the U.S. who are today underserved by traditional banking and investing products and services.

“There’s a ton of value being created [in crypto] and we want to make sure we have this nexus of providing safe, and trustworthy financial services in that world, as well as what we already exist in,” notes Sopp. “And then, lending, credit cards,” he adds, noting how important these moves are “done safely, in a respectful way for our demographic — because traditionally most of our members have a FICO score of 650.”

In addition, Current will use the new funds for hiring across all roles, including marketing, product, engineering, finance, customer success, fraud and risk, and, of course, crypto. The company today has 100 employees, and plans to grow to around 200 or 300 in the next 18 months.

Current’s fundraise remarkably falls on the same day that competitor Step and Greenlight, both which focus on families, also raised new rounds.

“This new generation of customers doesn’t want to bank in physical branches,” said a16z’s David George, in a statement. “We believe there will be a shift in the next 10 years to mobile and consumer-focused banking services powered by innovation in technology, and with Current’s exceptional growth over the past year, they’ve clearly demonstrated they’re at the forefront of this trend. Their product is among the best in the market, and they have proven an ability to reach customers who previously were unserved or underserved by traditional banks,” he said.

Powered by WPeMatico

Flux, the London fintech that has built a technology platform for banks and merchants to power itemised digital receipts and more, has seen its lengthy pilot with Barclays bear fruit.

Announced formally today — but actually quietly rolled out a few months ago — Flux-powered digital receipts are now available as an opt-in for all U.K. Barclays debit card holders within the bank’s main mobile banking app. Previously, the functionality was only available within the Barclays Launchpad app, which is available for customers that want to try out experimental or upcoming features.

Early last year, Barclays announced that it has invested in Flux, taking a minority stake, so the strengthening of its partnership isn’t too much of a surprise. Flux also went through the Techstars-powered Barclays accelerator in its very early days. However, not all corporate accelerators lead to great outcomes as corporates are notoriously risk-adverse. This one certainly wasn’t rushed but it’s meaningful regardless, giving Flux a major shot in the arm in reaching mainstream banking customers beyond the existing challenger bank partnerships it has forged.

“Customers who pay using their Barclays debit card for future in store purchases at H&M, shoe retailer schuh and food outlets, which include Just Eat and Papa Johns, will see their receipts sent automatically to their app after making a purchase. They can then easily and securely view their receipts whenever they need by tapping on the transaction,” says Barclays. Crucially, although opt-in, Barclays customers will receive a prompt to set up digital receipts when they purchase items from retailers currently on-boarded to Flux.

Founded in 2016 by former early employees at Revolut, Flux bridges the gap between the itemised receipt data captured by a merchant’s point-of-sale (POS) system and what little information typically shows up on your bank statement or mobile banking app. Off the back of this, it can also power loyalty schemes and card-linked offers, as well as give merchants much deeper POS analytics via aggregated and anonymised data on consumer behaviour, such as which products are selling best in unique baskets.

On the banking side, along with Barclays, Flux has partnered with challenger banks Starling and Monzo. Once banking customers link their account to the service, Flux delivers digital receipts (and where available rewards and loyalty) for transactions at Flux retailer partners.

Longer term, Flux wants to become a standard for the interchange of item level digital receipt data — and the proprietary platform that powers that standard — but has always faced a chicken-and-egg problem: It needs bank integrations to sign up merchants and it needs merchant integrations to sign up banks. Barclays going live properly is another significant turn in the upstart’s flywheel.

Powered by WPeMatico

U.S. challenger bank Current, which has doubled its member base in less than six months, announced this morning it raised $131 million in Series C funding, led by Tiger Global Management. The additional financing brings Current to over $180 million in total funding to date, and gives the company a valuation of $750 million.

The round also brought in new investors Sapphire Ventures and Avenir. Existing investors returned for the Series C, as well, including Foundation Capital, Wellington Management Company and QED.

Current began as a teen debit card controlled by parents, but expanded to offer personal checking accounts last year, using the same underlying banking technology. The service today competes with a range of mobile banking apps, offering features like free overdrafts, no minimum balance requirements, faster direct deposits, instant spending notifications, banking insights, check deposits using your phone’s camera and other now-standard baseline features for challenger banks.

In August 2020, Current debuted a points rewards program in an effort to better differentiate its service from the competition, which as of this month now includes Google Pay.

When Current raised its Series B last fall, it had over 500,000 accounts on its service. Today, it touts over 2 million members. Revenue has also grown, increasing by 500% year-over-year, the company noted today.

“We have seen a demonstrated need for access to affordable banking with a best-in-class mobile solution that Current is uniquely suited to provide,” said Current founder and CEO Stuart Sopp, in a statement about the fundraise. “We are committed to building products specifically to improve the financial outcomes of the millions of hard-working Americans who live paycheck to paycheck, and whose needs are not being properly served by traditional banks. With this new round of funding we will continue to expand on our mission, growth and innovation to find more ways to get members their money faster, help them spend it smarter and help close the financial inequality gap,” he added.

The additional funds will be used to further develop and expand Current’s mobile banking offerings, the company says.

Powered by WPeMatico

Another afternoon, another round of funding for a mobile banking app. This time, it’s Empower Finance, a San Francisco-based company that’s headed up by former Sequoia Capital partner Warren Hogarth and which just closed on $20 million in Series A funding from Icon Ventures and Defy Ventures.

David Velez, who is the founder and CEO of Nubank, the largest fintech in Latin America, also joined the round.

We’d first written about the company in 2017, when Hogarth was just getting the business off the ground. Fast-forward a bit and Empower now employs 35 people and has attracted more than 600,000 active users to its platform, says Hogarth. What has drawn them in: the company’s promise of combining AI and actual human financial planners to help millennials in particular accrue some wealth, including, more newly, through its own checking account product and through a savings account that’s currently promising 1.60% in annual percentage yield with no minimums, no overdraft fees and unlimited withdrawals.

It’s all part of an overall offering that crunches through account holders’ bank and credit card accounts, and recommends how much they save into which account, how much they should spend given their overall picture, various ways they can cut costs and where and when they’ve surpassed their pre-configured budgets.

Of course, the company has so much competition it’s dizzying, but like the various upstarts against which it’s battling for mindshare, the opportunity that Empower is chasing is enormous, too. Though companies like Chime can seem overpriced given how fast investors have marked up their rounds — Chime’s newest financing, announced in December, was done at a $5.8 billion post-money valuation, which was four times more than the company was worth at the outset of 2019 — digital banks are still tiny fish in an ocean of institutional financial services, representing something like 3% of the market.

They’re gaining more market share by the day, too, including by charging far lower fees for much more.

In Empower’s case, users pay $6 a month, but Hogarth says they also save $300 a year in additional fees they would pay a brick-and-mortar bank. He insists that on average, it also helps them save $1,300 more annually, too.

As for all those other companies — Mint, Acorns, the list goes on — Hogarth sounds surprisingly sanguine. “If you look at it from the outside, it looks crowded. But the consumer financial services in the U.S. is a $2 trillion business, and we haven’t had a fundamental shift since maybe Schwab came along 30 years ago.”

Indeed, says Hogarth, because Empower and its rivals are mobile and branchless and don’t have legacy software to contend with, they’re able to take 60 to 70% of the cost structure out of the business.

What that means on an individual company level is that even if each upstart can attract 2 to 3 million customers, they can get to a multibillion-dollar market cap. At least, that kind of math is “why there’s so much interest in this space,” says Hogarth.

It’s also why people like Nubank’s Velez, who have seen this story play out in Europe and Latin America and who are seeing the early phases of it in the U.S., are apparently keeping the money spigot open for now.

Empower had earlier raised an undisclosed amount of seed funding from Sequoia, followed by a $4.5 million round led by Initialized Capital.

Powered by WPeMatico

Mobile banking app Current, which began as a teen debit card controlled by parents, expanded to offer personal checking accounts earlier this year. Now the company says it has grown to host more than 500,000 accounts on its service and has closed on $20 million in Series B funding to further its growth.

The round included new investors Wellington Management Company, Galaxy Digital EOS VC Fund and CMFG Ventures — the venture capital arm of the CUNA Mutual Group, a mutual insurance company serving credit unions and their 120 million members. Returning investors included QED Investors, Expa and Elizabeth Street Ventures.

The first version of Current, which debuted in 2017, was focused on giving parents a more modern way to dole out allowances and reward their kids for chores. But over time, the product became more like a real bank account for teens, culminating with the addition of routing and account numbers late last year. This allowed working teens to direct their paycheck to Current, as they could with a traditional bank.

The first version of Current, which debuted in 2017, was focused on giving parents a more modern way to dole out allowances and reward their kids for chores. But over time, the product became more like a real bank account for teens, culminating with the addition of routing and account numbers late last year. This allowed working teens to direct their paycheck to Current, as they could with a traditional bank.

This year, Current launched personal checking using the same core technology powering its teen banking product. The product includes features like faster direct deposits, gas hold crediting and merchant blocking without charging overdraft fees, hidden fees or requiring minimum balances.

While the teen checking account users have an average age of 15, the average age for the new personal checking account users is 27.

Although personal checking was only launched in late January, it already accounts for about half of Current’s accounts. It also benefits from conversions from Current’s teen users who turn 18 and want to graduate to their own banking app. (Around 98% of teens on Current move to the personal checking app when they come of age, the company noted.)

This puts Current in a more competitive market, where a number of banking apps are now targeting a younger, more mobile generation that has begun to favor modern, feature-rich apps over brick-and-mortar banks. Among its rivals are apps like Step, Cleo, N26, Chime, Simple, Stash and others.

Like many in this space, Current isn’t actually a bank — its banking services are provided by Choice Financial Group and Metropolitan Commercial Bank, which allows it to offer FDIC insurance up to $250,000. Instead, many of the banking apps focus instead on the feature set and user experience they can offer.

Both of Current’s products include a Visa co-branded debit card tied to the Current account. Along with the funding, Current and Visa are also announcing an expanded joint marketing partnership, which will help Current reach new customers.

“We believe everyone should have access to affordable financial services that improve the chances for a better life,” said Stuart Sopp, Current founder and CEO. “We have made this a reality through rebuilding financial infrastructure with the Current Core. It allows us to build more products that offer new ways to interact with money. Our rapid growth to half a million accounts serves as a testament to the ways our products and cost savings are bringing better financial outcomes and we anticipate bringing those benefits to over 1,000,000 customers by mid-2020.”

The company is planning to launch more features starting next year, including a cash-back system with brands and merchants in Q1, and further down the road, it’s considering things like a credit product and maybe Bitcoin investing. But this will require further education and careful attention to do well.

“It’s expensive to be poor — it really is,” he says. “If you don’t have much money, you’re paying 30% or 35% for your credit, whereas if you’re rich you’re paying 5%. So it’s like the world is inverted for you and it holds you down,” Sopp says. “So if we were to do [credit], we are going to do it right.”

In the near-term, the focus is on offering better budgeting tools and more ways for users to save money. This, Sopp argues, is what Current’s young users need most.

To date, Current has raised $45 million in funding.

Powered by WPeMatico

Fintech startup N26 is opening an office, its fourth, in Vienna. Eventually, the company plans to hire 300 software engineers, product managers and IT specialists.

N26 is building a mobile bank and has managed to attract 2.5 million users over the past few years. It raised a $300 million round back in January.

This is interesting news, as the company says that the new tech hub will focus on security, in particular detecting fraudulent activity. N26 plans to use artificial intelligence to develop a sort of real-time risk scoring system. The company will compare card transactions with your smartphone location, as well.

Multiple articles have highlighted a handful of cases of fraud in recent weeks. Customers tried to use N26 for money-laundering purposes. It took some time before N26 reacted and closed those accounts.

Every bank suffers from this kind of issue. In France, BNP Paribas, Société Générale, Crédit Agricole and Crédit Mutuel have all been fined in the past, for instance. But it’s interesting to see how N26 is reacting to those risks.

N26 has experienced tremendous growth, and the startup wants to scale its workforce appropriately so that it’s not short-staffed when faced with those issues. Similarly, it creates challenges when it comes to customer support and average response time.

It’s in the company’s best interest to follow strict rules when it comes to fraudulent activity — as a company with a banking license, N26 is regularly audited. N26 sent me the following statement a couple of weeks ago regarding audits:

N26, as all licensed banks, is subject to regular internal and external independent audits, including those by regulatory bodies such as BaFin, the German Financial Authority. Since we have a German bank license, we’re supervised by BaFin and audited on a regular basis. Any findings are promptly reviewed, implemented and monitored in coordination with the BaFin. We strive to meet all requirements consistently and take any required measures as quickly as possible.

As a bank it is imperative to continuously evaluate and improve all our structures, safety measures and service. We continuously invest in our security systems, customer support, and in hiring the right talent. To ensure we have the right talent to handle our responsibilities as a bank, we’ve increased our company size to more than 1,000 employees. The number of employees in customer service alone has tripled in the last year, and we will continue to grow across all departments to ensure regulatory compliance and serve our customers in the best way.

That’s why today’s news makes a ton of sense. There are already hundreds of people working for N26 in Berlin. Opening a new office in Vienna is a way to reach a new talent pool and make sure N26 is at least as secure as a traditional bank.

The team in Vienna will also work on shared Spaces and peer-to-peer payment improvements so you can create sub-accounts and share them with other N26 users. The startup also launched local IBANs for new users in Spain today. The company currently has offices in Berlin, Barcelona and New York.

Powered by WPeMatico

San Francisco-based mobile banking startup Chime announced this morning it has raised an additional $200 million in Series D financing led by DST Global, valuing its business at $1.5 billion. The oversubscribed round also included participation from new investors Coatue, General Atlantic, ICONIQ Capital and Dragoneer Investment Group, along with existing investors Menlo Ventures, Forerunner Ventures, Cathay Innovation and others.

To date, Chime has raised approximately $300 million, including last year’s $70 million Series C, which then saw the company valued at $500 million.

With the new funding, Chime has now raised the most funding and has the highest valuation among other U.S. challenger banks.

The company is now one of several going after a younger, millennial audience who no longer sees the need for banks with physical branches, and who are sick of being nickel-and-dimed by bigger banks’ numerous fees. Like others in this space, Chime offers a “no fees” bank account, which won’t penalize users for things like dropping below a minimum balance or even overdrafts.

On top of this is a modern-day banking app with features that make it look like it was actually built by a technology company — not a traditional bank. That’s because its team’s background is a mix of both tech and finance. Chime’s co-founder and CEO Chris Britt previously worked at Flycast, was an early comScore employee and worked at Visa and Green Dot; co-founder and CTO Ryan King spent time at Plaxo and Comcast before Chime.

Chime also includes a couple of innovative features that help differentiate it from the other mobile banking apps on the market. This includes an automatic savings feature that rounds up purchases to pocket the change; another feature that automatically saves 10 percent of your paycheck into Chime’s savings account; and one that offers a no-fee paycheck advance that makes your money available sooner.

To date, customers have opened more than 3 million FDIC-insured bank accounts on Chime, which makes it the largest brand in its category, the company claims. (This appears to be true. SoFi had 500,000 members as of last year. Simple doesn’t disclose its account base beyond “hundreds of thousands.” Moven and Varo Money are smaller, according to American Banker’s round-up.)

Its size, scale and growth trajectory, perhaps, have aided Chime in poaching a few execs from its other fintech businesses — including rivals. For example, the company recently added Chime VP, Risk Brian Mullins, who was the former head of Risk Ops at Square; and Chime GM, Lending Aaron Plante, who was the former Business Unit leader for Student Loans at SoFi.

The company says it plans to use the new investment to continue to accelerate growth and launch new products, including those in lending and credit. It also plans to double its San Francisco-based team to more than 200 employees and expand its leadership.

“We’re excited to welcome some of the world’s leading growth investors to Chime,” said Britt in a statement about the funding. “Banking should be free, helpful and easy to use but traditional banks are reluctant to embrace this reality. We aim to set a new standard in the industry by using technology to create services that are truly aligned with the best interests of consumers.”

Powered by WPeMatico

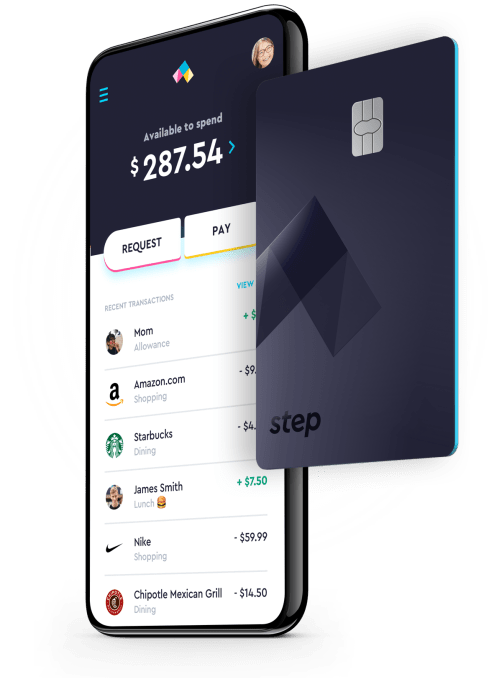

A new mobile banking startup called Step wants to help bring teenagers and other young adults into the cashless era. Today, cash is used less often, as more consumers shop online and send money to one another through payment apps like Venmo. But teenagers in particular are still heavily burdened with cash — even though they, too, want to spend their money on things that require a payment card, like Amazon.com purchases or mobile gaming, for example.

That’s where Step comes in.

The company aims to address the needs of what it believes is an underserved market in mobile banking — the 75 million children and young adults under the age of 21 in the U.S., who are still being forced to use cash.

This market isn’t the “unbanked,” it’s the “pre-banked,” explains Step CEO CJ MacDonald, whose previous startup, mobile gift card platform Gyft, sold to First Data several years ago.

Above: Step CEO, CJ MacDonald

“We’re building an all-in-one banking solution that primarily focuses on teens and parents,” he says. “We want it to be a teen’s first bank account. We want to be a teen’s first spending card. And we want to teach financial literacy and responsibility firsthand.”

MacDonald, along with CTO Alexey Kalinichenko, previously of Square and financial services startup Token, founded Step in May 2018. The 10-person team also includes several prior Gyft employees.

Last summer, Step closed on $3.8 million in seed funding from Sesame Ventures, Crosslink Capital and Collaborative Fund. Crosslink general partner Eric Chin sits on the board.

While there are a number of mobile banking apps out there today — like Chime, Monzo, Simple, Revolut and others — Step will specifically target teens, 13 and up, and other young adults with its marketing. Teens under 18 still need parents’ approval to sign up, of course. But the goal is to encourage the teens to bring the idea to their parents — not the other way around.

Step’s focus on this younger demographic puts it in a different space, where there are fewer competitors. Its more direct rivals are not the bigger mobile banks, but rather startups like teen debit card and bank app Current, or the parent-managed debit card for kids from Greenlight.

Step’s focus on this younger demographic puts it in a different space, where there are fewer competitors. Its more direct rivals are not the bigger mobile banks, but rather startups like teen debit card and bank app Current, or the parent-managed debit card for kids from Greenlight.

The mobile banking service Step provides will also aim to be more comprehensive than just a debit card. It will offer a combination of checking, savings and a Visa card that works as both credit and debit.

The card includes Visa’s Zero Liability Protection on all purchases from unauthorized use, and allows parents to set spending limits.

Parents will also be able to connect their own bank accounts to Step to instantly transfer in funds, which can then be distributed to kids’ accounts for things like allowances and chores, or other everyday spending needs. Step’s bank account itself is backed by Evolve Bank, so it’s FDIC-insured up to $250,000.

Unlike Current, which charges a subscription to use its service, Step aims to be a fee-free bank for consumers. Users don’t have to pay for their account, and there are no fees for things like overdrafts. Instead, Step’s plan is to generate revenue through traditional means — like interchange fees and by way of lending practices, once it has established a deposit base.

The company pays a 2.5 percent interest rate on deposits, offers a round-up savings feature and a range of budgeting tools and supports free instant transfers between Step accounts. It also provides access to a network of 35,000 ATMs with no fees.

The company pays a 2.5 percent interest rate on deposits, offers a round-up savings feature and a range of budgeting tools and supports free instant transfers between Step accounts. It also provides access to a network of 35,000 ATMs with no fees.

Beyond simply facilitating mobile banking, Step’s bigger goal is to teach teens to become financially responsible.

“Schools do not teach kids about money. A lot of families don’t talk about money. And it’s a crucial life skill that’s not really addressed properly when people are growing up,” says MacDonald, who says he was lacking in life skills in this area, even as a young college grad.

“There were ‘Money 101’ skills that I had not learned — that no one had talked to me about. Things like building credit, how many credit cards you should have, debt to income ratio,” he continues. “A lot of people get released into the real world without experience [in those areas],” he says.

Long-term, after solving the needs associated with everyday banking transactions, Step wants to layer on other products and services — like tools that allow a family to save together for college, for example.

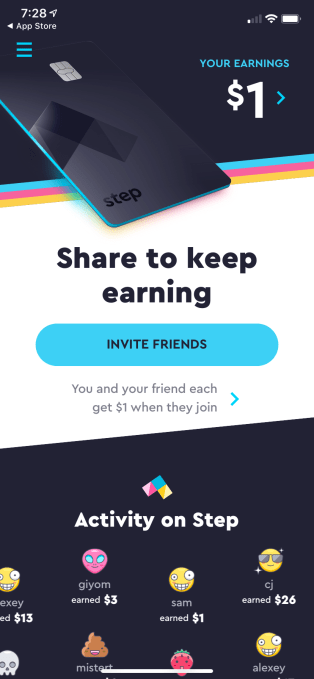

The company is launching the banking service under an invite-only system to scale up.

Today, it’s opening a waitlist and referral program. When you invite a friend, you each receive one dollar. Access will then be rolled out on a first-come, first-serve basis this spring. Users can join Step through the website, iOS or Android application.

Powered by WPeMatico

Revolut is merging traditional banking and cryptocurrency to let you buy, sell, trade, and hold Bitcoin, Litecoin, and Ether alongside 25 world fiat currencies. The $90 million-funded mobile banking startup is trying to erase the divide between old and new money. Revolut‘s CEO Nikolay Storonsky announced on stage today at TechCrunch’s Disrupt Berlin conference that… Read More

Revolut is merging traditional banking and cryptocurrency to let you buy, sell, trade, and hold Bitcoin, Litecoin, and Ether alongside 25 world fiat currencies. The $90 million-funded mobile banking startup is trying to erase the divide between old and new money. Revolut‘s CEO Nikolay Storonsky announced on stage today at TechCrunch’s Disrupt Berlin conference that… Read More

Powered by WPeMatico

Monzo, one of a number of “challenger” banks in the U.K. aiming to re-invent the current account, continues to be on a roll, both in terms of user numbers and now a significant new funding round.

Monzo, one of a number of “challenger” banks in the U.K. aiming to re-invent the current account, continues to be on a roll, both in terms of user numbers and now a significant new funding round.