Midwest

Auto Added by WPeMatico

Auto Added by WPeMatico

Bright Cellars, a six-year-old subscription-based wine seller has, like many upstarts, evolved over time. While it once sent its club members third-party wines that fit their particular profiles, Milwaukee, Wisconsin-based Bright Cellars says it’s now amassing enough data about its customers that it no longer sells wines made by other brands. Instead, while some of its “original” offerings are admittedly sold by other labels under different names, it is increasingly finding success by directing its winemaker partners to tweak the recipe, so to speak.

“We’re optimizing wine like you might optimize a more digital product,” says co-founder and CEO, Richard Yau, a San Francisco native whose startup entered into a regional accelerator program early on and stayed, though the company is now largely decentralized.

We talked earlier today with Yau about that shift, which investors are supporting with $11.2 million in Series B funding, led by Cleveland Avenue, with participation from earlier backers Revolution Ventures and Northwestern Mutual. (The company has now raised roughly $20 million altogether).

Yau also talked about industry trends that he’s seeing because of all that data collection.

TC: You’re building a portfolio of wines. What does that mean?

RY: We don’t own any land. We’re working primarily with suppliers [as do big companies like Gallo and Constellation], but at a larger scale than before, so we now get to shape what wines taste like and look like, and we can optimize across variables like how sweet should this wine be? How acidic? What do we want its color and brand and label to look like and which segment of our customers will really enjoy this wine the most?

TC: What’s one of your concoctions?

RY: We have a sparkling wine that’s produced in the Champagne method — not a Champagne wine; it’s a domestic wine — using grape varietals that no one uses for sparkling wine, and it’s one of the top-rated wines on our platform. Sparkling wine has been really good for us.

TC: How many subscribers do you have?

RY: We can’t share that, but we saw an acceleration in not just new subscribers throughout the pandemic but also in terms of seeing a larger share of [customers’] wallets going to D2C, and that impacted us pretty positively. Even as things eased up over the summer, we saw that people were cooking and eating at home more [and drinking wine].

TC: What’s the average price of a bottle of wine on the platform?

RY: $20 to $25.

TC: Where are your grape suppliers?

RY: A lot are on the West Coast, in Washington and California, but we also have grape suppliers internationally, including in South America and Europe.

TC: How many wines do you offer, and how long do you trial a wine?

RY: We’ve tested around 600, and at any given time, we’ll have 40 to 50 wines on the platform. We don’t stock everything forever; those that don’t do as well, we basically eliminate.

TC: A lot of D2C brands eventually branch into real-world locations. You aren’t doing that. Why not?

RY: It’s possible that we might at some point, but we like being D2C and it makes a lot of sense in a world where our members now work from home and are home to receive packages. It lines up with e-commerce trends in general. If you’re not buying your groceries at the store anymore, you aren’t buying wines at the store, either.

TC: From where are these bottles shipped?

RY: From a variety of places, but primarily from Santa Rosa [in the Bay Area].

TC: Have you seen the impact the weather is having on California winemakers, some of whom are now spraying sunscreen on their grapes to protect them?

RY: [Climate change] has certainly affected the wine industry. One of the fortunate things about us is we have flexibility in the suppliers we’re working with, so from a business-health perspective, we haven’t been as affected by that. Because a lot of our operations are in California, we did a couple of years ago have some interruptions with distribution where we weren’t able to ship some days; we were also impacted by warm temperatures. But fortunately, so far for this year, we haven’t had any operational or supply-chain disruptions.

TC: Have you been approached by one of legacy firms about a partnership or acquisition?

RY: We’ve had conversations, more in terms of partnerships because we have lots of data and can help them. For example, we can launch a new wine and get feedback almost like a focus group to figure out who likes what. We can split test two different blends for a wine and figure out which does better. That’s where conversations with legacy wine companies have happened.

TC: So they’d pay you for your data.

RY: We’re not opposed to selling data in the future, but we’ve approached it more like, here’s an opportunity to learn about how innovation works at a larger wine company. We don’t expect to be able to do what Constellation does well — with its large salesforce and distributors in every state — but what we can do in a complementary way is understand the consumer.

TC: What have you learned that might surprise outsiders?

RY: Petite sirah [offerings] do as well, if not better than, cabernet and pinot noir on the platform. Cab and pinot are fully 50 times the market size of petite sirah, but we see that our members really like it.

People also like merlot a lot more than they think — pretty much across all demographics. People like to hate merlot, but when we look at red blends that do well . . .

TC: What do people have against merlot?

RY: [Laughs.] Have you ever seen “Sideways?” That has something to do with it, still. Meanwhile, pinot noir remains popular, but people don’t like it as much as [other wine sellers] think.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Startups in the Midwest are optimistic despite the fact that a fair number of companies in the region are suffering from economic impacts stemming from COVID-19, recently collected data shows.

The global pandemic has shaken the U.S. economy, but it hasn’t affected each area in the same way. States have seen differing levels of infection, paces of response, qualities of medical infrastructure and so on. What happens to Silicon Valley startups in the COVID-19 era, therefore, might not be exactly the same as what happens to Boston’s or Utah’s startup ecosystems (more on Boston here, Utah here).

A report out this month from Sandalphon Capital that digs into the reality, reaction and sentiment of the Midwest’s startup scene paints an interesting picture. While data collected from 197 startup CEOs from the region includes worrisome responses regarding fundraising and cash runways, it also reflects more optimism and green shoots than we anticipated.

This morning, let’s study a few key data points from the Chicago-based, early stage venture capital firm’s survey to better understand one of America’s most interesting, if least-covered, startup scenes.

The full survey — you can find Sandalphon’s summation and the link here — contains a wealth of data, but today we’re focusing on three things:

Powered by WPeMatico

There comes a time for many startup companies where they either realize they need to do a nationwide rollout, or they need to actively target buyers in the middle of the country. If you are a startup on either the East or the West Coasts, it’s worth thinking about how this market might present its own set of unique challenges, and how you plan to overcome them.

There are a lot of misconceptions about what some people call “flyover country,” and as a San Francisco native who spent two decades in New York, Washington DC, and Boston before moving to Pittsburgh, I can assure you they are almost all wrong. Without getting into specifics, the reality of “middle America” is that it’s the same as anywhere else.

Income, education, world view, and waistlines are all varied. It’s pretty accurate that San Francisco possesses a culture obsessed with fitness and entrepreneurship, but California isn’t necessarily all like that, and if you think it is, I encourage you to go to Bakersfield, the Central Valley, or Eureka sometime.

In addition, just because the stereotypes are wrong doesn’t mean there’s nothing different about doing business here. As you think about how to conduct your rollout, here are some things you should consider:

As with any market, research is key since it informs every other aspect of the rollout. Start by looking into who your competition is.

Since there are fewer VC-backed startups in middle America, and smaller companies tend to get less press, the research may be harder. However, there are some major universities that are actively putting money into their own Entrepreneurship programs and those spinoffs often do very well.

Powered by WPeMatico

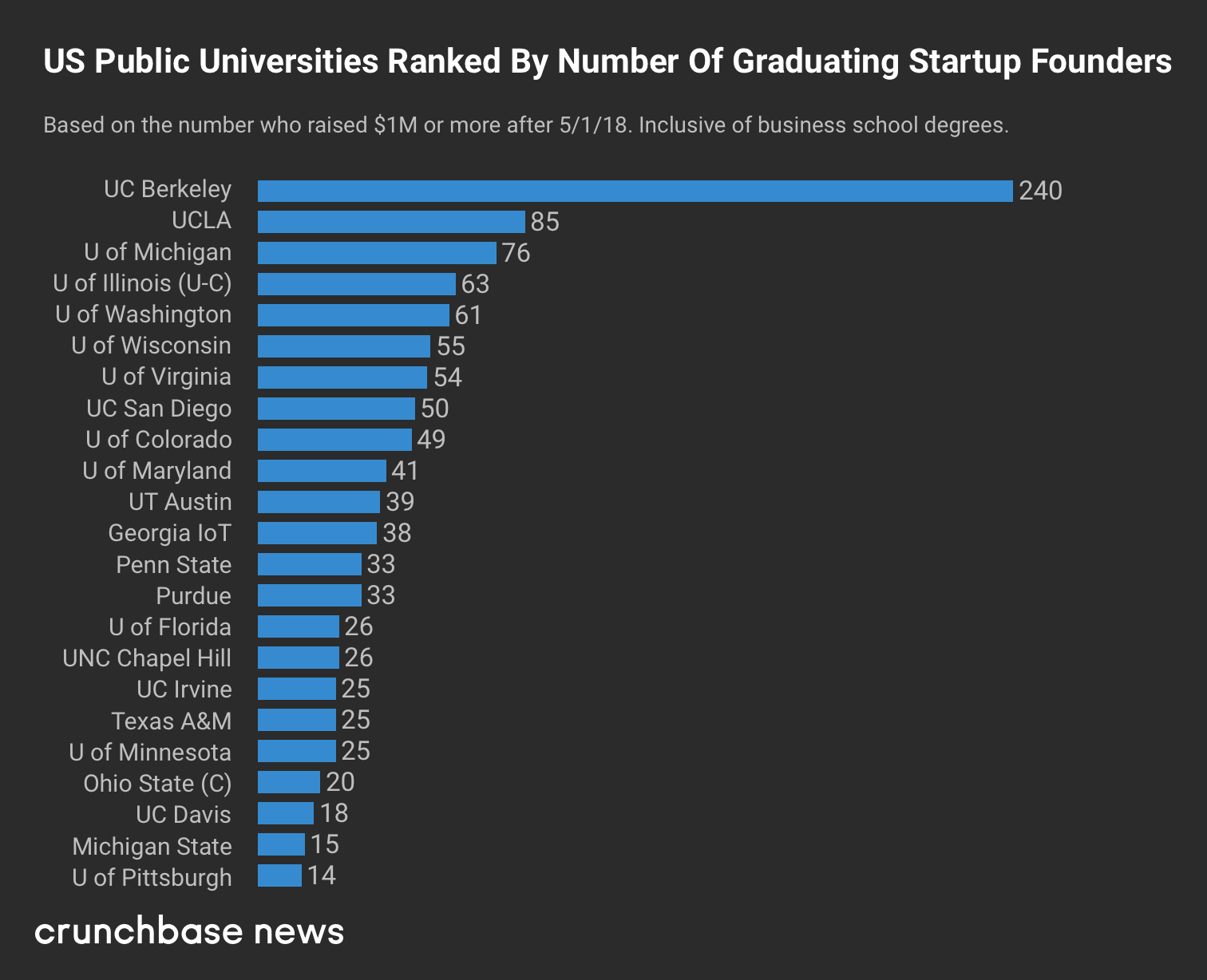

A lot of students attend public universities to lessen the financial burden of higher education. At last tally, tuition and fees at American public colleges and universities averaged around $6,800 a year, per the federal government. That’s far below the $32,600 mean price tag for private, nonprofit institutions.

Yet when it comes to public universities, the old adage “you get what you pay for” clearly does not apply. Leading public research universities in particular have a track record of turning out enviably knowledgeable and successful graduates. That includes a whole lot of funded startup founders.

And that leads us to our latest ranking. At Crunchbase News, we’ve been tracking the intersection of alumni affiliation and startup funding for the past few years. In a story published earlier this week, we looked at which U.S. universities graduated the most founders of startups that raised $1 million or more in roughly the past year.

For today’s follow-up, we’re focusing exclusively on public universities. Starting with a list of top-ranking research universities, we looked to see which have graduated the highest number of funded founders.

For the most part, we used the same criteria as the public-and-private list, focusing on startups that raised $1 million or more after May, 2018. The public list, however, does not separate out business school grads.

Without further ado, here’s the list:

Looking at the list above, a few things stand out. First, our top ranker, University of California at Berkeley, is multiples above the rest of the field when it comes to graduating funded founders.

Berkeley is a school that’s generally hard to get into, prominent in STEM and located in the VC-rich San Francisco Bay Area. So seeing it top the list isn’t necessarily surprising. However, the magnitude of its lead — with nearly three times the funded founders of runner-up UCLA — does warrant attention.

Big Midwestern schools also did well, with University of Michigan and University of Illinois, Urbana-Champaign nabbing the third and fourth spots.

More broadly, the list includes schools from all U.S. regions, including the East Coast, West Coast, South, Midwest and Southwest. So no particular region has a lock on graduating funded entrepreneurs. That’s also not surprising. But it’s good to have some more numbers to back up that notion.

Powered by WPeMatico