michigan

Auto Added by WPeMatico

Auto Added by WPeMatico

Accel announced Tuesday the close of three new funds totaling $3.05 billion, money that it will be using to back early-stage startups, as well as growth rounds for more mature companies. Notably, the 38-year-old Silicon Valley-based venture firm is doubling down on global investing.

The announcement underscores both the robust confidence investors continue to have for backing startups in the tech sector and the amount of money available to startups these days.

Specifically, today Accel is announcing its 15th early-stage U.S. fund at $650 million; its seventh early-stage European and Israeli fund also at $650 million and its sixth global growth stage fund at $1.75 billion. The latter fund is in addition, and designed to complement, a previously unannounced $2.3 billion global “Leaders” fund that is focused on later-stage investing that Accel closed in December.

Accel expects to invest in about 20 to 30 companies per fund on average, according to Partner Rich Wong. Its average investment in its growth fund will be in the $50 million to $75 million range, and $75 million and $100 million out of its global Leaders fund.

But the firm is also still eager and “excited” to incubate companies, Wong said.

“We’ll still write $500,000 to $1 million seed checks,” he told TechCrunch. “It’s important to us to work with companies from the very beginning and support them through their entire journey.”

Indeed, as TechCrunch recently reported, Accel has a history of backing companies that were previously bootstrapped (and often profitable) -– the latest example being Lower, a Columbus, Ohio-based fintech, which just raised a $100 million Series A.

Interestingly, Accel is often referred to some of these companies by existing portfolio companies (also in the case of Lower, whose CEO was referred to Accel by Galileo Clay Wilkes). More often than not, companies that Accel backs out of its early-stage and growth funds are bootstrapped and located outside of Silicon Valley.

The venture firm has long looked outside of Silicon Valley for opportunities, and has had offices not only in the Bay Area, but in London and Bangalore for years. Part of its investment thesis is to “invest early and locally,” according to Wong. Examples of this philosophy include investments in companies based all over the world — from Mexico to Stockholm to Tel Aviv to Munich.

Since the time of its last fund closure in 2019, the firm has seen 10 portfolio companies go public, including Slack, Austin-based Bumble, Bucharest-based UiPath, CrowdStrike, PagerDuty, Deliveroo and Squarespace, among others.

It also had 40 companies experience an M&A, including Utah-based Qualtrics’s $8 billion acquisition by SAP and Segment’s $3.2 billion acquisition by Twilio. Also, just last week, Rockwell Automation announced it was buying Michigan-based Plex Systems for $2.22 billion in cash. Accel first invested in Plex, which has developed a subscription-based smart manufacturing platform, in 2012.

Recent investments include a number of fintech companies such as LatAm’s Flink, Berlin-based Trade Republic, Unit and Robinhood rival Public. Accel has also backed as existing portfolio companies such as Webflow, a software company that helps businesses build no-code websites and events startup Hopin.

Wong says Accel is “open-minded but thematic” in its investment approach.

Accel Partner Sonali de Rycker, who is based out of London, agrees.

“For example, we’ll look at automation companies, consumer businesses and security companies, but at a global scale. Our goal is to find the best entrepreneurs regardless of where they are,” she said.

That has only been intensified by the recent rise of the smartphone and cloud, Wong said.

“Before, companies were mostly selling to the consumer in their own country,” he added. “But now the size of the market is so dramatically bigger, allowing them to become even larger, which is one of the reasons why I believe we’re seeing investment pace at this speed.”

To support this, it’s notable that Accel’s global Leaders fund is “dramatically” larger than the $500 million Leaders fund the firm closed in 2019.

Also, de Rycker points out, companies are staying private longer so the opportunity to invest in them until they sell or go public is greater.

Accel is also patient. In some cases, the firm’s investors will develop “years-long” relationships with companies they are courting.

“1Password is an example of this approach,” Wong said. “Arun [Mathew] had that relationship for at least six years before that investment was made. Finally, 1Password called and said ‘We’re ready, and we want you to do it.’ ”

And so Accel led the Canadian company’s first external round of funding in its 14-year history — a $200 million Series A — in 2019.

While the firm is open-minded, there are still some industries it has not yet embraced as much as others. For example, Wong said, “We’re not announcing a $2.2 billion crypto fund, but we have done crypto investments, and see some very interesting trends there. We’ll look at where crypto takes us.”

Powered by WPeMatico

Expensify may be the most ambitious software company ever to mostly abandon the Bay Area as the center of its operations.

Expensify may be the most ambitious software company ever to mostly abandon the Bay Area as the center of its operations.

The startup’s history is tied to places representative of San Francisco: The founding team worked out of Peet’s Coffee on Mission Street for a few months, then crashed at a penthouse lounge near the 4th and King Caltrain station, followed by a tiny office and then a slightly bigger one in the Flatiron building near Market Street.

Thirteen years later, Expensify still has an office a few blocks away on Kearny Street, but it’s no longer a San Francisco company or even a Silicon Valley firm. The company is truly global with employees across the world — and it did that before COVID-19 made remote working cool.

“Things got so much better when we stopped viewing ourselves as a Silicon Valley company. We basically said, no, we’re just a global company,” CEO David Barrett told TechCrunch. That globalism led to it opening a major office in — of all places —a small town in rural Michigan. That Ironwood expansion would eventually lead to a cultural makeover that would see the company broadly abandon its focus on the Bay Area, expanding from a headquarters in Portland to offices around the globe.

It makes sense that a company founded by internet pirates would let its workforce live anywhere they please and however they want to. Yet, how does it manage to make it all work well enough to reach $100 million in annual revenue with just a tad more than 100 employees?

As I described in Part 2 of this EC-1, that staffing efficiency is partly due to its culture and who it hires. It’s also because it has attracted top talent from across the world by giving them benefits like the option to work remotely all year as well as paying SF-level salaries even to those not based in the tech hub. It’s also got annual fully paid month-long “workcations” for every employee, their partner and kids.

Yet the real story is how a company can become untethered from its original geography, willing to adapt to new places and new cultures, and ultimately, give up the past while building the future.

Powered by WPeMatico

Coupa Software, a publicly traded company that helps large corporations manage spending, announced that it was buying Llamasoft, an 18-year-old Michigan company that helps large companies manage their supply chain. The deal was pegged at $1.5 billion.

This year Llamasoft released its latest tool, an AI-driven platform for managing supply chains intelligently. This capability in particular seemed to attract Coupa’s attention, as it was looking for a supply chain application to complement its spend management capabilities.

Coupa CEO and chairman Rob Bernshteyn says when you combine that supply chain data with Coupa’s spending data, it can produce a powerful combination.

“Llamasoft’s deep supply chain expertise and sophisticated data science and modeling capabilities, combined with the roughly $2 trillion of cumulative transactional spend data we have in Coupa, will empower businesses with the intelligence needed to pivot on a dime,” Bernshteyn said in a statement.

The purchase comes at a time when companies are focusing more and more on digitizing processes across enterprise, and when supply chains can be uncertain, depending on the location of COVID hotspots at any particular time.

“With demand uncertainty on one hand, and supply volatility on the other, companies are in need of supply chain technology that can help them assess alternatives and balance trade-offs to achieve desired business results. LLamasoft provides these capabilities with an AI-powered cloud platform that empowers companies to make smarter supply chain decisions, faster,” the company wrote in a statement.

Llamasoft was founded in 2002 in Ann Arbor, Michigan and has raised more than $56 million, according to Crunchbase data. Its largest raise was a $50 million Series B in 2015 led by Goldman Sachs .

The company generated more than $100 million in revenue and has 650 big customers, including Boeing, DHL, Kimberly-Clark and GM, according to company data.

Coupa has been extremely acquisitive over the years, buying 17 companies, according to Crunchbase data. This deal represents the fourth acquisition this year for the company. So far the stock market is not enamored with the acquisition; the company’s stock price is down 5.20% at publication.

Powered by WPeMatico

Companies that have leveraged technology to make the procurement and delivery of food more accessible to more people have been seeing a big surge of business this year, as millions of consumers are encouraged (or outright mandated, due to COVID-19) to socially distance or want to avoid the crowds of physical shopping and eating excursions.

Today, one of the companies that is supplying produce and other items both to consumers and other services that are in turn selling food and groceries to them, is announcing a new round of funding as it gears up to take its next step, an IPO.

GrubMarket, which provides a B2C platform for consumers to order produce and other food and home items for delivery, and a B2B service where it supplies grocery stores, meal-kit companies and other food tech startups with products that they resell, is today announcing that it has raised $60 million in a Series D round of funding.

Sources close to the company confirmed to TechCrunch that GrubMarket — which is profitable, and originally hadn’t planned to raise more than $20 million — has now doubled its valuation compared to its last round — sources tell us it is now between $400 million and $500 million.

The funding is coming from funds and accounts managed by BlackRock, Reimagined Ventures, Trinity Capital Investment, Celtic House Venture Partners, Marubeni Ventures, Sixty Degree Capital and Mojo Partners, alongside previous investors GGV Capital, WI Harper Group, Digital Garage, CentreGold Capital, Scrum Ventures and other unnamed participants. Past investors also included Y Combinator, where GrubMarket was part of the Winter 2015 cohort. For some context, GrubMarket last raised money in April 2019 — $28 million at a $228 million valuation, a source says.

Mike Xu, the founder and CEO, said that the plan remains for the company to go public (he’s talked about it before), but given that it’s not having trouble raising from private markets and is currently growing at 100% over last year, and the IPO market is less certain at the moment, he declined to put an exact timeline on when this might actually happen, although he was clear that this is where his focus is in the near future.

“The only success criteria of my startup career is whether GrubMarket can eventually make $100 billion of annual sales,” he said to me over both email and in a phone conversation. “To achieve this goal, I am willing to stay heads-down and hardworking every day until it is done, and it does not matter whether it will take me 15 years or 50 years.”

I don’t doubt that he means it. I’ll note that we had this call in the middle of the night his time in California, even after I asked multiple times if there wasn’t a more reasonable hour in the daytime for him to talk. (He insisted that he got his best work done at 4:30 a.m., a result of how a lot of the grocery business works.) Xu on the one hand is very gentle with a calm demeanor, but don’t let his quiet manner fool you. He also is focused and relentless in his work ethic.

When people talk today about buying food, alongside traditional grocery stores and other physical food markets, they increasingly talk about grocery delivery companies, restaurant delivery platforms, meal kit services and more that make or provide food to people by way of apps. GrubMarket has built itself as a profitable but quiet giant that underpins the fuel that helps companies in all of these categories by becoming one of the critical companies building bridges between food producers and those that interact with customers.

Its opportunity comes in the form of disruption and a gap in the market. Food production is not unlike shipping and other older, non-tech industries, with a lot of transactions couched in legacy processes: GrubMarket has built software that connects the different segments of the food supply chain in a faster and more efficient way, and then provides the logistics to help it run.

To be sure, it’s an area that would have evolved regardless of the world health situation, but the rise and growth of the coronavirus has definitely “helped” GrubMarket not just by creating more demand for delivered food, but by providing a way for those in the food supply chain to interact with less contact and more tech-fueled efficiency.

Sales of WholesaleWare, as the platform is called, Xu said, have seen more than 800% growth over the last year, now managing “several hundreds of millions of dollars of food wholesale activities” annually.

Underpinning its tech is the sheer size of the operation: economies of scale in action. The company is active in the San Francisco Bay Area, Los Angeles, San Diego, Seattle, Texas, Michigan, Boston and New York (and many places in between) and says that it currently operates some 21 warehouses nationwide. Xu describes GrubMarket as a “major food provider” in the Bay Area and the rest of California, with (as one example) more than 5 million pounds of frozen meat in its east San Francisco Bay warehouse.

Its customers include more than 500 grocery stores, 8,000 restaurants and 2,000 corporate offices, with familiar names like Whole Foods, Kroger, Albertson, Safeway, Sprouts Farmers Market, Raley’s Market, 99 Ranch Market, Blue Apron, Hello Fresh, Fresh Direct, Imperfect Foods, Misfit Market, Sun Basket and GoodEggs all on the list, with GrubMarket supplying them items that they resell directly, or use in creating their own products (like meal kits).

While much of GrubMarket’s growth has been — like a lot of its produce — organic, its profitability has helped it also grow inorganically. It has made some 15 acquisitions in the last two years, including Boston Organics and EJ Food Distributor this year.

It’s not to say that GrubMarket has not had growing pains. The company, Xu said, was like many others in the food delivery business — “overwhelmed” at the start of the pandemic in March and April of this year. “We had to limit our daily delivery volume in some regions, and put new customers on waiting lists.” Even so, the B2C business grew between 300% and 500% depending on the market. Xu said things calmed down by May and even as some B2B customers never came back after cities were locked down, as a category, B2B has largely recovered, he said.

Interestingly, the startup itself has taken a very proactive approach in order to limit its own workers’ and customers’ exposure to COVID-19, doing as much testing as it could — tests have been, as we all know, in very short supply — as well as a lot of social distancing and cleaning operations.

“There have been no mandates about masks, but we supplied them extensively,” he said.

So far it seems to have worked. Xu said the company has only found “a couple of employees” that were positive this year. In one case in April, a case was found not through a test (which it didn’t have, this happened in Michigan) but through a routine check and finding an employee showing symptoms, and its response was swift: the facilities were locked down for two weeks and sanitized, despite this happening in one of the busiest months in the history of the company (and the food supply sector overall).

That’s notable leadership at a time when it feels like a lot of leaders have failed us, which only helps to bolster the company’s strong growth.

Powered by WPeMatico

The Michigan startup scene is growing and venture capitalists see several key areas of opportunities. What follows is a survey of some of the top VCs in the state and how they see COVID-19 affecting the growth of Detroit, Ann Arbor and all of Michigan’s startup ecosystem. According to the Michigan Venture Capital Association (MVCA), there are 144 venture-backed startup companies in Michigan, which is an increase of 12% over the last five years.

The amount of capital available in the state hit a four-year high in 2019 after shrinking from record levels in 2015. The MVCA says the total amount of VC funds under management in Michigan is $4.3 billion. Out of that, 71% of the capital has been invested into companies and the MVCA states its members estimate an additional $1.2 billion of venture capital is needed to “adequately fund the growth of Michigan’s 144 startup companies in the next two years.”

As the VCs say below, life sciences is a large part of the Michigan ecosystem, attracting 38% of all investments made in the state. Information technology comes in second, receiving 34% of the total capital invested, with 85% going to those focused on software. Mobility, often thought as Michigan’s mainstay, only received 7% of the capital in 2019. Here’s who we spoke to:

Michigan has long been a hub for life science startups and the venture capitalists polled expect that to continue. Chris Stallman of Fontinalis Partners points to Michigan’s long-standing reputation in this field and expects this to continue.

Tim Streit of Grand Ventures agrees and sees the pandemic as accelerating the sector’s growth. In recent weeks he says his firm has seen a “number of promising digital therapeutics deals based in or near Michigan … and the timing couldn’t be more perfect for these kinds of companies to succeed.”

Chris Rizik of Renaissance Venture Capital notes that drug development will continue to drive growth around the country and is a strength of the Michigan ecosystem. He also points to Jeff Williams, CEO of NeuMoDx, as a leader in the life science community and who has led a number of Michigan’s most successful startups.

The notable exception to this are startups directly serving hospitals, according to Patricia Glaza of ID Ventures. She sees this as a challenging market in the era of COVID-19, saying “Hospitals are bleeding cash without elective surgeries and hard to prioritize nonessential technologies.”

Duo Security’s impressive exit to Cisco in 2018 is still resonating in the scene. As such, many venture capitalists are seeing Ann Arbor becoming a home for security startups.

Stallman of Fontinalis states, “I think the cybersecurity realm will be a bright spot as some of those spillover effects from the 2018 acquisition of Duo Security by Cisco take hold (this is still in its early days — employees will reach the end of their employment agreements and will start new companies, etc.).” Rizik of Renaissance Venture Capital said something similar: “The success of Duo Security highlighted Michigan’s growing reputation as a cybersecurity hub. The University of Michigan has always been strong in this area, and we now see a number of interesting startups in this field popping up around Ann Arbor.”

When asked about leaders in the Michigan startup scene, nearly all of the VCs listed Duo Security founders Dug Song and Jon Oberheide as key players. Perhaps Rizik said it best: “Dug Song is a great leader, who not only created a monster success for the region with Duo Security, but also has devoted much of his time to strategically working to help Michigan move forward as a responsible, startup-friendly community.”

Of course Michigan-based venture capitalists would be bullish on their own state, but nearly all of the VCs share the same reasons on why Michigan is a good place. They list low cost of living, amazing STEM-focused schools and a community of founders, VCs and business leaders eager to help each other.

Surprisingly, few of the VCs in the survey mention mobility or automotive as a highlight of the Michigan startup scene, which runs counter to the national narrative. Stallman sums up the situation this way: “The mobility space will see both headwinds and tailwinds. Companies vying for automotive customers may find that the industry’s challenges have resulted in a shorter ‘priority list’ for many automakers and suppliers; on the other side, companies helping to remove enterprise risk through innovation in supply chain, automation, workforce efficiency, etc. will have arguably more opportunity going forward.”

How much is local investing a focus for you now? If you are investing remotely in general now, are you filtering for local founders?

We have always been a thematically focused investor rather than a geographically focused investor; prior to COVID-19, we had invested 99% of our capital outside of Michigan. With that said, we’d love to invest more in Michigan and support more local founders.

What do you expect to happen to the startup climate in Detroit/Ann Arbor/Michigan longer term, with the shift to more remote work, possibly from more remote areas. Will it stay a tech hub?

Southeast Michigan has always been a story of two different startup worlds: health/life sciences and hardware/software tech. On the life sciences side, this region has a long-standing reputation of innovation and university research, and I expect that to remain largely the same going forward. It would seem to me that life sciences companies may not have as easy of a time adapting to new remote-work environments since much of the innovation work remains lab/clinic/facility-based.

For the world of other technology, I think there will certainly be more embracing of remote work and distributed teams — this area has always had some degree of that since it’s not uncommon to see companies with another office elsewhere or a few remote employees that come from very specific backgrounds that are hard to recruit for locally. Since this area has always had some of that, I could see a case that this new paradigm will be an easier adjustment for this region. However, the flip side of that is that so much of tech innovation and developing an ecosystem is about density and serendipitous collisions — for an area that was still on the come-up, losing what ground had been gained in recent years will no doubt make the spillover benefits of this aspect harder to come by. I worry a bit that angel and seed activity will slow locally (and hopefully that the growth in seed funds nationally will offset that).

Are there particular industry sectors that you expect to do uniquely well or poorly, locally?

I think a larger theme that is arising out of this COVID-19 situation is that people have a heightened sense of health, safety and security. Life sciences will remain resilient so long as there’s funding for continued research, and I think the cybersecurity realm will be a bright spot as some of those spillover effects from the 2018 acquisition of Duo Security by Cisco take hold (this is still in its early days — employees will reach the end of their employment agreements and will start new companies, etc.).

The mobility space will see both headwinds and tailwinds. Companies vying for automotive customers may find that the industry’s challenges have resulted in a shorter “priority list” for many automakers and suppliers; on the other side, companies helping to remove enterprise risk through innovation in supply chain, automation, workforce efficiency, etc. will have arguably more opportunity going forward.

In the short term, what challenges are facing Michigan’s startup scene?

Detroit has not yet hit a full critical mass from a startup ecosystem standpoint, and that is most evident in the more limited amount of angel and seed capital available to companies here; and, to a lesser extent, a more shallow pool of mentors and advisors for founders than what you would find in SF, LA, NYC, Boston, etc.

Who are some founders (who you’ve invested in or otherwise) that are leaders in the community?

Here are some of the prominent ones (note that we have invested in any): Dug Song and Jon Oberheide (Duo Security), Mina Sooch (has founded and led several prominent biotech companies), Amanda Lewan (Bamboo Detroit), Kyle Hoff (Floyd), Josh Luber and Greg Schwartz (StockX).

A lot of Bay Area founders and developers are looking to relocate. Why Michigan?

Quality research institutions, access to talent locally and ability to pull from Toronto/Ohio/etc., significant industry (automotive, logistics, manufacturing and financial services) in its footprint, supportive state programs for startups, cost of living, international airport with easy access (when the world moves again, that is), etc.

Powered by WPeMatico

Google, in collaboration with a number of academic leaders and its consulting partner SADA Systems, today announced the launch of the Open Usage Commons, a new organization that aims to help open-source projects manage their trademarks.

To be fair, at first glance, open-source trademarks may not sound like it would be a major problem (or even a really interesting topic), but there’s more here than meets the eye. As Google’s director of open source Chris DiBona told me, trademarks have increasingly become an issue for open-source projects, not necessarily because there have been legal issues around them, but because commercial entities that want to use the logo or name of an open-source project on their websites, for example, don’t have the reassurance that they are free to use those trademarks.

“One of the things that’s been rearing its ugly head over the last couple years has been trademarks,” he told me. “There’s not a lot of trademarks in open-source software in general, but particularly at Google, and frankly the higher tier, the more popular open-source projects, you see them more and more over the last five years. If you look at open-source licensing, they don’t treat trademarks at all the way they do copyright and patents, even Apache, which is my favorite license, they basically say, nope, not touching it, not our problem, you go talk.”

Traditionally, open-source licenses didn’t cover trademarks because there simply weren’t a lot of trademarks in the ecosystem to worry about. One of the exceptions here was Linux, a trademark that is now managed by the Linux Mark Institute on behalf of Linus Torvalds.

With that, commercial companies aren’t sure how to handle this situation and developers also don’t know how to respond to these companies when they ask them questions about their trademarks.

“What we wanted to do is give guidance around how you can share trademarks in the same way that you would share patents and copyright in an open-source license […],” DiBona explained. “And the idea is to basically provide that guidance, you know, provide that trademarks file, if you will, that you include in your source code.”

Google itself is putting three of its own open-source trademarks into this new organization: the Angular web application framework for mobile, the Gerrit code review tool and the Istio service mesh. “All three of them are kind of perfect for this sort of experiment because they’re under active development at Google, they have a trademark associated with them, they have logos and, in some cases, a mascot.”

One of those mascots is Diffi, the Kung Fu Code Review Cuckoo, because, as DiBona noted, “we were trying to come up with literally the worst mascot we could possibly come up with.” It’s now up to the Open Usage Commons to manage that trademark.

DiBona also noted that all three projects have third parties shipping products based on these projects (think Gerrit as a service).

Another thing DiBona stressed is that this is an independent organization. Besides himself, Jen Phillips, a senior engineering manager for open source at Google is also on the board. But the team also brought in SADA’s CTO Miles Ward (who was previously at Google); Allison Randal, the architect of the Parrot virtual machine and member of the board of directors of the Perl Foundation and OpenStack Foundation, among others; Charles Lee Isbell Jr., the dean of the Georgia Institute of Technology College of Computing, and Cliff Lampe, a professor at the School of Information at the University of Michigan and a “rising star,” as DiBona pointed out.

“These are people who really have the best interests of computer science at heart, which is why we’re doing this,” DiBona noted. “Because the thing about open source — people talk about it all the time in the context of business and all the rest. The reason I got into it is because through open source we could work with other people in this sort of fertile middle space and sort of know what the deal was.”

Update: even though Google argues that the Open Usage Commons are complementary to other open source organizations, the Cloud Native Computing Foundation (CNCF) released the following statement by Chris Aniszczyk, the CNCF’s CTO: “Our community members are perplexed that Google has chosen to not contribute the Istio project to the Cloud Native Computing Foundation (CNCF), but we are happy to help guide them to resubmit their old project proposal from 2017 at any time. In the end, our community remains focused on building and supporting our service mesh projects like Envoy, linkerd and interoperability efforts like the Service Mesh Interface (SMI). The CNCF will continue to be the center of gravity of cloud native and service mesh collaboration and innovation.”

Powered by WPeMatico

Michigan-based in-space propulsion startup Orbion is working with a major new partner: The U.S. Department of Defense (DOD). Orbion has secured a research contract from the U.S. Air Force Research Laboratory’s Propulsion Directorate, specifically aimed at helping the DOD “enhance resiliency of U.S. systems in space.”

Basically, it sounds like that will boil down to seeing how Orbion’s propulsion technology can be applied to DOD satellites when used in larger constellation form, to provide those satellites with the ability to move propulsively while in orbit, and to do so in a way that can scale cost-effectively. In a press release announcing the news, Orbion CEO Brad King says that volume is a strategy when it comes to fortifying U.S. systems in space against potential foreign attack.

“One way to increase the resilience of space systems is to improve our nation’s ability to build and deploy small satellites in large numbers at low costs,” said King in a statement, “Orbion is developing mass-production techniques to build propulsion systems for commercial customers. With this research contract we are investigating how or if our manufacturing processes must be modified to meet DOD requirements.”

It’s true that in the past, the U.S. and other international powers with access to space have mostly focused on large, expensive, singular pieces of orbital hardware as their strategic assets. Shifting to the small satellite constellation approach currently being pursued by a number of private companies definitely has advantages in terms of redundancy and replaceability.

Orbion’s entire business proposition as a startup is that it’s applying mass-production to in-space thrusters, which will bring down costs and make their technology accessible to a much wider range of potential clients, and practical for application in small satellite design. The DOD may not have the same budget-constraint issues as a cash-strapped satellite startup, but long-term cost savings that also comes with a tactical advantage is a hard bargain to pass up.

Powered by WPeMatico

Amazon will be stepping up its efforts to reduce its climate impact, CEO Jeff Bezos announced on Thursday. The company will be ordering 100,000 electric delivery trucks from Michigan’s Rivian as part of this commitment, Bezos said. The commerce giant will seek to meet its goal of becoming carbon-neutral by 2040 — 10 years earlier than is outlined by the United Nations Paris Agreement.

Bezos said at a National Press Club event in Washington where he made the announcement that the updated timeline is due to the increase in climate change, which has been more aggressive than even some of the more serious predictions had anticipated five years ago when the Paris agreement was reached.

Amazon’s overarching efforts to make the company carbon-neutral are bundled under a plan the company is calling the “Climate Pledge,” which will be open to other companies as well. In addition to efforts like the Rivian order for emission-free delivery vehicles, Amazon also will be seeking to reduce its footprint through other means, including solar energy and carbon offsets.

Rivian noted that this was the largest order to date of any electric delivery vehicles, and that they’d begin actually deploying for Amazon starting in 2021. Amazon led a $700 million investment round in Rivian in February, and the company announced a further $350 million from auto industry giant Cox Automotive earlier this month. Automaker Ford revealed a $500 million investment in Rivian in April, too.

Rivian also has plans to build and ship consumer vehicles, including the all-electric pickup truck and SUV it revealed late last year, which it aims to begin delivering to customers in 2020.

Powered by WPeMatico

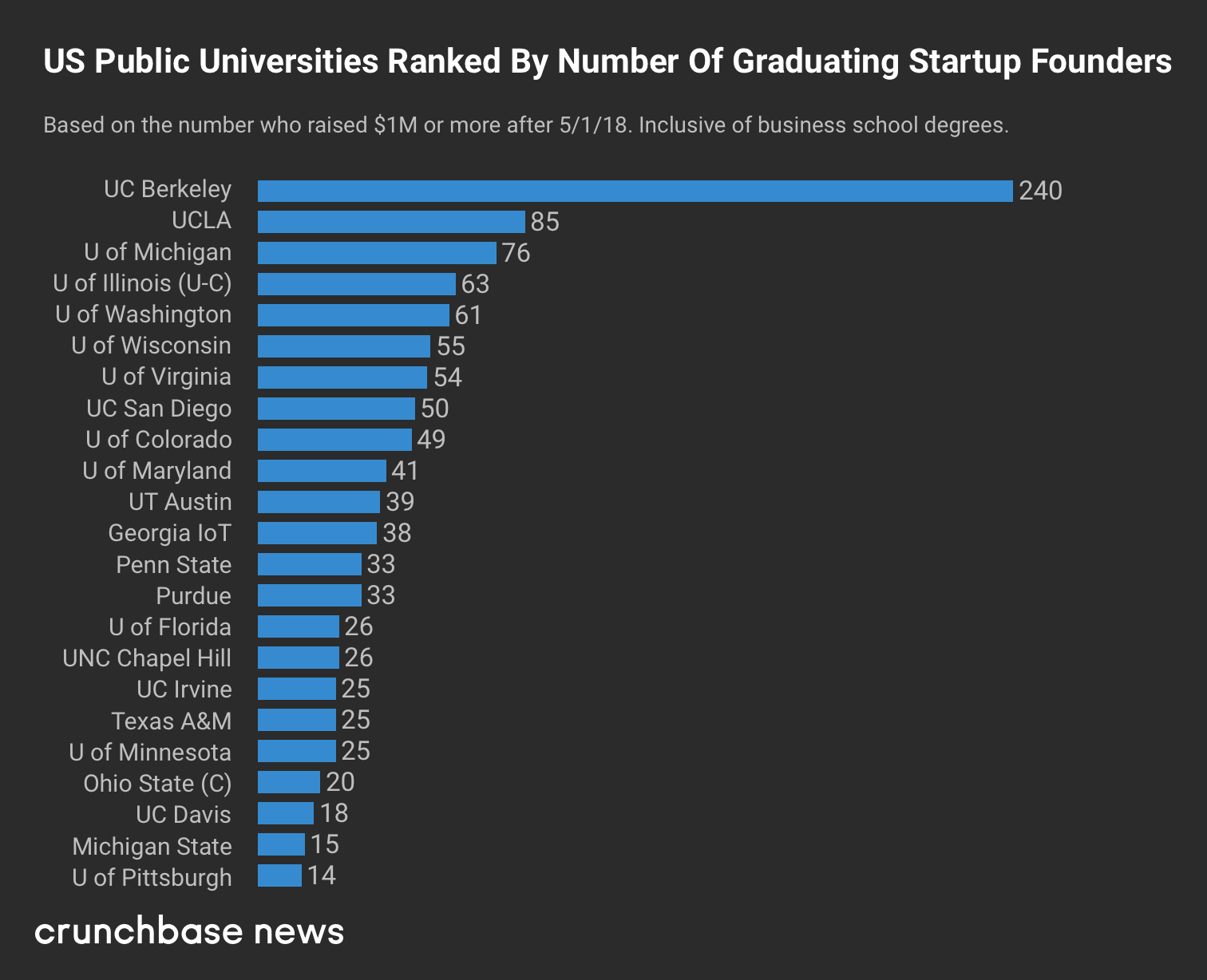

A lot of students attend public universities to lessen the financial burden of higher education. At last tally, tuition and fees at American public colleges and universities averaged around $6,800 a year, per the federal government. That’s far below the $32,600 mean price tag for private, nonprofit institutions.

Yet when it comes to public universities, the old adage “you get what you pay for” clearly does not apply. Leading public research universities in particular have a track record of turning out enviably knowledgeable and successful graduates. That includes a whole lot of funded startup founders.

And that leads us to our latest ranking. At Crunchbase News, we’ve been tracking the intersection of alumni affiliation and startup funding for the past few years. In a story published earlier this week, we looked at which U.S. universities graduated the most founders of startups that raised $1 million or more in roughly the past year.

For today’s follow-up, we’re focusing exclusively on public universities. Starting with a list of top-ranking research universities, we looked to see which have graduated the highest number of funded founders.

For the most part, we used the same criteria as the public-and-private list, focusing on startups that raised $1 million or more after May, 2018. The public list, however, does not separate out business school grads.

Without further ado, here’s the list:

Looking at the list above, a few things stand out. First, our top ranker, University of California at Berkeley, is multiples above the rest of the field when it comes to graduating funded founders.

Berkeley is a school that’s generally hard to get into, prominent in STEM and located in the VC-rich San Francisco Bay Area. So seeing it top the list isn’t necessarily surprising. However, the magnitude of its lead — with nearly three times the funded founders of runner-up UCLA — does warrant attention.

Big Midwestern schools also did well, with University of Michigan and University of Illinois, Urbana-Champaign nabbing the third and fourth spots.

More broadly, the list includes schools from all U.S. regions, including the East Coast, West Coast, South, Midwest and Southwest. So no particular region has a lock on graduating funded entrepreneurs. That’s also not surprising. But it’s good to have some more numbers to back up that notion.

Powered by WPeMatico

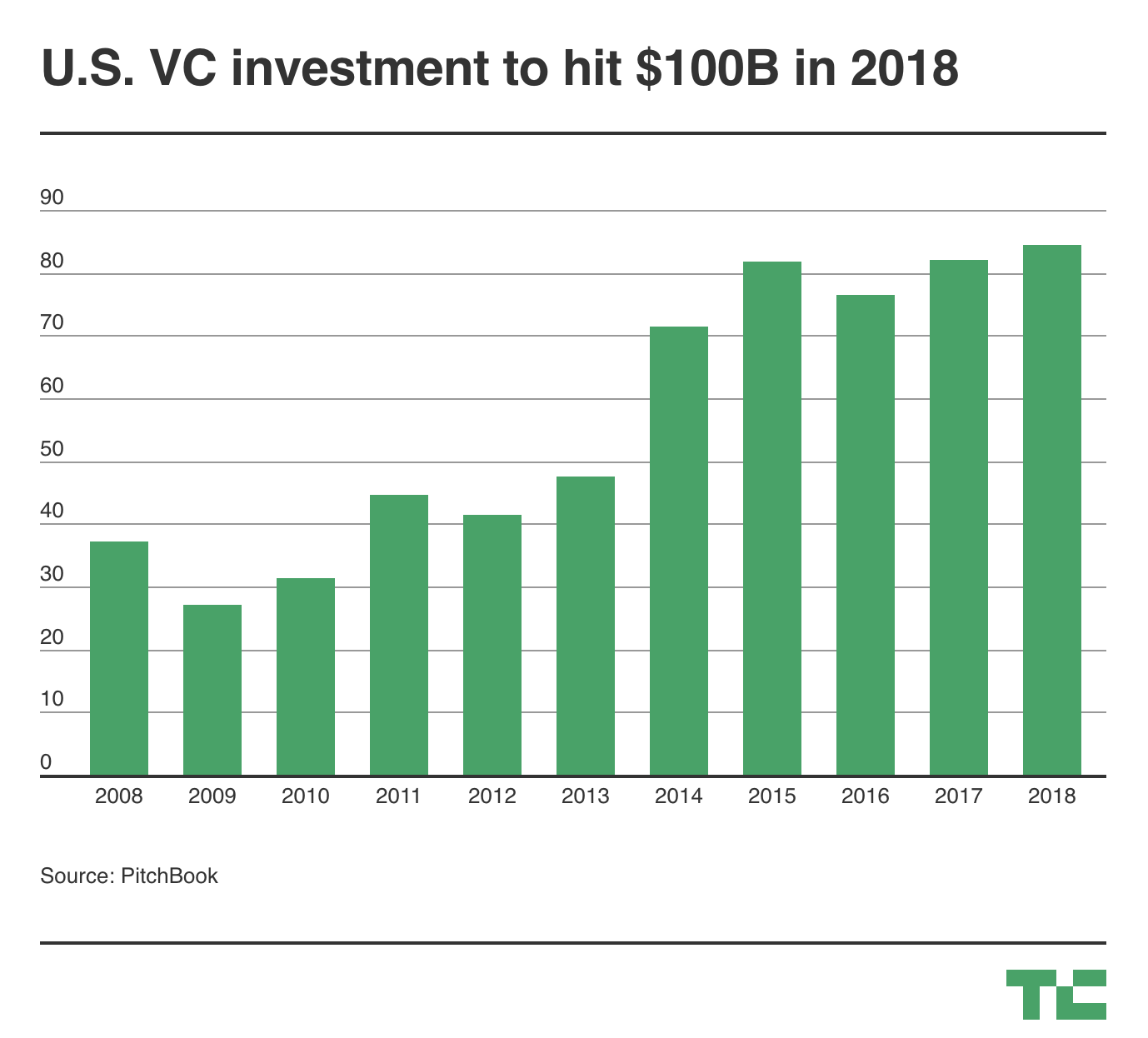

So many new unicorns valued at $1 billion-plus, countless $100 million venture financings, an explosion of giant funds — it’s no surprise 2018 is shaping up to be a banner year for venture capital investment in U.S.-based companies.

There are more than 2.5 months remaining in 2018 and already U.S. companies have raised $84.1 billion — more than all of 2017 — across 6,583 VC deals as of Sept. 30, 2018, according to data from PitchBook’s 3Q Venture Monitor.

Last year, companies raised $82 billion across more than 9,000 deals in what was similarly an impressive year for the industry. Many questioned whether the trend would — or could — continue this year, and oh, boy has it. VC investment has sprinted past decade-highs and shows no signs of slowing down.

Why the uptick? Fewer companies are raising money, but round sizes are swelling. Unicorns, for example, were responsible for about 25 percent of the capital dispersed in 2018. Those companies, which include Slack, Stripe and Lyft, have raised $19.2 billion so far this year — a record amount — up from $17.4 billion in 2017. There were 39 deals for unicorn companies valuing $7.96 billion in the third quarter of 2018 alone.

Some other interesting takeaways from PitchBook’s report on the U.S. venture ecosystem:

Powered by WPeMatico