menlo ventures

Auto Added by WPeMatico

Auto Added by WPeMatico

As the technologies that were once considered science fiction become the purview of science, the venture capital firms that were once investing at the industry’s fringes are now finding themselves at the heart of the technology industry.

Investing in the commercialization of technologies like genetic engineering, quantum computing, digital avatars, augmented reality, new human-computer interfaces, machine learning, autonomous vehicles, robots, and space travel that were once considered “frontier” investments are now front-and-center priorities for many venture capital firms and the limited partners that back them.

Earlier this month, Lux Capital raised $1.1 billion across two funds that invest in just these kinds of companies. “[Limited partners] are now more interested in frontier tech than ever before,” said Bilal Zuberi, a partner with the firm.

Lux Capital just closed on a whopping $1 billion in capital, doubling the amount of money it manages

He sees a few factors encouraging limited partners (the investors who provide financing for venture capital funds) to invest in the firms that are financing companies developing technologies that were once considered outside of the mainstream.

Powered by WPeMatico

Businesses need to understand cause and effect: Someone did X and it increased sales, or they did Y and it hurt sales. That’s why many of them turn to analytics — but Bilal Mahmood, co-founder and CEO of ClearBrain, said existing analytics platforms can’t answer that question accurately.

“Every analytics platform today is still based on a fundamental correlation model,” Mahmood said. It’s the classic correlation-versus-causation problem — you can use the data to suggest that an action and a result are related, but you can’t draw a direct cause-and-effect relationship.

That’s the problem that ClearBrain is trying to solve with its new “causal analytics” tool. As the company put it in a blog post, “Our goal was to automate this process [of running statistical studies] and build the first large-scale causal inference engine to allow growth teams to measure the causal effect of every action.”

You can read the post for (many) more details, but the gist is that Mahmood and his team claim they can draw accurate causal relationships where others can’t.

The idea is to use this in conjunction with A/B testing — customers look at the data to prioritize what to test next, and to make estimates about the impact of things that can’t be tested. Otherwise, Mahmood said, “If you wanted to measure the actual impact of every variable on your website and your app — the actual impact it has on conversation — it could take you years.”

When I wrote about ClearBrain last year, it was using artificial intelligence to improve ad targeting, but Mahmood said the company built the new analytics technology in response to customer demand: “People didn’t just want to know who was going to convert, they wanted to know why, and what caused them to do so.”

The causal analytics tool is currently available to early access users, with plans for a full launch in October. Mahmood said there will be a number of pricing tiers, but they’ll be structured to make the product free for many startups.

In addition to launching the analytics tool in early access, ClearBrain also announced this week that it’s raised an additional $2 million in funding from Harrison Metal and Menlo Ventures.

Powered by WPeMatico

If you are among those who thought that the scooter market sounded a little overhyped and overcrowded, we’ve gotten wind of a deal that could point to some impending consolidation. The on-demand scooter business Bird has agreed to acquire Scoot, a smaller two-wheeled mobility startup, sources tell TechCrunch.

The stage of the negotiations is not clear although from what our sources tell us, it sounds like the deal is not closed. Contacted for a response, both Scoot and Bird said they declined to comment on speculation.

If accurate, it would be far from a merger of equals. Scoot was last valued at around $71 million, having raised about $47 million in equity funding to date from Scout Ventures, Vision Ridge Partners, angel investor Joanne Wilson and more.

Bird is significantly larger. Led by chief executive officer Travis VanderZanden, earlier this year the company was working on a round of financing reportedly worth $300 million at a $2.3 billion valuation. We’ve been able to confirm that this round has now closed, although we don’t yet know the final amount or who the investors are. (Backers of Bird include Sequoia, Index, Charles River Ventures, Tusk Ventures, Upfront Ventures and dozens more.) Scoot would be Bird’s first full acquisition.

It’s still very early days in the scooter market in terms of consumer adoption, but that hasn’t stopped people from launching a lot of startups and raising funding to capitalise on what many believe will be a big opportunity longer term.

That promise is made bigger by the regulatory structure of the scooter market. Similar to their approach to bikes, many cities restrict the number of licenses they give out to companies to run on-street, hourly scooter services. Winning a license can give a company a near-monopoly on building a business in that city.

It also means that a combination between two companies whose geographic footprints do not overlap becomes a much cheaper and faster way of instantly creating a bigger business.

Notably, Scoot has a license to operate a pick-up/drop-off street service in the key market of San Francisco — where it competes with Skip, the only other licensed operator in the city. (Note: Bird last month did start up business again in SF, but only for the less popular offer of monthly rentals.)

What’s more, the two startups do not have any overlap in the rest of their footprints. Scoot is active in Barcelona, Spain and Santiago, Chile. Bird, on the other hand, has launched in about 100 cities spanning the U.S. and Europe, but its list does not include any of the cities where Scoot has rolled out its service.

Bird announced its new, two-seated electric vehicle earlier this week

On the vehicle front, the story is a little different. The two are providing, more or less, the same kinds of vehicles. Scoot has built out a network focused primarily on electric push scooters, seated scooters and electric bikes. Bird, meanwhile, has mostly built its service around electric push scooters, but just yesterday the company debuted its first seated vehicle to expand into a new product class.

Bird acquiring Scoot will help the two achieve better economies of scale in terms of vehicle purchasing power and device R&D.

It also helps them compete against the big boys. The market for scooters and other two-wheeled vehicles (collectively termed “micro-mobility”) is still a relatively new one, but Lyft and Uber have also waded in early to establish market share, as part of their own strategies to position themselves as the go-to platforms for any and all transportation needs.

Bird buying Scoot is one likely M&A move, but it’s not the only one.

Sources have told TechCrunch that an Uber acquisition of Skip (the other provider in SF) could also be in the works. Skip, much like Scoot, is another small player in the e-scooter market. To date, it has secured $31 million in venture capital funding from Initialized Capital, Accel and others.

Uber is already an active acquirer in the area of mico-mobility. If you remember, it acquired JUMP Bikes for $200 million in April 2018.

Uber’s acquisition of JUMP wasn’t surprising. In January 2018, the ride-hailing giant partnered with JUMP to launch Uber Bike, which lets Uber riders book JUMP bikes via the Uber app.

Other acquisitions in the nascent micro-mobility space include Lyft’s purchase of Motivate, a deal announced roughly one year ago. Motivate, the oldest and largest electric bike-share company in North America, did not disclose terms of the deal, though reports indicated it was asking for at least $250 million.

Bird — founded in 2017 — has yet to announce any acquisitions, although a spokesperson for the company said there have been quiet acqui-hires before now.

It was itself the subject of acquisition rumors for several months in 2018, too. Prior to Uber filing to go public in what was one of the most highly anticipated initial public offerings of the decade, many expected it to shell out cash for either Bird or Lime. From what we know, Uber was in discussions to acquire Bird, but ultimately it wasn’t able to meet Bird’s steep asking price.

Powered by WPeMatico

Greetings from Seattle, the land of Amazon, Microsoft, two of the world’s richest men and some startups.

I’m always surprised the Seattle startup ecosystem hasn’t grown to compete with the likes of Silicon Valley — or at least Boston and New York City — since the dot-com boom. Today, it’s the strongest it’s been due to the successes of companies like the newly minted unicorn Outreach, trucking business Convoy and, of course, the dog walking startup Rover. But the city still lags behind, failing to adopt the culture of entrepreneurship that defines San Francisco.

I spent a lot of time wondering why it hasn’t reached its full potential. Is it because Microsoft and Amazon pay their employees so well they don’t have the same urge to build something from the ground up? Is it a lack of access to capital? Is the city not attracting top talent? If you have thoughts, send them my way.

“We think part of the issue is a lack of capital and a lack of help,” Rover and Pioneer Square Labs co-founder Greg Gottesman told TechCrunch earlier this year. “If we can provide a little bit of both of those things, we can really put Seattle where it deserves to be, should be and will be.”

Despite its shortcomings, there is still some action in the city I want to highlight this week. A same-day delivery business, Dolly, is on the rise. The startup told me on Thursday it had raised a $7.5 million round from Unlock Venture Partners, Maveron and Jeff Wilke, the chief executive officer of Amazon Worldwide Consumer. Maveron, if you remember, is the VC fund co-founded by Starbucks founder Howard Schultz.

In other Seattle news, Madrona Venture Group, a well-regarded fund, raised an additional $100 million this week. Typically, Madrona focuses on companies based in the Pacific Northwest, but this fund will deploy capital throughout the entire U.S. Hmmm, that’s not necessarily a good sign for Seattle founders, but great progress for the ecosystem nonetheless.

If you’re interested in learning more about Seattle tech, I’ve covered it a bit because it’s my hometown! Start with this story, which dives deep into a Seattle accelerator that’s working hard to encourage entrepreneurship in the city. Alright, on to other news.

Want more TechCrunch newsletters? Sign up here.

WeWork: The co-working giant now known as The We Company submitted confidential IPO documents to the SEC, the company confirmed in a press release Monday. Is this the next massive startup win or a house of cards waiting to be toppled by the glare of the public markets? TechCrunch’s Danny Crichton investigates.

Slack: The business is in its final steps toward a much-anticipated direct listing, with one source telling TechCrunch the listing will be complete within 45 days. The WSJ reported this week that Slack will make an online presentation to potential shareholders on May 13. This week, we dug deep into Slack’s S-1 and decided to evaluate just how well the tech press, us included, did in covering the company. For the most part, the tech press did decently well, except for one curious, $162 million gap.

Uber: Finally! That ride-hailing company is going public next week. That latest news? Uber co-founder Travis Kalanick won’t be ringing the opening bell. Uber would not be where it is today without Kalanick, but him being there would surely be a reminder of Uber’s rocky past.

Beyond Meat: Shares of the company surged up 135 percent in their market opener last week, valuing the company as high as $3.52 billion. Volatility was so high on the company’s stock that the Nasdaq had to pause trading of “BYND” shares.

Ofo has run into its fair share of issues, laying off hundreds of workers, shutting down its international division and more. Now, you can buy a piece of the startup’s history.

Now you can buy a piece of startup history… Ofo bikes for ~$60 https://t.co/LLJbDOXm0C

— Jon Russell (@jonrussell) April 29, 2019

In other micro-mobility news, Lyft’s head of scooter & bikes Liam O’Connor, who was hired to help transportation company Lyft build its bike and scooter operations, has left after seven months with the newly-public company. TechCrunch’s Ingrid Lunden has the scoop. Plus, Bird, the electric scooter unicorn doing its best to overcome regulatory barriers, has made its way back to San Francisco. Bird is using its business license in San Francisco to introduce monthly personal rentals in the city. The program enables people to rent a scooter for $24.99 a month with no cap on the number of rides. We’ll how that goes.

For some reason, people are giving Magic Leap more money. The company has secured another $280 million in a deal with Japan’s largest mobile operator, Docomo. Do you know what that means? The developer fo AR/VR headsets has raised a total of $2.6 billion. We’re just as confused as you.

Brand new venture capital funds:

Unshackled Ventures raised $20 million.

Exclusive: @UnshackledVC has a new $20M pre-seed fund to invest only in immigrants. Why? Because immigrants are “inherently more entrepreneurial:” https://t.co/ZLiZ1UczJV

— Kate Clark (@KateClarkTweets) May 2, 2019

Jungle Ventures closed on $175 million.

And Toyota AI Ventures launched a $100 million fund.

I have the inside story on Menlo Ventures early Uber stake and TechCrunch’s Connie Loizos goes deep with early Uber backer Bradley Tusk.

This week, we offer TechCrunch Extra Crunch subscribers exclusive tips on building extraordinary teams. Plus, the final piece in TechCrunch’s Greg Kumparak’s series on Niantic, the fast-growing developer of Pokemon Go. If you recall, we’ve captured much of Niantic’s ongoing story in the first three parts of our EC-1, from its beginnings as an “entrepreneurial lab” within Google, to its spin-out as an independent company and the launch of Pokémon GO, to its ongoing focus on becoming a platform for others to build augmented reality products upon.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and TechCrunch’s Danny Crichton chat about updates at the Vision Fund, Cheddar’s big exit and more of this week’s headlines.

Powered by WPeMatico

Menlo Ventures was founded in 1976 but it took 35 years for the venture capital firm to hit the jackpot.

Since the dot-com boom, Menlo Ventures has teetered between good and great. A prolific Silicon Valley investor, it’s never quite reached the heights of Accel or Andreessen Horowitz (a16z), or established the level of name recognition as Benchmark or Sequoia, firms that struck gold with bets on Facebook, Instagram and Snap.

But where others missed the boat entirely on one of the most valuable tech startups of all time, Menlo Ventures gnawed its way into an early deal at the last possible moment.

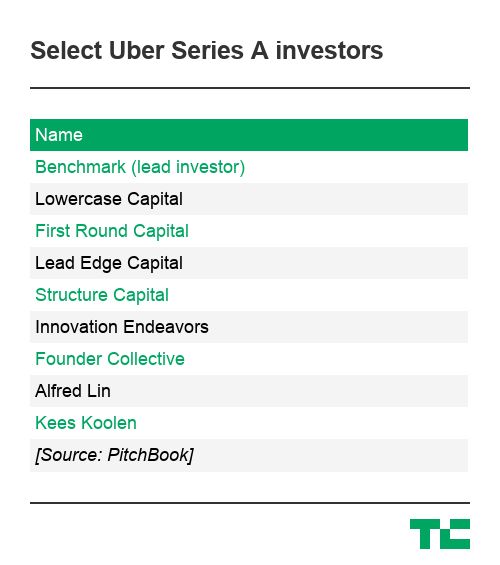

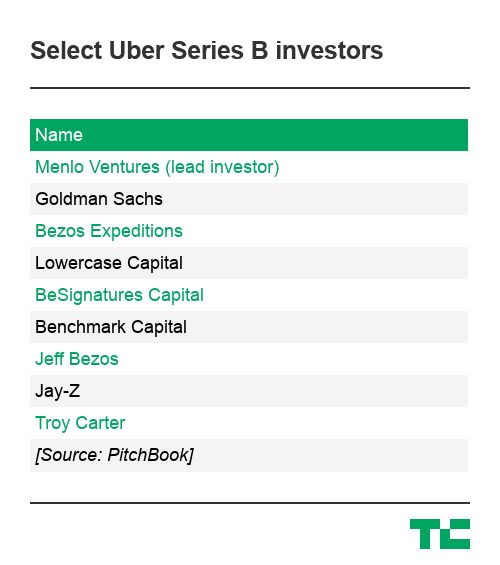

In 2011, the firm led a $32 million Series B funding in a fledgling on-demand car service called Uber, agreeing to value the startup at a colossal $322 million after the company’s first-choice investor, a16z, failed to accept Uber’s sky-high terms. Menlo would go on to invest a total of $66.5 million in the company on expected total returns of up to $3.1 billion.

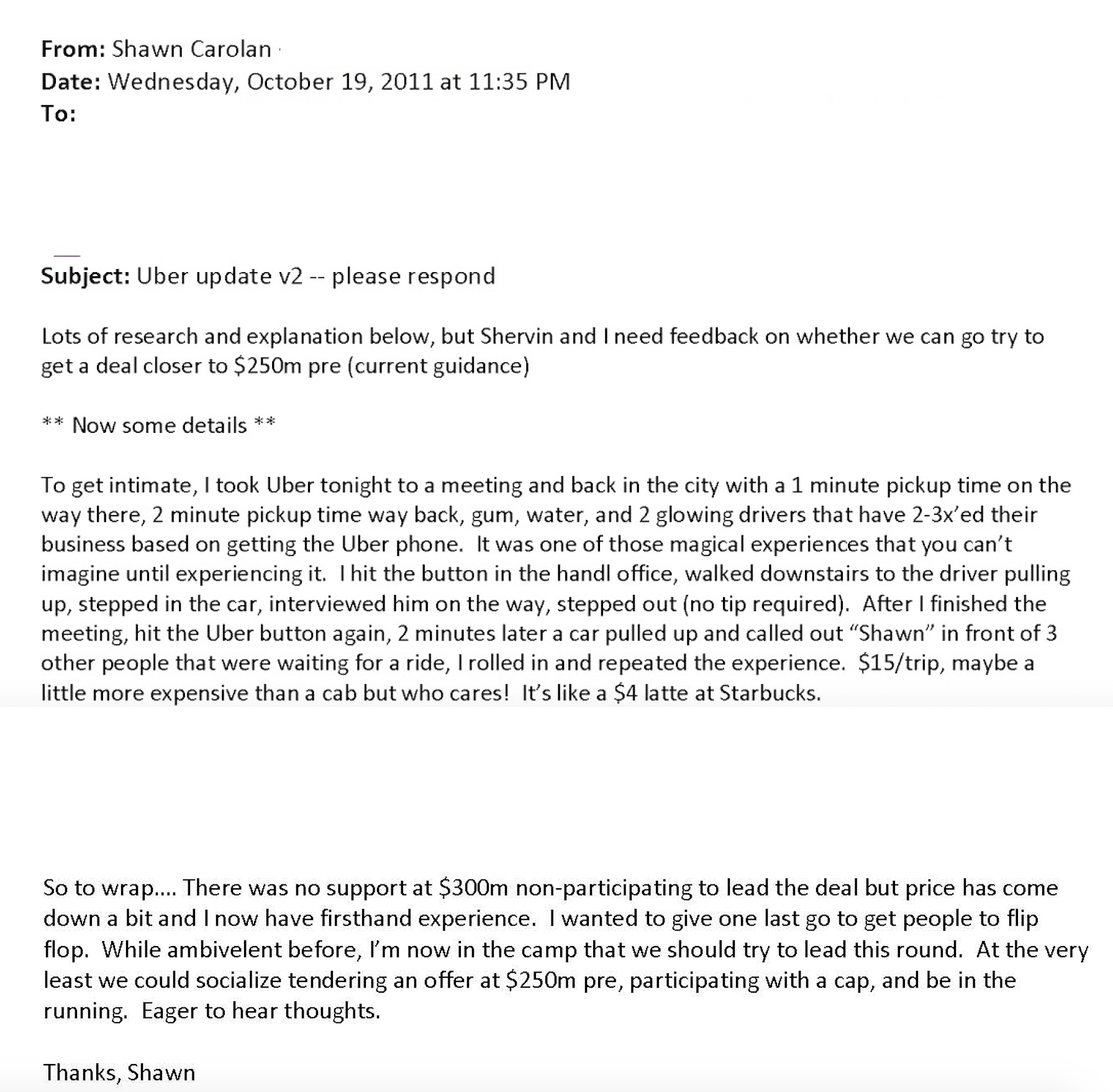

“I wouldn’t have dared to dream quite this big,” Menlo Ventures partner Shawn Carolan told TechCrunch. Carolan and embattled investor Shervin Pishevar, the former Menlo Ventures partner and founder of Sherpa Capital accused of sexual misconduct, secured Menlo a spot on Uber’s cap table years ago when several firms were vying for a stake.

The pair, according to discussions with insiders, are polar opposites, representatives of the diverging approaches to deal-making in Silicon Valley. While Pishevar, described to TechCrunch as “overpowering” and “self-promotional,” developed a lasting relationship with Uber co-founder and former chief executive officer Travis Kalanick crucial to the deal, Carolan, a reserved Midwesterner, crunched the numbers and worked to convince his firm that Uber, a young startup with a hot-headed leader, was worth their time and money.

Now, as Uber preps for an imminent initial public offering, the firm wants to shine a light on Carolan, an under-the-radar investor known more for his humility than his portfolio.

Menlo Ventures partner Shawn Carolan’s last-ditch effort to convince his firm to invest in Uber in late 2011.

As Uber approaches its IPO, a slew of investors that were in the right place at the right time await a payday of unforeseen scale.

Uber dropped its IPO prospectus in early April. Next week, it’s expected to debut on the New York Stock Exchange at a valuation between $80 billion and $100 billion, up from its most recent private valuation of $72 billion. The IPO will be amidst the largest liquidity events for a U.S. VC-backed technology company in history, on par with Facebook’s 2012 public offering that valued the social media empire at $104 billion.

In addition to Menlo Ventures, the Japanese telecom giant SoftBank, Benchmark, Uber co-founders Travis Kalanick and Garrett Camp, Saudi Arabia’s Public Investment Fund and GV, the investment arm of Alphabet, own stakes in Uber worth billions.

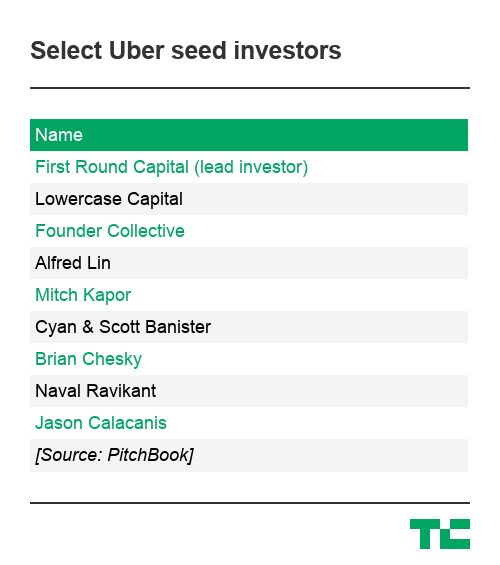

Seed backers like Chris Sacca of Lowercase Capital and Rob Hayes of First Round Capital, who invested in “UberCab” before it had anything to show for itself, will also earn tremendous payouts.

Menlo has already raked in hundreds of millions in profits from its Uber investment, as have several other investors that sold their shares on the secondary market. In 2018, Menlo earned $973 million when a group of investors led by SoftBank purchased nearly half of its Uber stock. The deal represented a 93x return on shares the firm had paid $10.5 million for years prior, according to the firm’s calculations.

Since that transaction, Menlo has expanded its Uber stake through the sale of its portfolio company Jump Bikes to Uber in 2018. The firm had invested $7.5 million in Jump, a provider of a dockless bicycle system, only months before it was acquired by Uber for $200 million. Menlo, as a result, banked another $50 million in Uber stock.

Today, it owns a 2.3 percent stake in Uber worth between $1.85 billion and $2.1 billion, depending on how Uber prices its IPO.

Uber founding CEO Travis Kalanick.

The story of Menlo Ventures’ investment in Uber dates back to 2005 when Carolan first met Travis Kalanick, Uber’s founder and former chief executive. The notorious entrepreneur was fundraising for an earlier company, a peer-to-peer file-sharing startup called Red Swoosh. Menlo didn’t invest, but Kalanick left a lasting impression.

Years later, Benchmark general partner Matt Cohler called Pishevar on his cell phone to let him know Uber had begun raising its Series B. Pishevar didn’t know Kalanick yet but had been introduced to his fast-growing car-sharing business by AngelList founder and Uber backer Naval Ravikant in 2010.

Pishevar was a garish type who would two years later leave Menlo to launch his own firm Sherpa Capital, a backer of Slack, Airbnb, Robinhood, Hyperloop One and more. Carolan was restrained, focused more on metrics than relationships. Together, the pair worked their way onto Uber’s cap table with Pishever serving as the lead investor externally and internally, both men receiving credit as leads.

Venture capitalists often brag about the skill required to land the best deals, but most of the time, it comes down to luck and timing. Menlo, in this case, got really lucky.

A recent feature on Andreessen Horowitz in Forbes detailed the firm’s biggest misstep: losing Uber. Hours before they were set to sign a term sheet, the firm shifted, offering Uber a lower valuation than what had been promised. Kalanick, known already at that point for his disdain for investors, walked. Little did the Menlo team know they were being used as a “stalking horse for leverage,” according to Forbes’ reporting. So when a16z tried to cheapen the deal, Uber turned immediately to its second-choice, Menlo Ventures.

A16z declined to provide additional details for this story.

“Whenever you have a company of this caliber that has that kind of growth rate, there’s a lot of people that are vying for the opportunity to invest,” Carolan said. “Frankly, there’s never been a company like Uber.”

With a sense of urgency, Pishevar hopped on a plane to Dublin, Ireland at Kalanick’s request. The CEO was speaking at a technology conference called Web Summit. It was there that the term sheets were signed over pints at the Shelbourne Hotel, and a close friendship between Pishevar and Kalanick would begin to blossom. Pishevar, according to The New York Times, later introduced the ride-hail chief to the club scene and Los Angeles celebrity culture. Until Kalanick’s final days as CEO, Pishevar would fiercely defend the founder’s dog-eat-dog style of management. To this day, the two are close friends.

Meanwhile, Carolan was heads down, benchmarking Uber against other tech companies, completing a thorough unit economics analysis and hoping his colleagues wouldn’t be disappointed by the Uber investment, a point of contention among certain Menlo staffers who viewed Uber as a limo dispatch company with an app, not the next billion-dollar business.

“There were a lot of things you had to believe back then and at that moment in time, Uber didn’t paint that picture, [Carolan] was the one who painted that picture,” Mark Siegel, a managing director at Menlo since 1996, told TechCrunch. “And he pounded the table pretty hard.”

After all, Uber was only active in four markets at the time of Menlo’s initial investment: San Francisco, Seattle, Chicago and New York City. Rider bookings were growing fast but were just $1 million per month, with close to zero net revenue after paying drivers. Carolan himself was unconvinced of the business’s longevity until his first ride in an Uber turned him.

Uber declined to confirm early booking figures.

“We had a lot of heartburn over the valuation,” Carolan said. “But it’s the ones you don’t chase, like YouTube, which I kind of dismissed as a lousy business and didn’t chase it. When you see something like Uber that has that type of repeated retention and essentially zero customer acquisition, it’s kind of like, okay, this is just a magical experience that’s going to sell itself.”

Carolan’s commitment was recognized internally but while Uber gained momentum, so did Pishevar. His involvement in Uber brought him notoriety, while Carolan’s role slipped through the cracks. Even when accusations of sexual misconduct against Pishevar surfaced in 2017, his name was often preceded by “early Uber investor.”

Pishevar was accused of sexually harassing multiple women, including Uber’s very own former head of global expansion, Austin Geidt. The Bloomberg expose highlighting allegations against him came just one month after a report he had been arrested in London for rape. Charges for the reported London incident were later dropped and Pishevar, through his lawyer, has said the other claims were part of a “smear campaign” against him.

Menlo Ventures sought to distance itself from the scandal, naturally, claiming in a series of tweets they had no knowledge of inappropriate behavior during his tenure at the firm.

A Chicago native, Shawn Carolan joined Menlo Ventures in 2002 as a 28-year-old fresh out of Stanford’s business school. His wife and high school sweetheart, Jennifer Carolan, would make a career as a venture capitalist, too, co-founding Reach Capital, an edtech-focused VC fund coincidentally located next door to Menlo’s San Francisco outpost.

Menlo Ventures partner Shawn Carolan.

In 2009, the Menlo team realized they had overcompensated on enterprise and made the call to pioneer a reinvigorated consumer tech strategy spearheaded largely by Carolan.

In 2011, to bolster the new effort, Carolan hired Pishevar, a rookie VC they hoped would bring a fresh perspective to a firm of engineering geeks. Immediately, Pishevar sourced Square, Jack Dorsey’s hot new payments startup. The team rallied behind him but ultimately, Square went with Kleiner Perkins’s Mary Meeker instead. Later, Pishevar would bring in Pinterest and Snap, mere months after the ephemeral messaging app had launched but the Menlo team passed, according to a source with knowledge of the deals.

In Pishevar’s first six months at Menlo, he invested in Tumblr, Warby Parker, Machine Zone and Uber.

Carolan, for his part, has returned more capital in a single year than any partner in its history, the firm said. In a 12-month period between 2017 to 2018, Roku’s IPO and the Uber stock sale brought in some $2 billion in returns for Menlo, capital that was used to fuel its latest fund, a $500 million vehicle focused on Series B and C-stage startups.

In addition to accumulating a 35.3 percent pre-IPO stake in the digital streaming business Roku, which the firm celebrated with boxes of popcorn implanted with several thousand dollars in cash bonuses for the administrative team, Carolan was the first institutional investor in Siri, the personal assistant application Apple paid a little more than $200 million for in 2010. More recently, he invested in Chime, a mobile banking platform valued at $1.5 billion in March.

Pishevar, since leaving Menlo, has continued to ink deals with high-flying unicorns, including Uber, in which Sherpa invested an additional $200 million. However, since resigning from Sherpa Capital following the sexual misconduct scandal in 2017, he’s kept a much lower profile. Most recently, he signed on as an investor and board member at Bolt Mobility, an electric scooter business in Florida. A 2018 Florida business filing listed him as the company’s sole officer, though the Bolt team recently told BuzzFeed Pishevar was strictly an investor. The Sherpa Capital team, for their part, have relaunched as ACME Capital.

Bolt has not responded to a request for comment.

Menlo remained one of the largest institutional backers in Uber for years, a position that, while lucrative, proved tricky when Uber began to unravel internally.

When Pishevar left Menlo Ventures to build Sherpa Capital in 2013, Carolan assumed the Menlo board observer seat for the next 21 months. Pishevar, now a close friend to Kalanick, stayed on the board as an observer until 2015.

Eventually, Carolan would take a step back from Menlo to focus on his productivity startup, Handle. But when Handle failed to become the rocket ship Carolan had dreamed of, he returned to investing at Menlo full-time with a newfound empathy for founders.

Little did he know he would play a role in the high-profile ouster of one of the most notable tech founders of all time.

In July 2016, talks of Kalanick’s resignation led by Benchmark general partner and Uber board member Bill Gurley began. Menlo had given up its board observer seat by then, but was part of a consortium of four key early Uber investors (Benchmark, First Round Capital and Lowercase Capital) that controlled the preferred share vote, which was needed to make impactful decisions; for example, approving new board seats or remove a founding CEO.

In 2017, it became abundantly clear that Uber would never achieve profitability nor complete its highly anticipated IPO with Kalanick at the helm. Susan Fowler had published her infamous blog post, executives were quitting, remarks on Uber’s toxic culture could be found just about anywhere and the #DeleteUber campaign had turned social media against the ride-hail company.

Shervin Pishevar (right) looks on as he gives a press conference during the Web Summit at Parque das Nacoes, in Lisbon on November 10, 2016. (PATRICIA DE MELO MOREIRA/AFP/Getty Images)

Uber was going to implode if the board didn’t act. Benchmark’s Gurley took center stage, calling on Kalanick to resign. Pishevar remained a Kalanick confidant and later when Benchmark sued Kalanick, he published a bizarre open letter in an eleventh-hour attempt to sway the public to rally behind the ousted CEO. Carolan, reluctant to be perceived as anything other than founder friendly, turned against the founder and advocated alongside Gurley for Kalanick’s removal.

“I imagine he wouldn’t be particularly happy with me for having done that but you gotta do what you gotta do sometimes,” Carolan said. “Ultimately, our job is to help that company achieve its mission. It’s not an allegiance to any one person at the company.”

Finally, Kalanick gave up the Uber C-suite in June 2017 and former Expedia Group CEO Dara Khosrowshahi stepped in as his replacement. Sixteen months later, Uber would file confidentially for a 2019 IPO.

Menlo Ventures leaped into cutting-edge consumer investing at a time when its reputation in The Valley was unremarkable. For years, decades even, the firm shielded itself from PR and declined to take the spotlight as the Andreessen Horowitzes of the world touted their successes.

Today, the firm is more accepting of attention, leveraging its Uber position to attract entrepreneurs and foster new unicorns, like the more recent portfolio additions Chime and Carta.

“It has clearly benefited us in terms of the overall perception of the firm and credibility,” Siegel said, admitting he was one of the Menlo partners dubious of its 2011 Uber investment. “There’s no doubt it has been a huge positive.”

In the years since Uber came along, Menlo has made key additions to its team, marking the beginning of a new era for the timeworn investor. In 2015, it hired Steve Sloane, who became the firm’s youngest partner to date when he was promoted earlier this year. Naomi Ionita, the firm’s only female partner, joined in early 2018. And Grace Ge, a fresh recruit from RRE Ventures in New York, started this week as a senior associate on the venture team. Another yet-to-be-announced hire will begin in June.

Uber, despite narrowly avoiding a complete implosion in 2017, has changed the game for many investors. The returns it will generate in the next several months will refresh the coffers of many venture capital funds. Money tied to Uber will flow toward the next generation of founders for years to come, and the investors responsible for its landmark success will boast about it for the remainder of their careers.

Even if Uber doesn’t turn out to be the Wall Street darling its investors hope — Lyft has struggled to accumulate value on the public markets — the company has indisputably transformed the Silicon Valley playbook for hypergrowth and execution in the gig-economy ecosystem.

Powered by WPeMatico

I sat down with Menlo Ventures partner Shawn Carolan this week to talk about his early investment in Uber. Menlo, if you remember, led Uber’s Series B and has made a hefty sum over the year selling shares in the ride-hailing company. I’ll have more on that later; for now, I want to share some of the insights Carolan had on his experience ditching venture capital to become a founder.

Around when Menlo made its first investment in Uber, Carolan began taking a step back from the firm and building Handle, a startup that built tools to help people be more productive. Despite years of hard work, Handle was ultimately a failure. Carolan said he shed a lot of tears over its demise, but used the experience to connect more intimately with founders and to offer them more candid, authentic advice.

“People in the valley are always achievement-oriented; it’s always about the next thing and crushing it and whatever,” Carolan told TechCrunch. “When [Handle] shut down, I had this spreadsheet of all the people who I felt like I disappointed: Seed investors who invested in me, all the people at Menlo and my friends who had tweeted out early stuff. It was a long spreadsheet of like 60 people. And when I started a sabbatical, what I said was I’m going to go connect with everyone and apologize.”

Today, Carolan encourages founders to own their vulnerabilities.

“It’s OK to admit when you’re wrong,” he said. “Now I can see it on [founders’] faces, I can see when they’re scared. And they’re not going to say they’re scared but I know it’s tough. This is one of the toughest things that you’re going to go through. Now I can be there emotionally for these founders and I can say ‘here’s how you do it, here’s how you talk to your team and here’s what you share.’ A lot of founders feel like they have to do this alone and that’s why you have to get comfortable with your vulnerability.”

After Handle shuttered, Carolan returned to Menlo full time and made the firm a boatload of money from Roku’s IPO and now Uber’s. Anyway, thought those were some nice anecdotes that should be shared since most of our feeds are dominated by Silicon Valley hustle porn.

Want more TechCrunch newsletters? Sign up here. Ok, on to other news…

IPO corner

There were so many fund announcements this week; here’s a quick list.

Lots of great new exclusive content for our Extra Crunch subscribers is on the site, including this deep dive into the challenges of transportation startup profits. Plus: When to ditch a nightmare customer, before they kill your startup; The right way to do AI in security; and The definitive Niantic reading guide.

Sinema, that one MoviePass competitor, has run into its fair share of bumps in the road. TechCrunch’s Brian Heater hopped on the phone with the startup’s CEO this week to learn more about those bumps, why its terminating accounts en masse, a class-action lawsuit its battling and more.

Photo by Stephen McCarthy / RISE via Sportsfile

TechCrunch’s Startup Battlefield brings the world’s top early-stage startups together on one stage to compete for non-dilutive prize money, and the attention of media and investors worldwide. Here’s a quick update on some of our BF winners and finalists:

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm, myself and Phil Libin, the founder of Evernote and AllTurtles, chat about the importance of IPOs. Plus, in a special Equity Shot, Alex and I unpack the Uber S-1.

Powered by WPeMatico

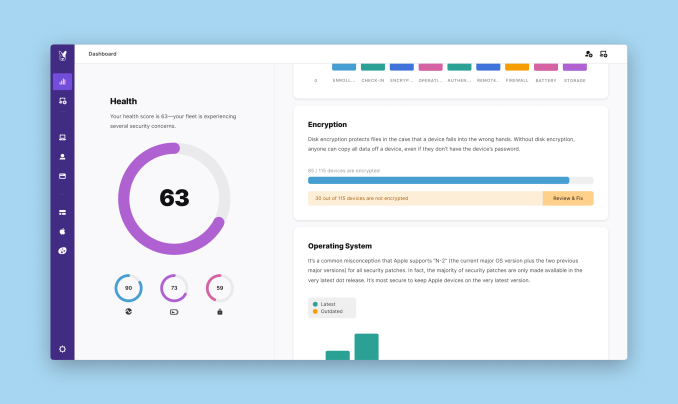

Fleetsmith launched in 2016 with a mission to manage Apple devices in the cloud. It simplified an IT activity that had previously been complex, with help from Apple’s Device Enrollment Program. Over the last year, the startup has beefed up its offering considerably, and today it announced a $30 million Series B round led by Menlo Ventures.

Tiger Global Management, Upfront Ventures and Harrison Metal also participated. Under the terms of the deal, Naomi Pilosof Ionita, a partner at Menlo, will join the company board. Her colleague Matt Murphy will become a board observer. With today’s announcement, the startup has now raised more than $40 million, according to data supplied by the company.

Company co-founder and CEO Zack Blum says the original mission was about solving a pain point he and his co-founders were feeling around finding a modern approach to managing Apple devices. “From a customer perspective, they can ship devices directly to their employees. The employee unwraps it, connects to Wi-Fi and the device is enrolled automatically in Fleetsmith,” Blum explained.

He says that this automated approach, combined with the product’s security and intelligence capabilities, means that IT doesn’t have to worry about devices being registered and up-to-date, regardless of where an employee happens to be in the world.

It has moved from solving that problem for SMBs to having a broader mission for companies of all sizes, especially those with distributed work forces, which can benefit from enrolling in this automated fashion from anywhere. Once enrolled, companies can push security updates to all of the company’s employees and force updates if desired (or at least send strong reminders to avoid updating in the middle of a client meeting).

Over the last year, the company developed a dashboard for IT to monitor all of the devices under its management, including providing an overall health score with any potential problems it has found. For example, there may be a number of MacBook Pros without disk encryption enabled.

The dashboard ties into the identity management component of Office 365 and G Suite. IT can import the employee directory into the dashboard from either tool, and employees can sign into Fleetsmith with either set of credentials, providing a quick way to manage all employees in an organization.

Screenshot: Fleetsmith

Fleetsmith has also set up a partner program with Managed Service Providers (MSPs) to expand its reach further. MSPs manage IT for SMBs, and building a relationship with these types of companies can help it expand much more quickly.

The approach seems to be working, as the company has 30 employees and 1,500 customers. With the new cash in pocket, it intends to hire more people and continue building out the product’s capabilities, while expanding beyond the U.S. to markets overseas.

Powered by WPeMatico

Several weeks after a sudden shutdown left customers and vendors in the lurch, meal-kit service Munchery has filed for bankruptcy. In the Chapter 11 filing, Munchery chief executive officer James Beriker cites increased competition, over-funding, aggressive expansion efforts and Blue Apron’s failed IPO as reasons for its demise.

Munchery owes $3 million in unfulfilled customer gift cards and another $3 million to its vendors, suppliers and various counterparties, the filing reveals. The company’s remaining debt includes $5.3 million in senior secured debt and convertible debt of approximately $23 million. Munchery says its scrounged up $5 million from a buyer of its equipment, machinery and San Francisco headquarters.

The business had raised more than $100 million in venture capital funding, reaching a valuation of $300 million in 2015 before ceasing operations on January 22 and laying off 257 employees in the process. Munchery was backed by Menlo Ventures, Sherpa Capital, e.Ventures, Cota Capital and others.

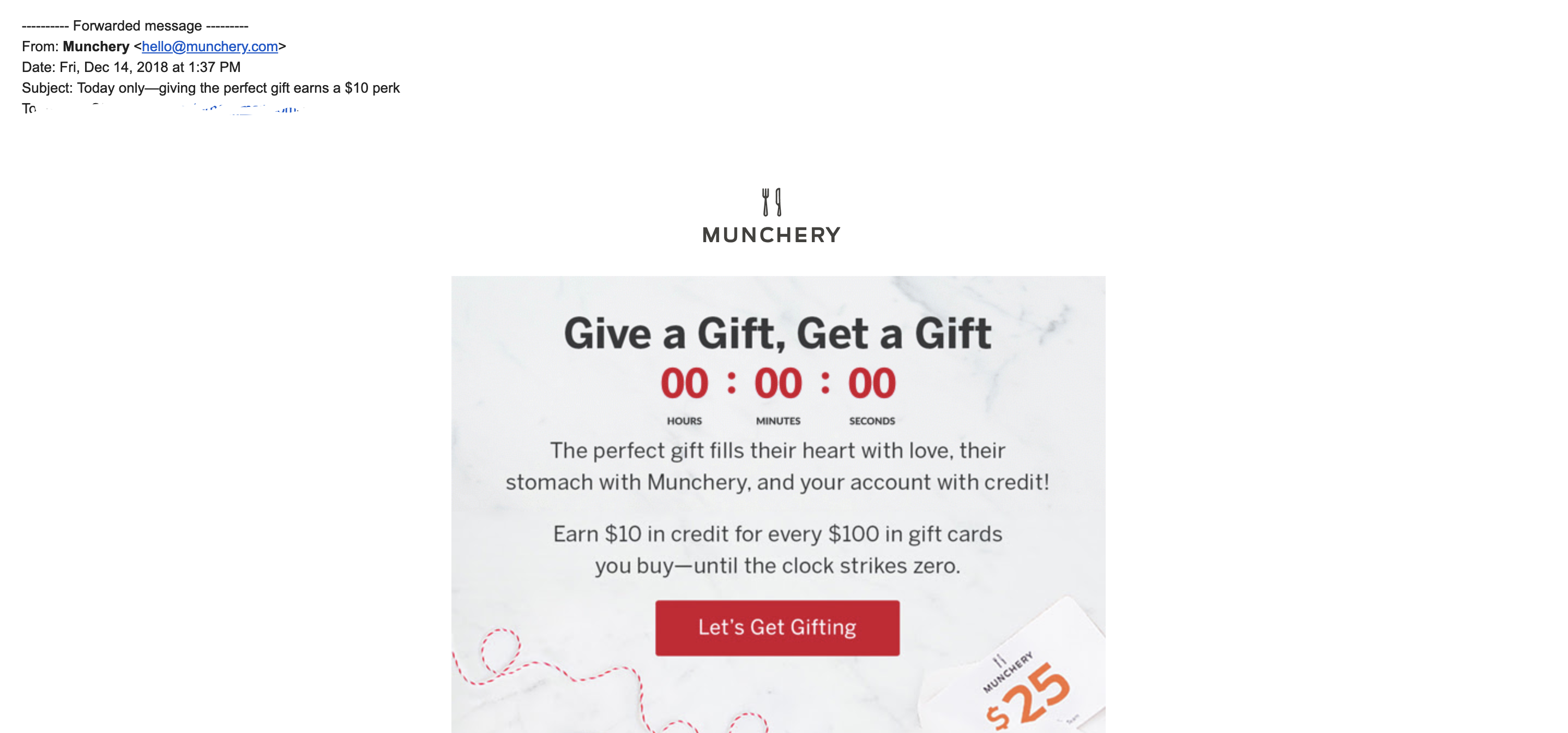

The company, which failed to notify its vendors it was going out of business, has been scrutinized for failing to pay those vendors in the wake of its shutdown. To make matters worse, emails viewed by TechCrunch show Munchery continued aggressively marketing its gift cards in emails sent to customers in December, weeks before a final email to those very same customers announced it was ceasing operations, effectively immediately.

An email advertising Munchery gift cards sent to a customer weeks before the startup went out of business.

The latest court filings shed light on Beriker’s decision-making process in those final months, touching on Munchery’s frequent pivots, the company’s 2017 layoffs, its plans to scale sales of Munchery products in Amazon Go stores and failed attempts at a sale. Beriker is the sole remaining Munchery board member. He has not responded to several requests for comment from TechCrunch.

In the third quarter of 2018, Munchery, at the recommendation of its board, hired an investment bank to find a buyer for the startup, to no avail. Beriker suggests the lack of a buyer, coupled with industry trends like larger-than-necessary venture capital rounds and inflated valuations, were cause for the startup’s failure to deliver.

“The company expanded too aggressively in its early years,” the filing states. “The access to significant amounts of capital from leading Silicon Valley venture capital firms at high valuations and low-cost debt from banks and venture debt firms, combined with the perception that the on-demand food delivery market was expanding quickly and would be dominated by one or two brands– as Uber had dominated the ridesharing market– drove the company to aggressively invest in its business ahead of having a well-established and scalable business model.”

Increased competition from well-funded competitors drove the startup off course, too, and the epic failure that was Blue Apron’s IPO, which had a “material negative impact on access to financing for startups in the online food delivery business,” was just the cherry on top, according to Beriker’s statements.

Former Munchery vendors protested today at @sherpa, one of the startup’s investors that’ve stayed silent as former employees, vendors and drivers claim to be owed thousands: “Startup idea don’t steal pies!” Photo by @ThreeBabesBake pic.twitter.com/kfaOZ9CFkq

— Kate Clark (@KateClarkTweets) January 30, 2019

Munchery’s vendors, who were not notified or paid following Munchery’s announcement, have provided outspoken criticism to the company and venture capital’s lack of accountability in the weeks following Munchery’s shutdown. Lenore Estrada of Three Babes Bakeshop, among several vendors owed thousands of dollars in unpaid invoices, orchestrated a protest outside of Munchery investor Sherpa Capital’s offices in January. She said she has spoken with Beriker and founding Munchery CEO Conrad Chu in an attempt to pick up the pieces of the failed startup puzzle.

“None of us who are owed money are going to get anything,” Estrada told TechCrunch earlier today. “But the CEO, after fucking it all up, is still getting paid.”

Beriker, indeed, is still earning a salary of $18,750 per month, one-half of his pre-bankruptcy salary, as well as a “success fee based on the net proceeds recovered from the sale of the company’s assets up to a maximum of $250,000,” the filing states.

View the full bankruptcy filing here:

Powered by WPeMatico

Thanks to environmentally conscious young buyers, throwaway culture is dying not only in the U.S., but also in Latin America — and startups are poised to jump in with services to help people recycle used clothing.

GoTrendier, a peer-to-peer fashion marketplace operative in Mexico and Colombia, has raised $3.5 million USD to do just that. And investors are eyeing the startup as the digital fashion marketplace growth leader in Spanish-speaking countries.

GoTrendier, founded by Belén Cabido, is a platform that lets users buy and sell secondhand clothing. Cabido tells me that the new capital will enable GoTrendier to expand deeper into Mexico and Colombia, and launch in a new country: Chile.

GoTrendier enables users to buy and sell used items through the GoTrendier site and app. The platform categorizes users as either salespeople or buyers. Salespeople create their own stores by uploading photos of garments along with a description and sale price. Buyers browse the platform for deals and once a buyer bites, the seller is given a prepaid shipping label.

Sound familiar? Businesses like Poshmark and GoTrendier have no actual inventory, which allows the companies to take on less of a risk by having smaller overhead costs. In turn, the company acts as more of a social community for fashion exchanges.

In order to make money, Poshmark takes a flat commission of $2.95 for sales under $15. For anything more than that, the seller keeps 80 percent of their sale and Poshmark takes a 20 percent commission. Poshmark also owes its success to the socially connected shopping experience it created and the audience building features available to sellers — as detailed in this Harvard Business School study. GoTrendier has a similar commission pricing strategy, taking 20 percent off plus an additional nine pesos (about 48 cents in U.S. currency) for all purchases. The service also takes advantage of social media and sharing features to help connect and engage its fashion-loving community.

But these companies are also largely venture-backed. In the case of GoTrendier, the round gave shareholder entry to Ataria, a Peruvian fund that invests in early-stage tech companies with high earning potential. Existing investors Banco Sabadell and IGNIA reinforced their position, along with Barcelona-based investors Antai Venture Builder, Bonsai Venture Capital and Pedralbes Partners.

GoTrendier amassed a user base of 1.3 million buyers and sellers throughout its four years of existence. The service operates in Mexico and Colombia, and will use its newest capital to launch in Chile — another market Cabido says is experiencing high demand for a secondhand fashion buying and selling service.

Online marketplace companies are growing in Latin America as smartphone adoption and digital banking services multiply in the region. But international expansion has proven to be an issue. Enjoei, a similar fashion marketplace that owns the market share in Brazil, had a botched attempt at expanding to Argentina due to Portugese-Spanish language barriers and eventually determined that Brazil was a large enough market in which to build its business — thus carving out an opportunity for companies like GoTrendier that offer the same services to dominate the surrounding Spanish-speaking markets in Latin America.

Many have remarked that Latin America’s tech scene is filled with copycats — or companies that emulate the business models of American or European startups and bring the same service to their home market. In order to secure bigger foreign investment checks, founders from growing tech regions like Latin America certainly must invent proprietary technologies. Yet there’s still value — and capital — in so-called copycat businesses. Why? Because the users are there and in some cases it’s just easier to start up.

According to investor Sergio Pérez of Sabadell Venture Capital, “The volume of the market for buying and selling second-hand clothes in the world was 360 million transactions in 2017 and is expected to reach 400 million in 2022.” A 2018 report from ThredUp also claimed that the size of the global secondhand market is set to hit $41 billion by 2022. The “throwaway” culture is disappearing thanks to environmentally conscious millennial buyers. As designer Stella McCartney famously said, “The future of fashion is circular – it will be restorative and regenerative by design and the clothes we love never end up as waste.” By buying on GoTrendier, the company claims its users have been able to save USD $12 million and have avoided more than 1,000 tons of CO2 emissions.

Founders building companies in Latin America aren’t necessarily as capital-hungry as Silicon Valley-based founders, (where a Series A can now equate to $68 million, apparently). Cabido tells me her company is able to fulfill operations and marketing needs with a lean staff of 30, noting that there’s a lot of natural demand for buying and selling used clothing in these regions, thus creating organic growth for her business. She wasn’t looking to raise capital, but investors had their eye on her. “[Investors] saw the tension of the marketplace, and we demonstrated that GoTrendier’s user base could be bigger and bigger,” she says. With sights set on new markets like Chile and Peru, Cabido decided to move forward and close the round.

Poshmark, which benefits from indirect and same-side network effects, has raised $153 million to date from investors like Temasek Holdings, GGV and Menlo Ventures. Just like GoTrendier, Poshmark’s Series A was also a $3.5 million round.

Who’s to say that that amount of capital can’t boost a network effects growth model in Latin America too? The users are certainly waiting.

Powered by WPeMatico

The Munchery saga continues.

In a new class-action lawsuit, former Munchery facilities worker Joshua Philips is claiming the startup owes him and 250 other employees 60 days’ wages, citing The Worker Adjustment and Retraining Notification Act, a U.S. labor law that requires employers with an excess of 100 employees to give notice 60 days ahead of mass layoffs.

Munchery, a prepared meal delivery company headquartered in San Francisco, announced in an email to customers on January 21 that it would cease operations, effectively immediately. The abrupt shutdown not only came as a surprise to Munchery’s community of customers, but shocked vendors, many whom had been expecting payments from the business for several weeks. Munchery’s own employees were left in the dark, too, according to several former workers who spoke to TechCrunch about their debt and dissatisfaction with chief executive James Beriker.

Munchery ordered mass layoffs on January 21, per the lawsuit, the same day customers were notified the company would go out of business. In total, Philips is seeking equal to the sum of his and other affected employees’ “unpaid wages, salary, commissions, bonuses, accrued holiday pay, accrued vacation pay, pension and 401(k) contributions and other ERISA benefits, for 60 days, that would have been covered and paid under the then-applicable employee benefit plans.”

Munchery is deep in a pile of debt. The startup’s former vendors, which includes San Francisco-based Dandelion Chocolate and Three Babes Bakeshop, say they’re owed tens of thousands in overdue payments. Those businesses, and several other small vendors in San Francisco and Los Angeles that notified TechCrunch following the publication of this story, are still awaiting overdue payments, with one supplier claiming to be owed north of $100,000.

As of Monday morning, Munchery had yet to file for bankruptcy.

“They entered into a 14-month payment plan with us to cover nearly $150,000 in debt, but never had the intention of fulfilling their obligation,” an LA-based Munchery vendor, who asked not to be named, told TechCrunch. “The entire meal prep business is not sustainable on a grand scale like these companies envision.”

On top of its outstanding debts to vendors and facilities workers, Munchery also failed to send final paychecks to delivery drivers. Several Instagram messages provided to TechCrunch show a cluster of drivers in the San Francisco and Sacramento area are confused by the lack of communication from the venture-funded startup and are hopeful checks will arrive.

After arguing with Munchery employees, a delivery driver in Sacramento by the name of Sharon Howard said she finally received a “janky looking handwritten check” from the business on Monday and is hopeful it will clear.

“My co-workers up here in Sacramento have not received their final checks and are just um…waiting,” Howard wrote in an Instagram message shared with TechCrunch. “I sort of have the feeling that if they don’t speak up, they’re just gonna be forgotten about … It’s just not right to work with the expectation of getting paid and then just allow Munchery to turn a blind eye.”

Munchery chief executive officer James Beriker joined the startup in 2016

Munchery had raised $125 million in venture capital funding at a peak valuation of $300 million from key investors e.Ventures, Infinity Ventures, Sherpa Capital and Menlo Ventures, as well as from Greycroft, M13, Northgate Capital and more since its founding in 2010 by Tran and Conrad Chu. Aside from a small $5 million check, all that cash was deployed under the leadership of Tran, who struggled to improve Munchery’s margins and was eventually replaced by Beriker, the former CEO of Simply Hired.

Munchery, however, struggled under Beriker, too, and ultimately shut down its Los Angeles, Seattle and New York operations and laid off 30 percent of its workforce. A former Munchery employee, who asked not to be named, said Beriker’s poor leadership is to blame for the startup’s failure.

“The CEO was very disconnected to the business,” the person said in a text message. “We would see him maybe once every other week and only for 15 minutes — if that. The kitchen staff didn’t even know who he was when he came to the facility. In my time with the company, he was rarely truthful or transparent about the current state of the business and the future direction. Not to mention his very hefty salary that compared to that of a publicly traded Fortune 500 company.”

“My heart goes out to all of the big and small businesses that Munchery’s closure has and will affect,” the person added. “I am also hopeful that the staff who had zero advance knowledge of the closure will find employment quickly.”

Beriker has not responded to multiple requests for comment from TechCrunch. We’ve reached out to Munchery’s investors for additional details surrounding the strange, sudden and silent shutdown.

Here’s a look at the full legal complaint:

Powered by WPeMatico