Maverick Ventures

Auto Added by WPeMatico

Auto Added by WPeMatico

Cityblock Health, a company that provides healthcare services to low-income communities, is now commanding a high-priced valuation of over $1 billion after venture capitalists poured $160 million into the company.

The round was led by new investor General Catalyst with participation from crossover investor Wellington Management and support from major existing investors, including Kinnevik AB, Maverick Ventures, Thrive Capital, Redpoint Ventures and more, according to a statement from the company.

Cityblock works with community caregivers to work with residents to provide primary care, behavioral health and other services to address social determinants of health, in person and… increasingly… through virtual consultations.

The company first spun out of Alphabet’s Sidewalk Labs in 2017 and initially partnered with EmblemHealth. By relying primarily on licensed clinical social workers, community health partners and a network of specialized practice clinicians and doctors to provide basic primary care and supporting health services, Cityblock believes it can drive down the costs of healthcare.

Some 70,000 patients use Cityblock services in four major U.S. cities, the company said.

To date, Cityblock has raised $300 million.

The company said in a statement that the new funding will be used to support Cityblock’s national expansion in caring for Medicaid and dually-eligible communities, to attract and onboard talent across its product, engineering, data science, clinical and business operations, to launch new service lines and to continue investing in its proprietary technology platform, Commons.

Powered by WPeMatico

Depending on which study you believe, the wearable and digital health market could be worth anywhere from $30 billion to nearly $90 billion in the next six years.

If the numbers around the size of the market are a moving target, just think about how to gauge the validity and efficacy of the products that are behind all of those billions of dollars in spending.

Andy Coravos, the co-founder of Elektra Labs, certainly has.

Coravos, whose parents were a dentist and a nurse practitioner, has been thinking about healthcare for a long time. After a stint in private equity and consulting, she took a coding bootcamp and returned to the world she was raised in by taking an internship with the digital therapeutics company Akili Interactive.

Coravos always thought she wanted to be in healthcare, but there was one thing holding her back, she says. “I’m really bad with blood.”

That’s why digital therapeutics made sense. The stint at Akili led to a position at the U.S. Food and Drug Administration as an entrepreneur in residence, which led to the creation of Elektra Labs roughly two years ago.

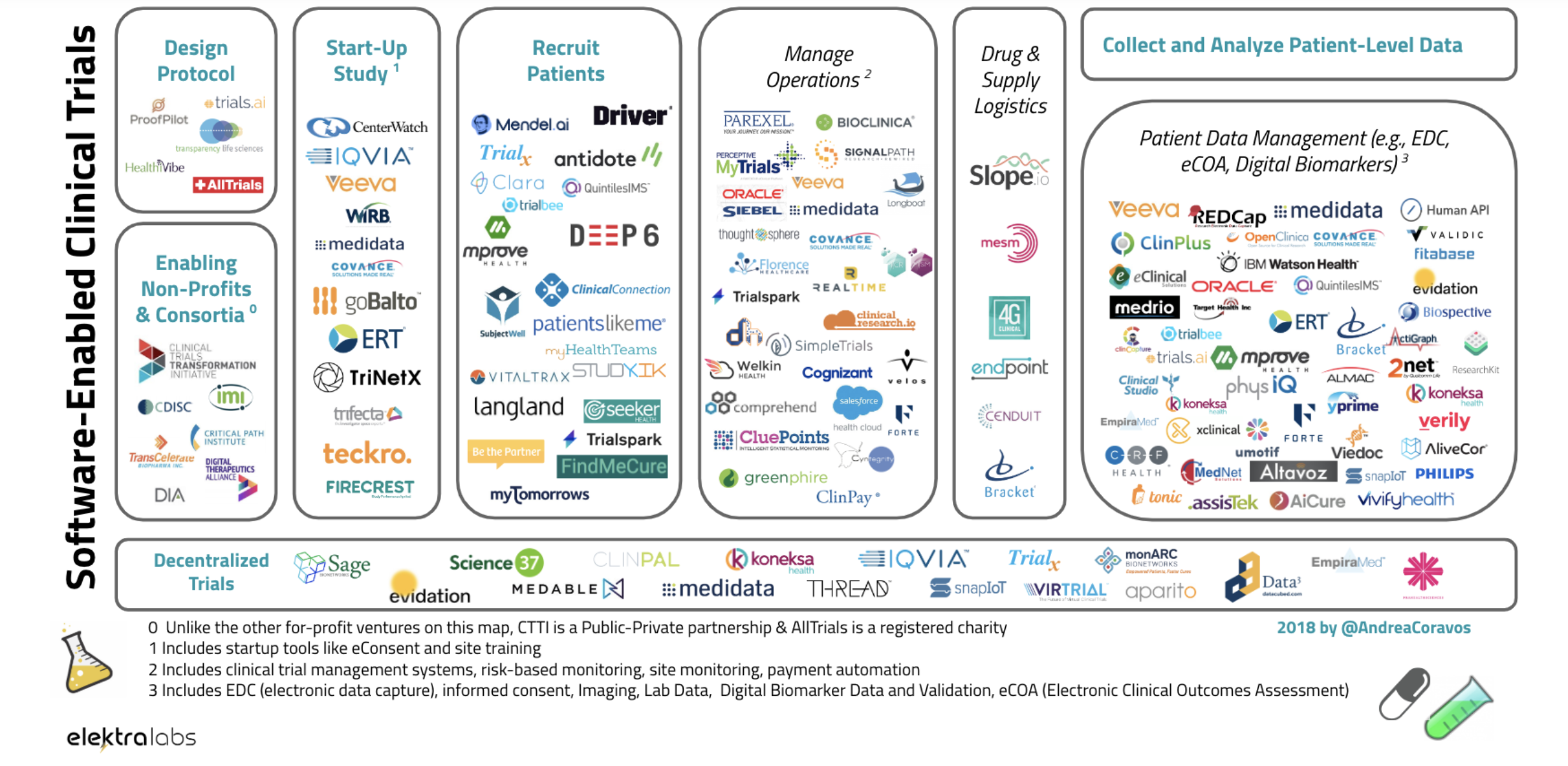

Now the company is launching Atlas, which aims to catalog the biometric monitoring technologies that are flooding the consumer health market.

These monitoring technologies, and the applications layered on top of them, have profound implications for consumer health, but there’s been no single place to gauge how effective they are, or whether the suggestions they’re making about how their tools can be used are even valid. Atlas and Elektra are out to change that.

The FDA has been accelerating its clearances for software-driven products like the atrial fibrillation detection algorithm on the Apple Watch and the ActiGraph activity monitors. And big pharma companies like Roche, Pfizer and Novartis have been investing in these technologies to collect digital biomarker data and improve clinical trials.

Connected technologies could provide better care, but the technologies aren’t without risks. Specifically, the accuracy of data and the potential for bias inherent in algorithms that were created using flawed data sets mean there’s a lot of oversight that still needs to be done, and consumers and pharmaceutical companies need to have a source of easily accessible data about the industry.

”The increase in FDA clearances for digital health products coupled with heavy investment in technology has led to accelerated adoption of connected tools in both clinical trials and routine care. However, this adoption has not come without controversy,” said Coravos in a statement. “During my time as an Entrepreneur in Residence in the FDA’s Digital Health Unit, it became clear to me that like pharmacies which review, prepare, and dispense drug components, our healthcare system needs infrastructure to review, prepare, and dispense connected technologies components.”

The analogy to a pharmacy isn’t an exact fit, because Elektra Labs currently doesn’t prepare or dispense any of the treatments that it reviews. But Atlas is clearly the first pillar that the digital therapeutics industry needs as it looks to supplant pharmaceuticals as treatments for some of the largest and most expensive chronic conditions (like diabetes).

Courtesy of Andrea Coravos/Elektra Labs

Coravos and here team interviewed more than 300 professionals as they built the Atlas toolkit for pharmaceutical companies and other healthcare stakeholders seeking a one-stop shop for all their digital healthcare data needs. Like a drug label, or nutrition label, Atlas publishes labels that highlight issues around the usability, validation, utility, security and data governance of a product.

In an article in Quartz earlier this year, Coravos made her pitch for Elektra Labs and the types of things it would monitor for the nascent digital therapeutics industry. It includes the ability to handle adverse events involving digital therapies by providing a single source where problems could be reported; a basic description for consumers of how the products work; an assessment of who should actually receive digital therapies, based on the assessment of how well certain digital products perform with certain users; a description of a digital therapy’s provenance and how it was developed; a database of the potential risks associated with the product; and a record of the product’s security and privacy features.

As the projections on market size show, the problem isn’t going to get any smaller. As Google’s recent acquisition bid for Fitbit and the company’s reported partnership with Ascension on “Project Nightingale” to collect and digitize more patient data shows, the intersection of technology and healthcare is a huge opportunity for technology companies.

“Google is investing more. Apple is investing more… More and more of these devices are getting FDA cleared and they’re becoming not just wellness tools but healthcare tools,” says Coravos of the explosion of digital devices pitching potential health and wellness benefits.

Elektra Labs is already working with undisclosed pharmaceutical companies to map out the digital therapeutic environment and identify companies that might be appropriate partners for clinical trials or acquisition targets in the digital market.

“The FDA is thinking about these digital technologies, but there were a lot of gaps,” says Coravos. And those gaps are what Elektra Labs is designed to fill.

At its core, the company is developing a catalog of the digital biomarkers that modern sensing technologies can track and how effective different products are at providing those measurements. The company is also on the lookout for peer-reviewed published research or any clinical trial data about how effective various digital products are.

Backing Coravos and her vision for the digital pharmacy of the future are venture capital investors, including Maverick Ventures, Arkitekt Ventures, Boost VC, Founder Collective, Lux Capital, SV Angel and Village Global.

Alongside several angel investors, including the founders and chief executives from companies including: PillPack, Flatiron Health, National Vision, Shippo, Revel and Verge Genomics, the venture investors pitched in for a total of $2.9 million in seed funding for Coravos’ latest venture.

“Timing seems right for what Elektra is building,” wrote Brandon Reeves, an investor at Lux Capital, which was one of the first institutional investors in the company. “We have seen the zeitgeist around privacy data in applications on mobile phones and now starting to have the convo in the public domain about our most sensitive data (health).”

If the validation of efficacy is one key tenet of the Atlas platform, then security is the other big emphasis of the company’s digital therapeutic assessment. Indeed, Coravos believes that the two go hand-in-hand. As privacy issues proliferate across the internet, Coravos believes that the same troubles are exponentially compounded by internet-connected devices that are monitoring the most sensitive information that a person has — their own health records.

In an article for Wired, Koravos wrote:

Our healthcare system has strong protections for patients’ biospecimens, like blood or genomic data, but what about our digital specimens? Due to an increase in biometric surveillance from digital tools—which can recognize our face, gait, speech, and behavioral patterns—data rights and governance become critical. Terms of service that gain user consent one time, upon sign-up, are no longer sufficient. We need better social contracts that have informed consent baked into the products themselves and can be adjusted as user preferences change over time.

We need to ensure that the industry has strong ethical underpinning as it brings these monitoring and surveillance tools into the mainstream. Inspired by the Hippocratic Oath—a symbolic promise to provide care in the best interest of patients—a number of security researchers have drafted a new version for Connected Medical Devices.

With more effective regulations, increased commercial activity, and strong governance, software-driven medical products are poised to change healthcare delivery. At this rate, apps and algorithms have the opportunity to augment doctors and complement—or even replace—drugs sooner than we think.

Powered by WPeMatico

Microsoft today announced that it has acquired BlueTalon, a data privacy and governance service that helps enterprises set policies for how their employees can access their data. The service then enforces those policies across most popular data environments and provides tools for auditing policies and access, too.

Neither Microsoft nor BlueTalon disclosed the financial details of the transaction. Ahead of today’s acquisition, BlueTalon had raised about $27.4 million, according to Crunchbase. Investors include Bloomberg Beta, Maverick Ventures, Signia Venture Partners and Stanford’s StartX fund.

“The IP and talent acquired through BlueTalon brings a unique expertise at the apex of big data, security and governance,” writes Rohan Kumar, Microsoft’s corporate VP for Azure Data. “This acquisition will enhance our ability to empower enterprises across industries to digitally transform while ensuring right use of data with centralized data governance at scale through Azure.”

Unsurprisingly, the BlueTalon team will become part of the Azure Data Governance group, where the team will work on enhancing Microsoft’s capabilities around data privacy and governance. Microsoft already offers access and governance control tools for Azure, of course. As virtually all businesses become more data-centric, though, the need for centralized access controls that work across systems is only going to increase and new data privacy laws aren’t making this process easier.

“As we began exploring partnership opportunities with various hyperscale cloud providers to better serve our customers, Microsoft deeply impressed us,” BlueTalon CEO Eric Tilenius, who has clearly read his share of “our incredible journey” blog posts, explains in today’s announcement. “The Azure Data team was uniquely thoughtful and visionary when it came to data governance. We found them to be the perfect fit for us in both mission and culture. So when Microsoft asked us to join forces, we jumped at the opportunity.”

Powered by WPeMatico

Bounce, a Bangalore-based startup that offers thousands of electric scooters for rent in India, has raised $72 million to accelerate its bid to impact how people navigate India’s traffic-clogged urban areas.

The Series C funding round for the five-year-old startup was led by B Capital — the VC firm founded by Facebook co-founder Eduardo Saverin — and Falcon Edge Capital. Chiratae Ventures, Maverick Ventures, Omidyar Network India, Qualcomm Ventures and existing investors Sequoia Capital India and Accel Partners India also participated in the round.

This new money means that the startup has raised $92 million to date. The current round valued it at more than $200 million, a person familiar with the matter said.

Bounce, formerly known as Metro Bikes, operates in Bangalore. Its app allows users to pick up a scooter and, when their ride is finished, drop it off at any parking spot. It charges customers based on the time and model of electric scooter they choose. An hour-long ride could cost as little as Rs 15 (21 cents). The startup claims it has already clocked two million rides.

Vivekananda Hallekere, co-founder and CEO of Bounce, told TechCrunch in an interview that the startup plans to use the fresh capital to add more than 50,000 electric scooters to its fleet by the end of the year, up from its current mix of 5,000 electric and gasoline scooters. Additionally, Bounce, which employs about 200 people, plans to enter more cities in India and invest in growing its tech infrastructure and head count.

“We have about 10 metro and non-metro cities in mind. Starting next quarter, we will start to expand in those cities,” he said. The startup also aims to service one million rides in the next year.

Hallekere said Bounce, which currently offers IoT hardware and design for the scooters, is also working on building its own form factor for scooters.

The rise of Bounce comes as it bets that shared two-wheeler vehicles — already a common mode of transportation in the nation — will play an important role in the future of ridesharing, with electric vehicles replacing petrol ones.

This bet has gained more momentum in recent years. Startups such as Yulu, which partnered with Uber earlier this year to conduct a trial in Bangalore; Vogo, which raised money from Uber rival Ola; and Ather Energy have expanded their businesses and gained the backing of major investors.

Their adoption, though still in their nascent stages, is increasingly proving that for millions of people, rides from Uber and Ola are just too expensive for their wallets. Besides, in jam-packed traffic in Bangalore and Delhi and other cities in India, two wheels are more efficient than four.

Powered by WPeMatico

Redpoint Ventures has led a $65 million Series B in Cityblock, a healthcare company focused on providing improved care to low-income neighborhoods.

The business launched roughly 18 months ago out of Alphabet’s Sidewalk Labs, an urban innovation incubator known for projects like mobility data startup Coord, which itself raised a $5 million round in October.

“We’re a tech-enabled services company focused on caring for a population that has been traditionally overlooked by the innovation community and generally underserved across healthcare,” co-founder and chief executive officer Iyah Romm told TechCrunch. “We believe we can fundamentally redefine the way that health services are built across the country for low-income populations. These are populations that have never been prioritized.”

Romm has spent his entire career in the public health sector. Prior to joining Sidewalk Labs as an entrepreneur-in-residence in 2017, he spent one year as the chief transformation officer of the Commonwealth Care Alliance, a nonprofit medical care delivery organization.

Cityblock provides personalized medical and behavioral health and social services across a growing number of clinics on the East Coast. The company will use the investment to open additional clinics and continue the development of its core platform, Commons. The care delivery platform helps care workers collaborate and stay up to date on patients, with real-time hospital admission alerts to tools for tracking treatment progress.

Cityblock opened its first clinic, or “neighborhood hub,” in Brooklyn, New York after forging a partnership with EmblemHealth, a New York neighborhood health insurance business. They’ve since expanded to Connecticut via a partnership with ConnectiCare, a Connecticut insurance provider. Cityblock will open clinics in North Carolina later this year. Cityblock’s services come at no additional costs to members covered by partner insurance businesses.

The startup’s hope is to get these low-income demographics regular access to more affordable care. Preventative care, after all, is a whole lot cheaper than emergency room visits.

“People end up going to the ER when problems are really bad, for conditions that can be managed,” Redpoint partner and newly appointed Cityblock board member Elliot Geidt told TechCrunch. “There are 75 million people on Medicaid alone and a good portion of these people are living in the inner cities. It’s a problem that has a scope larger than most things that we see in the venture community. The big problem with this population is the existing healthcare system doesn’t work for them, it falls short on so many levels.”

New investors 8VC, Echo Health Ventures and StartUp Health also participated in the latest round, as did existing investors including Sidewalk Labs, Thrive Capital, Maverick Ventures, Town Hall Ventures and EmblemHealth.

Powered by WPeMatico

We’re three weeks into January. We’ve recovered from our CES hangover and, hopefully, from the CES flu. We’ve started writing the correct year, 2019, not 2018.

Venture capitalists have gone full steam ahead with fundraising efforts, several startups have closed multi-hundred million dollar rounds, a virtual influencer raised equity funding and yet, all anyone wants to talk about is Slack’s new logo… As part of its public listing prep, Slack announced some changes to its branding this week, including a vaguely different looking logo. Considering the flack the $7 billion startup received instantaneously and accusations that the negative space in the logo resembled a swastika — Slack would’ve been better off leaving its original logo alone; alas…

On to more important matters.

Rubrik more than doubled its valuation

The data management startup raised a $261 million Series E funding at a $3.3 billion valuation, an increase from the $1.3 billion valuation it garnered with a previous round. In true unicorn form, Rubrik’s CEO told TechCrunch’s Ingrid Lunden it’s intentionally unprofitable: “Our goal is to build a long-term, iconic company, and so we want to become profitable but not at the cost of growth,” he said. “We are leading this market transformation while it continues to grow.”

Deal of the week: Knock gets $400M to take on Opendoor

Will 2019 be a banner year for real estate tech investment? As $4.65 billion was funneled into the space in 2018 across more than 350 deals and with high-flying startups attracting investors (Compass, Opendoor, Knock), the excitement is poised to continue. This week, Knock brought in $400 million at an undisclosed valuation to accelerate its national expansion. “We are trying to make it as easy to trade in your house as it is to trade in your car,” Knock CEO Sean Black told me.

While we’re on the subject of VCs’ favorite industries, TechCrunch cybersecurity reporter Zack Whittaker highlights some new data on venture investment in the industry. Strategic Cyber Ventures says more than $5.3 billion was funneled into companies focused on protecting networks, systems and data across the world, despite fewer deals done during the year. We can thank Tanium, CrowdStrike and Anchorfree’s massive deals for a good chunk of that activity.

Send me tips, suggestions and more to kate.clark@techcrunch.com or @KateClarkTweets.

I would be remiss not to highlight a slew of venture firms that made public their intent to raise new funds this week. Peter Thiel’s Valar Ventures filed to raise $350 million across two new funds and Redpoint Ventures set a $400 million target for two new China-focused funds. Meanwhile, Resolute Ventures closed on $75 million for its fourth early-stage fund, BlueRun Ventures nabbed $130 million for its sixth effort, Maverick Ventures announced a $382 million evergreen fund, First Round Capital introduced a new pre-seed fund that will target recent graduates, Techstars decided to double down on its corporate connections with the launch of a new venture studio and, last but not least, Lance Armstrong wrote his very first check as a VC out of his new fund, Next Ventures.

More money goes toward scooters

In case you were concerned there wasn’t enough VC investment in electric scooter startups, worry no more! Flash, a Berlin-based micro-mobility company, emerged from stealth this week with a whopping €55 million in Series A funding. Flash is already operating in Switzerland and Portugal, with plans to launch into France, Italy and Spain in 2019. Bird and Lime are in the process of raising $700 million between them, too, indicating the scooter funding extravaganza of 2018 will extend into 2019 — oh boy!

TechCrunch’s Josh Constine introduced readers to Squad this week, a screensharing app for social phone addicts.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase editor-in-chief Alex Wilhelm and I marveled at the dollars going into scooter startups, discussed Slack’s upcoming direct listing and debated how the government shutdown might impact the IPO market.

Powered by WPeMatico

Devoted Health, a Waltham, Mass.-based insurance startup, has raised a $300 million Series B and is enrolling to its Medicare Advantage plan members in eight Florida counties.

The company, which helps Medicare beneficiaries access care through its network of physicians and tech-enabled healthcare platform, has raised the funds from lead investor Andreessen Horowitz, Premji Invest and Uprising.

The company declined to disclose its valuation.

Devoted’s founders are brothers Todd and Ed Park — the company’s executive chairman and chief executive officer, respectively. Todd co-founded a pair of now publicly traded companies, Athenahealth, a provider of electronic health record systems, and health benefits platform Castlight Health. He also served as the U.S. chief technology officer during the Obama administration. Ed, for his part, was the chief operating officer of Athenahealth until 2016 and a member of Castlight’s board of directors for several years.

Venrock partners Bryan Roberts — Devoted’s founding investor — and Bob Kocher — its chief medical officer — are also part of the company’s founding team.

The Park brothers have tapped Jeremy Delinsky, the former CTO at Wayfair and Athenahealth, as COO; DJ Patil, a former data scientist at the White House, as its head of technology; and Adam Thackery, the former CFO of Universal American, as its chief financial officer.

Its board includes former Health and Human Services Secretary Kathleen Sebelius and former Senate Majority Leader Bill Frist. As part of the latest round, a16z’s Vijay Pande will join its board, too.

The company says it’s committed to treating its customers as if they were members of its employees’ own families. For Patil, the startup’s head of tech, that’s made the entire process of building Devoted a very emotional one.

“I’ve cried a lot at this company,” Patil told TechCrunch. “You meet these seniors and they’ve done everything right. They’ve worked so incredibly hard their entire lives. They’ve given it their all for the American dream. They’ve paid into this model of healthcare and they deserve better.”

Devoted, which previously raised $69 million across two financing rounds in 2017 from Oak HC/FT, Venrock, F-Prime Capital Partners, Maverick Ventures and Obvious Ventures, has begun enrolling to its Medicare Advantage plan seniors located in Broward, Hillsborough, Miami-Dade, Osceola, Palm Beach, Pinellas, Polk and Seminole counties. It will begin providing care January 1, 2019.

Its long-term goal is to offer insurance plans to seniors nationwide.

“We are responsible for these people’s healthcare, so we need to get it right,” Patil said.

Powered by WPeMatico