MassChallenge

Auto Added by WPeMatico

Auto Added by WPeMatico

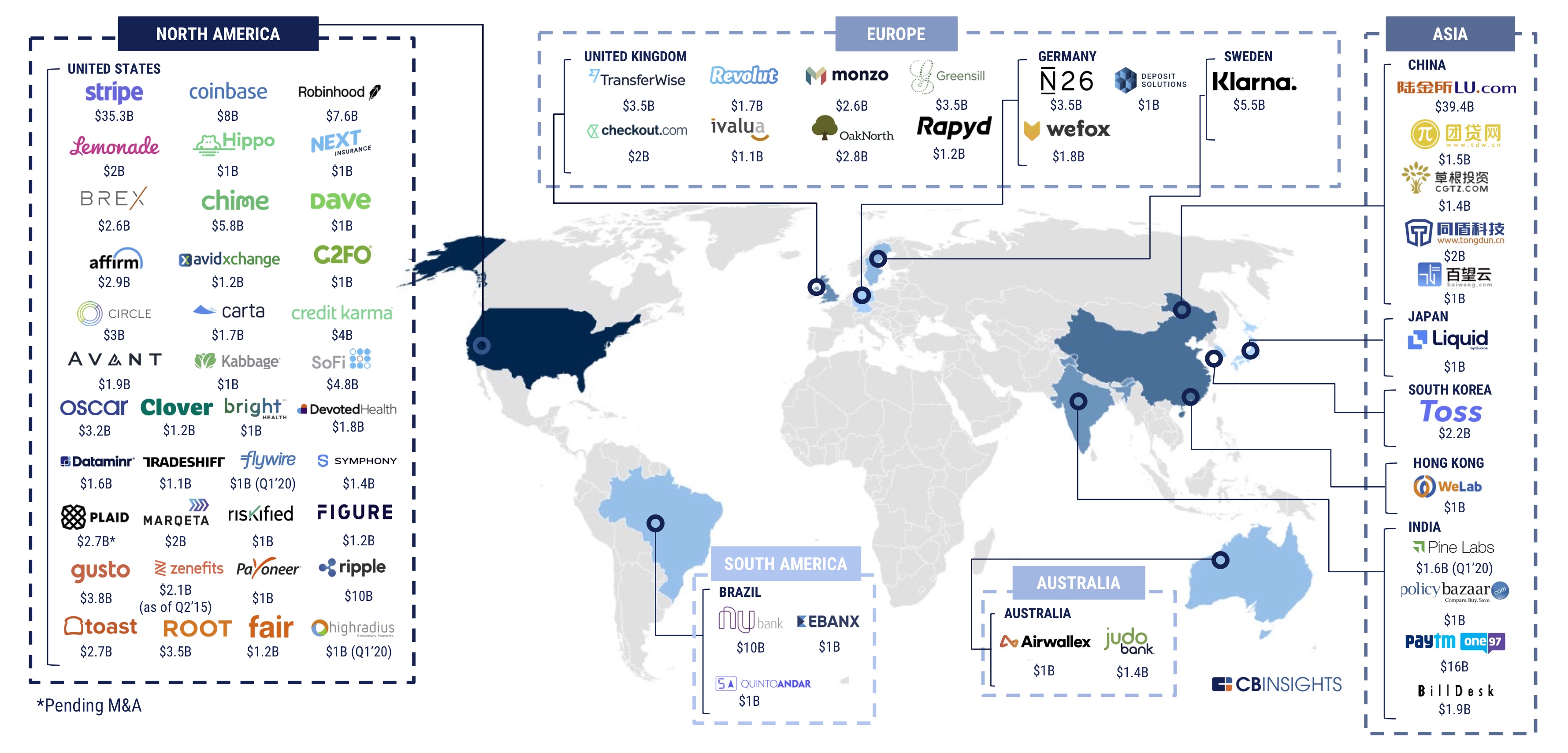

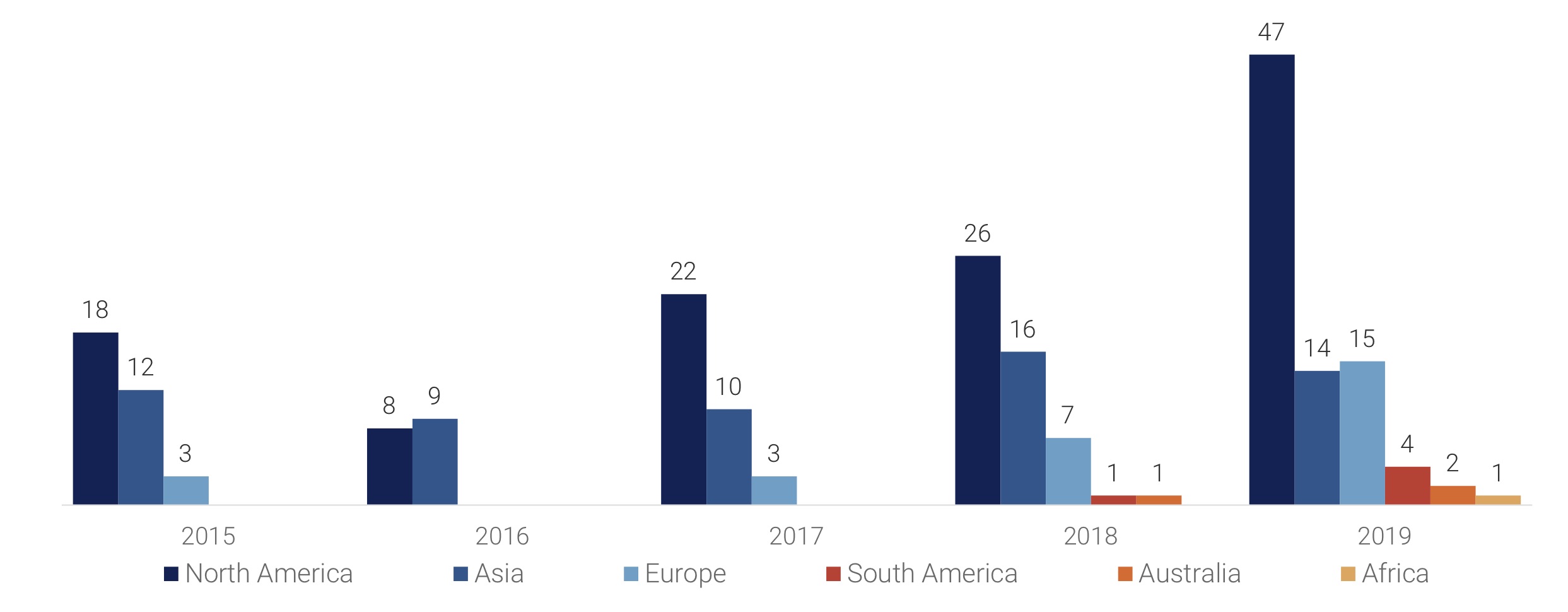

Financial services startups raised less money in 2019 than they did in 2018 as VC firms looked to back late stage firms and focused on developing markets, a new report has revealed.

According to research firm CB Insights’ annual report published this week, fintech startups across the world raised $33.9 billion* in total last year across 1,912 deals*, down from $40.8 billion they picked up by participating in 2,049 deals the year before.

It’s a comprehensive report, which we recommend you read in full here (your email is required to access it), but below are some of the key takeaways.

Early-stage deals dropped to a 12-quarter low as deal share globally shifts to mid- and late-stages (CB Insights)

The fintech market globally today has 67 unicorns as of earlier this month (CB Insights)

2019 saw 83 mega-rounds totaling $17.2B, a record year in every market except Europe

*CB Insights report includes a $666 million financing round of Paytm . It was incorrectly reported by some news outlets and the $666 million raise was part of the $1 billion round the Indian startup had revealed weeks prior. We have adjusted the data accordingly.

Powered by WPeMatico

Ginkgo Bioworks is now worth $4 billion after a $290 million capital infusion that will give the company the cash to dramatically expand its developer shop for genetic programming.

The Boston-based company is one of a handful of U.S.-based early-stage companies that are on the forefront of developing the tools to modify genetic material for everyday applications.

“Cells are programmable similar to computers because they run on digital code in the form of DNA,” said Jason Kelly, CEO and co-founder of Ginkgo Bioworks, in a statement. “Ginkgo has the best compiler and debugger for writing genetic code and we use it to program cells for customers in a range of industries. Today’s fundraise will allow us to expand our technology and continue our drive to bring biology into every physical goods industry — materials, clothing, electronics, food, pharmaceuticals and more. They are all biotech industries but just don’t know it yet.”

Ginkgo makes money in two ways. The company sells its development services to anyone who comes in with an idea. Kelly said that it’d be like any agreement with an entrepreneur who hires a coding shop to develop an application.

For example, if an entrepreneur wanted to develop houseplants that smelled like roses or lilies, they could approach Ginkgo, pay a (not-insignificant) fee and Ginkgo would do the research into designing something like a lily-scented fern. (Kelly puts the sticker price on that kind of development somewhere in the neighborhood of $10 million, so a founder best believe their product can sell.)

“You don’t need to come in with deep biological know-how,” Kelly says. “The question is, is capital interested in the problem?”

The other way that Ginkgo is approaching the market is by taking equity stakes in businesses that rely on its technology.

Those take the form of joint ventures with companies like Bayer (the first joint venture partner for Ginkgo) and the launch of Joyn, a $100 million spin-out that was created in the summer of 2018.

The two companies are collaborating on the development of seeds that require less fertilizer for growth — something that could save the industry millions and decrease pollution associated with traditional chemical fertilizers.

Since that first spin-out, Ginkgo has created three other companies and joint ventures. There’s the $122 million deal to produce rare cannabinoids with the Canadian cannabis company, Cronos; a partnership with Roche that was born out of Ginkgo’s acquisition of Warp Drive Bio; and Motif Foodworks, which is working on manufacturing alternative proteins with a $120 million in financing.*

Alongside these large-scale initiatives, Ginkgo has signed partnerships with the West Coast powerhouse accelerator program from Y Combinator and a new Boston-based life sciences-focused group called Petri to conduct development work for startups from those programs in exchange for an equity stake.

“We’re not going to have all the good ideas,” says Kelly. “We want to tap the much larger pool of smart people and really have them building on our platform. Of all of the people we can give value to, we can give the most to startups. If we can offer them to do their biowork without all of the fixed costs of building a lab,” that’s valuable, he says.

Investors in the company include Y Combinator, DCVC, MassChallenge, Felicis Ventures, General Atlantic, Baillie Gifford, Bill Gates and Viking Global.

Powered by WPeMatico

This guest post was written by David Teten, Venture Partner, HOF Capital. You can follow him at teten.com and @dteten. This is part of an ongoing series on revenue-based investing VC that will hit on:

A new wave of revenue-based investors are emerging who are using creative investing structures with some of the upside of traditional VC, but some of the downside protection of debt.

I’ve been a traditional equity VC for 8 years, and I’m researching new business models in venture capital. As I’ve learned about this model, I’ve been impressed by how these venture capitalists are accomplishing a major social impact goal… without even trying to.

Many are reporting that they’re seeing a more diverse pool of applicants than traditional equity VCs — even though virtually none have a particular focus on women or underrepresented founders. In addition, their portfolios look far more diverse than VC industry norms.

For context, revenue-based investing (“RBI”) is a new form of VC financing, distinct from the preferred equity structure most VCs use. RBI normally requires founders to pay back their investors with a fixed percentage of revenue until they have finished providing the investor with a fixed return on capital, which they agree upon in advance. For more background, see “Revenue-based investing: A new option for founders who care about control“.

I contacted every RBI venture capital investor I could identify, and learned:

By contrast, according to PitchBook Data, since the beginning of 2016, companies with women founders have received only 4.4% of venture capital deals. Those companies have garnered only about 2% of all capital invested. This is despite the fact that the data says that in fact you’re better off investing in women.

Paul Graham href=”http://www.paulgraham.com/bias.html”> observes, “many suspect that venture capital firms are biased against female founders. This would be easy to detect: among their portfolio companies, do startups with female founders outperform those without?

A couple months ago, one VC firm (almost certainly unintentionally) published a study showing bias of this type. First Round Capital found that among its portfolio companies, startups with female founders outperformed those without by 63%.”

Image via Getty Images / runeer

Why are RBI investors investing disproportionately in women & underrepresented founders, and vice versa: why do these founders approach RBI investors?

I’d argue it’s not that RBI is so unbiased and attractive; it’s that traditional equity VC is biased structurally against some women and underrepresented founders.

The Boston Consulting Group and MassChallenge, a US-based global network of accelerators, partnered to study why “women-owned startups are a better bet”. Through their analysis and interviews, BCG identified three primary reasons why female founders are less likely to receive VC funds.

The study used multivariate regression analysis to control for education levels and pitch quality to conclude that gender was a statistically significant factor. I argue that these 3 reasons are much less applicable for RBI investors than for conventional VCs.

Traditional equity VCs are looking for high-risk, high-reward, “swing for the fences” models. The founders of such companies inherently are taking financial risk, reputational risk, and career risk.

Paul Graham, co-founder of Y Combinator, said, “few successful founders grew up desperately poor.” Ricky Yean, a serial founder, agrees: “building and sustaining a company that is “designed to grow fast” is especially hard if you grew up desperately poor”.

Most of the founders of the paradigmatic VC home runs were privileged: male, cisgender, well-educated, from affluent families, etc. Think Bill Gates and Mark Zuckerberg .

That privilege makes it easier for them to take very high risk. The average person, worried about students loans and long term employability, quite rationally is less likely to take the huge risk of founding a company. It’s far safer to just get a job.

Investors who back diverse teams can win much higher returns than the industry norm. Both RBI investors and the founders they back will hopefully benefit from this pattern.

Note that none of the lawyers quoted or I are rendering legal advice in this article, and you should not rely on our counsel herein for your own decisions. I am not a lawyer. Thanks to the experts quoted for their thoughtful feedback.

Powered by WPeMatico

Lausanne, a small town in the Western part of Switzerland, has emerged as a surprising melting pot of innovative technology, and the latest feather in the town’s tech nest will be hosting the first Swiss chapter of MassChallenge. A large Boston-based accelerator program that is rapidly expanding across the globe, MassChallenge is a nonprofit and does not take an equity stake in… Read More

Lausanne, a small town in the Western part of Switzerland, has emerged as a surprising melting pot of innovative technology, and the latest feather in the town’s tech nest will be hosting the first Swiss chapter of MassChallenge. A large Boston-based accelerator program that is rapidly expanding across the globe, MassChallenge is a nonprofit and does not take an equity stake in… Read More

Powered by WPeMatico

Last year as I was visiting colleges with my son, I noticed schools often had facilities to train students with a distinctly 20th century bent, but lacked the modern skills training students will need in today’s highly competitive and shifting job market. Early-stage startup, Gradberry, which comes out of beta this week, wants to fix that by teaming with employers and graduates and… Read More

Last year as I was visiting colleges with my son, I noticed schools often had facilities to train students with a distinctly 20th century bent, but lacked the modern skills training students will need in today’s highly competitive and shifting job market. Early-stage startup, Gradberry, which comes out of beta this week, wants to fix that by teaming with employers and graduates and… Read More

Powered by WPeMatico