Mark Suster

Auto Added by WPeMatico

Auto Added by WPeMatico

Though 2021 is far from over, it’s already witnessed a record level of venture capital activity in the technology sector. With larger round sizes announced daily, founders may have their pick of term sheets — but they need to think critically and strategically about which firms to add to their cap table.

So far this year, we’ve seen $292.4 billion in venture financing across the globe, of which $138.9 billion was raised in the United States. Specific to tech companies, the capital is only accelerating: In Q2, founders raised 157% more capital compared to the same period last year, according to the latest data from CB Insights.

It’s not just that more companies are raising money — they are doing so at a higher valuation. Median seed and Series A stage valuations today stand at $12 million and $42 million, respectively, up 20% to 30% from 2020. This can be partly attributed to growing exits/M&A activity in the technology sector, a record number of IPOs and a general bullishness around technology, as well as low interest rates and liquidity in the market.

Good VCs who are aligned with a startup’s vision create more value than the dollars they bring to the table.

At a time when we are witnessing record VC activity, founders would be well served to go back to the basics and focus on the principles of fundraising when determining who sits on their cap table. Here are a few pointers for founders in that direction:

Good VCs who are aligned with a startup’s vision create more value than the dollars they bring to the table. Typically, such value is created across a few distinct functions — product, sales, domain expertise, business development and recruiting, to name a few — based on the background of the partners of the fund and the composition of their limited partners (investors in the venture fund).

Further, the right VC can serve as an authentic, objective sounding board for CEOs, which can be an asset to have as a startup navigates uncertainty and the typical challenges that come with scaling a young company. As founders assess multiple term sheets, it’s worth thinking through whether they should optimize for VCs who offer the highest valuation, or for ones who bring the most value to the table.

Running an efficient fundraising process, in part, entails holding VCs accountable to their own diligence requests. While it is unfortunately common for VCs to request a lot of data upfront, startups should share information after assessing intent and appetite on the investors’ part.

For every additional data request, founders are well within their rights (and should) check with their potential investors on where the process stands and get indicative timelines for moving forward with next steps. Mark Suster said it best: “Data rooms are where fundraising processes go to die.”

Powered by WPeMatico

Startups have done some wild things to get the attention of VCs. In fact, Instacart founder Apoorva Mehta sent YC partner (at the time) Garry Tan a six-pack of beer through the service after missing the deadline for Y Combinator by two months.

Yesterday, the ingenuity of startups struck again.

Tadabase.io, an enterprise startup that offers no-code tools to help businesses automate their processes, has had an ad running that was… well, hyper targeted.

ProductHunt founder and WeekendFund investor Ryan Hoover discovered the ad and shared it on Twitter.

I google’d @msuster’s LinkedIn and this is what I found

pic.twitter.com/ANMZ2dg6AD

— Ryan Hoover (@rrhoover) March 13, 2020

Hoover told TechCrunch he was Googling Mark Suster to facilitate an introduction between Suster and one of Hoover’s portfolio companies. Instead, he found a Google ad directed squarely at Suster from Tadabase.io.

“Mark Suster, you haven’t invested in nocode” read the paid listing. “Therefore, we put this ad here to get your attention. If you’re not Mark, please don’t click here and save us some money.”

I reached out to Suster, managing partner at UpFront Ventures, to see what he thought of the ad. He told me he “loved it” and has already contacted the CEO to set up a call for next week.

Whether this clever Google ad will result in an actual investment is yet to be determined. Also unclear: will Ryan Hoover get in on the deal?

I reached out to Tadabase founder and CEO Moe Levine via email to ask about the ad, how they went about targeting, and how he feels about his upcoming phone call next week. He hasn’t responded yet. I’ll update if/when he does.

Powered by WPeMatico

When “Law & Order” ended its 20-year run in 2010, it had already cemented its place as one of the longest-running television dramas in history. Its success was a testament to the enduring popularity of a good mystery.

Mining that same well of a demand for whodunnits, a roughly one-year-old Los Angeles-based startup called Solve has raised $20 million in financing to update the genre for a new generation of media consumers.

Its eponymously titled social media programming, available on Instagram and Snap, has managed to nab roughly 30 million interactions over the year-and-a-half that it distributed its productions. Now the company is launching a true crime podcast on the iHeartMedia and Apple platforms to tap into another potentially high-growth market.

Solve began as a series developed within the mobile-focused entertainment studio, Vertical Networks. Helmed by Tom Wright and financed by Elisabeth Murdoch (through her Freelands Ventures fund, which Wright also managed) and Snap, the company was one of the early entrants to raise cash as a production studio for mobile content. But it was far from the only studio to see money in mobile-first entertainment. All of the major internet-age media companies had their own mobile strategies.

Murdoch eventually replaced Wright (so that he could work on spinning up Solve as an independent entity) and sold Vertical Networks two months ago to the online media startup, Whistle, for an undisclosed amount.

“I spent a year looking deep, deep, deep into audience behavioral data on Snap and Facebook,” Wright says. “The DNA of what I thought [audience] sensibilities was leading towards was this format.”

As Vertical Networks was winding down, Solve was spinning up with help from Lightspeed Venture Partners, Upfront Ventures and Advancit Capital.

“We’ve seen incredibly popular crime mystery shows across media, including podcasts like Serial and Dirty John, TV shows like Making a Murderer and Law & Order, and movies like The Usual Suspects and Gone Girl,” said Jeremy Liew, partner at Lightspeed Venture Partners, in a statement. “Games have attained a first class status as media but we’ve yet to see a crime mystery format game achieve the same success, and Solve is going to right that wrong.”

The gamification element that’s made Solve’s episodes resonate with mobile audiences on social platforms will be a small part of the initial series, says Wright, with plans to expand the interactive elements going forward.

Produced in partnership with SALT audio, whose previous work includes “Blackout” and “Carrier” and iHeartMedia, the 10-episode series uses the same “ripped from the headlines” storytelling for its 30-minute broadcasts and offers listeners clues in leaked audio files, voicemails, courtroom testimony and other evidence to try to guess the killer.

For now, Solve is content to be a studio producing ad-supported media for platforms like Apple, Snap, Facebook, iHeartMedia and other distributors, according to Wright. It’s a different path than studios like Quibi, which is creating its own streaming service dedicated to mobile storytelling and backed by many of the major Hollywood studios.

The current pace of production means that Solve is making 18 original episodes per month. For the 40-year-old Wright, Solve represents a fourth foray into the world of startups. And while he’s not a fan of the crime or mystery genre himself, Wright said that the data around engagement was too compelling to not try to launch a business around it.

“The Internet has changed how we interact with the world from taxis to news to shopping. We believe that Solve can fundamentally change how we interact with narrative video storytelling,” said Mark Suster, managing partner, Upfront Ventures, in a statement. “When we heard Tom’s vision for short-form video that you not only watch but also must ‘solve‘, we knew that it had enormous potential.”

Powered by WPeMatico

In the context of a term sheet, pro rata rights (or pro rata) govern whether investors may continue to invest in subsequent rounds of funding in proportion with their ownership. Investors with pro rata rights can invest in the company’s next round an amount that will allow them to maintain their ownership percentage.

This is an excerpt from the Holloway Guide to Raising Venture Capital, a comprehensive resource for founders of early-stage startups, covering technical details, practical knowledge, real-world scenarios, and pitfalls to avoid. Read our accompanying article about the company over on TechCrunch.

Pro rata is Latin for “in proportion.” Most people are familiar with the concept of prorating from dealing with landlords: if you’re entering into a lease halfway through the month, your rent may be prorated, where you pay an amount of the rent that is in proportion to your time actually occupying the property.

Almost all investors try to negotiate for pro rata rights, because if a company is doing well they want to own as much of it as possible. After all, why not double down on a winner than use that same money to invest in a newer, unproven company? In the 2018–2019 fundraising climate, though, it’s safe to say we’re at “peak pro rata.” Everybody wants pro rata, even those who don’t entirely understand how it works or affects companies.

Some founders include a major investor clause in the term sheet, which reserves certain rights and privileges to those they deem “major investors,” based on amount invested or number of shares purchased. Whether to grant pro rata rights to all investors or only those above a major investor threshold is a tricky decision for two reasons.

Powered by WPeMatico

Upfront Ventures, a Los Angeles-based venture capital firm, has filed paperwork with the U.S. Securities and Exchange Commission to raise its third growth-stage investment fund.

Though the firm typically invests at the seed and Series A, capital from Upfront Growth III will be used for follow-on or late-stage deals.

The firm, known for its investments in Bird, Goat, Ring, ThredUP and Parachute, plans to raise $250 million for the effort. Mark Suster and Yves Sisteron, listed on the filing, lead the firm as managing partners. Upfront’s investor line-up also includes partners Kobie Fuller, Greg Bettinelli, Kara Nortman and Kevin Zhang.

One of the oldest VCs rooted in LA, Upfront previously closed on $400 million for its sixth flagship early-stage fund in 2017.

LA is on pace for a banner year of VC investment, attracting $33 billion across more than 1,000 deals already in 2019, according to PitchBook. Last year, companies headquartered in LA raised more than $60 billion.

Powered by WPeMatico

Three years ago, I met with a founder who had raised a massive seed round at a valuation that was at least five times the market rate. I asked what firm made the investment.

She said it was not a traditional venture firm, but rather a strategic investor that not only had no ties to her space but also had no prior investment experience. The strategic investor, she said, was looking to “get their hands dirty” and “get in on the ground floor.”

Over the next 2 years, I kept a close eye on the founder. Although she had enough capital to pivot her business focus multiple times, she seemed to be at odds, serving the needs of her strategic investor and her customer base.

Ultimately, when the business needed more capital to survive, the strategic investor didn’t agree with the founder’s focus, opted not to prop it up, and the business had to shut down.

Sadly, this is not an uncommon story as examples abound of strategic investors influencing startup direction and management decisions to the point of harm for the startup. Corporate strategics, not to be confused with dedicated funds focused on financial returns like a traditional venture investor like Google Ventures, often care less about return on investment, and more about a startup’s focus, and sector specificity. If corporate imperatives change, the strategic may cease to be the right partner or could push the startup in a challenging direction.

And yet, fortunately, as the disruptive power of technology is being unleashed on nearly every major industry, strategic investors are now getting smarter, both in terms of how they invest and how they partner with entrepreneurs.

From making strong acquisitive plays (i.e. GM’s purchase of Cruise Automation or Toyota’s early-stage investment in Uber) to building dedicated funds, to executing commercial agreements in tandem with capital investment, strategics are getting savvier, and by extension, becoming better partners. In some instances, they may be the best partner.

Negotiating a term sheet with a strategic investor necessitates a different set of considerations. Namely: the preference for a strategic to facilitate commercial milestones for the startup, a cautious approach to avoid the “over-valuation” trap, an acute focus on information rights, and the limitation of non-compete provisions.

Powered by WPeMatico

Mark Suster of Upfront Ventures bonded with Trevor O’Brien in prison. The pair, Suster was quick to clarify, were on site at a correctional facility in 2017 to teach inmates about entrepreneurship as part of a workshop hosted by Defy Ventures, a nonprofit organization focused on addressing the issue of mass incarceration.

They hit it off, sharing perspectives on life and work, Suster recounted to TechCrunch. So when O’Brien, a former director of product management at Twitter, mentioned he was in the early days of building a startup, Suster listened.

Less than two years later, O’Brien is ready to talk about the idea that captured the attention of the Bird, FabFitFun and Ring investor. It’s called Projector.

It’s the brainchild of a product veteran (O’Brien) and a gaming industry engineer turned Twitter’s vice president of engineering (Projector co-founder Jeremy Gordon), a combination that has given way to an experiential and well-designed platform. Projector is browser-based, real-time collaborative design software tailored for creative teams that feels and looks like a mix of PowerPoint, Google Docs and Instagram . Though it’s still months away from a full-scale public launch, the team recently began inviting potential users to test the product for bugs.

“We want to reimagine visual communication in the workplace by building these easier to use tools and giving creative powers to the non-designers who have great stories to tell and who want to make a difference,” O’Brien told TechCrunch. “They want change to happen and they need to be empowered with the right kinds of tools.”

Today, Projector is a lean team of 13 employees based in downtown San Francisco. They’ve kept quiet since late 2016 despite closing two rounds of venture capital funding. The first, a $4 million seed round, was led by Upfront’s Suster, as you may have guessed. The second, a $9 million Series A, was led by Mayfield in 2018. Hunter Walk of Homebrew, Jess Verrilli of #Angels and Nancy Duarte of Duarte, Inc. are also investors in the business, among others.

O’Brien leads Projector as chief executive officer alongside co-founder and chief technology officer Gordon. Years ago, O’Brien was pursuing a PhD in computer graphics and information visualization at Brown University when he was recruited to Google’s competitive associate product manager program. He dropped out of Brown and began a career in tech that would include stints at YouTube, Twitter, Coda and, finally, his very own business.

O’Brien and Gordon crossed paths at Twitter in 2013 and quickly realized a shared history in the gaming industry. O’Brien had spent one year as an engineer at a games startup called Mad Doc Software, while Gordon had served as the chief technology officer at Sega Studios. Gordon left Twitter in 2014 and joined Redpoint Ventures as an entrepreneur-in-residence before O’Brien pitched him on an idea that would become Projector.

Projector co-founders Jeremy Gordon (left), Twitter’s former vice president of engineering, and Trevor O’Brien, Twitter’s former director of product management

“We knew we wanted to create a creative platform but we didn’t want to create another creative platform for purely self-expression, we wanted to do something that was a bit more purposeful,” O’Brien said. “At the end of the day, we just wanted to see good ideas succeed. And with all of those good ideas, succeeding typically starts with them being presented well to their audience.”

Initially, Projector is targeting employees within creative organizations and marketing firms, who are frequently tasked with creating visually compelling presentations. The tool suite is free for now and will be until it’s been sufficiently tested for bugs and has fully found its footing. O’Brien says he’s not sure just yet how the team will monetize Projector, but predicts they’ll adopt Slack’s per user monthly subscription pricing model.

As original and user-friendly as it may be, Projector is up against great competition right out of the gate. In the startup landscape, it’s got Canva, a graphic design platform valued at $2.5 billion earlier this week with a $70 million financing. On the old-guard, it’s got Adobe, which sells a widely used suite of visual communication and graphic design tools. Not to mention Prezi, Figma and, of course, Microsoft’s PowerPoint, which is total crap but still used by millions of people.

“There are many tools scratching at the surface, but there’s not one visual communications tool that wins them all,” Suster said of his investment in Projector.

Projector is still in its very early days. The company currently has just two integrations: Unsplash for free stock images and Giphy for GIFs. O’Brien would eventually like to incorporate iconography, typography and sound to liven up Projector’s visual presentation capabilities.

The ultimate goal, aside from generally improving workplace storytelling, is to make crafting presentations fun, because shouldn’t a corporate slideshow or even a startup’s pitch be as entertaining as scrolling through your Instagram feed?

“We wanted to try to create something that doesn’t feel like work,” O’Brien said.

Powered by WPeMatico

Did anyone else listen to season one of StartUp, Alex Blumberg’s OG Gimlet podcast? I did, and I felt like a proud mom this week reading stories of the major, first-of-its-kind Spotify acquisition of his podcast production company, Gimlet. Spotify also bought Anchor, a podcast monetization platform, signaling a new era for the podcasting industry.

On top of that, Himalaya, a free podcast app I’d never heard of until this week, raised a whopping $100 million in venture capital funding to “establish itself as a new force in the podcast distribution space,” per Variety.

The podcasting business definitely took center stage, but Lime and Bird made headlines, as usual, a new unicorn emerged in the mental health space and Instacart, it turns out, has been screwing its independent contractors.

As mentioned, Spotify, or shall we say Spodify, gobbled up Gimlet and Anchor. More on that here and a full analysis of the deal here. Key takeaway: it’s the dawn of podcasting; expect a whole lot more venture investment and M&A activity in the next few years.

This week’s biggest “yikes” moment was when reports emerged that Instacart was offsetting its wages with tips from customers. An independent contractor has filed a class-action lawsuit against the food delivery business, claiming it “intentionally and maliciously misappropriated gratuities in order to pay plaintiff’s wages even though Instacart maintained that 100 percent of customer tips went directly to shoppers.” TechCrunch’s Megan Rose Dickey has the full story here, as well as Instacart CEO’s apology here.

Slack confidentially filed to go public this week, its first public step toward either an IPO or a direct listing. If it chooses the latter, like Spotify did in 2018, it won’t issue any new shares. Instead, it will sell existing shares held by insiders, employees and investors, a move that will allow it to bypass a roadshow and some of Wall Street’s exorbitant IPO fees. Postmates confidentially filed, too. The 8-year-old company has tapped JPMorgan Chase and Bank of America to lead its upcoming float.

Reddit CEO Steve Huffman delivers remarks on “Redesigning Reddit” during the third day of Web Summit in Altice Arena on November 08, 2017 in Lisbon, Portugal. (Horacio Villalobos-Corbis/Contributor)

It was particularly tough to decide which deal was the most notable this week… But the winner is Reddit, the online platform for chit-chatting about niche topics — r/ProgMetal if you’re Crunchbase editor Alex Wilhelm . The company is raising up to $300 million at a $3 billion valuation, according to TechCrunch’s Josh Constine. Reddit has been around since 2005 and has raised a total of $250 million in equity funding. The forthcoming Series D round is said to be led by Chinese tech giant Tencent at a $2.7 billion pre-money valuation.

Runner up for deal of the week is Calm, the app that helps users reduce anxiety, sleep better and feel happier. The startup brought in an $88 million Series B at a $1 billion valuation. With 40 million downloads worldwide and more than one million paying subscribers, the company says it quadrupled revenue in 2018 from $20 million to $80 million and is now profitable — not a word you hear every day in Silicon Valley.

Here’s your weekly reminder to send me tips, suggestions and more to kate.clark@techcrunch.com or @KateClarkTweets.

I listened to the Bird CEO’s chat with Upfront Ventures’ Mark Suster last week and wrote down some key takeaways, including the challenges of seasonality and safety in the scooter business. I also wrote about an investigation by Consumer Reports that found electric scooters to be the cause of more than 1,500 accidents in the U.S. I’m also required to mention that e-scooter unicorn Lime finally closed its highly anticipated round at a $2.4 billion valuation. The news came just a few days after the company beefed up its executive team with a CTO and CMO hire.

Databricks raises $250M at a $2.75B valuation for its analytics platform

Retail technology platform Relex raises $200M from TCV

Raisin raises $114M for its pan-European marketplace for savings and investment products

Self-driving truck startup Ike raises $52M

Signal Sciences secures $35M to protect web apps

Ritual raises $25M for its subscription-based women’s daily vitamin

Little Spoon gets $7M for its organic baby food delivery service

By Humankind picks up $4M to rid your morning routine of single-use plastic

We don’t spend a ton of time talking about the growing, venture-funded, tech-enabled logistics sector, but one startup in the space garnered significant attention this week. Turvo poached three key Uber Freight employees, including two of the unit’s co-founders. What’s that mean for Uber Freight? Well, probably not a ton… Based on my conversation with Turvo’s newest employees, Uber Freight is a rocket ship waiting to take off.

Who knew that investing in female-focused brands could turn a profit for investors? Just kidding, I knew that and this week I have even more proof! This is L., a direct-to-consumer, subscription-based retailer of pads, tampons and condoms made with organic materials sold to P&G for $100 million. The company, founded by Talia Frenkel, launched out of Y Combinator in August 2015. According to PitchBook, it was backed by Halogen Ventures, 500 Startups, Fusion Fund and a few others.

Speaking of ladies getting stuff done, Bessemer Venture Partners promoted Talia Goldberg to partner this week, making the 28-year-old one of the youngest investing partners at the Silicon Valley venture fund. Plus, Palo Alto’s Eclipse Ventures, hot off the heels of a $500 million fundraise, added two general partners: former Flex CEO Mike McNamara and former Global Foundries CEO Sanjay Jha.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase editor-in-chief Alex Wilhelm and I chat about the expanding podcast industry, Reddit’s big round and scooter accidents.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico

Bird’s electric scooters were on full display at the Upfront Summit in Malibu last week, a two-day event that brings together the likes of Hollywood, Silicon Valley and Washington, DC’s elite.

Not only were a dozen or so brand spanking new scooters available to ride throughout the event but Upfront general partner Mark Suster, an investor in the startup, was seen riding a Bird on stage to the tune of Chamillionaire’s ‘Ridin’ Dirty.’ Plus, Bird founder and chief executive officer Travis VanderZanden was on site to mingle with attendees before closing the summit with a fireside chat with Suster himself.

The pair hit on a number of topics, including the unit economics, safety and seasonality of the scooter business. Neither confirmed Bird’s latest raise; the startup is said to be in the process of securing another $300 million at a $2.3 billion valuation, according to PitchBook. In a 12-month period, the company brought in more than $250 million at a roughly $1 billion valuation.

On unit economics: When Bird bursted onto the scene in 2017, VanderZanden knew he had to move quickly to beat copycats, he explained. Operating under Reid Hoffman’s ‘Blitzscaling’ philosophy, he dispersed hundreds of Alibaba-imported electric scooters that were, well, pretty shitty.

“Those things were fragile,” VanderZanden told Suster. “Clearly the unit economics didn’t work on those scooters but that was a test anyway … Once we knew people liked riding them, we quickly scrambled and started creating our own scooters. Bird Zero is the first iteration of that. What we see on the unit economics of those, it’s like night and day.”

The company unveiled Bird Zero, in October, equipped with a digital screen to display riders’ speed, a tougher exterior and improved battery life.

“2018 was about scaling,” he said. “2019 is about really focusing on the unit economics of the business.”

On seasonality: Some have critiqued Bird for poor unit economics, while others have pointed out that the success of the business is heavily dependent on…weather. No one wants to ride a Bird in the snow, slashing its revenue potential in the cold months. VanderZanden said he’s not concerned with seasonality and revealed Bird operates on a $100 million revenue run rate even in the winter. He did not, however, clarify if that run rate is based on fourth quarter 2018 projections — when Bird introduced Bird Zero — or 2018 annual revenue.

“Obviously, there is seasonality in the scooters business, there’s no doubt about that,” he said. “Yes, it’s slower in December but this market is so big, even in our slow [weeks] most companies would love to have that in their best [month] … We used to say when we’re heading into the holiday season that the Birds would migrate south but it turns out the logistics are really expensive, so the Birds hibernate. That’s a lesson we learned.”

On safety: In the year or so that scooters hit the mainstream in the U.S., there were casualties. Moreover, many — kids included — realized just how easy it is to get away with scootering sans helmet, while others rode throughout the night. Bird, to keep children off scooters, at least, requires customers to provide a driver’s license when they sign up. Given the number of issues that have arisen as scooters become increasingly popular, improved safety measures are bound to be in the news in the year ahead.

“Safety has to be prioritized over growth,” VanderZanden said.

On electric bikes: Bird is one of few scooter businesses that doesn’t offer bikes. With all the capital its raised, will Bird make the leap? VanderZanden seemed lukewarm toward the prospect.

“Yeah, we think about it,” he said. “We [aren’t] religious [about] scooters per se, we just think it’s the thing people like the most so that’s where we started and we think that’s the best thing to do now. We get excited about micromobility generally… We are open and looking at all sorts of different short-range electric vehicles in the future.”

On Bird Platform: Last year, Bird began selling its electric scooters to entrepreneurs and small business owners, who can then rent them out as part of a service called Bird Platform. VanderZanden said the service has opened Bird up to tons of new markets.

“From early on at Bird, we had people asking ‘hey, how do we take Bird to my city,’” he said. “We thought why don’t we empower the local entrepreneurs to take Bird to their market… Now we have people from 77 countries from around the world that are interested in taking Bird to their market, which is exciting because there is no way we as a company could get there in the short-term. This is a way to bring Bird to the world.”

On growth: Given the number of stories on Bird and its competitors in the tech press, it’s easy to forget that most of the startups in the space have launched in the last year or so. VanderZanden took a moment to remind the venture capitalists in the audience that in that time, Bird has expanded to 100 cities. Impressive, yes, but let’s remember the manner in which Bird introduced scooter fleets to new markets. The company showed up unannounced in Santa Monica, for example, a decision that resulted in a lawsuit in the startup’s own hometown.

“It’s pretty incredible that 100 cities have opened their arms and embraced electric scooters,” VanderZanden said.

On Bird’s future: VanderZanden explained that despite a long-held interest in transportation — his mother was a public school bus driver for 30 years — he’s only recently come to understand the industry’s most urgent needs. He plans to put more energy in transportation infrastructure in 2019 as a result.

“The deeper I get into transportation, the more I realize we don’t need autonomous vehicles, we don’t need tunnels, all we need are more bike lanes,” he said.

Powered by WPeMatico

The dream of a startup founder can often be summarized by the following well-intentioned, and mostly delusional, quote: “We’ll raise a few rounds and in a few years we’ll IPO on Nasdaq.”

But a more likely scenario looks something like this:

You invest a few years of hard work to build something of value. One day you receive an acquisition offer out of the blue. You’re elated. And you’re not prepared. You drop everything to focus on this opportunity. Exclusive due diligence starts. Your company is a mess (IP, contracts, burn). Days become weeks; weeks become months. You’ve neglected business and fundraising. You’re running out of money. M&A is now your one and only option. The buyer says they found a bunch of cockroaches in the walls and drops the price. Now what?

Sound unlikely?

This is still a favorable situation: You had an offer! Think about how much time you invested in your various funding rounds. The hundreds of names and Google spreadsheet or Streak-powered quasi-CRM process.

Have you spent even a fraction of that on understanding exit paths? If you’d rather not live the situation described above, read along.

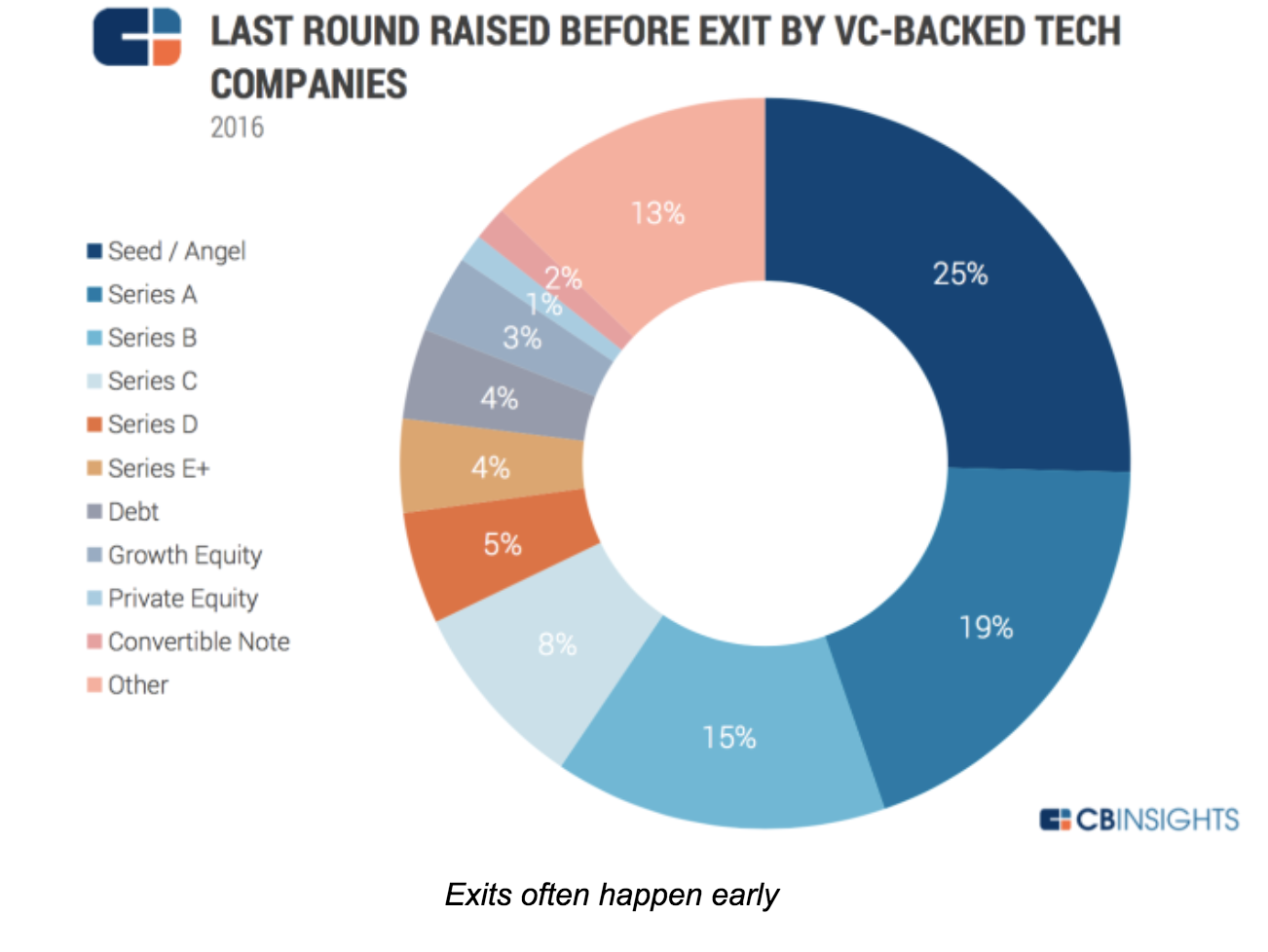

Investors live by exits, but many founders keep dreaming of unicornization and avoid the “E-word” until it’s too late. Yet, in 2016, 97 percent of exits were M&As. And most happened before Series B.

Exits matter because that’s when you, your team and your investors get paid. Oddly enough, and to use a chess metaphor, we hear a lot about the “opening game” (lean startup) and the “mid-game” (growth), but very little about this “end game.”

As a result, founders miss opportunities or leave money on the table. This is a shame. Our fund has more than 700 companies in portfolio. We want the best possible exit for each of them. And fortune favors the prepared! Now, how to get 700 exits (and counting)?

To explore the topic, we organized a series of Master Classes tapping corporate buyers, bankers, investors, lawyers and startup CEOs with M&A or IPO experience in San Francisco. It was a group that included the founders of Guitar Hero — bought by Activision; JUMP Bikes — a SOSV portfolio company bought by Uber, Ubiquisys — bought by Cisco and Withings — bought by Nokia. Each one for hundreds of millions.

Their observations can be summarized below.

“Founders must be aware of what contributes to an exit. This means understanding partnerships and how they are formed in the business space the entrepreneur is working in,” said one Master Class participant.

As founders, you build your product, your company and… optionality. You need to understand the options open to your company, and take steps to enable them.

The most likely one is an acquisition, but there are others like IPO (including small cap), RTO, SBO, LBO, Equity Crowdfunding and even ICO.

“Exit is not a goal per se, but as a CEO it is something you should think about as early in your cycle as possible, while being business-focused,” said the London-based investor Frederic Rombaut, of Seraphim Capital.

Indeed, most participants said that exits should always be on the chief executive’s agenda, no matter how early in the process. “Exits should be on the CEO agenda. Not front and center, but on the agenda. M&A is a by-product of a great business and targeted BD. IPOs are always an option once you’ve built significant cashflow forecasting.”

It’s important to ask questions like: How many “strategic engagements” with potential buyers have you had this month? Is your message and value clear in their eyes? Have you considered an acquisition track in parallel to a fundraise?

It doesn’t stop there:

One thing is sure: The time to exit is not when you’re running out of money.

Unicorn or not, the most likely exit is an acquisition.

As George Patterson, managing director at HSBC in New York said, “Good tech companies are bought, not sold. The question is thus: how to get bought?”

Patterson says it’s important to understand how mergers and acquisitions actually work; how to prepare a startup for an exit; and how to develop a “feel” for the market you’re exiting through and into.

Hearing from corp dev veterans from Cisco, Logitech, Dassault and IBM, a few key ideas emerged:

Motivations vary

It could be from least to most expensive, or as a mix, as listed by Mark Suster, managing partner at Upfront Ventures:

How corporates find you

Corporates find deals via the development of partnerships, investment (CVC), their business units, corp dev research, media and investor connections.

Asked about the best approach, Todd Neville, manager of Corporate Business Development and Strategy at IBM (who gave the most detailed description of the corp dev process), said, “Do something cool to one of the IBM customers. If they rave about even a POC, we’re interested.”

In other words, business development is corporate development.

Get the house in order

Buyers typically want to know three things:

For IP, they will check your contracts (staff and contractors), and run some automated code analysis for proprietary code and open source use. They will evaluate potential IP infringement. No point buying you if you end up costing more in lawsuits!

For your team skills: Sitting down with your engineers will tell them plenty enough without understanding the details of this or that algorithm. The last thing a corporate wants is to be accused of stealing!

Lawyers engaged early can help. The later the clean-up, the more costly and painful.

Develop a feel for your “market”

Develop relationships and create champions within corporates. It will help promote your deal when the time comes, and will let you keep your finger on the pulse of corporate strategy to time your moves.

Do you read the earning calls of Cisco or IBM (or others relevant to you)? This is where strategies are presented. Are your keywords coming up there or in their press releases?

Chris Gilbert, former CEO of Ubiquisys (sold to Cisco for more than $300 million) was very deliberate in planning his exit.

“Selling starts on day one and is a leadership-only function — work out who will be your buyer. Only the CEO can do this. Constantly articulate why a company should buy you,” Gilbert said. Bring clear messages into the acquiring company so it can be presented upwards: give them the presentation you would like them to show their boss! When the time is right, force decisions through competition. If you know they have to buy you, your starting position is strong.”

The dark art of price discovery

There are dozens of formulas (from DCF to comparables) to evaluate a deal — which also means none is “correct.” What matters is: How much would you sell for, and how much is the buyer ready to pay?

Gilbert, at Ubiquisys, described how close interactions with his banker helped drive the price up among the bidders assembled.

Just like buyers, we meet bankers and lawyers too rarely at startup events, but there is much to learn with them. They make deals happen, avoid value erosion and optimize price. They often also make introductions before you engage them, to build goodwill and earn your business.

And if you worry about fees, the right banker handsomely pays for itself by finding more bidders and playing “bad cop” for you, avoiding direct confrontation with your future employer. Do you want a slice of the watermelon or the whole grape?

When asked about what happens after an M&A or IPO, buyers said they generally hoped the founders would stay with them for many years. Often using re-vesting, earn-outs or shares of the acquiring company to incentivize them. Neville, from IBM, mentioned a security company they acquired whose founder is now the head of one of the largest IBM divisions.

In the case of IPOs, supposedly the ultimate “exit,” any block of shares sold by founders would face extreme scrutiny and might cause a price drop.

So who’s exiting during those deals? Investors (and not always).

Eventually, if the average age of a startup at exit is 8-10 years, the active duty period of founders (if not replaced in the meantime) extends even more. Better love the problem you’re solving, and your customers!

Thanks to speakers, participants and supporters of this Master Class series:

London: Frederic Rombaut (Seraphim Capital), Joe Tabberer (FirstBank), Chris Gilbert (Ubiquisys), Jonathan Keeling (Crowdcube), Fred Destin, Tony Fish (AMF Ventures, James Clark (London Stock Exchange), Denise Law (SGCIB).

Paris: Frederic Rombaut (Seraphim Capital), Manuel Gruson (Dassault Systemes), Pierre-Henri Chappaz (Rothschild Global Advisory), Christine Lambert-Goue (All Invest), Olivier Younes (EXPEN), Eric Carreel (Withings), Fabien Bardinet (Balyo), Xavier Lazarus (Elaia Partners), Pierre-Eric Leibovici(Daphni). Jean de La Rochebrochard (Kima Ventures), Jeremy Sartre (SmartAngels), Gwen Regina Tan (Entrepreneur First).

San Francisco: Natasha Ligai (Logitech), Matt Cutler (Cisco),Will Hawthorne, (CODE Advisors), Ryan Rzepecki (JUMP Bikes), Charles Huang (Guitar Hero), Jeff Thomas (Nasdaq), Shahin Farshchi (Lux Capital), Ammar Hanafi (Moment Ventures), Adam J. Epstein (Third Creek Advisors), Nathan Harding (EKSO Bionics), Kate Whitcomb, Anthony Marino and Ethan Haigh (SOSV).

New York: Todd Neville (IBM), George Patterson (HSBC), Ryan Rzepecki (JUMP Bikes), Aaron Kellner (SeedInvest), Jeremy Levine (Bessemer Venture Partners), Taylor Greene (Collaborative Fund), Adam Rothenberg (BoxGroup), Eli Curi (Fenwick & West), Ian Engstrand and Salil Gandhi (Goodwin), Warren Spar(Sparring Partners Capital), Duncan Turner, Vivian Law and Sheng Ge (SOSV).

Powered by WPeMatico