Marc Benioff

Auto Added by WPeMatico

Auto Added by WPeMatico

One of the consequences of rising CO2 levels in our atmosphere is that levels also rise proportionately in the ocean, harming wildlife and changing ecosystems. Heimdal is a startup working to pull that CO2 back out at scale using renewable energy and producing carbon-negative industrial materials, including limestone for making concrete, in the process, and it has attracted significant funding even at its very early stage.

If the concrete aspect seems like a bit of a non sequitur, consider two facts: concrete manufacturing is estimated to produce as much as 8% OF all greenhouse gas emissions, and seawater is full of minerals used to make it. You probably wouldn’t make this connection unless you were in some related industry or discipline, but Heimdal founders Erik Millar and Marcus Lima did while they were working in their respective masters programs at Oxford. “We came out and did this straight away,” he said.

They both firmly believe that climate change is an existential threat to humanity, but were disappointed at the lack of permanent solutions to its many and various consequences across the globe. Carbon capture, Millar noted, is frequently a circular process, meaning it is captured only to be used and emitted again. Better than producing new carbons, sure, but why aren’t there more ways to permanently take them out of the ecosystem?

The two founders envisioned a new linear process that takes nothing but electricity and CO2-heavy seawater and produces useful materials that permanently sequester the gas. Of course, if it was as easy that, everyone would already be doing it.

Image Credits: Heimdal

“The carbon markets to make this economically viable have only just been formed,” said Millar. And the cost of energy has dropped through the floor as huge solar and wind installations have overturned decades-old power economies. With carbon credits (the market for which I will not be exploring, but suffice it to say it is an enabler) and cheap power come new business models, and Heimdal’s is one of them.

The Heimdal process, which has been demonstrated at lab scale (think terrariums instead of thousand-gallon tanks), is roughly as follows. First the seawater is alkalinized, shifting its pH up and allowing the isolation of some gaseous hydrogen, chlorine and a hydroxide sorbent. This is mixed with a separate stream of seawater, causing the precipitation of calcium, magnesium and sodium minerals and reducing the saturation of CO2 in the water — allowing it to absorb more from the atmosphere when it is returned to the sea. (I was shown an image of the small-scale prototype facility but, citing pending patents, Heimdal declined to provide the photo for publication.)

Image Credits: Heimdal

So from seawater and electricity, they produce hydrogen and chlorine gas, calcium carbonate, sodium carbonate and magnesium carbonate, and in the process sequester a great deal of dissolved CO2.

For every kiloton of seawater, one ton of CO2 is isolated, and two tons of the carbonates, each of which has an industrial use. MgCO3 and Na2CO3 are used in, among other things, glass manufacturing, but it’s CaCO3, or limestone, that has the biggest potential impact.

As a major component of the cement-making process, limestone is always in great demand. But current methods for supplying it are huge sources of atmospheric carbon. All over the world industries are investing in carbon reduction strategies, and while purely financial offsets are common, moving forward the preferred alternative will likely be actually carbon-negative processes.

To further stack the deck in its favor, Heimdal is looking to work with desalination plants, which are common around the world where fresh water is scarce but seawater and energy are abundant, for example the coasts of California and Texas in the U.S., and many other areas globally, but especially where deserts meet the sea, like in the MENA region.

Desalination produces fresh water and proportionately saltier brine, which generally has to be treated, as to simply pour it back into the ocean can throw the local ecosystem out of balance. But what if there were, say, a mineral-collecting process between the plant and the sea? Heimdal gets the benefit of more minerals per ton of water, and the desalination plant has an effective way of handling its salty byproduct.

“Heimdal’s ability to use brine effluent to produce carbon-neutral cement solves two problems at once,” said Yishan Wong, former Reddit CEO, now CEO of Terraformation and individually an investor in Heimdal. “It creates a scalable source of carbon-neutral cement, and converts the brine effluent of desalination into a useful economic product. Being able to scale this together is game-changing on multiple levels.”

Terraformation is a big proponent of solar desalination, and Heimdal fits right into that equation; the two are working on an official partnership that should be announced shortly. Meanwhile a carbon-negative source for limestone is something cement makers will buy every gram of in their efforts to decarbonize.

Wong points out that the primary cost of Heimdal’s business, beyond the initial ones of buying tanks, pumps and so on, is that of solar energy. That’s been trending downwards for years and with huge sums being invested regularly there’s no reason to think that the cost won’t continue to drop. And profit per ton of CO2 captured — already around 75% of over $500-$600 in revenue — could also grow with scale and efficiency.

Millar said that the price of their limestone is, when government incentives and subsidies are included, already at price parity with industry norms. But as energy costs drop and scales rise, the ratio will grow more attractive. It’s also nice that their product is indistinguishable from “natural” limestone. “We don’t require any retrofitting for the concrete providers — they just buy our synthetic calcium carbonate rather than buy it from mining companies,” he explained.

All in all it seems to make for a promising investment, and though Heimdal has not yet made its public debut (that would be forthcoming at Y Combinator’s Summer 2021 Demo Day) it has attracted a $6.4 million seed round. The participating investors are Liquid2 Ventures, Apollo Projects, Soma Capital, Marc Benioff, Broom Ventures, Metaplanet, Cathexis Ventures and, as mentioned above, Yishan Wong.

Heimdal has already signed LOIs with several large cement and glass manufacturers, and is planning its first pilot facility at a U.S. desalination plant. After providing test products to its partners on the scale of tens of tons, they plan to enter commercial production in 2023.

Powered by WPeMatico

Aforza, developing cloud and mobile apps for consumer goods companies, announced a $22 million Series A round led by DN Capital.

The London-based company’s technology is built on the Salesforce and Google Cloud platforms so that consumer goods companies can digitally transform product distribution and customer engagement to combat issues like unprofitable promotions and declining market share, Aforza co-founder and CEO Dominic Dinardo told TechCrunch. Using artificial intelligence, the company recommends products and can predict the order a retailer can make with promotions and pricing based on factors like locations.

The global market for consumer packaged goods apps is forecasted to reach $15 billion by 2024. However, the industry is still using outdated platforms that, in some cases, lead to a loss of 5% of sales when goods are out of stock, Dinardo said.

Aforza’s trade promotion designer mobile image. Image Credits: Aforza

Dinardo and his co-founders, Ed Butterworth and Nick Eales, started the company in 2019. All veterans of Salesforce, they saw how underserved the consumer goods industry was in terms of moving to digital.

Aforza is Dinardo’s first time leading a company. However, from his time at Salesforce he feels he got an education like going to “Marc Benioff’s School of SaaS.” The company raised an undisclosed seed round in 2019 from Bonfire Ventures, Daher Capital, DN Capital, Next47 and Salesforce Ventures.

Then the pandemic happened, which had many of the investors leaning in, which was validation of what Aforza was doing, Dinardo said.

“Even before the pandemic, the consumer goods industry was challenged with new market entrants and horrible legacy systems, but then the pandemic turned off pathways to customers,” he added. “Our mission is to improve the lives of consumers by bringing forth more sustainable products and packaging, but also helping companies be more agile and handle changes as the biggest change is happening.”

Joining DN Capital in the round were Bonfire Ventures, Daher Capital and Next47.

Brett Queener, partner at Bonfire Ventures, said he helped incubate Aforza with Dinardo and Eales, something his firm doesn’t typically do, but saw a unique opportunity to get in on the ground floor.

Also working at Salesforce, he saw the consumer goods industry as a major industry with a compelling reason to make a technology shift as customers began expecting instant availability and there were tons of emerging startups coming into the direct-to-consumer space.

Those startups don’t have a year or two to pull together the kind of technology it took to scale. With Aforza, they can build a product that works both online and off on any device, Queener said. And rather than planning promotions on a quarterly basis, companies can make changes to their promotional spend in real time.

“It is time for Aforza to tell the world about its technology, time to build out its footprint in the U.S. and in Europe, invest more in R&D and execute the Salesforce playbook,” he said. “That is what this round is about.”

Dinardo intends on using the new funding to continue R&D and to double its employee headcount over the next six months as it establishes its new U.S. headquarters in the Northeast. It is already working with customers in 20 countries.

As to growth, Dinardo said he is using his past experiences at startups like Veeva and Vlocity, which was acquired by Salesforce in 2020, as benchmarks for Aforza’s success.

“We have the money and the expertise — now we need to take a moment to breathe, hire people with the passion to do this and invest in new product tiers, digital assets and even payments,” he said.

Powered by WPeMatico

Salesforce just closed a $28 billion mega-deal to buy Slack, generating significant debt along the way, but it’s not through spending big money.

Today the CRM giant announced it was taking a leap into streaming media with Salesforce+, a forthcoming digital media network with a focus on video that, in the words of the company, “will bring the magic of Dreamforce to viewers across the globe with luminary speakers.” (Whether that’s a good thing or not is in the eye of the beholder.)

Over the last year, Salesforce has watched companies struggle to quickly transform into fully digital entities. The Slack purchase is part of Salesforce’s response to the evolving market, but the company believes it can do even more with an on-demand video service providing business content around the clock.

Salesforce president and CMO Sarah Franklin said in an official post that her company has had to “reimagine how to succeed in the new digital-first world.” The answer apparently involves getting the larger Salesforce community together in a new live, and recorded video push.

In a Q&A with Colin Fleming, Salesforce’s senior vice president of Global Brand Marketing, he sees it as a way to evolve the content the company has been sharing all along. “As a result of the pandemic, we looked at the media landscape, where people are consuming content, and decided the days of white papers in a business-to-business setting were no longer interesting to people. We’re staring at a cookie-less future. And looking at the consumer world, we reflected on that for Salesforce and asked, “Why shouldn’t we be thinking about this too,” he said in the Q&A.

The company’s efforts are not small. Axios reports that there are “50 editorial leads” aboard the project to help it launch, and “hundreds of people at Salesforce currently working on Salesforce+” more broadly.

Notably Salesforce does not have near-term monetization plans for Salesforce+. The service will be free, and will not feature external advertising. Salesforce+ will launch in September in conjunction with Dreamforce and include four channels: Primetime for news and announcements, Trailblazer for training content, Customer 360 for success stories and Industry Channels for industry-specific offerings.

The company hopes that by combining the announcement with Dreamforce, it will help drive interest in what Salesforce has cooked up. After the Dreamforce push, Salesforce+ will enter into interesting territory. How much do Salesforce customers, and the larger business community, really want what the company describes as “compelling live and on-demand content for every role, industry and line of business,” and “engaging stories, thought leadership and expert advice”?

Salesforce is considered the most successful SaaS-first company in history, and as such may have an opinion that people are interested in hearing. In its most recent quarterly earnings report in May, the company disclosed $5.96 billion in revenue, up 23% compared to the year-ago quarter, putting it close to a $25 billion run rate. The company also generates lots of cash. But being cash-rich doesn’t absolve the question of whether this new streaming effort will prove to be a money pit, costing buckets of cash to produce with limited returns.

The service sounds a bit like your LinkedIn feed brought to life, but in video form. At the very least, it’s probably the largest content marketing scheme of all time, but can it ever pay for itself either as a business unit or through some other monetization plans (like advertising) down the road?

Brent Leary, founder and principal analyst at CRM essentials, says that he could see Salesforce eyeing advertising revenue with this venture and having it all tie into the Salesforce platform. “A customer could sponsor a show, advertise a show or possibly collaborate on a show… and have leads generated from the show directly tied to the activity from those options while tracking ROI, and it’s all done on one platform. And the content lives on with ads living on with them,” Leary told TechCrunch.

Whether that’s the ultimate goal of this venture remains to be seen, but Salesforce has proven that there is market appetite for Dreamforce content at least in the physical world, with over a hundred thousand people involved in 2019, the last time the company was able to hold a live event. While the pandemic shifted most traditional conference activity into the digital realm, making Dreamforce and related types of content available year-round in video format makes some sense in that context.

Precisely how the company will justify the sizable addition to its marketing budget will be interesting; measuring ROI from video products is not entirely straightforward when it is not monetized directly. And sooner or later it will have to have some direct or indirect impact on the business or face questions from shareholders on the purpose of the venture.

Powered by WPeMatico

Last month Jeff Bezos announced he would step down as CEO of Amazon later this year, moving into the executive chairman role, while passing the baton to AWS CEO Andy Jassy. Could Marc Benioff, co-founder, chairman and CEO at Salesforce be the next big-name executive to make a similar move?

A Reuter’s story published on Monday suggested that could be the case. Citing unnamed sources, the story indicated that Benioff’s CEO exit could happen this year. Further those same sources suggested that current Salesforce president and COO Bret Taylor is the likely heir apparent.

We wrote a story at the end of last year speculating on possible successors to Benioff, were he to step away from the CEO role. There were a number of worthy candidates, several of whom, like Taylor, came to the company via an acquisition. All the same, we thought that Taylor seemed to be the most likely candidate to replace Benioff.

We asked Salesforce for a comment on the Reuter’s story. A company spokesperson told us that the company doesn’t comment on rumors or speculation.

While the entire scenario fits firmly in the rumor and speculation column, it is not entirely unlikely either. What would it mean if Benioff stepped away and what if Taylor was truly the next in line? And how would that swap compare with the Bezos decision were it to happen?

Salesforce and Amazon are both companies founded in the 1990s, each looking to shake up its industry.

For Amazon, it was changing the way goods (starting with books) were bought and sold. And for Benioff the goal was changing the way software was sold. Bezos famously founded his company in his garage. Benioff built his in a rented apartment. From these humble beginnings both have built iconic companies and accumulated enormous wealth. You could understand why either could be ready to step away from the daily grind of running a company after all these years.

Bezos announced that veteran executive Andy Jassy, who runs the company’s cloud arm, would be his replacement when the handoff comes. Jassy knows the organization’s priority mix as he’s been working at the company for more than two decades. He’s locked into the culture and helped take AWS from idea to $50 billion juggernaut.

While Benioff hasn’t made any actual firm pronouncement, we have seen Bret Taylor — who joined the company in 2016 when Salesforce purchased his startup Quip for $750 million — move quickly up the ladder.

Laurie McCabe, co-founder and analyst at SMB Group, who has been following Salesforce since its earliest days, says that if Benioff were to leave, he would obviously leave big shoes to fill. But she agreed that everything seems to point to Taylor as his successor should that happen.

“Salesforce has been grooming Taylor for awhile. He has some stellar credentials both at Salesforce, his own start-up, Quip, that Salesforce acquired, and at Facebook. There’s no doubt in my mind he can lead Salesforce forward, but he’ll bring a different more low-key style to the role. And I’m sure Benioff will stay very involved […],” McCabe said.

Brent Leary, founder and principal analyst at CRM Essentials says that while he believes Taylor could be chosen as Benioff’s successor, and would be qualified to lead the company, he’s taken a very different path from Jassy.

“I think Benioff moving on could be different from Bezos in the sense that Jassy has been at Amazon for over 20 years and was there to basically see and be part of most of the story. […] But if Taylor were to succeed Benioff there’s not as much [history] at Salesforce with him not being on board until the Quip acquisition in 2016,” Leary said.

Leary wonders if this relatively short history with the company could create some political friction in the organization if he were chosen to succeed Benioff. “I’m not saying that this would happen, but choosing one of the many possible heirs that have come via a number of high profile acquisitions could possibly lead to high level turnover from those not picked to succeed Benioff,” he said.

But Holger Mueller, an analyst at Constellation Research says that if you look at the range of candidates available, he believes that Taylor would be the best choice. “I don’t expect any issue because there is no one with a similar or even better background, which is when there are problems — that or when people are in an open competition as it used to be at GE,” he said.

We don’t know for sure what the final outcome will be, but if Benioff does decide to join Bezos and takes the executive chairman mantle at the company, it makes sense that the person to replace him will be Taylor. But for now, it remains in the realm of speculation, and we’ll just to wait and see if that’s what comes to pass.

Powered by WPeMatico

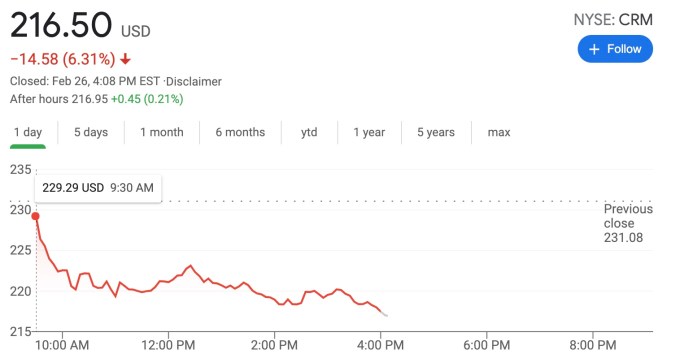

Wall Street investors can be fickle beasts. Take Salesforce as an example. The CRM giant announced a $5.82 billion quarter when it reported earnings yesterday. Revenue was up 20% year over year. The company also reported $21.25 billion in total revenue for the just-closed FY2021, up 24% YoY. If that wasn’t enough, it raised its FY2022 guidance (its upcoming fiscal year) to over $25 billion. What’s not to like?

You want higher quarterly revenue, Salesforce gave you higher revenue. You want high growth and solid projected revenue — check and check. In fact, it’s hard to find anything to complain about in the report. The company is performing and growing at a rate that is remarkable for an organization of its size and maturity — and it is expected to continue to perform and grow.

How did Wall Street react to this stellar report? It punished the stock with the price down over 6%, a pretty dismal day considering the company brought home such a promising report card.

Image Credits: Google

So what is going on here? It could be that investors simply don’t believe the growth is sustainable or that the company overpaid when it bought Slack at the end of last year for over $27 billion. It could be it’s just people overreacting to a cooling market this week. But if investors are looking for a high-growth company, Salesforce is delivering that.

While Slack was expensive, it reported revenue over $250 million yesterday, pushing it over the $1 billion run rate with more than 100 customers paying over $1 million in ARR. Those numbers will eventually get added to Salesforce’s bottom line.

Canaccord Genuity analyst David Hynes Jr. wrote that he was baffled by investors’ reaction to this report. Like me, he saw a lot of positives. Yet Wall Street decided to focus on the negative, and see “the glass half empty,” as he put it in his note to investors.

“The stock is clearly in the show-me camp, which means it’s likely to take another couple of quarters for investors to buy into the idea that fundamentals are actually quite solid here, and that Slack was opportunistic (and yes, pricey), but not an attempt to mask suddenly deteriorating growth,” Hynes wrote.

During the call with analysts yesterday, Brad Zelnick from Credit Suisse asked how well the company could accelerate out of the pandemic-induced economic malaise, and Gavin Patterson, Salesforce’s president and chief revenue officer, says the company is ready whenever the world moves past the pandemic.

“And let me reassure you, we are building the capability in terms of the sales force. You’d be delighted to hear that we’re investing significantly in terms of our direct sales force to take advantage of that demand. And I’m very confident we’ll be able to meet it. So I think you’re hearing today a message from us all that the business is strong, the pipeline is strong and we’ve got confidence going into the year,” Patterson said.

While Salesforce execs were clearly pumped up yesterday with good reason, there’s still doubt out in investor land that manifested itself in the stock starting down and staying down all day. It will be, as Hynes suggested, up to Salesforce to keep proving them wrong. As long as they keep producing quarters like the one they had this week, they should be just fine, regardless of what the naysayers on Wall Street may be thinking today.

Powered by WPeMatico

Zack Parisa and Max Nova, the co-founders of the carbon offset company SilviaTerra, have spent the last decade working on a way to democratize access to revenue-generating carbon offsets.

As forestry credits become a big, booming business on the back of multibillion-dollar commitments from some of the world’s biggest companies to decarbonize their businesses, the kinds of technologies that the two founders have dedicated 10 years of their lives to building are only going to become more valuable.

That’s why their company, already a profitable business, has raised $4.4 million in outside funding led by Union Square Ventures and Version One Ventures, along with Salesforce founder and the driving force between the One Trillion Trees Initiative, Marc Benioff .

“Key to addressing the climate crisis is changing the balance in the so-called carbon cycle. At present, every year we are adding roughly 5 gigatons of carbon to the atmosphere. Since atmospheric carbon acts as a greenhouse gas this increases the energy that’s retained rather than radiated back into space which causes the earth to heat up,” writes Union Square Ventures managing partner Albert Wenger in a blog post. “There will be many ways such drawdown occurs and we will write about different approaches in the coming weeks (such as direct air capture and growing kelp in the oceans). One way that we understand well today and can act upon immediately are forests. The world’s forests today absorb a bit more than one gigatons of CO2 per year out of the atmosphere and turn it into biomass. We need to stop cutting and burning down existing forests (including preventing large scale forest fires) and we have to start planting more new trees. If we do that, the total potential for forests is around 4 to 5 gigatons per year (with some estimates as high as 9 gigatons).”

For the two founders, the new funding is the latest step in a long journey that began in the woods of Northern Alabama, where Parisa grew up.

After attending Mississippi State for forestry, Parisa went to graduate school at Yale, where he met Louisville, Kentucky native Max Nova, a computer science student who joined with Parisa to set up the company that would become SilviaTerra.

SilviaTerra co-founders Max Nova and Zack Parisa. Image Credit: SilviaTerra

The two men developed a way to combine satellite imagery with field measurements to determine the size and species of trees in every acre of forest.

While the first step was to create a map of every forest in the U.S., the ultimate goal for both men was to find a way to put a carbon market on equal footing with the timber industry. Instead of cutting trees for cash, potentially landowners could find out how much it would be worth to maintain their forestland. As the company notes, forest management had previously been driven by the economics of timber harvesting, with over $10 billion spent in the U.S. each year.

The founders at SilviaTerra thought that the carbon market could be equally as large, but it’s hard for most landowners to access. Carbon offset projects can cost as much as $200,000 to put together, which is more than the value of the smaller offset projects for landowners like Parisa’s own family and the 40 acres they own in the Alabama forests.

There had to be a better way for smaller landowners to benefit from carbon markets too, Parisa and Nova thought.

To create this carbon economy, there needed to be a single source of record for every tree in the U.S. and while SilviaTerra had the technology to make that map, they lacked the compute power, machine learning capabilities and resources to build the map.

That’s where Microsoft’s AI for Earth program came in.

Working with AI for Earth, SilviaTierra created their first product, Basemap, to process terabytes of satellite imagery to determine the sizes and species of trees on every acre of America’s forestland. The company also worked with the U.S. Forestry Service to access their data, which was used in creating this holistic view of the forest assets in the U.S.

With the data from Basemap in hand, the company has created what it calls the Natural Capital Exchange. This program uses SilviaTerra’s unparalleled access to information about local forests, and the knowledge of how those forests are currently used to supply projects that actually represent land that would have been forested were it not for the offset money coming in.

Currently, many forestry projects are being passed off to offset buyers as legitimate offsets on land that would never have been forested in the first place — rendering the project meaningless and useless in any real way as an offset for carbon dioxide emissions.

“It’s a bloodbath out there,” said Nova of the scale of the problem with fraudulent offsets in the industry. “We’re not repackaging existing forest carbon projects and trying to connect the demand side with projects that already exist. Use technology to unlock a new supply of forest carbon offset.”

The first Natural Capital Exchange project was actually launched and funded by Microsoft back in 2019. In it, 20 Western Pennsylvania land owners originated forest carbon credits through the program, showing that the offsets could work for landowners with 40 acres, or, as the company said, 40,000.

Landowners involved in SilviaTerra’s pilot carbon offset program paid for by Microsoft. Image Credit: SilviaTerra

“We’re just trying to get inside every landowners annual economic planning cycle,” said Nova. “There’s a whole field of timber economics… and we’re helping answer the question of given the price of timber, given the price of carbon does it make sense to reduce your planned timber harvests?”

Ultimately, the two founders believe that they’ve found a way to pay for the total land value through the creation of data around the potential carbon offset value of these forests.

It’s more than just carbon markets, as well. The tools that SilviaTerra have created can be used for wildfire mitigation as well. “We’re at the right place at the right time with the right data and the right tools,” said Nova. “It’s about connecting that data to the decision and the economics of all this.”

The launch of the SilviaTerra exchange gives large buyers a vetted source to offset carbon. In some ways it’s an enterprise corollary to the work being done by startups like Wren, another Union Square Ventures investment, that focuses on offsetting the carbon footprint of everyday consumers. It’s also a competitor to companies like Pachama, which are trying to provide similar forest offsets at scale, or 3Degrees Inc. or South Pole.

Under a Biden administration there’s even more of an opportunity for these offset companies, the founders said, given discussions underway to establish a Carbon Bank. Established through the existing Commodity Credit Corp. run by the Department of Agriculture, the Carbon Bank would pay farmers and landowners across the U.S. for forestry and agricultural carbon offset projects.

“Everybody knows that there’s more value in these systems than just the product that we harvest off of it,” said Parisa. “Until we put those benefits in the same footing as the things we cut off and send to market…. As the value of these things goes up… absolutely it is going to influence these decisions and it is a cash crop… It’s a money pump from coastal America into middle America to create these things that they need.”

Powered by WPeMatico

When Salesforce acquired Quip in 2016 for $750 million, it gained CEO and co-founder Bret Taylor as part of the deal. Taylor has since risen quickly through the ranks of the software giant to become president and COO, second in command behind CEO Marc Benioff. Taylor’s experience shows that startup founders can sometimes play a key role in the companies that acquire them.

Benioff, 56, has been running Salesforce since its founding more than 20 years ago. While he hasn’t given any public hints that he intends to leave anytime soon, if he wanted to step back from the day-to-day running of the company or even job share the role, he has a deep bench of executive talent including many experienced CEOs, who like Taylor came to the company via acquisition.

One way to step back from the enormous responsibility of running Salesforce would be by sharing the role.

He and his wife Lynne have been active in charitable giving and in 2016 signed The Giving Pledge, an initiative from the The Bill and Melinda Gates Foundation, to give a majority of their wealth to philanthropy. One could see him wanting to put more time into pursuing these charitable endeavors just as Gates did 20 years ago. As a means of comparison, Gates founded Microsoft in 1975 and stayed for 25 years until he left in 2000 to run his charitable foundation full time.

Even if this remains purely speculative for the moment, there is a group of people behind him with deep industry experience, who could be well-suited to take over should the time ever come.

One way to step back from the enormous responsibility of running Salesforce would be by sharing the role. In fact, for more than a year starting in 2018, Benioff actually shared the top job with Keith Block until his departure last year. When they worked together, the arrangement seemed to work out just fine with Block dealing with many larger customers and helping the software giant reach its $20 billion revenue goal.

Before Block became co-CEO, he had a myriad other high-level titles including co-chairman, president and COO — two of which, by the way, Taylor has today. That was a lot of responsibility for one person inside a company the size of Salesforce, but promoting him to co-CEO from COO gave the company a way to reward his hard work and help keep him from jumping ship (he eventually did anyway).

As Holger Mueller, an analyst at Constellation Research points out, the co-CEO concept has worked out well at major enterprise companies that have tried it in the past, and it helped with continuity. “Salesforce, SAP and Oracle all didn’t miss a beat really with the co-CEO departures,” he said.

If Benioff wanted to go back to the shared responsibility model and take some work off his plate, making Taylor (or someone else) co-CEO would be one way to achieve that. Certainly, Brent Leary, lead analyst at CRM Essentials sees Taylor gaining increasing responsibility as time goes along, giving credence to the idea.

“Ever since Quip was acquired Taylor seemed to be on the fast track, becoming president and chief product officer less than a year-and-a-half after the acquisition, and then two years later being promoted to chief operating officer,” Leary said.

While Taylor isn’t the only person who could step into Benioff’s shoes, he looks like he has the best shot at the moment, especially in light of the $27.7 billion Slack deal he helped deliver earlier this month.

“Taylor being publicly praised by Benioff for playing a significant role in the Slack acquisition, Salesforce’s largest acquisition to date, shows how much he has solidified his place at the highest levels of influence and decision-making in the organization,” Leary pointed out.

But Mueller posits that his rapid promotions could also show something might be lacking with internal options, especially around product. “Taylor is a great, smart guy, but his rise shows more the product organization bench depth challenges that Salesforce has,” he said.

Powered by WPeMatico

Richard Socher, former chief scientist at Salesforce, who helped build the Einstein artificial intelligence platform, is taking on a new challenge — and it’s a doozy. Socher wants to fix consumer search and today he announced you.com, a new search engine to take on the mighty Google.

“We are building you.com. You can already go to it today. And it’s a trusted search engine. We want to work on having more click trust and less clickbait on the internet,” he said. He added that in addition to trust, he wants it to be built on kindness and facts, three worthy but difficult goals to achieve.

He said that there were several major issues that led him and his co-founders to build a new search tool. For starters, he says that there is too much information and nobody can possibly process it all. What’s more, as you find this information, it’s impossible to know what you can trust as accurate, and he believes that issue is having a major impact on society at large. Finally, as we navigate the internet in 2020, the privacy question looms large as is how you balance the convenience-privacy trade-off.

He believes his background in AI can help in a consumer-focused search tool. For starters the search engine, while general in nature, will concentrate on complex consumer purchases where you have to open several tabs to compare information.

“The biggest impact thing we can do in our lives right now is to build a trusted search engine with AI and natural language processing superpowers to help everyone with the various complex decisions of their lives, starting with complex product purchases, but also being general from the get-go as well,” he said.

While Socher was light on details, preferring to wait until GA in a couple of months to share some more, he said he wants to differentiate from Google by not relying on advertising and what you know about the user. He said he learned from working with Marc Benioff at Salesforce that you can make money and still build trust with the people buying your product.

He certainly recognizes that it’s tough to take on an entrenched incumbent, but he and his team believe that by building something they believe is fundamentally different, they can undermine the incumbent with a classic “Innovator’s Dilemma” kind of play where they’re doing something that is hard for Google to reproduce without undermining their primary revenue model.

He also sees Google running into antitrust issues moving forward and that could help create an opening for a startup like this. “I think a lot of stuff that Google [has been doing] … with the looming antitrust will be somewhat harder for them to get away with on a continued basis,” he said.

He acknowledges that trust and accuracy elements could get tricky as social networks have found out. Socher hinted at some social sharing elements they plan to build into the search tool including allowing you to have your own custom you.com URL with your name to facilitate that sharing.

Socher said he has funding and a team together working actively on the product, but wouldn’t share how much or how many employees at this point. He did say that Benioff and venture capitalist Jim Breyer are primary backers and he would have more information to share in the coming months.

For now, if you’re interested, you can go to the website and sign up for early access.

Powered by WPeMatico

Calm, a well-known meditation app, has raised new capital at a valuation of $2 billion. The round was anticipated after the company was reported to be hunting for up to $150 million at a valuation of $2.2 billion; perhaps Calm will follow in the steps of Robinhood and add a second tranche to the round in time.

Prior investor Lightspeed Venture Partners led the investment, which also saw participation from Insight, TPG and Salesforce CEO and new Slack owner Marc Benioff, among others.

That Calm was able to secure more capital is not surprising. The company has a history of quick revenue growth, and is reportedly profitable, to boot. And the investment comes after mental health-focused startups as a category have performed well from a venture capital perspective.

The coronavirus pandemic has likely also played into Calm’s attractiveness as an investment. Since the beginning, researchers have warned about the psychological toll that a pandemic could have on humanity. A recent Pew Research study suggested that people who have lost their jobs during the pandemic might be feeling higher levels of distress during this time. Rival service Headspace offered an annual subscription to its platform for free for those that are unemployed.

Calm responded to the toll of coronavirus by launching a page of free resources, and focusing on a partnership with nonprofit health system Kaiser Permanente. Kaiser was the first health system to make Calm app’s Premium subscription free for its members.

The startups sells a consumer service for around $70 per year, or $15 per month. And the startup has built out a corporate arm, “Calm for Business,” that likely brings revenue stability that augments its consumer efforts.

As part of a release concerning today’s news, Calm detailed a number of nearly useful growth metrics. The service has over 100 million downloads, up from 40 million downloads in February 2019. It also grew up from 1 million paying users to 4 million paying users in the same time period (we asked if that data was inclusive of any Calm for Business customers, a question Calm did not answer).

Other TechCrunch queries regarding the company’s economics, revenue growth and performance compared to its pre-COVID plan also went unanswered.

Calm and rival service Headspace have now raised a combined $434 million according to Crunchbase data, underscoring how attractive their models have proved to venture capitalists. According to a Bloomberg interview, Calm is considering acquiring smaller companies in the wake of its new capital event.

Regardless, Calm now has a refreshed war chest heading into 2021 and a plan to go hunting. That should generate a headline or two.

Powered by WPeMatico

In a case of bizarre timing, Salesforce announced it was laying off 1,000 employees at the end of last month just a day after announcing a monster quarter with over $5 billion in revenue, putting the company on a $20 billion revenue run rate for the first time. The juxtaposition was hard to miss.

Earlier today, Salesforce CEO and co-founder Marc Benioff announced in a tweet that the company would be hiring 4,000 new employees in the next six months, and 12,000 in the next year. While it seems like a mixed message, it’s probably more about reallocating resources to areas where they are needed more.

Salesforce will add 4K jobs over the next 6 mos & 12K over the next year. Join our 54K employee strong Ohana defining the future of software. Salesforce is the worlds fastest growing Top 5 enterprise software company. jobs@salesforce.com @salesforcejobs https://t.co/ffzlmeHhCz

— Marc Benioff (@Benioff) September 18, 2020

While Salesforce wouldn’t comment further on the hirings, the company has obviously been doing well in spite of the pandemic, which has had an impact on customers. In the prior quarter, the company forecasted that it would have slower revenue growth due to giving some customers facing hard times with economic downturn time to pay their bills.

That’s why it was surprising when the CRM giant announced its earnings in August and that it had done so well in spite of all that. While the company was laying off those 1,000 people, it did indicate it would give those employees 60 days to find other positions in the company. With these new jobs, assuming they are positions the laid-off employees are qualified for, they could have a variety of positions from which to choose.

The company had 54,000 employees when it announced the layoffs, which accounted for 1.9% of the workforce. If it ends up adding the 12,000 news jobs in the next year, that would put the company at approximately 65,000 employees by this time next year.

Powered by WPeMatico