managing partner

Auto Added by WPeMatico

Auto Added by WPeMatico

When “Law & Order” ended its 20-year run in 2010, it had already cemented its place as one of the longest-running television dramas in history. Its success was a testament to the enduring popularity of a good mystery.

Mining that same well of a demand for whodunnits, a roughly one-year-old Los Angeles-based startup called Solve has raised $20 million in financing to update the genre for a new generation of media consumers.

Its eponymously titled social media programming, available on Instagram and Snap, has managed to nab roughly 30 million interactions over the year-and-a-half that it distributed its productions. Now the company is launching a true crime podcast on the iHeartMedia and Apple platforms to tap into another potentially high-growth market.

Solve began as a series developed within the mobile-focused entertainment studio, Vertical Networks. Helmed by Tom Wright and financed by Elisabeth Murdoch (through her Freelands Ventures fund, which Wright also managed) and Snap, the company was one of the early entrants to raise cash as a production studio for mobile content. But it was far from the only studio to see money in mobile-first entertainment. All of the major internet-age media companies had their own mobile strategies.

Murdoch eventually replaced Wright (so that he could work on spinning up Solve as an independent entity) and sold Vertical Networks two months ago to the online media startup, Whistle, for an undisclosed amount.

“I spent a year looking deep, deep, deep into audience behavioral data on Snap and Facebook,” Wright says. “The DNA of what I thought [audience] sensibilities was leading towards was this format.”

As Vertical Networks was winding down, Solve was spinning up with help from Lightspeed Venture Partners, Upfront Ventures and Advancit Capital.

“We’ve seen incredibly popular crime mystery shows across media, including podcasts like Serial and Dirty John, TV shows like Making a Murderer and Law & Order, and movies like The Usual Suspects and Gone Girl,” said Jeremy Liew, partner at Lightspeed Venture Partners, in a statement. “Games have attained a first class status as media but we’ve yet to see a crime mystery format game achieve the same success, and Solve is going to right that wrong.”

The gamification element that’s made Solve’s episodes resonate with mobile audiences on social platforms will be a small part of the initial series, says Wright, with plans to expand the interactive elements going forward.

Produced in partnership with SALT audio, whose previous work includes “Blackout” and “Carrier” and iHeartMedia, the 10-episode series uses the same “ripped from the headlines” storytelling for its 30-minute broadcasts and offers listeners clues in leaked audio files, voicemails, courtroom testimony and other evidence to try to guess the killer.

For now, Solve is content to be a studio producing ad-supported media for platforms like Apple, Snap, Facebook, iHeartMedia and other distributors, according to Wright. It’s a different path than studios like Quibi, which is creating its own streaming service dedicated to mobile storytelling and backed by many of the major Hollywood studios.

The current pace of production means that Solve is making 18 original episodes per month. For the 40-year-old Wright, Solve represents a fourth foray into the world of startups. And while he’s not a fan of the crime or mystery genre himself, Wright said that the data around engagement was too compelling to not try to launch a business around it.

“The Internet has changed how we interact with the world from taxis to news to shopping. We believe that Solve can fundamentally change how we interact with narrative video storytelling,” said Mark Suster, managing partner, Upfront Ventures, in a statement. “When we heard Tom’s vision for short-form video that you not only watch but also must ‘solve‘, we knew that it had enormous potential.”

Powered by WPeMatico

Raysecur says at least ten times a day someone sends a suspicious package containing powder, liquid, or some other kind of hazard.

The Boston, Mass.-based startup says its desktop-sized 3D real-time scanning technology, dubbed MailSecur, can intercept and detect threats in the mailroom before they ever make it onto the office floor.

Mailroom security may not seem fancy or interesting, but they’re a common gateway into a corporate environment. They’re a huge attack vector for attackers — both physical and cyber. Earlier this year we wrote about warshipping, a “Trojan horse”-type attack that can be used as a way for hackers to ship hardware exploits into a business, break the Wi-Fi, and pivot onto the corporate network to steal data.

Now, the company has raised $3 million in seed-round funding led by One Way Ventures, with participation from Junson Capital, Launchpad Venture Group, and also Dreamit Ventures, a Philadelphia-based early stage investor and accelerator, which last year announced it would move into the early-stage security space.

Raysecur’s proprietary millimeter-wave scanner, MailSecur. (Image: supplied)

Raysecur uses millimeter-wave technology — similar to the scanners you find at airport security — to examine suspicious letters, flat envelopes, and small parcels. Its technology can detect powders as small as 2% of a teaspoon or a single drop of liquid, the company claims.

The startup said the funding will help expand its customer base. Although still in its infancy, the company has about ten Fortune 500 customers using its MailSecur scanner.

Since it was founded in 2018, the company has scanned more than 9.2 million packages.

Semyon Dukach, managing partner at One Way Ventures, said the funding will help “bring this compelling technology to an even broader market.”

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

We have something a bit different for you this week. Equity co-host Kate Clark recently sat down with Manish Chandra, the co-founder and chief executive officer of Poshmark, and one of his earliest investors, NFX managing partner James Currier.

If you haven’t heard of Poshmark, it’s an online platform for buying and selling clothes. Basically, it’s the thrift shop of the 21st century. We asked Chandra how he and co-founders Tracy Sun, Gautam Golwala and Chetan Pungaliya cooked up the idea for Poshmark, what bumps they faced along the way, how they raised venture capital and, of course, what details of their upcoming initial public offering he could share with us. Meanwhile, Currier dished about the company’s early days, when the Poshmark team worked hard on the floor of Currier’s office.

Unfortunately, neither Chandra or Currier were willing to share deets about Poshmark’s IPO, reportedly expected soon. But they both shared interesting insights into building a successful venture-backed company, battling competition and putting your best foot forward.

Glad you guys came back for another episode, we’ll see you soon.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

If you’re an avid TechCrunch reader, someone who loves to absorb endless startup profiles and pore through fundraising stories, you might think raising venture capital is easy. In reality, it’s very, very difficult and not the best source of capital for most businesses.

For startups hoping to scale far and wide as fast as possible, VC may be the right fit. To shed light on the process of raising equity capital from venture capital firms and provide some exclusive tips and tricks for Extra Crunch subscribers, we sat down with three experts on the subject. Below are the top pieces of advice from Charles Hudson, founder and managing partner of Precursor Ventures, Redpoint Ventures general partner Annie Kadavy, and DocSend founder Russ Heddleston. The following has been lightly edited for length and clarity.

Charles Hudson: I think venture capital, it’s really a specialty type of capital. It’s really for companies that have the aspiration to grow really quickly, to build really large businesses … If you’re not a company that needs to grow quickly, venture capital might not be the right source of capital for you. There has to be a really big prize at the end of the journey.

Russ Heddleston: If you’re thinking about whether or not to raise, there are a couple of reasons that I will often advise people to raise early. One is if they’re really stressing about buying a whiteboard for their office, or like some something of relatively small cost. If you think it could be a big company, and you’re stressing about small things, raise money and buy the whiteboard, hire the additional person and get back to what you should be doing, which is running your business and growing it quickly.

The other thing is if you ask the question, ‘is there a competitor I don’t know about?’ If you heard tomorrow, that competitor just raised $2 million, or $5 million or $10 million, how nervous would that make you? For some businesses, you’re like, I don’t really care, it’s a services industry, it’s not a winner take all market. And other times, you’re like, oh, I’d be really nervous. So if either those apply, that’s a good reason to make a compelling case to someone like Charles.

The number one thing you can do to get a VC’s attention is make [your pitch] really simple. Precursor Ventures’ Charles Hudson

Annie Kadavy: I’d be hard-pressed to think of an example where a founder is not paying themselves, the question, though, is how much? You’re paying yourself enough so that the basic costs of life and running your business are not giving you anxiety, because as an early stage investor one of our primary roles is to try and keep the baseline stress as low as it can be, because it’s really hard to go build a company.

If a founder is coming in at the Series A and they say I’m going to go pay myself $300,000, we might be like, well, that doesn’t really feel right, shouldn’t you want to put some of that money into the company? The ranges I’ve seen are anything from $60,000 up to probably $120,000 at the Series A, or maybe $150,000. Then, as the company grows and as the balance sheet grows and it’s de-risked, your salary as an executive at the company will scale with that.

Powered by WPeMatico

There are a lot of people who never thought they’d see the day venture capitalists would funnel millions into femtech businesses, direct-to-consumer tampon retailers no less. But that’s our new reality and Cora is proof.

San Francisco-based Cora, which develops and sells organic tampons, pads and other personal care products, has just closed a $7.5 million Series A led by Harbinger Ventures. Cora is one of many femtech startups to raise funding this week alone, in what is turning out to be a red-hot year for VC investment in the space.

Femtech, defined as any software, diagnostics, products and services that leverage technology to improve women’s health, has attracted at least $241 million in VC funding so far this year, according to PitchBook. That puts the sector on pace to secure nearly $1 billion in investment by year-end, greatly surpassing last year’s record of $650 million. For more historical context, startups in the space brought in only $62 million in 2012, $225 million in 2014 and $231 million in 2016.

“Investors have realized there is a huge pent-up demand in the market for healthier products for women,” Cora co-founder Molly Hayward tells TechCrunch. “The way in which the VC world is structured, there just has not been a lot of representation. It’s really difficult to understand the value of a product you aren’t ever going to use or to understand a problem you aren’t ever going to have, particularly around period care. This isn’t something we were talking about as a society five years ago.”

The four-year-old startup operates a little differently than your run-of-the-mill D2C company. Like TOMS, the popular footwear brand, Cora donates a month’s supply of products for every month’s supply sold. To date, Cora has donated 5 million pads to girls in India and Kenya and 100,000 products to women in the U.S.

“To me, [Cora] was this incredible, holistic opportunity to change the way that women experience their period,” Hayward said.

Investors must be excited about Cora’s growth. Though she didn’t disclose specific numbers, Hayward says the brand has expanded 400 percent year-over-year, a metric they are expecting to sustain with this new bout of funding. Cora’s products are sold on a subscription basis, with prices ranging from $8 per month for six tampons to $16 per month for 24. For those unfamiliar with the costs of such products, $8 for six tampons comes at quite the premium. A box of 50 Playtex tampons, for example, retails for around $9.

Investors must be excited about Cora’s growth. Though she didn’t disclose specific numbers, Hayward says the brand has expanded 400 percent year-over-year, a metric they are expecting to sustain with this new bout of funding. Cora’s products are sold on a subscription basis, with prices ranging from $8 per month for six tampons to $16 per month for 24. For those unfamiliar with the costs of such products, $8 for six tampons comes at quite the premium. A box of 50 Playtex tampons, for example, retails for around $9.

In Cora’s case, customers are shelling out extra cash for millennial-inspired branding, a soothing unboxing experience and a general ease of access to its products, as well as Cora’s organic, hypoallergenic and compostable materials, which aren’t characteristic of many similar products on the market.

Cora plans to use the capital to put more of its items in Target stores, where it already sells its tampons and pads, and expand its portfolio of products. As part of the funding, Cora has added two more women to its board of directors: Lisa Bougie, the former GM of Stitch Fix, and Andrea Freedman, the former chief financial officer of Method. Its board is now 80 percent female.

Powered by WPeMatico

Backed with nearly $87 million in venture capital funding from GV, Oak HC/FT and F-Prime Capital, Quartet Health was founded in 2014 by Arun Gupta, Steve Shulman and David Wennberg to improve access to behavioral healthcare. Its mission: “enable every person in our society to thrive by building a collaborative behavioral and physical health ecosystem.”

Recent shakeups within the New York-based company’s c-suite and a perusal of its Glassdoor profile suggest Quartet’s culture is not fully in line with its own philosophy.

In the last few weeks, chief product officer Rajesh Midha has left the company and president and chief operating officer David Liu is on his way out, TechCrunch has learned and confirmed with Quartet. Founding chief executive officer Arun Gupta, meanwhile, has stepped into the executive chairman role, relinquishing responsibility of the company’s day-to-day operations to former chief science officer David Wennberg, who’s taken over as CEO.

“I’m focusing on our external growth,” Gupta told TechCrunch on Friday. “David has really stepped up as CEO.”

Gupta and Wennberg said Liu’s role was no longer needed because Wennberg had assumed his responsibilities. Liu will formally exit the company at the end of the month. As for its product chief, the pair say Midha had “transitioned out” of the role and that an unnamed internal candidate was tapped to replace him.

When asked whether other employees had left in recent weeks, Wennberg provided the following indeterminate statement: “We are always having people coming in. I don’t think we’ve had any unusual turnover. We’re hiring and people’s roles change and that’s just part of growth.”

Quartet, which provides a platform that allows providers to collaborate on treatment plans, currently has 150 employees, according to its executives.

In a LinkedIn status update published this week — after TechCrunch’s initial inquiries — Gupta announced his transition to executive chairman:

“Still full-time, though focused largely on our opportunity to further evangelize our mission, [I will] drive the change we want to see in this world, and expand our reach … I have tremendous confidence in David’s ability to lead our many talented Quartetians to deliver this next phase.”

Several former employees seemed less than pleased with Gupta’s performance, writing in a number of Glassdoor reviews that he was “abominable,” “kind of a monster” and “by far the worst executive.”

When asked for comment on those reviews, Gupta and Wennberg shrugged it off: “Glassdoor is Glassdoor.” They agreed its important to pay attention to but impossible to vet.

Gupta began his career as a management consultant at McKinsey and served as a consultant to The World Bank before joining Palantir, Peter Thiel’s data-mining company, as an advisor in 2014. Wennberg, for his part, was the CEO of The High Value Healthcare Collaborative, a consortium of 15 healthcare delivery systems, before co-founding Quartet.

In January, Quartet raised a $40 million Series C to expand throughout the U.S. F-Prime Capital and Polaris Partners led the round, with participation from GV and Oak HC/FT. The financing valued the company at $300 million, according to PitchBook.

As part of the funding, Quartet announced it was adding three new directors to its board: F-Prime’s executive partner Carl Byers; Ken Goulet, an executive vice president at health insurance provider Anthem; and former Rackspace CEO and BuildGroup co-founder Lanham Napier. Other outside board members include Oak HC/FT’s managing partner Annie Lamont, GV partner Krishna Yeshwant, Polaris managing partner Brian Chee and former U.S. Congressman Patrick Kennedy.

Quartet previously raised a $40 million Series B in April 2016 led by GV. The investment marked the venture capital investment arm of Google’s first in a mental health startup. Before that, the startup brought in a $7 million Series A led by Oak HC/FT’s managing partner Annie Lamont.

For now, Quartet remains committed to growth.

“We learn from what we are doing and we continue to learn,” Wennberg said. “That is part of growth. It’s hard and you just keep working and growing because we have a huge mission.”

Powered by WPeMatico

In the days leading up to TechCrunch Disrupt SF 2018, The Economist published the cover story, ‘Why Startups Are Leaving Silicon Valley.’

The author outlined reasons why the Valley has “peaked.” Venture capital investors are deploying capital outside the Bay Area more than ever before. High-profile entrepreneurs and investors, Peter Thiel, for example, have left. Rising rents are making it impossible for new blood to make a living, let alone build businesses. And according to a recent survey, 46 percent of Bay Area residents want to get the hell out, an increase from 34 percent two years ago.

Needless to say, the future of Silicon Valley was top of mind on stage at Disrupt.

“It’s hard to make a difference in San Francisco as a single entrepreneur,” said J.D. Vance, the author of ‘Hillbilly Elegy’ and a managing partner at Revolution’s Rise of the Rest Fund, which backs seed-stage companies based outside Silicon Valley. “It’s not as a hard to make a difference as a successful entrepreneur in Columbus, Ohio.”

In conversation with Vance, Revolution CEO Steve Case said he’s noticed a “mega-trend” emerging. Founders from cities like Pittsburgh, Detroit or Portland are opting to stay in their hometowns instead of moving to U.S. innovation hubs like San Francisco.

“The sense that you have to be here or you can’t play is going to start diminishing.”

“We are seeing the beginnings of a slowing of what has been a brain drain the last 20 years,” Case said. “It’s not just watching where the capital flows, it’s watching where the talent flows. And the sense that you have to be here or you can’t play is going to start diminishing.”

J.D. Vance says that most entrepreneurs don’t need to move to Silicon Valley.

Here’s why. #TCDisrupt pic.twitter.com/0mFPeTuHLe

— TechCrunch (@TechCrunch) September 6, 2018

Farewell, San Francisco

“It’s too expensive to live here,” said Aileen Lee, the founder of seed-stage VC firm Cowboy Ventures, amid a conversation with leading venture capitalists Spark Capital general partner Megan Quinn and Benchmark general partner Sarah Tavel .

“I know that there are a lot of people in the Bay Area that are trying to work on that problem and I hope that they are successful,” Lee added. “It’s an amazing place to live and we’ve made it really challenging for people to live here and not worry about making ends meet.”

One of Cowboy’s portfolio companies opted to relocate from Silicon Valley to Colorado when it came time to scale their business. That kind of move would’ve historically been seen as a failure. Today, it may be a sign of strong business acumen.

Quinn said that of all 28 of Spark’s growth-stage portfolio companies, Raleigh, North Carolina-based Pendo has the easiest time recruiting folks locally and from the Bay Area.

She advises her Bay Area-based late-stage companies to open a second office outside of the Valley where lower-cost talent is available.

“We often say go to [flySFO.com], draw a three-hour circle around San Francisco where they have direct flights, find a city that has a university and open up a second office as quickly as possible,” Quinn said.

Still, all three firms invest in a lot of companies based in San Francisco. Of Benchmark’s 10 most recent investments, for example, eight were based in SF, according to Crunchbase.

“I used to believe really strongly if you wanted to build a multi-billion dollar company you had to be based here,” Tavel said. “I’ve stopped giving that soap speech.”

Aileen Lee (Cowboy Ventures), Megan Quinn (Spark Capital), and Sarah Tavel (Benchmark Capital) on whether or not Silicon Valley is on the wane for investors #TCDisrupt pic.twitter.com/SOpn7p0eNQ

— TechCrunch (@TechCrunch) September 5, 2018

Underestimated talent

A lot of Bay Area VCs have been blind to the droves of tech talent located outside the region. Believe it or not, there are great engineers in America’s small- and medium-sized markets too.

At Disrupt, Backstage Capital founder Arlan Hamilton announced the firm would launch an accelerator to further amplify companies led by underestimated founders. The program will have cohorts based in four cities; San Francisco was noticeably absent from that list.

Instead, the firm, which invests in underrepresented founders and recently raised a $36 million fund, will work with companies in Philadelphia, Los Angeles, London and one more city, which will be determined by a public vote. Aniyia Williams, the founder of Tinsel and Black & Brown Founders, will spearhead the Philadelphia effort.

“For us, it’s about closing that wealth gap to address inequity in tech,” Williams said. “There needs to be more active participation from everyone.”

Hamilton added that for her, the tech talent in LA and London is undeniable.

“There is a lot of money and a lot of investors … it reminds me of three years ago in Silicon Valley,” Hamilton said.

Silicon Valley vs. China

Silicon Valley’s demise may not be just as a result of increased costs of living or investors overlooking talent in other geographies. It may be because of heightened competition abroad.

Doug Leone, an early- and growth-stage investor at Sequoia Capital, said at Disrupt that he’s noticed a very different work ethic in China.

Chinese entrepreneurs, he explained, are more ruthless than their American counterparts and they’re putting in a whole lot more hours.

Doug Leone of Sequoia Capital says founders in the US and China both want to change the world, but Chinese founders are a little more desperate (and you see it in the crazy work ethic they have).#TCDisrupt pic.twitter.com/dPxsRTbJoq

— TechCrunch (@TechCrunch) September 6, 2018

“I’ve had dinner in China until after 10 p.m. and people go to work after 10 p.m.,” Leone recalled.

“We don’t see that in the U.S. I’m not saying the U.S. founders oughta do that but those are the differences. They are similar in character. They are similar in dreams. They are similar in how they want to change the world. They are ultra-driven … The Chinese founders have a half other gear because I think they are a little more desperate.”

Much of this, however, has been said before and still, somehow, Silicon Valley remained the place to be for investors and startup entrepreneurs.

The reality is, those engaged in tech culture are always anxiously awaiting for the bubble to pop, the market to crash and for “peak Valley” to finally arrive.

Maybe, just maybe, Silicon Valley is forever.

Here’s more of our coverage of Disrupt 2018.

Powered by WPeMatico

Sometimes smart contracts can be pretty dumb.

All of the benefits of a cryptographically secured, publicly verified, anonymized transaction system can be erased by errant code, malicious actors or poorly defined parameters of an executable agreement.

Hoping to beat back the tide of bad contracts, bad code and bad actors, Sagewise, a new Los Angeles-based startup, has raised $1.25 million to bring to market a service that basically hits pause on the execution of a contract so it can be arbitrated in the event that something goes wrong.

Co-founded by a longtime lawyer, Amy Wan, whose experience runs the gamut from the U.S. Department of Commerce to serving as counsel for a peer-to-peer real estate investment platform in Los Angeles, and Dan Rice, a longtime entrepreneur working with blockchain, Sagewise works with both Ethereum and the Hedera Hashgraph (a newer distributed ledger technology, which purports to solve some of the issues around transaction processing speed and security which have bedeviled platforms like Ethereum and Bitcoin).

The company’s technology works as a middleware, including an SDK and a contract notification and monitoring service. “The SDK is analogous to an arbitration clause in code form — when the smart contract executes a function, that execution is delayed for a pre-set amount of time (i.e. 24 hours) and users receive a text/email notification regarding the execution,” Wan wrote to me in an email. “If the execution is not the intent of the parties, they can freeze execution of the smart contract, giving them the luxury of time to fix whatever is wrong.”

Sagewise approaches the contract resolution process as a marketplace where priority is given to larger deals. “Once frozen, parties can fix coding bugs, patch up security vulnerabilities, or amend/terminate the smart contract, or self-resolve a dispute. If a dispute cannot be self-resolved, parties then graduate to a dispute resolution marketplace of third party vendors,” Wan writes. “After all, a $5 bar bet would be resolved differently from a $5M enterprise dispute. Thus, we are dispute process agnostic.”

Wavemaker Genesis led the round, which also included strategic investments from affiliates of Ari Paul (Blocktower Capital), Miko Matsumura (Gumi Cryptos), Youbi Capital, Maja Vujinovic (Cipher Principles), Jordan Clifford (Scalar Capital), Terrence Yang (Yang Ventures) and James Sowers.

“Smart contracts are coded by developers and audited by security auditing firms, but the quality of smart contract coding and auditing varies drastically among service providers,” said Wan, the chief executive of Sagewise, in a statement. “Inevitably, this discrepancy becomes the basis for smart contract disputes, which is where Sagewise steps in to provide the infrastructure that allows the blockchain and smart contract industry to achieve transactional confidence.”

In an email, Wan elaborated on the thesis to me, writing that, “smart contracts may have coding errors, security vulnerabilities, or parties may need to amend or terminate their smart contracts due to changing situations.”

Contracts could also be disputed if their execution was triggered accidentally or due to the actions of attackers trying to hack a platform.

“Sagewise seeks to bring transactional confidence into the blockchain industry by building a smart contract safety net where smart contracts do not fulfill the original transactional intent,” Wan wrote.

Powered by WPeMatico

The dream of a startup founder can often be summarized by the following well-intentioned, and mostly delusional, quote: “We’ll raise a few rounds and in a few years we’ll IPO on Nasdaq.”

But a more likely scenario looks something like this:

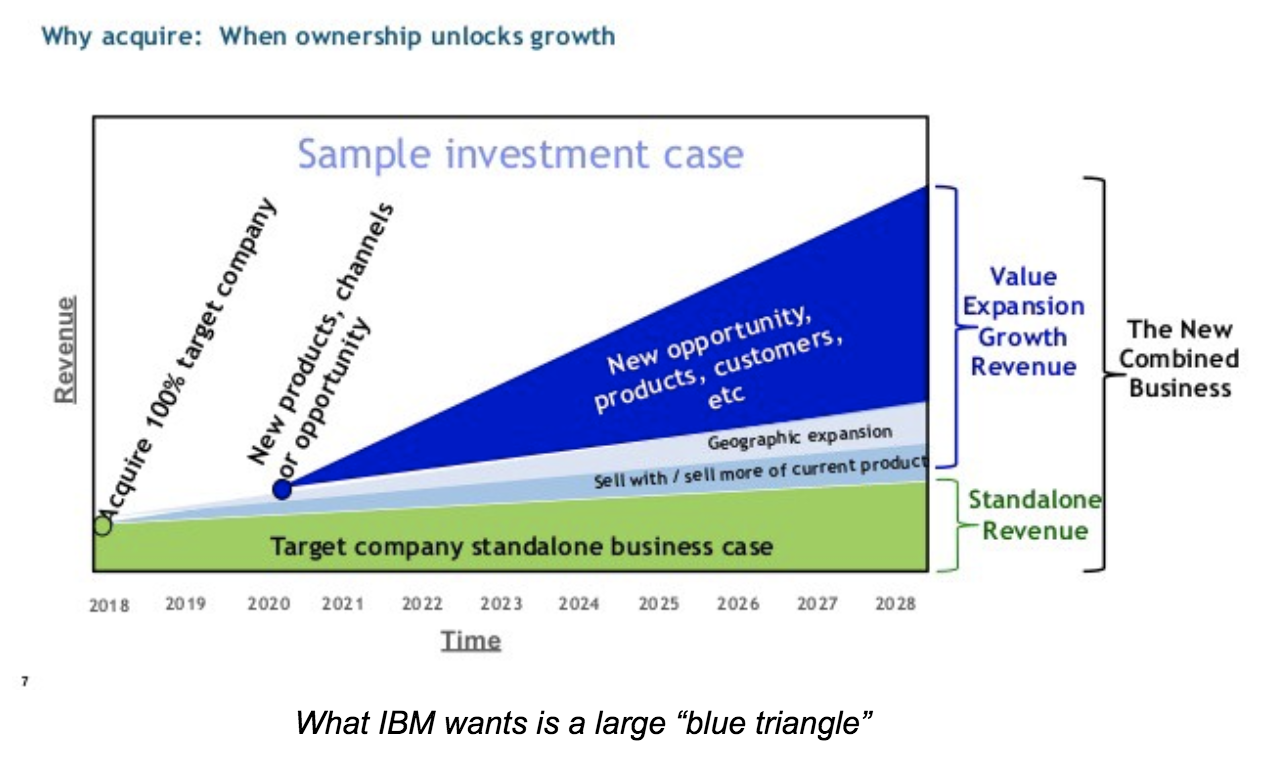

You invest a few years of hard work to build something of value. One day you receive an acquisition offer out of the blue. You’re elated. And you’re not prepared. You drop everything to focus on this opportunity. Exclusive due diligence starts. Your company is a mess (IP, contracts, burn). Days become weeks; weeks become months. You’ve neglected business and fundraising. You’re running out of money. M&A is now your one and only option. The buyer says they found a bunch of cockroaches in the walls and drops the price. Now what?

Sound unlikely?

This is still a favorable situation: You had an offer! Think about how much time you invested in your various funding rounds. The hundreds of names and Google spreadsheet or Streak-powered quasi-CRM process.

Have you spent even a fraction of that on understanding exit paths? If you’d rather not live the situation described above, read along.

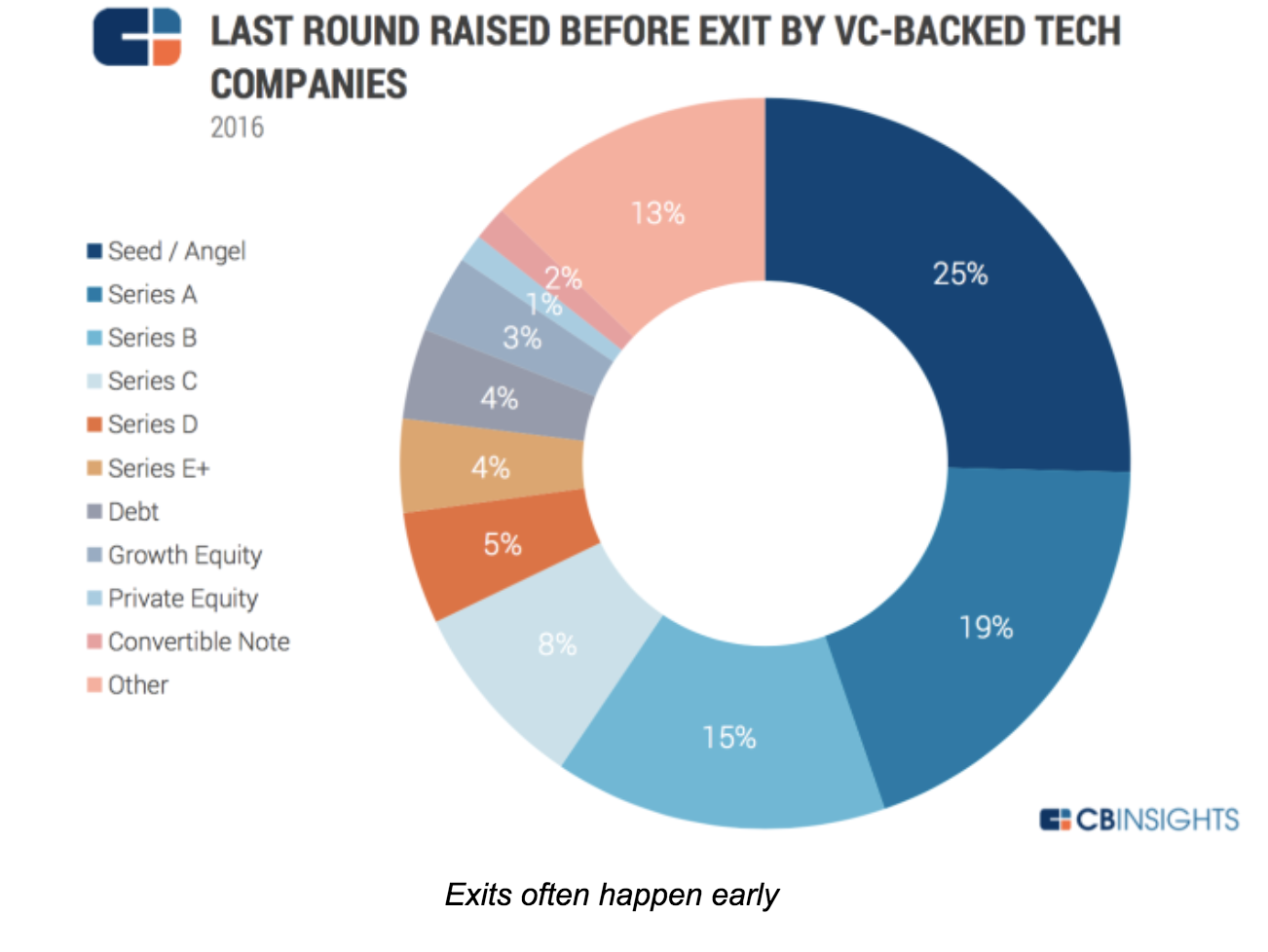

Investors live by exits, but many founders keep dreaming of unicornization and avoid the “E-word” until it’s too late. Yet, in 2016, 97 percent of exits were M&As. And most happened before Series B.

Exits matter because that’s when you, your team and your investors get paid. Oddly enough, and to use a chess metaphor, we hear a lot about the “opening game” (lean startup) and the “mid-game” (growth), but very little about this “end game.”

As a result, founders miss opportunities or leave money on the table. This is a shame. Our fund has more than 700 companies in portfolio. We want the best possible exit for each of them. And fortune favors the prepared! Now, how to get 700 exits (and counting)?

To explore the topic, we organized a series of Master Classes tapping corporate buyers, bankers, investors, lawyers and startup CEOs with M&A or IPO experience in San Francisco. It was a group that included the founders of Guitar Hero — bought by Activision; JUMP Bikes — a SOSV portfolio company bought by Uber, Ubiquisys — bought by Cisco and Withings — bought by Nokia. Each one for hundreds of millions.

Their observations can be summarized below.

“Founders must be aware of what contributes to an exit. This means understanding partnerships and how they are formed in the business space the entrepreneur is working in,” said one Master Class participant.

As founders, you build your product, your company and… optionality. You need to understand the options open to your company, and take steps to enable them.

The most likely one is an acquisition, but there are others like IPO (including small cap), RTO, SBO, LBO, Equity Crowdfunding and even ICO.

“Exit is not a goal per se, but as a CEO it is something you should think about as early in your cycle as possible, while being business-focused,” said the London-based investor Frederic Rombaut, of Seraphim Capital.

Indeed, most participants said that exits should always be on the chief executive’s agenda, no matter how early in the process. “Exits should be on the CEO agenda. Not front and center, but on the agenda. M&A is a by-product of a great business and targeted BD. IPOs are always an option once you’ve built significant cashflow forecasting.”

It’s important to ask questions like: How many “strategic engagements” with potential buyers have you had this month? Is your message and value clear in their eyes? Have you considered an acquisition track in parallel to a fundraise?

It doesn’t stop there:

One thing is sure: The time to exit is not when you’re running out of money.

Unicorn or not, the most likely exit is an acquisition.

As George Patterson, managing director at HSBC in New York said, “Good tech companies are bought, not sold. The question is thus: how to get bought?”

Patterson says it’s important to understand how mergers and acquisitions actually work; how to prepare a startup for an exit; and how to develop a “feel” for the market you’re exiting through and into.

Hearing from corp dev veterans from Cisco, Logitech, Dassault and IBM, a few key ideas emerged:

Motivations vary

It could be from least to most expensive, or as a mix, as listed by Mark Suster, managing partner at Upfront Ventures:

How corporates find you

Corporates find deals via the development of partnerships, investment (CVC), their business units, corp dev research, media and investor connections.

Asked about the best approach, Todd Neville, manager of Corporate Business Development and Strategy at IBM (who gave the most detailed description of the corp dev process), said, “Do something cool to one of the IBM customers. If they rave about even a POC, we’re interested.”

In other words, business development is corporate development.

Get the house in order

Buyers typically want to know three things:

For IP, they will check your contracts (staff and contractors), and run some automated code analysis for proprietary code and open source use. They will evaluate potential IP infringement. No point buying you if you end up costing more in lawsuits!

For your team skills: Sitting down with your engineers will tell them plenty enough without understanding the details of this or that algorithm. The last thing a corporate wants is to be accused of stealing!

Lawyers engaged early can help. The later the clean-up, the more costly and painful.

Develop a feel for your “market”

Develop relationships and create champions within corporates. It will help promote your deal when the time comes, and will let you keep your finger on the pulse of corporate strategy to time your moves.

Do you read the earning calls of Cisco or IBM (or others relevant to you)? This is where strategies are presented. Are your keywords coming up there or in their press releases?

Chris Gilbert, former CEO of Ubiquisys (sold to Cisco for more than $300 million) was very deliberate in planning his exit.

“Selling starts on day one and is a leadership-only function — work out who will be your buyer. Only the CEO can do this. Constantly articulate why a company should buy you,” Gilbert said. Bring clear messages into the acquiring company so it can be presented upwards: give them the presentation you would like them to show their boss! When the time is right, force decisions through competition. If you know they have to buy you, your starting position is strong.”

The dark art of price discovery

There are dozens of formulas (from DCF to comparables) to evaluate a deal — which also means none is “correct.” What matters is: How much would you sell for, and how much is the buyer ready to pay?

Gilbert, at Ubiquisys, described how close interactions with his banker helped drive the price up among the bidders assembled.

Just like buyers, we meet bankers and lawyers too rarely at startup events, but there is much to learn with them. They make deals happen, avoid value erosion and optimize price. They often also make introductions before you engage them, to build goodwill and earn your business.

And if you worry about fees, the right banker handsomely pays for itself by finding more bidders and playing “bad cop” for you, avoiding direct confrontation with your future employer. Do you want a slice of the watermelon or the whole grape?

When asked about what happens after an M&A or IPO, buyers said they generally hoped the founders would stay with them for many years. Often using re-vesting, earn-outs or shares of the acquiring company to incentivize them. Neville, from IBM, mentioned a security company they acquired whose founder is now the head of one of the largest IBM divisions.

In the case of IPOs, supposedly the ultimate “exit,” any block of shares sold by founders would face extreme scrutiny and might cause a price drop.

So who’s exiting during those deals? Investors (and not always).

Eventually, if the average age of a startup at exit is 8-10 years, the active duty period of founders (if not replaced in the meantime) extends even more. Better love the problem you’re solving, and your customers!

Thanks to speakers, participants and supporters of this Master Class series:

London: Frederic Rombaut (Seraphim Capital), Joe Tabberer (FirstBank), Chris Gilbert (Ubiquisys), Jonathan Keeling (Crowdcube), Fred Destin, Tony Fish (AMF Ventures, James Clark (London Stock Exchange), Denise Law (SGCIB).

Paris: Frederic Rombaut (Seraphim Capital), Manuel Gruson (Dassault Systemes), Pierre-Henri Chappaz (Rothschild Global Advisory), Christine Lambert-Goue (All Invest), Olivier Younes (EXPEN), Eric Carreel (Withings), Fabien Bardinet (Balyo), Xavier Lazarus (Elaia Partners), Pierre-Eric Leibovici(Daphni). Jean de La Rochebrochard (Kima Ventures), Jeremy Sartre (SmartAngels), Gwen Regina Tan (Entrepreneur First).

San Francisco: Natasha Ligai (Logitech), Matt Cutler (Cisco),Will Hawthorne, (CODE Advisors), Ryan Rzepecki (JUMP Bikes), Charles Huang (Guitar Hero), Jeff Thomas (Nasdaq), Shahin Farshchi (Lux Capital), Ammar Hanafi (Moment Ventures), Adam J. Epstein (Third Creek Advisors), Nathan Harding (EKSO Bionics), Kate Whitcomb, Anthony Marino and Ethan Haigh (SOSV).

New York: Todd Neville (IBM), George Patterson (HSBC), Ryan Rzepecki (JUMP Bikes), Aaron Kellner (SeedInvest), Jeremy Levine (Bessemer Venture Partners), Taylor Greene (Collaborative Fund), Adam Rothenberg (BoxGroup), Eli Curi (Fenwick & West), Ian Engstrand and Salil Gandhi (Goodwin), Warren Spar(Sparring Partners Capital), Duncan Turner, Vivian Law and Sheng Ge (SOSV).

Powered by WPeMatico