Madrona

Auto Added by WPeMatico

Auto Added by WPeMatico

Coda entered the market with an ambitious, but simple, mission. Since launching in 2014, it has seemingly forged a path to realizing its vision with $140 million in funding and 25,000 teams across the globe using the platform.

Coda is simple in that its focus is on the document, one of the oldest content formats/tools on the internet, and indeed in the history of software. Its ambition lies in the fact that there are massive incumbents in this space, like Google and Microsoft.

Co-founder and CEO Shishir Mehrotra told TechCrunch that that level of competition wasn’t a hindrance, mainly because the company was very good at communicating its value and building highly effective flywheels for growth.

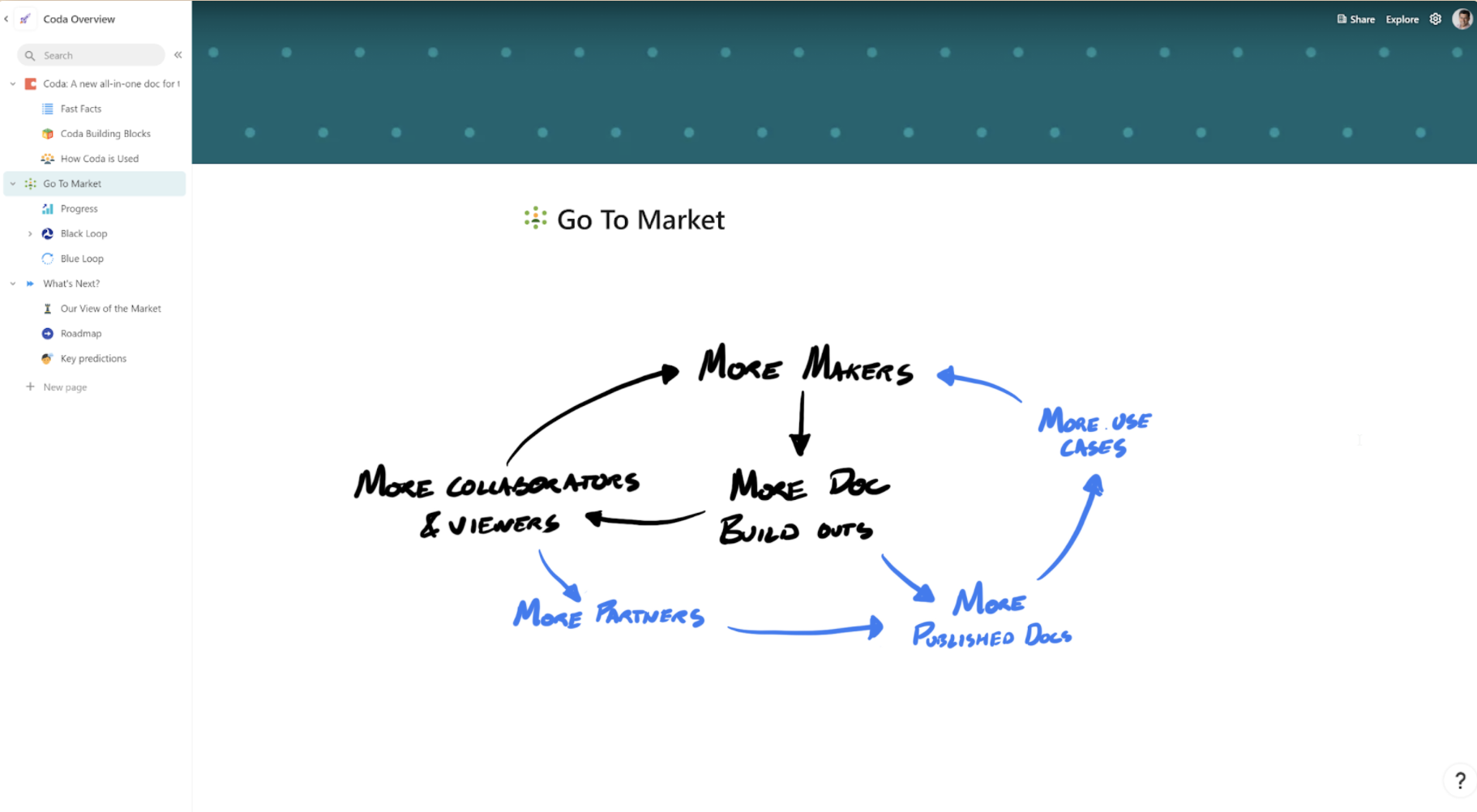

Mehrotra was generous enough to let us take a look through his pitch doc (not deck!) on a recent episode of Extra Crunch Live, diving not only into the factors that have made Coda successful, but how he communicated those factors to investors.

A screenshot from Coda’s pitch doc.

Extra Crunch Live also features the ECL Pitch-off, where founders in the audience come “onstage” to pitch their products to our guests. Mehrotra and his investor, Madrona partner S. Somasegar, gave their live feedback on pitches from the audience, which you can check out in the video (full conversation and pitch-off) below.

As a reminder, Extra Crunch Live takes place every Wednesday at 3 p.m. EDT/noon PDT. Anyone can hang out during the episode (which includes networking with other attendees), but access to past episodes is reserved exclusively for Extra Crunch members. Join here.

Like many investors and founders, Mehrotra and Somasegar met well before Mehrotra was working on his own project. They met when both of them worked at Microsoft and maintained a relationship while Mehrotra was at Google.

In their earliest time together, the conversations centered around advice on the Seattle tech ecosystem or on working with a particular team at Microsoft.

“Many people will tell you building relationships with investors … you want to do it outside of a fundraise as much as possible,” said Mehrotra.

Eventually, Mehrotra got to work on Coda and kept in touch with Somasegar. He even pitched him for Series B fundraising — and ultimately got a no. But the relationship persisted.

Powered by WPeMatico

Snowflake announced earlier this month that it would give up its dual-class shareholder structure, a corporate governance setup that often gives founders and executives superior voting rights, typically involving 10 times as many votes for their own shares as others receive. The mechanism can enable founders to maintain control despite later dilution and may sometimes even grant ironclad control to an individual in perpetuity.

For many companies, these supervoting shares represent a highly powerful tool, allowing founders to have their cake and eat it, too — to go public and receive the advantages of being a public company while limiting the power of external shareholders to influence how they run the company once it floats.

Some founders and their investors argue that these preferred shares protect them from the short-term whims of the market, but the perspective isn’t universally accepted.

Some founders and their investors argue that these preferred shares protect them from the short-term whims of the market, but the perspective isn’t universally accepted. Dual-class shares are a controversial governance structure, and some wonder if they are setting up an unfair playing field by allowing a cabal to wield outsized power.

Why would Snowflake give up such a powerful tool a mere six months after it went public? We decided to look at the notion of dual-class shares and why Snowflake may have been willing to let them go.

If one of the primary purposes of dual-class shares is to consolidate CEO power, then perhaps Snowflake felt they weren’t necessary, given the history of CEO-shuffling at the company. While Snowflake’s founders are still part of the organization, they hired Sutter Hill investor Mike Speiser to be their first CEO, followed by former Microsoft exec Bob Muglia before finally bringing in veteran CEO Frank Slootman to take their company public.

Without an all-powerful CEO founder in place, perhaps the company felt that supervoting shares weren’t necessary. Regardless, Snowflake CFO Mike Scarpelli framed the move as a decision that works for all parties when he announced that his company would abandon the special shares during its earnings call earlier this month.

“Today, we announced that on March 1st, 2021, our Class B shareholders in accordance with our governing documents converted all of our Class B common stock to Class A common stock, eliminating the dual-class structure of our common stock and ensuring that each share has an equal vote. We view this as operationally beneficial to the company and our shareholders,” Scarpelli said during the call.

Powered by WPeMatico

Venture capitalists are still hungry for food delivery startups.

Foodsby, the provider of a lunch delivery service based out of Minneapolis, has raised a $13.5 million Series B led by Piper Jaffray Merchant Banking. Greycroft Partners, Corazon Capital and Rally Ventures also participated. With the new capital, Foodsby plans to expand to 15 to 25 new markets. The round brings Foodsby’s total raised to $21 million.

“We have established a successful model for new market entry with a tried and true combination of talent and technology,” Foodsby founder and CEO Ben Cattoor said in a statement. “We look forward to building on our early successes and learnings to deliver continued growth for our investors and our team.”

Founded in 2012, the company connects employees in office buildings in 15 cities with local restaurants. How it works: A hungry worker uses Foodsby to pre-order a meal from a restaurant in its network, Foodsby aggregates all the orders it receives, sends the orders to the restaurants and the restaurants then make all the deliveries at once, streamlining what can be a logistically complicated process.

That strategy, the company says, sets Foodsby apart from competitors. Because Foodsby only works with businesses and has restaurants make the deliveries rather than its own fleet of delivery agents, the overall costs of the operation are lower. It’s free to join the Foodsby network as both a company that wants to provide the service to its employees and as a restaurant. Deliveries cost $1.99 per person.

While continued VC support may give the company a vote of confidence, the food delivery space is crowded and competitive. Foodsby is not unlike Peach, a Seattle-based office lunch delivery service that shed one-third of its staff in March. Peach had also landed VC support, raising about $11 million from Madrona and others. Munchery, another similar meal delivery service, also looks to be in hot water, laying off 30 percent of its workforce in May and ceasing operations in Los Angeles, Seattle and New York.

Food delivery startups are hit or miss, but VCs continue to flock to investment rounds in hopes of betting on the next Uber of food delivery — though Uber itself is really the Uber of food delivery, its food delivery service is reportedly the most profitable arm of the ride-hailing giant. And Uber, much like Amazon, is not a company you want to be going head-to-head with.

Powered by WPeMatico