machine learning

Auto Added by WPeMatico

Auto Added by WPeMatico

Just months after raising $28 million, Jerry announced today that it has raised $75 million in a Series C round that values the company at $450 million.

Existing backer Goodwater Capital doubled down on its investment in Jerry, leading the “oversubscribed” round. Bow Capital, Kamerra, Highland Capital Partners and Park West Asset Management also participated in the financing, which brings Jerry’s total raised to $132 million since its 2017 inception. Goodwater Capital also led the startup’s Series B earlier this year. Jerry’s new valuation is about “4x” that of the company at its Series B round, according to co-founder and CEO Art Agrawal.

“What factored into the current valuation is our annual recurring revenue, growing customer base and total addressable market,” he told TechCrunch, declining to be more specific about ARR other than to say it is growing “at a very fast rate.” He also said the company “continues to meet and exceed growth and revenue targets” with its first product, a service for comparing and buying car insurance. At the time of the company’s last raise, Agrawal said Jerry saw its revenue surge by “10x” in 2020 compared to 2019.

Jerry, which says it has evolved its model to a mobile-first car ownership “super app,” aims to save its customers time and money on car expenses. The Palo Alto-based startup launched its car insurance comparison service using artificial intelligence and machine learning in January 2019. It has quietly since amassed nearly 1 million customers across the United States as a licensed insurance broker.

“Today as a consumer, you have to go to multiple different places to deal with different things,” Agrawal said at the time of the company’s last raise. “Jerry is out to change that.”

The new funding round fuels the launch of the company’s “compare-and-buy” marketplaces in new verticals, including financing, repair, warranties, parking, maintenance and “additional money-saving services.” Although Jerry also offers a similar product for home insurance, its focus is on car ownership.

Image Credits: Jerry

“Access to reliable and affordable transportation is critical to economic empowerment,” said Rafi Syed, Jerry board member and general partner at Bow Capital, which also doubled down on its investment in the company. “Jerry is helping car owners make the most of every dollar they earn. While we see Jerry as an excellent technology investment showcasing the power of data in financial services, it’s also a high-performing investment in terms of the financial inclusion it supports.”

Goodwater Capital Partner Chi-Hua Chien said the firm’s recurring revenue model makes it stand out from lead generation-based car insurance comparison sites.

CEO Agrawal agrees, noting that Jerry’s high-performing annual recurring revenue model has made the company “attractive to investors” in addition to the fact that the startup “straddles” the auto, e-commerce, fintech and insurtech industries.

“We recognized those investment opportunities could drive our business faster and led to raising the round earlier than expected,” he told TechCrunch. “We’re eager to launch new categories to save customers time and money on auto expenses and the new investment shortens our time to market.”

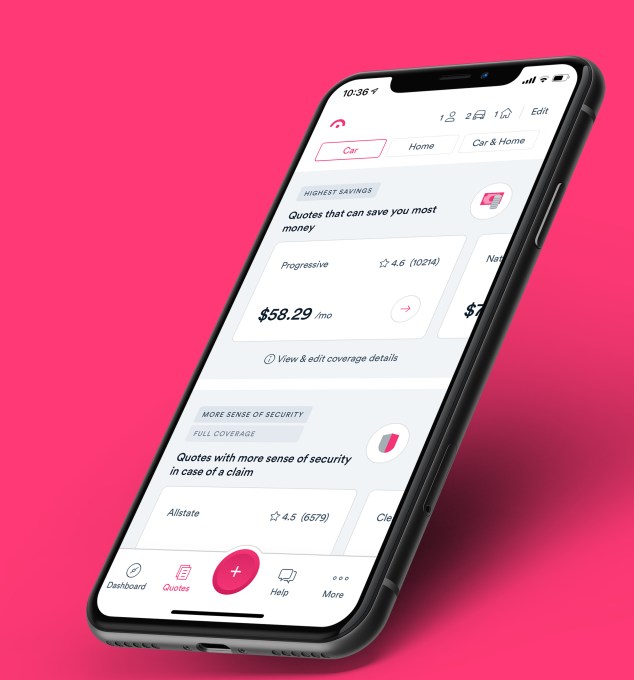

Agrawal also believes Jerry is different from other auto-related marketplaces out there in that it aims to help consumers with various aspects of car ownership (from repair to maintenance to insurance to warranties), rather than just one. The company also believes it is set apart from competitors in that it doesn’t refer a consumer to an insurance carrier’s site so that they still have to do the work of signing up with them separately, for example. Rather, Jerry uses automation to give consumers customized quotes from more than 45 insurance carriers “in 45 seconds.” The consumers can then sign on to the new carrier via Jerry, which can then cancel former policies on their behalf.

Jerry makes recurring revenue from earning a percentage of the premium when a consumer purchases a policy on its site from carriers such as Progressive.

Powered by WPeMatico

With the fourth quarter now upon us, every industry faces a challenge in managing a holiday production calendar that will deliver the goods. The key for startups looking to defend the quarter from disruptions is to adopt a proactive, data-driven approach to inventory management.

Here are five methods we’ve been counseling clients to adopt:

Ultimately, AI will help startups understand how myriad disruptions affect their supply chain so they can better respond with a Plan B when the unthinkable happens.

Powered by WPeMatico

Two decades after businesses first started deploying AI solutions, one can argue that they’ve made little progress in achieving significant gains in efficiency and profitability relative to the hype that drove initial expectations.

On the surface, recent data supports AI skeptics. Almost 90% of data science projects never make it to production; only 20% of analytics insights through 2022 will achieve business outcomes; and even companies that have developed an enterprisewide AI strategy are seeing failure rates of up to 50%.

But the past 25 years have only been the first phase in the evolution of enterprise AI — or what we might call Enterprise AI 1.0. That’s where many businesses remain today. However, companies on the leading edge of AI innovation have advanced to the next generation, which will define the coming decade of big data, analytics and automation — Enterprise AI 2.0.

The difference between these two generations of enterprise AI is not academic. For executives across the business spectrum — from healthcare and retail to media and finance — the evolution from 1.0 to 2.0 is a chance to learn and adapt from past failures, create concrete expectations for future uses and justify the rising investment in AI that we see across industries.

Two decades from now, when business leaders look back to the 2020s, the companies who achieved Enterprise AI 2.0 first will have come to be big winners in the economy, having differentiated their services, scooped up market share and positioned themselves for ongoing innovation.

Framing the digital transformations of the future as an evolution from Enterprise AI 1.0 to 2.0 provides a conceptual model for business leaders developing strategies to compete in the age of automation and advanced analytics.

Starting in the mid-1990s, AI was a sector marked by speculative testing, experimental interest and exploration. These activities occurred almost exclusively in the domain of data scientists. As Gartner wrote in a recent report, these efforts were “alchemy … run by wizards whose talents will not scale in the organization.”

Powered by WPeMatico

The President’s Council of Advisors on Science and Technology predicts that U.S. companies will spend upward of $100 billion on AI R&D per year by 2025. Much of this spending today is done by six tech companies — Microsoft, Google, Amazon, IBM, Facebook and Apple, according to a recent study from CSET at Georgetown University. But what if you’re a startup whose product relies on AI at its core?

Can early-stage companies support a research-based workflow? At a startup or scaleup, the focus is often more on concrete product development than research. For obvious reasons, companies want to make things that matter to their customers, investors and stakeholders. Ideally, there’s a way to do both.

Before investing in staffing an AI research lab, consider this advice to determine whether you’re ready to get started.

Assuming it’s your organization’s priority to do innovative AI research, the first step is to hire one or two researchers. At Unbabel, we did this early by hiring Ph.D.s and getting started quickly with research for a product that hadn’t been developed yet. Some researchers will build from scratch and others will take your data and try to find a pre-existing model that fits your needs.

While Google’s X division may have the capital to focus on moonshots, most startups can only invest in innovation that provides them a competitive advantage or improves their product.

From there, you’ll need to hire research engineers or machine learning operations professionals. Research is only a small part of using AI in production. Research engineers will then release your research into production, monitor your model’s results and refine the model if it stops predicting well (or otherwise is not operating as planned). Often they’ll use automation to simplify monitoring and deployment procedures as opposed to doing everything manually.

None of this falls within the scope of a research scientist — they’re most used to working with the data sets and models in training. That said, researchers and engineers will need to work together in a continuous feedback loop to refine and retrain models based on actual performance in inference.

The CSET research cited above shows that 85% of AI labs in North America and Europe do some form of basic AI research, and less than 15% focus on development. The rest of the world is different: A majority of labs in other countries, such as India and Israel, focus on development.

Powered by WPeMatico

Environmental, social and governance (ESG) factors should be key considerations for CTOs and technology leaders scaling next generation companies from day one. Investors are increasingly prioritizing startups that focus on ESG, with the growth of sustainable investing skyrocketing.

What’s driving this shift in mentality across every industry? It’s simple: Consumers are no longer willing to support companies that don’t prioritize sustainability. According to a survey conducted by IBM, the COVID-19 pandemic has elevated consumers’ focus on sustainability and their willingness to pay out of their own pockets for a sustainable future. In tandem, federal action on climate change is increasing, with the U.S. rejoining the Paris Climate Agreement and a recent executive order on climate commitments.

Over the past few years, we have seen an uptick in organizations setting long-term sustainability goals. However, CEOs and chief sustainability officers typically forecast these goals, and they are often long term and aspirational — leaving the near and midterm implementation of ESG programs to operations and technology teams.

Until recently, choosing cloud regions meant considering factors like cost and latency to end users. But carbon is another factor worth considering.

CTOs are a crucial part of the planning process, and in fact, can be the secret weapon to help their organization supercharge their ESG targets. Below are a few immediate steps that CTOs and technology leaders can take to achieve sustainability and make an ethical impact.

As more businesses digitize and more consumers use devices and cloud services, the energy needed by data centers continues to rise. In fact, data centers account for an estimated 1% of worldwide electricity usage. However, a forecast from IDC shows that the continued adoption of cloud computing could prevent the emission of more than 1 billion metric tons of carbon dioxide from 2021 through 2024.

Make compute workloads more efficient: First, it’s important to understand the links between computing, power consumption and greenhouse gas emissions from fossil fuels. Making your app and compute workloads more efficient will reduce costs and energy requirements, thus reducing the carbon footprint of those workloads. In the cloud, tools like compute instance auto scaling and sizing recommendations make sure you’re not running too many or overprovisioned cloud VMs based on demand. You can also move to serverless computing, which does much of this scaling work automatically.

Deploy compute workloads in regions with lower carbon intensity: Until recently, choosing cloud regions meant considering factors like cost and latency to end users. But carbon is another factor worth considering. While the compute capabilities of regions are similar, their carbon intensities typically vary. Some regions have access to more carbon-free energy production than others, and consequently the carbon intensity for each region is different.

So, choosing a cloud region with lower carbon intensity is often the simplest and most impactful step you can take. Alistair Scott, co-founder and CTO of cloud infrastructure startup Infracost, underscores this sentiment: “Engineers want to do the right thing and reduce waste, and I think cloud providers can help with that. The key is to provide information in workflow, so the people who are responsible for infraprovisioning can weigh the CO2 impact versus other factors such as cost and data residency before they deploy.”

Another step is to estimate your specific workload’s carbon footprint using open-source software like Cloud Carbon Footprint, a project sponsored by ThoughtWorks. Etsy has open-sourced a similar tool called Cloud Jewels that estimates energy consumption based on cloud usage information. This is helping them track progress toward their target of reducing their energy intensity by 25% by 2025.

Beyond reducing environmental impact, CTOs and technology leaders can have significant, direct and meaningful social impact.

Include societal benefits in the design of your products: As a CTO or technology founder, you can help ensure that societal benefits are prioritized in your product roadmaps. For example, if you’re a fintech CTO, you can add product features to expand access to credit in underserved populations. Startups like LoanWell are on a mission to increase access to capital for those typically left out of the financial system and make the loan origination process more efficient and equitable.

When thinking about product design, a product needs to be as useful and effective as it is sustainable. By thinking about sustainability and societal impact as a core element of product innovation, there is an opportunity to differentiate yourself in socially beneficial ways. For example, Lush has been a pioneer of package-free solutions, and launched Lush Lens — a virtual package app leveraging cameras on mobile phones and AI to overlay product information. The company hit 2 million scans in its efforts to tackle the beauty industry’s excessive use of (plastic) packaging.

Responsible AI practices should be ingrained in the culture to avoid social harms: Machine learning and artificial intelligence have become central to the advanced, personalized digital experiences everyone is accustomed to — from product and content recommendations to spam filtering, trend forecasting and other “smart” behaviors.

It is therefore critical to incorporate responsible AI practices, so benefits from AI and ML can be realized by your entire user base and that inadvertent harm can be avoided. Start by establishing clear principles for working with AI responsibly, and translate those principles into processes and procedures. Think about AI responsibility reviews the same way you think about code reviews, automated testing and UX design. As a technical leader or founder, you get to establish what the process is.

Promoting governance does not stop with the board and CEO; CTOs play an important role, too.

Create a diverse and inclusive technology team: Compared to individual decision-makers, diverse teams make better decisions 87% of the time. Additionally, Gartner research found that in a diverse workforce, performance improves by 12% and intent to stay by 20%.

It is important to reinforce and demonstrate why diversity, equity and inclusion is important within a technology team. One way you can do this is by using data to inform your DEI efforts. You can establish a voluntary internal program to collect demographics, including gender, race and ethnicity, and this data will provide a baseline for identifying diversity gaps and measuring improvements. Consider going further by baking these improvements into your employee performance process, such as objectives and key results (OKRs). Make everyone accountable from the start, not just HR.

These are just a few of the ways CTOs and technology leaders can contribute to ESG progress in their companies. The first step, however, is to recognize the many ways you as a technology leader can make an impact from day one.

Powered by WPeMatico

PayPal’s plan to morph itself into a “super app” has been given a go for launch.

According to PayPal CEO Dan Schulman, speaking to investors during this week’s second-quarter earnings call, the initial version of PayPal’s new consumer digital wallet app is now “code complete” and the company is preparing to slowly ramp up. Over the next several months, PayPal expects to be fully ramped up in the U.S., with new payment services, financial services, commerce and shopping tools arriving every quarter.

The company has spoken for some time about its “super app” ambitions — a shift in product direction that would make PayPal a U.S.-based version of something like China’s WeChat or Alipay or India’s Paytm. Like those apps, PayPal aims to offer a host of consumer services under one roof, beyond just mobile payments.

In previous quarters, PayPal said these new features may include things like enhanced direct deposit, check cashing, budgeting tools, bill pay, crypto support, subscription management, and buy now, pay later functionality. It also said it would integrate commerce, thanks to the mobile shopping tools acquired by way of its $4 billion Honey acquisition in 2019.

So far, PayPal has continued to run Honey as a standalone application, website and browser extension, but the super app could incorporate more of its deal-finding functions, price-tracking features and other benefits.

On Wednesday’s earnings call, Schulman revealed the super app would have a few other features as well, including high-yield savings, early access to direct deposit funds and messaging functionality outside of peer-to-peer payments — meaning you could chat with family and friends directly through the app’s user interface.

PayPal hadn’t announced its plans to include a messaging component until now, but the feature makes sense in terms of how people often combine chat and peer-to-peer payments today. For example, someone may want to make a personal request for the funds instead of just sending an automated request through an app. Or, after receiving payment, a user may want to respond with a “thank you,” or other acknowledgment. Currently, these conversations take place outside of the payment app itself on platforms like iMessage. Now, that could change.

“We think that’s going to drive a lot of engagement on the platform,” said Schulman. “You don’t have to leave the platform to message back and forth.”

With the increased user engagement, the company expects to see a bump in average revenue per active account.

Schulman also hinted at “additional crypto capabilities,” which were not detailed. However, PayPal earlier this month increased the crypto purchase limit from $20,000 to $100,000 for eligible PayPal customers in the U.S., with no annual purchase limit. The company also this year made it possible for consumers to check out at millions of online businesses using their cryptocurrencies, by first converting the crypto to cash then settling with the merchant in U.S. dollars.

Though the app’s code is now complete, Schulman said the plan is to continue to iterate on the product experience, noting that the initial version will not be “the be-all and end-all.” Instead, the app will see steady releases and new functionality on a quarterly basis.

However, he did say that early on, the new features would include the high-yield savings, improved bill pay with a better user experience, and more billers and aggregators, as well as early access to direct deposit, budgeting tools and the new two-way messaging feature.

To integrate all the new features into the super app, PayPal will undergo a major overhaul of its user interface.

“Obviously, the [user experience] is being redesigned,” Schulman noted. “We’ve got rewards and shopping. We’ve got a whole giving hub around crowdsourcing, giving to charities. And then, obviously, buy now, pay later will be fully integrated into it. … The last time I counted, it was like 25 new capabilities that we’re going to put into the super app.”

The digital wallet app will also be personalized to the end user, so no two apps are the same. This will be done using both artificial intelligence and machine learning capabilities to “enhance each customer’s experiences and opportunities,” said Schulman.

PayPal delivered an earnings beat in the second quarter with $6.24 billion in revenue, versus the $6.27 billion Wall Street expected, and earnings per share of $1.15, versus the $1.12 expected. Total payment volume from merchant customers also jumped 40% to $311 billion, while analysts had projected $295.2 billion. But the company’s stock slipped due to a lowered outlook for Q3, impacted by eBay’s transition to its own managed payments service.

In addition, PayPal gained 11.4 million net new active accounts in the quarter, to reach 403 million total active accounts.

Powered by WPeMatico

Anomaly detection is one of the more difficult and underserved operational areas in the asset-servicing sector of financial institutions. Broadly speaking, a true anomaly is one that deviates from the norm of the expected or the familiar. Anomalies can be the result of incompetence, maliciousness, system errors, accidents or the product of shifts in the underlying structure of day-to-day processes.

For the financial services industry, detecting anomalies is critical, as they may be indicative of illegal activities such as fraud, identity theft, network intrusion, account takeover or money laundering, which may result in undesired outcomes for both the institution and the individual.

There are different ways to address the challenge of anomaly detection, including supervised and unsupervised learning.

Detecting outlier data, or anomalies according to historic data patterns and trends can enrich a financial institution’s operational team by increasing their understanding and preparedness.

Anomaly detection presents a unique challenge for a variety of reasons. First and foremost, the financial services industry has seen an increase in the volume and complexity of data in recent years. In addition, a large emphasis has been placed on the quality of data, turning it into a way to measure the health of an institution.

To make matters more complicated, anomaly detection requires the prediction of something that has not been seen before or prepared for. The increase in data and the fact that it is constantly changing exacerbates the challenge further.

There are different ways to address the challenge of anomaly detection, including supervised and unsupervised learning.

Powered by WPeMatico

Today, Tractable is worth $1 billion. Our AI is used by millions of people across the world to recover faster from road accidents, and it also helps recycle as many cars as Tesla puts on the road.

And yet six years ago, Tractable was just me and Raz (Razvan Ranca, CTO), two college grads coding in a basement. Here’s how we did it, and what we learned along the way.

In 2013, I was fortunate to get into artificial intelligence (more specifically, deep learning) six months before it blew up internationally. It started when I took a course on Coursera called “Machine learning with neural networks” by Geoffrey Hinton. It was like being love struck. Back then, to me AI was science fiction, like “The Terminator.”

Narrowly focusing on a branch of applied science that was undergoing a paradigm shift which hadn’t yet reached the business world changed everything.

But an article in the tech press said the academic field was amid a resurgence. As a result of 100x larger training data sets and 100x higher compute power becoming available by reprogramming GPUs (graphics cards), a huge leap in predictive performance had been attained in image classification a year earlier. This meant computers were starting to be able to understand what’s in an image — like humans do.

The next step was getting this technology into the real world. While at university — Imperial College London — teaming up with much more skilled people, we built a plant recognition app with deep learning. We walked our professor through Hyde Park, watching him take photos of flowers with the app and laughing from joy as the AI recognized the right plant species. This had previously been impossible.

I started spending every spare moment on image classification with deep learning. Still, no one was talking about it in the news — even Imperial’s computer vision lab wasn’t yet on it! I felt like I was in on a revolutionary secret.

Looking back, narrowly focusing on a branch of applied science undergoing a breakthrough paradigm shift that hadn’t yet reached the business world changed everything.

I’d previously been rejected from Entrepreneur First (EF), one of the world’s best incubators, for not knowing anything about tech. Having changed that, I applied again.

The last interview was a hackathon, where I met Raz. He was doing machine learning research at Cambridge, had topped EF’s technical test, and published papers on reconstructing shredded documents and on poker bots that could detect bluffs. His bare-bones webpage read: “I seek data-driven solutions to currently intractable problems.” Now that had a ring to it (and where we’d get the name for Tractable).

That hackathon, we coded all night. The morning after, he and I knew something special was happening between us. We moved in together and would spend years side by side, 24/7, from waking up to Pantera in the morning to coding marathons at night.

But we also wouldn’t have got where we are without Adrien (Cohen, president), who joined as our third co-founder right after our seed round. Adrien had previously co-founded Lazada, an online supermarket in South East Asia like Amazon and Alibaba, which sold to Alibaba for $1.5 billion. Adrien would teach us how to build a business, inspire trust and hire world-class talent.

Tractable started at EF with a head start — a paying customer. Our first use case was … plastic pipe welds.

It was as glamorous as it sounds. Pipes that carry water and natural gas to your home are made of plastic. They’re connected by welds (melt the two plastic ends, connect them, let them cool down and solidify again as one). Image classification AI could visually check people’s weld setups to ensure good quality. Most of all, it was real-world value for breakthrough AI.

And yet in the end, they — our only paying customer — stopped working with us, just as we were raising our first round of funding. That was rough. Luckily, the number of pipe weld inspections was too small a market to interest investors, so we explored other use cases — utilities, geology, dermatology and medical imaging.

Powered by WPeMatico

Reliance on a single technology as a lifeline is a futile battle now. When simple automation no longer does the trick, delivering end-to-end automation needs a combination of complementary technologies that can give a facelift to business processes: the digital operations toolbox.

According to a McKinsey survey, enterprises that have likely been successful with digital transformation efforts adopted sophisticated technologies such as artificial intelligence, Internet of Things or machine learning. Enterprises can achieve hyperautomation with the digital ops toolbox, the hub for your digital operations.

The hyperautomation market is burgeoning: Analysts predict that by 2025, it will reach around $860 billion.

The toolbox is a synchronous medley of intelligent business process management (iBPM), robotic process automation (RPA), process mining, low code, artificial intelligence (AI), machine learning (ML) and a rules engine. The technologies can be optimally combined to achieve the organization’s key performance indicator (KPI) through hyperautomation.

The hyperautomation market is burgeoning: Analysts predict that by 2025, it will reach around $860 billion. Let’s see why.

The toolbox, the treasure chest of technologies it is, helps with three crucial aspects: process automation, orchestration and intelligence.

Process automation: A hyperautomation mindset introduces the world of “automating anything that can be,” whether that’s a process or a task. If something can be handled by bots or other technologies, it should be.

Orchestration: Hyperautomation, per se, adds an orchestration layer to simple automation. Technologies like intelligent business process management orchestrate the entire process.

Intelligence: Machines can automate repetitive tasks, but they lack the decision-making capabilities of humans. And, to achieve a perfect harmony where machines are made to “think and act,” or attain cognitive skills, we need AI. Combining AI, ML and natural language processing algorithms with analytics propels simple automation to become more cognitive. Instead of just following if-then rules, the technologies help gather insights from the data. The decision-making capabilities enable bots to make decisions.

Here’s a story of evolving from simple automation to hyperautomation with an example: an order-to-cash process.

Powered by WPeMatico

Technology plays a huge role in nearly every aspect of financial services today. As the world moved online, tools and infrastructure to help people manage their money and make payments have burgeoned the world over in the past decade.

With much of the finance world now leveraging technology to conduct business, predict trends and deliver services, financial services regulators are also developing new technologies to monitor markets, supervise financial institutions and conduct other administrative activities. The emergence of purpose-built technologies to facilitate regulator oversight has, over the past few years, garnered its own moniker of supervisory technology, or suptech.

Interest in suptech is proliferating across the globe thanks to a diverse set of prudential and conduct regulators. A sampling of regulators developing suptech include the FDIC, CFPB, FINRA and Federal Reserve in the U.S.; the U.K.’s FCA and Bank of England; the National Bank of Rwanda in Africa; as well as the ASIC, HKMA and MAS in Asia. Several “super regulators” are also engaged in suptech efforts such as the Bank of International Settlements, the Financial Stability Board and the World Bank.

The strides in suptech demonstrate that creative thinking coupled with experimentation and scalable, easily accessible technologies are jump-starting a new approach to regulation.

In this post, we’ll examine a few core suptech use cases, consider its future and explore the challenges facing regulators as the market matures. The uses are diverse, so we’ll focus on three key areas: regulatory reporting, machine-readable regulation, and market and conduct oversight.

A quick general note: Nearly every financial services regulator is engaged in some type of suptech activity and the use cases discussed in this article are intended as a sample, not a comprehensive list.

As a preliminary matter, we should quickly survey a few definitions of suptech to frame our understanding. Both the World Bank and BIS have offered definitions that provide useful outlines for this discussion. The World Bank states that suptech “refers to the use of technology to facilitate and enhance supervisory processes from the perspective of supervisory authorities.” It’s a little circular, but helpful.

The BIS defines suptech as “the use of technology for regulatory, supervisory and oversight purposes.” This is a similarly loose definition that describes the broader scope better.

Regardless of differences on the margins, the “sup” in these suptech definitions acknowledges the primacy of the idea that regulators’ objectives are to oversee the conduct, structure, and health of the financial system. Suptech technologies facilitate related regulatory supervision and enforcement processes.

Regulatory reporting refers to a broad swath of activities such as financial firms providing trading data to regulatory authorities and regulators’ analysis of financial data or corporate information to determine the projected health or potential risks facing an institution or the market.

The MAS and FDIC are incorporating transactional and financial data reported by firms as a means to assess their financial viability. The MAS, in conjunction with BIS, has run tech sprints soliciting new ideas relating to regulatory reporting, while the FDIC has “a regulatory reporting solution that would allow ‘on-demand’ monitoring of banks as opposed to being constrained by ‘point-in-time’ reporting. This project is particularly targeted at smaller, community banks that provide only aggregated data on their financial health on a quarterly basis.”

The HKMA recently outlined its three-year plan for the development of suptech, which includes developing an approach to “network analysis.” The HKMA will analyze reporting data related to corporate shareholding and financial exposure to bring them “to life as network diagrams, so that the relationships between different entities become more apparent. Greater transparency of the connections and dependencies between banks and their customers will enable HKMA supervisors to detect early warning signals within the entire credit network.”

These reporting initiatives touch on a theme regulators have continuously struggled with: How to regulate markets and firms based on a reactive approach to historical data. Regulation and enforcement are often retrospective activities — examining past behavior and data to decide how to sanction an organization or develop a regulatory framework to govern a particular type of activity or financial product. This can result in an approach to regulation too rooted in past failures, which might lack the flexibility to anticipate or adapt to emerging risks or financial products.

Powered by WPeMatico