M&A

Auto Added by WPeMatico

Auto Added by WPeMatico

Black Friday may still be 10 days away, but shopping season started early in the enterprise this year. We have seen acquisitions totaling almost $50 billion in the last couple of months alone, topped by the mega $34 billion IBM-Red Hat deal two weeks ago. What exactly is going on here?

While not every deal has been for that kind of money, we are seeing an unusually large number of mega deals this year, something that some folks were predicting would happen when the big tech companies were allowed to repatriate their money as part of last year’s tax deal.

Let’s look at some of the multi-billion deals we have seen so far this year:

Big companies are opening their checkbooks in a big way right now, buying everything from marketing to analytics to security companies. They are grabbing open source and proprietary. They are looking at ways to bridge the cloud and on-prem. There is a whole host of software and not much rhyme or reason across the deals.

What they have in common is that they are enormous offers that are simply too huge to refuse. These companies flush with cash see opportunities to fill holes, and they are going for one piece after another.

One of the reasons the prices are going so high is that there is a limited number of companies available to buy, and that is driving up the price, says Ray Wang, founder and principal analyst at Constellation Research. As he sees it, there are only 3-5 decent players per category right now. He compares that with 10 years ago when we were seeing 10-15 players per category. With a limited number of viable startups, companies seem to be going after these companies harder. Combine that with fat wallets full of cash, and you suddenly have this wave of super-sized deals.

The companies being acquired by large organizations can justify selling in the usual ways. They can reward shareholders and investors. These larger organizations allow them to push their product roadmaps much more quickly than they could on their own. They give them access to international markets and mega sales teams.

Still, companies have been spending unusually large sums for relatively small amounts of revenue. In deals over the last three weeks, we have seen IBM pay $34 billion for a company with around $3 billion in revenue. We saw SAP paying $8 billion for a mere $400 million in revenue.

This certainly seems on its face to be a massive overpay, but Constellation’s Wang says ultimately this often comes down to a classic build versus buy decision. SAP could build a similar product to Qualtrics, or they could simply buy it and put the massive SAP salesforce to bear on it. “SAP can sell into 100,000 customers. They only have a 10 percent overlap with Qualtrics. The numbers work, and it beats taking a new product to market,” Wang told TechCrunch.

Wang believes this could be the strategy behind many of these acquisitions, while admitting that the numbers sound a bit crazy. As he says, the formula used to be three times, three years trailing revenues. Now it’s 15-20 times. While those may be hard numbers to justify, he believes it’s a win-win for buyer and acquired — and investors win big too, of course.

In many instances like Red Hat, GitHub and Qualtrics, the companies will likely remain separate, independent units inside the larger organization, at least for the time being, while looking for meaningful crossover inside the larger company when it makes sense.

But Tony Byrne, founder and principal analyst at Real Story Group, says these large companies tend to listen to Wall Street, and customers should be wary of what they hear when it comes to their favorite products and services. “You cannot trust the initial pleasantries about continuity that come out of the first press release. These are huge vendors that listen first and foremost to Wall Street. If there’s an offering that doesn’t totally align with their story to investors, it is not going to get much love and is at risk for getting eliminated or calved off,” Byrne explained.

It’s also hard to know how well two companies are going to fit together until the deal actually closes. Sometimes the acquiring company doesn’t know what they have or how to sell it. Sometimes the two companies don’t fit well together or the founders or key executives don’t fit smoothly into the new hierarchy. They try to figure this all out beforehand, but it’s not always easy to know how it will play out in reality.

Regardless, we are seeing an unusually high level of massive acquisitions, and chances are, there are more coming.

Powered by WPeMatico

Some consolidation and subsequent divestment are in play in the worlds of imaging and voice recognition. Today, Kofax and Nuance announced that Kofax would be acquiring Nuance’s imaging division, for $400 million in cash. The deal, which had been rumoured in recent days, is expected to close in Q1 2019.

The acquisition is a notable move for Kofax — itself acquired by Thoma Bravo last year in a $1.5 billion deal — as it continues to build up its business in Robotic Process Automation (RPA), the area of enterprise IT services that uses machine learning, computer vision and other AI-based tools to bring automation to repetitive or mundane back-office tasks that would have in the past been done by humans. (The idea is that this frees up the humans to make more sophisticated assessments in specific cases, or focus on entirely different tasks.)

On the side of Nuance, the company is a leader in voice recognition services that served as an early partner to the likes of Apple with Siri, and has also worked on a number of other AI-based solutions to improve how enterprises build services and work.

Publicly traded Nuance’s imaging division accounted for about 11 percent of its revenues last year, and it has stated would be making several changes in its business to rationalise it and focus on more profitable operations. The biggest parts of its $5 billion business today are healthcare solutions, enterprise and automotive.

Kofax is bringing on Nuance Document Imaging, as the division is officially called, specifically to bring more services in the area of imaging services, which include services like providing security and compliance around any image scanning or printing that takes place across an organization. NDI, Kofax said, is one of the biggest companies of its kind in the field, covering 6 million knowledge workers and over 100,000 active deployments of its Print Management solutions.

“Through the acquisition of Nuance’s document imaging division, Kofax will drive customer value by adding key technologies, including cloud compatibility, scan-to-archive, scan-to-workflow, print management and document security, to our end-to-end Intelligent Automation platform,” said Reynolds C. Bish, Chief Executive Officer of Kofax. “In addition we will now be able to combine the best capture and print management capabilities available in the market into one product portfolio.”

Kofax said this makes it the leader in this area globally: and indeed it is racing to keep ahead of competition.

RPA has been one of the fastest-growing areas in IT, fueled by the rising interest in bringing more AI into enterprise services. UiPath, one of the leading startups in the space, has raised close to $400 million in two separate rounds this year on the back of its rapid growth. Just last week, UiPath just last week expanded its own imaging capabilities.

Powered by WPeMatico

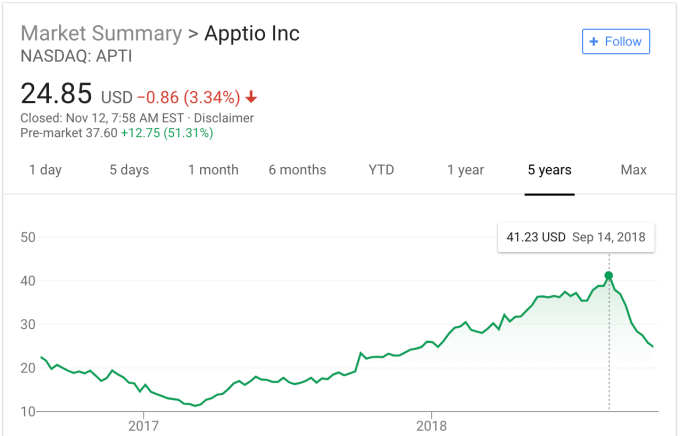

It seems that Sunday has become a popular day to announce large deals involving enterprise companies. IBM announced the $34 billion Red Hat deal two weeks ago. SAP announced its intent to buy Qualtrics for $8 billion last night, and Vista Equity Partners got into the act too, announcing a deal to buy Apptio for $1.94 billion, representing a 53 percent premium for stockholders.

Vista paid $38 per share for Apptio, a Seattle company that helps companies manage and understand their cloud spending inside a hybrid IT environment that has assets on-prem and in the cloud. The company was founded in 2007 right as the cloud was beginning to take off, and grew as the cloud did. It recognized that companies would have trouble understanding their cloud assets alongside on-prem ones. It turned out to be a company in the right place at the right time with the right idea.

Investors like Andreessen Horowitz, Greylock and Madrona certainly liked the concept, showering the company with $261 million before it went public in 2016. The stock price has been up and down since, peaking in August at $41.23 a share before dropping down to $24.85 on Friday. The $38 a share Vista paid comes close to the high-water mark for the stock.

Stock Chart: Google

Sunny Gupta, co-founder and CEO at Apptio, liked the idea of giving his shareholders a good return while providing a good landing spot to take his company private. Vista has a reputation for continuing to invest in the companies it acquires and that prospect clearly excited him. “Vista’s investment and deep expertise in growing world-class SaaS businesses and the flexibility we will have as a private company will help us accelerate our growth…,” Gupta said in a statement.

The deal was approved by Apptio’s board of directors, which will recommend shareholders accept it. With such a high premium, it’s hard to imagine them turning it down. If it passes all of the regulatory hurdles, the acquisition is expected to close in Q1 2019.

It’s worth noting that the company has a 30-day “go shop” provision, which would allow it to look for a better price. Given how hot the enterprise market is right now and how popular hybrid cloud tools are, it is possible it could find another buyer, but it could be hard to find one willing to pay such a high premium.

Vista clearly likes to buy enterprise tech companies, having snagged Ping Identity for $600 million and Marketo for $1.8 billion in 2016. It grabbed Jamf, an Apple enterprise device management company and Datto, a disaster recovery company last year. It turned Marketo around for $4.75 billion in a deal with Adobe just two months ago.

Powered by WPeMatico

The second wave of Internet-era travel companies has captured the attention of venture capitalists.

In the last five years, travel companies have raised more than $1 billion in venture capital funding. That includes short-term rental startups, travel and tourism apps, marketplaces for “experiences” and other travel or hospitality tech platforms. Airbnb, a $38 billion company and an anomaly in the category, has raised $3 billion in that same time frame, according to PitchBook.

In the last few months alone, aspiring Concur-competitor TripActions and travel activities platform Klook entered the “unicorn” club with large venture rounds that valued both of the businesses at more than $1 billion. Meanwhile, luggage maker Away raised $50 million at a $400 million valuation and smaller startups in the space like Freebirds, IfOnly, KKDay, Duffel and RedDoorz all closed modest funding rounds.

“Something is really happening in the industry; something bigger than us,” TripActions co-founder Ariel Cohen said in a recent conversation with TechCrunch about his company’s $154 million Series C financing. “Different startups are identifying the opportunity here and the fact that companies want to make sure their employees are happy while they are on the go. That’s why you see investments in companies like Brex and like TripActions.”

Brex, though not classified as a travel startup, lets startup employees earn extra points on business travel with its corporate credit card for startups. It recently raised a $125 million Series C at a $1.1 billion valuation.

Global travel and tourism is one of the most valuable industries worth some $7 trillion. The online travel market, in particular, is expected to grow to $817 billion by 2020. VCs are hunting for tech-enabled startups poised to dominate that slice.

“You have a new wave of businesses where all of that digital infrastructure is set up, so the focus can be on things like efficiency, improved customer service, scale and growth — you have a ton of companies popping up catering to those needs,” Defy Partners co-founder Neil Sequeira told TechCrunch. Sequeira was a managing director at General Catalyst when the firm made its first investment in Airbnb.

On the other hand, you have a whole cohort of travel business founded amid the dot-com boom that are looking to technology startups for a much-needed infusion of innovation. Many of those larger companies have become active acquirers, fueling VC interest in the space. SAP Concur, for example, acquired the formerly VC-backed travel-booking startup Hipmunk in 2016. Before that, it bought travel planning company TripIt for $120 million, among others.

Expedia has gobbled up a number of travel brands too, like travel photography community Trover; Airbnb-competitor HomeAway, which it paid a whopping $3.9 billion for in 2015; and most recently, both Pillow and ApartmentJet.

Many of these acquisitions are for peanuts, which is far from ideal for a venture-funded company. And building a travel business is cash intensive, hence the $4.4 billion Airbnb has raised to date or even TripActions’ $236 million in total VC funding. To keep momentum in the space, companies need to be striking larger M&A deals.

It doesn’t help that many in and around the venture capital industry are predicting an imminent turn in the market. Travel companies, which are reliant upon a consumer’s tendency to spend excess cash, will be among the first sectors to be impacted by hostile economic conditions.

“If the market turns, people aren’t going to spend $10,000 on a trip to Zimbabwe,” Sequeira said, referencing companies like IfOnly, which sells curated experiences.

Travel startups should raise now while the market is hot. The conditions may not remain favorable for long.

Powered by WPeMatico

Microsoft is continuing to invest in a broad spectrum of developers for its Xbox gaming ecosystem with the acquisition of Obsidian and InXile, makers of complex RPGs primarily aimed at PC users. The two studios will join four others snatched up in June, significantly bolstering Xbox’s first-party development resources.

The company announced the acquisitions (rumored for some time) at its XO18 event alongside numerous other interesting developments for the Xbox One and Windows gaming platforms. Xbox Director of Programming Larry Hyrb, better known by his pseudonym Major Nelson, welcomed them to the Microsoft Studios team of owned but independent devs:

So happy to welcome @Inxile_Ent and @Obsidian to the Xbox family. Look forward to working with you and your teams on future projects! pic.twitter.com/j5YormTwU6

— Larry Hryb @ X018 (@majornelson) November 10, 2018

Of the two studios Obsidian is probably the best known; Fallout: New Vegas is a modern classic of the open world genre, while Pillars of Eternity and its enormous sequel are a welcome revival of the classic isometric PC RPG. InXile is a bit more niche, though also successful: the Wasteland, Torment, and Bard’s Tale games are similarly appreciated by RPG lovers. The studios will, like the others in Microsoft’s stable, be given significant operational independence, not folded into some internal unit.

Microsoft announced the acquisition of Compulsion, Undead Labs, Ninja Theory, and Playground Games in June. But what’s clear from the more recent gets, that the earlier ones didn’t necessarily indicate, is a big focus on core PC gamers. Microsoft has had a rather mixed mission in that it wants to ensure the success of its Xbox One (and future) consoles, but also wants to bring the huge population of PC gamers into the fold somehow. It would help offset the significant but yet necessarily decisive lead Sony has in the ongoing console wars.

Numerous efforts over the years have failed to impress them and some are in fact still ridiculed. But the collection of some seriously PC-first developers commanding a hardcore audience may help bring some PC gaming wisdom to the Xbox world.

Although console exclusives are not as appreciated as they once were — gamers value cross-platform play far more — it doesn’t help to have a couple to sway undecided buyers or even tempt consumers to buy both. These acquisitions suggest an investment in Microsoft’s first-party development platform that could help close the gap, or prepare a real blitz for the next generation of consoles.

The studios issued videos talking about their take on the development, which you can watch below:

And now, a very special announcement from us here at Obsidian on becoming a part of the Microsoft family!https://t.co/bq5GGrM2UC

— Obsidian (@Obsidian) November 10, 2018

Some big news for #inXile Entertainment today! Here to talk about it is inXile CEO @BrianFargo. We’re excited about the future and our ability to continue to bring you great role playing games! https://t.co/C4FTh5whQ5

— InXile Entertainment (@Inxile_Ent) November 10, 2018

Powered by WPeMatico

As you look at the $34 billion IBM-Red Hat deal announced yesterday, if you follow the enterprise closely, it seems like a good move, at least on its face. It could be years before we understand the true value of it for IBM (or lack thereof, depending on how it ultimately goes). The questions stands then, is this a savvy move, a desperate one or perhaps a bit of both. It turns out, it depends on whom you ask.

For starters, there is the sheer amount of money involved, a 63 percent premium on Friday’s closing price of just under $117 a share. IBM spent $190 a share, but as Ray Wang, founder and chief analyst at Constellation Research said, Red Hat didn’t necessarily want to be sold, so IBM had to overpay to get their company.

Wang sees cloud, Linux and security as the big drivers on IBM’s part. “IBM is doubling down on the cloud, but they also are going for a grab in Linux for their largest and most important open source communities and some of the newer tech on Red Hat security,” he told TechCrunch. He acknowledges that it’s a huge premium for the stock, but he believes IBM needs the M&A action to drive down customer acquisition costs and drive up cross sell.

Photo: Ron Miller

IBM is placing a big bet here says Dharmesh Thakker, general partner at Battery Ventures, believing it to be worth 30x its current earnings in the next 12 months. “Needless to say, the hybrid cloud opportunity that we have been working on the last few years, is real and IBM/Cisco/HP/Dell all want a piece of this action going forward as the $300B in datacenter spend gets dislocated by public and hybrid cloud vendors,” Thakker explained in a statement.

He believes this deal could actually trigger a new set of mega mergers between the traditional tech vendors and cloud native, container and DevOps companies over the next few months.

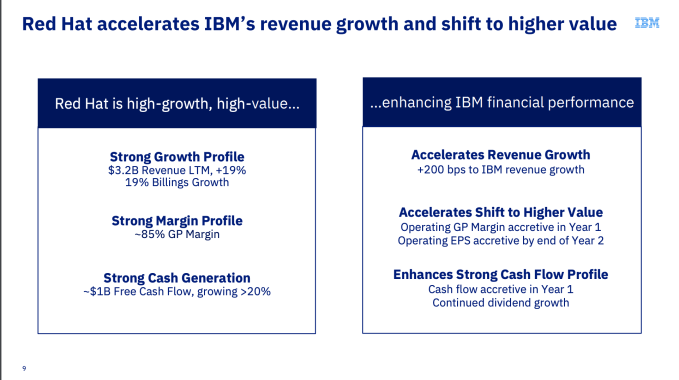

IBM CEO Ginni Rometty was positively giddy at the prospects of a combined IBM-Red Hat in a call with analysts and press this morning, pointing out that only 20 percent of enterprise workloads have been moved to the cloud. She sees a big opportunity, one she projects to be worth $1 trillion by 2020. Keeping in mind you should take market projections with a grain of salt, this is undoubtedly a big market and one that Oracle and Microsoft have also targeted.

She said that Red Hat was a rare company indeed. “Red Hat on its own has been a high value company and has done a great job with strong growth, is highly profitable and generates cash. There are not many companies out there that look like that in this area,” Rometty said.

Slide: IBM

Dan Scholnick, general partner at Trinity Ventures, whose investments have included New Relic and Docker, was not terribly impressed with the deal, believing it smacked of desperation on IBM’s part.

“IBM is a declining business that somehow needs to become relevant in the cloud era. Red Hat is not the answer. Red Hat’s business centers around an operating system, which is a layer of the technology stack that has been completely commoditized by cloud. (If you use AWS, you can get Amazon’s OS for free, so why would you pay Red Hat?) Red Hat has NO story for cloud,” he claimed in a statement.

That might not be an entirely fair assessment. While Red Hat Enterprise Linux is a big part of the company’s revenue, it’s not the only piece. Over the last couple of years it has moved into Kubernetes and containerization and has grown the cloud native side of the business alongside RHEL.

In fact, Forrester analyst Dave Bartoletti sees the cloud native piece as being key here. “The combined company has a leading Kubernetes and container-based cloud-native development platform, and a much broader open source middleware and developer tools portfolio than either company separately. While any acquisition of this size will take time to play out, the combined company will be sure to reshape the open source and cloud platforms market for years to come,” he said.

Photo: IBM

Wang believes the deal could hinge on how long Red Hat CEO Jim Whitehurst, who had led the company for over a decade, stays with the unit. According to IBM, they will maintain the Red Hat brand and operate it as an independent entity inside Big Blue. “If Whitehurst doesn’t stick around for awhile, the deal could go south,” he said. But the company could dangle the CEO job when Rometty decides to leave as incentive to stay.

Regardless, Wall Street was not entirely happy with IBM’s move with their stock down all day. Needless to say the 63 percent premium IBM paid for the stock has driven Red Hat higher today.

The deal must pass shareholder muster, but given the premium IBM has offered, it’s hard to believe they would turn it down. In addition, since these companies operate across the world, they are subject to the global regulatory approval process. They won’t officially come together until at least the second half of next year at the soonest. That’s when we might begin to learn whether this was a brilliant or desperate move by IBM.

Powered by WPeMatico

After announcing earlier this year that it planned to shut down HipChat and Stride and sell the IP of both to Slack, today enterprise software company Atlassian made another move related to its retreat from enterprise chat. It is selling Jitsi, a popular open-source chat and videoconferencing tool, to 8X8, a provider of cloud-based business phone and internal communications services. 8X8 says it plans to integrate Jitsi with its current conferencing solutions, specifically a product called 8X8 Meetings, and to keep it open source.

Terms of this latest sale to 8×8 have not been disclosed. Both the tech and the engineering team working on Jitsi, led by Emil Ivov, are coming with the acquisition.

Atlassian originally acquired Jitsi and its owner BlueJimp for an undisclosed sum in 2015 with the intention of adding video communications to HipChat, and later Stride (which launched in 2017).

But now those two products are headed for the graveyard — they are both being discontinued on February 15, 2019 — and that made Jitsi less core to Atlassian’s new direction, where it is focusing less on enterprise chat, and more on tools for developers and customer care, including Jira, Trello, and Bitbucket (a competitor to GitHub).

The deal is one of the final moves for Atlassian as it focuses more on its business building and operating productivity tools that are not direct competitors in the crowded field of enterprise chat applications. It seems that in any case, Jitsi is hoping for more investment under its new owner.

“This is a great thing and will only help to keep Jitsi’s momentum with renewed investment,” writes Ivov in a blog post announcing the news. “The Jitsi team will remain 100 percent intact and will continue to be an independent group. Operationally things will work much the same way as they did under Atlassian. Jitsi users and developers won’t see any impact, though we do expect with continued funding and support you will see even more new features and capabilities from the project!”

Technology in the acquisition includes Jitsi’s modular open-source projects for businesses to build and deploy secure video communication solutions based around WebRTC; the Jitsi Videobridge conferencing server; and the Jitsi Meet conferencing and collaboration application.

“The best video communications solutions are so intuitive and reliable that they help employees conduct shorter, more productive meetings. 8×8 has already developed a world-class meetings solution for enterprises, and we’re focused on maintaining leadership in delivering reliable, crystal-clear video and audio conferencing quality across mobile and desktop applications,” said Dejan Deklich, Chief Product Officer at 8×8, in a statement. “Incorporating Jitsi’s open-source technology into our video communications technology platform, and having Jitsi’s talented engineering team play a role in leading our development of dedicated conferencing applications and WebRTC, will open new paths for our customers and further enhance our meetings solution.”

Jitsi’s tools are used by a variety of platforms and businesses that want to include videoconferencing but would rather use an independent third-party service rather than incorporate one from a would-be competitor or build it themselves. Customers include Comcast and Symphony, the chat app used by the financial services industry.

“Some of the most innovative WebRTC products and companies use Jitsi to support millions of minutes of daily usage as part of their meetings, messaging and collaboration product ecosystems. The open source community has played a critical role in advancing Jitsi’s projects by validating its use in a diverse set of environments and complementing the core team’s development. As part of this acquisition, 8×8 is committed to continuing to support the growing developer community, and we are excited to engage even more,” commented Bryan Martin, Chairman and Chief Technology Officer at 8×8.

This past weekend’s big news of IBM acquiring Red Hat for $34 million has emphasised just how central open source and cloud-based software are in today’s enterprise IT market. This purchase is far smaller, but is also part of that bigger trend.

“8×8 sees tremendous value in the open source community and is committed to helping grow the community even larger,” Ivov notes. “With a major, high-motivated backer like 8×8 behind the project, we are confident about our ability to continue building great open source products.”

Powered by WPeMatico

Who expects a $34 billion deal involving two enterprise powerhouses to drop on a Sunday afternoon, but IBM and Red Hat surprised us yesterday when they pulled the trigger on a historically large deal.

IBM has been a poster child for a company moving through a painful transformation. As Box CEO (and IBM business partner) Aaron Levie put it on Twitter, sometimes a company has to make a bold move to push that kind of initiative forward:

Brilliant move by IBM. Transformation requires big bets, and this is a good one.

— Aaron Levie (@levie) October 28, 2018

They believe they can take their complex mix of infrastructure/software/platform services and emerging technologies like artificial intelligence, blockchain and analytics, and blend all of that with Red Hat’s profitable fusion of enterprise open source tools, cloud native, hybrid cloud and a keen understanding of the enterprise.

As Jon Shieber pointed out yesterday, it was a tacit acknowledgement that company was not going to get the results it was hoping for with emerging technologies like Watson artificial intelligence. It needed something that translated more directly into sales.

Red Hat can be that enterprise sales engine. It already is a company on a $3 billion revenue run rate, and it has a goal of hitting $5 billion. While that’s somewhat small potatoes for a company like IBM that generates $19 billion a quarter, it represents a crucial addition.

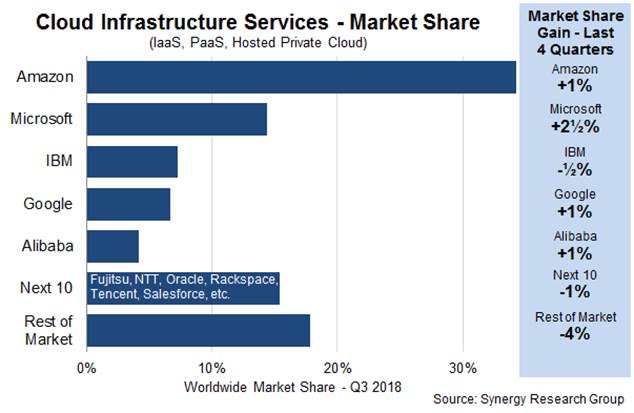

That’s because in spite of its iffy earnings reports over the last five years, Synergy Research reported that IBM had 7 percent of the cloud infrastructure market in its most recent report, which it defines as Infrastructure as a Service, Platform as a Service and hosted private cloud. It is the latter that IBM is particularly good at.

The company has the pieces in place now and a decent amount of marketshare, but Red Hat gives it a much more solid hybrid cloud story to tell. They can potentially bridge that hosted private cloud business with their own public cloud (and presumably even those of their competitors) and use Red Hat as a cloud native and open source springboard, giving their sales teams a solid story to tell.

IBM already has a lot of enterprise credibility on its own, of course. It sells on top of many of the same open source tools as Red Hat, but it hasn’t been getting the sales and revenue momentum that Red Hat has enjoyed. If you combine the enormous IBM sales engine and their services business with that of Red Hat, you have the potential to crank this into a huge business.

Photo: Ron Mller

It’s worth noting that the deal needs to pass shareholder muster and clear global regulatory hurdles before they can combine the two organizations. IBM has predicted that it will take at least until the second half of next year to close this deal and it could take even longer.

IBM has to use that time wisely and well to make sure when they pull the trigger, these two companies blend as smoothly as possible across technology and culture. It’s never easy to make these mega deals work with so much money and pressure involved, but it is imperative that Big Blue not screw this up. This could very well represent its last best chance to right the ship once and for all.

Powered by WPeMatico

To keep up with the rising demand for short-term rentals in U.S. cities and compete with the home-sharing giant Airbnb, travel booking site Expedia has picked up a pair of venture-backed hospitality startups, Pillow and ApartmentJet.

Employees of both companies will join Expedia . The company declined to disclose the financial terms of the deals.

“Acquiring Pillow and ApartmentJet will help unlock urban growth opportunities that, over time, will contribute to HomeAway’s ability to add an even broader selection of accommodations to its marketplace and marketplaces across Expedia Group brands, ensuring travelers always find the perfect place to stay,” the company explained in a statement.

Expedia paid $3.9 billion for HomeAway and its portfolio of travel brands in 2015. The deal was its first major move in the alternative accommodations space, as well as the beginning of a series of efforts to outdo VC darling Airbnb. Its latest targets provide software tools for property managers to easily manage short-term rentals on Airbnb competitors like HomeAway and VRBO.

Located in San Francisco, Pillow helps residents list their apartments as short-term rentals without violating their leases. It’s raised a total of $16.5 million in VC backing since 2013, including a $13.5 million round last year led by Mayfield, with participation from Sterling.VC, Peak Capital Partners, Expansion VC, Chris Anderson, Gary Vaynerchuk, Dennis Phelps and Veritas Investments.

ApartmentJet helps property owners earn money off vacancies. Founded in 2016, the Chicago-headquartered startup had raised a reported $1.2 million in capital from Network Ventures and BlueTree.

Bellevue-based Expedia Group owns several travel brands, including HomeAway, VRBO, Travelocity, trivago, Orbitz and Hotels.com. The company is both an active investor in and acquirer of startups.

Expedia’s shares rose 9.4 percent Thursday after its third-quarter earnings beat analyst expectations. The company posted $3.28 billion in revenue, a notable increase from last year’s $2.97 billion.

Powered by WPeMatico

Teamable, a provider of hiring software that leverages employees’ social networks, has brought in $5 million from new investor Foundation Capital and existing backers True Ventures and SaaStr Fund.

The startup also announced its acquisition of Simppler‘s referral recommendation engine and matchmaking recruiting software. Teamable’s co-founder and chief executive officer Laura Bilazarian declined to disclose the terms of the deal but said none of the $5 million investment was used to finance the transaction.

According to Crunchbase, Simppler had raised $3.2 million in equity funding from Foundation Capital, Greylock, Vertex Ventures and others. The company, which is akin to Teamable, creates a referral platform using existing employee networks; it was founded by Vipul Sharma in 2013. Sharma previously ran machine learning at Eventbrite and, according to his LinkedIn profile, he’s been an engineering director at Indeed for the past year.

Sharma and the Simppler team will not be joining Teamable .

Using Gmail, Facebook, GitHub and other social media platforms, Teamable aggregates its employees’ contacts to connect recruiters with a more focused set of potential candidates. Companies using Teamable, including Spotify and Lyft, then facilitate a warm introduction between a candidate and the employee in their network. The startup says its social recruiting algorithms lead to more efficient and diverse hiring practices.

“I don’t think candidates love the way recruiting is done,” Bilazarian told TechCrunch. “They are throwing applications over a wall and not hearing back. And I don’t think companies love the way recruiting is done because people are just making guesses based off a job description and they aren’t getting the right applicants.”

“Instead of few people at a company spamming the entire world, you have people who really understand the company reaching out to you,” she added. “Teamable is very precise. It’s reach out to five people to get a hire versus reach out to 200 just to get one response.”

The Foundation-led investment brings Teamable’s total equity funding to date to $10 million, including last year’s $5 million Series A. Bilazarian says the 50-person company is cash flow positive with 200 customers. With offices in San Francisco and Yerevan, Armenia, Teamable will use the capital to expand its team and recruiting platform.

Powered by WPeMatico