Lyft

Auto Added by WPeMatico

Auto Added by WPeMatico

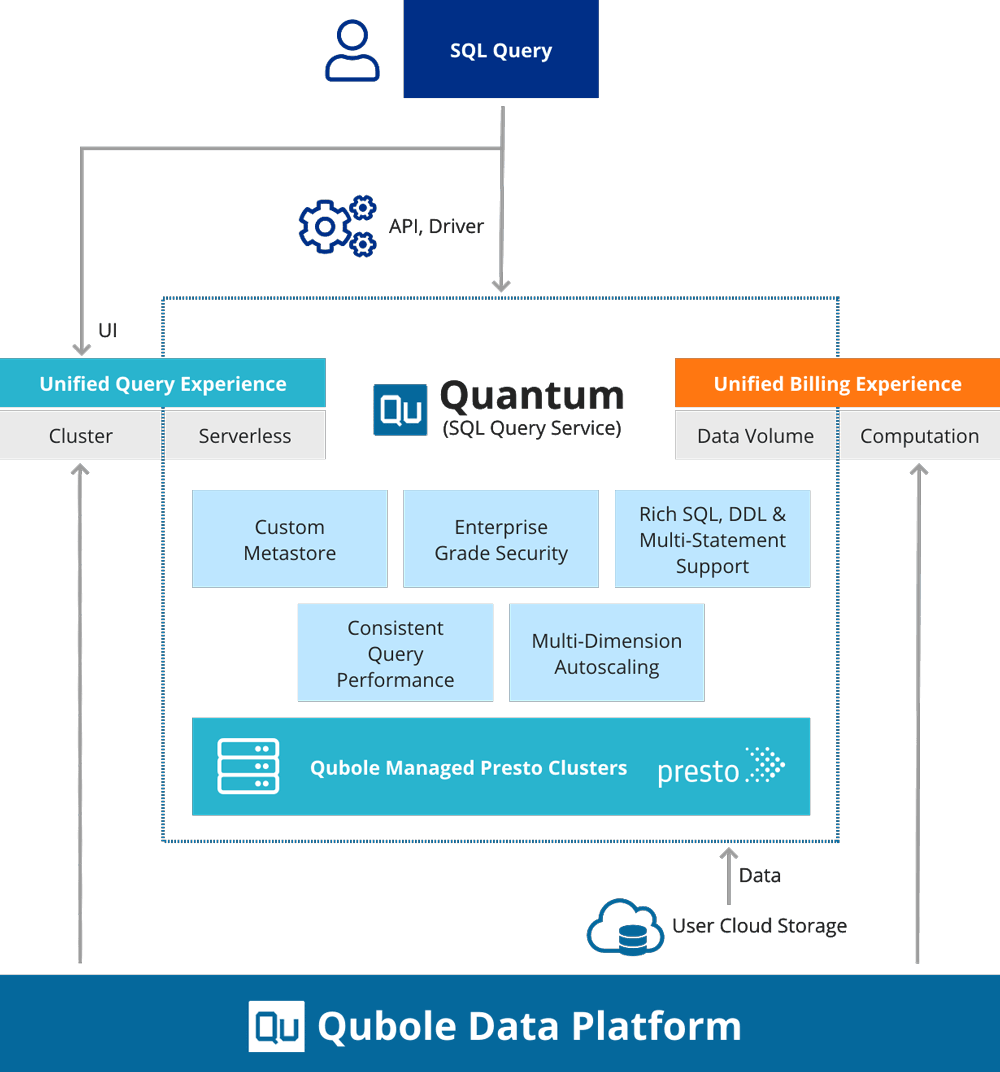

Qubole, the data platform founded by Apache Hive creator and former head of Facebook’s Data Infrastructure team Ashish Thusoo, today announced the launch of Quantum, its first serverless offering.

Qubole may not necessarily be a household name, but its customers include the likes of Autodesk, Comcast, Lyft, Nextdoor and Zillow . For these users, Qubole has long offered a self-service platform that allowed their data scientists and engineers to build their AI, machine learning and analytics workflows on the public cloud of their choice. The platform sits on top of open-source technologies like Apache Spark, Presto and Kafka, for example.

Typically, enterprises have to provision a considerable amount of resources to give these platforms the resources they need. These resources often go unused and the infrastructure can quickly become complex.

Qubole already abstracts most of this away, offering what is essentially a serverless platform. With Quantum, however, it is going a step further by launching a high-performance serverless SQL engine that allows users to query petabytes of data with nothing else but ANSI-SQL, giving them the choice between using a Presto cluster or a serverless SQL engine to run their queries, for example.

The data can be stored on AWS and users won’t have to set up a second data lake or move their data to another platform to use the SQL engine. Quantum automatically scales up or down as needed, of course, and users can still work with the same metastore for their data, no matter whether they choose the clustered or serverless option. Indeed, Quantum is essentially just another SQL engine without Qubole’s overall suite of engines.

Typically, Qubole charges enterprises by compute minutes. When using Quantum, the company uses the same metric, but enterprises pay for the execution time of the query. “So instead of the Qubole compute units being associated with the number of minutes the cluster was up and running, it is associated with the Qubole compute units consumed by that particular query or that particular workload, which is even more fine-grained,” Thusoo explained. “This works really well when you have to do interactive workloads.”

Thusoo notes that Quantum is targeted at analysts who often need to perform interactive queries on data stored in object stores. Qubole integrates with services like Tableau and Looker (which Google is now in the process of acquiring). “They suddenly get access to very elastic compute capacity, but they are able to come through a very familiar user interface,” Thusoo noted.

Powered by WPeMatico

If you are among those who thought that the scooter market sounded a little overhyped and overcrowded, we’ve gotten wind of a deal that could point to some impending consolidation. The on-demand scooter business Bird has agreed to acquire Scoot, a smaller two-wheeled mobility startup, sources tell TechCrunch.

The stage of the negotiations is not clear although from what our sources tell us, it sounds like the deal is not closed. Contacted for a response, both Scoot and Bird said they declined to comment on speculation.

If accurate, it would be far from a merger of equals. Scoot was last valued at around $71 million, having raised about $47 million in equity funding to date from Scout Ventures, Vision Ridge Partners, angel investor Joanne Wilson and more.

Bird is significantly larger. Led by chief executive officer Travis VanderZanden, earlier this year the company was working on a round of financing reportedly worth $300 million at a $2.3 billion valuation. We’ve been able to confirm that this round has now closed, although we don’t yet know the final amount or who the investors are. (Backers of Bird include Sequoia, Index, Charles River Ventures, Tusk Ventures, Upfront Ventures and dozens more.) Scoot would be Bird’s first full acquisition.

It’s still very early days in the scooter market in terms of consumer adoption, but that hasn’t stopped people from launching a lot of startups and raising funding to capitalise on what many believe will be a big opportunity longer term.

That promise is made bigger by the regulatory structure of the scooter market. Similar to their approach to bikes, many cities restrict the number of licenses they give out to companies to run on-street, hourly scooter services. Winning a license can give a company a near-monopoly on building a business in that city.

It also means that a combination between two companies whose geographic footprints do not overlap becomes a much cheaper and faster way of instantly creating a bigger business.

Notably, Scoot has a license to operate a pick-up/drop-off street service in the key market of San Francisco — where it competes with Skip, the only other licensed operator in the city. (Note: Bird last month did start up business again in SF, but only for the less popular offer of monthly rentals.)

What’s more, the two startups do not have any overlap in the rest of their footprints. Scoot is active in Barcelona, Spain and Santiago, Chile. Bird, on the other hand, has launched in about 100 cities spanning the U.S. and Europe, but its list does not include any of the cities where Scoot has rolled out its service.

Bird announced its new, two-seated electric vehicle earlier this week

On the vehicle front, the story is a little different. The two are providing, more or less, the same kinds of vehicles. Scoot has built out a network focused primarily on electric push scooters, seated scooters and electric bikes. Bird, meanwhile, has mostly built its service around electric push scooters, but just yesterday the company debuted its first seated vehicle to expand into a new product class.

Bird acquiring Scoot will help the two achieve better economies of scale in terms of vehicle purchasing power and device R&D.

It also helps them compete against the big boys. The market for scooters and other two-wheeled vehicles (collectively termed “micro-mobility”) is still a relatively new one, but Lyft and Uber have also waded in early to establish market share, as part of their own strategies to position themselves as the go-to platforms for any and all transportation needs.

Bird buying Scoot is one likely M&A move, but it’s not the only one.

Sources have told TechCrunch that an Uber acquisition of Skip (the other provider in SF) could also be in the works. Skip, much like Scoot, is another small player in the e-scooter market. To date, it has secured $31 million in venture capital funding from Initialized Capital, Accel and others.

Uber is already an active acquirer in the area of mico-mobility. If you remember, it acquired JUMP Bikes for $200 million in April 2018.

Uber’s acquisition of JUMP wasn’t surprising. In January 2018, the ride-hailing giant partnered with JUMP to launch Uber Bike, which lets Uber riders book JUMP bikes via the Uber app.

Other acquisitions in the nascent micro-mobility space include Lyft’s purchase of Motivate, a deal announced roughly one year ago. Motivate, the oldest and largest electric bike-share company in North America, did not disclose terms of the deal, though reports indicated it was asking for at least $250 million.

Bird — founded in 2017 — has yet to announce any acquisitions, although a spokesperson for the company said there have been quiet acqui-hires before now.

It was itself the subject of acquisition rumors for several months in 2018, too. Prior to Uber filing to go public in what was one of the most highly anticipated initial public offerings of the decade, many expected it to shell out cash for either Bird or Lime. From what we know, Uber was in discussions to acquire Bird, but ultimately it wasn’t able to meet Bird’s steep asking price.

Powered by WPeMatico

Services meshes. They are the hot new thing in the cloud native computing world. At KubeCon, the bi-annual festival of all things cloud native, Microsoft today announced that it is teaming up with a number of companies in this space to create a generic service mesh interface. This will make it easier for developers to adopt the concept without locking them into a specific technology.

In a world where the number of network endpoints continues to increase as developers launch new micro-services, containers and other systems at a rapid clip, they are making the network smarter again by handling encryption, traffic management and other functions so that the actual applications don’t have to worry about that. With a number of competing service mesh technologies, though, including the likes of Istio and Linkerd, developers currently have to choose which one of these to support.

“I’m really thrilled to see that we were able to pull together a pretty broad consortium of folks from across the industry to help us drive some interoperability in the service mesh space,” Gabe Monroy, Microsoft’s lead product manager for containers and the former CTO of Deis, told me. “This is obviously hot technology — and for good reasons. The cloud-native ecosystem is driving the need for smarter networks and smarter pipes and service mesh technology provides answers.”

“I’m really thrilled to see that we were able to pull together a pretty broad consortium of folks from across the industry to help us drive some interoperability in the service mesh space,” Gabe Monroy, Microsoft’s lead product manager for containers and the former CTO of Deis, told me. “This is obviously hot technology — and for good reasons. The cloud-native ecosystem is driving the need for smarter networks and smarter pipes and service mesh technology provides answers.”

The partners here include Buoyant, HashiCorp, Solo.io, Red Hat, AspenMesh, Weaveworks, Docker, Rancher, Pivotal, Kinvolk and VMware . That’s a pretty broad coalition, though it notably doesn’t include cloud heavyweights like Google, the company behind Istio, and AWS.

“In a rapidly evolving ecosystem, having a set of common standards is critical to preserving the best possible end-user experience,” said Idit Levine, founder and CEO of Solo.io. “This was the vision behind SuperGloo — to create an abstraction layer for consistency across different meshes, which led us to the release of Service Mesh Hub last week. We are excited to see service mesh adoption evolve into an industry-level initiative with the SMI specification.”

For the time being, the interoperability features focus on traffic policy, telemetry and traffic management. Monroy argues that these are the most pressing problems right now. He also stressed that this common interface still allows the different service mesh tools to innovate and that developers can always work directly with their APIs when needed. He also stressed that the Service Mesh Interface (SMI), as this new specification is called, does not provide any of its own implementations of these features. It only defines a common set of APIs.

Currently, the most well-known service mesh is probably Istio, which Google, IBM and Lyft launched about two years ago. SMI may just bring a bit more competition to this market since it will allow developers to bet on the overall idea of a service mesh instead of a specific implementation.

In addition to SMI, Microsoft also today announced a couple of other updates around its cloud-native and Kubernetes services. It announced the first alpha of the Helm 3 package manager, for example, as well as the 1.0 release of its Kubernetes extension for Visual Studio Code and the general availability of its AKS virtual nodes, using the open source Virtual Kubelet project.

Powered by WPeMatico

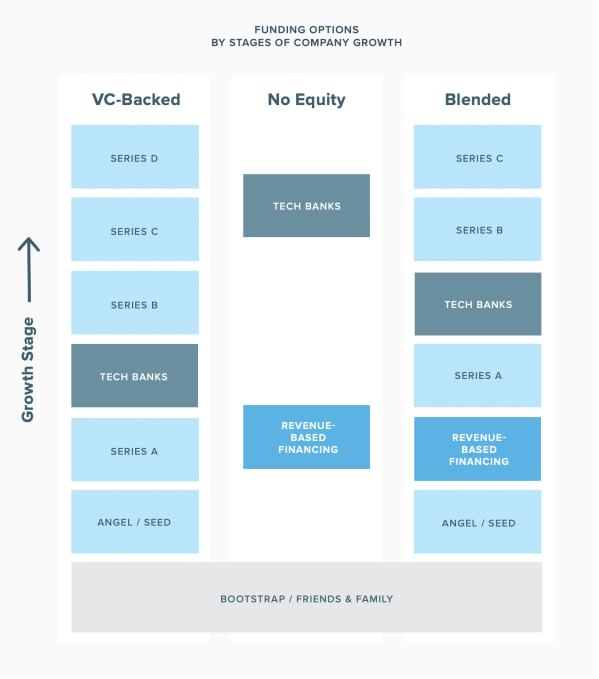

Revenue-based financing is on the rise, at least according to Lighter Capital, a firm that doles out entrepreneur-friendly debt capital.

What exactly is RBF you ask? It’s a relatively new form of funding for tech companies that are posting monthly recurring revenue. Here’s how Lighter Capital, which completed 500 RBF deals in 2018, explains it: “It’s an alternative funding model that mixes some aspects of debt and equity. Most RBF is technically structured as a loan. However, RBF investors’ returns are tied directly to the startup’s performance, which is more like equity.”

Source: Lighter Capital

What’s the appeal? As I said, RBFs are essentially dressed up debt rounds. Founders who opt for RBFs as opposed to venture capital deals hold on to all their equity and they don’t get stuck on the VC hamster wheel, the process in which you are forced to continually accept VC while losing more and more equity as a means of pleasing your investors.

RBFs, however, are better than traditional debt rounds because the investors are more incentivized to help the companies they invest in because they are receiving a certain portion of that business’s monthly revenues, typically 1% to 9%. Eventually, as is explained thoroughly in Lighter Capital’s newest RBF report, monthly payments come to an end, usually 1.3 to 2.5X the amount of the original financing, a multiple referred to as the “cap.” Three to five years down the line, any unpaid amount of said cap is due back to the investor. When all is said in done, ideally, the startup has grown with the support of the capital and hasn’t lost any equity.

At this point, they could opt to raise additional revenue-based capital, they could turn to venture capital or they could tap a tech bank to help them get to the next step. The idea is RBF is easier on the founder and it allows them optionality, something that is often lost when companies turn to VCs.

IPO corner, rapid-fire edition

Slack’s direct listing will be on June 20th. Get excited.

China’s Luckin Coffee raised $650 million in upsized U.S. IPO

Crowdstrike, a cybersecurity unicorn, dropped its S-1.

Freelance marketplace Fiverr has filed to go public on the NYSE.

Plus, I had a long and comprehensive conversation with Zoom CEO Eric Yuan this week about the company’s closely watched IPO. You can read the full transcript here.

Silicon Valley entrepreneur Hosain Rahman, the man behind Jawbone, has managed to raise $65.4 million for his new company, according to an SEC filing. The paperwork, coincidentally or otherwise, was processed while most of the world’s attention was focused on Uber’s IPO. Jawbone, if you remember, produced wireless speakers and Bluetooth earpieces, and went kaput in 2017 after burning up $1 billion in venture funding over the course of 10 years. Ouch.

On the heels of enterprise startup UiPath raising at a $7 billion valuation, the startup’s biggest investor is announcing a new fund to double down on making more investments in Europe. VC firm Accel has closed a $575 million fund — money that it plans to use to back startups in Europe and Israel, investing primarily at the Series A stage in a range of between $5 million and $15 million, reports TechCrunch’s Ingrid Lunden. Plus, take a closer look at Contrary Capital. Part accelerator, part VC fund, Contrary writes small checks to student entrepreneurs and recent college dropouts.

Our paying subscribers are in for a treat this week. Our in-house venture capital expert Danny Crichton wrote down some thoughts on Uber and Lyft’s investment bankers. Here’s a snippet: “Startup CEOs heading to the public markets have a love/hate relationship with their investment bankers. On one hand, they are helpful in introducing a company to a wide range of asset managers who will hopefully hold their company’s stock for the long term, reducing price volatility and by extension, employee churn. On the other hand, they are flagrantly expensive, costing millions of dollars in underwriting fees and related expenses…”

Read the full story here and sign up for Extra Crunch here.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about the notable venture rounds of the week, CrowdStrike’s IPO and more of this week’s headlines.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico

Slack this morning disclosed estimated preliminary financial results for the first quarter of 2019 ahead of a direct listing planned for June 20.

Citing an addition of paid customers, the workplace messaging service posted revenues of about $134 million, up 66% from $81 million in the first quarter of 2018. Losses from operations increased from $26 million in Q1 2018 to roughly $39 million this year.

In addition to filing updated paperwork, the Slack executive team gathered on Monday to make a final pitch to potential shareholders, emphasizing its goal of replacing email within enterprises across the world.

“People deserve to do the best work of their lives,” Slack co-founder and chief executive officer Stewart Butterfield said in a video released alongside a live stream of its investor day event. “This desire of feeling aligned with your team, of removing confusion, of getting clarity; the desire for support in doing the best work of your life, that’s universal, that’s deeply human. It appeals to people with all kinds of roles, in all kinds of industries, at all scales of organization and all cultures.”

“We believe that whoever is able to unlock that potential for people … is going to be the most important software company in the world. We aim to be that company,” he added.”

Slack, valued at more than $7 billion with its last round of venture capital funding, plans to list on the NYSE under the ticker symbol “SK.”

The business filed to go public in April as other well-known tech companies were finalizing their initial public offerings. Following Uber’s disastrous IPO last week, public and private market investors alike will be keeping a close-eye on Slack’s stock market performance, which may determine Wall Street’s future appetite for Silicon Valley’s unicorns.

Though some of the recent tech IPOs performed famously, like Zoom, Uber and Lyft’s performance has served as a cautionary tale for going out in poor market conditions with lofty valuations. Uber began trading last week at below its IPO price of $45 and is today down significantly at just $36 per share. Lyft, for its part, is selling for $47.5 apiece today after pricing at $72 per share in March.

Slack isn’t losing billions per year like Uber, but it’s also not as close to profitability as expected. In the year ending January 31, 2019, Slack posted a net loss of $138.9 million and revenue of $400.6 million. That’s compared to a loss of $140.1 million on revenue of $220.5 million for the year ending January 31, 2018. In its S-1, the company attributed its losses to scaling the business and capitalizing on its market opportunity.

Workplace messaging startup Slack said Monday, February 4, 2019 it had filed a confidential registration for an initial public offering, becoming the latest of a group of richly valued tech enterprises to look to Wall Street. (Photo by Eric BARADAT / AFP) (Photo credit should read ERIC BARADAT/AFP/Getty Images)

Slack currently boasts more than 10 million daily active users across more than 600,000 organizations — 88,000 on the paid plan and 550,000 on the free plan.

Slack has been able to bypass the traditional roadshow process expected of an IPO-ready business, opting for a path to Wall Street popularized by Spotify in 2018. The company plans to complete in mid-June a direct listing, which allows companies to forgo issuing new shares and instead sell directly to the market existing shares held by insiders, employees and investors. The date, however, is subject to change.

Slack has previously raised a total of $1.2 billion in funding from investors, including Accel, Andreessen Horowitz, Social Capital, SoftBank, Google Ventures and Kleiner Perkins.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

We are back, as promised. Kate Clark and Alex Wilhelm re-convened today to discuss the latest from the Uber IPO. Namely that it opened down, and then kept falling.

A few questions spring to mind. Why did Uber lose ground? Was it the company’s fault? Was it simply the macro market? Was it something else altogether? What we do know is that Uber’s pricing wasn’t what we were expecting and its first day was not smooth.

There are a whole bunch of reasons why Uber went out the way it did. Firstly, the stock market has had a rough week. That, coupled with rising U.S.-China tensions made this week one of the worst of the year for Uber’s monstrous IPO.

But, to make all that clear, we ran back through some history, recalled some key Lyft stats, and more.

We don’t know what’s next but we will be keeping a close watch, specifically on the next cohort of unicorn companies ready to IPO (Postmates, hi!).

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Pocket Casts, Downcast and all the casts.

Powered by WPeMatico

Uber’s much heralded public offering has arrived not so much with a bang as with a whimper, thanks largely to the ongoing trade war between the U.S. and China.

Overnight, the U.S. government made good on the threat from President Donald Trump to hike tariffs on $200 billion worth of Chinese goods to 25% up from 10%.

As a result, stock markets slid further on Friday, and their decline hit Uber’s initial public offering. The company’s shares began trading at $42.54, below its initial pricing of $45 per share.

At its initial pricing, Uber was valued at $75.5 billion, below the $120 billion price that Wall Street thought the company would fetch late last year, but still among the biggest public offerings in history. Only Facebook’s $81 billion public offering and the whopping $169 billion debut of Alibaba were bigger, according to a Dealogic analysis cited by Business Insider.

Uber’s historic public offering — which was designed to raise at least $90 billion for the ride-hailing giant — was no match for the equally historic struggle between the U.S. and China’s emerging economic superpower.

The rising tariffs were designed to hit business equipment, but will also affect prices on some $40 billion in consumer goods — ranging from clothes to furniture, refrigerators, washers and dryers.

Trump boosted tariffs after China reneged on certain concessions it had made during the trade negotiations. Chiefly, the U.S. was looking for written commitments from the Chinese government that it would provide less direct support to its state-owned enterprises and loosen restrictions on U.S. companies operating in the country.

Uber’s disappointing debut can’t be chalked up to trade woes alone. Its immediate American rival, Lyft, has seen its stock decline precipitously since its opening at nearly $79 per share. Lyft is now trading at around $55 per share.

Yesterday, Lyft reported its first earnings as a public company, losing $1.14 billion on $776 million in revenue.

While Lyft is focused on consumer transportation, Uber has expanded to include freight shipping and meal delivery as part of its attempts to become an all-in-one hub for consumer and business logistics.

That expansion has come at a cost. The company may have generated revenues of $11.3 billion in 2018, but it operated at a $3 billion loss for the year. And Uber is deeply in the red. With deficits reaching nearly $8 billion by the end of 2018, as MarketWatch points out.

Trade wars, it seems, trump transportation disruption.

Powered by WPeMatico

Greetings from Seattle, the land of Amazon, Microsoft, two of the world’s richest men and some startups.

I’m always surprised the Seattle startup ecosystem hasn’t grown to compete with the likes of Silicon Valley — or at least Boston and New York City — since the dot-com boom. Today, it’s the strongest it’s been due to the successes of companies like the newly minted unicorn Outreach, trucking business Convoy and, of course, the dog walking startup Rover. But the city still lags behind, failing to adopt the culture of entrepreneurship that defines San Francisco.

I spent a lot of time wondering why it hasn’t reached its full potential. Is it because Microsoft and Amazon pay their employees so well they don’t have the same urge to build something from the ground up? Is it a lack of access to capital? Is the city not attracting top talent? If you have thoughts, send them my way.

“We think part of the issue is a lack of capital and a lack of help,” Rover and Pioneer Square Labs co-founder Greg Gottesman told TechCrunch earlier this year. “If we can provide a little bit of both of those things, we can really put Seattle where it deserves to be, should be and will be.”

Despite its shortcomings, there is still some action in the city I want to highlight this week. A same-day delivery business, Dolly, is on the rise. The startup told me on Thursday it had raised a $7.5 million round from Unlock Venture Partners, Maveron and Jeff Wilke, the chief executive officer of Amazon Worldwide Consumer. Maveron, if you remember, is the VC fund co-founded by Starbucks founder Howard Schultz.

In other Seattle news, Madrona Venture Group, a well-regarded fund, raised an additional $100 million this week. Typically, Madrona focuses on companies based in the Pacific Northwest, but this fund will deploy capital throughout the entire U.S. Hmmm, that’s not necessarily a good sign for Seattle founders, but great progress for the ecosystem nonetheless.

If you’re interested in learning more about Seattle tech, I’ve covered it a bit because it’s my hometown! Start with this story, which dives deep into a Seattle accelerator that’s working hard to encourage entrepreneurship in the city. Alright, on to other news.

Want more TechCrunch newsletters? Sign up here.

WeWork: The co-working giant now known as The We Company submitted confidential IPO documents to the SEC, the company confirmed in a press release Monday. Is this the next massive startup win or a house of cards waiting to be toppled by the glare of the public markets? TechCrunch’s Danny Crichton investigates.

Slack: The business is in its final steps toward a much-anticipated direct listing, with one source telling TechCrunch the listing will be complete within 45 days. The WSJ reported this week that Slack will make an online presentation to potential shareholders on May 13. This week, we dug deep into Slack’s S-1 and decided to evaluate just how well the tech press, us included, did in covering the company. For the most part, the tech press did decently well, except for one curious, $162 million gap.

Uber: Finally! That ride-hailing company is going public next week. That latest news? Uber co-founder Travis Kalanick won’t be ringing the opening bell. Uber would not be where it is today without Kalanick, but him being there would surely be a reminder of Uber’s rocky past.

Beyond Meat: Shares of the company surged up 135 percent in their market opener last week, valuing the company as high as $3.52 billion. Volatility was so high on the company’s stock that the Nasdaq had to pause trading of “BYND” shares.

Ofo has run into its fair share of issues, laying off hundreds of workers, shutting down its international division and more. Now, you can buy a piece of the startup’s history.

Now you can buy a piece of startup history… Ofo bikes for ~$60 https://t.co/LLJbDOXm0C

— Jon Russell (@jonrussell) April 29, 2019

In other micro-mobility news, Lyft’s head of scooter & bikes Liam O’Connor, who was hired to help transportation company Lyft build its bike and scooter operations, has left after seven months with the newly-public company. TechCrunch’s Ingrid Lunden has the scoop. Plus, Bird, the electric scooter unicorn doing its best to overcome regulatory barriers, has made its way back to San Francisco. Bird is using its business license in San Francisco to introduce monthly personal rentals in the city. The program enables people to rent a scooter for $24.99 a month with no cap on the number of rides. We’ll how that goes.

For some reason, people are giving Magic Leap more money. The company has secured another $280 million in a deal with Japan’s largest mobile operator, Docomo. Do you know what that means? The developer fo AR/VR headsets has raised a total of $2.6 billion. We’re just as confused as you.

Brand new venture capital funds:

Unshackled Ventures raised $20 million.

Exclusive: @UnshackledVC has a new $20M pre-seed fund to invest only in immigrants. Why? Because immigrants are “inherently more entrepreneurial:” https://t.co/ZLiZ1UczJV

— Kate Clark (@KateClarkTweets) May 2, 2019

Jungle Ventures closed on $175 million.

And Toyota AI Ventures launched a $100 million fund.

I have the inside story on Menlo Ventures early Uber stake and TechCrunch’s Connie Loizos goes deep with early Uber backer Bradley Tusk.

This week, we offer TechCrunch Extra Crunch subscribers exclusive tips on building extraordinary teams. Plus, the final piece in TechCrunch’s Greg Kumparak’s series on Niantic, the fast-growing developer of Pokemon Go. If you recall, we’ve captured much of Niantic’s ongoing story in the first three parts of our EC-1, from its beginnings as an “entrepreneurial lab” within Google, to its spin-out as an independent company and the launch of Pokémon GO, to its ongoing focus on becoming a platform for others to build augmented reality products upon.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and TechCrunch’s Danny Crichton chat about updates at the Vision Fund, Cheddar’s big exit and more of this week’s headlines.

Powered by WPeMatico

The San Francisco Bay Area is a global powerhouse at launching startups that go on to dominate their industries. For locals, this has long been a blessing and a curse.

On the bright side, the tech startup machine produces well-paid tech jobs and dollars flowing into local economies. On the flip side, it also exacerbates housing scarcity and sky-high living costs.

These issues were top-of-mind long before the unicorn boom: After all, tech giants from Intel to Google to Facebook have been scaling up in Northern California for over four decades. Lately however, the question of how many tech giants the region can sustainably support is getting fresh attention, as Pinterest, Uber and other super-valuable local companies embark on the IPO path.

The worries of techie oversaturation led us at Crunchbase News to take a look at the question: To what extent do tech companies launched and based in the Bay Area continue to grow here? And what portion of employees work elsewhere?

For those agonizing about the inflationary impact of the local unicorn boom, the data offers a bit of reassurance. While companies founded in the Bay Area rarely move their headquarters, their workforces tend to become much more geographically dispersed as they grow.

Just because a company is based in Northern California doesn’t mean most workers are there also. Headquarters, our survey shows, does not always translate into headcount.

“Headquarters location can often be the wrong benchmark to use to identify where employees are located,” said Steve Cadigan, founder of Cadigan Talent Ventures, a Silicon Valley-based talent consultancy. That’s particularly the case for large tech companies.

Among the largest technology employers in Northern California, Crunchbase News found most have fewer than 25 percent of their full-time employees working in the city where they’re headquartered. We lay out the details for 10 of the most valuable regional tech companies in the chart below.

With the exception of Intel, all of these companies have a double-digit percentage of employees at headquarters, so it’s not as if they’re leaving town. However, if you’re a new hire at Silicon Valley’s most valuable companies, it appears chances are greater that you’ll be based outside of headquarters.

Tesla, meanwhile, is somewhat of a unique case. The company is based in Palo Alto, but doesn’t crack the city’s list of top 10 employers. In nearby Fremont, Calif., however, Tesla is the largest city employer, with roughly 10,000 reportedly working at its auto plant there.(Tesla has about 49,000 employees globally.)

High-valuation private and recently public tech companies can also be pretty dispersed.

Although they tend to have a larger percentage of employees at headquarters than more-established technology giants, the unicorn crowd does like to spread its wings.

Take Uber, the poster child for this trend. Although based in San Francisco, the ride-hailing giant has fewer than one-fourth of its employees there. Out of a global workforce of around 22,300, only about 5,000 are SF-based.

It’s unclear if that kind of breakdown is typical. We had trouble assembling similar geographic employee counts at other Bay Area unicorns, mainly because cities break out numbers only for their 10 largest employers. The lion’s share of regional unicorns are San Francisco-based, and of them only Uber made the Top 10.

That said, there is another, rougher methodology for assessing who works at headquarters: job postings. At a number of the most valuable Bay Area-based unicorns — including Airbnb, Juul, Lime, Instacart, Stripe and the now-public Lyft — a high number of open positions are far from the home office. And as we wrote last year, private companies have been actively seeking out cities to set up secondary hubs.

Even for earlier-stage startups, it’s not uncommon to set up headquarters in the San Francisco area for access to financing and networking, while doing the bulk of hiring in another location, Cadigan said. The evolution of collaborative work tools has also enabled more companies to add staff working remotely or in secondary offices.

Plus, of course, unicorn startups tend to be national or global in focus, and that necessitates hiring where their customers are located.

As we wrap up, it’s worth bringing up how unusual it once was for denizens of a metro area to oppose a big influx of high-skill jobs. In the past couple of years, however, these attitudes have become more common. Witness Queens residents’ mixed reactions to Amazon’s HQ2 plans. And in San Francisco, a potential surge of newly minted IPO millionaires is causing some consternation among locals, along with jubilation among the realtor crowd.

Just as college towns retain room for new students by graduating older ones, however, it seems reasonable that sustaining Northern California’s strength as a startup hub requires locating jobs out-of-area as companies scale. That could be good news for other cities, including Austin, Phoenix, Nashville, Portland and others, which have emerged as popular secondary locations for fast-growing unicorns.

That said, we’re not predicting near-term contraction in Bay Area tech employment, particularly of the startup variety. The region’s massive entrepreneurial and venture ecosystem keeps on producing valuable newcomers well-capitalized to keep hiring.

Methodology

We looked only at employment at company headquarters (except for Apple) . Companies on the list may have additional employees based in other Northern California cities. For Apple, we included all Silicon Valley employees, per estimates by the Silicon Valley Business Journal.

Numbers are rounded to the nearest hundred for the largest employers. Most of the data is for full-time employees only. Large tech employers hire predominantly full-time for staff positions, so part-time, whether included or not, is expected to reflect only a very small percentage of employment.

Cities list their 10 largest employers in annual reports. We used either the annual reports themselves or data excerpted in Wikipedia, using calendar year 2017 or 2018.

Powered by WPeMatico

Fastly, the content delivery network that’s raised $219 million in financing from investors (according to Crunchbase), is ready for its close up in the public markets.

The eight-year-old company is one of several businesses that improve the download time and delivery of different websites to internet browsers and it has just filed for an IPO.

Media companies like The New York Times use Fastly to cache their homepages, media and articles on Fastly’s servers so that when somebody wants to browse the Times online, Fastly’s servers can send it directly to the browser. In some cases, Fastly serves up to 90 percent of browser requests.

E-commerce companies like Stripe and Ticketmaster are also big users of the service. They appreciate Fastly because its network of servers enable faster load times — sometimes as quickly as 20 or 30 milliseconds, according to the company.

The company raised its last round of financing roughly nine months ago, a $40 million investment that Fastly said would be the last before a public offering.

True to its word, the company is hoping public markets have the appetite to feast on yet another “unicorn” business.

While Fastly lacks the sizzle of companies like Zoom, Pinterest or Lyft, its technology enables a huge portion of the activities in which consumers engage online, and it could be a bellwether for competitors like Cloudflare, which recently raised $150 million and was also exploring a public listing.

The company’s public filing has a placeholder amount of $100 million, but given the amount of funding the company has received, it’s far more likely to seek closer to $1 billion when it finally prices its shares.

Fastly reported revenue of roughly $145 million in 2018, compared to $105 million in 2017, and its losses declined year on year to $29 million, down from $31 million in the year-ago period. So its losses are shrinking, its revenue is growing (albeit slowly) and its cost of revenues are rising from $46 million to around $65 million over the same period.

That’s not a great number for the company, but it’s offset by the amount of money that the company’s getting from its customers. Fastly breaks out that number in its dollar-based net expansion rate figure, which grew 132 percent in 2018.

It’s an encouraging number, but as the company notes in its prospectus, it’s got an increasing number of challenges from new and legacy vendors in the content delivery network space.

The market for cloud computing platforms, particularly enterprise-grade products, “is highly fragmented, competitive and constantly evolving,” the company said in its prospectus. “With the introduction of new technologies and market entrants, we expect that the competitive environment in which we compete will remain intense going forward. Legacy CDNs, such as Akamai, Limelight, EdgeCast (part of Verizon Digital Media), Level3, and Imperva, and small business-focused CDNs, such as Cloudflare, InStart, StackPath, and Section.io, offer products that compete with ours. We also compete with cloud providers who are starting to offer compute functionality at the edge like Amazon’s CloudFront, AWS Lambda, and Google Cloud Platform.”

Powered by WPeMatico