Lydia

Auto Added by WPeMatico

Auto Added by WPeMatico

French startup Lydia is better known as the dominant app for peer-to-peer payments. But the company has been adding more features, such as a debit card, account aggregation, donations, money pots and more. This week, the company is adding savings accounts thanks to a partnership with French fintech startup Cashbee.

If you aren’t familiar with Cashbee, the company lets you open savings accounts through a mobile app. After connecting your bank account with Cashbee, you can transfer money back and forth between your bank account and a savings account.

Right now, Cashbee partners with My Money Bank for the savings accounts. Cashbee doesn’t keep your money, it just acts as a middle person between your bank account and My Money Bank. With those savings accounts, users can expect an interest rate of 0.6% after an introductory rate of 2% for a few months.

Lydia basically offers the same terms and conditions with a few differences. Instead of earning 2% interest for the first three months, Lydia users only earn more interest during the first two months.

The other big difference is that Lydia asks you to put at least €1,000 on your savings account when you open it. If you go through Cashbee’s app, you only have to put €10 or more. But users can do whatever they want after that when it comes to putting some money aside and withdrawing money from the savings account.

But the fact that Cashbee is seamlessly integrated in Lydia is interesting. It’s going to expose Cashbee to a lot more users as Lydia has more than 5 million users. It’s also an important feature if Lydia wants to become a financial super app.

This savings feature competes with Livret A, the most prevailing savings account in France. Everybody can open a Livret A in a retail bank. You get an interest rate of 0.5% net of taxes. On paper, 0.6% is better than 0.5%. But Cashbee’s savings accounts aren’t net of taxes.

If you’re a student and don’t pay any taxes, that’s a better deal. But many people pay 30% in taxes on accrued interests, which means that you end up earning 0.42% in interests net of taxes with a Cashbee account.

But it’s hard to beat the simplicity of Lydia’s solution here. For instance, you can save up to €1,000,000 on your savings account while the Livret A is limited to €22,950. In other words, if you’re already using Lydia to send, receive and spend money, you might want to check out those savings accounts.

Powered by WPeMatico

Fintech startups have been massively successful over the past few years. The biggest consumer startups managed to attract millions — sometimes even tens of millions — of users and have raised some of the biggest funding rounds in late-stage venture capital. That’s why they’ve also reached incredible valuations.

After a few wild years of growth, fintech startups are starting to act more like traditional finance companies.

And yet, this year’s economic downturn has been a challenge for the current class of fintech startups: Some have grown nicely, while others have struggled, but the vast majority of them have changed their focus.

Instead of focusing on growth at all costs, fintech startups have been drawing a path to profitability. It doesn’t mean that they’ll have a positive bottom line at the end of 2020. But they’ve laid out the core products that will secure those startups over the long term.

Usage of consumer products vary greatly with its users. And when you’re growing rapidly, supporting growth and opening new markets require a ton of effort. You have to onboard new employees constantly and your focus is split between product and corporate organization.

Lydia is the leading peer-to-peer payments app in France. It has four million users in Europe with most of them in its home country. For the past few years, the startup has been growing rapidly; engagement drives user signups, which drives engagement.

But what do you do when users stop using your product? “In April, the number of transactions was down 70%,” said Lydia co-founder and CEO Cyril Chiche in a phone interview.

“As for usage, it was obviously very quiet during some months and euphoric during other months,” he said. Overall, Lydia grew its user base by 50% in 2020 compared to 2019. When France wasn’t experiencing a lockdown or a curfew, the company beat its all-time high records across various metrics.

“In 2019, we grew all year long. In 2020, we’ve had very good growth numbers overall — but it should have been amazingly good during a normal year, without the month of March, April, May, November.” Chiche said.

In March and early April, Chiche didn’t know whether users would come back and send money using Lydia. Back in January, the company raised money from Tencent, the company behind WeChat Pay. “Tencent was ahead of us in China when it comes to lockdown,” Chiche said.

On April 30, during a board meeting, Tencent listed Lydia’s priorities for the rest of the year: Ship as many product updates as possible, keep an eye on their burn rate without firing people and prioritize product updates to reflect what people want.

“We’ve worked hard and shipped everything related to card payments, contactless mobile payments and virtual cards. It reflected the huge boost in contactless and e-commerce transactions,” Chiche said.

And it also repositioned the company’s trajectory to reach profitability more quickly. “The next step is bringing Lydia to profitability and it’s something that has always been important for us,” Chiche said.

Let’s list the most frequent revenue sources for consumer fintech startups such as challenger banks, peer-to-peer payment apps and stock-trading apps can be divided into three cohorts:

First, many companies hand customers a debit card when they create an account. Sometimes, it’s just a virtual card that they can use with Apple Pay or Google Pay. While there are some fees involved with card issuance, it also represents a revenue stream.

When people pay with their card, Visa or Mastercard takes a cut of each transaction. They return a portion to the financial company that issued the card. Those interchange fees are ridiculously small and often represent a few cents. But they can add up when you have millions of users actively using your cards to transfer money out of their accounts.

Many fintech companies, such as Revolut and Ant Group’s Alipay, are developing superapps to serve as financial hubs that cover all your needs. Popular superapps include Grab, Gojek and WeChat.

In some cases, they have their own paid products. But in most cases, they partner with specialized fintech companies to provide additional services. Sometimes, they are perfectly integrated in the app. For instance, this year, PayPal has partnered with Paxos so that you can buy and sell cryptocurrencies from their apps. PayPal doesn’t run a cryptocurrency exchange, it takes a cut on fees.

Powered by WPeMatico

French fintech startup Lydia has extended its Series B round. Accel is leading the extension with all major existing shareholders also participating. Lydia first raised $45 million in January 2020 — Tencent led that investment. The startup is now raising another $86 million, which means that Lydia has raised $131 million in total as part of its Series B round.

While Lydia wouldn’t discuss the valuation of the round, its co-founder and CEO gave me a hint. “The value of the company has really significantly increased between the two parts of the B round,” he told me.

Interestingly, Amit Jhawar is heading this investment for Accel . He joined Accel as a venture partner in July and he’s going to join Lydia’s board of directors.

Jhawar joined payments company Braintree in 2011 as COO and CFO. Shortly after, Braintree acquired peer-to-peer payment app Venmo. “When we acquired Venmo it was only 15 people. They had just released their mobile app in April of 2012,” Jhawar told me in a phone interview.

PayPal later acquired Braintree and Venmo — Jhawar stuck around until early 2020 to scale Venmo to the huge fintech consumer app that 52 million people use in the U.S. Jhawar believes that peer-to-peer payments represent the beginning of a long-term consumer relationship.

“You know that P2P is successful when they leave money in their account because they’re going to come back,” he said.

Back in 2014, when I first covered Lydia, I called it the Venmo for France — they had only raised €600,000 back then. It seems like Jhawar agrees with that take. Since then, Lydia has grown quite a lot and has expanded beyond peer-to-peer payments in various ways.

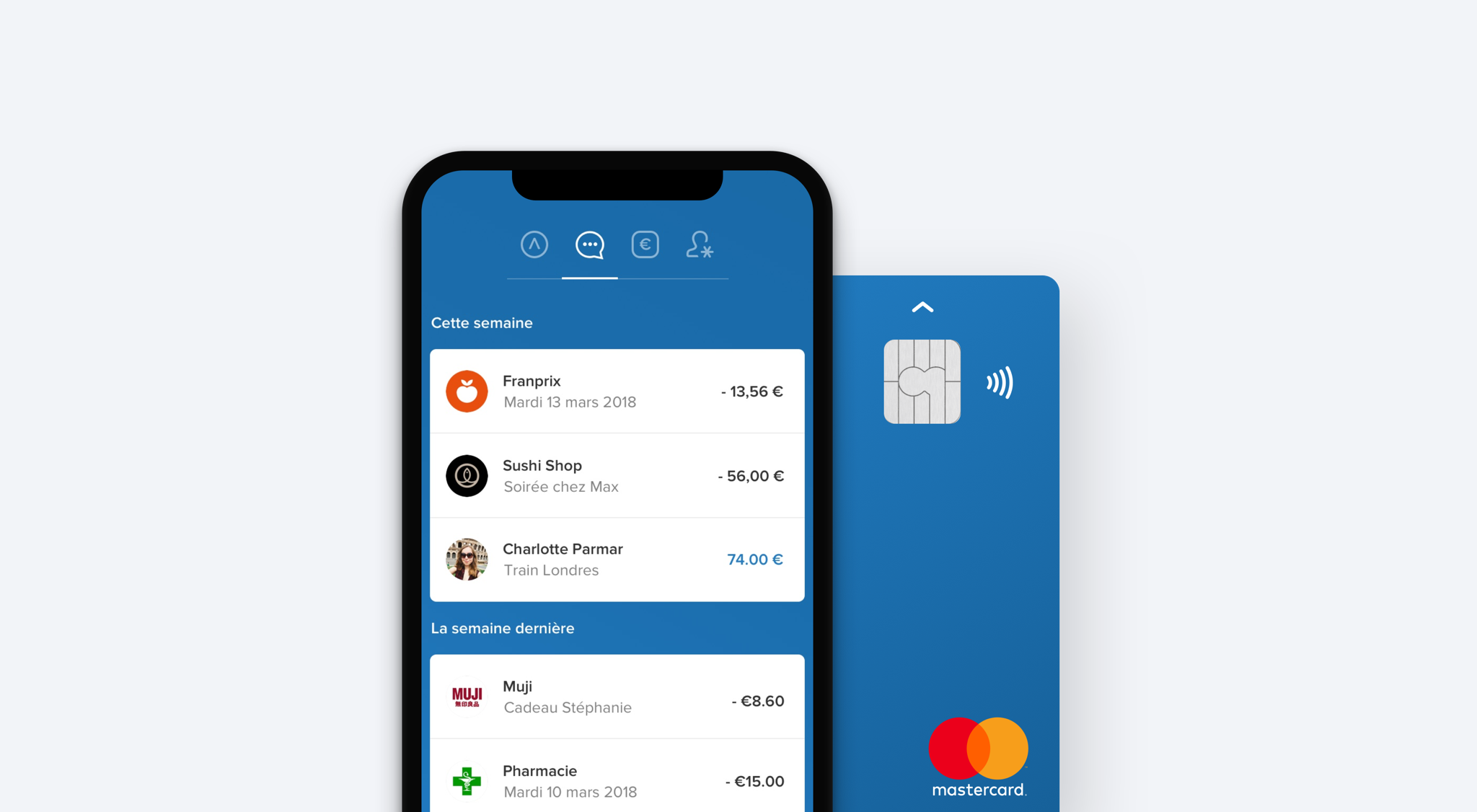

With Lydia, you can send money to another user in just a few seconds. You don’t have to enter an account number in your banking app — as long as you know their phone number, they’ll receive your payment.

If you have money in your account, you can choose to spend it directly using a Visa debit card. Lydia lets you generate a virtual card that works with Apple Pay and Google Pay — you can also order a plastic card.

Lydia also supports direct deposit as you get your own IBAN in the app. You can also create money pots and send a link to other users, view your bank accounts in Lydia, donate money to hospitals and charities, get a credit line, etc.

But there’s one killer feature that stands out over the rest. Bank accounts tend to be monolithic and don’t reflect how you use money. “If you look at banks today, they call the main account a checking account. It’s outdated by design,” CEO Cyril Chiche said.

Lydia has created flexible sub-accounts that you can use in many different ways. You can create a second sub-account and set some money aside for your bills. You can create a third one and share it with a few friends because you’re going on a vacation together.

You can move money from one account to another by swiping your finger across the account grid. As you can have multiple contributors and you can change the account associated with your debit card, it means that money flows more naturally. It feels like using a messaging app, not a financial app.

And it’s been working well in France. The company now has more than 4 million users. Transactions have doubled over the past year, which means that usage is accelerating.

“Lydia has the largest P2P network in Europe outside of PayPal and has the potential to grow all across Europe with a mobile-first, customer-focused solution. This will bring demand for incremental consumer financial products and high merchant interest to accept the payment,” Jhawar told me in an email.

And 2020 has been a busy year for Lydia. The company has just released a complete redesign to better position the app as a super app for financial services. All the interactions and all the main tabs have been changed.

Lydia also re-launched its premium offering with two new premium plans that offer you higher limits over the free plan and an insurance package for the most expensive offer. Those plans are more in line with what the app offers today and should contribute to the company’s bottom line. “The next step is bringing Lydia to profitability and it’s something that has always been important for us,” Chiche said in a recent interview.

Behind the scenes, Lydia has also upgraded many core features, such as migrating cards to a new infrastructure, adding alerts to account aggregation, supporting instant SEPA transfers to bank accounts, etc.

In 2021, the company plans to build on top of that new foundation with more financial products. “We’re going to try every single product — credit, savings, investment,” Chiche said.

The company is also slowly expanding to more countries. But it wants to offer a product that feels like a local product with a local card and a local IBAN to increase acceptance rates. Lydia is starting with Portugal.

Powered by WPeMatico

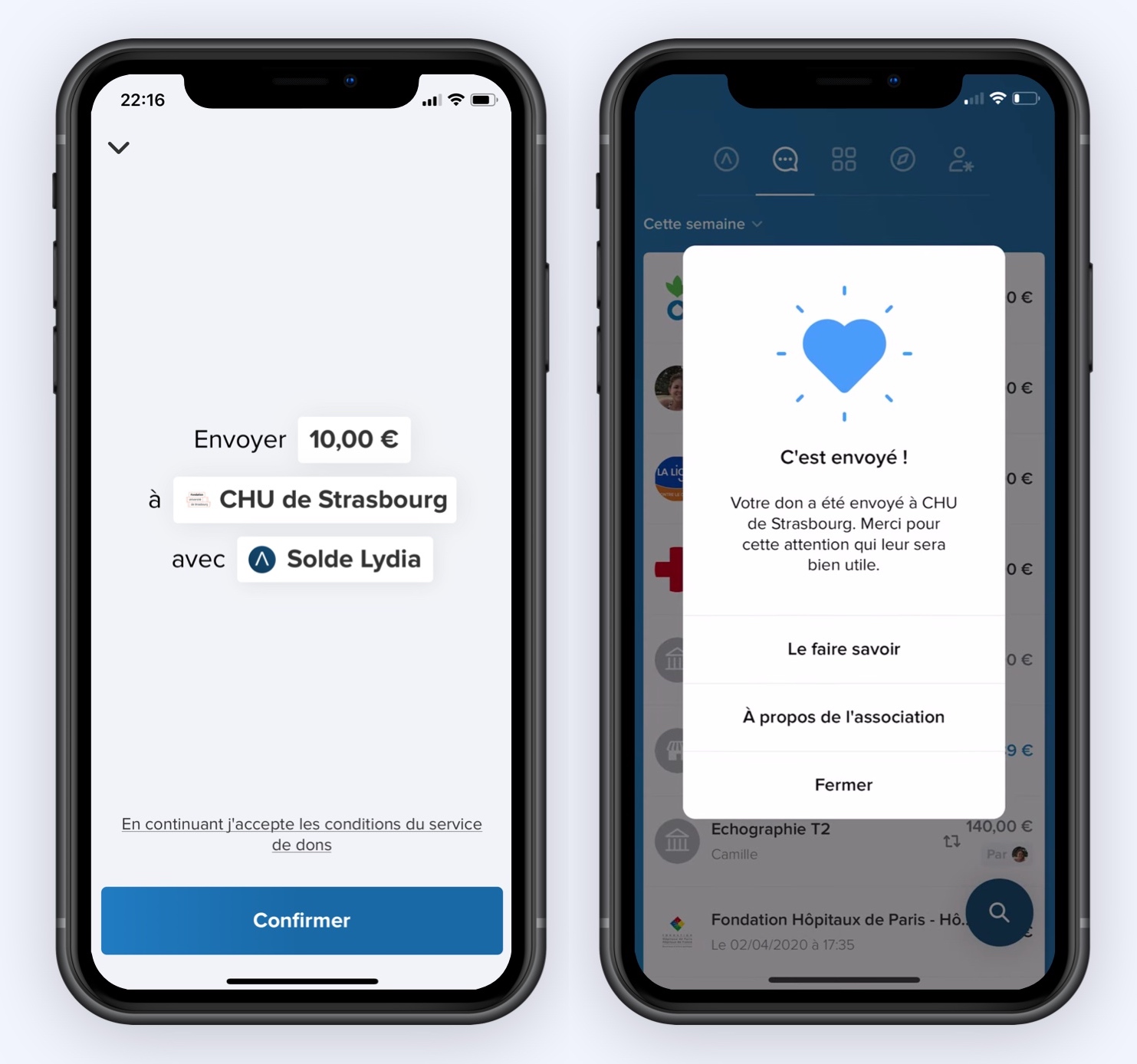

Fintech startup Lydia is the dominating mobile payment app in France with most of its 3.3 million users in its home country. That’s why the startup has been working hard over the past ten days to ship a feature that was originally planned for this summer — donations to charities and hospitals.

Starting today, Lydia users can choose between 17 charities and send money to those charities using the familiar Lydia payment flow. It works like sending money to your friends and family.

Donations start at €0.50 and those are one-off payments — you can’t set up recurring payments or round up transactions for instance.

Lydia recently introduced “the market”, a marketplace of financial products, such as small credit lines, phone insurance and free credit on home insurance and utility bills. The market menu was buried under the profile tab. The company is now surfacing that screen in its own tab right next to your accounts and transaction history. You can find donations as a new button in the market.

There’s another way to donate. On the payment screen, when you tap a sum and hit next, in addition to the usual list of recipients, you can choose to send money to a charity from there as well. This feature is live on Android and will be available soon on iOS — iOS users have to go through the market for now.

The startup has selected 17 charities for now, but that list could grow over time. You’ll find public hospitals (Paris, Nantes, Strasbourg, Grenoble, Lille and Nice), charities focused on health as well as general public interest charities (Fondation de France, Fondation 101, Médecins du Monde, Epic, Action contre la Faim, La Croix Rouge française, La Fondation Abbé Pierre, La Ligue Nationale contre le Cancer, Réseau Entourage and La Maison des Femmes de Saint-Denis).

If you’re not a Lydia user, you can still use Lydia’s payment flow in your web browser with a credit or debit card. (But nothing is stopping you from donating directly on the charity websites of course.)

If you want to give a large sum of money and deduct part of your donation from your income taxes, you’ll have to ask charities directly. Lydia can’t give you a tax form directly as it only acts as an intermediary.

Eventually, Lydia will deduct processing fees from your donations before handing them over to charities. But the company is waving fees until June 30 due to the coronavirus crisis.

Powered by WPeMatico

French startup Lydia is raising a $45 million Series B round (€40 million). Tencent is leading the round with existing investors CNP Assurances, XAnge and New Alpha also participating.

If you live in France, chances are you already know Lydia quite well. The company has become a ubiquitous mobile payment app, especially for people under 30 years old. Think about it as a sort of Square Cash or Venmo, but for France.

“At first, we wanted to raise less but we ended up raising more,” Lydia co-founder and CEO Cyril Chiche told me in a phone interview.

The company has managed to attract 3 million users in France. More impressive, 25% of French people between 18 and 30 years old have a Lydia account — and 5,000 people sign up every day. Lydia currently has 90 employees.

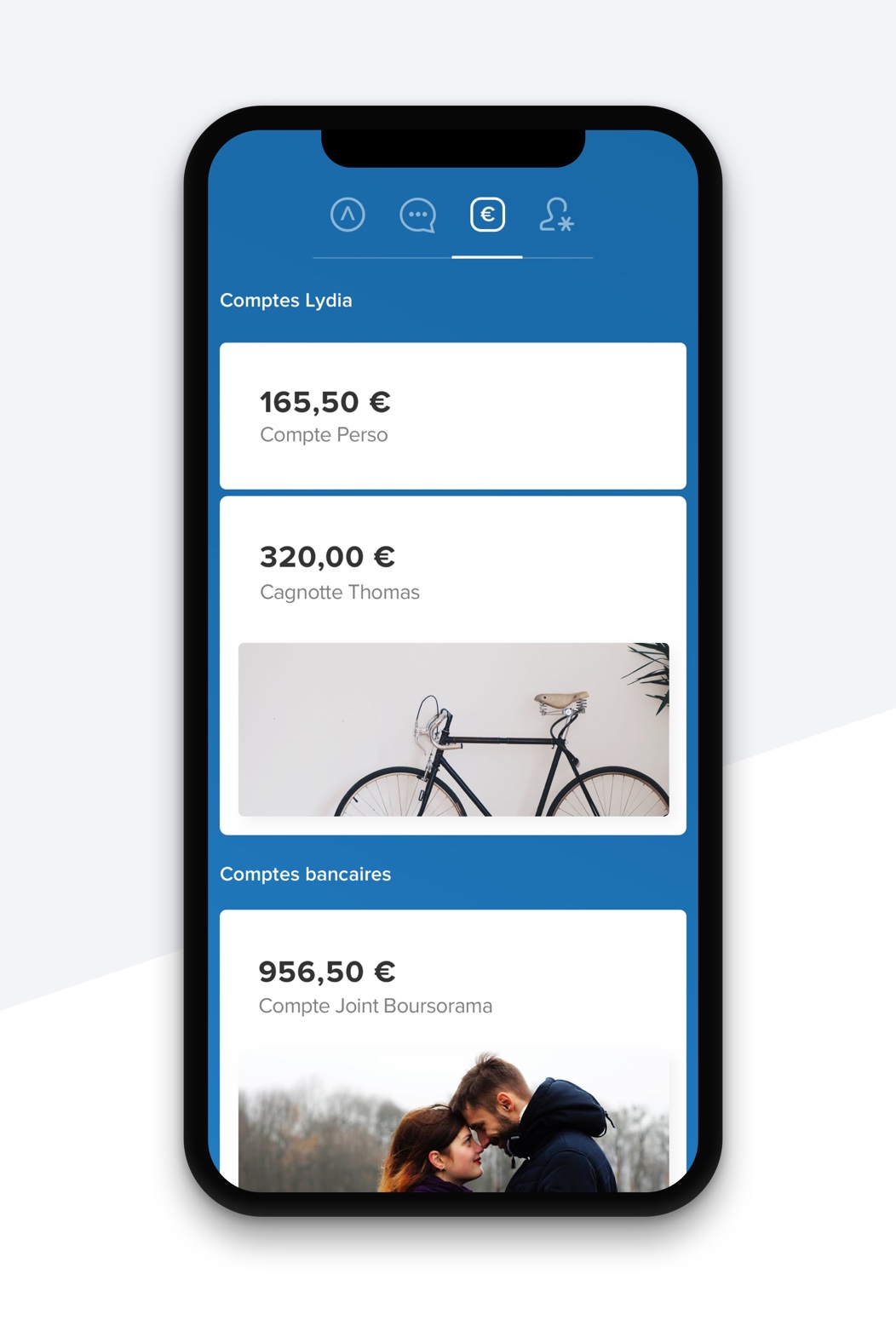

More recently, the company has expanded beyond peer-to-peer payment. First, the company wants to help you manage your money in many different ways with an important value — everything should happen in real time.

You can create multiple Lydia accounts to put some money aside or use money in that sub-account for a specific purpose. That feature alone turns the app into a versatile money management app.

For instance, you can associate a Lydia payment card with a Lydia account and a virtual card with another Lydia account — that virtual card works with Apple Pay, Google Pay, Samsung Pay and more. You can change those settings in real time.

You can share accounts with other Lydia users. And shared accounts are truly shared — everyone can top up and withdraw money from that account. You can spend directly from that account or withdraw money to another account.

You can also turn any Lydia account into a money pot account. In just a few taps, you can generate a link and share it with your friends so that they can add money using their regular payment card or a Lydia account.

More recently, the company has introduced “the market”, a marketplace of other financial products. From the Lydia app, you can borrow up to €1,000 in just a few seconds. You can also insure your phone and other mobile devices. You can get some free credit when you open a bank account, insure your home with Luko, switch to another electricity and gas provider, compare mobile phone and internet providers and more.

And that strategy is going to be key in the future. “We have an ambitious goal, which is turning Lydia into a mobile financial service app,” Chiche said.

He also pointed out that the company that has been the most successful when it comes to creating a mobile marketplace of financial products is Tencent with WeChat.

“Tencent is also the number one player in the video game industry, and there’s no industry with as much user engagement,” Chiche said. Tencent acquired Supercell, bought 40% of Epic Games, acquired Riot Games (League of Legends), invested in Ubisoft, Activision Blizzard, Discord, etc. Lydia hopes that it can learn from Tencent on the user engagement front.

Compared to many fintech startups, Lydia doesn’t want to replace banks altogether — the company says it wants to build a meta-banking app. Peer-to-peer payments represent the top of the funnel and a great user acquisition strategy thanks to networking effects.

You can then connect your Lydia account with your bank account and your debit card. This way, you can send money back and forth between your Lydia accounts and your bank account. As a user, that strategy slowly pays off over time. After a while, you end up spending money directly from your Lydia account and relying more heavily on Lydia’s native payment features, with your bank account acting as a money back end.

At the bottom of the funnel, Lydia hopes that it can turn active Lydia users into paid customers with a handful of in-house and third-party financial products. In other words, Lydia doesn’t want to become a credit institution like a traditional bank, it wants to become a financial hub. Expanding the marketplace will be a big focus for the company going forward.

While Lydia is available in other European countries, Lydia is still massively used in its home market with other markets lagging behind. With today’s funding round, growth in foreign countries is going to be the second key topic.

Powered by WPeMatico

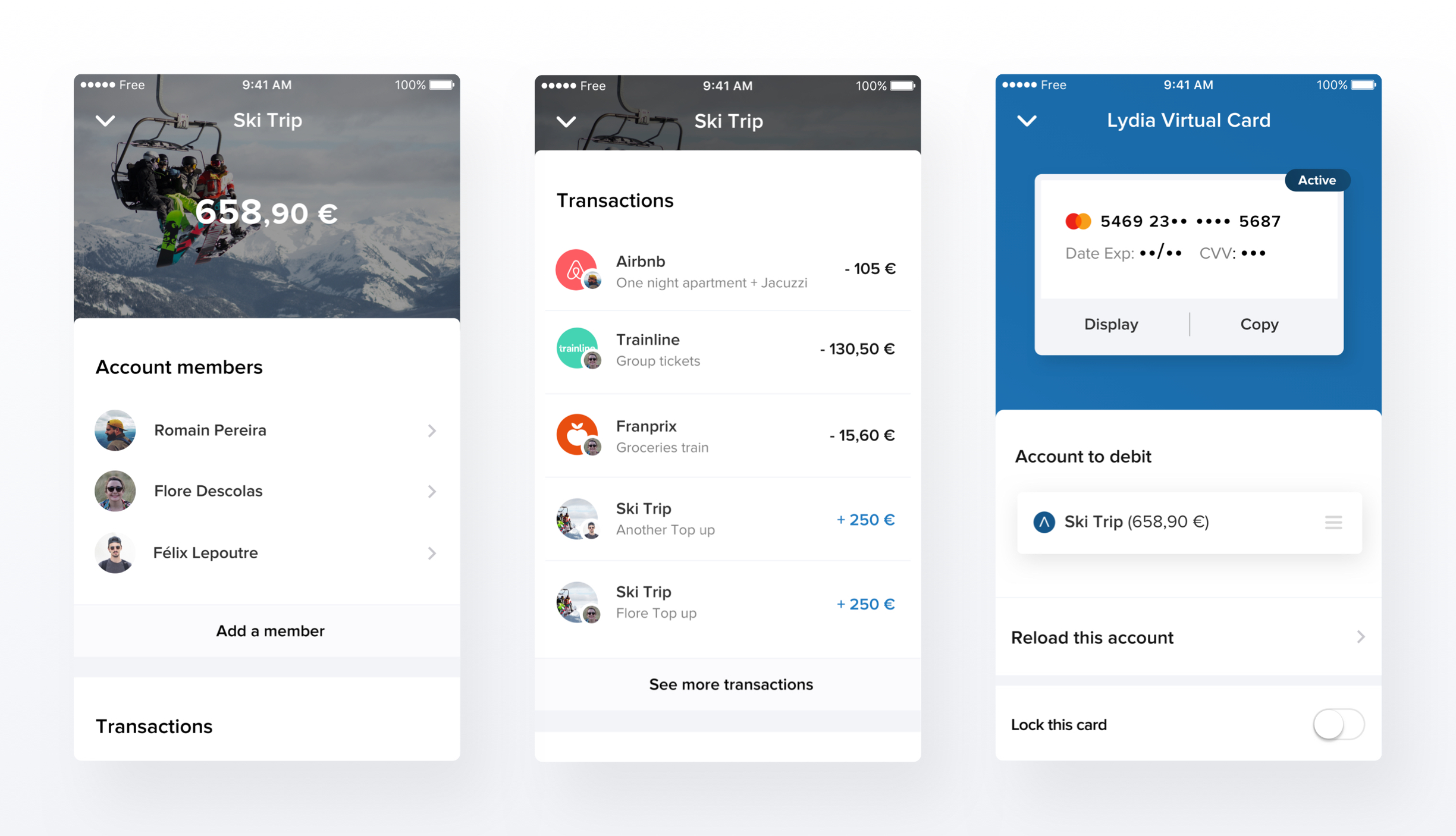

French startup Lydia now lets you share your Lydia sub-accounts with other people. The company wants to make it easier to manage money when you’re traveling with friends, sharing an apartment with someone and more.

When Lydia introduced its premium offering back in March 2018, the company completely rethought the way Lydia accounts worked. Users had a single Lydia account and were basically limited to sending, receiving and withdrawing money — it was all about peer-to-peer payments. Now, you can create as many Lydia accounts as you want, move money around, set money aside and top up each account separately.

That was just the first step as you can now share those accounts with other people. This way, you don’t have to create a Splitwise group and track who owes what to whom. Instead of getting your money back after a while, people chip in and top up the shared account directly. Anybody can then safely spend that money.

As always, Lydia is all about getting money in the app and out of the app as seamlessly as possible. When you create a shared account, each user can top up the account using other Lydia sub-accounts, a traditional bank account that you have already connected to the app or a debit card if it’s a small amount.

If your bank account isn’t compatible with Lydia, you also get an IBAN number for this sub-account in particular. So you can initiate a traditional bank transfer from your bank account as well.

Once the account is up and running, anybody can spend money. You can generate a virtual card, add it to Apple Pay, Google Pay or Samsung Pay, and associate it with the shared account. If you’re on a ski trip and buying raclette cheese for your group of friends, you can then pay with your phone and debit the shared account.

If you’re a premium user and have a good old plastic Lydia card, you can also use it in any card reader and associate transactions with your shared account. Some websites already let you pay with your Lydia account directly as well. You can select your sub-account when confirming the transaction on your phone.

You can imagine multiple different use cases for such a feature. This is a good way to share an account with your significant other without switching to the same bank. This could be a way to pay for utility bills with your roommates.

“I use it with my son for instance. I created a shared account, I set up a virtual card and he added it to his Google Pay,” co-founder and CEO Cyril Chiche told me. He can then send him money that he can use instantly whenever he needs to.

This feature will become more valuable over time, when you can pay with your Lydia account in more places. Mobile payment systems, such as Apple Pay and Google Pay, are slowly becoming more widespread. And Lydia has also been working with popular payment service providers to add support for more e-commerce websites.

It’s a radical way of sharing expenses with friends and family members, but it could become the obvious way if Lydia becomes ubiquitous.

Powered by WPeMatico

French startup Lydia announced a partnership with Banque Casino today for small credit lines. Starting tomorrow, Lydia users in France will be able to borrow as much as €1,000 in just a few seconds.

While Lydia started as a peer-to-peer money transferring app, fintech startups always end up offering credit at some point. It’s hard to make money without offering some form of credit.

Banque Casino is a subsidiary of Casino and Crédit Mutuel. As the name suggests, it’s a bank that can issue credit lines. Lydia has developed a seamless integration with Banque Casino so you can instantly get money from Banque Casino.

The credit feature lets you borrow between €100 and €1,000 and reimburse that credit line over three months. If you’re eligible, you’ll instantly see how much you’ll end up paying after three months.

But the most interesting feature is that you can either get your money instantly on your Lydia account for a fee, or you can wait a couple of weeks to wave this fee.

Combining instant credit with instant spending is key to this feature. Lydia lets you instantly spend money on your Lydia account on e-commerce websites that support Lydia, using Lydia’s debit card, or using a virtual card in Apple Pay, Google Pay or Samsung Pay. And if Lydia wants to replace cash, it needs to be as quick as giving a money bill to someone.

Lydia currently has 1.5 million users; 3,500 people open a Lydia account every day. The company recently released two insurance products for your mobile devices, as well.

Powered by WPeMatico

French startup Lydia is launching an insurance product for your mobile phone. For €4.29 per month ($4.89), you can insure your phone from the Lydia app.

Lydia is one of the most popular peer-to-peer payment apps in Europe, with 1.5 million users. Think about it as a sort of Venmo or Square Cash for Europe. More recently, the company started offering more options to manage your money with a premium subscription and additional features.

While Lydia doesn’t want to replace your bank and insurance company, the company is offering an insurance product for the first time. Lydia is partnering with its investor CNP Assurances — having an insurance company as an investor has a few advantages.

So here’s what you get. You’re instantly covered against cracked screens, liquid damage and accidental damage. There’s no excess, but you’re limited to one claim per year. Phones now cost a small fortune, but you’re limited to €500 ($570) per claim.

Optionally, you can subscribe to a better insurance product for €9.99 per month ($11.39). In addition to phone insurance, your laptop, tablet, Nintendo Switch, Kindle, camera and other electronics are covered. You can make two claims per year and you can get back up to €500 for your phone and €1,800 for other devices. More importantly, you’re also covered against theft.

Many phone carriers sell mobile phone insurance. But they usually cost more than that. In most cases, you also need to subscribe for at least one year. In Lydia’s case, you can cancel your subscription whenever you want in the app.

If that product sounds familiar, it’s because Revolut offers a similar feature (with some drawbacks). You can subscribe to mobile phone insurance from Revolut’s mobile app.

Pricing isn’t as straightforward with Revolut, as Premium subscribers get a discount. For an iPhone X, the insurance product costs as much as €9.58 per month ($10.92) without a Revolut Premium account, or as little as €6.67 per month ($7.60) if you pay upfront and you have a Revolut Premium account.

It’s a 12-month contract with a €125 excess and no theft protection. You also need to start insuring your phone quickly after buying (within six months), otherwise you aren’t covered. Revolut works with Allianz and Simplesurance for this insurance product.

Lydia may have borrowed the idea from Revolut, but I’m not sure why you’d choose Revolut’s insurance product over Lydia’s product.

It’s interesting to see that fintech companies are creating alternative revenue streams with insurance products. Subscribing to an insurance product is quick and painless, as they already manage your money and have your card on file.

Powered by WPeMatico

While French banks are just catching up to Apple Pay, French startup Lydia is adding support for Samsung Pay. If you have a recent Samsung phone, you can now add a virtual card to Samsung Pay and pay using your phone in your favorite stores.

Lydia started as a peer-to-peer payment app. It works more or less like Venmo or Square Cash in the U.S. After signing up, you can add a debit card to your account and send and receive money for free. You can withdraw your balance to a traditional bank account whenever you want.

The company has been adding more features to turn Lydia into the only banking app you need. You can now connect Lydia to your bank accounts, view your balances, get an IBAN, initiate transfers, create Lydia sub-accounts with multiple people and get a physical MasterCard.

Some features are now part of a premium subscription for €2.99 per month ($3.47) or €3.99 per month with the physical card ($4.62). The company also expanded to the U.K., Ireland, Spain and Portugal. There are a million registered users on Lydia.

More interestingly, Lydia wants to go beyond peer-to-peer payments. You can use Lydia to pay in some grocery stores, such as Franprix stores. You can also pay online by receiving a push notification and confirming the transaction in the Lydia app — Cdiscount supports Lydia for instance.

And when you can’t pay with your Lydia account directly, the startup doesn’t want to play favorites. You can generate a virtual card and enter the card number on an e-commerce website. You can add this virtual card to Apple Pay or Samsung Pay. Let’s see if Google Pay is next.

This could be particularly interesting for users who can’t use those payment systems because their banks don’t support those features. Let’s be honest, you rarely change your bank. With Lydia, you can still use Apple Pay or Samsung Pay with your existing bank account.

Powered by WPeMatico

French startup Lydia announces two new things today. First, the company is launching a financial hub with multiple new products. Second, Lydia is announcing a new premium subscription to access those new features.

“Today, we’re lucky enough to have you here to announce you the biggest thing we’ve done since Lydia’s launch,” co-founder and CEO Cyril Chiche said in a press conference. “We’ve been working on this for a while — and it’s not a challenger bank.”

Lydia is no longer just a peer-to-peer payment app with a few other features. The company says it is now building a meta-banking app, sitting above other financial products. So you’ll find and control a handful of financial products in the Lydia app.

“We didn’t want to stop at aggregating services,” Chiche said. “But we tried to think about people-centric, exclusive features that you can’t find anywhere else.”

![]()

Let’s go through the new features. There’s a new IBAN menu where you can add new recipients using a good old IBAN account. Lydia also asks you if you want to add specific IBANs to your own bank accounts. This way, instead of opening BNP Paribas’ app to copy and paste an IBAN into Société Générale’s app, you can add recipients from Lydia.

And of course, you can also send money to your recipient. You can use money from your Lydia e-wallet or from one of your own bank account. You don’t have to open your banking app anymore. Lydia leverages Budget Insight for this feature.

Lydia also supports recurring transactions. “It’s been the most requested features for multiple years,” co-founder and CTO Antoine Porte said. For instance, you can pay for your share of the internet bill every month using Lydia. The app sends you a notification every month to confirm the transaction.

Finally, there’s a brand new tab to get an overview of multiple accounts. You can see your bank account and Lydia sub-accounts. For instance, if you’re going on vacation with a few friends, you can create a Lydia sub-account and manage all your expenses from Lydia without any fee.

Interestingly, you can create a URL and send it to friends who are not using Lydia. Other users can then pay using your debit card. It feels like a streamlined version of Lydia’s existing money pot feature.

This is a big step for the company as Lydia is launching Lydia Premium for those new features. You can connect to your bank accounts, create recurring payments and sub-accounts for a monthly post. It’ll cost €2.99 per month ($3.69).

Existing features are still free. You can send and receive money in a just a few seconds with a Lydia transaction. You can pay in Franprix stores or on Cdiscount with your Lydia account.

You can try some of the new features with a free account. For instance, you can link one bank account, you can create one recurring payment, you can generate one virtual card, you can create money pots with some fees, etc.

Just like before, you can generate a virtual card for free so that you can pay on the internet or use Apple Pay with it. But if you’re a Lydia Premium subscriber, you’ll be able to generate multiple virtual cards to manage your online subscriptions. For instance, you can stop a subscription by deleting a virtual card or change the payment source for this card.

If you want to get a good old plastic card, you can pay an extra euro. For €3.99 per month ($4.92), you get everything I just described and a MasterCard. When you pay, the card uses your Lydia e-wallet and sends you a notification. You can open the app and choose one of your bank accounts to debit your bank account instantly.

Personal IBAN numbers and direct debits are no longer available for now — you could generate one for free. They’ll be back as part of Lydia Premium with new features as well as shared accounts. You’ll be able to pick a bank account for each transaction. For instance, you can say that you use LCL for your electricity bill and Fortuneo for your taxes. Lydia partners with Treezor for IBANs, virtual and physical cards.

Lydia currently has a little bit over a million registered users. And the startup is currently attracting around 2,000 new users every day. Over 80 percent of this user base has less than 30 years.

Lydia is currently available in France, Ireland, the U.K., Spain and Portugal. The startup also recently raised $16.1 million (€13 million) from CNP Assurances and others.

It’s interesting to see that Lydia isn’t competing head-to-head with challenger banks, such as N26 or Revolut (soon). The company thinks you can provide more value by partnering with multiple companies and building the interface that makes everything work together.

Powered by WPeMatico