Lordstown Motors

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

We were a smaller team this week, with Natasha and Alex joined by Grace and Chris to sort through a week that brought together both this quarter’s earnings cycle and the Q3 IPO rush. So, it was just a little busy!

Before we get to topics, however, a note that we are having a lot of fun recording these live on Twitter Spaces. We’ve found a hacky way to capture local audio and also share the chats live. So, hit us up on Twitter so you can hang out with us. It’s fun — and we may even bring you up on stage to play guest host.

OK, now, to the Great List of Subjects:

Powered by WPeMatico

Lordstown Motors continues to stumble. The beleaguered electric vehicle startup is now being investigated by the Department of Justice, in addition to an ongoing investigation by the Securities and Exchange Commission.

The investigation, first broke by the Wall Street Journal on Friday, is still in its early stages, according to unnamed sources. It is being conducted by the U.S. attorney’s office in Manhattan.

“Lordstown Motors is committed to cooperating with any regulatory or governmental investigations and inquiries,” a company spokesperson told TechCrunch. “We look forward to closing this chapter so that our new leadership – and entire dedicated team – can focus solely on producing the first and best full-size all-electric pickup truck, the Lordstown Endurance.”

The probe is just the latest in a series of woes for the startup, which recently said it had to cut production volumes for its debut electric pickup, Endurance, by half — from around 2,200 vehicles to 1,000. Just a few weeks after it made that announcement, there followed news of a corporate shakeup: the resignation of founding CEO Steve Burns and CFO Julio Rodriguez. Burns started the company as an offshoot of his previous startup, Workhorse Group.

Lordstown had a strong start, with investments from General Motors that helped it purchase a 6.2-million-square-foot factory from the leading automaker in late 2019. Lordstown made positive headlines last August, when it announced it would go public via a merger with a special purpose acquisition company (SPAC). The deal injected the EV startup with around $675 million in gross proceeds and skyrocketed its market value to $1.6 billion. Less than a year later, Lordstown informed the SEC that it does not have sufficient capital to manufacture Endurance.

Then, in March, the short-seller firm Hindenburg Research released a report disputing the company’s claims that it had booked 100,000 pre-orders for the electric pickup. It wrote that “extensive research reveals that the company’s orders appear largely fictitious and used as a prop to raise capital and confer legitimacy.” The SEC opened its investigation in the wake of these accusations.

The WSJ story is unclear on the scope of the inquiry and the company declined to provide details. TechCrunch will update the story if it learns more.

Powered by WPeMatico

The continuing saga of Lordstown Motor’s struggles as a public company took a new turn today as the electric truck manufacturer made yet more news. Bad news.

Shares of Lordstown are down sharply today after the company reported in an SEC filing that it does not have enough capital to build and launch its electric truck. Here’s the official verbiage (formatting, bolding: TechCrunch):

Since inception, the Company has been developing its flagship vehicle, the Endurance, an electric full-size pickup truck. The Company’s ability to continue as a going concern is dependent on its ability to complete the development of its electric vehicles, obtain regulatory approval, begin commercial scale production and launch the sale of such vehicles.

The Company believes that its current level of cash and cash equivalents are not sufficient to fund commercial scale production and the launch of sale of such vehicles. These conditions raise substantial doubt regarding our ability to continue as a going concern for a period of at least one year from the date of issuance of these unaudited condensed consolidated financial statements.

Now, companies that are trying to invent the future are more risky than, say, established banking concerns that are generating stable GAAP net income. I’m sure that SpaceX looked dicey at times when it was busy crashing rockets on its way to learning how to land them on drone ships.

But in the case of Lordstown’s admission that it cannot “fund commercial scale production and the launch of sale” of its Endurance pickup are fucking galling.

Why? Because when the company pitched its SPAC-led combination and public debut, it was pretty freaking confident that it would have enough cash to do so.

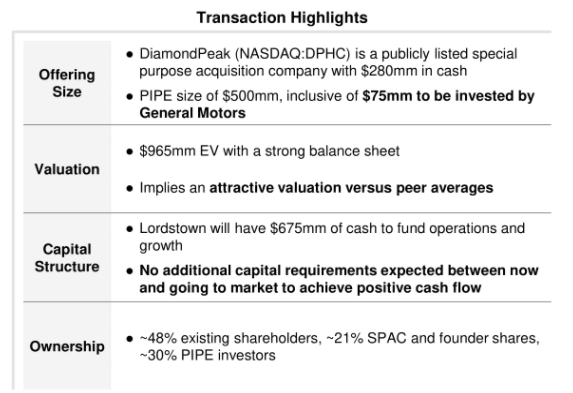

Don’t take my word for it. Here’s an excerpt from Lordstown’s investor deck:

You will note in the “Capital Structure” section that the company claimed that it would not need more funding to go to market.

Now Lordstown is pretty sure it’s going to need more money. If it’s putting the possible need in a filing, it means it.

Here’s what the company may do to solve its problems (formatting, bolding: TechCrunch):

To alleviate these conditions, management is currently evaluating various funding alternatives and may seek to raise additional funds through the issuance of equity, mezzanine or debt securities, through arrangements with strategic partners or through obtaining credit from government or financial institutions.

As we seek additional sources of financing, there can be no assurance that such financing would be available to us on favorable terms or at all. Our ability to obtain additional financing in the debt and equity capital markets is subject to several factors, including market and economic conditions, our performance and investor sentiment with respect to us and our industry.

In other words, the company is going to have to lever itself using debt, or dilute existing shareholders through the sale of equity, and Lordstown can’t promise that it will be able to do either “on favorable terms or at all.”

What we’re seeing here is the difference between SEC filings, which are no-bullshit zones, and SPAC decks, which are business propaganda. Shares of Lordstown fell more than 16% during regular trading, and another 6.9% in after-hours trading, as of the time of writing.

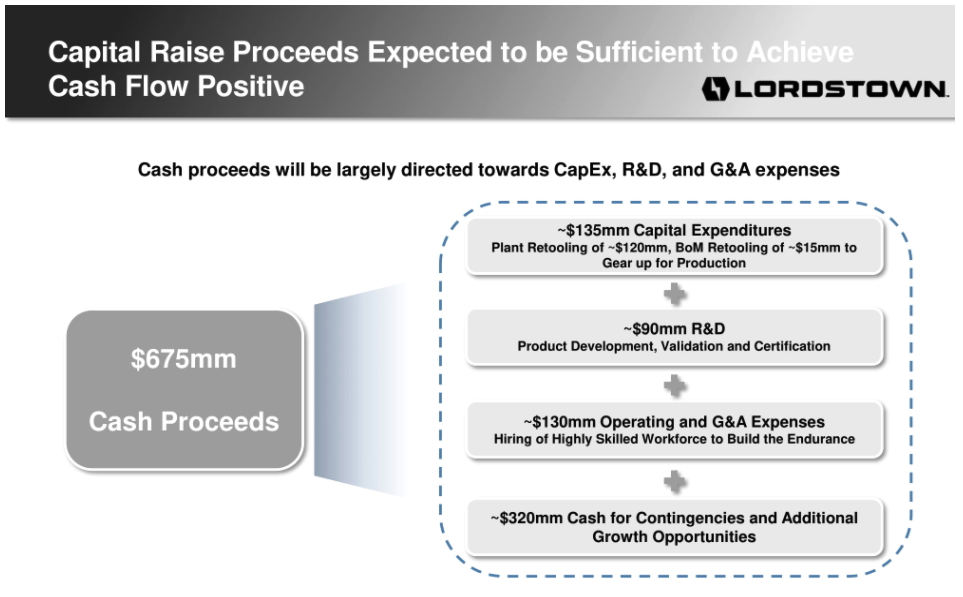

This mess from the company that put out this diagram in its investor deck:

In separate news, TechCrunch received an invite to a media availability to visit Lordstown’s operations in May, which included a note that the company “look[s] forward to opening [its] doors and showing you the latest progress from Lordstown Motors as [it] prepare[s] for the beginning of production in late September.” In a new missive sent today concerning the same event, the production timeline was not present.

So, yeah, maybe don’t trust SPAC decks much, if at all.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

This week had the whole crew aboard to record: Grace and Chris making us sound good, Danny to provide levity, Natasha to actually recall facts and Alex to divert us from staying on topic. It’s teamwork, people — and our transitions are proof of it.

And it’s good that we had everyone around the virtual table, as there was quite a lot to get through:

Thanks for hanging out this week, Equity is back on Tuesday with our usual weekly kickoff, thanks to the American holiday on Monday. Chat then, unless you want to follow us on Twitter and get a first-look at all of Chris’ meme work.

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday morning at 7:00 a.m. PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Lordstown Motors released its Q1 earnings yesterday, and the electric vehicle manufacturer is facing a few challenges.

Expenses were higher than expected, it plans to slash production by about 50%, and the company reported zero revenue and a net loss of $125 million. Oh, it also needs more capital.

“But there’s more to the Lordstown mess than merely a single bad quarter,” writes Alex Wilhelm. “Lordstown’s earnings mess and the resulting dissonance with its own predictions are notable on their own, but they also point to what could be shifting sentiment regarding SPAC combinations.”

In light of the company’s lackluster earnings report (and a pending SEC investigation), Alex unpacks the company’s Q1, “but don’t think that we’re only singling out one company; others fit the bill, and more will in time.”

Image Credits: TechCrunch

Join TechCrunch reporter Ron Miller and Patrik Liu Tran, co-founder and CEO of automated real-time data validation and quality monitoring platform Validio, on Thursday, May 27 at 9 a.m. PDT/noon EDT for a Clubhouse chat about ensuring data quality in the era of Big Data.

The world produces 2.5 quintillion bytes of data daily, but modern data infrastructure still lacks solutions for monitoring data quality and data validation.

Among other topics, they’ll discuss the build versus buy debate, how to better understand data failures, and why traditional methods for identifying data failures are no longer operational.

Click here to join the conversation.

Thanks very much for reading Extra Crunch; have a great week!

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

Image Credits: Nigel Sussman

Expensify may be the most ambitious software company ever to mostly abandon the Bay Area as the center of its operations.

The startup’s history is tied to places representative of San Francisco: The founding team worked out of Peet’s Coffee on Mission Street for a few months, then crashed at a penthouse lounge near the 4th and King Caltrain station, followed by a tiny office and then a slightly bigger one in the Flatiron building near Market Street.

Thirteen years later, Expensify still has an office a few blocks away on Kearny Street, but it’s no longer a San Francisco company or even a Silicon Valley firm. The company is truly global with employees across the world — and it did that before COVID-19 made remote working cool.

It makes sense that a company founded by internet pirates would let its workforce live anywhere they please and however they want to. Yet, how does it manage to make it all work well enough to reach $100 million in annual revenue with just a tad more than 100 employees?

As I described in Part 2 of this EC-1, that staffing efficiency is partly due to its culture and who it hires. It’s also because it has attracted top talent from across the world by giving them benefits like the option to work remotely all year as well as paying SF-level salaries even to those not based in the tech hub. It’s also got annual fully paid month-long “workcations” for every employee, their partner and kids.

Image Credits: TechCrunch

Managing Editor Jordan Crook interviewed Airbnb co-founder and CEO Brian Chesky to discuss the future of travel and what it was like leading the world’s biggest hospitality startup during a global pandemic.

“Our business initially dropped 80% in eight weeks. I say it’s like driving a car. You can’t go 80 miles an hour, slam on the brakes, and expect nothing really bad to happen.

Now imagine you’re going 80 miles an hour, slam on the brakes, then rebuild the car kind of while still moving, and then try to accelerate into an IPO, all on Zoom.”

Image Credits: alexsl (opens in a new window)/ Getty Images

There’s latent demand for life insurance currently unaddressed by much of the financial services industry, and embedded finance can be the solution.

It’s imperative for companies to consider product lines and partnerships to expand markets, create new revenue streams and provide added value to their customers.

Connecting consumers with products they need through channels they already know and trust is both a massive revenue opportunity and a social good, providing financial resilience to families at a time when they need it most.

Image Credits: Nigel Sussman (opens in a new window)

Zeta Global raised north of $600 million in private capital in the form of both equity financing and debt, making it a unicorn worth understanding.

The gist is that Zeta ingests and crunches lots of data, helping its users market to their customers on a targeted basis throughout their individual buying lifecycles. In simpler terms, Zeta helps companies pitch customers in varied manners depending on their own characteristics.

You can imagine that, as the digital economy has grown, the sort of work Zeta Global supports has only expanded. So, has Zeta itself grown quickly? And does it have an attractive business profile? We want to know.

Image Credits: Busakorn Pongparnit (opens in a new window) / Getty Images

In 2016, more than 20 years after Amazon’s founding and 10 years since Shopify launched, it would have been easy to assume e-commerce penetration (the percentage of total retail spend where the goods were bought and sold online) would be over 50%.

But what we found was shocking: The U.S. was only approximately 8% penetrated — only 8% for arguably the most advanced economy in the world!

Despite e-commerce growth skyrocketing over the past year, the reality is the U.S. has still only reached an e-commerce penetration rate of around 17%. During the last 18 months, we’ve closed the gap to South Korea and China’s e-commerce penetration of more than 25%, but there is still much progress to be made.

Here are five key predictions for what this road to further penetration will hold.

Image Credits: Nora Carol Photography (opens in a new window) / Getty Images

Every company wants to be innovative, but innovation comes with its share of difficulties. One key challenge for early-stage companies that are disrupting a particular space or creating a new category is figuring out how to sell a unique product to customers who have never bought such a solution.

This is especially the case when a solution doesn’t have many reference points and its significance may not be obvious.

Some buyers could use a walkthrough of the buying process. If you are building a singular product in a nascent market that necessitates forward-looking customers and want to drastically shorten sales cycles, create a buyer’s guide.

Image Credits: cruphoto (opens in a new window) / Getty Images

Pay attention to red flags when meeting with VCs: If they cancel late or leave you waiting, it’s a sign, just like being asked generic questions that demonstrate little or no understanding of the proposition. If they critique you or your business, that’s fine (obviously), but make sure you find out what’s behind their assertions to judge how well informed they are.

If you’re going to face these people each month and debate the direction of your business, the least you can expect is a robust argument outlining precisely why you may not have all the right answers.

If you fail to spot the warning signs, you’ll live to regret it. But do your due diligence and work constructively with them and, together, you might actually build a sustainable future.

Image via Getty Images / Westend61

This column aims to collect some of the most relevant recent discoveries and papers — particularly in, but not limited to, artificial intelligence — and explain why they matter.

In this edition, we have a lot of items concerned with the interface between AI or robotics and the real world. Of course, most applications of this type of technology have real-world applications, but specifically, this research is about the inevitable difficulties that occur due to limitations on either side of the real-virtual divide.

Image Credits: PeopleImages (opens in a new window) / Getty Images

Netflix has two CEOs: Co-founder Reed Hastings oversees the streaming side of the company, while Ted Sarandos guides Netflix’s content.

Warby Parker has co-CEOs as well — its co-founders went to college together. Other companies like the tech giant Oracle and luggage maker Away have shifted from having co-CEOs in recent years, sparking a wave of headlines suggesting that the model is broken.

While there isn’t a lot of research on companies with multiple CEOs, the data is more promising than the headlines would suggest. One study on public companies with co-CEOs revealed that the average tenure for co-CEOs, about 4.5 years, was comparable to solitary CEOs, “suggesting that this arrangement is more stable than previously believed.”

Furthermore, it’s impossible to be in two places at once or clone yourself. With co-CEOs, you can effectively do just that.

Powered by WPeMatico