LOL

Auto Added by WPeMatico

Auto Added by WPeMatico

The continuing saga of Lordstown Motor’s struggles as a public company took a new turn today as the electric truck manufacturer made yet more news. Bad news.

Shares of Lordstown are down sharply today after the company reported in an SEC filing that it does not have enough capital to build and launch its electric truck. Here’s the official verbiage (formatting, bolding: TechCrunch):

Since inception, the Company has been developing its flagship vehicle, the Endurance, an electric full-size pickup truck. The Company’s ability to continue as a going concern is dependent on its ability to complete the development of its electric vehicles, obtain regulatory approval, begin commercial scale production and launch the sale of such vehicles.

The Company believes that its current level of cash and cash equivalents are not sufficient to fund commercial scale production and the launch of sale of such vehicles. These conditions raise substantial doubt regarding our ability to continue as a going concern for a period of at least one year from the date of issuance of these unaudited condensed consolidated financial statements.

Now, companies that are trying to invent the future are more risky than, say, established banking concerns that are generating stable GAAP net income. I’m sure that SpaceX looked dicey at times when it was busy crashing rockets on its way to learning how to land them on drone ships.

But in the case of Lordstown’s admission that it cannot “fund commercial scale production and the launch of sale” of its Endurance pickup are fucking galling.

Why? Because when the company pitched its SPAC-led combination and public debut, it was pretty freaking confident that it would have enough cash to do so.

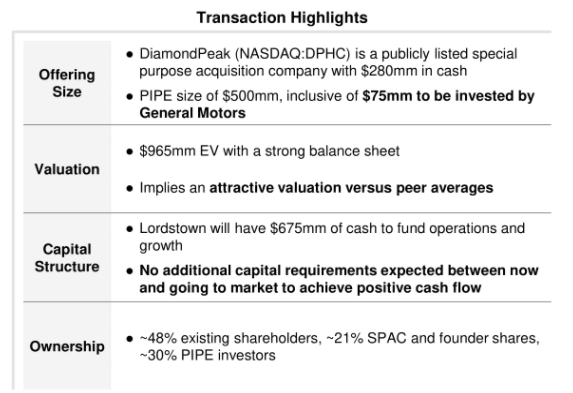

Don’t take my word for it. Here’s an excerpt from Lordstown’s investor deck:

You will note in the “Capital Structure” section that the company claimed that it would not need more funding to go to market.

Now Lordstown is pretty sure it’s going to need more money. If it’s putting the possible need in a filing, it means it.

Here’s what the company may do to solve its problems (formatting, bolding: TechCrunch):

To alleviate these conditions, management is currently evaluating various funding alternatives and may seek to raise additional funds through the issuance of equity, mezzanine or debt securities, through arrangements with strategic partners or through obtaining credit from government or financial institutions.

As we seek additional sources of financing, there can be no assurance that such financing would be available to us on favorable terms or at all. Our ability to obtain additional financing in the debt and equity capital markets is subject to several factors, including market and economic conditions, our performance and investor sentiment with respect to us and our industry.

In other words, the company is going to have to lever itself using debt, or dilute existing shareholders through the sale of equity, and Lordstown can’t promise that it will be able to do either “on favorable terms or at all.”

What we’re seeing here is the difference between SEC filings, which are no-bullshit zones, and SPAC decks, which are business propaganda. Shares of Lordstown fell more than 16% during regular trading, and another 6.9% in after-hours trading, as of the time of writing.

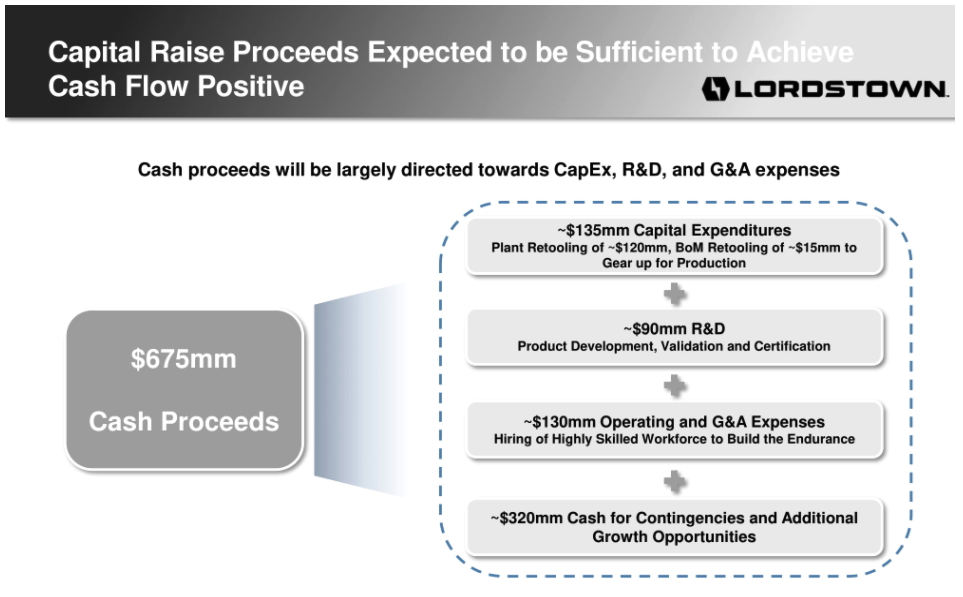

This mess from the company that put out this diagram in its investor deck:

In separate news, TechCrunch received an invite to a media availability to visit Lordstown’s operations in May, which included a note that the company “look[s] forward to opening [its] doors and showing you the latest progress from Lordstown Motors as [it] prepare[s] for the beginning of production in late September.” In a new missive sent today concerning the same event, the production timeline was not present.

So, yeah, maybe don’t trust SPAC decks much, if at all.

Powered by WPeMatico

Today’s WWDC keynote from Apple covered a huge range of updates. From a new macOS to a refreshed watchOS to a new iOS, better privacy controls, FaceTime updates, and even iCloud+, there was something for everyone in the laundry list of new code.

Apple’s keynote was essentially what happens when the big tech companies get huge; they have so many projects that they can’t just detail a few items. They have to run down their entire parade of platforms, dropping packets of news concerning each.

But despite the obvious indication that Apple has been hard at work on the critical software side of its business, especially its services-side (more here), Wall Street gave a firm, emphatic shrug.

This is standard but always slightly confusing.

Investors care about future cash flows, at least in theory. Those future cash flows come from anticipated revenues, which are born from product updates, driving growth in sales of services, software, and hardware. Which, apart from the hardware portion of the equation, is precisely what Apple detailed today.

And lo, Wall Street looked upon the drivers of its future earnings estimates, and did sayeth “lol, who really cares.”

Shares of Apple were down a fraction for most of the day, picking up as time passed not thanks to the company’s news dump, but because the Nasdaq largely rose as trading raced to a close.

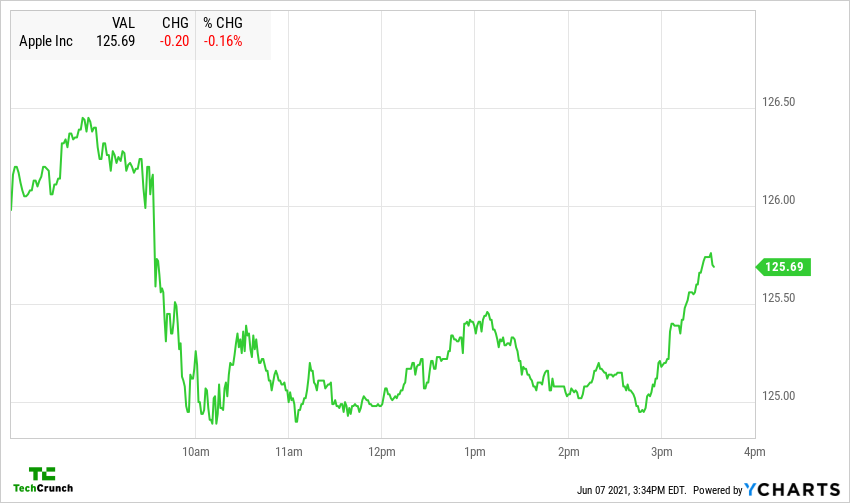

Here’s the Apple chart, via YCharts:

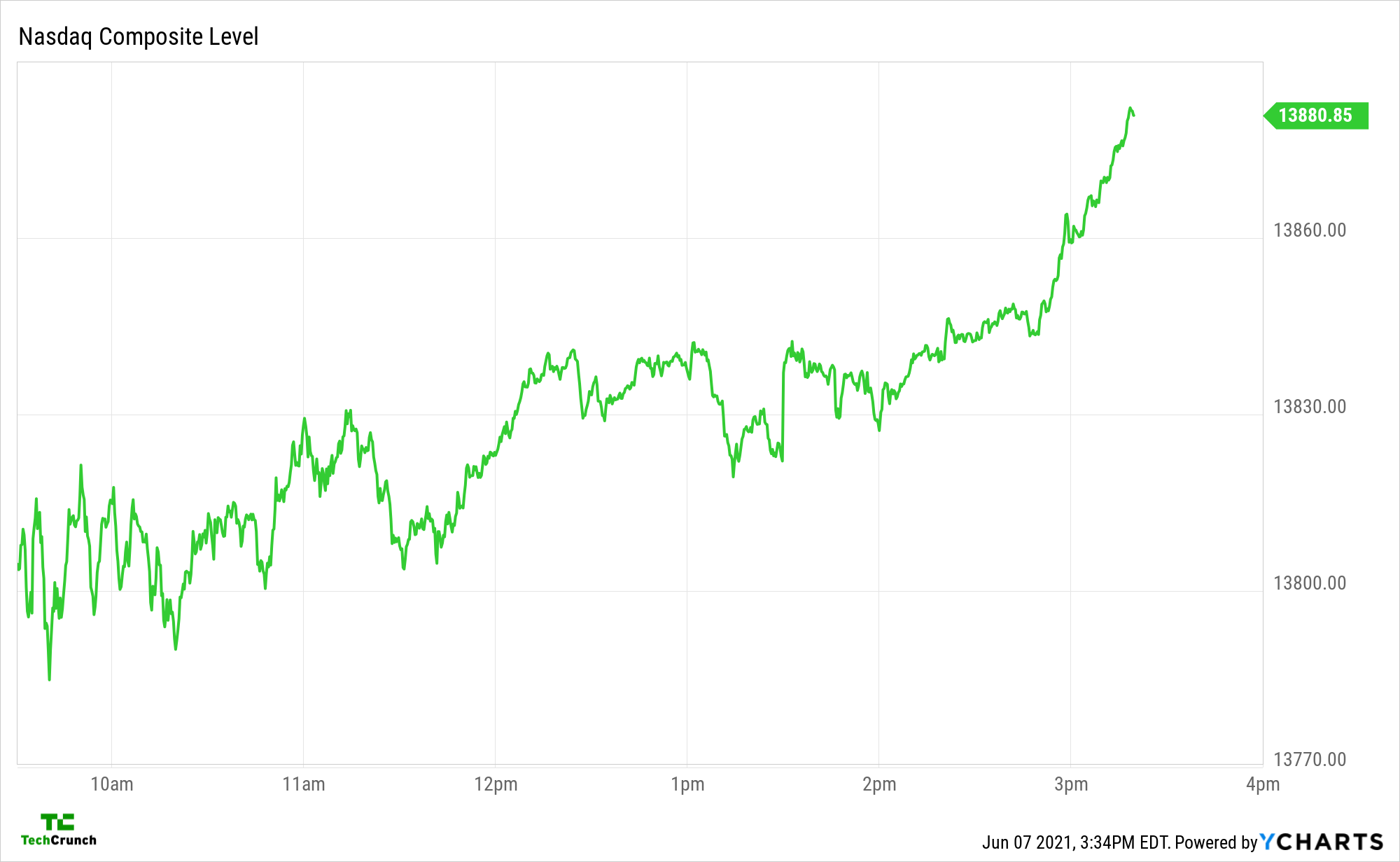

And here’s the Nasdaq:

Presuming that you are not a ChartMaster , those might not mean much to you. Don’t worry. The charts say very little all-around so you are missing little. Apple was down a bit, and the Nasdaq up a bit. Then the Nasdaq went up more, and Apple’s stock generally followed. Which is good to be clear, but somewhat immaterial.

, those might not mean much to you. Don’t worry. The charts say very little all-around so you are missing little. Apple was down a bit, and the Nasdaq up a bit. Then the Nasdaq went up more, and Apple’s stock generally followed. Which is good to be clear, but somewhat immaterial.

So after yet another major Apple event that will help determine the health and popularity of every Apple platform — key drivers of lucrative hardware sales! — the markets are betting that all their prior work estimating the True and Correct value of Apple was dead-on and that there is no need for any sort of up-or-down change.

That, or Apple is so big now that investors are simply betting it will grow in keeping with GDP. Which would be a funny diss. Regardless, more from the Apple event here in case you are behind.

Powered by WPeMatico

This morning the tech-heavy Nasdaq Composite index is off 2.34% after falling yesterday. Shares of Tesla are off more than 6% today, now mired in a bear-market correction after reaching new all-time highs earlier this year. Apple stock is worth $122.02 per share, down from its recent highs of more than $145.

After a long period of time when it felt like tech stocks only went up, the recent correction is starting to feel material.

There are other ways to measure the selloff. Bessemer’s cloud index is off 4.5% today, after falling over 5% yesterday. And the now-infamous $ARKK, or ARK Innovation ETF that many investors have used as a proxy for growthy tech stocks, is off 6.6% today after falling 5.9% yesterday.

Hell, even bitcoin has taken a pounding in the last few days, after its recent, relentless rise.

What’s driving the rapid turnaround in the value of tech companies, tech-focused indices and tech-adjacents, like cryptocurrencies? Not merely one thing, of course, in an environment as complex as the world’s capital markets. But there is a rising narrative that you should consider.

Namely that the money-is-cheap-and-bond-yield-is-garbage-so-everyone-is-putting-money-into-stocks trade is losing steam. As some yields rise, bonds are become more attractive bets. And as COVID-19 vaccines roll out, some investors are pushing their stock-market bets into categories other than tech.

The result is that the landscape of value is shifting; the winds that were at the back of every tech company are receding, at least for now. If the changed weather persists until the very investment climate that tech stocks exist in reaches a new equilibrium, we could see the appetite for tech IPOs lessen, late-stage private valuations for startup shares dip, and more.

Here’s CNBC from earlier today on what’s changing:

Stocks dropped again on Tuesday as tech shares continued to tumble in the face of higher interest rates and a rotation into stocks more linked to the economic comeback.

Here’s The Wall Street Journal on the same theme, from yesterday:

The lift in yields largely reflects investor expectations of a strong economic recovery. However, the collateral damage could include higher borrowing costs for businesses, more options for investors who had seen few alternatives to stocks and less favorable valuation models for some hot technology shares, investors and analysts said.

And here’s Barrons from this morning, noting that what we’re seeing at home is not merely a U.S. issue:

While members of the NYSE FANG+ index including Tesla, Facebook and Apple have dropped sharply as the yield on the 10-year Treasury has climbed, the sector also is on the retreat overseas.

Powered by WPeMatico

Back in 2017, a formerly hot, formerly profitable company called Blue Apron went public. It didn’t go well. Today as the global stock market continues to fall, shares in the former venture darling are soaring, up more than 140% in midday trading.

Before its IPO, the company had to reduce its price range from $15 to $17 per share to $10 to $11 per share. That pricing change limited the company’s worth, and reduced the capital it raised in its debut. The meal kit delivery company finally priced at $10 per share. It opened up a hair, but closed the day a mere penny above its IPO price.

Then things got worse. In fact, Blue Apron’s share price decline got so bad that in mid-2019 Blue Apron had to execute a 1-for-15 reverse split. In most stock splits, a company’s share price gets too high for comfort. So, the firm decides to give its investors the same value of the company, but in new, smaller chunks. So a concern trading for $1,000 per share that wanted to split would normally give, say, its investors 10 new shares worth $100 apiece in exchange for their single $1,000 share.

A reverse split is the other way. You get fewer shares at a higher per-share value. It’s what you do if you need to avoid slipping under $1 per share, or other, similar fates.

Time passed, and everyone forgot about Blue Apron in the same manner as they did Grubhub, companies that came, made an impact, went public and then slowly dissolved.

Until now. Suddenly Blue Apron is the hottest stock in the world, skyrocketing as other companies shed value. Today in regular trading, American indices fell so far that they triggered protective circuit breakers. At the same time, Blue Apron was doing this (via Google Finance):

Bear in mind that we are looking at the company after its reverse split. So, no, the company is not worth 60% more than its IPO price of $10 per share. It’s worth far less. Indeed, Blue Apron is worth just $211 million today including its day’s gains, according to Google Finance.

Blue Apron was worth about $1.9 billion when it went public, for reference.

Anyway, why is the company skyrocketing? TechCrunch thinks it figured it out. Walk with us:

Don’t pop the champagne. Blue Apron is still worth about what it raised as a private company; its market cap is only about 40% of the money it raised while private in addition to its IPO haul. This company is still priced like it’s on life support.

And that makes some sense. Here are some facts from its Q4 and full-year 2019 report:

Not great! Perhaps Blue Apron will explode, beating guidance and earning its newly resurrected share price. Maybe. But before you pile into the company, pause, and then probably don’t.

Powered by WPeMatico