loans

Auto Added by WPeMatico

Auto Added by WPeMatico

Mortgages may not be considered sexy, but they are a big business.

If you’ve refinanced or purchased a home digitally lately, you may not have noticed the company powering the software behind it — but there’s a good chance that company is Blend.

Founded in 2012, the startup has steadily grown to be a leader in the mortgage tech industry. Blend’s white label technology powers mortgage applications on the site of banks including Wells Fargo and U.S. Bank, for example, with the goal of making the process faster, simpler and more transparent.

The San Francisco-based startup’s SaaS (software-as-a-service) platform currently processes over $5 billion in mortgages and consumer loans per day, up from nearly $3 billion last July.

Today, Blend made its debut as a publicly traded company on the New York Stock Exchange, trading under the symbol “BLND.” As of early afternoon, Eastern Time, the stock was trading up over 13% at $20.36.

On Thursday night, the company had said it would offer 20 million shares at a price of $18 per share, indicating the company was targeting a valuation of $3.6 billion.

That compares to a $3.3 billion valuation at the time of its last raise in January — a $300 million Series G funding round that included participation from Coatue and Tiger Global Management. Also, let’s not forget that Blend only became a unicorn last August when it raised a $75 million Series F. Over its lifetime, Blend had raised $665 million before Friday’s public market debut.

In filing its S-1 on June 21, Blend revealed that its revenue had climbed to $96 million in 2020 from $50.7 million in 2019. Meanwhile, its net loss narrowed from $81.5 million in 2019 to $74.6 million in 2020.

In 2020, the San Francisco-based startup significantly expanded its digital consumer lending platform. With that expansion, Blend began offering its lender customers new configuration capabilities so that they could launch any consumer banking product “in days rather than months.”

Looking ahead, the company had said it expects its revenue growth rate “to decline in future periods.” It also doesn’t envision achieving profitability anytime soon as it continues to focus on growth. Blend also revealed that in 2020, its top five customers accounted for 34% of its revenue.

Today, TechCrunch spoke with co-founder and CEO Nima Ghamsari about the company’s decision to go with a traditional IPO versus the ubiquitous SPAC or even a direct listing.

For one, Blend said he wanted to show its customers that it is an “around for a long time company” by making sure there’s enough on its balance sheet to continue to grow.

“We had to talk and convince some of the biggest investors in the world to invest in us, and that speaks to how long we’ll be around to serve these customers,” he said. “So it was a combination of our capital need and wanting to cement ourselves as a really credible software provider to one of the most regulated industries.”

Ghamsari emphasized that Blend is a software company that powers the mortgage process and is not the one offering the mortgages. As such, it works with the flock of fintechs that are working to provide mortgages.

“A lot of them are using Blend under the hood, as the infrastructure layer,” he said.

Overall, Ghamsari believes this is just the beginning for Blend.

“One of the things about financial services is that it’s still mostly powered by paper. So a lot of Blend’s growth is just going deeper into this process that we got started in years ago,” he said. As mentioned above, the company started out with its mortgage product but just keeps adding to it. Today, it also powers other loans such as auto, personal and home equity.

“A lot of our growth is actually powered by our other lines of business,” Ghamsari told TechCrunch. “There’s a lot to build because the larger digitization trends are just getting started in financial services. It’s a relatively large industry that has lots of change.”

In May, digital mortgage lender Better.com announced it would combine with a SPAC, taking itself public in the second half of 2021.

Powered by WPeMatico

FinanZero, a Brazilian online credit marketplace, announced today that it has closed a $7 million round of funding — its fourth since it launched in 2016. It has raised a total of $22.85 million to date.

The real-time online loan broker allows people to apply for a personal loan, a car equity loan or a home equity loan for free and receive an answer in minutes. A key to FinanZero’s success is that it doesn’t offer the loans itself, but has instead partnered with about 51 banks and fintechs who back the loans.

FinanZero is based in Brazil’s financial capital, São Paulo, and has 52 employees.

“From day one we said, ‘We only work with a success fee,’ so we only get paid when the customer signs the loan contract,” said Olle Widen, the company’s co-founder and CEO.

Instead of charging the customer, FinanZero gets a commission from one of its partners, and with a growing volume of credit applications — an average of 750,000 applications per month — the company has seen 61% revenue growth from 2019-2020.

Olle Widen, co-founder and CEO of FinanZero. Image Credits: FinanZero

The Brazilian finance and banking market has been ripe for disruption, as it has traditionally favored the rich.

Those with low incomes — the vast majority of Brazilian citizens — are then left with few options when it comes to financing, and which in turn forces them into compounding debt from which they’ll likely never escape. Traditionally, young Brazilians have lived with their families until they got married, and while there is a cultural aspect to it, the bottom line is that mortgages were infinitely hard to get approved.

With products like FinanZero and Nubank — Latin America’s largest digital bank — Brazilians are starting to see more economic mobility and independence from the legacy institutions that dictated their lives for so long.

Widen, who is Swedish, moved to Brazil about 10 years ago for personal reasons, and while there, was pitched the idea of FinanZero by Webrock Ventures, an investment company focused on bringing Nordic innovation to Brazil.

At the time, Swedish startup Lendo — a precursor to FinanZero — was making waves in Sweden, and the team felt that a similar model would succeed in Brazil, a country known for its bureaucracy and red tape, and thus primed for a streamlined and hassle-free approach to loans.

The original idea was to just copy Lendo, Widen said, but as others have discovered, along the way the team needed to “tropicalize” the product and the experience, meaning they had to build a custom solution for the Brazilian market and its people.

“The founder of Lendo was a childhood friend of mine,” said Widen, of his close ties to the Swedish fintech.

To apply for a loan on FinanZero you don’t need to provide your credit score. Instead, all you need is a utility bill (proof of address), proof of income and your government ID. The process is so simple, Widen said, that 92% of loan applications are initiated from a smartphone.

“Our business model is very based on the bank’s risk appetite and we saw 60% growth from 2019-2020. We are close to 3 million visits per month, about 1.5 are unique and in March of 2021, we had 800,000 people fill out the entire loan form. We have about a 10% approval rating across all products,” Widen said.

The round was led by the Swedish investors VEF, Dunross & Co, and Atlant Fonder, which are all previous investors in the company. The funding will go toward marketing — most of which will be on T.V. — product development, and talent acquisition.

Powered by WPeMatico

As a small business owner, I was excited to learn about the $2.2 trillion Coronavirus Aid, Relief, and Economic Security Act that offers low-interest loans to firms impacted by the COVID-19 pandemic. However, as I read through the details and began to apply, it became clear that this legislation — while well-intentioned — may not be enough to help many SMBs and startups.

Here’s a quick recap of my experience.

First and foremost: You need to act swiftly. Emergency Economic Injury Grant and Economic Injury Disaster Loan programs included in the CARES Act function on a first-come, first-served basis, and are funded from a limited pool of resources.

I began my company’s application process by submitting our EIDL and EEIG applications through the SBA website. This was easy, if tedious. It took about two hours to complete the necessary online forms and about two seconds to click the EEIG checkbox. Submission was seamless, but I haven’t received any further communication from the SBA since completing my application, which is a bit confusing — EEIG funds are supposed to be dispersed within 3-5 days of the submission date.

However, I know there’s been a huge volume of submissions recently and this must be exceptionally difficult to handle. I look forward to any email correspondence or updates from the SBA that might give me — and other applicants — an updated estimate of the expected dispersal timeline.

Powered by WPeMatico

Another tech unicorn is feeling the pinch of doing business during the coronavirus pandemic. Today, Kabbage, the SoftBank-backed lending startup that uses machine learning to evaluate loan applications for small and medium businesses, is furloughing a “significant number” of its U.S. team of 500 employees, according to a memo sent to staff and seen by TechCrunch, in the wake of drastically changed business conditions for the company. It is also completely closing down its office in Bangalore, India, and executive staff is taking a “considerable” pay cut.

The announcement is effective immediately and was made to staff earlier today by way of a video conference call, as the whole company is currently remote working in the current conditions.

Kabbage is not disclosing the full number of staff that are being affected by the news (if you know, you can contact us anonymously). It’s also not putting a time frame on how long the furlough will last, but it’s going to continue providing benefits to affected employees. The intention is to bring them back on when things shift again.

“We realize this is a shock to everyone. No business in the world could have prepared for what has transpired these past few weeks and everyone has been impacted,” co-founder and CEO Rob Frohwein wrote in the memo. “The economic fallout of this virus has rattled the small business community to which Kabbage is directly linked. It’s painful to say goodbye to our friends and colleagues in Bangalore and to furlough a number of U.S. team members. While the duration of the furlough remains uncertain, please bear in mind that the full intention of furloughing is temporary. We simply have no clear idea of how long quarantining or its reverberations in the economy will last.”

Kabbage’s predicament underscores the complicated and stressful calculus faced by tech companies built around providing services to SMBs, or fintech (or both, as in the case of Kabbage).

SMBs are struggling right now in the U.S.: many operate on very short terms when it comes to finances, and closing their businesses (or seeing a drastic reduction in custom) means they will not have the cash to last 10 days without revenue, “and we’re already well past that window,” Frohwein noted in his memo.

In Kabbage’s case, that means not only are SMBs not able to be evaluated and approved for normal loans at the moment, but SMBs that already have loans out are likely facing delinquencies.

The decision to furlough is hard but in relative terms it’s good news: it was made at the eleventh hour after a period when Kabbage was considering layoffs instead.

The company has raised hundreds of millions of dollars in equity and debt, and it was in a healthy state before the coronavirus outbreak. The memo notes that the “board and our top investors are aware of the challenges we are facing and have committed to helping us through this period,” although it doesn’t specify what that means in terms of financial support for the business, and whether that support would have been there for the business as-is.

The shift to furlough from layoffs came in the wake of an announcement yesterday by Steven Mnuchin, the U.S. Secretary of the Treasury, who clarified that “any FDIC bank, any credit union, any fintech lender will be authorized” to make loans to small businesses as a part of the U.S. government’s CARE Act, the giant stimulus package that included nearly $350 billion in loan guarantees for small businesses.

While that provides much-needed relief for these businesses, the implementation of it — the Small Business Administration has already received nearly 1 million claims for disaster-relief loans since the crisis started — has been and is going to be a challenge.

That effectively opens up an opportunity for Kabbage and companies like it to revive and reorient some of its business. (Its USP was always that the AI it uses, which draws on a number of different sources of online data for the business, means a more creative, faster and more accurate assessment of loan applications than what traditional banks typically provide.) Kabbage said it is in “deep discussions” with the Treasury Department, the White House and the Small Business Administration to help expedite applications for aid.

While loans still make up the majority of Kabbage’s business, the company has been making a move to diversify its services, and in recent times it has made acquisitions and launched new services around market intelligence insights and payments services. While there has certainly been a jump in e-commerce, overall the tightening economy will have a chilling effect on the wider market, and it will be worth seeing what happens with other tech companies that focus on loans, as well as adjacent financial services.

Powered by WPeMatico

I work every day with company founders who are grappling with the challenges of driving business growth while keeping their finances on an even keel. One topic we often discuss is how to take advantage of debt to drive business growth — without it turning into a problem.

In my experience, debt can serve as a valuable piece of a company’s capital structure. The key is to use debt for the right purposes and to understand the implications of doing so. For example, short-term loans (one to two-year terms) are useful for financing receivables and inventory to help manage cash flow. These working capital facilities have attractive interest rates (often in the 5% range) and are well understood by the lending community.

By contrast, mezzanine loans (usually three to five-year terms) are better suited to provide the flexibility and runway needed to prove out certain initiatives prior to securing an equity investment or a liquidity event. These loans tend to have limited covenants, are not secured by specific working capital assets and are junior to the working capital loans. Given their higher-risk profile, they are more expensive than short-term loans, with lenders typically targeting a return of 15% to 20%, split between a current pay interest rate of 10%+ and expected stock appreciation from the receipt of warrant coverage.

Regardless of the type of debt a company takes on, there are certain principles to consider to keep the debt from threatening the success of the business. Should you decide to take on debt, understand the implications and consider the following five rules:

Powered by WPeMatico

Kabbage, the AI-based small business loans platform backed by SoftBank and others, is adding more firepower to its lending machine: the Atlanta-based startup has secured an additional $200 million in the form of a revolving credit facility from an unnamed subsidiary of a large life insurance company, managed and administered by 20 Gates Management, and Atalaya Capital Management.

The money comes on the heels of a $700 million securitization Kabbage secured just three months ago and it is notable not just for its size but its terms: it’s a four-year facility, a length of time that underscores a level of confidence in the company’s performance.

Kabbage, which loans up to $250,000 in a single deal to small and medium businesses, has built a platform that harnesses the long tail of big data from across the web. It uses not just indicators from a company’s own public activities, but also sources comparative information from across a wider group of similar companies, with “2 million live data connections” currently helping to feed its algorithm.

Together, these help Kabbage determine whether to provide the loans, and at what rates. Notably, the whole process takes mere minutes, making Kabbage disruptive to the traditional route of applying for loans from banks, which can come at higher rates, often take longer to close and may never get approved.

The company was last valued at $1.2 billion in its most recent equity round from the Vision Fund in 2017, with about $500 million raised in equity to date from it and other investors, including BlueRun Ventures and Mohr Davidow Ventures. Rob Frohwein, the co-founder and CEO, confirmed to me via email that there are “no plans on the equity side right now.” We’ve asked about IPO plans and will update if we learn anything more on that front.

More importantly, alongside its equity story is the company’s business story: Kabbage has to date loaned out $7 billion in capital — amassed through securitizations and other facilities alongside that — to 185,000 businesses, and the company has seen an acceleration of business activity over the last two years. Nearly $700 million was loaned out in Q2 of this year, passing the record in Q1 of $600 million. This puts Kabbage on track to loan out between $2.4 billion and $3 billion this year.

“This transaction further diversifies Kabbage’s committed sources of funding and prepares us to meet the escalating demand for capital access among small businesses,” said Kabbage head of Capital Markets, Deepesh Jain, in a statement. “2019 has proven to be a tide-shifting year as customers accessed more than $670 million from Kabbage in Q2 2019, well surpassing our previously set record last quarter.”

While a lot of Kabbage’s business has come out of its direct consumer relationships, it’s also been expanding by way of more third-party relationships. It has white-label partnerships with banks to power their own loan offerings for SMBs, and earlier this year it was also tapped by e-commerce giant Alibaba to provide loans to its small business customers of up to $150,000 to help finance purchases, part of the latter company’s redoubled efforts to build out its business in the U.S. by way of its quiet acquisition of OpenSky.

Powered by WPeMatico

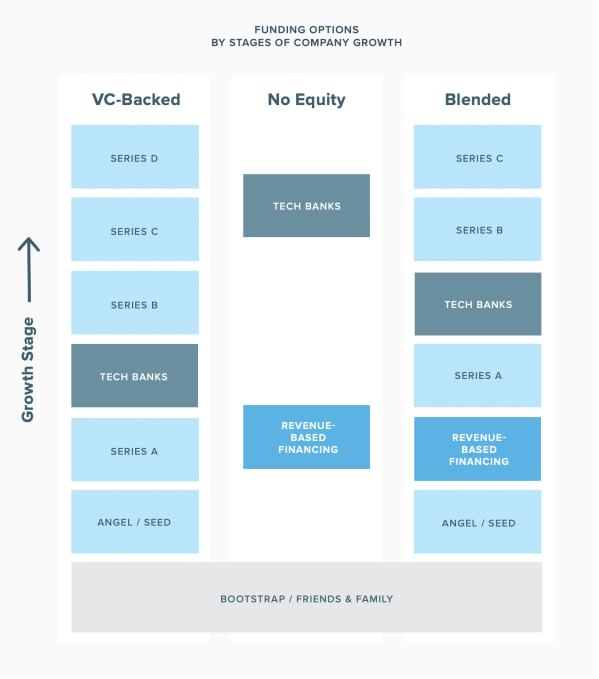

Revenue-based financing is on the rise, at least according to Lighter Capital, a firm that doles out entrepreneur-friendly debt capital.

What exactly is RBF you ask? It’s a relatively new form of funding for tech companies that are posting monthly recurring revenue. Here’s how Lighter Capital, which completed 500 RBF deals in 2018, explains it: “It’s an alternative funding model that mixes some aspects of debt and equity. Most RBF is technically structured as a loan. However, RBF investors’ returns are tied directly to the startup’s performance, which is more like equity.”

Source: Lighter Capital

What’s the appeal? As I said, RBFs are essentially dressed up debt rounds. Founders who opt for RBFs as opposed to venture capital deals hold on to all their equity and they don’t get stuck on the VC hamster wheel, the process in which you are forced to continually accept VC while losing more and more equity as a means of pleasing your investors.

RBFs, however, are better than traditional debt rounds because the investors are more incentivized to help the companies they invest in because they are receiving a certain portion of that business’s monthly revenues, typically 1% to 9%. Eventually, as is explained thoroughly in Lighter Capital’s newest RBF report, monthly payments come to an end, usually 1.3 to 2.5X the amount of the original financing, a multiple referred to as the “cap.” Three to five years down the line, any unpaid amount of said cap is due back to the investor. When all is said in done, ideally, the startup has grown with the support of the capital and hasn’t lost any equity.

At this point, they could opt to raise additional revenue-based capital, they could turn to venture capital or they could tap a tech bank to help them get to the next step. The idea is RBF is easier on the founder and it allows them optionality, something that is often lost when companies turn to VCs.

IPO corner, rapid-fire edition

Slack’s direct listing will be on June 20th. Get excited.

China’s Luckin Coffee raised $650 million in upsized U.S. IPO

Crowdstrike, a cybersecurity unicorn, dropped its S-1.

Freelance marketplace Fiverr has filed to go public on the NYSE.

Plus, I had a long and comprehensive conversation with Zoom CEO Eric Yuan this week about the company’s closely watched IPO. You can read the full transcript here.

Silicon Valley entrepreneur Hosain Rahman, the man behind Jawbone, has managed to raise $65.4 million for his new company, according to an SEC filing. The paperwork, coincidentally or otherwise, was processed while most of the world’s attention was focused on Uber’s IPO. Jawbone, if you remember, produced wireless speakers and Bluetooth earpieces, and went kaput in 2017 after burning up $1 billion in venture funding over the course of 10 years. Ouch.

On the heels of enterprise startup UiPath raising at a $7 billion valuation, the startup’s biggest investor is announcing a new fund to double down on making more investments in Europe. VC firm Accel has closed a $575 million fund — money that it plans to use to back startups in Europe and Israel, investing primarily at the Series A stage in a range of between $5 million and $15 million, reports TechCrunch’s Ingrid Lunden. Plus, take a closer look at Contrary Capital. Part accelerator, part VC fund, Contrary writes small checks to student entrepreneurs and recent college dropouts.

Our paying subscribers are in for a treat this week. Our in-house venture capital expert Danny Crichton wrote down some thoughts on Uber and Lyft’s investment bankers. Here’s a snippet: “Startup CEOs heading to the public markets have a love/hate relationship with their investment bankers. On one hand, they are helpful in introducing a company to a wide range of asset managers who will hopefully hold their company’s stock for the long term, reducing price volatility and by extension, employee churn. On the other hand, they are flagrantly expensive, costing millions of dollars in underwriting fees and related expenses…”

Read the full story here and sign up for Extra Crunch here.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about the notable venture rounds of the week, CrowdStrike’s IPO and more of this week’s headlines.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico

Capital Float, the fintech startup that says it is India’s largest online lender, announced today that it has raised $22 million in new funding from Amazon. At the end of last year, reports surfaced that Amazon was considering an investment in Capital Float as an extension of its $45 million Series C, which was announced last August. The Bangalore-based startup confirmed to TechCrunch that Amazon’s investment is indeed an extension of that round and brings the total equity it has raised over the past 12 months to $67 million.

Over the same period, Capital Float also raised $80 million of debt from banks and other financial companies, which it combines with its own balance sheet to finance loans to small businesses and other borrowers. Amazon India is among several e-commerce platforms that the company has partnered with to provide loans to sellers, including Snapdeal and Shopclues.

Since its inception in 2013 by co-founders Sashank Rishyasringa and Gaurav Hinduja, Capital Float has raised a total of about $110 million in equity funding from investors, including Ribbit Capital, SAIF Partners, Sequoia India, Creation Investments and Aspada, as well as total debt lines of $130 million.

During the last six months, Capital Float added 50,000 new customers, bringing its total customer base to more than 80,000 people in more than 300 cities. The startup says it currently disburses more than 10,000 loans each month and now has an outstanding loan portfolio of more than $170 million, with a default rate of about 2 percent. About 70 percent of its loans are microloans ranging from 25,000 rupees to 500,000 rupees (about $376 to $7,530).

With the investment from Amazon, the startup has set an ambitious goal of adding 300,000 new customers and originating more than $800 million in loans this year.

In a press statement, Amazon India’s country manager Amit Agarwal said, “We’re excited to work with Capital Float and invest alongside other investors. We are highly impressed with what Gaurav and Sashank have built and we back missionary entrepreneurs and management teams. Credit in India is highly under-penetrated and Capital Float is bringing the right kind of credit solutions to the underserved and informally served segments of SMEs to help realize their full potential.”

Over the last year, Capital Float expanded into more verticals, including products for small- to mid-sized manufacturers, point-of-sale financing for retailers and loans for school construction and self-employed professionals like doctors. It also added new online payment gateways to make it easier for borrowers to repay loans and began piloting deep learning-based underwriting models that use data points like image processing, geotags and new policies such as the Goods and Service Tax (GST), an indirect tax launched last year that is levied at every step of the production chain and the banknote demonetization started by Prime Minister Narendra Modi’s government in 2016.

Powered by WPeMatico

Kabbage, a company with some 115,000 customers and $3.5 billion in loans that has built an automated platform for lending money to small businesses and individuals using a large set of data points to determine a customer’s credit score, is announcing some big cabbage of its own today. SoftBank Group is investing $250 million in Kabbage — funding that Rob Frohwein, the co-founder… Read More

Kabbage, a company with some 115,000 customers and $3.5 billion in loans that has built an automated platform for lending money to small businesses and individuals using a large set of data points to determine a customer’s credit score, is announcing some big cabbage of its own today. SoftBank Group is investing $250 million in Kabbage — funding that Rob Frohwein, the co-founder… Read More

Powered by WPeMatico

In a rare move, Battery Ventures, Andreessen Horowitz and Ribbit Capital, investors in a number of Silicon Valley’s fintech startups, have backed the bank enabling many of their investments to lurch forward. Cross River Bank, the obscure financial institution that seemingly everyone in fintech has heard of but doesn’t really know, originated more than $2.4 billion in loans for… Read More

In a rare move, Battery Ventures, Andreessen Horowitz and Ribbit Capital, investors in a number of Silicon Valley’s fintech startups, have backed the bank enabling many of their investments to lurch forward. Cross River Bank, the obscure financial institution that seemingly everyone in fintech has heard of but doesn’t really know, originated more than $2.4 billion in loans for… Read More

Powered by WPeMatico