Livongo

Auto Added by WPeMatico

Auto Added by WPeMatico

Thirty Madison, the New York-based startup developing a range of direct to consumer treatments for hair loss, migraines and chronic indigestion, has raised $47 million in new financing.

After last week’s nearly $19 billion merger between Teladoc and Livongo, remote therapies and virtual care companies are all the rage among the healthcare industry, and Thirty Madison’s business is no exception.

An indicator of just how important these companies are to the future of the healthcare business can be seen in the presence of Johnson & Johnson Innovation – JJDC, Inc. (JJDC) in the latest round for Thirty Madison.

Existing investors Maveron and Northzone also returned to back the company in a deal led by Polaris Partners. Thirty Madison has raised a total of $70 million so far.

Founded just three years ago by Steven Gutentag and Demetri Karagas, Thirty Madison expanded from treating hair loss with its Keeps brand in 2018 to migraine treatments in early 2019 with Cove, and launched Evens (the company’s acid reflux treatment service) later that year.

Thirty Madison has just begun offering urgent care consultations for users on a pay-what-you-will model.

And the company’s founders differentiate Thirty Madison’s business from their better-funded competitors like Hims and Ro by emphasizing that their company provides continuing care after a diagnosis and offers a range of treatment options for the conditions that the company treats. That, coupled with the more narrow focus on a few specific conditions, distinguish Thirty Madison from its peers in the industry.

“Over 59% of Americans suffer from at least one chronic condition, but few resources exist to help them connect the dots of their care,” said Amy Schulman, a partner with Polaris Partners and new director on the Thirty Madison board.

Powered by WPeMatico

Telehealth, or remote, tech-enabled healthcare, has existed for years in primary medical care through companies like Teladoc (NYSE: TDOC), Doctors on Demand and MDLIVE.

In recent years, the application of telehealth had rapidly expanded to address specific chronic and behavioral health issues like mental health, weight loss and nutrition, addiction, diabetes and hypertension, etc. These are real and oftentimes very severe issues faced by people all over the world, yet until now have seen little to no use of technology in providing care.

We believe behavioral health is particularly suited to benefit from the digitization trends COVID-19 has accelerated. Previously, we’ve written about the pandemic’s impact on online learning and education, both for K-12 students and adult learners. But behavioral health is another area impacted by the fundamental change in consumers’ behavior today. Below are four reasons we think the time is now for behavioral health startups — followed by five key factors we think characterize successful companies in this area.

Traditional behavioral healthcare is cost-prohibitive for most people. In-person therapy costs $100+ per session in the U.S., and many mental health and substance-use providers don’t accept insurance because they don’t get paid enough by insurers.

By contrast, telehealth reduces overhead costs and scales more effectively. Leveraging technology, providers can treat more patients in less time with almost zero marginal costs. Mobile-based communications enable asynchronous care that further helps providers scale. Access to digital content gives patients on-going support without the need for a human on the other side. This is particularly useful in treating behavioral health issues where ongoing support and motivation may be necessary.

Globally, we face an extreme shortage of behavioral health providers. For example, the United States has fewer than 30,000 licensed psychiatrists (translating to <1 for every 10,000 people). Outside of big cities, the problem gets worse: ~50-60% of nonmetro counties have no psychologists or psychiatrists at all.

Even when providers are available, wait times for appointments are notoriously long. This is a huge issue when behavioral health conditions often require timely intervention.

We are seeing new platforms build large networks of certified coaches, licensed psychologists and psychiatrists, and other providers, aggregating supply in what has historically been a scarce and a highly fragmented provider population.

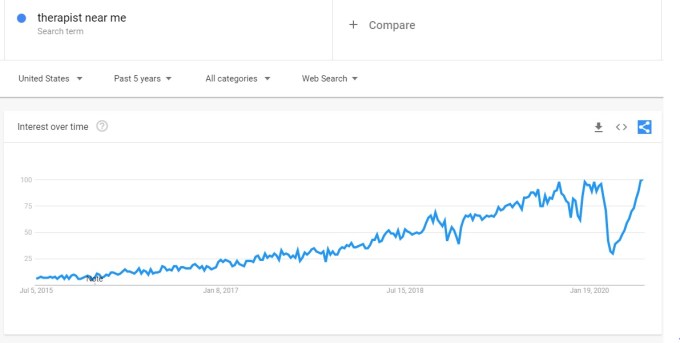

We believe the stigma associated with mental illness and other behavioral health conditions is dissipating. More and more public figures are speaking out about their struggle with anxiety, depression, addiction and other behavioral health issues. Our zeitgeist is shifting fast, and there’s an all-time high in people seeking help as the Google Trends data below demonstrates.

Image Credits: Google

Note: The anomalous dip in March/April ’20 was driven by mandatory shelter-in-place due to COVID-19.

Powered by WPeMatico

“Our real focus is on democratizing mental healthcare,” says SonderMind co-founder chief executive, Mark Frank.

His company, founded back in 2017, is having a moment. With the restrictions and economic stresses caused by the government’s efforts to mitigate the spread of the COVID-19 epidemic in the U.S., demand for mental health services is soaring. And it’s compounding what was already a mental health crisis in the U.S.

A 2019 article from Bloomberg Businessweek laid out the scope of the problem in stark terms. In 2017, 47,000 people died by suicide in the U.S. and there were 1.4 million suicide attempts — a suicide rate that’s the country’s highest since World War II, according to the Centers for Disease Control and Prevention. Drug overdoses, another measure of the nation’s anguish, killed 70,000 people in 2017. Another 7% of U.S. adults reported suffering at least one major depressive episode in 2018.

Taken together, the data points to a tremendous health problem. One that the current healthcare system is only now grappling with.

SonderMind’s chief executive sees his company as part of the solution.

Most mental health practitioners don’t operate within a healthcare network or take insurance, which means that the only folks with access to care are the ones that can afford the high price of therapy. SonderMind changes that equation by offering practitioners a toolkit and back office services so they can bill insurance providers and take care of the operational side of running a healthcare practice. It also acts as a funnel, gauging the needs of potential patients and connecting them to the therapists that are best suited to provide them the care they need. That lets practitioners focus on seeing patients, the company said.

The company currently counts 500 providers on its marketplace, which operates in Colorado, Arizona and Texas, and has raised $27 million in its latest round of financing to extend its services to other parts of the U.S.

The San Francisco-based investment firm General Catalyst led the financing, which also included additional new investors F-Prime Capital and participation from previous investors like the Kickstart Seed Fund, Diōko Ventures (managed by FCA Venture Partners) and Jonathan Bush.

“This financing provides the fuel to support our growth objectives and advance our mission to make behavioral health more accessible, approachable and utilized by building a modern marketplace that holds great appeal to both clinician and patient,” said Frank in a statement.

The investment extends General Catalyst’s funding into healthcare services in recent years and represents a continued emphasis on healthcare services for the firm. “Healthcare is obviously a really important thesis for GC as a whole,” says Holly Maloney, a managing director at General Catalyst. “This is going to be one of the largest value drivers for VC this decade.”

General Catalyst already had a robust portfolio of healthcare-focused companies — including Livongo, OM1 and Oscar Health.

For Maloney, the investment in SonderMind grew out of the firm’s exposure to mental health investment through another portfolio company, Mindstrong Health. “Mindstrong forced us to explore… access to care and finding care,” says Maloney.

The General Catalyst investor sees the investment in SonderMind as also helping to open doors for more people to join the profession.

“It helps people to start their business for sure. It helps more people pursue it as a career path,” she said. And that’s good for a country where more mental health professionals and better access to care are desperately needed.

Powered by WPeMatico

The world of healthcare has notoriously been described as “broken” — plagued with high-friction workflows, sky-high costs and convoluted business models.

Over the past several years, a long list of innovative startups and salivating venture investors have pinned their focus on repairing the healthcare industry, but its digital transformation still appears to be in the very early innings. After a record-setting 2018, however, digital health investing continued to reach meteoric heights in 2019.

Mammoth pools of capital have flooded into various sub-verticals and business models, backing collections of new B2B and B2C companies focused on optimizing healthcare workflows, improving healthcare access and offering lower-cost distribution models. Over the past two years, digital health startups have raised well over $10 billion in funding across nearly 1,000 deals, according to data from Pitchbook and Crunchbase.

As we close out another strong year for innovation and venture investing in the sector, we asked nine leading VCs who work at firms spanning early to growth stages to share what’s exciting them most and where they see opportunity in the sector:

Participants discuss trends in digital therapeutics, telehealth, mental health and the latest in biotech and medical devices, while also diving into startups improving medical practitioner efficiency, evaluating the evolving regulatory environment and debating valuations and offering a ‘temp check’ on the market for digital health startups leveraging ML.

Although Kleiner Perkins has a long history of investing in iconic health companies, we believe it is still the early innings of digital health as a category today.

When I evaluate new opportunities in the space, I often start by thinking through how the company will move the needle on cost, quality, and access to care — the “iron triangle” of health care systems. Conventional wisdom has been that it’s impossible to improve all three dimensions simultaneously, but we are seeing companies leverage technology to shift this paradigm in meaningful ways.

It’s no longer just a promise. For example, Viz.ai is using artificial intelligence to detect and alert stroke teams to suspected large vessel occlusion strokes, enabling patients to get treatment faster. Their workflows improve access to life-saving care, deliver higher quality through reduced time to treatment (every minute counts as ‘time is brain’ in stroke care), and dramatically reduce the costs associated with long-term disability.

We are also seeing companies provide this type of tech-enabled care outside of the hospital setting. Modern Health is a mental health benefits platform that employers are making available to their employees. The platform triages individual employees to the right level of care, providing clinical care to those with diagnosable depression or anxiety, and making self-guided or preventative care available to everyone else. Their solution improves quality and access by offering mental health services to every employee and reduces the cost associated with untreated mental illness, lost productivity, or employee churn.

Heading into 2020, we’re eager to back digital health companies in new areas that leverage technology to impact cost, quality, and access. A few spaces that I’m excited about are behavioral health (mental health, substance abuse, addiction, etc), care navigation, digital therapeutics, and new models integrating telehealth, remote care and AI to better leverage medical professionals’ time.

Below are some thoughts and coming predictions on health tech broadly:

- Digital therapeutics continue to pick up steam — on the back of Pear and Akili, more companies push to FDA and enter the market. In addition, broader consumer platforms like Calm and Headspace look to broaden their offerings by investigating clinical approvals.

- At least one major pharma looks to expand its consumer surface area by acquiring one of the new digital, consumer-facing generics platform (ex Hims, Ro, NuRx).

- Venture funding for biotech continues to boom with at least three Series A’s of $100M or more in size.

- Drug discovery for neurodegeneration sees a renaissance. High-profile failings of Biogen and the beta-amyloid hypothesis sees a shift of innovation to early-stage biotech and venture creation.

- Big pharma has its DeepMind moment acquiring at least one machine-learning (AI) enabled drug discovery company.

- Clinical trial tech investments heat up; new companies and technologies emerge to make trials patients first and systems get smarter at finding the right patients at their point of care; large incumbents like IQVIA, LabCorp and PPD get acquisitive.

- At least three traditional Sand Hill Road tech venture firms open life science practices or raise dedicated funds.

- Machine learning targets chemistry driven by large advancements in transformer (NLP) models; has the time for computational chemistry finally come?

- HCIT sees a renaissance driven by increased CIO responsibility towards data interoperability. Companies either working on federated ML to allow systems to speak to each other or lightweight edge applications enabling rapid clinical deployment will see quick uptake and traction, until now impossible in HC.

Kristin Baker Spohn, CRV

In the last 10 years, digital health has exploded. Over $16B has been invested in the sector by VCs and we’ve seen IPOs from Livongo, Progyny and Health Catalyst, just in the last year alone. That said, there’s still a lot that mystifies people about the sector — there are spots that are overheated and models that will struggle to deliver venture scale outcomes. I’ve seen digital health evolve first hand as both an operator and investor, and I’m more excited than ever about the future of the space.

A few areas and trends that I’ve been following recently include:

Powered by WPeMatico

Glen Tullman doesn’t like it when someone tells him he’s sick when he’s feeling fine. It’s something he thinks his customers probably don’t want to hear, either. Tullman runs a startup called Livongo Health, which offers a blood glucose monitor accompanied with a service designed to intervene and help coach people through managing diabetes. Livongo Health helps… Read More

Glen Tullman doesn’t like it when someone tells him he’s sick when he’s feeling fine. It’s something he thinks his customers probably don’t want to hear, either. Tullman runs a startup called Livongo Health, which offers a blood glucose monitor accompanied with a service designed to intervene and help coach people through managing diabetes. Livongo Health helps… Read More

Powered by WPeMatico