liquidity

Auto Added by WPeMatico

Auto Added by WPeMatico

As startups have stayed private longer and liquidity has become harder to secure for early employees and investors, more and more shareholders have looked for ways to unload their shares to others. All the way back in 2011, companies like SecondMarket were seeing nine-figures’ worth of shares being traded on their secondary share platforms.

That wave of liquidity startups ran into two problems: One was regulatory, and the other was a lack of company information about cap tables and that company’s current financial picture. Stock buyers were essentially flying blind while buying into companies, which some investors were more than willing to do, but that blindness limited the market demand for secondary shares significantly.

Carta is hoping that its base as the cap table management solution of choice for many startups will allow it to parlay that position into a new service it has called CartaX. We’ve heard rumblings about the service for more than a year now, but according to a new blog post by founder Henry Ward, it looks like the product is exiting beta and starting to operate in the real world with real money.

Yesterday, Carta sold just shy of $100 million of its shares across 1,484 market orders to 414 participants through its own CartaX product at a price of $6.9 billion. Ward says that is up from the $3.1 billion valuation of the company’s Series F round from last year.

As a comparison, secondary transactions typically involve secondary buyers who negotiate these deals manually one-on-one with individual sellers. What makes CartaX interesting is that it could allow for much faster and more frequent secondary sales at companies based on the same sort of computerized trading models that currently power the stock market.

Liquidity is a huge issue for startups, and while CartaX is just getting going, it fulfills a key need for many participants in the startup ecosystem, and it’s a key financial product to watch as it expands in 2021.

Meanwhile, revenues are looking good at Carta these days. According to an article earlier today by Zoë Bernard and Cory Weinberg at The Information, Carta has an ARR of $150 million. That’s a 46x revenue multiple if all the numbers are correct, which these days is good if not great for SaaS companies approaching the public markets.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

As investors struggle to price the stock market as economic and political news continues to break, the private market is entering a rough period. It seems increasingly likely that the period of disruption due to COVID-19 will persist for months, if not quarters. That means missed Q1 and Q2 revenue growth, bookings, and the like from startups domestically and around the world.

And that’s the bullish case. For some cohorts of startups, the outlook is even worse. Think about travel startups, ride-hailing upstarts, and any grouping of private companies that pursued a high-burn, high-growth model; that final category is about to run into the twin issues of the inflexibility of cost structure and the impact of slowing sales. That alone would make fundraising more difficult; toss in a deflating stock market and possible recession, and the mixture is a downright mess.

But we owe it to ourselves to survey what is going on in an attempt to answer our own questions about IPOs, exits, unicorn tallies, and who might be in trouble. Unlike when things were less bad, there will be no laughing this morning and no jokes. Just notes on what’s going wrong and what it might mean for private companies.

Powered by WPeMatico

The increase in activity in the pre-IPO secondary market means that founders, early employees, and investors are receiving liquidity much sooner in a company’s lifecycle than ever before. For most startups and privately-held companies, liquidity is often an issue for stockholders, as no market exists for selling shares and/or transfer restrictions can prevent their sale. Secondary stock transactions, however, are a way to work around this problem.

Here’s a quick look at how they work and what to keep in mind, especially if you’re going through the process for the first time. (If you’re not familiar, secondaries are transactions in which an existing stockholder sells their stock for cash to third parties or back to the company itself before the company undergoes an exit; traditionally, an exit refers to an M&A or an IPO.)

Offering secondary transactions to founders is a tool VCs have been using to win deals. For example, if a VC promises that the founders will receive $1,000,000 in cash through a secondary sale from a $15,000,000 venture financing round, the founders will likely prefer that VC’s term sheet to a term sheet from a VC that does not offer that deal.

Powered by WPeMatico

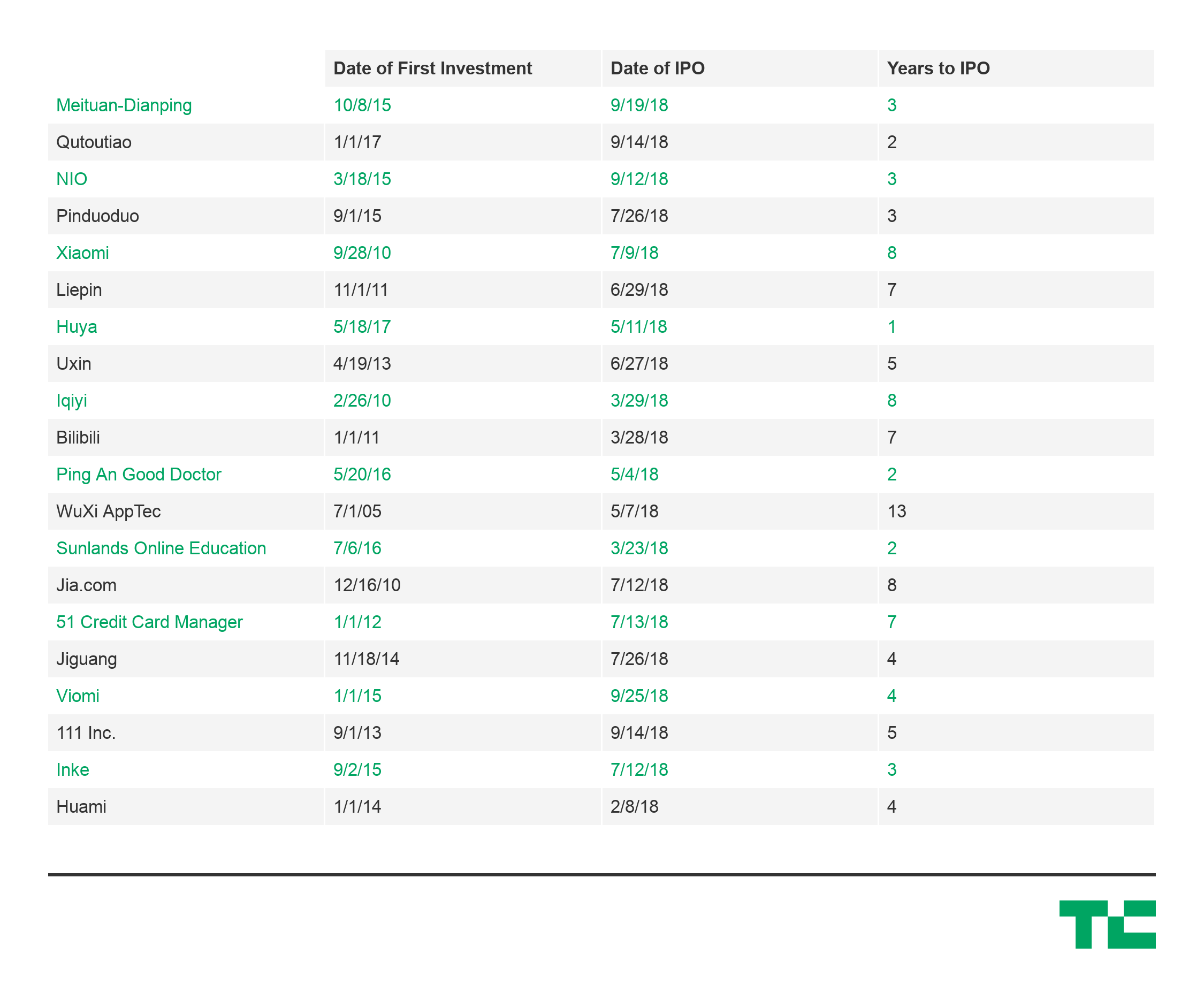

This year’s rush of IPOs from Chinese tech companies has dominated headlines, but what’s more interesting is how quickly they got there.

Traditionally, “going public” represented the gratifying culmination of sleepless nights and missed birthdays that went into building a company. The peak of a lengthy climb, where founders and VCs would finally see the fruits of their labor.

However, Chinese companies appear to be reaching that peak much quicker than their American peers, heading to the public markets only a few years after initial venture investments, and often with little operating history.

Analyzing twenty of the most high profile Chinese tech IPOs this year, the average time from first venture investment to IPO was only around three to five years. Take e-commerce platform Pinduoduo, which pulled in $1.6 billion less than three years after its Series A. Or the recent IPO of EV-manufacturer NIO, which raised a billion dollars just three-and-a-half years after its Series A and having just delivered its first car in June.

China IPO data for 2018 compiled from NASDAQ, Pitchbook, and Crunchbase

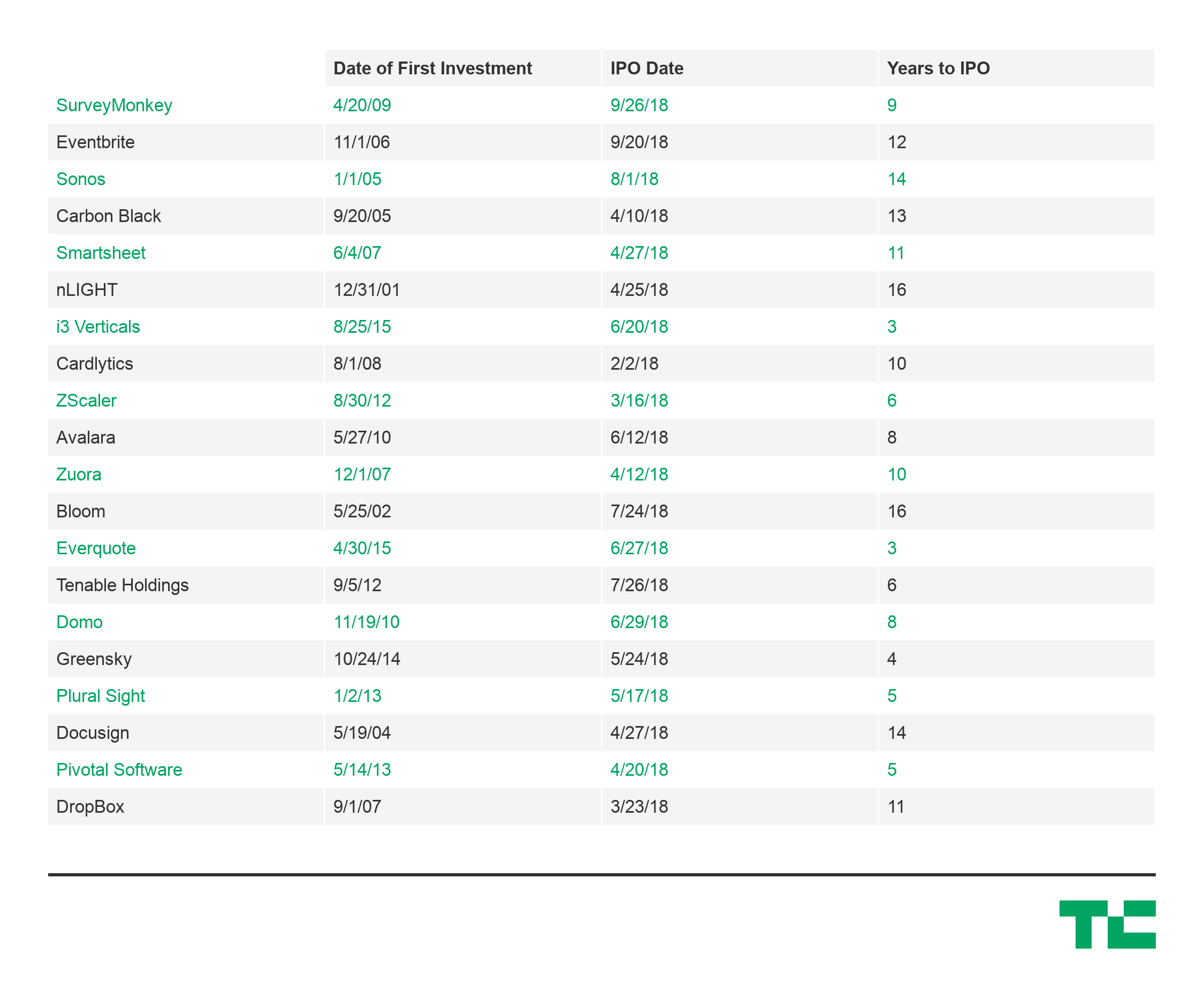

That’s less than half the average 10-year timeline for venture-backed US tech companies that went public in 2018, including Dropbox, Eventbrite, and DocuSign, which all IPO’d more than a decade after their initial investments.

Differences in market maturity, government involvement, and support from large tech incumbents all undoubtedly play a factor, but the speed to liquidity for the Chinese companies is still astounding.

Speed to liquidity is a critical metric for the health of a startup ecosystem. It creates a positive cycle where faster liquidity can drive faster fundraising, faster reinvestment, faster startup building, and faster public liquidity again. An accelerated cycle could be especially appealing for funds with LPs that require faster returns due to cash commitments or otherwise.

It’s important to note that venture returns are a function of capital and time, so quicker exits will also drive higher returns for the same amount invested. For example, a $1 million investment with a $5 million exit after ten years would generate an Internal Rate of Return (a commonly used metric to evaluate VC performance) of 20%. If the same exit occurred after five years, the IRR would be 50%.

Liquidity is a key consideration as China’s influence on the flow of global venture capital intensifies. As China’s tech ecosystem sees more of its darlings mature and more consistently deliver smashing exits, investments in China will have to be a more serious consideration for VCs, even if only to minimize the sheer amount of time, resources, and painstaking energy needed to build a company in the U.S.

Powered by WPeMatico

This year’s Disrupt NY Startup Battlefield was amazing. At the very beginning, there were 24 great companies presenting in front of multiple groups of industry leaders serving as judges. The startups were competing for $50,000 and the highly coveted Disrupt Cup. After hours of deliberations, TechCrunch editors pored over the judges’ notes and narrowed the list down to seven… Read More

This year’s Disrupt NY Startup Battlefield was amazing. At the very beginning, there were 24 great companies presenting in front of multiple groups of industry leaders serving as judges. The startups were competing for $50,000 and the highly coveted Disrupt Cup. After hours of deliberations, TechCrunch editors pored over the judges’ notes and narrowed the list down to seven… Read More

Powered by WPeMatico