life insurance

Auto Added by WPeMatico

Auto Added by WPeMatico

Marshmallow — a U.K.-based car insurance provider that has made a name for itself in the market by providing a new approach to car insurance aimed at using a wider set of data points and clever algorithms to net a more diverse set of customers and provide more competitive rates — is announcing a milestone today in its life as a startup, as well as in the bigger U.K. tech world.

The London company — co-founded by identical twins Oliver and Alexander Kent-Braham and David Goaté — has raised $85 million in a new round of funding. The Series B valuation is significant on two counts: it catapults Marshmallow to a “unicorn” valuation above $1 billion — specifically, $1.25 billion; and Marshmallow itself becomes one of a very small group of U.K. startups founded by Black people — Oliver and Alexander — to reach that figure.

(To be clear, Marshmallow describes itself as “the first UK unicorn to be founded by individuals that are Black or have Black heritage”, although I can think of at least one that preceded it: WorldRemit, which last month rebranded to Zepz, and is currently valued at $5 billion; co-founder and chairman Ismail Ahmed has been described as the most influential Black Briton.)

Regardless of whether Marshmallow is the first or one of the first, given the dearth of diversity in the U.K. technology industry, in particular in the upper ranks of it, it’s a notable detail worth pointing out, even as I hope that one day it will be less of a rarity.

Meanwhile, Marshmallow’s novel, big-data approach and successful traction in the market speak for themselves. When we covered the company’s most recent funding round before this — a $30 million raise in November 2020 — the startup was valued at $310 million. Now less than a year later, Marshmallow’s valuation has nearly quadrupled, and it has passed 100,000 policies sold in its home country, growing 100% over the last six months.

The plan now, Oliver told me in an interview, will be to deepen its relationships with customers, in part by providing more engagement to make them better drivers, but also potentially selling more services to them, too.

In this, the startup will be tapping into a new approach that other insurtech startups are taking as they rethink traditional insurance models, much like YuLife is positioning its life insurance products within a bigger wellness and personal improvement business. Currently, the average age of Marshmallow’s customers is 20 to 40, Oliver said — and there are thoughts of potentially new products aimed at even younger users. That means there is long-term value in improving loyalty and keeping those customers for many years to come.

Alongside that, Marshmallow will also use the funding to inch closer to its plan to expand to markets outside of the U.K. — a strategy that has been in the works for a while. Marshmallow talked up international expansion in its last round but has yet to announce which markets it will seek to tackle first.

Insurance — and in particular insurance startups — are often thought of together with fintech startups, not least because the two industries have a lot in common: they both operate in areas of assessing and mitigating risk and fraud; they are in many cases discretionary investments on the part of the customers; and they are both highly regulated and require watertight data protection for their users.

Perhaps because so much of the hard work is the same for both, it’s not uncommon to see services built to serve both sectors (FintechOS and Shift Technology being two examples), for fintech companies to dabble in insurance services, and so on.

But in reality, insurance — and specifically car insurance — has seen a massive impact from COVID-19 unique to that industry. Separate reports from EY and the Association of British Insurers noted that 2020 actually saw a lift for many car insurance companies: lockdowns meant that fewer people were driving, and therefore fewer were getting into accidents and making fewer claims.

2021, however, has been a different story: new pricing rules being put into place will likely see a number of providers tip into the red for the year. And the Chartered Insurance Institute points out that it will also be worth watching to see how the low use of cars in one year will impact use going forward: some car owners, especially in urban areas where keeping a car is expensive, will inevitably start to question whether they need to own and insure a car at all.

All of this, ironically, actually plays into the hand of a company like Marshmallow, which is providing a more flexible approach to customers who might otherwise be rejected by more traditional companies, or might be priced out of offerings from them. Interestingly, while neobanks have definitely spurred more traditional institutions to try to update their products to compete, the same hasn’t really happened in insurance — not yet, at least.

“We started with the idea of the power of data and using a wider range of resources [than incumbents], and using that in our pricing led us to be able to offer better rates to more people,” Oliver said, but that hasn’t led to Marshmallow seeing sharper competition from older incumbents. “They are big companies and stuck in their ways. These companies have been around for decades, some for centuries. Change is not happening quickly.”

That leaves a big opportunity for companies like Marshmallow and other newer players like Lemonade, Hippo and Jerry (not an insurance startup per se but also dabbling in the space), and a big opening for investors to back new ideas in an industry estimated to be worth $5 trillion.

“The traction the team has achieved demonstrates the demand for a new kind of insurance provider, one that focuses more on consumer experience and uses the latest technology and data to give fair prices,” said Eileen Burbidge, a partner at Passion Capital, in a statement. “We’ve been proud to support the team’s ambitions since the start, and now look forward to its next chapter in Europe as it continues its mission to change the industry for the better.”

Powered by WPeMatico

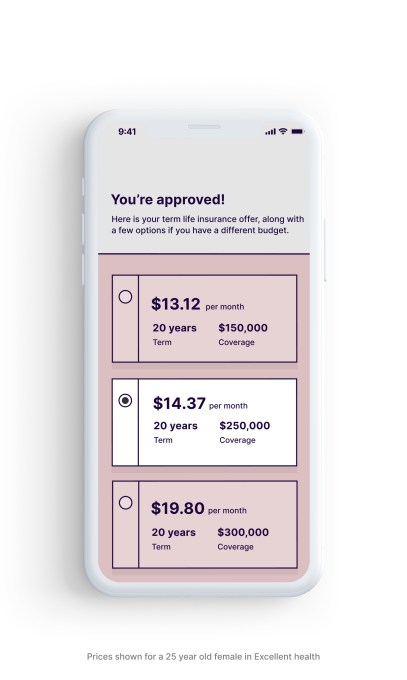

More than half of the U.S. population has stayed away from considering life insurance because they believe it’s probably too expensive, and the most common way to buy it today is in person. A startup that’s built a platform that aims to break down those conventions and democratize the process by making life insurance (and the benefits of it) more accessible is today announcing significant funding to fuel its rapidly growing business.

Ethos, which uses more than 300,000 data points online to determine a person’s eligibility for life insurance policies, which are offered as either term or whole life packages starting at $8/month, has picked up $100 million from a single investor, SoftBank Vision Fund 2. Peter Colis, Ethos’s CEO and co-founder, said that the funding brings the startup’s valuation to over $2.7 billion.

This is a quick jump for the company: It was only two months ago that Ethos picked up a $200 million equity round at a valuation of just over $2 billion.

It has now raised $400 million to date and has amassed a very illustrious group of backers. In addition to SoftBank they include General Catalyst, Sequoia Capital, Accel, GV, Jay-Z’s Roc Nation, Glade Brook Capital Partners, Will Smith and Robert Downey Jr.

This latest injection of funding — which will be used to hire more people and continue to expand its product set into adjacent areas of insurance like critical illness coverage — was unsolicited, Colis said, but comes on the heels of very rapid growth.

Ethos — which is sold currently only in the U.S. across 49 states — has seen both revenues and user numbers grow by over 500% compared to a year ago, and it’s on track to issue some $20 billion in life insurance coverage this year. And it is approaching $100 million in annualized growth profit. Ethos itself is not yet profitable, Colis said.

There are a couple of trends going on that speak to a wide opportunity for Ethos at the moment.

The first of these is the current market climate: Globally we are still battling the COVID-19 global health pandemic, and one impact of that — in particular given how COVID-19 has not spared any age group or demographic — has been more awareness of our mortality. That inevitably leads at least some part of the population to considering something like life insurance coverage that might not have thought about it previously.

However, Colis is a little skeptical on the lasting impact of that particular trend. “We saw an initial surge of demand in the COVID period, but then it regressed back to normal,” he said in an interview. Those who were more inclined to think about life insurance around COVID-19 might have come around to considering it regardless: It was being driven, he said, by those with pre-existing health conditions going into the pandemic.

That, interestingly, brings up the second trend, which goes beyond our present circumstances, and Colis believes will have the more lasting impact.

While there have been a number of startups, and even incumbent providers, looking to rethink other areas of insurance such as car, health and property coverage, life insurance has been relatively untouched, especially in some markets like the U.S. Traditionally, someone taking out life insurance goes through a long vetting process, which is not all carried out online and can involve medical examinations and more, and yes, it can be expensive: The stereotype you might best know is that only wealthier people take out life insurance policies.

Much like companies in fintech that have rethought how loan applications (and payback terms) can be rethought and evaluated afresh using big data — pulling in a new range of information to form a picture of the applicant and the likelihood of default or not — Ethos is among the companies that is applying that same concept to a different problem. The end result is a much faster turnaround for applications, a considerably cheaper and more flexible offer (term life insurance lasts only as long as a person pays for it), and generally a lot more accessibility for everyone potentially interested. That pool of data is growing all the time.

“Every month, we get more intelligent,” said Colis.

There is also the matter of what Ethos is actually selling. The company itself is not an insurance provider but an “insuretech” — similar to how neobanks use APIs to integrate banking services that have been built by others, which they then wrap with their own customer service, personalization and more — Ethos integrates with third-party insurance underwriters, providing customer service, more efficient onboarding (no in-person medical exams for example) and personalization (both in packages and pricing) around them. Given how staid and hard it is to get more traditional policies, it’s essentially meant completely open water for Ethos in terms of finding and securing new customers.

Ethos’s rise comes at a time when we are seeing other startups approaching and rethinking life insurance also in the U.S. and further afield. Last week, YuLife in the U.K. raised a big round to further build out its own take on life insurance, which is to sell policies that are linked to an individual’s own health and wellness practices — the idea being that this will make you happier and give more reason to pay for a policy that otherwise feels like some dormant investment; but also that it could help you live longer (Sproutt is another also looking at how to emphasize the “life” aspect of life insurance). Others like DeadHappy and BIMA are, like Ethos, rethinking accessibility of life insurance for a wider set of demographics.

There are some signs that Ethos is catching on with its mission to expand that pool, not just grow business among the kind of users who might have already been considering and would have taken out life insurance policies. The startup said that more than 40% of its new policy holders in the first half of 2021 had incomes of $60,000 or less, and nearly 40% of new policy holders were under the age of 40. The professions of those customers also speak to that democratization: The top five occupations, it said, were homemaker, insurance agent, business owner, teacher and registered nurse.

That traction is likely one reason why SoftBank came knocking.

“Ethos is leveraging data and its vertically integrated tech stack to fundamentally transform life insurance in the U.S.,” said Munish Varma, managing partner at SoftBank Investment Advisers, in a statement. “Through a fast and user-friendly online application process, the company can accurately underwrite and insure a broad segment of customers quickly. We are excited to partner with Peter Colis and the exceptional team at Ethos.”

Powered by WPeMatico

Life insurance — financial protection you buy against your death — may not read like the liveliest of industries on paper. But a life insurance startup that believes it can turn that stigma around, by infusing the concept with gamification and a push toward wellness and health — and change the life insurance industry in the process — is today announcing significant funding, a sign of the traction it’s getting for its big ideas.

YuLife, a London startup that has built a new kind of life insurance concept — it incentivizes and rewards users to focus on their physical and mental health through a gamified interface — has raised $70 million in what is, to date, one of the largest Series Bs raised by an insurtech startup in Europe.

Led by Target Global, the round also included Eurazeo, Latitude and previous backers Creandum, Notion Capital, Anthemis, MMC Ventures, and OurCrowd. Sammy Rubin, YuLife’s CEO and founder, confirmed that the round values YuLife at $346 million (£250 million).

The company will be using the funding to continue expanding its business, build more products on its platform, and importantly continue to invest in the technology that it uses to run its service and determine how its policies should run.

“Our insurance is about helping people live healthier and longer lives,” Rubin said in an interview. “If we can help to reduce claims while incentivizing people to do that, it’s a win-win.” But it’s about more than that, he added. “We are building a new type of risk model where we are able to create new actuarial tables, which have not been updated in 200 years. Actually, I think smoker rates and how they’ve changed was the last update. So, most will just look at your age and whether you are a smoker and that’s it.”

YuLife is currently active only in the U.K. and is only sold directly to organizations, who in turn provide it to their employees. That business currently — which also includes income protection and critical illness cover — provides $15 billion of coverage and has seen 10x growth in the last year — a bumper one for life insurance policies, possibly for the worst reasons (hello, pandemic; goodbye, predicting what the future might look like). Customers include Capital One, Co-op, Curve, Havas Media, Severn Trent and Sodexo.

That $15 billion is just a drop in the bucket in an industry that is currently estimated to be worth some $2.2 trillion.

The company got its start on the back of a persistent problem that Rubin experienced at his previous insurance startup PruProtect (which is now called Vitality Life).

“Usually insurance benefits just sit on a shelf and never get used,” he said. YuLife set out to change that by making the policy “all about engagement.”

The app — built by veterans of the gaming industry — is designed around the concept of different environments, currently covering forest, ocean, desert and mountains, which YuLife collectively terms its “Yuniverse.” (This incidentally also became a template for the company’s HQ design in London.)

Within each of these environments, users are encouraged to walk, cycle, meditate and do other activities to get around their environments in a healthy way, while at the same time being able to compare their progress against other co-workers. There is a degree of personalization in everyone’s experience, in that one person leaning into one activity over another seems to produce different subsequent scenarios.

Along with this, users are offered discounts on third-party products to further engage with the game within YuLife, which could include a subscription to meditation app Calm, FitBit and Garmin devices, and more.

As users make their way through their worlds, they get rewards, in the form of something called YuCoins. The YuCoins can in turn be used to redeem vouchers from the likes of Amazon and Asos to buy things … consumerism being another way to improve happiness for some of us.

All of this sums up as more than just a policy aimed at giving people peace of mind for their families should they depart this world.

“Long term, it’s not just about health, it’s about lifestyle,” Rubin said.

It’s also about YuLife’s business: The various products that it offers are built around an affiliate model, so there is a business interest for the company around offering and seeing items purchased and redeemed. However, this is not essential to using the app as a policy holder.

The win-win theme runs strong, but so too does the fact that YuLife is taking a different approach altogether, in an industry where most of the “disruption” has up to now been more about how to buy life insurance, rather than reassessing what life insurance actually is. For others in the space doing just that, see DeadHappy, BIMA, and the Jay-Z-backed Ethos. That being said, it’s also not the only one tackling “lifestyle” as part of life insurance: Sproutt is another rethinking that area as well.

“YuLife is redefining life insurance, using the most innovative technologies to transform a largely traditional industry,” said Ben Kaminski, partner, Target Global, in a statement. “With health and well-being increasingly thrust into the limelight in the wake of COVID-19, YuLife is fundamentally changing insurance by incentivizing people to lead healthier lifestyles. YuLife is ideally positioned to build on its tenfold growth during the pandemic and lead the way in helping its clients respond to the challenges posed by an ever-changing working environment. We are very proud to partner with YuLife on its journey of becoming a global leader in life insurance.”

Powered by WPeMatico

Super.mx, an insurtech startup based in Mexico City, has raised $7.2 million in a Series A round led by ALLVP.

Co-founded in 2019 by a trio of former insurance industry executives, Super.mx’s self-proclaimed mission is to design insurance for “the emerging Latin American middle class,” according to CEO Sebastian Villarreal.

“That means insurance that is easy to buy – it can be bought on a cell phone in minutes – and that pays quickly with no adjusters,” he said. The company has built its offering with proprietary models that are used both on the underwriting side to predict risk and on the claims side to make payments automatically.

Goodwater Capital, Kairos Angels and Bridge Partners also participated in the Series A round in addition to angels such as Joe Schmidt IV, vice president of business development at insurtech Ethos and former investor at Accel and Kyle Nakatsuji, founder and CEO of auto insurance startup Clearcover (and also a former VC). Better Tomorrow Ventures led Super.mx’s $2.4 million seed round, which also saw capital from 500 Startups Mexico, Village Global, Anthemis and Broadhaven Ventures, among others.

Unlike most insurtech startups in Latin America, Villarreal emphasizes that Super.mx is neither an aggregator nor a carrier. Instead, it’s an MGA, or managing general agent.

“This lets us have a ‘best of both worlds’ approach,” Villarreal said. “We handle the entire user experience just like a direct to consumer carrier, but with the breadth of product choice offered by an aggregator.”

That product choice includes property, natural disasters and life insurance. The company soon plans to expand to also offer health insurance.

The founding team brings a variety of insurance experience to the table. Villarreal previously co-founded Chicago-based Kin Insurance (which raised over $150 million in funding from the likes of Flourish Ventures, Commerce Ventures and QED Investors). He was also once head of auto product at Avant, a growth-stage company funded by General Atlantic and Tiger Global, among others.

With over two decades of insurance industry experience, Dario Luna once served as Mexico’s insurance regulator and helped develop Mexico’s disaster risk management strategy. Marco Ahedo has designed parametric insurance products for 19 Caribbean countries. He was also once a solvency expert for life and health insurance lines at MetLife, and has developed financial models for several P&C carriers.

Villarreal lived in the U.S. for a while before deciding to move back to Mexico, which he recognized was home to an “underinsurance problem.”

“That’s actually a very acute problem,” he said. “People in Latin America buy a lot less insurance than they do in the U.S., and people in Mexico, in particular, buy a lot less insurance than they do in other Latin countries.”

Some have blamed the lack of insurance coverage on the country’s culture but Super.mx operates under the belief that this notion is “total BS.”

“It’s not a cultural problem,” Villarreal said. “The problem is that the insurance products that exist in the market just suck. They’re super expensive. They’re really hard to buy, and they pay very little.”

Image Credits: Super.mx

So far, Super.mx has sold “thousands of policies” but is more focused now on increasing the number of products that it’s selling. The company started out by selling earthquake insurance before adding COVID insurance, and more recently, in April, it launched life insurance. Next, it’s going to offer property, renter’s and health insurance.

“It’s really a different strategy than what you would find in the U.S.,” Villarreal said. “In the U.S, when you look at insurtechs, it’s like everyone just does one thing, but here, it’s very different because when someone says ‘I want insurance,’ really what they’re saying is ‘Hey, something happened that makes me nervous that didn’t make me nervous before.’”

That something could be a new child, for example, that prompts a need for life insurance.

“What we’re trying to do is like Lemonade, Roots and Hippo or Kin all rolled into one,” he added. It’s a big, big play.”

Digital adoption in Mexico, and Latin America in general, has increased exponentially in recent years. The bigger hurdle for Super.mx, according to Villarreal, has less to do with technology and more to do with Mexicans getting over what he describes a “deep mistrust” based on bad experiences in the past.

“People are really distrustful and that’s a huge hurdle, but once you show them that you actually are different,” Villarreal told TechCrunch, “that you actually do things in a different way, you get this incredible emotional response.”

Eventually, Super.mx plans to outside of Mexico to other countries in Latin America.

ALLVP’s Federico Antoni said his Mexico City-based firm had been looking for a team building in this space “for years” before investing in Super.mx. The venture firm was impressed with the company’s technical knowledge and industry expertise. It was also drawn to their multi-product approach and “capacity to ship highly complex products to the market quickly” — both of which he believes are “unique” in the region.

Citing statistics from MAPFRE Economics, Antoni pointed out that globally, the insurance market has been growing over the last 10 years. During that time, Latin America expanded faster on average (4.4% vs. 2.4% worldwide), albeit with more volatility. Life insurance has been driving this growth, at 6.1%, over the period.

“Insurtech may be even bigger than fintech. Also, harder,” he told TechCrunch via email. “We knew the team to unlock the market potential would need to be highly competent and highly disruptive.”

Antoni said he is also convinced that Insurtech is the “next frontier” in financial inclusion in Latin America especially as digitization continues to increase.

“Providing risk coverage to individuals and businesses in the region, brings financial stability to families and unlocks economic potential for SMEs,” he said. “Moreover, the insurance incumbents have been unable to address a growing and underserved market.”

Powered by WPeMatico

An estimated 41 million Americans say they need life insurance but have yet to purchase coverage. Despite this awareness among consumers, the Life Insurance Marketing and Research Association estimates a $12 trillion coverage gap, with about 50% of millennials planning to purchase coverage within the next year.

There’s latent demand for life insurance currently unaddressed by much of the financial services industry, and embedded finance can be the solution. It’s imperative for companies to consider product lines and partnerships to expand markets, create new revenue streams and provide added value to their customers.

There’s latent demand for life insurance currently unaddressed by much of the financial services industry, and embedded finance can be the solution.

Connecting consumers with products they need through channels they already know and trust is both a massive revenue opportunity and a social good, providing financial resilience to families at a time when they need it most.

The concept of digitally bundling financial products in a packaged offering to a customer is certainly not new — but it is for the life insurance space.

Embedded finance uses technology and operations infrastructure to offer products and services through entities that may not be financial institutions at all. Think of embedded finance like on-demand shopping; customers benefit from both the transaction (buying financial protection for their families) and the convenience it provides (from whatever platform they are currently engaging with).

Similar to how Amazon saves shoppers 75 hours a year, bundling life insurance gives consumers back time in their day and can improve their financial health.

Powered by WPeMatico

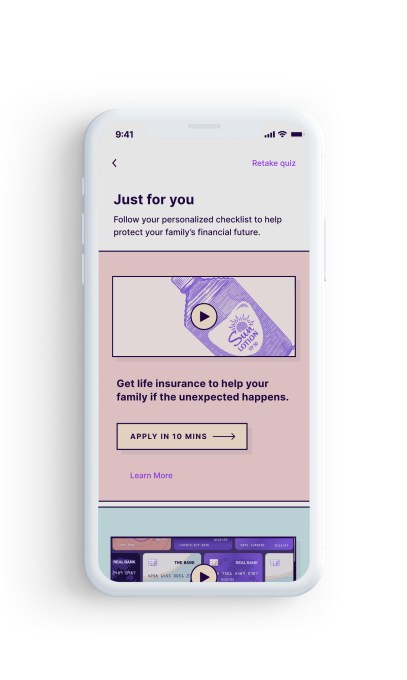

A new app called Fabric aims to make it simpler for parents to plan for their family’s long-term financial well-being. The goal is to offer parents a one-stop-shop that includes the ability to ability for term life insurance from their phone, create a free will in about five minutes, and collaborate with a spouse or partner to organize key financial accounts or other important documents. In addition, parents are able to coordinate with beneficiaries, children’s guardians, attorneys, financial advisors, and others right from the app.

Fabric was originally founded in 2015 by Adam Erlebacher, previously the COO at online bank Simple, and Steven Surgnier, previously the Director of Data at Simple. The company last year raised a $10 million Series A led by Bessemer Venture Partners, after having sold life insurance coverage to thousands of families.

Since launch, Fabric has expanded beyond life insurance to offer other services, like easy will creation and the addition of tools that help families organize their financial and legal information in one place. The idea, the company explained at the time, was to offer today’s busy parents a better alternative to meetings with agents to discuss complicated life insurance products. Instead, the company offers a simple, 10-minute life insurance application and the option to connect with a licensed team if they need additional help, as well as a similarly simplified will creation workflow.

As with the founders’ earlier company, Simple, which offered a better front-end to banking while actual bank accounts were held elsewhere, Fabric’s life insurance policies are issued by “A” rated insurer, Vantis Life, not Fabric itself.

However, until now, Fabric’s suite of services were only available on the web. They’re now offered in an app for added convenience. The app is initially available on iOS with an Android version in the works.

“Money can be especially stressful when you’re trying to build a family and a career,” said Fabric co-founder and CEO Adam Erlebacher. “In one survey by Everyday Health, 52% of respondents said financial issues regularly stress them out, and people between the ages of 38 to 53 were the most stressed out financially. Parents want to have more control over their families’ long-term financial well-being and today’s dusty old products and tools are failing them,” he added.

Using the Fabric app, parents can take advantage of any of its offerings, including the option to apply for life insurance from the phone and get immediate approval. The app also makes it possible to share the policy information with beneficiaries, so it doesn’t get lost.

Another feature lets you create your will for free, and share that information with key people as well, including the witnesses you need to coordinate with in order to finalize the will, for example. And a spouse can choose to mirror your will, which speeds up the process of creating a second one with the same set of choices.

Fabric also helps to address an issue that often only comes up after it’s too late or in other emergency situations — organizing both parents’ finances in a single place. Many working adults today have not just a bank account, but also have investment accounts, 401Ks, IRAs, and credit cards, or a combination of those. But their partner may not know where to find this information or where the accounts are held.

The app, which we put through its paces (but didn’t purchase life insurance through), is very easy to use. It starts off with a short quiz to get a handle on your financial picture. It then delivers you to a personalized homescreen with a checklist of suggestions of what to do next. Naturally, this includes the life insurance application, as this is where Fabric’s revenue lies. And if you’re lacking a will and have other fiances to organize, these are featured, too.

The online forms are easy to fill out, despite the smartphone’s reduced screen space compared with a web browser, and Fabric has taken the time to get the small touches right — like when you enter a phone number, the numeric keypad appears, for example, or the integration of address lookup so you can just tap on the match and have the rest autofill. It also saves your work in progress, so you can finish later in case you get interrupted — as parents often do. And it explains terms, like “executor,” so you know what sort of rights you’re assigning.

Given its focus, Fabric protects user information with bank-grade security, including 256-bit encryption, two-factor authentication, automatic lockouts, biometrics, and other adaptive security features.

Fabric isn’t alone in helping parents and others financially plan wills and more from their iPhone. Other apps exist in this space, including will planning apps from Tomorrow, LegalZoom, Qwill, and others. Plus many insurers offer a mobile experience. Fabric is unique because it puts wills, insurance, and other tools into a single destination, without complicating the user interface.

Fabric’s app is a free download on the App Store.

Powered by WPeMatico