Libra Association

Auto Added by WPeMatico

Auto Added by WPeMatico

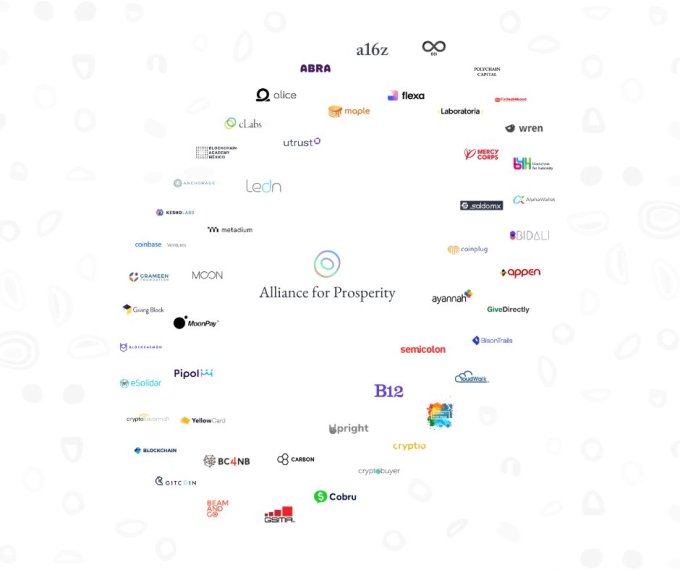

Some Libra Association members like Andreessen Horowitz and Coinbase Ventures are double-dipping, backing a competing cryptocurrency developer platform. Launching today with over 50 partners, non-profit The Celo Foundation’s ‘Alliance For Prosperity’ offers a way for developers to build decentralized mobile apps that are based on Celo’s blockchain platform and USD stablecoin.

The open-source Celo platform is still in testing with plans to officially launch its mainnet in April. The non-profit founded in 2017 has raised $36.4 million, including its Series A where Andreessen Horowitz’s a16z Crypto bought $15 million worth of Celo Gold tokens.

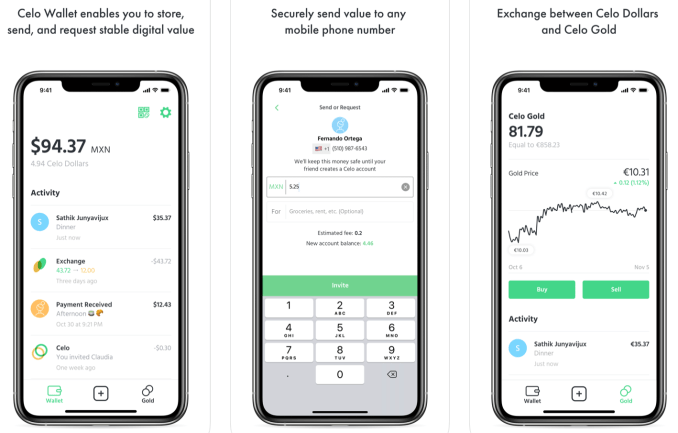

The biggest differentiator of Celo’s network versus other blockchains is that payments in the Celo Dollar stablecoin can be sent to people’s phone numbers rather than complicated addresses. The goal is to make delivering utility via blockchain easier by building a flexible network of applications that doesn’t scare regulators like Libra has.

The Alliance For Prosperity includes Andreessen Horowitz (which funded Celo), Coinbase (Ventures), Bison Trails, Anchorage, and Mercy Corps — all of which are also Libra Association members. That could potentially create a conflict of interest regarding which cryptocurrency and developer platform they promote to their portfolio companies, integrate into their products, or focus on for delivering financial services to the needy.

Other high-profile Alliance partners include Carbon, GiveDirectly, Grameen Foundation, Maple, and Polychain. Partners have made a somewhat vague commitment to “backing development efforts of the project, building infrastructure, implementing desired use cases on the platform, integrating Celo assets in their projects, or collaborating on education campaigns in their communities to further advance the use of blockchain technology” according to Chuck Kimble, Celo’s cLabs head of business development and head of the Alliance. Anyone can apply to join the open network, and there’s no minimum financial investment like Libra’s $10 million prerequisite.

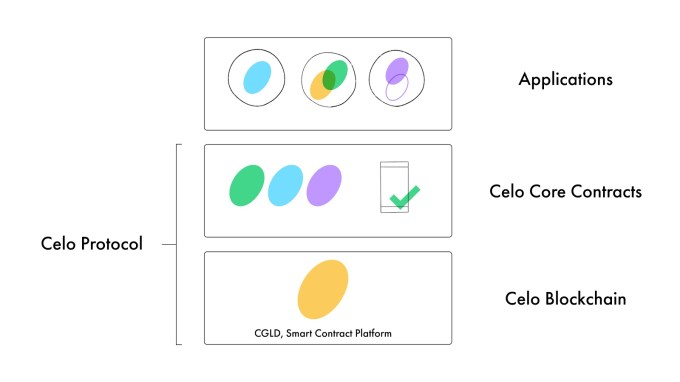

Celo isn’t trying to replace the dollar with its own synthetic currency, and its reserve is backed with other cryptocurrencies rather than fiat cash. That might make it more acceptable to regulators who were worried that Libra’s token and fiat currency bundle-backed reserve could impact the global financial system. The first of the decentralized apps on the platform, the Celo Wallet, is already available for iOS and Android.

Like many blockchain projects, there are some lofty intentions for social impact with Celo. Use cases include “powering mobile and online work, enabling faster and affordable remittances, reducing the operational complexities of delivering humanitarian aid, facilitating payments, and enabling microlending” says Kimble. The real driver of this potential is Celo’s promise of much lower transaction fees than traditional middlemen charge.

When asked what the biggest threats to Celo’s success are, he told me “Banking infrastructure improving faster than we expect” and “Mobile adoption or LTE data not expanding on their current trajectory.” He did not mention the developer fatigue, regulatory scrutiny, technical complexity, or slow adoption of blockchain utilities that have plagued other crypto for good projects.

Here’s the full list of members working towards these goals:

Abra, Alice, AlphaWallet, Anchorage, Appen, Ayannah, Andreessen Horowitz, B12, BC4NB (Blockchain for the Next Billion), BeamAndGo, Bidali, Bison Trails, Blockchain Academy Mexico, Blockchain.com, Blockchain for Humanity (b4h), Blockchain for Social Impact (BSIC), Blockdaemon, Carbon, cLabs, CloudWalk Inc, Cobru, Coinbase, Coinplug, Cryptio, Cryptobuyer, CryptoSavannah, eSolidar, Fintech4Good, Flexa, Gitcoin, GiveDirectly, Grameen Foundation, GSMA, KeshoLabs, Laboratoria, Ledn, Maple, Mercy Corps, Metadium, Moon, MoonPay, Pipol, Pngme, Polychain, Project Wren, SaldoMX, Semicolon Africa, The Giving Block, Utrust, Upright, Yellow Card, and 88i. [Update: Ledger joined this morning.]

“Many of these organizations have on-the-ground operations that will begin to get Celo into the hands of those who have been underserved by the current global financial system” Andreessen Horowitz general partner Katie Haun told me. “Our hope is that this partnership will start unlocking the potential of internet money”. To spur adoption, the Alliance will distribute ‘Prosperity Gifts’ in the form of financial grants to developers proposing Celo products that would benefit society.

There are also some peculiar characteristics of Celo’s system. People exchange other cryptocurrencies for Celo Gold, then exchange that for Celo Dollars they can spend. The reserve is backed with other cryptocurrencies like bitcoin and ethereum rather that fiat, and isn’t fully collateralized. That could make it vulnerable to a Celo bank run or crash in price of those currencies. Celo also lets arbitrageurs pocket the difference if Celo Gold and Celo Dollars get out of sync.

While it might not be a danger to the world financial system like Libra, it could be a danger to itself. At least on the anti-money laundering front, cLabs — the team that’s kicking off development of the Celo platform — has hired former Capital One head of enterprise risk management Jai Ramaswamy. Plus, the Celo founders come well pedigreed, including Marek Olszewski and Rene Reinsberg who spun out machine learning startup Locu from MIT and sold it to GoDaddy, as well as EigenTrust inventor and former MIT Media Lab professor Sep Kamvar.

While it might not be a danger to the world financial system like Libra, it could be a danger to itself. At least on the anti-money laundering front, cLabs — the team that’s kicking off development of the Celo platform — has hired former Capital One head of enterprise risk management Jai Ramaswamy. Plus, the Celo founders come well pedigreed, including Marek Olszewski and Rene Reinsberg who spun out machine learning startup Locu from MIT and sold it to GoDaddy, as well as EigenTrust inventor and former MIT Media Lab professor Sep Kamvar.

So far, 130 teams have expressed interest in building on the Celo platform. For reference, Libra said 1,500 organizations had said they wanted to work on that project four months after its reveal. Celo Camp and Blockchain for Social Impact Incubator will also be fostering projects for the blockchain.

Celo could make banking cheaper and more accessible while power new fintech innovation. But for any of that to happen, it will need to get enough developers building truly useful products, make the blockchain and currency exchange simple enough for mainstream audiences in developing nations, and grow adoption to meaningful levels few cryptocurrency projects have yet achieved. The Alliance For Prosperity will have to throw their weight into this project, not just their names, if it’s going to succeed.

Powered by WPeMatico

TechCrunch has learned that $28 million-funded crypto startup Tagomi will be the newest member of the Libra Association that governs the Facebook-backed Libra stablecoin. A formal announcement is slated for Friday or next week.

Tagomi offers a platform that helps large traders and funds easily access cryptocurrency markets. The news comes days after Libra added Shopify, a reversal of dwindling membership after major partners like Visa, PayPal and Stripe dropped out late last year.

We’ve reached out to the Libra Association and have been promised a response by Facebook’s communications team.

Joining Libra means Tagomi will be expected to contribute at least $10 million toward developing the cryptocurrency, with that investment eligible to reap dividends from interest earned on money kept in the Libra Reserve. Tagomi will also operate a node that validates transactions coming through the Libra blockchain.

Tagomi was founded by Jennifer Campbell, a former investor at Union Square Ventures, which is also a Libra Association Member. The company has 25 employees across five offices. Tagomi will be the 22nd member of the Libra Association, according to information from the startup’s press representative, who was apparently supposed to hold this news until later. “Tagomi is joining the Libra Foundation and Jennifer will be the newest member,” they emailed TechCrunch. We’ll update this story following our interview with Campbell tomorrow.

Campbell and Tagomi will offer technical and policy support to Libra in an effort to make the cryptocurrency more safe and compliant with international law. That will be critical for the Libra Association to get the green light from regulators for a launch in 2020 like it originally planned. Lawmakers in the U.S. and EU have slammed Libra in hearings and the press over its potential to facilitate money laundering, harm privacy and destabilize the global financial system.

The full membership of the Libra Association is now:

Current Members:

Facebook’s Calibra, Tagomi, Shopify, PayU, Farfetch, Lyft, Spotify, Uber, Illiad SA, Anchorage, Bison Trails, Coinbase, Xapo, Andreessen Horowitz, Union Square Ventures, Breakthrough Initiatives, Ribbit Capital, Thrive Capital, Creative Destruction Lab, Kiva, Mercy Corps, Women’s World Banking.

Former Members:

Vodafone, Visa, Mastercard, Stripe, PayPal, Mercado Pago, Bookings Holdings, eBay.

Powered by WPeMatico

After eBay, Visa, Stripe and other high-profile partners ditched the Facebook -backed cryptocurrency collective, Libra scored a win today with the addition of Shopify. The e-commerce platform will become a member of Libra Association, contributing at least $10 million and operating a node that processes transactions for the Facebook-originated stable coin.

If Libra manages to assuage international regulators’ concerns, which are currently blocking its roll out, Shopify could gain a way to process transactions without paying credit card fees. Libra is designed to move between wallets with zero or nearly-zero fees. That could save money for Shopify and the 1 million merchants running online shops on its platform.

Shopify stressed that helping merchants reduce fees and bringing commerce opportunities to developing nations as reasons it’s joining the Libra Association . “Much of the world’s financial infrastructure was not built to handle the scale and needs of internet commerce,” Shopify writes. Here are the most critical parts of its announcement:

Our mission is to make commerce better for everyone and to do that, we spend a lot of our time thinking about how to make commerce better in parts of the world where money and banking could be far better . . . As a member of the Libra Association, we will work collectively to build a payment network that makes money easier to access and supports merchants and consumers everywhere . . . Our mission has always been to support the entrepreneurial journey of the more than one million merchants on our platform. That means advocating for transparent fees and easy access to capital, and ensuring the security and privacy of our merchants’ customer data. We want to create an infrastructure that empowers more entrepreneurs around the world.

As part of the Libra Association, Shopify will become a validator node operator, gain one vote on the Libra Association council and can earn dividends from interest earned on the Libra reserve in proportion to its investment, which is $10 million at a minimum.

The Libra Association had lost much of its e-commerce expertise when a string of members abandoned the project in October amidst regulatory scrutiny. That included traditional payment processors like Visa and Mastercard, online processors like Stripe and PayPal and marketplaces like eBay. That threw into question whether Libra would have the right partners to make the cryptocurrency accepted in enough places to be useful to people.

As it works to convince regulators Libra is safe, Facebook has been working on its other payment plays, including Facebook Pay and WhatsApp Pay, that rely on traditional bank transfers or credit cards.

Shopify’s CEO Tobi Lutke tweeted that “Shopify spends a lot of time thinking about how to make commerce better in parts of the world where money and banking could be far better. That’s why we decided to become a member of the Libra Association.”

“We are proud to welcome Shopify, Inc. (SHOP) to the Libra Association. As a multinational commerce platform with over one million businesses in approximately 175 countries, Shopify, Inc. brings a wealth of knowledge and expertise to the Libra project,” writes Dante Disparte, the Libra Association’s head of Policy and Communications. “Shopify joins an active group of Libra Association members committed to achieving a safe, transparent, and consumer-friendly implementation of a global payment system that breaks down financial barriers for billions of people.”

A recent hire further tied the two companies together. Facebook’s former lead product manager for its payment platform and billing teams, Kaz Nejatian, in September became Shopify’s VP and GM of money.

Operating an e-commerce store can be difficult or impossible without a traditional bank account that can be tough to attain in some developing countries. Libra could allow these merchants to establish a Libra Wallet where payments are sent instantly, without steep credit card fees, and in theory could be cashed out at local brick-and-mortar establishments or ATMs for local fiat currency.

Shopify’s credit card readers

But for any of that to happen, the Libra Association will have to convince the U.S. government, the EU and more that it won’t help terrorists launder money, hurt people’s privacy or weaken nations’ power in the global financial system. “The French Finance Minister Bruno Le Maire said, “the monetary sovereignty of countries is at stake from a possible privatisation of money . . . we cannot authorise the development of Libra on European soil.”

Libra was initially slated to launch in 2020. We’ll see.

—

Here’s the full list of Libra Association members:

Current

Facebook’s Calibra, Shopify, PayU, Farfetch, Lyft, Spotify, Uber, Illiad SA, Anchorage, Bison Trails, Coinbase, Xapo, Andreessen Horowitz, Union Square Ventures, Breakthrough Initiatives, Ribbit Capital, Thrive Capital, Creative Destruction Lab, Kiva, Mercy Corps, Women’s World Banking.

Former members

Vodafone, Visa, Mastercard, Stripe, PayPal, Mercado Pago, Bookings Holdings, eBay.

Powered by WPeMatico

Not the city, the $57 million-funded cryptocurrency custodian startup. When someone wants to keep safe tens or hundreds of millions of dollars in Bitcoin, Ethereum or other coins, they put them in Anchorage’s vault. And now they can trade straight from custody so they never have to worry about getting robbed mid-transaction.

With backing from Visa, Andreessen Horowitz and Blockchain Capital, Anchorage has emerged as the darling of the cryptocurrency security startup scene. Today it’s flexing its muscle and war chest by announcing its first acquisition, crypto risk modeling company Merkle Data.

Anchorage Founders

Anchorage has already integrated Merkle’s technology and team to power today’s launch of its new trading feature. It eliminates the need for big crypto owners to manually move assets in and out of custody to buy or sell, or to set up their own in-house trading. Instead of grabbing some undisclosed spread between the spot price and the price Anchorage quotes its clients, it charges a transparent per transaction fee of a tenth of a percent.

It’s stressful enough trading around digital fortunes. Anchorage gives institutions and token moguls peace of mind throughout the process while letting them stake and vote while their riches are in custody. Anchorage CEO Nathan McCauley tells me, “Our clients want to be able to fund a bank account with USD and have it seamlessly converted into crypto, securely held in their custody accounts. Shockingly, that’s not yet the norm — but we’re changing that.”

Founded in 2017 by leaders behind Docker and Square, Anchorage’s core business is its omnimetric security system that takes out of the equation passwords that can be lost or stolen. Instead, it uses humans and AI to review scans of your biometrics, nearby networks and other data for identity confirmation. Then it requires consensus approval for transactions from a set of trusted managers you’ve whitelisted.

With Anchorage Trading, the startup promises efficient order routing, transparent pricing and multi-venue liquidity from OTC desks, exchanges and market makers. “Because trading and custody are directly integrated, we’re able to buy and sell crypto from custody, without having to make risky external transfers or deal with multiple accounts from different providers,” says Bart Stephens, founder and managing partner of Blockchain Capital.

Trading isn’t Anchorage’s primary business, so it doesn’t have to squeeze clients on their transactions, and can instead try to keep them happy for the long-term. That also sets up Anchorage to be a foundational part of the cryptocurrency stack. It wouldn’t disclose the terms of the Merkle Data acquisition, but the Pantera Capital-backed company brings quantitative analysts to Anchorage to keep its trading safe and smart.

“Unlike most traditional financial assets, crypto assets are bearer assets: In order to do anything with them, you need to hold the underlying private keys. This means crypto custodians like Anchorage must play a much larger role than custodians do in traditional finance,” says McCauley. “Services like trading, settlement, posting collateral, lending and all other financial activities surrounding the assets rely on the custodian’s involvement, and in our view are best performed by the custodian directly.”

Anchorage will be competing with Coinbase, which offers integrated custody and institutional brokerage through its agency-only OTC desk. Fidelity Digital Assets combines trading and brokerage, but for Bitcoin only. BitGo offers brokerage from custody through a partnership with Genesis Global Trading. But Anchorage hopes its experience handling huge sums, clear pricing and credentials like membership in Facebook’s Libra Association will win it clients.

McCauley says the biggest threat to Anchorage isn’t competitors, though, but hazy regulation. Anchorage is building a core piece of the blockchain economy’s infrastructure. But for the biggest financial institutions to be comfortable getting involved, lawmakers need to make it clear what’s legal.

Powered by WPeMatico

“I don’t control Libra” was the central theme of Facebook CEO Mark Zuckerberg’s testimony today in Congress. The House of Representatives unleashed critiques of his approach to cryptocurrency, privacy, encryption and running a giant corporation during six hours of hearings. Zuckerberg tried to assuage their fears while stoking concerns that if Facebook doesn’t build Libra, the world will end up using China’s version. Yet Facebook won’t stop shaking up society, with Zuckerberg saying its News tab feature will be announced this week.

During the hearing before the House Financial Services Committee that you can watch here, Zuckerberg recommitted to only releasing Libra with full U.S. regulatory approval. But given the tone of the questioning and Zuckerberg’s lack of fresh answers since Facebook’s David Marcus testified about Libra in July, Libra now looks even less likely to launch in 2020.

The hearing started tensely, with Rep. Maxine Waters (D-CA) declaring that “Perhaps you believe that you’re above the law, and it appears that you are aggressively increasing the size of your company, and are willing to step over anyone, including your competitors, women, people of color, you own users, and even our democracy to get what you want . . . In fact, you have opened up a serious discussion about whether Facebook should be broken up.“

However, some members of Congress used their time to advocate for American dominance instead of heavy regulation. Rep. Patrick McHenry (R-NC) said “the question is, are we going to spend our time trying to devise ways for government planners to centralize and control as to who, when and how innovators can innovate.” Many Republicans complimented Zuckerberg on his business acumen, though none showed outright support for Libra.

With few highlights or positive moments coming from the hearing, here are the major takeaways followed by a chronicle of the top exchanges between Zuckerberg and Congress:

Zuckerberg tried to leverage nationalist sentiment to deflect scrutiny. “As soon as we put forward the white paper around the Libra project, China immediately announced a public private partnership, working with companies . . . to extend the work that they’ve already done with AliPay into a digital Renminbi as part of the Belt and Road Initiative that they have, and they’re planning on launching that in the next few months.” He later said that for Libra, “Chinese companies would be the primary competitors.”

Facebook’s executives have repeatedly leaned on this “let us, or China will” argument we chronicle here.

What if the Libra Association chooses to add the Chinese currency to the basket used to back Libra and reduces the U.S. dollar’s fraction of the basket? “I think it would be completely reasonable for our regulators to try to [implement] a restriction that says that it has to be primarily U.S. dollars,” Zuckerberg responded in one of his most substantial answers of the day. Zuckerberg was receptive to feedback that the Libra Association should keep its white paper updated.

As for why Libra isn’t just backed 100% with the U.S. dollar, Zuckerberg explained that “I think from a U.S. regulatory perspective, it would probably be significantly simpler. But because we’re trying to build something that can also be a global payment system that works in other places, it may be less welcome in other places if it’s only 100% based on the dollar.” Still, Zuckerberg said he would leave his children their inheritance in Libra because it’s backed one-to-one by the Libra reserve.

Zuckerberg wouldn’t commit to blocking anonymous Libra wallets that could facilitate money laundering, only saying Facebook’s own Calibra wallet would have strong identity checks. He did say Libra was exploring whether it could encode “know your customer” protections at the network level instead of relying on developers to build this into their wallets.

On whether Facebook will increasingly seek to verify users’ identities through government ID, Zuckerberg was enthusiastic. “This is an area where I think we are going to do a lot more in the years to come. We started with political ads . . . over the coming years for anything that people are doing that is sensitive, we’re likely going to increasingly require verification either by government ID or other things so we can have a clear sense of people’s authentic identity.”

Rep. Dean Phillips (D-MN) mentioned this could be a competitive advantage, implying Facebook’s size and resources might allow it to embark on a verification initiative other companies couldn’t.

Facebook has assured regulators that Calibra’s data would be kept separate from the social network. But Facebook said the same when it acquired WhatsApp, then reneged and integrated its data. This time around, Congresswoman Nydia Velázquez declared that “we’re going to need to make sure that . . . you learned that you should not lie.”

When pushed on why Libra Association members like Visa, Stripe and eBay left the organization, Zuckerberg admitted, “I think because it’s a risky project and there’s been a lot of scrutiny.” Zuckerberg struck back at finance incumbents, saying “I think that the U.S. financial industry . . . is just frankly behind where it needs to be to innovate and continue American financial leadership going forward.”

In an awkward moment, Zuckerberg could not answer which Libra members were run by women, minorities or LGBTQ+ people. “Is it true that the overwhelming majority of persons associated with this endeavor are white men?,” Rep. Al Green (D-TX) asked. “Congressman, I don’t know off the top of my head,” Zuckerberg responded.

Zuckerberg was criticized for trying to profit and potentially helping money laundering while claiming Libra is designed to help the unbanked. Zuckerberg said the Libra Association “hadn’t nailed down policies” about whether anonymous payments are allowed.

Rep. Brad Sherman (D-CA) said “for the richest man in the world to come here and hide behind the poorest people in the world, and say that’s who you’re really trying to help. You’re trying to help those for whom the dollar is not a good currency — drug dealers, terrorists.” Some members of Congress like Sherman chose to use their entire time monologuing instead of actually asking questions.

Zuckerberg got a chance to clear up a major snafu from Marcus’ testimony, where he said the Libra Association was in contact with the Swiss data regulator, which CNBC reported hadn’t heard from Libra. Zuckerberg explained today that the Libra Association had been in contact with the primary Swiss Financial Market Supervisory Authority instead. He says Facebook plans to earn money from Libra on ads from small businesses if cheap transactions lead to more e-commerce.

In one revealing exchange, Rep. Lance Gooden (R-TX) asked if the Libra Association still planned to offer profit incentives by offering dividends based on interest earned on currency in the Libra reserve after expenses are paid. Zuckerberg said the idea had either been “modified or abandoned.”

The highlighted section detailing how Libra Association members earn dividends on Libra reserve interest has been removed from the Libra whitepaper

Throughout the testimony, Zuckerberg tried to distance himself and Facebook from the Libra Association’s decision making process. “We might be required to pull out if the Association independently decides to move forward on something that we’re not comfortable with,” Zuckerberg said. That means if Facebook can’t launch Libra, it could still theoretically launch without the social network, though it does most of the engineering heavy-lifting.

The strategy was crystallized by Zuckerberg’s response to whether he could commit to moving Libra’s headquarters from Switzerland to the U.S. “At this point, we do not control the independent Libra Association so I don’t think we can make that decision.” Rep. Ayanna Pressley (D-MA) refuted this position, stating, “Mr. Zuckerberg, Libra is Facebook, and Facebook is you.”

The Facebook CEO, Mark Zuckerberg, testified before the House Financial Services Committee on Wednesday October 23, 2019 Washington, D.C. (Photo by Aurora Samperio/NurPhoto via Getty Images)

The “we don’t control Libra” argument provides Facebook and Libra an escape hatch from criticism, because any member and even the newly appointed chairperson and board can’t unilaterally control or make promises about its actions.

Many Congress members remain fixated on Facebook’s recently solidified policy of refusing to submit political ads for fact-checking. Rep Sean Casten (D-IL) asked if in Zuckerberg’s recent meeting with President Trump, “Did anyone discuss the policy change along the exemption of political figures and parties from misinformation prohibition on Facebook?” Zuckerberg responded, “Congressman, that did not come up,” quieting theories that Trump pushed for the policy that would exempt false claims in his ads.

Zuckerberg defended the policy to Rep. Alexandria Ocasio-Cortez (D-NY), saying “I think lying is bad, and I think if you were to run an ad that had a lie, that would be bad,” but that outside of calls for violence or voter suppression, Facebook thinks it’s best to leave lies in ads from politicians so they can be scrutinized by the press and public. Yet that too heavily leans on the media to scrutinize thousands of ad variants being run as part of multi-hundred-million-dollar political ad campaigns.

Rep. Ann Wagner (R-MO) chided Zuckerberg, saying “you’re not working hard enough” to stop the spread of child exploitation imagery online despite Facebook submitting millions of reports. She brought up worries that Facebook moving entirely to encrypted messaging could hide child abusers, and Zuckerberg merely said “I think we work harder than any other company.” He failed to explain how Facebook would continue improving detection through encryption.

Oddly, Zuckerberg was directly confronted about his views on vaccines since Facebook works to hide vaccine hoaxes and avoid recommending groups spreading unverified information about them. “I don’t think it would be possible for anyone to be 100% confident, but my understanding of the scientific consensus is that it is important that people get their vaccines,” Zuckerberg said, defending Facebook’s decision to hide some of this content.

In another strange moment, Rep. Madeleine Dean (D-PA) demanded if Facebook had bought blocks of hotel rooms at Trump properties but never used them just to curry favor with the president. Zuckerberg said he’d never heard of that and would be surprised if it was true.

On deepfakes, Zuckerberg confirmed that “I think deepfakes are clearly one of the emerging threats that we need to get in front of and develop policy around to address. We’re currently working on what the policy should be to differentiate between media that has manipulated and been manipulated by AI tools like deepfakes, with the intent to mislead people.” Zuckerberg later said the doctored Nancy Pelosi video should have been flagged sooner, and highlighted Facebook needs a separate deepfakes policy. Yet Facebook’s policy allows politicians’ ads to mislead people, weakening faith that it will properly address this new problem.

Questions about Facebook’s fair practices led Zuckerberg to reiterate his call for regulation, saying “I think we need federal privacy legislation. I think we need data portability legislation. I think clear rules on elections-related content would be helpful too because it’s not clear to me that we want private companies making so many decisions on these important areas by themselves.”

Regarding housing discrimination via Facebook ads, Zuckerberg committed to working with regulators to provide information under subpoena, noted Facebook has banned discriminatory housing ads, and said “Nobody wants to redline and I’m sure that was accidental.”

Zuckerberg received his heaviest criticism of the day from Rep. Joyce Beatty (D-OH), who grilled him about not knowing if diverse bankers manage Facebook’s cash or if diverse law firms handle its court cases. She chastised Facebook for a lack of diverse leadership, saying “this is appalling and disgusting to me.” Of COO Sheryl Sandberg, who leads Facebook’s civil rights task force, Beatty said “we know she’s not really civil rights.”

WASHINGTON, DC – OCTOBER 23: Facebook co-founder and CEO Mark Zuckerberg arrives to testify before the House Financial Services Committee in the Rayburn House Office Building on Capitol Hill October 23, 2019 in Washington, DC. Zuckerberg testified about Facebook’s proposed cryptocurrency Libra, how his company will handle false and misleading information by political leaders during the 2020 campaign and how it handles its users’ data and privacy. (Photo by Chip Somodevilla/Getty Images)

Some of the day’s most astute questioning came from Congresswoman Katherine Porter (D-CA). She hammered Zuckerberg about Facebook lawyers fighting to avoid liability over data breaches. Then she trapped Zuckerberg on the issue of the mental health harms of being a Facebook content moderator that reviews horrific and graphic violence.

“Would you be willing to commit to spending one hour a day for the next year, watching these videos and acting as a content monitor and only accessing the same benefits available to your workers?,” she asked. “I’m not sure that would serve our community for me to spend my time,” Zuckerberg said. “What you’re saying is you’re not willing to do it,” she replied.

Rep. Katie Porter challenges Mark Zuckerberg to work as a content moderator and view the same violent, disturbing videos Facebook contractors do https://t.co/iVB9nAcvHO pic.twitter.com/TfPuXkiJp8

— Bloomberg Technology (@technology) October 23, 2019

There’ll be more major launches from Facebook that could raise questions about its impact on society, Zuckerberg revealed. “Later this week we actually have a big announcement coming up on launching a big initiative around news and journalism, where we’re partnering with a lot of folks to build a new product that’s supporting high-quality journalism.” Facebook plans to launch a News section featuring headlines from top outlets, though only some will be paid.

“I think that there’s an opportunity within Facebook in our services to build a dedicated surface, a tab within the apps for example, where people who really want to see high quality curated news, not just social content . . . I’m looking forward to discussing that in more length in the coming days.” That service is sure to trigger debates about whether Facebook is trustworthy enough to be a formal conduit for news.

Overall, the questioning today was much more intelligent than the vague and easily-Googleable queries launched at Zuckerberg by Congress in April 2018. We had no “Senator, we run ads” moments. Instead, it was Zuckerberg who repeatedly used the separation between Facebook and the Libra Association plus the fact that Libra’s policies are still being defined to avoid giving many substantial answers. Combined with the short five-minute Q&A period per member of Congress, Zuckerberg was often able to just repeat existing talking points.

WASHINGTON, DC – OCTOBER 23: Facebook co-founder and CEO Mark Zuckerberg testifies before the House Financial Services Committee in the Rayburn House Office Building on Capitol Hill October 23, 2019 in Washington, DC. Zuckerberg testified about Facebook’s proposed cryptocurrency Libra, how his company will handle false and misleading information by political leaders during the 2020 campaign and how it handles its users’ data and privacy. (Photo by Chip Somodevilla/Getty Images)

In one of the few lighthearted moments of the day, Rep. Juan Vargas recognized the tough position Zuckerberg has gotten himself into. “It’s good to have someone that’s sturdy and resilient. You’re probably the right person at the right time to take this beating.” Yet Rep. McHenry depressingly concluded that, after six hours, “I’m not sure we’ve learned anything new here.”

The question is what array of Libra and Facebook executives would Congress need to have testify together to get real answers to critical questions about how to keep the two from harming the global economy.

The hearing is ongoing and we’ll continue to update this article with major take-aways.

Powered by WPeMatico

There’s a strategic cost to the defection of Visa, Stripe, eBay, and more from the Facebook -led cryptocurrency Libra Association . They’re not just names dropping off a list. Each potentially made Libra more useful, ubiquitous, or reputable. Now they could become obstacles to the token’s launch or growth.

Fearing regulators’ inquiries not just into their Libra involvement but the rest of their businesses, these companies are pulling out at least for now. None had made precise commitments to integrating Libra into their products, and they’ve said they could still get involved later. But their exit clouds the project’s future and leaves Facebook to absorb more of the blowback.

Here’s what each of the departing Libra Association members brought to the table and how they could spawn new challenges for the cryptocurrency:

With one of most widely-accepted payment methods, Visa could have helped make Libra universally spendable. It’s also one of the most prestigious names in finance, lending deep credibility to the project. Visa’s departure leaves Libra looking more like tech companies barging into payments, conjuring fears of their move fast, break things approach that could cause financial ruin if Libra runs into problems. It also could leave Libra with a much weaker presence in brick-and-mortar shops. No one will want to own a cryptocurrency that doesn’t appreciate in value and can’t be easily spent.

The involvement of MasterCard alongside Visa made Libra look like the incumbents adapting to modern technologies. This made it less threatening, and gave cryptocurrency an air of inevitability. MasterCard would have also brought an even wider network of locations where Libra could one day be used for payment. Now MasterCard and Visa might actively work against Libra to prevent their payment methods being made obsolete by Libra and its elimination of transaction fees through the blockchain. Two of Libras biggest allies could become its biggest foes.

Facebook has repeatedly told regulators that its Calibra app plus integrations into Messenger and WhatsApp would not be the only Libra wallets, pointing to PayPal . Facebook’s head of Libra David Marcus told Congress when asked about the social network’s outsized power to exploit Libra through its own Calibra wallet that “you have companies like PayPal and others that will, of course, collaborate, but [also] compete with us”. Now Facebook won’t have a scaled payment method it doesn’t own to point to as a likely alternative for people who don’t want to trust Facebook’s Calibra, Messenger, or WhatsApp to be their Libra wallet. The Libra Association also loses PayPal’s enormous network of online merchants that accept it, plus the inroad to integration into its peer-to-peer payback app Venmo. PayPal convinced the mainstream public to trust online payments — the exact kind of trust Facebook desperately needs. The fact that Marcus was also the former president of PayPal but couldn’t keep it in the association raises concerns about the group’s coalition-building prowess.

Stripe’s enormous popularity with ecommerce vendors made it a valuable Libra Association member. Together with PayPal, Stripe facilitates a huge portion of online transactions outside of China. Its ease of integration made it a top pick for developers Facebook surely hoped would build atop Libra. Stripe’s exit destroys a critical bridge to the fintech startup ecosystem that could have helped institutionalize Libra. Now the association will have to work on engineering payment widgets from scratch without Stripe’s assistance, which could slow adoption if it ever launches.

There’s a clear reason all these payment processors bailed. Senators Brian Schatz (D-HI) and Sherrod Brown (D-OH) wrote a letter to Visa, MasterCard, and Stripe’s CEOs this week explaining that “If you take this on, you can expect a high level of scrutiny from regulators not only on Libra-related activities, but on all payment activities.”

As one of the longest standing ecommerce companies, eBay bolstered beliefs that Libra could be used to power transactions between untrusted strangers without a costly middleman. It might have also put Libra into practice on one of the top western online marketplaces outside of Amazon. Without destinations like eBay onboard, average netizens will have fewer opportunities to be exposed to Libra’s potential to eliminate transaction fees.

One of the lesser-known Libra Association members, Mercado Pago helps merchants receive payments via email or in installments. The idea of connecting financially underserved populations has been core to Facebook’s pitch for why Libra should exist. The Libra Association has been light on the details of how exactly it serves this demographic, relying on the inclusion of partners like Mercado Pago to help it figure this out later. Mercado Pago’s departure leaves Libra looking more like a financial power grab rather than a tool to assist the disadvantaged.

On Monday, the remaining Libra Association members will meet to finalize the initial member list, elect a board, and create a charter to govern the project. This forced the hands of the companies above, who had their last chance to depart this week before being pulled deeper into Libra.

UNITED STATES – JULY 16: David Marcus, head of Facebook’s Calibra digital wallet service, prepares to testify during the Senate Banking, Housing and Urban Affairs Committee hearing on “Examining Facebook’s Proposed Digital Currency and Data Privacy Considerations” on Tuesday, July 16, 2019. (Photo By Bill Clark/CQ Roll Call)

Who’s left includes venture capital firms, ride sharing companies, non-profits, and cryptocurrency companies. They are less tied up with the status quo of payment processing, and therefore had less to lose. The blockchain-specific companies were likely hoping to piggyback on financial giants like Visa to get Libra approved and create more legitimacy for their industry as a whole.

These partners could help fund an ecosystem of Libra developers, create daily use cases, spread the system in the developing world, and push for alliances between Libra and cryptocurrency players. Facebook will need to fight to keep them aboard if it wants to avoid Libra looking like a unilateral disruption of the economy.

For Libra to actually launch, Facebook needs to make serious concessions and divert from its initial vision. Otherwise if it continues to butt heads with regulators, more members could flee. One option floated by Libra Association member Andreessen Horowitz’s a16z Crypto partner Chris Dixon was for Libra to be denominated in US dollars instead of a basket of international currencies. That might lessen fears that Libra intends to compete directly with the dollar.

It’s become apparent that Facebook will not get its ideal cryptocurrency out the door. This is the brand tax of 100 scandals coming back to bite it. Now the best it can hope for is to get even a watered-down version launched, prove it can actually help the underbanked, and then hope to convince regulators it’s well-intentioned.

Powered by WPeMatico

Facebook will only build its own Calibra cryptocurrency wallet into Messenger and WhatsApp, and will refuse to embed competing wallets, the head of Calibra David Marcus told the Senate Banking Committee today. While some, like Senator Brown, blustered that “Facebook is dangerous!,” others surfaced poignant questions about Libra’s risks.

Calibra will be interoperable, so users can send money back and forth with other wallets, and Marcus committed to data portability so users can switch entirely to a competitor. But solely embedding Facebook’s own wallet into its leading messaging apps could give the company a sizable advantage over banks, PayPal, Coinbase or any other potential wallet developer.

Other highlights from the “Examining Facebook’s Proposed Digital Currency and Data Privacy Considerations” hearing included Marcus saying:

But Marcus also didn’t clearly answer some critical questions about Libra and Calibra, and may be asked again when he testifies before the House Financial Services Committee tomorrow.

Chairman Crapo asked if Facebook would collect data about transactions made with Calibra that are made on Facebook, such as when users buy products from businesses they discover through Facebook. Marcus instead merely noted that Facebook would still let users pay with credit cards and other mediums as well as Calibra. That means that even though Facebook might not know how much money is in someone’s Calibra wallet or their other transactions, it might know how much they paid and for what if that transaction happens over their social networks.

Senator Tillis asked how much Facebook has invested in the formation of Libra. TechCrunch has also asked specifically how much Facebook has invested in the Libra Investment Token that will earn it a share of interest earned from the fiat currencies in the Libra Reserve. Marcus said Facebook and Calibra hadn’t determined exactly how much it would invest in the project. Marcus also didn’t clearly answer Senator Toomey’s question of why the Libra Association is considered a not-for-profit organization if it will pay out interest to members.

Senator Menendez asked if the Libra Association would freeze the assets if terrorist organizations were identified. Marcus said that Calibra and other custodial wallets that actually hold users’ Libra could do that, and that regulated off-ramps could block them from converting Libra into fiat. But this answer underscores that there may be no way for the Libra Association to stop transfers between terrorists’ non-custodial wallets, especially if local governments where those terrorists operate don’t step in.

Perhaps the most worrying moment of the hearing was when Senator Sinema brought up TechCrunch’s article citing that “The real risk of Libra is crooked developers.” There I wrote that Facebook’s VP of product Kevin Weil told me that “There are no plans for the Libra Association to take a role in actively vetting [developers],” which I believe leaves the door open to a crypto Cambridge Analytica situation where shady developers steal users money, not just their data.

Senator Sinema asked if an Arizonan was scammed out of their Libra by a Pakistani developer via a Thai exchange and a Spanish wallet, would that U.S. citizen be entitled to protection to recuperate their lost funds. Marcus responded that U.S. citizens would likely use American Libra wallets that are subject to protections and that the Libra Association will work to educate users on how to avoid scams. But Sinema stressed that if Libra is designed to assist the poor who are often less educated, they could be especially vulnerable to scammers.

Here @SenatorSinema cites my article warning that we need protection from Facebook Libra’s unvetted developers https://t.co/gYeYIQVFLj pic.twitter.com/QSqVDztpCU

— Josh Constine (@JoshConstine) July 16, 2019

Overall, the hearing was surprisingly coherent. Many Senators showed strong base knowledge of how Libra worked and asked the right questions. Marcus was generally forthcoming, beyond the topics of how much Facebook has invested in the Libra project and what data it will glean from transactions atop its social network.

Some of the top concerns, such as terrorist money laundering, encompass the entire cryptocurrency ecosystem and can’t be solved even by strong rules around Libra. Little regard was given to how Libra could improve remittance or cut transaction fees that see corporations profit off families and small businesses.

Still, if Libra actually becomes popular and evolves as an open ecosystem full of unvetted developers, the currency could be used to facilitate scams. Precisely because of the lack of trust in Facebook that many Senators harped on, consumers could go seeking Libra wallet alternatives to the company that might push them into the hands of evildoers. The Libra Association may need to shift the balance further toward safety and away from cryptocurrency’s prevailing philosophies from openness. Otherwise, the frontiers of this Wild West could prove dangerous, even if its civilized regions are well-regulated.

Powered by WPeMatico

The head of Facebook’s blockchain subsidiary Calibra David Marcus has released his prepared testimony before Congress for tomorrow and Wednesday, explaining that the Libra Association will be regulated by the Swiss government because that’s where it’s headquartered. Meanwhile, he says the Libra Association and Facebook’s Calibra wallet intend to comply will all U.S. tax, anti-money laundering and anti-fraud laws.

“The Libra Association expects that it will be licensed, regulated, and subject to supervisory oversight. Because the Association is headquartered in Geneva, it will be supervised by the Swiss Financial Markets Supervisory Authority (FINMA),” Marcus writes. “We have had preliminary discussions with FINMA and expect to engage with them on an appropriate regulatory framework for the Libra Association. The Association also intends to register with FinCEN [The U.S. Treasury Department’s Financial Crimes Enforcement Network] as a money services business.”

Marcus will be defending Libra before the Senate Banking Committee on July 16th and the House Financial Services Committees on July 17th. The House subcomittee’s Rep. Maxine Waters has already issued a letter to Facebook and the Libra Association requesting that it halt development and plans to launch Libra in early 2020 “until regulators and Congress have an opportunity to examine these issues and take action.”

The big question is whether Congress is savvy enough to understand Libra to the extent that it can coherently regulate it. Facebook CEO Mark Zuckerberg’s testimonies before Congress last year were rife with lawmakers dispensing clueless or off-topic questions.

Sen. Orin Hatch infamously demanded to know “how do you sustain a business model in which users don’t pay for your service?,” to which Zuckerberg smirked, “Senator, we run ads.” If that concept trips up Congress, it’s hard to imagine it grasping a semi-decentralized stablecoin cryptocurrency that took us 4,000 words to properly explain, and a six-minute video just to summarize.

Attempting to assuage a core concern that Libra is trying to replace the dollar or meddle in financial policy, Marcus writes that “The Libra Association, which will manage the Reserve, has no intention of competing with any sovereign currencies or entering the monetary policy arena. It will work with the Federal Reserve and other central banks to make sure Libra does not compete with sovereign currencies or interfere with monetary policy. Monetary policy is properly the province of central banks.”

Marcus’ testimony comes days after President Donald Trump tweeted Friday to condemn Libra, claiming that “Unregulated Crypto Assets can facilitate unlawful behavior, including drug trade and other illegal activity. Similarly, Facebook Libra’s ‘virtual currency’ will have little standing or dependability. If Facebook and other companies want to become a bank, they must seek a new Banking Charter and become subject to all Banking Regulations, just like other Banks, both National and International.”

TechCrunch asked Facebook for a response Friday, which it declined to provide. However, a Facebook spokesperson noted that the Libra Association won’t interact with consumers or operate as a bank, and that Libra is meant to be a complement to the existing financial system.

Regarding how Libra will comply with U.S. anti-money laundering (AML) and know-your-customer (KYC) laws, Marcus explains that “The Libra Association is similarly committed to supporting efforts by regulators, central banks, and lawmakers to ensure that Libra contributes to the fight against money laundering, terrorism financing, and more,” Marcus explains. “The Libra Association will also maintain policies and procedures with respect to AML and the Bank Secrecy Act, combating the financing of terrorism, and other national security-related laws, with which its members will be required to comply if they choose to provide financial services on the Libra network.”

He argues that “Libra should improve detection and enforcement, not set them back,” because cash transactions are frequently used by criminals to avoid law enforcement. “A network that helps move more paper cash transactions—where many illicit activities happen—to a digital network that features regulated on- and off-ramps with proper know-your-customer (KYC) practices, combined with the ability for law enforcement and regulators to conduct their own analysis of on-chain activity, will present an opportunity to increase the efficacy of financial crimes monitoring and enforcement.”

As for Facebook itself, Marcus writes that “The Calibra wallet will comply with FinCEN’s rules for its AML/CFT program and the rules set by the Office of Foreign Assets Control (OFAC) . . . Similarly, Calibra will comply with the Bank Secrecy Act and will incorporate KYC and AML/CFT methodologies used around the world.”

These answers might help to calm finance legal eagles, but I expect much of the questioning from Congress will deal with the far more subjective matter of whether Facebook can be trusted after a decade of broken privacy promises, data leaks and fake news scandals like Cambridge Analytica.

That’s why I don’t expect the following statement from Marcus about how Facebook has transformed the state of communication will play well with lawmakers that are angry about how those changes impacted society. “We have done a lot to democratize free, unlimited communications for billions of people. We want to help do the same for digital currency and financial services, but with one key difference: We will relinquish control over the network and currency we have helped create.” Congress may interpret “democratize” as “screw up,” and not want to see the same happen to money.

Facebook and Calibra may have positive intentions to assist the unbanked who are indeed swindled by banks and money transfer services that levy huge fees against poorer families. But Facebook isn’t acting out of pure altruism here, as it stands to earn money from Libra in three big ways that aren’t mentioned in Marcus’ testimony:

The real-world stakes are much higher here than in photo sharing, and warrant properly regulatory scrutiny. No matter how much Facebook tries to distance itself from ownership of Libra, it started, incubated and continues to lead the project. If Congress is already convinced “big is bad,” and Libra could make Facebook bigger, that may make it difficult to separate their perceptions of Facebook and Libra in order to assess the currency on its merits and risks.

Below you can read Marcus’ full testimony:

For full details on how Libra works, read our feature story on everything you need to know:

Powered by WPeMatico

Facebook provided TechCrunch with new information on how its cryptocurrency will stay legal amidst allegations from President Trump that Libra could facilitate “unlawful behavior.” Facebook and Libra Association executives tell me they expect Libra will incur sales tax and capital gains taxes. They confirmed that Facebook is also in talks with local convenience stores and money exchanges to ensure anti-laundering checks are applied when people cash-in or cash-out Libra for traditional currency, and to let you use a QR code to buy or sell Libra in person.

A Facebook spokesperson said the company wouldn’t respond directly to Trump’s tweets, but noted that the Libra association won’t interact with consumers or operate as a bank, and that Libra is meant to be a complement to the existing financial system.

Trump had tweeted that “Unregulated Crypto Assets can facilitate unlawful behavior, including drug trade and other illegal activity. Similarly, Facebook Libra’s ‘virtual currency’ will have little standing or dependability. If Facebook and other companies want to become a bank, they must seek a new Banking Charter and become subject to all Banking Regulations, just like other Banks, both National and International.”

For a primer on how Libra works, watch our explainer video below or read our deep dive into everything you need to know:

In a wide-reaching series of interviews this week, the Libra Association’s head of policy Dante Disparte, Facebook’s head economist for blockchain Christian Catalini and Facebook’s blockchain project subsidiary Calibra’s VP of product Kevin Weil answered questions about regulation of Libra. Here’s what we’ve learned (their answers were trimmed for clarity but not edited):

Calibra’s Kevin Weil: We believe that creating a financial ecosystem that has significantly broader access where all it takes is a phone and lower transaction fees across the board is good for people. And we want to bring it to as many people around the world as we can. But as a custodial wallet we are regulated and will be compliant and we will only operate in markets where we’re allowed.

We want that to be as many markets as possible. That’s why we announced well in advance of actually launching a product — because we’ve been engaging with regulators. We’re continuing to engage with regulators and we can help them understand the effort that we’re taking to make sure that people are safe and also the value that accrues to the people in their countries when there’s broader access to financial services with lower transaction fees across the board.

TechCrunch: But what if you’re banned in the U.S.?

Weil: I’m hesitant to give a blanket answer. But in general, we believe that Libra is positive for people and we want to launch as broadly as possible. The world where the U.S. does that I think would probably cause other regulatory regimes to also be concerned about it. I think that’s very much a bridge that we’ll cross when we get there. But so far we’re having frank, open and honest discussions with regulators. Obviously, that continues next week with David’s testimony. And I hope it doesn’t come to that, because I think that Libra can do a lot of good for a lot of people.

TechCrunch’s Analysis: The U.S. House subcommittee has already submitted a letter to Facebook requesting that it cease development of Libra and Calibra until regulators can better examine it and take action. It sounds like Facebook believes a U.S. ban on Libra/Calibra would cause a domino effect in other top markets, and therefore make it tough to rationalize still launching. That puts even more pressure on the outcome of July 16th and 17th’s congressional hearings on Libra with the head of Facebook’s head of Calibra, David Marcus.

We already know that Facebook’s own Libra wallet called Calibra will be baked into Messenger and WhatsApp plus have its own standalone app. There, those with connected bank accounts and government ID that go through a Know Your Customer (KYC) anti-fraud/laundering check will be able to buy and sell Libra. But a big goal of Libra is to bring the unbanked into the modern financial system. How does that work?

Weil: Because Libra is an open ecosystem, any money exchange business or entrepreneur can begin supporting cash-in/cash-out without needing any permission from anyone associated with the Libra Association or member of the Libra Association. They can just do it. Today in a lot of emerging markets [there’s a service for matching you with someone to exchange cryptocurrency for cash or vice-versa called] LocalBitcoins.com and I think you’ll see that with Libra too.

Second, we can augment that by by working with local exchanges, convenience stores and other cash-in/cash-out providers to make it easy from within Calibra. You could imagine an experience in the Calibra app or within Messenger or WhatsApp, where if you want to cash in or cash out, you’ll pop up a map that highlights physical locations around that allow you to do it. You select one that’s nearby, you select an amount, and you get a QR code that you can take to them and complete the transaction.

I’d imagine that most of these businesses that we work with will support Libra more broadly, so even if we get these deals started it will benefit the whole ecosystem and every Libra wallet, not just Calibra.

TechCrunch: Have you struck relationships with any convenience store operators or money exchangers like Western Union or MoneyGram, or Walgreens, CVS or 7-Eleven? Are you in talks with them yet?

Weil: I probably shouldn’t comment on any specific deals but we’re in conversation with a lot of the folks you might think, because ultimately being able to move between Libra and your local currency is critical to driving adoption and utility in the early days . . . If you’re banked there are easier ways to do that. If you’re not banked and you’re in cash — those are the people we really want to serve with Libra — we’re working very hard to make that process easy for people.

TechCrunch’s analysis: This approach will let Calibra largely avoid the complicated and potentially error-prone process of KYCing people in person or handing out cash by offloading the responsibility and liability to other parties.

Weil: There are very important populations that don’t have an ID. People in a refugee camp may not, as an example, and we want Libra to serve them. So this is one example of many of why it’s important that Calibra isn’t the only option for people who want to participate in the Libra ecosystem . . . Others of these will be run by local providers and they have programs to meet customers face-to-face and other ways to serve people and even KYC them that we may not . . . We’re not going be the only wallet, we don’t want to be the only wallet.

This is one of the reasons NGOs have been members of the Libra association from the start, because we want to encourage the monetization of identity processes both through working with governments issuing credentials for more people and also making use of new types of information for identity and authentication. We hope this process will hep the last mile problem.

In the case of a non-custodial wallet, the user isn’t trusting anyone. The way the regulations have worked and this is evolving as we speak. The on-ramps and off-ramps to the crypto world are regulated and they have direct customer relationships and it’s their responsibility to KYC people. In our case we’ll be a custodial wallet and we’ll KYC people. There are a number of wallets in the Bitcoin or Ethereum ecosystem — non-custodial wallets that don’t have a direct relationships with the users. . . They have to get that Bitcoin somehow. Usually they’re going through an exchange where usually as part of the process they’re KYC’d.

In a lot of emerging markets you have LocalBitcoins.com where you can find a representative or agent who will meet you in person and exchange cash for bitcoin in whatever market you have to be in. And I believe that they just started making sure that they KYC everyone, but they’re doing it in person. And they have more flexibility in how they do it than you might otherwise. I think there are lots of ways that this will happen and the fact that Libra is an open ecosystem will enable people to be entrepreneurial about it.

There are lots an lots of people who are underserved by today’s financial ecosystem who have government ID. So even with requiring everyone go through a KYC process, we’ll be able to serve many, many people who are not well-served by today’s financial ecosystem. We want to find ways to support people who can’t KYC and the important part is that Calibra will fully interoperate with any other wallet, including ones that people in local markets are using because it’s a better fit for their needs.

TechCrunch: Through that interoperability, if someone with a non-custodial wallet receives Libra and then sends it a Calibra wallet user, does that mean you Libra coming into Calibra from users who weren’t KYC’d and could be laundering money?

Weil: So it’s part of the regulatory situation that’s evolving as we speak. There’s something called the Travel Rule . . . If there’s a transfer above a certain value you have to make sure that you understand both who the sender is, which you do if they’re using a custodial wallet, and who the receiver is. These are evolving regulations, but it’s something that obviously we’re going to make sure that we implement as regulations solidify.

TechCrunch’s Analysis: Calibra appears to be inviting regulation that it can strictly abide by rather than trying to guess at what the best approach is. But given it’s unclear when concrete rules will be established for transfers between non-custodial wallets and custodial wallets, or for in-person cashing, Facebook and Calibra may need to establish their own strong protocols. Otherwise they could be guilty of permitting the “unlawful behavior” Trump describes.

Dante Disparte of Libra: Taxing of digital assets is something that’s being designed at the local level and at the jurisdiction level. Our view of the world is that like with any form of money or any form of payment or banking, the onus in terms of compliance with tax is with the individual user and consumer, and the same would hold true broadly here.

We expect that the many, many wallets and financial services providers building solutions on the Libra blockchain would begin to provide tools that make it much easier than it is today [to calculate and file taxes] for digital assets and cryptocurrencies more generally . . . There’s plenty of time between now and Libra hitting the market to begin defining this more strictly at the jurisdictional level among providers.

TechCrunch’s Analysis: Again, here Facebook, Calibra and the Libra Association are hoping to avoid shouldering all the responsibility for taxes. Their position is that just as you have to take the initiative of paying your taxes whether or not you use a Visa card or your bank’s checks to transact, it’s on you to pay your Libra taxes.

TechCrunch: Do you think in the United States that it’s reasonable for the government to ask that Libra transactions be taxed?

Disparte: Tax treatments of digital assets broadly hasn’t been entirely clarified in most places around the world. And we hope that this is something that this project and the ecosystem around it helps to clarify.

Tax authorities will see a benefit from Libra at the consumption level and at the household level, while some cryptocurrencies have avoided taxes until the point they tried to cash out. But the nature of it and the lack of speculation and its design we think should give it a light tax treatment the way you would find with traditional currencies.

Christian Catalini of Facebook: Cryptocurrencies are taxed right now every time you have a sale on the differences in gains and losses. Because Libra is designed to be a medium of exchange, those gains and losses are likely to be very tiny relative to your local currency . . . Sales tax would likely be implemented the exact same way on Libra as it is today when you pay with a credit card.

At launch giving current regulations, the Calibra wallet will have to track every purchase and sale of Libra for a U.S. user and those differences will have to be reported on tax day. You can think of the losses, albeit they may be very small gains and losses relative to USD, as similar to the what people do today when they have a Coinbase account with Bitcoin.

The sales tax I think could be implemented in the exact same way as it today with any other sort of digital payment, it would be no different. If you’re buying goods or services with Libra you’ll be paying sales tax the same way as if you used a different form of payment. Like today when you see a percentage, that is the sales tax on your total.

Disparte: Maybe the best way to frame how taxes work all over the world is that it’s not up to Libra, Calibra, Facebook or any company to make that determination. It’s up to regulators and authorities.

TechCrunch: Does Calibra already have plans in place for how to handle sales tax?

Weil: That’s also a pretty rapidly evolving part of the regulatory ecosystem right now. It’s really an ongoing discussion. We will do whatever the regulation says we need to do.

TechCrunch’s Analysis: Here we have the firmest answers of our interviews. Facebook, Calibra and the Libra Association believe the proper approach to taxes is that Libra transactions carry a country’s traditional sales tax, and that Libra you hold in your wallet will have to pay taxes based on the Libra stablecoin’s value (that’s pegged to a basket of international currencies) relative to the U.S. dollar.

If the Libra Association recommends all wallets and transactions follow these rules and Calibra builds in protocols to handle these taxes simply, at least the government can’t argue Libra is a method of dodging taxes and everyone paying their fair share.

Powered by WPeMatico

Visa and Andreessen Horowitz are betting even bigger on cryptocurrency, funding a big round for fellow Facebook Libra Association member Anchorage’s omnimetric blockchain security system. Instead of using passwords that can be stolen, Anchorage requires cryptocurrency withdrawals to be approved by a client’s other employees. Then the company uses both human and AI review of biometrics and more to validate transactions before they’re executed, while offering end-to-end insurance coverage.

This new-age approach to cryptocurrency protection has attracted a $40 million Series B for Anchorage, led by Blockchain Capital and joined by Visa and Andreessen Horowitz. The round adds to Anchorage’s $17 million Series A that Andreessen led just six months ago, demonstrating extraordinary momentum for the security startup.

“As a custodian, our work is focused on building financial plumbing that other companies depend on for their operations to run smoothly. In this regard we have always looked at Visa as a model,” Anchorage co-founder and president Diogo Mónica tells me.

“Visa was ‘fintech’ before the term existed, and has always been on the vanguard of financial infrastructure. Visa’s investment in Anchorage is helpful not only to our company but to our industry, as a validation of the entire ecosystem and a recognition that crypto will play a key role in the future of global finance.”

Cold-storage, where assets are held in computers not connected to the internet, has become a popular method of securing Bitcoin, Ether and other tokens. But the problem is that this can prevent owners from participating in governance of certain cryptocurrency where votes are based on their holdings, or earning dividends. Anchorage tells me it’s purposefully designed to permit this kind of participation, helping clients to get the most out of their assets like capturing returns from staking and inflation, or joining in on-chain governance.

As three of the 28 founding members of the Libra Association that will govern the new Facebook-incubated cryptocurrency, Anchorage, Visa and Andreessen Horowitz will be responsible for ensuring the stablecoin stays secure. While Facebook is building its own custodial wallet called Calibra for users, other Association members and companies hoping to dive into the ecosystem will need ways to protect their Libra stockpiles.

“Libra is exactly the kind of asset that Anchorage was created to hold,” Mónica wrote the day Libra was revealed. “Our custody solution enables online participation with offline assets, so that asset-holders don’t face a trade-off between security and usability.” The company believes that custodians shouldn’t dictate which coins their clients hold, so it’s working to support all types of digital assets. Anchorage tells me that will include support for securing Libra in the future.

You’ve probably already used technology secured by Anchorage’s founders, who engineered Docker’s containers that are used by Microsoft, and Square’s first encrypted card reader. Mónica was at Square when he met his future Anchorage co-founder Nathan McCauley, who’d been working on anti-reverse-engineering tech for the U.S. military. When a company that had lost the password to a $1 million cryptocurrency account asked for their help with security, they recognized the need for a more idiot-proof take on asset protection.

“Anchorage applies the best of modern security engineering for a more advanced approach: we generate and store private keys in secure hardware so they are never exposed at any point in their life cycle, and we eliminate human operations that expose assets to risk,” Mónica says. The startup competes with other crypto custody firms like Bitgo, Ledger, Coinbase and Gemini.

Last time we spoke, Anchorage was cagey about what I could reveal regarding how its transaction validation system worked. With the new funding, it’s feeling a little more secure about its market position and was willing to share more.

Last time we spoke, Anchorage was cagey about what I could reveal regarding how its transaction validation system worked. With the new funding, it’s feeling a little more secure about its market position and was willing to share more.

Anchorage ditches usernames, passwords, email addresses and phone numbers completely. That way a hacker can’t just dump your coins into their account by stealing your private key or SIM-porting your number to their phone. Instead, clients whitelist devices held by their employees, who use the Anchorage app to submit transactions. You’d propose selling $10 million worth of Bitcoin or transferring it to someone else as payment, and a minimum of two-thirds of your designated co-workers would need to concur to form a quorum that approves the transfer.

But first, Anchorage’s artificial intelligence and human staff would check for any suspicious signals that might indicate a hack in progress. It uses behavioral analysis (do you act like a real human and similar to how you have before), biometric signals (do you look like you) and network signals (is your device what and where it should be) to confirm the transaction is legitimate. The same process goes down if you try to add a new whitelisted device or change who has permission to do what.

The challenge will be scaling security to an ever-broadening range of digital assets, each with their own blockchain quirks and complex smart contracts. Even if Anchorage keeps coins safely in custody, those variables could expose assets to risk while in transit. Now with deeper pockets and the Visa vote of confidence, Anchorage could solve those problems as clients line up.

While most blockchain attention has focused on the cryptocurrencies themselves and the exchanges where you can buy and sell them, a second order of critical infrastructure startups is emerging. Companies like Anchorage could make Bitcoin, Ether, Libra and more not just objects of speculation or the domain of experts, but safely functioning elements of the new world economy.

Powered by WPeMatico