lemonade

Auto Added by WPeMatico

Auto Added by WPeMatico

In the wake of insurtech unicorn Root’s IPO, it felt safe to say that the big transactions for the insurance technology startup space were done for the year.

After all, 2020 had been a big one for the broad category, with insurtech marketplaces raising lots, rental insurance startup Lemonade going public, Root itself debuting even more recently on the back of its automotive insurance business, a big round to help Hippo keep building its homeowners company and more.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But yesterday brought with it even more news: Metromile, a startup competing in the auto insurance market, is going public via a blank-check company (SPAC), and Hippo raised a huge, unpriced round.

So let’s talk about why Metromile might be plying the public markets, and why Hippo may have have decided to pick up more cash. Hint: The reasons are related.

So let’s talk about why Metromile might be plying the public markets, and why Hippo may have have decided to pick up more cash. Hint: The reasons are related.

The Lemonade IPO was a key moment for neoinsurance startups, a key part of the broader insurtech space. When the rental insurance provider went public, it helped set the tone for public exit valuations for companies of its type: fast-growing insurance companies with slick consumer brands, improving economics, a tech twist and stiff losses.

For the Roots and Metromiles and Hippos, it was an important moment.

So, when Lemonade raised its IPO range, and then traded sharply higher after its debut, it boded well for its private comps. Not that rental insurance and auto insurance or homeowners insurance are the same thing. They very most decidedly are not, but Lemonade’s IPO demonstrated that private investors were correct to bet generally on the collection of startups, because when they reached IPO-scale, they had something that public investors wanted.

Powered by WPeMatico

From a cluster of insurance marketplace startups raising capital earlier this year, to neoinsurance provider Lemonade going public this summer at a strong valuation, Hippo’s huge new round and Root’s impending unicorn IPO, 2020 has proven to be a busy year for startups and other growth-oriented private tech companies focused on insurance.

That news cycle continues today, with The Zebra announcing that it has reached a roughly $100 million run rate, and, perhaps even more notably, that it has turned profitable.

TechCrunch most recently covered the car and home insurance marketplace startup in February, when it raised the first $38.5 million in a Series C eventually worth $43.5 million that Accel led. As we noted at the time, the startup joined “Insurify ($23 million), Gabi ($27 million) and Policygenius ($100 million) in raising new capital this year.”

The Zebra released a number of financial performance metrics as part of its Series C cycle, including that it recorded revenues of $37 million in 2019, and that it had reached a $60 million annual run rate around the time of its Series C. The Zebra also said that it could double in size this year, putting it above a $100 million run rate by the end of 2020.

With that history in hand, let’s talk about the company’s more recent performance.

According to the company, The Zebra recorded net revenue of $6 million in May, 2020. That number grew to around $8 million in September. For those of you able to multiply, $8 million times 12 is $96 million, or a hair under $100 million. According to a call with the The Zebra’s CEO Keith Melnick, the company’s September was very close to $8.3 million, a figure that would put it on a $100 million run rate.

Given that our $100 million ARR club has a history of granting startups a little wiggle room when it comes to their size, it seems perfectly fine to say that The Zebra has reached revenue scale of $100 million; at its current rate of growth, even if its final September revenue tally is a hair light. the company should reach a nine-figure topline pace in October.

According to Melnick, while the bulk of The Zebra’s revenue isn’t recurring, a growing portion of it is. Per the CEO, around 2-5% of The Zebra’s revenue was recurring last year, a figure that he said is up to around 10% today. (If The Zebra binds an insurance policy itself, and that policy is renewed, its commissions can recur.)

What drove the company’s quick 2020 growth? In part, the insurance market changed, with insurance networks that depended on in-person sales seeing their ability to drive business slow thanks to COVID-19. Insurance marketplaces like The Zebra stepped in to assist, helping move some offline demand online. Melnick detailed that dynamic to TechCrunch, adding that when certain advertising channels saw demand fall, his company was able to leverage inexpensive inventory.

A number of factors appear to have added to The Zebra’s rapid growth thus far in 2020. Our next question is whether other, related players in the insurtech startup space have seen similar acceleration. More on that in a few days.

Finally, regarding The Zebra, the company said that it is now profitable. Of course, profit is a squishy word in 2020, so we wanted to know precisely what the company meant by the statement. Per the company’s CEO, it is generating positive net income, the gold-standard for profitability as the metric is inclusive of all costs, including the non-cash expenses that startups tend to strip out of their numbers to make the results look better than they really are.

If other players in the insurtech space are surfing similar trajectories, all that capital that went into the sector around the start of the year is going to appear prescient.

Powered by WPeMatico

During the week’s news cycle one particular bit of reporting slipped under our radar: Root Insurance is tipped by Reuters to be prepping an IPO that could value the neo-insurance provider at around $6 billion.

Coming after two 2020 insurtech IPOs, Root’s steps toward the public markets are not surprising. But they are good news all the same for a number of insurance startups that have raised lots of capital and will eventually need to prepare their own debuts if they don’t find a larger corporate home.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Programming note: The Exchange column is off starting tomorrow through next week. The newsletter will go out as always on Saturdays. I’m taking a week to sit and do nothing.

The Root IPO will also help clarify Lemonade’s own public offering and ensuing valuation. Lemonade’s debut brought a strong price to the rental-focused insurance provider, leading to a more buoyant attitude toward the valuation of its class of startups. More precisely, the public price assigned to Lemonade when it floated was, no bullshit, very bullish.

If Root can repeat the feat it would cast a warm light on the yet-private players in its niche that will have their eyes pinned to the flotation. Names like MetroMile and Hippo could be next if Root’s IPO goes well.

If Root can repeat the feat it would cast a warm light on the yet-private players in its niche that will have their eyes pinned to the flotation. Names like MetroMile and Hippo could be next if Root’s IPO goes well.

But, first, does Root make sense at a $6 billion valuation? We can do a little digging on that this morning, using Lemonade’s present-day valuation to get a handle on the figure. Let’s go!

Before we get into the numbers, bear in mind that we’re going to compare apples and oranges today, and that we’ll have to use some dated numbers as well. That said, we can still get somewhere about what Root could be worth. So, roll with me but don’t take every number as engraved onto an obelisk.

Back in July of this year, in the wake of the Lemonade IPO and Hippo’s latest funding round, a $150 million investment at a $1.5 billion post-money valuation, we started to do some math. Lemonade’s valuation was much richer than Hippos’ when you look at their multiples, which got us thinking about private and public neo-insurance provider valuations: Why was Lemonade worth so much more than its peers per dollar of written premium?

To better understand the situation, we dug up some 2019 data on the dollar value of gross written premium Hippo and Lemonade wrote and found new valuation multiples for them based on those numbers. Lemonade was worth 28.4x its Q1 annualized gross written premium, while Hippo was worth just 5.6x its own.

Then we also found Root and MetroMile gross written premium numbers for 2019, which allowed us to calculate their own effective valuations (albeit using dated numbers).

As before when we found that Hippo’s private valuation looked light compared to Lemonade’s public valuation when we contrasted their valuation/gross written premium multiple, we discovered that MetroMile and Root also looked cheap. Very cheap.

Powered by WPeMatico

Despite today’s bucket of plus-and-minus economic data, stocks are heading higher in regular trading. And among the shares rising the most are today’s two venture-backed IPOs: Lemonade and Accolade.

TechCrunch wrote this morning that the firms’ aggressive IPO pricing arcs boded well for the IPO market itself, that investors were willing to price growth-y shares of unprofitable companies with vigor, which could help other companies looking at the public markets get off the sidelines.

Then the two companies opened sharply higher, and at the current moment stand as follows (Data via Yahoo Finance):

Yep those are big numbers.

Expect the regular round of complaints that the firms were mispriced (maybe) and could have charged more from their equity in their public debuts (again, maybe). But for the two companies, it’s still a lovely day. Pricing above range and then seeing public investors frantically bid your equity higher is much better than the alternatives.

How the companies will fare when they report earnings (Q3 is upon us, making Q2’s earnings cycle just around the bend) will help settle their real valuations. But, for today at least, Lemonade and Accolade have done their yet-private brethren a solid by going up and not down.

Powered by WPeMatico

Earlier today, insurtech unicorn Lemonade filed an S-1/A, providing context into how the former startup may price its IPO and what the company may be worth when it begins to trade.

According to its new filing, Lemonade expects its IPO to price at $23 to $26 per share. As the company intends to sell 11 million shares in its debut, the rental and home insurance-focused unicorn would raise between $253 million and $286 million at those prices.

Counting an additional 1.65 million shares that it will make available to its underwriting banks, the company’s fundraise grows to $291 million to $328.9 million. Including shares offered to underwriters, Lemonade’s implied valuation given its IPO price range runs from $1.30 billion to $1.47 billion.

That’s the news. Now, is that expected valuation interval strong, and, if not, what might it portend for other insurtech startups? Let’s talk about it.

TechCrunch is speaking with the CEOs of Hippo (homeowner’s insurance) and Root (car insurance) later today, so we’ll get their notes in quick order regarding how Lemonade’s IPO is shaping up, and if they are surprised by its pricing targets.

But even without external commentary, the pricing range that Lemonade is at least initially targeting is not terribly impressive. That said, it’s stronger than I anticipated.

Powered by WPeMatico

While we await a fresh IPO filing from heavily backed insurtech startup Lemonade, let’s talk a little more about its public offering.

Since our first dig into its S-1 filing, TechCrunch has spoken to a number of investors and operators in Lemonade’s space to find out if our initial read was off — were we being too generous or too kind to Lemonade after reading its somewhat complex financial results?

The Exchange is a daily look at startups and the private markets for Extra Crunch subscribers; use code EXCHANGE to get full access and take 25% off your subscription.

The short answer is not really, though there are some positive notes and themes worth highlighting. This morning, let’s ask three questions about Lemonade’s IPO filing that will help us understand what’s ahead for the SoftBank-backed unicorn.

Three questions

Three questions1. How quickly can Lemonade accelerate its rental insurance graduation rate?

On the theme of things that bode well for Lemonade is its ability to “graduate” customers from low-cost rental insurance to more lucrative products.

In its S-1 filing, Lemonade noted this fact early on. After stating that a “an entry-level $60 a year [rental] policy [corresponds] to $10,000 of possessions,” the company said that as its customers age, they tend to buy more insurance and sometimes swap rental plans for homeowner policies. Moving from the former to the latter is graduating in the company’s parlance.

If many customers moved from rental insurance to homeowner insurance while keeping Lemonade as their provider, the company could do very well, as illustrated by this section of its SEC filing:

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

This time around we’re recording what we call an Equity Shot, a single-topic show that we pull together whenever there’s a news item of sufficient weight that it demands we break our regular cadence and record a little more.

So Danny and Tash and Alex got together to discuss the recent Vroom IPO and Lemonade filing to go public. These are topics that TechCrunch has covered quite a lot lately, so here’s a chronology to help you keep it all straight:

So you can catch up as you need to. What matters is that public investors have swooned over the Vroom IPO, pushing its pricing and, today, more than doubling its value as a public company. It’s a huge debut, and that bodes well for other gross-margin-light businesses — unicorns, even — that might want to go public.

The IPO window is pretty open, it appears. And best of all, we three disagreed quite a bit this week. It’s a fun show.

OK, that’s enough from us. We are back on Friday. Take care, and keep up the good fight.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Yesterday evening, Vroom, a digital used car retailer, priced its IPO at $22 per share, a figure that was a full $7 above the low end of its first proposed IPO price range. The venture-backed firm first proposed a $15 to $17 per-share IPO price range, which it later raised to $18 to $20 per share.

Pricing at $22 per share meant that there was strong demand for the company’s equity during its IPO process. Pricing strength doesn’t guarantee performance as a public company, but it does provide a proxy for investor interest.

TechCrunch has covered a few IPOs lately, noting along the way that some recent offerings have featured heavy financial backing and incredibly slim margins. Not profit margins, mind, those don’t exist for the firms we’re talking about — we’re discussing gross margins, the most basic element of corporate profitability.

Gross margins are part of why software companies are so valuable. Their incredibly strong gross margins make their revenues, and therefore their operations, attractive to investors; higher gross margins mean more money left over to cover expenses and redistribute to shareholders via dividends and buybacks. Lower gross margin businesses, in contrast, have less money once they are done paying for revenue costs, making it harder for those companies to cover operating costs, let alone give away leftover funds to their owners.

So it has been to our surprise that Kingsoft Cloud, Vroom, and, soon, Lemonade are seeing such strong responses. It’s perhaps even more surprising that these companies managed to raise as much private capital as they did in their youth, despite not sporting gross margins that track with what we expect from venture-backed, tech and tech-ish companies.

With markets at all-time highs — and thus comparable valuations contentedly stretched — it’s probably a great time to take low-margin, growth-y companies public. But that doesn’t mean the situation makes perfect financial sense.

Powered by WPeMatico

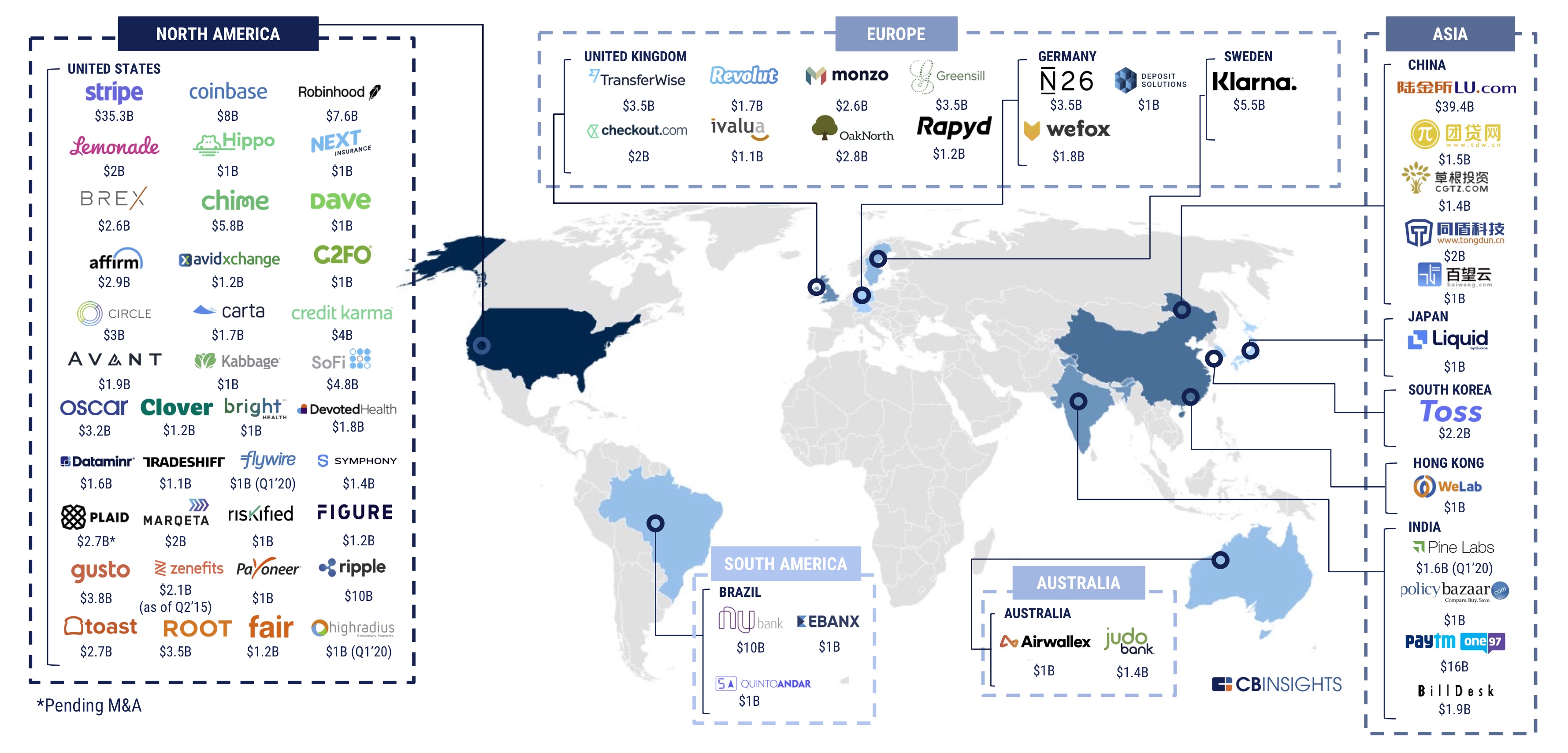

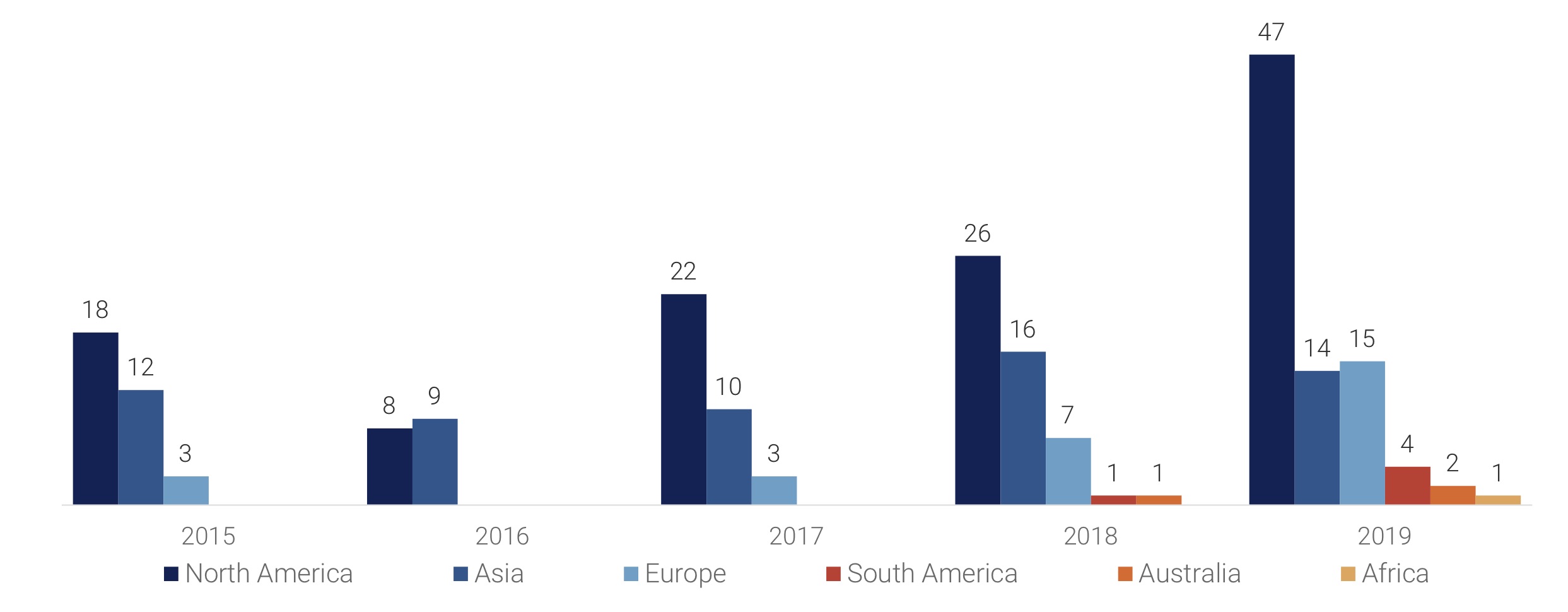

Financial services startups raised less money in 2019 than they did in 2018 as VC firms looked to back late stage firms and focused on developing markets, a new report has revealed.

According to research firm CB Insights’ annual report published this week, fintech startups across the world raised $33.9 billion* in total last year across 1,912 deals*, down from $40.8 billion they picked up by participating in 2,049 deals the year before.

It’s a comprehensive report, which we recommend you read in full here (your email is required to access it), but below are some of the key takeaways.

Early-stage deals dropped to a 12-quarter low as deal share globally shifts to mid- and late-stages (CB Insights)

The fintech market globally today has 67 unicorns as of earlier this month (CB Insights)

2019 saw 83 mega-rounds totaling $17.2B, a record year in every market except Europe

*CB Insights report includes a $666 million financing round of Paytm . It was incorrectly reported by some news outlets and the $666 million raise was part of the $1 billion round the Indian startup had revealed weeks prior. We have adjusted the data accordingly.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re adding four new names to the growing $100 million annual recurring revenue (ARR) club. The firms — Sisense, SiteMinder, Monday.com, and Lemonade — add diversity to our current group of yet-private companies which have reached the nine-figure recurring revenue threshold.

Our goal in tracking the companies in this high-flying cohort is to keep tabs on the private firms (often unicorns, it should be said) that could go public if needed. While not every unicorn will or could go public, companies with nine-figure ARR have a clear path to the public markets provided that their economics are in reasonable shape.

And we’ve seen some remarkably efficient companies meet the mark, including Egnyte with just $137.5 million raised, and Braze, with only $175 million on its books. For growth-oriented, venture-backed companies, those are efficient results.

But let’s add a few more members to the club today. Please meet our new centurions, centaurs, or whatever we end up calling them.

Sisense is a business intelligence company that merged with Periscope Data earlier this year. The combined firm has raised just over $200 million, according to Crunchbase, with the lion’s share of that landing in Sisense’s column (about $175 million).

What’s notable about the combination is that the two firms were public about saying that, when brought together, they would have combined ARR of $100 million. That was back in May. Today, Sisense has crested the $100 million mark by itself, according to an interview with TechCrunch. With Periscope added to the mix the company’s total ARR is naturally higher.

Sisense had a few original goals according to CEO Amir Orad, including helping businesses “take complex data and bring it together to get insights.” Its second focus is helping companies “take complex data sets and build [them out] as an analytical application in their products,” he said.

Periscope came into the picture when Orad and the smaller company’s CEO Harry Glaser (now Sisense’s CMO) started talking as friends about their respective markets. According to Orad, Glaser outlined a new sort of organization being built inside some companies that “were not traditional BI teams” or “traditional product teams,” but instead brought together “data engineers and data scientists and very capable individuals who [wanted] to make sense of [the] data sitting in the cloud.” Periscope had built “a very impressive business” supporting those new organizations, with “many hundreds of customers,” Orad said.

That meant that Sisense’s pair of focuses were somewhat two of out three, making the corporate combination an obvious bet.

Regarding what changed as Sisense grew, cresting the $50 million ARR mark and later the $100 million ARR mark, Orad told TechCrunch that what differed was “scale,” saying that at its size “what you do impacts more people, more individuals, more companies, [and] more customers.” (I have interesting notes on how the two companies managed their combination from a culture perspective, let me know if you’d like to read them.)

The first Australian member of the nine-figure ARR club is SiteMinder, which we’re letting in on a technicality; the firm’s ARR figure is in Australian dollars, which works out to around $70 million USD. However, its growth curve appears steep so we’re not too worried about including it a little early from a domestic dollar perspective.

Powered by WPeMatico