layoffs

Auto Added by WPeMatico

Auto Added by WPeMatico

Layoffs have struck the startup world swiftly, hurting hospitality and travel startups, as well as recruitment and scooter companies. New data shows that some of those layoffs, brought on by COVID-19, might be disproportionately impacting satellite campuses.

By nature, satellite offices are secondary to a startup’s headquarters. Opening smaller offices is a strategic move when a company gets a fresh round of funding or wants to expand to a new market. We’ve seen satellite offices pop up in cities like Portland, Phoenix or Austin, which has satellite offices for Apple, Facebook and Oracle, for example.

While most layoffs are coming from companies whose headquarters are located in the main entrepreneurial hubs of the Bay area and New York, the actual staff members are located in the satellite cities, according to data from Layoffs.fyi, a tracker created by former Y Combinator grad Roger Lee.

EasyPost in San Francisco laid off 75 employees, nearly all in Salt Lake City and Louisville. U.K.-based Challenger bank Monzo laid off 165 customer support employees recently in Las Vegas.

Toast, based in Boston, laid off 1,300 employees, or 50% of its entire staff. Per Layoffs.fyi data, 12% of those layoffs were in Omaha, and another 10% were in Chicago.

KeepTruckin, based in San Francisco and last valued at $1.25 billion, laid off around 350 employees, and 33% of those employees were located in Nashville or Chicago.

These numbers are only a fraction of the total layoffs across the country, as Layoffs.fyi’s data set only includes publicly disclosed actions and tips. But even if the data is just serving as an anecdotal snapshot, it’s an important one to note.

Once the economy does recover to a new normal, it’s unclear whether HQ cities or satellite cities will be in a better position to bounce back. We caught up with some investors in Boston, a top startup hub that has recently faced its own flurry of layoffs, to hear their thoughts.

According to Lily Lyman, a partner at Boston-based venture capital firm Underscore, satellite offices are often where a company might locate the sales, customer success and business development staff. Logistically, those roles are the most vulnerable as consumer activity slows. For a lot of businesses, there are no sales and deals to be done right now.

“[These roles are getting] disproportionately affected in [reduction of forces] as companies expect a slowdown on the commercial side,” Lyman said. “While a logical decision to extend the cash runway, it does come with the risk that this withdrawal can damage relationships with customers that may be hard to recover.”

Not everyone sees cuts hitting satellite offices the hardest. Michael Skok, another partner at Underscore, said that “in some cases, we’ve seen that satellite offices are established in emerging markets which come with cost savings, so these offices may actually be more protected in these times.” In other words, if you’re cutting costs, San Francisco employee expenses might be higher than Denver employee expenses by sheer nature of the former having exorbitantly high living costs. Revolution Ventures, which invests in startups in emerging tech scenes, said it has not heard about satellite office layoffs from its portfolio as of recently.

And finally, to put it crassly, layoffs in a non-HQ city might quell some of the negative signaling that founders and venture capitalists are trying so hard to avoid (well, most of them at least). Slimming down operations is becoming a proactive response, not a reactive strategy as the pandemic continues to evolve.

Today’s data reminds us that layoffs are rarely an isolated occurrence, and staff cuts appear to be landing harder on less robust tech ecosystems.

Powered by WPeMatico

Thumbtack CEO Marco Zappacosta announced in a blog post today that the company has laid off 250 employees.

Much has been written about the impact that COVID-19 and the resulting social distancing/shelter in place measures are having on small businesses (and the steps that internet platforms like Facebook and Yelp — which, after all, make money from small businesses advertising — are taking to help).

Similarly, Zappacosta said the local services that Thumbtack showcases in its marketplace are also seeing anything from a “dramatic decline” to an “outright collapse.” Apparently the company’s business has fallen 61% in San Francisco, 55% in Detroit and 50% in New York City.

Thumbtack raised a $150 million round of funding last year, but Zappacosta said, “No business operates with enough of a buffer to sustain prolonged revenue declines of 40%+ without making radical changes.”

Those changes include reduced marketing, a hiring freeze and 25% salary reductions for executives. (Zappacosta said he will not take any salary at all, starting today.) And it also includes big layoffs.

Laid off workers will receive a severance package with both “cash and equity components,” Zappacosta said. He also said Thumbtack is doing what it can to help its service providers, such as “building features that support more remote work with customers — like video consults for a sink replacement that would typically be done onsite.”

Powered by WPeMatico

Bird is the latest startup hit by the COVID-19 pandemic. Today, Bird laid off about 30% of its employees amid the uncertainty caused by the coronavirus, TechCrunch has learned.

“The unprecedented COVID-19 crisis has forced our leadership team and the board of directors to make many extremely difficult and painful decisions relating to some of your teammates,” Bird CEO Travis VanderZanden wrote to staffers in a memo, obtained by TechCrunch, today. “As you know, we’ve had to pause many markets around the world and drastically cut spending. Due to the financial and operational impact of the ongoing COVID-19 crisis, we are saying goodbye to about 30% of our team.”

Bird has confirmed the layoffs and says it is providing four weeks of pay, three months of health coverage* and an extended time frame of 12 months to exercise their stock options. According to a source, Bird’s balance sheet is strong but it needed to reduce burn in order to extend its runway into 2021.

Bird’s layoffs come shortly after news broke that Lime is looking for a funding round that would cut its valuation from $2.4 billion to $400 million.

Last week Bird and Lime suspended their respective services in response to the pandemic.

Bird is not the only startup forced to have layoffs amid the crisis. As The Information reported earlier this week, layoffs are accelerating across Silicon Valley. Meanwhile, Lime is reportedly considering laying off up to 70 people in the San Francisco Bay Area.

Here’s the full memo VanderZanden sent this morning:

We’ve watched the COVID-19 pandemic radically and quickly transform our lives, the world, and our business in less than a month. This once in a decade black swan event presents one of the greatest challenges in history because of the viral impact it has not just on our health, but also on our lives—our families, friends, communities, finances, work, emotions—the list goes on.

The unprecedented COVID-19 crisis has forced our leadership team and the board of directors to make many extremely difficult and painful decisions relating to some of your teammates. As you know, we’ve had to pause many markets around the world and drastically cut spending. Due to the financial and operational impact of the ongoing COVID-19 crisis, we are saying goodbye to about 30% of our team.

In business, I feel like every challenge is surmountable with the right team. And I believe Bird has been building the right team these past few years. Until today, there wasn’t a problem we couldn’t solve together. That’s what makes this such a painful situation. To say goodbye to some of the most incredible, intelligent, scrappy, funny, loving, dedicated members of our Bird Family for reasons totally outside our control, hurts deeply.

I recognize and sympathize that this situation adds to an already difficult time. As you know, we strive to be community-focused at Bird—we always try to care deeply about the people we serve. The impacted individuals are an important part of this community and I hope that our commitment to caring and supporting them during this transition by providing severance pay, extended health insurance, and an extended window to exercise options makes a positive impact during this crisis.

We looked at many different options and scenarios and took as many preventive measures as possible to reduce the impact of the virus. Given the unknown timeline and current economic situation, we were forced to cut back in this way to elongate the trajectory of Bird and our mission. As you know, we just raised hundreds of millions from investors, but given all the uncertainty, we needed to ensure a cash runway to last through the end of 2021.

Moving forward, together

As we all know: yes, the world has changed and continues to change. This will be a difficult season, but we continue to work around the clock to move us forward as a team. As mentioned last week, we’re aggressively shoring up resources and protecting our existing assets. We’ve curbed all spending company-wide that is not directly related to helping us weather this storm together. We appreciate all your help identifying unnecessary spend during this down time.

History also tells us something important: micromobility, especially scooters, will very likely have an important role to play as communities begin to get moving again in the wake of the COVID-19 pandemic.

This is not the first time that a public health crisis has had a direct impact on the micromobility industry. When the SARS outbreak was sweeping through China, e-bike sales surged as riders looked for more personalized alternatives to public transit.

History suggests that people will demand a large scale mobility option that still allows for personal distancing. And Bird will be there, working hand in hand with cities to help communities heal, and help riders regain mobility, in the wake of the most serious global pandemic in recent memory.

I just want to give a heartfelt thank you to everyone who has rallied to keep up with such a rapidly changing situation. We’ll try to keep everyone informed as it relates to changing priorities and business impact. We’ve had successes that allow businesses to persevere in times of uncertainty and, with your trust, patience and determination, we will overcome the challenges we face today as well.

Lean on each other. Over communicate. Support each other. Reach out to your teammates and managers to understand what you can do to keep us moving forward.

*An earlier version of this story said three weeks of health insurance instead of three months. We apologize for the error.

Powered by WPeMatico

The coronavirus demand crunch has taken another bite: Palo Alto-based corporate travel-focused unicorn TripActions has confirmed laying off hundreds of staff.

Per this post on Blind — written by someone with a verified TripActions email address — the company laid off 350 people. Business Insider reported the same figure yesterday, and the Wall Street Journal said the layoffs amount to between one-quarter to one-fifth of the startup’s total staff, citing a person familiar with the situation.

Update: A spokesman for TripActions told us the number of impacted employees impacted is “less than 300” — although he qualified the remark by saying the figure includes 25 people who were offered other roles within the company.

In an earlier email to Crunchbase News TripActions confirmed axing jobs in response to the COVID-19 global health crisis — saying it had “cut back on all non-essential spend.” It did not confirm exactly how many employees it had fired at that point.

“[We] made the very difficult decision to reduce our global workforce in line with the current climate,” TripActions wrote in the statement. “We look forward to when the strength of the global economy and business travel inevitably return and we can hire back our colleagues to rejoin us in our mission to make business travel effortless for our customers and users.”

“This global health crisis is unlike anything we’ve ever seen in our lifetimes, and our hearts go out to everyone impacted around the world, including our own customers, partners, suppliers and employees,” it added. “The coronavirus has had [a] wide-reaching effect on the global economy. Every business has been impacted including TripActions. While we were fortunate to have recently raised funding and secured debt financing, we are taking appropriate steps in our business to ensure we are here for our customers and their travelers long into the future.”

Per the post on Blind, TripActions is providing one week of severance to sacked staff and medical cover until end of month. “With [the coronavirus pandemic] going on you think they would do better,” the OP wrote. The layoffs were made by Zoom call, they also said.

However TripActions’ spokesman disputed the details about severance and medical cover, saying it is offering severance packages for U.S. employees that include two months of company-paid COBRA health insurance coverage, extending health benefits through the end of June, along with a minimum of 3 weeks salary.

He added that U.S. employees who were given notice yesterday were told their last day would be April 1, 2020 — meaning their health benefits continue through the end of April.

Travel startups are facing an unprecedented nuclear winter as demand has fallen off a cliff globally — with little prospect of a substantial change to the freeze on most business travel in the coming months as rates of COVID-19 infections continue to grow exponentially outside China.

However, TripActions is one of the highest valued and best financed of such startups, securing a $500 million credit facility for a new corporate product only last month. At the time, Crunchbase recorded $480 million in tracked equity funding for the company, including a $250M Series D TripActions raised in June from investors including a16z, Group 11, Lightspeed and Zeev Ventures.

Before the layoffs, the company had already paused all hiring, per one former technical sourcer for the company writing on LinkedIn.

This post was updated with additional comment from TripActions

Powered by WPeMatico

Boosted, the startup behind the Boosted Boards and, more recently, the Boosted Rev electric scooter, has laid off “a significant portion” of its team, the company announced today. The company is now actively seeking a buyer.

Boosted attributes the layoffs to the costs of developing, producing and maintaining electric vehicles and the “unplanned challenge with the high expense of the US-China tariff war,” Boosted CEO Jeff Russakow and CTO John Ulmen wrote in a blog post.

“The Boosted brand will continue to pursue strategic options under new ownership,” they wrote.

Boosted, which got its start back in 2012, made its first foray outside of electric skateboards last year with the launch of an electric scooter. Boosted says more than 100,000 riders have traveled tens of millions of miles on the company’s vehicles.

“We are extremely proud of what our company has accomplished, and gratified to see so many happy customers riding their Boosted vehicles every day,” Russakow and Ulmen wrote.

This perhaps should not come as a surprise. For starters, micromobility is a hard business — one that no company can confidently say it has cracked. Meanwhile, The Verge reported earlier this month that the company was at risk of running out of money. On top of that, Boosted reportedly struggled to pay its vendors for the electric scooter.

“To Boosted’s customers and community, we’d like to thank you for your passionate support and encouragement over the last nine years,” Ulmen and Russakow wrote. “It’s been the thrill of our lives to spend time with you and help shape the future of mobility together. To the Boosted team, you made this company a special place, created multiple generations of incredibly innovative products, and created a compelling global brand; thank you so much for your hard work and dedication over the years.”

Powered by WPeMatico

Fearing weak fundraising options in the wake of the WeWork implosion, late stage startups are tightening their belts. The latest is another Softbank-funded company, joining Zume Pizza (80% of staff laid off), Wag (80%+), Fair (40%), Getaround (25%), Rappi (6%), and Oyo (5%) that have all cut staff to slow their burn rate and reduce their funding needs. Freight forwarding startup Flexport that is laying off 3% of its global staff.

“We’re restructuring some parts of our organization to move faster and with greater clarity and purpose. With that came the difficult decision to part ways with around 50 employees” a Flexport spokesperson tells TechCrunch after we asked today if it had seen layoffs like its peers.

Flexport CEO Ryan Petersen

Flexport had raised a $1 billion Series D led by SoftBank at a $3.2 billion valuation a year ago, bringing it to $1.3 billion in funding. The company helps move shipping containers full of goods between manufacturers and retailers using digital tools unlike its old-school competitors.

“We underinvested in areas that help us serve clients efficiently, and we over-invested in scaling our existing process, when we actually needed to be agile and adaptable to best serve our clients, especially in a year of unprecedented volatility in global trade” the spokesperson explained.

Flexport still had a record year, working with 10,000 clients to finance and transport goods. The shipping industry is so huge that it’s still only the seventh largest freight forwarder on its top Trans-Pacific Eastbound leg. The massive headroom for growth plus its use of software to coordinate supply chains and optimize routing is what attracted SoftBank.

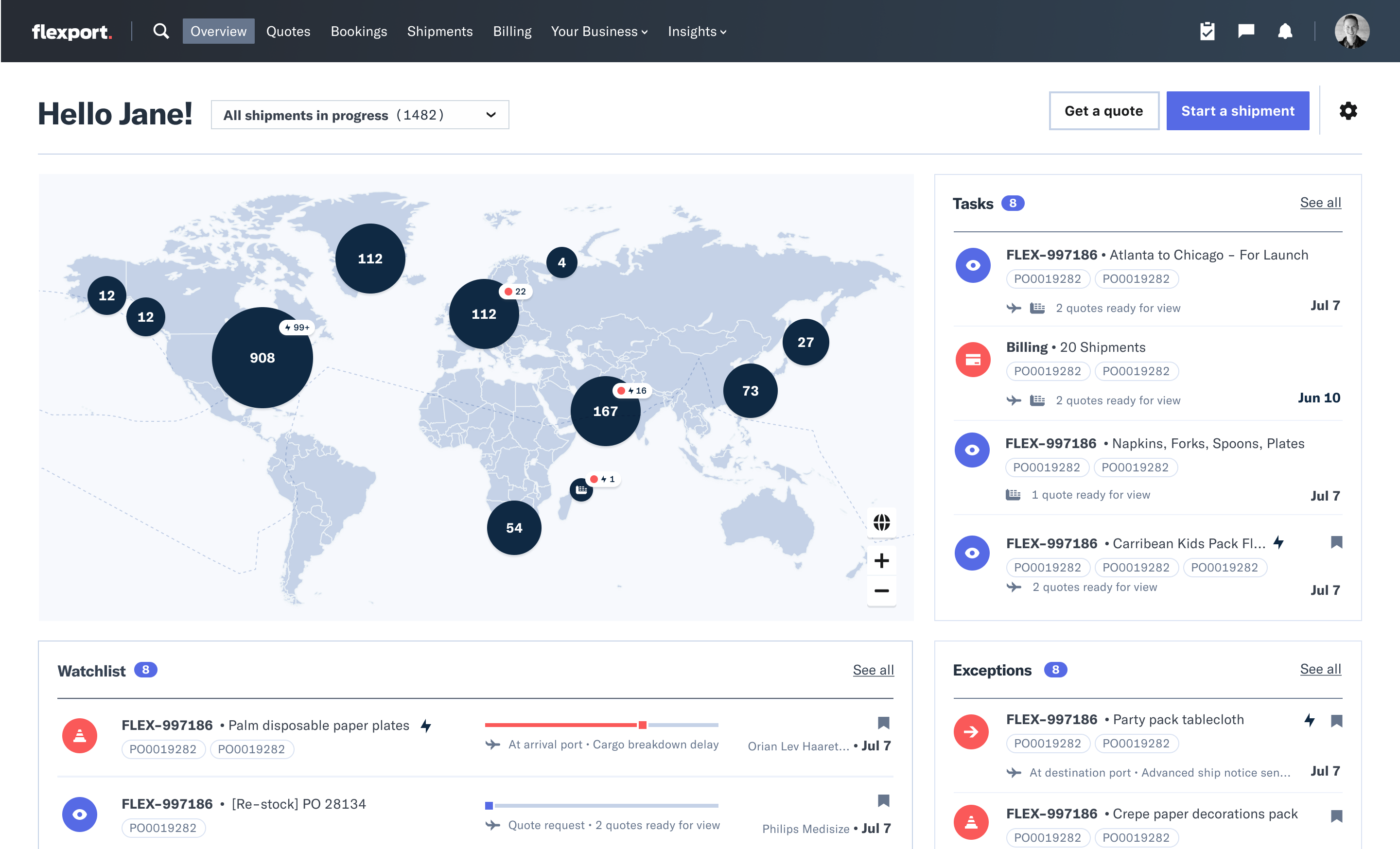

The Flexboard Platform dashboard offers maps, notifications, task lists, and chat for Flexport clients and their factory suppliers.

But many late-stage startups are worried about where they’ll get their next round after taking huge sums of cash from SoftBank at tall valuations. As of November, SoftBank had only managed to raise about $2 billion for its Vision Fund 2 despite plans for a total of $108 billion, Bloomberg reported. LPs were partially spooked by SoftBank’s reckless investment in WeWork. Further layoffs at its portfolio companies could further stoke concerns about entrusting it with more cash.

Unless growth stage startups can cobble together enough institutional investors to build big rounds, or other huge capital sources like sovereign wealth funds materialize for them, they might not be able to raise enough to keep rapidly burning. Those that can’t reach profitability or find an exit may face down-rounds that can come with onerous terms, trigger talent exodus death spirals, or just not provide enough money.

Flexport has managed to escape with just 3% layoffs for now. Being proactive about cuts to reach sustainability may be smarter than gambling that one’s business or the funding climate with suddenly improve. But while other SoftBank startups had to spend tons to edge out direct competitors or make up for weak on-demand service margins, Flexport at least has a tried and true business where incumbents have been asleep at the wheel.

Powered by WPeMatico

Quora, a 10-year-old question-and-answer startup based in Mountain View, is laying off staff in its Bay Area and New York offices, the company’s CEO announced on the site today.

Like other startup leaders being pushed by investors to focus more heavily on cash flow, CEO Adam D’Angelo wrote that the layoffs and “organizational changes” were being pursued in order to focus on “scaling the organization in a financially responsible way.”

D’Angelo did not disclose the scale of the layoffs. Recode reported last year that Quora was locking down $60 million at a $2 billion valuation, noting at the time that the startup had around 200 employees. The company has publicly disclosed $225 million to date according to Crunchbase, from investors including Benchmark, Peter Thiel and Y Combinator.

We’ve reached out to the company for additional comment.

“[W]e need to reduce our burn rate to a sustainable level from which we can focus on pursuing the mission and growing the business over the long term. We do not want to be dependent on outside capital, so self-reliance and careful management of our resources are crucial to our future,” D’Angelo wrote.

Over the past several weeks, layoffs have been hitting startups, including several in SoftBank’s portfolio as well as Mozilla and, just today, genetic testing startup 23andMe.

Powered by WPeMatico

Layoffs in the technology and venture-backed worlds continued today, as 23andMe confirmed to CNBC that it laid off around 100 people, or about 14% of its formerly 700-person staff. The cuts would be notable by themselves, but given how many other reductions have recently been announced, they indicate that a rolling round of belt-tightening amongst well-funded private companies continues. (TechCrunch confirmed the numbers with the company.)

Mozilla, for example, cut 70 staffers earlier this year. As TechCrunch’s Frederic Lardinois reported earlier in January, the company’s revenue-generating products were taking longer to reach market than expected. And with less revenue coming in than expected, its human footprint had to be reduced.

23andMe and Mozilla are not alone, however. Playful Studios cut staff just this week, 2019 itself saw more than 300% more tech layoffs than in the preceding year and TechCrunch has covered a litany of layoffs at Vision Fund-backed companies over the past few months, including:

Scooter unicorns Lime and Bird have also reduced staff this year. The for-profit drive is firing on all cylinders in the wake of the failed WeWork IPO attempt. WeWork was an outlier in terms of how bad its financial results were, but the fear it introduced to the market appears pretty damn mainstream by this point. (Forsake hope, alle ye whoe require a Series H.)

The money at risk, let alone the human cost, is high. Zume has raised more than $400 million. 23andMe has raised an even sharper $786.1 million. Rappi? How about $1.4 billion. And Oyo? $3.2 billion so far. Every company that loses money eventually dies. And every company that always makes money lives forever. It seems that lots of companies want to jump over the fence, make some money and rebuild investor confidence in their shares.

It’s just too bad that the rank-and-file are taking the brunt of the correction.

Powered by WPeMatico

After appointing a new CEO and CFO last summer, cloud infrastructure provider DigitalOcean is embarking on a wider reorganisation: the startup has announced a round of layoffs, with potentially between 30 and 50 people affected.

DigitalOcean has confirmed the news with the following statement:

“DigitalOcean recently announced a restructuring to better align its teams to its go-forward growth strategy. As part of this restructuring, some roles were, unfortunately, eliminated. DigitalOcean continues to be a high-growth business with $275M in [annual recurring revenues] and more than 500,000 customers globally. Under this new organizational structure, we are positioned to accelerate profitable growth by continuing to serve developers and entrepreneurs around the world.”

Before the confirmation was sent to us this morning, a number of footprints began to emerge last night, when the layoffs first hit, with people on Twitter talking about it, some announcing that they are looking for new opportunities and some offering help to those impacted. Inbound tips that we received estimate the cuts at between 30 and 50 people. With around 500 employees (an estimate on PitchBook), that would work out to up to 10% of staff affected.

It’s not clear what is going on here — we’ll update as and when we hear more — but when Yancey Spruill and Bill Sorenson were respectively appointed CEO and CFO in July 2019 (Spruill replacing someone who was only in the role for a year), the incoming CEO put out a short statement that, in hindsight, hinted at a refocus of the business in the near future:

“My aspiration is for us to continue to provide everything you love about DO now, but to also enhance our offerings in a way that is meaningful, strategic and most helpful for you over time.”

The company provides a range of cloud infrastructure services to developers, including scalable compute services (“Droplets” in DigitalOcean terminology), managed Kubernetes clusters, object storage, managed database services, Cloud Firewalls, Load Balancers and more, with 12 data centers globally. It says it works with more than 1 million developers across 195 countries. It has also been expanding the services that it offers to developers, including more enhancements in its managed database services, and a free hosting option for continuous code testing in partnership with GitLab.

All the same, as my colleague Frederic pointed out when DigitalOcean appointed its latest CEO, while developers have generally been happy with the company, it isn’t as hyped as it once was, and is a smallish player nowadays.

And in an area of business where economies of scale are essential for making good margins on a business, it competes against some of the biggest leviathans in tech: Google (and its Google Cloud Platform), Amazon (which as AWS) and Microsoft (with Azure). That could mean that DigitalOcean is either trimming down as it talks to investors for a new round; or to better conserve cash as it sizes up how best to compete against these bigger, deep-pocketed players; or perhaps to start thinking about another kind of exit.

In that context, it’s notable that the company not only appointed a new CFO last summer, but also a CEO with prior CFO experience. It’s been a while since DigitalOcean has raised capital. According to PitchBook data, DigitalOcean last raised money in 2017, an undisclosed amount from Mighty Capital, Glean Capital, Viaduct Ventures, Black River Ventures, Hanaco Venture Capital, Torch Capital and EG Capital Advisors. Before that, it took out $130 million in debt, in 2016. Altogether it has raised $198 million, and its last valuation was from a round in 2015, $683 million.

It’s been an active week for layoffs among tech startups. Mozilla laid off 70 employees this week; and the weed delivery platform Eaze is also gearing up for more cuts amid an emergency push for funding.

We’ll update this post as we learn more. Best wishes to those affected by the news.

Powered by WPeMatico

Seventy-five-million-dollar-funded legal services startup Atrium doesn’t want to be the next company to implode as the tech industry tightens its belt and businesses chase margins instead of growth via unsustainable economics. That’s why Atrium is laying off most of its in-house lawyers.

Now, Atrium will focus on its software for startups navigating fundraising, hiring and collaborating with lawyers. Atrium plans to ramp up its startup advising services. And it’s also doubling down on its year-old network of professional service providers that help clients navigate day-to-day legal work. Atrium’s laid-off attorneys will be offered spots as preferred providers in that network if they start their own firm or join another.

“It’s a natural evolution for us to create a sustainable model,” Atrium co-founder and CEO Justin Kan tells TechCrunch. “We’ve made the tough decision to restructure the company to accommodate growth into new business services through our existing professional services network,” Kan wrote on Atrium’s blog. He wouldn’t give exact figures, but confirmed that more than 10 but less than 50 staffers are impacted by the change, with Atrium having a headcount of 150 as of June.

The change could make Atrium more efficient by keeping fewer expensive lawyers on staff. However, it could weaken its $500 per month Atrium membership that included some services from its in-house lawyers that might be more complicated for clients to get through its professional network. Atrium will also now have to prove the its client-lawyer collaboration software can survive in the market with firms paying for it rather than it being bundled with its in-house lawyers’ services.

“We’re making these changes to move Atrium to a sustainable model that provides high-quality services to our clients. We’re doing it proactively because we see the writing on the wall that it’s important to have a sustainable business,” Kan says. “That’s what we’re doing now. We don’t anticipate any disruption of services to clients. We’re still here.”

Justin Kan (Atrium) at TechCrunch Disrupt SF 2017

Founded in 2017, Atrium promised to merge software with human lawyers to provide quicker and cheaper legal services. Its technology can help automatically generate fundraising contracts, hiring offers and cap tables for startups while using machine learning to recommend procedures and clauses based on anonymized data from its clients. It also serves like a Dropbox for legal, organizing all of a startup’s documents to ensure everything’s properly signed and teams are working off the latest versions without digging through email.

The $500 per month Atrium membership offered this technology plus limited access to an in-house startup lawyer for consultation, plus access to guide books and events. Clients could pay extra if they needed special help such as with finalizing an acquisition deal, or access to its Fundraising Concierge service for aid with developing a pitch and lining up investor meetings.

Kan tells me Atrium still has some in-house lawyers on staff, which will help it honor all its existing membership contracts and power its new emphasis on advising services. He wouldn’t say if Atrium is paid any equity for advising, or just cash. The membership plan may change for future clients, so lawyer services are provided through its professional network instead.

“What we noticed was that Atrium has done a really good job of building a brand with startups. Often what they wanted from attorneys was…advice on ‘how to set my company up,’ ‘how to set my sales and marketing team up,’ ‘how to get great terms in my fundraising process,’ ” so Atrium is pursuing advising, Kan tells me. “As we sat down to look at what’s working and what’s not working, our focus has been to help founders with their super-hero story, connect them with the right providers and advisors, and then helping quarterback everything you need with our in-house specialists.”

LawSites first reported Saturday that Atrium was laying off in-house lawyers. A source says that Atrium’s lawyers only found out a week ago about the changes, and they’ve been trying to pitch Atrium clients on working with them when they leave. One Atrium client said they weren’t surprised by the changes because they got so much legal advice for just $500 per month, which they suspected meant Atrium was losing money on the lawyers’ time as it was so much less expensive than competitors. They also said these cheap legal services rather than the software platform were the main draw of Atrium, and they’re unsure if the tech on its own is valuable enough.

One concern is Atrium might not learn as quickly about which services to translate into software if it doesn’t have as many lawyers in-house. But Kan believes third-party lawyers might be more clear and direct about what they need from legal technology. “I feel like having a true market for the software you’re building is better than having an internal market,” he says. “We get feedback from the outside firms we work with. I think in some ways that’s the most valuable feedback. I think there’s a lot of false signals that can happen when you’re the both the employer and the supplier.”

It was critical for Atrium to correct course before getting any bigger, given the fundraising problems hitting late-stage startups with poor economics in the wake of the WeWork debacle and SoftBank’s troubles. Atrium had raised a $10.5 million Series A in 2017 led by General Catalyst alongside Kleiner, Founders Fund, Initialized and Kindred Ventures. Then in September 2018, it scored a huge $65 million Series B led by Andreessen Horowitz.

Raising even bigger rounds might have been impossible if Atrium was offering consultations with lawyers at far below market rate. Now it might be in a better position to attract funding. But the question is whether clients will stick with Atrium if they get less access to a lawyer for the same price, and whether the collaboration platform is useful enough for outside law firms to pay for.

Kan had gone through tough pivots in the past. He had strapped a camera to his head to create content for his live-streaming startup Justin.tv, but wisely recentered on the 3% of users letting people watch them play video games. Justin.tv became Twitch and eventually sold to Amazon for $970 million. His on-demand personal assistant startup Exec had to switch to just cleaning in 2013 before shutting down due to rotten economics.

Rather than deny the inevitable and wait until the last minute, with Atrium Kan tried to make the hard decision early.

Powered by WPeMatico