law

Auto Added by WPeMatico

Auto Added by WPeMatico

On Tuesday, the Open Cap Table Coalition announced its launch through an inaugural Medium post. The goal of this project is to standardize startup capitalization table data as well as make it far more accessible, transparent and portable.

For those unfamiliar with a cap table, it’s a list of who owns your company’s securities, which includes your company shares, options and more. A clear and simple cap table should quickly indicate who owns what and how much of it they own. For a variety of reasons (sometimes inexperience or bad advice) too many equity holders often find companies’ capitalization information to be opaque and not easily accessible.

This is particularly important for the small percentage of startups that survive in the long term, as growth makes for far more complicated cap tables.

A critical part of good startup hygiene is to always have a clean and updated cap table. Since there is no set format and cap tables are generally not out in the open, they are often siloed rather than collaborative.

Cap tables are near and dear to me as someone who has advised hundreds of startups over the past two decades as the founder of an accelerator, a venture partner and a senior adviser at a government-funded startup launchpad. I have been on the shareholder side of the equation as well and can assure you that pretty much nothing destroys trust between shareholders and startups quicker than poor communication, especially around issues such as the current status of the cap table.

A critical part of good startup hygiene is to always have a clean and updated cap table.

I really like the idea of a cap table being an open corporate record, because the value proposition to the companies is clear. From the time a startup creates a cap table, it’s prone to inaccuracy, friction and mistakes. What this means in practice is that startups may spend money on cap-table-related issues that they should be spending on other things. From a legal process perspective, the law firm that is brought in to help with these issues has to deal with tedious back-end work, so the legal time isn’t high value for either the startup or the law firm.

The value proposition for equity holders is equally clear. All equity holders have a general and legal interest in a company’s capitalization information. They have the right to this information, which they may need for a variety of reasons (including, if things ever get really bad, an aggrieved shareholder action). So making this information clear and easily accessible is a service to equity holders and can also encourage more investment, especially from less experienced investors.

When I imagine what this project could become in the next couple of years, I think back to late 2013, when Y Combinator announced the SAFE (simple agreement for future equity). I think the SAFE is a good analogy here, as no one knew what it was and people wondered if this was a nice-to-have rather than a must-have for startups. But the end result was a dramatic improvement in the early-stage capital-raising process.

While the coalition’s founders include Morgan Stanley’s Shareworks, LTSE Software and Carta, it’s also heavy on Big Law, with Cooley, Goodwin Procter, Wilson Sonsini Goodrich & Rosati, Orrick, Gunderson Dettmer, Latham & Watkins, and Fenwick & West rounding out the group of 10 founding members.

So what’s the real motivation of seven law firms, which together saw revenue of over $10 billion in 2020 to collaborate on an open cap table product for startups? Deal flow.

Big Law has been trying for a couple of decades to build relationships with startups at the stage where it makes no sense for a startup to be dealing with a massive and expensive law firm. Their efforts to build startup programs have often fallen short and received mixed reviews. They have also been far too heavy on the self-serve and too light on the “we’re going to give you our regular Big Law level of services at a small fraction of the costs just in case you make it big and can one day pay our regular fees.” So these firms are trying to separate themselves from the rest of the Big Law pack by building this entrepreneur-friendly tech.

The coalition has already produced its initial version of the open cap table. The real question is whether this is going to be a big deal, as the SAFE was, or whether it’s going to be a vanity solution in search of a real problem. My best guess is that if this coalition gets all the relationships right, doesn’t get greedy and understands that there is a social good component at play here, this could be, reasonably quickly, as impactful as the SAFE was.

Powered by WPeMatico

Successfully selling a business has much to do with timing. For many entrepreneurs, it’s the high-stakes end game where they cash out and reap the rewards of their efforts. At a certain point, when both buyers and sellers are working hard to close the deal, negotiations can move very quickly. If you’re the seller, this is not the time to discover unanticipated problems in your business.

Distressingly often, these problems are related to employment. Inattention to employment issues can have a significant impact on deals — from preventing closings and reducing the deal value to altering the deal terms or significantly limiting the pool of potential buyers.

Poor compliance, lack of policies or flawed practices mean potential liability exposure or expensive policy revisions and employee retraining — all of which can devalue your business.

Fortunately, such issues typically can be resolved well in advance with a little forethought and legal guidance. It’s important to get your employment ducks in a row long before you start planning your exit.

What follows is an overview of the three main categories of employment issues that can derail or delay a sale. For the most part, these assume an asset sale, but may vary in the case of a stock sale.

By far the most significant problem is general employment law compliance. This means creating strong employment policies and practices that are documented, in place and operating long before you pursue a deal. The key area is wage and hour issues — timekeeping and payroll practices, worker classification issues (employee vs. independent contractor; exempt vs. non-exempt), meal and rest periods, PTO policies and payouts at termination.

Powered by WPeMatico

When the world shifted toward virtual one year ago, one service in particular saw heated demand: remote online notarization.

The ability to get a document notarized without leaving one’s home suddenly became more of a necessity than a luxury. Pat Kinsel, founder and CEO of Boston-based Notarize, worked to get appropriate legislation passed across the country to make it possible for more people in more states to get documents notarized digitally.

That hard work has paid off. Today, Notarize has announced $130 million in Series D funding led by fintech-focused VC firm Canapi Ventures after experiencing 600% year over year revenue growth. The round values Notarize at $760 million, which is triple its valuation at the time of its $35 million Series C in March of 2020. This latest round is larger than the sum of all of the company’s previous rounds to date, and brings Notarize’s total raised to $213 million since its 2015 inception.

A slew of other investors participated in the round, including Alphabet’s independent growth fund CapitalG, Citi Ventures, Wells Fargo, True Bridge Capital Partners and existing backers Camber Creek, Ludlow Ventures, NAR’s Second Century Ventures and Fifth Wall Ventures.

Notarize insists that it “isn’t just a notary company.” Rather, Canapi Ventures partner Neil Underwood described it as the “last mile” of businesses (such as iBuyers, for example).

The company has also evolved to “also bring trust and identity verification” into those businesses’ processes.

Over the past year, Notarize has seen a massive increase in transactions and inked new partnerships with companies such as Adobe, Dropbox, Stripe and Zillow Group, among others. It’s seen big spikes in demand from the real estate, financial services, retail and automotive sectors.

“In 2020, the world rushed to digitize. Online commerce ballooned, and businesses in almost every industry needed to transition to digital basically overnight so they could continue uninterrupted,” Kinsel said. “Notarize was there to help them safely close these deals with trust and convenience.”

The company plans to use its new capital to expand its platform and product and scale “to serve enterprises of all sizes.” It also plans to double down on hiring in the next year.

“Notarize is disrupting outdated business models and technologies, and there’s massive potential, particularly in the financial services space, as more companies will need to offer secure digital alternatives to in-person transactions,” Canapi’s Underwood said.

Notarize’s success comes after a difficult 2019, when the company saw “critical financing” fall through and had to lay off staff, according to Kinsel. Talk about a turnaround story.

Powered by WPeMatico

When salespeople in California’s dynamic tech economy transition between jobs, the value they bring to their new company is often their customer relationships. Startup founders and salespeople considering joining competitors often assume continuing to maintain these customer relationships is noncontroversial given California’s well-known policy favoring employment mobility and outlawing non-competition agreements.

Yet California trade secret law regarding the ability of salespeople to solicit these customers once they jump to a competitor is increasingly confused and fails to provide meaningful guidance on what type of conduct is permissible. Thus, a salesperson’s move from their current company to a competitor is risky given it is unclear whether and to what extent they can continue servicing clients or contacts they previously worked with.

A salesperson working for a value-added reseller (VAR), for instance, should understand what they are getting into before moving to a competitor — they may risk longstanding relationships with original equipment manufacturers (OEMs) and end users. This article explains the conflicting law on this issue so that salespeople planning on jumping ship, and the companies considering hiring them, can be informed regarding the current legal landscape.

In the vast majority of states, employers can, and do, require employees to enter into some form of non-competition agreement in exchange for continued employment.1 In contrast, California has a long-standing policy of favoring employment mobility over an employer’s concerns. California’s policy is embodied in Business and Professions Code section 16600, which provides: “Except as provided in this chapter, every contract by which anyone is restrained from engaging in a lawful profession, trade, or business of any kind is to that extent void.”

California courts “have consistently affirmed that section 16600 evinces a settled legislative policy in favor of open competition and employee mobility” that is intended to “ensure that every citizen shall retain the right to pursue any lawful employment and enterprise of their choice.”2 The policy also allows California employers to “compete effectively for the most talented, skilled employees in their industries, wherever they may reside.”3 Accordingly, unlike in most states, the “interests of the employee in [their] own mobility and betterment” generally outweigh the “competitive business interests of the employers.”4

Courts have broadly applied section 16600, invalidating non-competition agreements, which would prohibit or restrict an employee from leaving to work for a competitor.5 Importantly, courts have also invalidated contractual provisions purporting to restrict an employee’s ability to leave and then solicit the company’s customers.6 In other words, a salesperson cannot be contractually precluded from leaving their company, joining a competitor and continuing to solicit, service and communicate with their former company’s clients. Furthermore, with limited exceptions, California courts will disregard a “choice of law” provision purporting to mandate that the court follow the law from a state that enforces noncompetes.7

Powered by WPeMatico

A new startup is clearing the way for other companies to better monitor and manage their risk and compliance with privacy laws.

Osano, an Austin, Texas-based startup, bills itself as a privacy platform startup, which uses a software-as-a-service solution to give businesses real-time visibility into their current privacy and compliance posture. On one hand, that helps startups and enterprises large and small insight into whether or not they’re complying with global or state privacy laws, and manage risk factors associated with their business such as when partner or vendor privacy policies change.

The company launched its privacy platform at Disrupt SF on the Startup Battlefield stage.

Risk and compliance is typically a fusty, boring and frankly unsexy topic. But with ever-changing legal landscapes and constantly moving requirements, it’s hard to keep up. Although Europe’s GDPR has been around for a year, it’s still causing headaches. And stateside, the California Consumer Privacy Act is about to kick in and it is terrifying large companies for fear they can’t comply with it.

Osano mixes tech with its legal chops to help companies, particularly smaller startups without their own legal support, to provide a one-stop shop for businesses to get insight, advice and guidance.

“We believe that any time a company does a better job with transparency and data protection, we think that’s a really good thing for the internet,” the company’s founder Arlo Gilbert told TechCrunch.

Gilbert, along with his co-founder and chief technology officer Scott Hertel, have built their company’s software-as-a-service solution with several components in mind, including maintaining its scorecard of 6,000 vendors and their privacy practices to objectively grade how a company fares, as well as monitoring vendor privacy policies to spot changes as soon as they are made.

One of its standout features is allowing its corporate customers to comply with dozens of privacy laws across the world with a single line of code.

You’ve seen them before: The “consent” popups that ask (or demand) you to allow cookies or you can’t come in. Osano’s consent management lets companies install a dynamic consent management in just five minutes, which delivers the right consent message to the right people in the best language. Using the blockchain, the company says it can record and provide searchable and cryptographically verifiable proof-of-consent in the event of a person’s data access request.

“There are 40 countries with cookie and data privacy laws that require consent,” said Gilbert. “Each of them has nuances about what they consider to be consent: what you have to tell them; what you have to offer them; when you have to do it.”

Osano also has an office in Dublin, Ireland, allowing its corporate customers to say it has a physical representative in the European Union — a requirement for companies that have to comply with GDPR.

And, for corporate customers with questions, they can dial-an-expert from Osano’s outsourced and freelance team of attorneys and privacy experts to help break down complex questions into bitesize answers.

Or as Gilbert calls it, “Uber, but for lawyers.”

The concept seems novel but it’s not restricted to GDPR or California’s upcoming law. The company says it monitors international, federal and state legislatures for new laws and changes to existing privacy legislation to alert customers of upcoming changes and requirements that might affect their business.

In other words, plug in a new law or two and Osano’s customers are as good as covered.

Osano is still in its pre-seed stage. But while the company is focusing on its product, it’s not thinking too much about money.

“We’re planning to kind of go the binary outcome — go big or go home,” said Gilbert, with his eye on the small- to medium-sized enterprise. “It’s greenfield right now. There’s really nobody doing what we’re doing.”

The plan is to take on enough funding to own the market, and then focus on turning a profit. So much so, Gilbert said, that the company is registered as a B Corporation, a more socially conscious and less profit-driven approach of corporate structure, allowing it to generate profits while maintaining its social vision.

The company’s idea is strong; its corporate structure seems mindful. But is it enough of an enticement for fellow startups and small businesses? It’s either dominate the market or bust, and only time will tell.

Powered by WPeMatico

It is a simple question with a complex answer. How does a startup get from zero to execution when negotiating contracts with potential customers that are large enterprises? The 800-pound gorillas. Situations in which your negotiating leverage is limited (often severely so).

As a commercial contracts attorney, clients often ask me about the one right way to approach deals. Many are looking for a cheat sheet of universal terms they should push for in contracts. But there is no one answer.

Deals are not cookie-cutter, and neither are the contracts on which they are built. That said, a basic framework can help provide startups with some grounding to better think about negotiations with large enterprises. The idea is to avoid over-lawyering, and instead approach the discussion with a legally prudent yet deal-centric mindset.

There are generally six overarching considerations as you head into negotiations with large, enterprise organizations.

Powered by WPeMatico

Contract management isn’t exactly an exciting subject, but it’s a real pain point for many companies. It also lends itself to automation, thanks to recent advances in machine learning and natural language processing. It’s no surprise then, that we see renewed interest in this space and that investors are putting more money into it. Earlier this week, Icertis raised a $115 million Series E round, for example, at a valuation of more than $1 billion. Icertis has been in this business for 10 years, though. On the other end of the spectrum, contract management startup Lexion today announced that it has raised a $4.2 million seed round led by Madrona Venture Group and law firm Wilson Sonsini Goodrich & Rosati, which was also one of the first users of the product.

Lexion was incubated at the Allen Institute for Artificial Intelligence (AI2), one of the late Microsoft co-founders’ four scientific research institutes. The company’s co-founder and CEO, Gaurav Oberoi, is a bit of a serial entrepreneur, whose first startup, BillMonk, was first featured on TechCrunch back in 2006. His second go-around was Precision Polling, which SurveyMonkey then acquired shortly after it launched. Oberoi founded the company together with former Microsoft research software development engineering lead Emad Elwany and engineering veteran James Baird.

“Gaurav, Emad, and James are just the kind of entrepreneurs we love to back: smart, customer obsessed and attacking a big market with cutting-edge technology,” said Madrona Venture Group managing director Tim Porter. “AI2 is turning out some of the best applied machine learning solutions, and contract management is a perfect example — it’s a huge issue for companies at every size and the demand for visibility into contracts is only increasing as companies face growing regulatory and compliance pressures.”

Contract management is becoming a bit of a crowded space, though, something Oberoi acknowledged. But he argues that Lexion is tackling a different market from many of its competitors.

“We think there’s growing demand and a big opportunity in the mid-market,” he said. “I think similar to how back in the 2000s, Siebel or other companies offered very expensive CRM software and now you have Salesforce — and now Salesforce is the expensive version — and you have this long tail of products in the mid-market. I think the same is happening to contracts. […] We’re working with companies that are as small as post-seed or post-Series A to a publicly traded company.”

Given that it handles plenty of highly confidential information, it’s no surprise that Lexion says that it takes security very seriously. “I think, something that all young startups that are selling into business or enterprise in 2019 need to address upfront,” Oberoi said. “We realized, even before we raised funding and got very serious about growing this business, that security has to be part of our DNA and culture from the get-go.” He also noted that every new feature and product iteration at Lexion goes through a security review.

Like most startups at this stage, Lexion plans to invest the new funding into building out its product — and especially its AI engine — and go-to-market and sales strategy.

Powered by WPeMatico

GDPR, and the newer California Consumer Privacy Act, have given a legal bite to ongoing developments in online privacy and data protection: it’s always good practice for companies with an online presence to take measures to safeguard people’s data, but now failing to do so can land them in some serious hot water.

Now — to underscore the urgency and demand in the market — one of the bigger companies helping organizations navigate those rules is announcing a huge round of funding. OneTrust, which builds tools to help companies navigate data protection and privacy policies both internally and with its customers, has raised $200 million in a Series A led by Insight that values the company at $1.3 billion.

It’s an outsized round for a Series A, being made at an equally outsized valuation — especially considering that the company is only three years old — but that’s because of the wide-ranging nature of the issue, according to CEO Kabir Barday, and OneTrust’s early moves and subsequent pole position in tackling it.

“We’re talking about an operational overhaul in a company’s practices,” Barday said in an interview. “That requires the right technology and reach to be able to deliver that at a low cost.” Notably, he said that OneTrust wasn’t actually in search of funding — it’s already generating revenue and could have grown off its own balance sheet — although he noted that having the capitalization and backing sends a signal to the market and in particular to larger organizations of its stability and staying power.

Currently, OneTrust has around 3,000 customers across 100 countries (and 1,000 employees), and the plan will be to continue to expand its reach geographically and to more businesses. Funding will also go toward the company’s technology: it already has 50 patents filed and another 50 applications in progress, securing its own IP in the area of privacy protection.

OneTrust offers technology and services covering three different aspects of data protection and privacy management.

Its Privacy Management Software helps an organization manage how it collects data, and it generates compliance reports in line with how a site is working relative to different jurisdictions. Then there is the famous (or infamous) service that lets internet users set their preferences for how they want their data to be handled on different sites. The third is a larger database and risk management platform that assesses how various third-party services (for example advertising providers) work on a site and where they might pose data protection risks.

These are all provided either as a cloud-based software as a service, or an on-premises solution, depending on the customer in question.

The startup also has an interesting backstory that sheds some light on how it was founded and how it identified the gap in the market relatively early.

Alan Dabbiere, who is the co-chairman of OneTrust, had been the chairman of Airwatch — the mobile device management company acquired by VMware in 2014 (Airwatch’s CEO and founder, John Marshall, is OneTrust’s other co-chairman). In an interview, he told me that it was when they were at Airwatch — where Barday had worked across consulting, integration, engineering and product management — that they began to see just how a smartphone “could be a quagmire of privacy issues.”

“We could capture apps that an employee was using so that we could show them to IT to mitigate security risks,” he said, “but that actually presented a big privacy issue. If [the employee] has dyslexia [and uses a special app for it] or if the employee used a dating app, you’ve now shown things to IT that you shouldn’t have.”

He admitted that in the first version of the software, “we weren’t even thinking about whether that was inappropriate, but then we quickly realised that we needed to be thinking about privacy.”

Dabbiere said that it was Barday who first brought that sensibility to light, and “that is something that we have evolved from.” After that, and after the VMware sale, it seemed a no-brainer that he and Marshall would come on to help the new startup grow.

Airwatch made a relatively quick exit, I pointed out. His response: the plan is to stay the course at OneTrust, with a lot more room for expansion in this market. He describes the issues of data protection and privacy as “death by 1,000 cuts.” I guess when you think about it from an enterprising point of view, that essentially presents 1,000 business opportunities.

Indeed, there is obvious growth potential to expand not just its funnel of customers, but to add more services, such as proactive detection of malware that might leak customers’ data (which calls to mind the recently fined breach at British Airways), as well as tools to help stop that once identified.

While there are a million other companies also looking to fix those problems today, what’s interesting is the point from which OneTrust is starting: by providing tools to organizations simply to help them operate in the current regulatory climate as good citizens of the online world.

This is what caught Insight’s eye with this investment.

“OneTrust has truly established themselves as leaders in this space in a very short time frame, and are quickly becoming for privacy professionals what Salesforce became for salespeople,” said Richard Wells of Insight. “They offer such a vast range of modules and tools to help customers keep their businesses compliant with varying regulatory laws, and the tailwinds around GDPR and the upcoming CCPA make this an opportune time for growth. Their leadership team is unparalleled in their ambition and has proven their ability to convert those ambitions into reality.”

Wells added that while this is a big round for a Series A it’s because it is something of an outlier — not a mark of how Series A rounds will go soon.

“Investors will always be interested in and keen to partner with companies that are providing real solutions, are already established and are led by a strong group of entrepreneurs,” he said in an interview. “This is a company that has the expertise to help solve for what could be one of the greatest challenges of the next decade. That’s the company investors want to partner with and grow, regardless of fund timing.”

Powered by WPeMatico

The immigration process in the U.S. has become a high-stakes undertaking for employers, workers, and entrepreneurs. Predictability has eroded. Processing times have soared. And any mistake or misstep now has dire consequences.

Over the past three years, immigration policies and procedures have been in a state of flux and the process has become more unforgiving for even the smallest mistakes. Putting your best foot forward is crucial. Employers and individuals need to formulate a long-term strategy and backup options to stay protected.

The increase in Requests for Evidence and the backlog for many visa and green card categories has meant longer waiting times. What’s more, the Trump administration’s recent decision to close all USCIS’s international offices—and shift that workload back to the U.S.—is expected to compound the backlogs and delays.

We are seeing these issues affect startups every day. My law firm works with hundreds of startups every year to help them and their employers figure out their immigration paperwork. The overall piece of advice we give is to decide on a specific goal based on a deep understanding of the company and the individual and by examining the options strategically.

Then, you can figure out the right approach for a visa, green card, or citizenship application. Regardless of my personal interest in the matter, now more than ever, I recommend consulting with an experienced immigration attorney who can handle the process with integrity, creativity, compassion, and rigor.

The new normal for immigration means increased employee recruiting and retention costs for employers. However, hiring immigrants remains possible.

Powered by WPeMatico

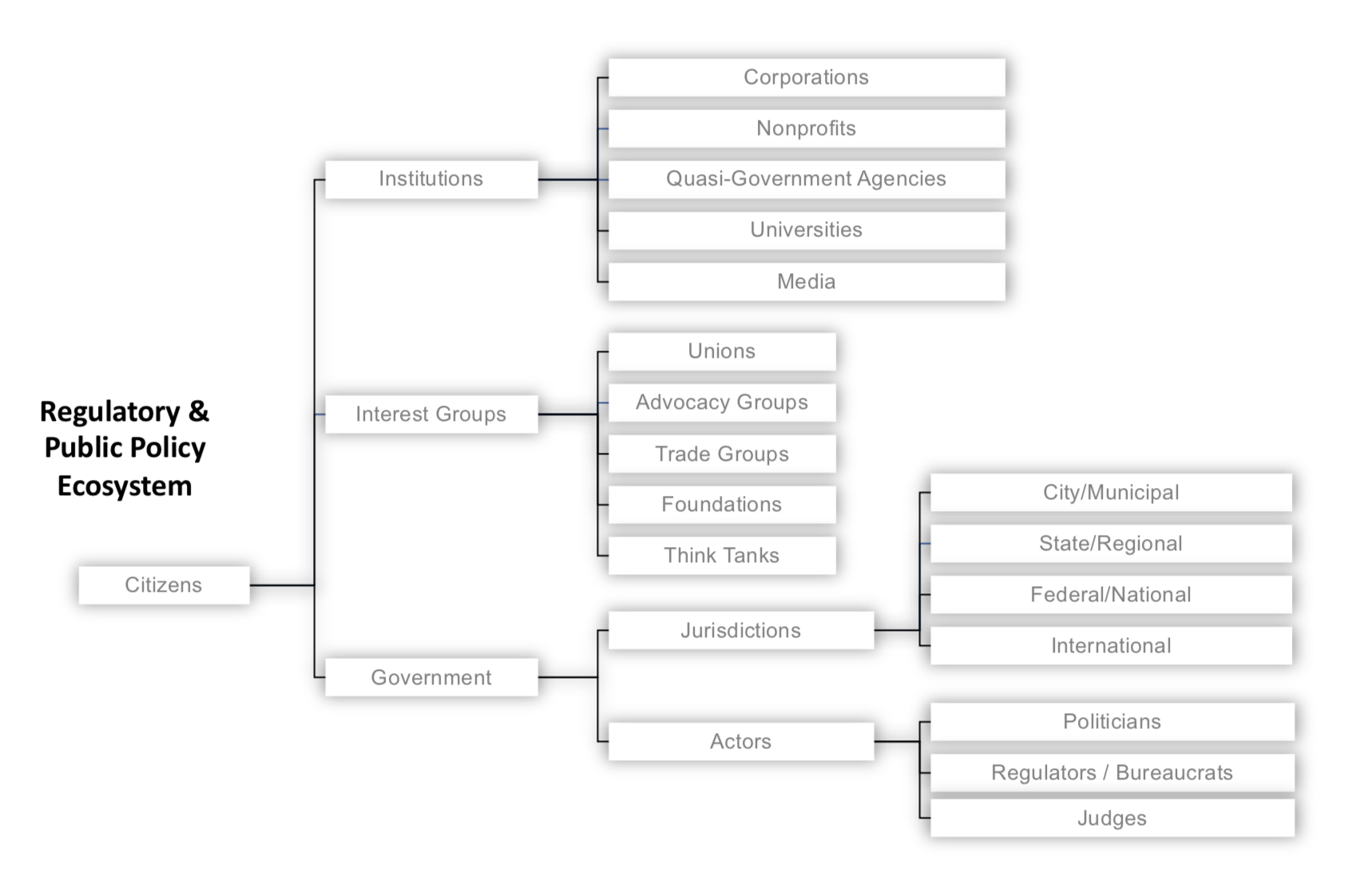

Startups are but one species in a complex regulatory and public policy ecosystem. This ecosystem is larger and more powerfully dynamic than many founders appreciate, with distinct yet overlapping laws at the federal, state and local/city levels, all set against a vast array of public and private interests. Where startup founders see opportunity for disruption in regulated markets, lawyers counsel prudence: regulations exist to promote certain strongly-held public policy objectives which (unlike your startup’s business model) carry the force of law.

Snapshot of the regulatory and public policy ecosystem. Image via Law Office of Daniel McKenzie

Although the canonical “ask forgiveness and not permission” approach taken by Airbnb and Uber circa 2009 might lead founders to conclude it is strategically acceptable to “move fast and break things” (including the law), don’t lose sight of the resulting lawsuits and enforcement actions. If you look closely at Airbnb and Uber today, each have devoted immense resources to building regulatory and policy teams, lobbying, public relations, defending lawsuits, while increasingly looking to work within the law rather than outside it – not to mention, in the case of Uber, a change in leadership as well.

Indeed, more recently, examples of founders and startups running into serious regulatory issues are commonplace: whether in healthcare, where CEO/Co-founder Conrad Parker was forced to resign from Zenefits and later fined approximately $500K; in the securities registration arena, where cryptocurrency startups Airfox and Paragon have each been fined $250K and further could be required to return to investors the millions raised through their respective ICOs; in the social media and privacy realm, where TikTok was recently fined $5.7 million for violating COPPA, or in the antitrust context, where tech giant Google is facing billions in fines from the EU.

Suffice it to say, regulation is not a low-stakes table game. In 2017 alone, according to Duff and Phelps, US financial regulators levied $24.4 billion in penalties against companies and another $621.3 million against individuals. Particularly in today’s highly competitive business landscape, even if your startup can financially absorb the fines for non-compliance, the additional stress and distraction for your team may still inflict serious injury, if not an outright death-blow.

The best way to avoid regulatory setbacks is to first understand relevant regulations and work to develop compliant policies and business practices from the beginning. This article represents a step in that direction, the fifth and final installment in Extra Crunch’s exclusive “Startup Law A to Z” series, following previous articles on corporate matters, intellectual property (IP), customer contracts and employment law.

Given the breadth of activities subject to regulation, however, and the many corresponding regulations across federal, state, and municipal levels, no analysis of any particular regulatory framework would be sufficiently complete here. Instead, the purpose of this article is to provide founders a 30,000-foot view across several dozen applicable laws in key regulatory areas, providing a “lay of the land” such that with some additional navigation and guidance, an optimal course may be charted.

The regulatory areas highlighted here include: (a) Taxes; (b) Securities; (c) Employment; (d) Privacy; (e) Antitrust; (f) Advertising, Commerce and Telecommunications; (g) Intellectual Property; (h) Financial Services and Insurance; and finally (i) Transportation, Health and Safety.

Of course, some regulations may touch on multiple regulatory areas, for example, the “Fair Credit Reporting Act” is a law ultimately about privacy, but it impacts many financial and employment-related services as well. Certain laws may therefore be cross-listed in more than one regulatory area. Also, since we can’t look at every U.S. state and city, this article will focus primarily on the federal and California state laws.

After you focus on the particular regulatory areas that may implicate your business, next reference the short quotations and links to relevant primary and secondary sources below, then work to identify the specific compliance risks you face. This is where other Extra Crunch resources can help. For example, the Verified Experts of Extra Crunch include some of the most experienced and skilled startup lawyers in practice today. Use these profiles to identify attorneys who are focused on serving companies at your particular stage and then seek out any further guidance you need to address the regulatory matters pertinent to your startup.

With that as context, the Startup Law A to Z – Regulatory Compliance checklist is below:

Before diving into further detail, it may be helpful for some readers to note the distinction between a law and a regulation. Simply put, regulations provide more detailed direction on how certain laws should be followed. So regulations are not technically laws, but they carry the force of law (including penalties for violation), since they are adopted by governmental agencies under authority granted by statute. Beyond that, understanding how laws and regulations are actually enacted is helpful to illustrate the extent to which the process is politically driven.

In the U.S., a bill must first pass both legislative branches of government, then, if signed by the executive branch, it will be codified in statute as law (Schoolhouse Rock anyone?). Once codified, the legislative branch will authorize the relevant executive department or agency to determine whether specific regulations are necessary to give the law effect. If so, those executive departments or agencies will determine what further rules are needed, and in turn, work to enforce them.

At the federal level, for example, proposed regulations are developed first through a “Notice of Proposed Rulemaking,” listed in the Federal Register and filed in the corresponding executive agency’s official docket (available at Regulations.gov). This affords the public an opportunity to comment on the regulations. After receiving comments, the filing agency may revise the proposed regulation before final rules are issued, which again will be published in the Federal Register and then filed in the agency’s official docket at Regulations.gov, before they are codified in the Code of Federal Regulations (CFR).

At nearly every step in this process then, institutions, government, and interest groups are working – sometimes at cross purposes – to shape what the law will be and how it will impact your startup.

The Startup Law A to Z – Regulatory Compliance reference guide is below:

Powered by WPeMatico