Latch

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

For this week’s deep dive Natasha and Alex and Chris dug into the world of the IPO. Not just the numbers and the metrics and the calculations of valuations at diluted, and non-diluted, share counts. No. We wanted to talk about the morality and efficacy of going public.

So to round out our conversation we enlisted Steve Cakebread, the CFO of Yext, and Garth Mitchell, the CFO of Latch. Cakebread is known for being aboard the Salesforce, Pandora and Yext IPOs. Mitchell has sat on both sides of the table during the IPO process, and is currently helming the money equations as Latch approaches the public markets via a SPAC.

For more context, Yext, a company that first launched at a TechCrunch event back in 2009, provides data tooling and search software to businesses, while Latch builds software and hardware for rental-focused buildings. Yext is public. Latch will be in a few months.

Back to our topic, we asked Cakebread to talk about his thesis on why going public earlier than later can help a company’s maturity process and can help provide greater returns to the general public. The CFO has written a rather good book about the IPO process more generally and what it means for a company’s internal processes, but his morality notes especially stood out because it’s an argument far less noisy than the POP critics. Baked beans come up, somehow!

We also asked Mitchell to talk about Latch’s choice to go public, and what opportunities and challenges the SPAC route brings for the company. Of course, there’s a SPAC joke in there (or two), but we get into broader “what’s next” debates about if more companies will start to leave the private world, venture capital’s role in this whole mess and the financial lift of going to the public market.

Hope you enjoy the show, and get excited: Equity is going to have more guests on from time to time, and we welcome any suggestions you want to throw at us.

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 AM PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

The public markets give, and the public markets take away. Earlier this morning, enterprise cloud storage and productivity company Box got into a more public spat with some of its shareholders upset with its performance and management decisions. But while Box endures the more difficult chapters of being a public company, other companies are racing to join the ranks of the listed concerns of the world.

If it feels like IPO news slowed for a few weeks at the start of the second quarter, your gut is correct. Investors previously told The Exchange that the first, third and fourth quarters of 2021 would be hot periods for public debuts, but that Q2 would be slower. Their argument revolved around reporting cadences and how long it takes for certain periods of accounting work to be completed.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

So we weren’t surprised when the second quarter’s IPO cycle began to feel a bit soft compared to the rapid-fire first quarter. And, as we’ve all heard in recent days, the great SPAC rush is slowing.

But that hasn’t stopped a number of firms from defying expectations and going public all the same. Online hosting and website builder Squarespace has not only filed but filled in its public filing with notes on its anticipated direct listing. We have to talk about its choice to list directly in light of new financial information we have concerning its recent performance.

But there’s more: Expensify filed to go public yesterday, albeit privately. And the SmartRent SPAC combination, though now slightly dated, is also worth a moment of our time.

But there’s more: Expensify filed to go public yesterday, albeit privately. And the SmartRent SPAC combination, though now slightly dated, is also worth a moment of our time.

The final element in the current IPO landscape is the recent Darktrace IPO in the United Kingdom, which, after that market had a rough start to its tech IPO calendar, is now seeing better results. So, let’s discuss IPOs to fully understand where we stand today in the realm of unicorn liquidity.

When The Exchange first dug into Squarespace’s IPO filing, we did our best to parse its full-year results because we lacked its quarterly details. This leaves us with two things to chew on: Why is Squarespace pursuing a direct listing over another listing technique, and what can its current and more granular operating results tell us about the choice?

On the first count, if Squarespace is direct listing, we can presume that it doesn’t need more cash to operate. So, how much cash does the company have on hand? A good chunk of change: $183.3 million.

Powered by WPeMatico

The first quarter of 2021 was a busy season for technology exits. Coming off a hot period in the final quarter of 2020, it was no surprise that tech upstarts pursued liquidity through a variety of mechanisms as the new year began.

There were IPOs, there were direct listings, there were PE deals. Hell, we even saw enough SPACs that we lost track of a few; amid all the noise, you’ll miss the occasional note no matter how well-tuned your ear.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Each path is still open for later-stage startups to pursue exits: The IPO market was welcoming until a few minutes ago and private equity firms are stacked with cash and willing to pay higher multiples than they might in more normal times. And there are sufficient SPACs to take the entire recent Y Combinator class public.

Choosing which option is best from a buffet’s worth of possibilities is an interesting task for startup CEOs and their boards.

DigitalOcean went public via a traditional IPO, raising a slug of capital in the process. The SMB-focused public cloud company likely felt like a somewhat obvious IPO candidate when you read its results. The Exchange spoke with the company’s CEO, Yancey Spruill, about the choice.

DigitalOcean went public via a traditional IPO, raising a slug of capital in the process. The SMB-focused public cloud company likely felt like a somewhat obvious IPO candidate when you read its results. The Exchange spoke with the company’s CEO, Yancey Spruill, about the choice.

Latch, in contrast, decided that a SPAC was its best route out the gate. The Exchange caught up with the company’s CFO, Garth Mitchell, about the transaction and why it made sense for his company.

And, finally, The Exchange spoke with AlertMedia’s founder and CEO, Brian Cruver, about his decision to sell his Texas-based company to a private equity firm.

To prevent this post from reaching an astronomic word count, we’ll give a brief overview of each deal and then summarize the company’s views about why their liquidity choice was the right one.

Kicking off with DigitalOcean, a few notes: First, the company has been pretty darn public about its growth in the last few years. We knew that it had an annualized run rate of around $200 million in 2018, $250 million in 2019 and around $300 million in the first half of 2020. It later announced that it hit that mark in May of last year.

So when DigitalOcean decided to go public, we weren’t bowled over. The company wound up pricing at $47 per share, the high end of its range. Since then, its stock has struggled somewhat, falling below $37 per share before recovering to $43.80 at the end of trading yesterday.

Enough of all that. Why did the company choose to go public via a traditional IPO? Spruill said his company looked at SPAC deals and direct listings. It selected the IPO route because it fit the company’s goals of generating a broad base of shareholders while creating a branding opportunity.

The cost of an IPO is comparable, he added, to other exit options. Spruill also praised the IPO process itself, noting that its rigorous requirements made DigitalOcean a better company.

Earlier in our chat, I asked Spruill a question that I put to every CEO on IPO day: How are you feeling? It’s a bit of a sop, but it sometimes elicits insights from executives and founders who, after weeks of discussing their companies’ inner workings, are asked a rare personal question.

Spruill said he felt incredible and that nothing could replicate an IPO as the culmination of so much work put into building a company and its team. If you add up the wins and losses over time, with more of the former than the latter, and can cross the finish line with the right metrics and market, you can earn a spot to be “grilled” by the “best investors,” he said.

Those investors put $750 million or so into his company, Spruill added. Funds that it can use to retire debt and free up more cash flow. Not a bad day, I’d say.

Powered by WPeMatico

This week, Latch becomes the latest company to join the SPAC parade. Founded in 2014, the New York-based company came out of stealth two years later, launching a smart lock system. Though, like many companies primarily known for hardware solutions, Latch says it’s more, offering a connected security software platform for owners of apartment buildings.

The company is set to go public courtesy of a merger with blank check company TS Innovation Acquisitions Corp. As far as partners go, Tishman Speyer Properties makes strategic sense here. The New York-based commercial real estate firm is a logical partner for a company whose technology is currently deployed exclusively in residential apartment buildings.

“With a standard IPO, you have all of the banks take you out to all of the big investors,” Latch founder and CEO Luke Schoenfelder tells TechCrunch. “We felt like there was an opportunity here to have an extra level of strategic partnership and an extra level of product expansion that came as part of the process. Our ability to go into Europe and commercial offices is now accelerated meaningfully because of this partnership.

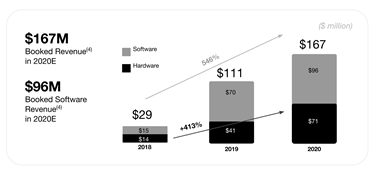

The number of SPAC deals has increased substantially over the past several months, including recent examples like Taboola. According to Crunchbase, Latch has raised $152 million, to date. And the company has seen solid growth over the past year — not something every hardware or hardware adjacent company can say about the pandemic.

As my colleague Alex noted on Extra Crunch today, “Doing some quick match, Latch grew booked revenues 50.5% from 2019 to 2020. Its booked software revenues grew 37.1%, while its booked hardware top line expanded over 70% during the same period.”

“We’ve been a customer and investor in Latch for years,” Tishman Speyer President and CEO Rob Speyer tells TechCrunch. “Our customers — the people who live in our buildings — love the Latch product. So we’ve rolled it out across our residential portfolio […] I hope we can act as both a thought partner and product incubator for them.”

While the company plans to expand to commercial offices, apartment buildings have been a nice vertical thus far — meaning the company doesn’t have to compete as directly in the crowded smart home lock category. Among other things, it’s probably a net positive if you’re going head to head against, say Amazon. That the company has built in partners in real estate firms like Tishman Speyer is also a net positive.

Schoenfelder says the company is looking toward such partnerships as test beds for its technology. “Our products have been in the field for many years in multifamily. The usage patterns are going to be slightly different in commercial offices. We think we know how they’re going to be different, but being able to get them up and running and observe the interaction with products in the wild is going to be really important.”

The deal values Latch at $1.56 billion and is expected to close in Q2.

Powered by WPeMatico

This morning, investor and SPAC raconteur Chamath Palihapitiya announced two new blank-check deals involving Latch and Sunlight Financial.

Latch, an enterprise SaaS company that makes keyless-entry systems, has raised $152 million in private capital, according to Crunchbase. Sunlight Financial, which offers point-of-sale financing for residential solar systems, has raised north of $700 million in venture capital, private equity and debt.

We’re going to chat about the two transactions.

There’s no escaping SPACs for a bit, so if you are tired of watching blind pools rip private companies into the public markets, you are not going to have a very good next few months. Why? There are nearly 300 SPACs in the market today looking for deals, and many will find one.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Think of SPACs are increasingly hungry sharks. As a shark get hungrier while the clock winds down on its deal-making window, it may get less choosy about what it eats (take public). There are enough SPACs on the hunt today that they would be noisy even if they were not time-constrained investment vehicles. But as their timers tick, expect their deal-making to get all the more creative.

This brings us back to Chamath’s two deals. Are they more like the Bakkt SPAC, which led us to raise a few questions? Or more akin to the Talkspace SPAC, which we found pretty reasonable? Let’s find out.

Let’s start with the Latch deal.

New York-based Latch sells “LatchOS,” a hardware and software system that works in buildings where access and amenities matter. Latch’s hardware works with doors, sensors and internet connectivity.

The company has raised a number of private rounds, including a $126 million deal in August of 2019 that valued the company at $454.3 million on a post-money basis, according to PitchBook data. The company raised another $30 million in October of 2020, though its final private valuation is not known.

As Chamath tweeted this morning, Latch is merging with TS Innovation Acquisitions Corp, or $TSIA. The SPAC is associated with Tishman Speyer, a commercial real estate investor. You can see the synergies, as Latch’s products fit into the commercial real estate space.

Up front, Latch is not a company that is only reporting future revenues. It has a history as an operating entity. Indeed, here’s its financial data per its investor presentation:

Image Credits: Latch

Doing some quick match, Latch grew booked revenues 50.5% from 2019 to 2020. Its booked software revenues grew 37.1%, while its booked hardware top line expanded over 70% during the same period.

That could be due to strong hardware installation fees, which could later result in software revenues; the company claims an average of a six-year software deal, so hardware revenues that are attached to new software incomes could low key declaim long-term SaaS revenues.

Update: Adding some clarity here, the above are “booked” revenues, which I’ve made more clear, not actual revenues. Its net revenues, better known as actual revenues, were $18 million, with $14 million of that coming from hardware. So, today, the company is certainly more hardware-heavy than I first thought. Damn non-S-1 filings!

While some were quick to note that the company is far from pure-SaaS — correct — I suspect that the model that could get some traction amongst investors is that this feels a bit like Peloton for real estate. How so? Peloton has large hardware incomes up front from new users, which convert to long-term subscription revenues. Latch may prove similar, albeit for a different customer base and market.

Per the deal’s reported terms, Latch will be worth $1.56 billion after the transaction. The combined entity will have $510 million in cash, including $190 million from a PIPE — a method of putting private money into a public entity — from “BlackRock, D1 Capital Partners, Durable Capital Partners LP, Fidelity Management & Research Company LLC, Chamath Palihapitiya, The Spruce House Partnership, Wellington Management, ArrowMark Partners, Avenir and Lux Capital.”

Powered by WPeMatico

Latch announced this morning that it has raised $70 million in Series B funding.

The round was led by Brookfield Ventures, the investment arm of Brookfield Asset Management. As part of the deal, Brookfield Properties will also be installing Latch systems in its multi-family properties that are currently under development.

“We are thrilled to support Latch, the clear market leader in a nearly $25 billion space that is expected to grow at twice the rate of traditional access over the next several years,” said Brookfield’s Josh Raffaelli in the funding announcement.

Lux Capital, RRE Ventures, Primary Venture Partners, Third Prime, Camber Creek, Corigin Ventures, Tishman Speyer and Balyasny Asset Management also participated int he new funding.

Latch’s smart lock system is designed for apartment buildings rather than single family homes, allowing you to open doors with a smartphone, keycard or door code. It also allows residents to create temporary access codes for guests and service providers.

Speaking of service providers, Latch announced a pilot partnership with UPS earlier this summer that will allow UPS drivers to receive unique credentials for entering buildings to make deliveries.

Latch was founded five years ago, but stayed in stealth mode until 2016. It previously raised $26 million funding.

Powered by WPeMatico

Enterprise-grade smart lock startup Latch has added a third product to its portfolio. The ‘Latch C’ is notable as its first smart lock to be certified to work with Apple’s HomeKit.

Enterprise-grade smart lock startup Latch has added a third product to its portfolio. The ‘Latch C’ is notable as its first smart lock to be certified to work with Apple’s HomeKit.