Kunal Shah

Auto Added by WPeMatico

Auto Added by WPeMatico

Even as hundreds of millions of people in India have a bank account, only a tiny fraction of this population invests in any financial instrument.

Fewer than 30 million people invest in mutual funds or stocks, for instance. In recent years, a handful of startups have made it easier for users — especially the millennials — to invest, but the figure has largely remained stagnant.

Now, an Indian startup believes that it has found the solution to tackle this challenge — and is already seeing good early traction.

Nishchay AG, former director of mobility startup Bounce, and Misbah Ashraf, co-founder of Marsplay (sold to Foxy), founded Jar earlier this year.

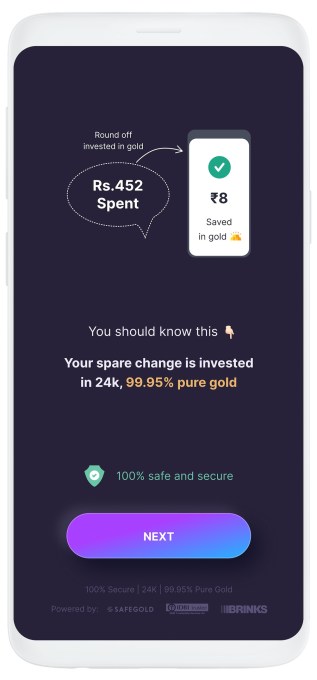

The startup’s eponymous six-month-old Android app enables users to start their savings journey for as little as 1 Indian rupee.

Users on Jar can invest in multiple ways and get started within seconds. The app works with Paytm (PhonePe support is in the works) to set up a recurring payment. (The startup is the first to use UPI 2.0’s recurring payment support.) They can set up any amount between 1 Indian rupee to 500 for daily investments.

The Jar app can also glean users’ text messages and save a tiny amount based on each monetary transaction they do. So, for instance, if a user has spent 31 rupees in a transaction, the Jar app rounds that up to the nearest tenth figure (40, in this case) and saves nine rupees. Users can also manually open the app and spend any amount they wish to invest.

Once users have saved some money in Jar, the app then invests that into digital gold.

The startup is using gold investment because people in the South Asian market already have an immense trust in this asset class.

India has a unique fascination for gold. From rural farmers to urban working class, nearly everyone stashes the yellow metal and flaunts jewelry at weddings.

Indian households are estimated to have a stash of over 25,000 tons of the precious metal whose value today is about half of the country’s nominal GDP. Such is the demand for gold in India that the South Asian nation is also one of the world’s largest importers of this precious metal.

Jar’s Android app (Image Credits: Jar)

“When you’re thinking about bringing the next 500 million people to institutional savings and investments, the onus is on us to educate them on the efficacies of the other instruments that are in the market,” said Nishchay.

“We want to give them the instrument they trust the most, which is gold,” he said. The startup plans to eventually offer several more investment opportunities, he said.

The founders met several years ago when they were exploring if MarsPlay and Bounce could have any synergies. They stayed in touch and, last year during one of their many conversations, realized that neither of them knew much about investments.

“That’s when the dots started to connect,” said Misbah, drawing stories from his childhood. “I come from a small town in Bihar called Bihar Sharif. During my childhood days, I saw my family deeply troubled with debt because of poor financial decisions and no savings,” he said.

“We both understand what a typical middle class family goes through. Someone who comes from this background never had any means in the past but their aspirations are never-ending. So when you start earning, you immediately start to spend it all,” said Nishchay.

“The market needs products that will help them get started,” he said.

That idea, which is similar to Acorn and Stash’s play in the U.S. market, is beginning to make inroads. The app has already amassed about half a million downloads, the founders said. Investors have taken notice, too.

On Wednesday, Jar announced it has raised $4.5 million from a clutch of high-profile investors, including Arkam Ventures, Tribe Capital, WEH Ventures, and angels including Kunal Shah (founder of CRED), Shaan Puri (formerly with Twitch), Ali Moiz (founder of Stonks), Howard Lindzon (founder of Social Leverage), Vivekananda Hallekere (co-founder of Bounce), Alvin Tse (of Xiaomi) and Kunal Khattar (managing partner at AdvantEdge).

“Over 400 million Indians are about to embrace digital financial services for the first time in their lives. Jar has built an app that is poised to help them — with several intuitive ways including gamification — start their investment journey. We love the speed at which the team has been executing and how fast they are growing each week,” said Arjun Sethi, co-founder of Tribe Capital, in a statement.

Transactions and AUM on the Jar app are surging 350% each month, said Nishchay. The startup plans to broaden its product offerings in the coming days, he said.

Powered by WPeMatico

Bangalore-based CRED is kickstarting the new year on a high note.

The two-year-old startup, led by high-profile entrepreneur Kunal Shah, said on Monday it has raised $81 million in a new financing round and bought shares worth $1.2 million (about 90 million Indian rupees) from employees.

The Series C financing round, as first reported by TechCrunch in late November, was led by DST Global. Existing investors Sequoia Capital, Ribbit Capital, Tiger Global and General Catalyst also participated in the round, and so did a few new names, including Satyan Gajwani of Indian conglomerate Times Internet, Sofina and Coatue.

The round gave CRED — which operates an eponymous app to reward customers for paying their credit card bill on time and offers deals from interesting online brands — a post-money valuation of $806 million.

In an interview with TechCrunch, Shah said that about 10% of CRED’s cap table is currently allocated to employees, and those who held vested stocks were eligible to sell up to 50% of their shares back to the startup in its first ESOP liquidity program. “We believe that startups should think about creating wealth for every shareholder, including employees.”

CRED has nearly doubled its customer base to about 5.9 million in the past year, or about 20% of the credit card holder base in India. The startup said that the median credit score of its customer was about 830, and about 30% of its customer base today holds a premium credit card. (On a side note, more than 50% of CRED customers pay their bills using UPI.)

CRED is one of the most talked-about startups in India, in part because of the scale at which its valuation has soared and the amount of capital it has been able to raise in such a short period.

One of the biggest questions surrounding CRED is just how it makes money, given how most fintech startups in the country — and there are many of them — are struggling to find a business model.

Shah said CRED makes money by cross-selling financing products — for which it has a revenue-sharing arrangement with banks and other financial institutions — and levies a similar cut from merchants who are on the platform today. More than 1,300 brands — including big names Starbucks, TAGG, Eat.Fit, Nykaa and emerging premium direct-to-consumer brands such as The Man Company, Sleepy Cat and Crossbeats –have joined the platform in recent years.

Direct-to-consumer market in India is still in its nascent stage, though some estimates say it could be worth $100 billion by 2025.

“I don’t think we were very deliberate to make D2C happen. It just so happened that in the early days when we offered rewards for D2C brands, they started to see huge traction,” he said, adding that CRED drove more than 30% sales for some brands.

“We realized that we were able to solve the discovery problem for customers. We are approaching this with themes — work-from-home and coffee — and it’s working out well. We are now playing matchmaking role between customers and brands that otherwise had to spend a lot of money in marketing.”

One of the biggest propositions of CRED is that it has been able to court some of the most sought-after customers in India. Unlike many other startups and giants such as Google and Facebook, CRED is not going after the next billion users.

“About 20 million customers account for 90% of all online consumption in India. These are the customers we are focusing on,” said Shah, who previously ran financial services firm Freecharge and delivered one of the rare successful exits in the country. The core challenge in chasing customers in smaller cities and towns in India is that very few people have the financial capacity to buy things, Shah said.

For that model to work, the GDP of India — where the average annual income of an individual is about $2,000 — needs to grow. And for that, we need more participation from females, said Shah. Less than 10% of the female population in India are currently part of the workforce, compared to over 90% in China.

An interesting use case for CRED today is that it could potentially license to venture firms data about the traction D2C brands are seeing on its platform, which could use it as a signal to inform their investment decisions.

Shah cautioned that the startup is “extraordinarily sensitive about data” but said the team is thinking about ways to help venture firms discover these firms. “We are planning to create a newsletter to showcase many of these brands to the investor world,” he said.

And finally, will CRED launch a credit card or other banking products? “Can we partner with banks to cross-sell every product that they today offer? The answer is yes,” said Shah, though he cautioned that the startup is in no hurry to supercharge its offerings.

Powered by WPeMatico