Klarna

Auto Added by WPeMatico

Auto Added by WPeMatico

Are founders in fundraising mode short-sighted when it comes to working with Chinese venture funds?

Runa Capital’s Asia business development manager Denis Kalinin studied data from iTjuzi, a database of Chinese venture capitalists, and found:

“…Chinese funds invested around $250 billion in 2020 (three times higher than the figure reported in Crunchbase). This figure puts Chinese VC investments only 30% lower than investments by U.S. funds, but three times that of U.K. funds and 12.5 times more than German funds.”

The pandemic, geopolitical tensions and other factors led many Chinese venture funds to pare back their international investments, but that’s largely “because during COVID, China’s economy recovered much faster than other countries’,” writes Kalinin.

His analysis covers multiple angles: Chinese investments in Europe are catching up with those in Asia and the United States, half of China’s top cross-border investors are CVCs, and investors are particularly interested in fintech, deep tech and digital health at the moment.

“Chinese investors can bring value to foreign startups, but you need to study their expertise and how it can be useful for you.”

Full Extra Crunch articles are only available to members

Use discount code ECFriday to save 20% off a one- or two-year subscription

Today at 2 p.m. PT/5 p.m. ET on Twitter Spaces, Managing Editor Danny Crichton and immigration law attorney Sophie Alcorn will discuss whether remote work is making H-1B visas less critical for international founders.

It’s a provocative question: If remote teams are becoming the norm, tech hubs are decentralizing and investors are comfortable cutting checks after a Zoom call, how important is it to do business as a startup inside the U.S?

It’s sure to be an interesting conversation; to get a reminder, please follow @TechCrunch on Twitter.

Thanks very much for reading Extra Crunch this week!

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Nigel Sussman (opens in a new window)

Toast released an early IPO price range of $30 to $33 per share on Monday, and Alex Wilhelm digs into the S-1/A filing to “better understand how to value vertical SaaS startups that are pursuing a payments-and-SaaS business approach.”

Is the restaurant software startup worth the $18 billion valuation it’s aiming for?

Image Credits: Peter Dazeley (opens in a new window) / Getty Images

Every founder who launches an enterprise software startup has to figure out the “right” pricing model for their products.

It’s a consequential decision: Per-seat licenses are easy to manage, but what if customers prefer a concurrent licensing model?

“Early pricing discussions should center around the buyer’s perspective and the value the product creates for them,” says Ridge Ventures partner Yousuf Khan, who previously worked as a CIO.

“Of course,” he notes, “self-evaluation is hard, especially when you’re asking someone else to pay you for something you’ve created.”

Image Credits: jayk7 / Getty Images

India’s mom-and-pop businesses are experiencing a digital transformation that’s creating new e-commerce opportunities; smartphones have replaced paper records, and a new government-backed instant payments system is disrupting how value is exchanged.

But instead of importing legacy credit systems, buy now, pay later systems are the “next step for solving the digital B2B puzzle,” writes Anubhav Jain, co-founder and CEO of Rupifi.

Image Credits: scyther5 / Getty Images

Freshworks, which develops and offers a variety of business software tools, set an IPO price range of $28 to $32 per share on Monday, meaning its valuation could reach nearly $10 billion, Alex Wilhelm writes.

“It appears that the Freshworks IPO is pretty reasonably priced as is, though a boost to its price range is not out of the question if public market investors decide that they are bullish on its future growth prospects. We just don’t see dramatic upside.”

ish on its future growth prospects. We just don’t see dramatic upside.”

Image Credits: Nigel Sussman (opens in a new window)

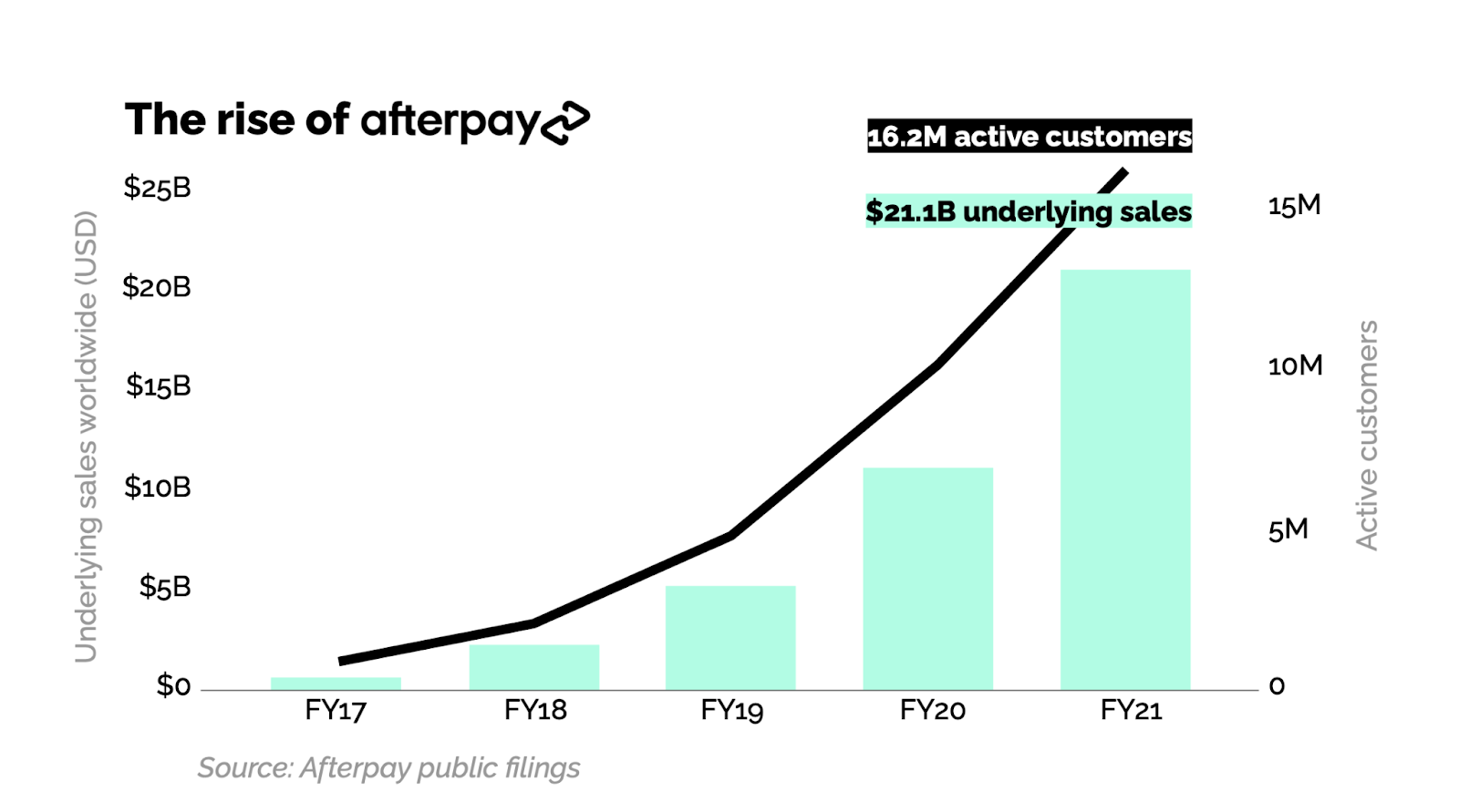

The multibillion-dollar exits of Japanese startup Paidy (to PayPal) and Australian buy now, pay later company Afterpay (to Square) “provided hard market proof that what BNPL startups are building has value beyond simple operating results,” Alex Wilhelm writes in The Exchange.

He breaks down the value of Afterpay, Paidy and Klarna using a simple metric: What would you pay for $1 of BNPL GMV?

Image Credits: mikkelwilliam (opens in a new window) / Getty Images

Video game livestreaming is booming.

Twitch has an average of almost 3 million concurrent viewers; by comparison, on the night of the 2020 U.S. presidential election, CNN’s livestream averaged 1.1 million.

The most successful streamers use their ad revenue and sponsorship money to hire video editors and social media teams to make them look good, but new automated tools are giving part-time streamers the ability to spotlight their best moments as well.

Image Credits: Boris Zhitkov (opens in a new window) / Getty Images

A data breach costs a company an average of $3.8 million, Marc Ellenbogen, Foursquare’s general counsel, notes in a guest post, adding up to a “concrete financial incentive to having The Privacy Talk.”

What is it?

“It’s the conversation that goes beyond the written, publicly posted privacy policy and dives deep into a customer, vendor, supplier or partner’s approach to ethics,” he writes.

If you think the talk doesn’t apply to you, think again.

Image Credits: Alexander Spatari (opens in a new window) / Getty Images

In an effort to “reassure local administrations that micromobility is safe, compliant and a good thing for cities,” scooter operators are “implementing technology similar to advanced driver assistance systems (ADAS) usually found in cars,” Rebecca Bellan writes.

She breaks down how the tech could help prevent unwanted behavior and explores the cost for scooter operators and opportunities for startups.

Powered by WPeMatico

It’s a two-Exchange Tuesday, everyone. First up, we’re talking fintech valuations. Next up, we’re digging into Atlanta.

Last week’s news that PayPal intends to buy Japanese startup Paidy marked the second major acquisition of a buy now, pay later (BNPL) company this year. PayPal’s news followed an even larger deal by Square for the Australian BNPL company Afterpay.

The multibillion-dollar exits provided hard market proof that what BNPL startups are building has value beyond simple operating results; major fintech platforms are willing to shell out large sums for their revenues and possible strategic value.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Because both deals happened in 2021, they provide two data points for the value of BNPL companies operating at scale. And because both Square and PayPal provided some information to their investors concerning their transactions, we have a little bit of comparative work to do.

Let’s do a little math and figure out how much PayPal and Square investors are paying for transaction volume across both platforms. Then, we’ll peek at what Affirm is worth along similar lines. We’ll wrap with a look at Klarna’s numbers to see if there’s anything we can dig up there.

Our goal is to find out what sort of price floor or ceiling the Paidy and Afterpay deals imply, if other players in their space are matching that figure, and why. This will be fun!

Our goal is to find out what sort of price floor or ceiling the Paidy and Afterpay deals imply, if other players in their space are matching that figure, and why. This will be fun!

Square’s Afterpay deal is worth some $29 billion, a huge sum. It isn’t hard to see why the U.S. consumer- and business-focused fintech is willing to write so large a check — Afterpay does volume.

Powered by WPeMatico

On Sunday Square announced it was gobbling up Afterpay in a deal worth $29 billion at the time of announcement. Alex followed up yesterday with more details on why the deal made sense for Square and Afterpay over here, but we wanted to ask some notable VCs what it means for the startup market.

For context, the Square deal follows a ton of money and interest flowing into the BNPL market. Just this year, VCs have invested in companies like Alma ($59.4 million, January 2021), Scalapay ($48 million, January 2021), Wisetack ($19 million, February 2021), Zilch ($80 million, April 2021) and Dividio ($30 million, June 2021).

Most of the investors we reached out to were generally bullish on the Square and Afterpay integration, but they were less excited about opportunities for other consumer BNPL businesses to emerge.

Then there’s Klarna, which raised $639 million at a post-money valuation of $45.6 billion in June, after raising $1 billion in March at a post-money valuation of $31 billion.

There’s also interest from some major public companies. After a slow start, PayPal is aggressively pushing BNPL services with merchants that offer it as a payment option. And there are reports that Apple is building its own BNPL offering through Apple Pay.

We reached out to Commerce Ventures founder and GP Dan Rosen, Better Tomorrow Ventures founding partner Jake Gibson, Fika Ventures partner TX Zhuo, and Matthew Harris of Bain Capital Ventures to see what they thought of the deal, as well as what it might mean for the opportunity for other BNPL companies and startups.

The main takeaways? “Buy now, pay later” may be effective at driving retail conversion, but scale matters and long-term margins look slim for BNPL startups.

Now, let’s hear from the venture community.

Why is the BNPL market so hot?

Powered by WPeMatico

Sunday was a big day in fintech: Afterpay has agreed to merge with Square. This agreement sets two of the most admired financial technology companies in recent history on a path to becoming one.

Afterpay and Square have the potential to build one of the world’s most important payments networks. Square has built a very significant merchant payment network, and, via Cash App, a thriving high-growth consumer payment service. However, these two lines of business have historically not been integrated. Together, Square and Afterpay will be able to weave all of these services together into a single integrated experience.

Afterpay and Cash App each have double-digit millions of consumers, and Square’s seller ecosystem and Afterpay’s merchant network both record double-digit billions of payment volume per year. From the offline register and the online checkout flow to sending money in just a few taps, Square and Afterpay will tell a complete story of next-generation economic empowerment.

As Afterpay’s only institutional venture investor, I wanted to share some perspective on how we got here and what this merger means for the future of consumer finance and the payments industry.

Afterpay and Square have the potential to build one of the world’s most important payments networks.

Every five to 10 years, the global payments industry undergoes a critical innovation cycle that determines the winners and losers for the next several decades. The last major transition was the shift to NFC-based mobile payments, which I wrote about in 2015. The major mobile OS vendors (Apple and Google) cemented their position in the global payments stack by deftly bridging the needs of the networks (Visa, Mastercard, etc.) and consumers by way of the mobile devices in their pockets.

Afterpay sparked the latest critical innovation cycle. Conceived in a living room in Sydney by a millennial, Nick Molnar, for millennials, Afterpay had a key insight: Millennials don’t like credit.

Millennials came of age during the global mortgage crisis of 2008. As young adults, they watched their friends and family lose their homes by overextending on mortgage debt, bolstering their already lower trust for banks. They also have record levels of student debt. Therefore, it’s no surprise that millennials (and Gen Z right behind them) strongly prefer debit cards over credit cards.

But it’s one thing to recognize the paradigm shift and quite another to do something about it. Nick Molnar and Anthony Eisen did something, ultimately building one of the fastest-growing payments startups in history on their core product: Buy now, pay later … and never any interest.

Afterpay’s product is simple. If you have $100 in your cart and choose to pay with Afterpay, it will charge your bank card (typically a debit card) $25 every two weeks in four installments. No interest, no revolving debt and no fees with on-time payments. For the millennial consumer, this meant they could get the primary benefit of a credit card (the ability to pay later) with their debit card, without the need to worry about all the bad things that come with credit cards — high interest rates and revolving debt.

All upside, no downside. Who could resist? For the early merchants, virtually all of whom relied on millennials as their key growth segment, they got a fair trade: Pay a small fee above payment processing to Afterpay, get significantly higher average order values and conversions to purchase. It was a win-win proposition and, with lots of execution, a new payment network was born.

Image Credits: Matrix Partners

Afterpay went somewhat unnoticed outside Australia in 2016 and 2017, but once it came to the U.S. in 2018 and built a business there that broke $100 million net revenues in only its second year, it got attention.

Klarna, which had struggled with product-market fit in the U.S., pivoted their business to emulate Afterpay. And Affirm, which had always been about traditional credit — generating a significant portion of their revenue from consumer interest — also noticed and introduced their own BNPL offering. Then came PayPal with “Pay in 4,” and just a few weeks ago, there has been news that Apple is expected to enter the space.

Afterpay created a global phenomenon that has now become a category embraced by mainstream players across the industry — a category that is on track to take a meaningful share of global retail payments over the next 10 years.

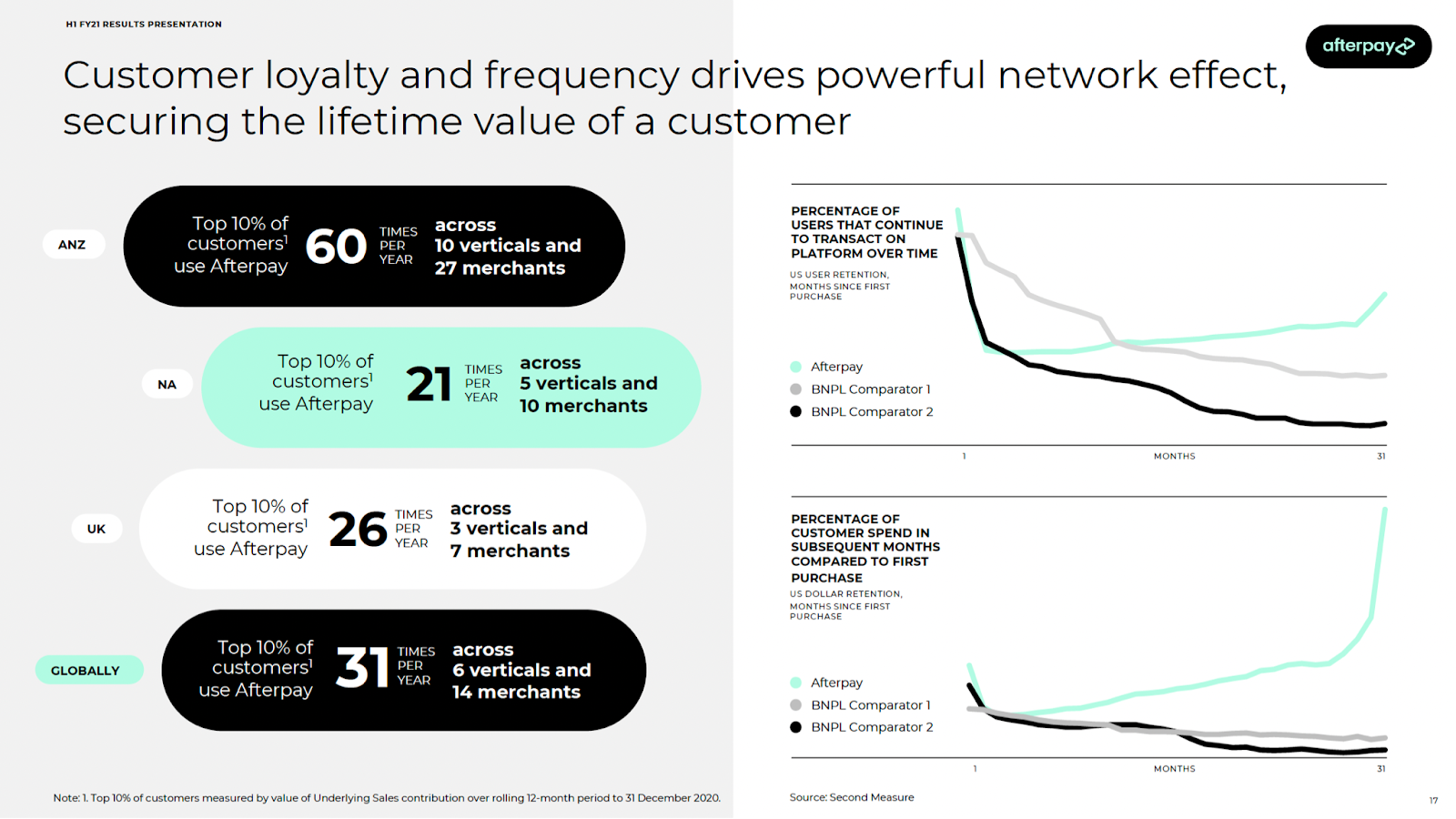

Afterpay stands apart. It has always been the BNPL leader by virtually every measure, and it has done it by staying true to their customers’ needs. The company is great at understanding the millennial and Gen Z consumer. It’s evident in the voice, tone and lifestyle brand you experience as an Afterpay user, and in the merchant network it continues to build strategically. It’s also evident in the simple fact that it doesn’t try to cross-sell users revolving debt products.

Most importantly, it’s evident in the usage metrics relative to competition. This is a product that people love, use and have come to rely on, all with better, fairer terms than were ever available to them than with traditional consumer credit.

Image Credits: Afterpay H1 FY21 results presentation

I’ve been building payment companies for over 15 years now, initially in the early days of PayPal and more recently as a venture investor at Matrix Partners. I’ve never seen a combination that has such potential to deliver extraordinary value to consumers and merchants. Even more so than eBay + PayPal.

Beyond the clear product and network complementarity, what’s most exciting to me and my partners is the alignment of values and culture. Square and Afterpay share a vision of a future with more opportunity and fewer economic hurdles for all. As they build toward that future together, I’m confident that this combination is a winner. Square and Afterpay together will become the world’s next generation payment provider.

Powered by WPeMatico

Shares of Square are up this morning after the company announced its second-quarter earnings and that it will buy Afterpay, an Australian buy now, pay later (BNPL) player in a $29 billion deal. As TechCrunch reported this morning, Afterpay shareholders will receive 0.375 shares of Square in exchange for their existing equity.

Shares of Afterpay are sharply higher after the deal was announced thanks to its implied premium, while shares of Square are up 7% in early-morning trading.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Over the past year, we’ve written extensively about the BNPL market, usually from the perspective of earnings from companies in the space. Afterpay has been a key data source, along with the yet-private Klarna and U.S. public BNPL outfit Affirm. Recall that each company has posted strong growth in recent periods, with the United States arising as a prime competitive market.

Most recently, consumer hardware and services giant Apple is reportedly preparing a move into the BNPL space. Our read at the time was that any such movement by Cupertino would impact mass-market BNPL players more than niche-focused companies. Apple has a fintech base and broad IRL payment acceptance, making it a potentially strong competitor for BNPL services aimed at consumers; BNPL services targeted at particular industries or niches would likely see less competition from Apple.

Most recently, consumer hardware and services giant Apple is reportedly preparing a move into the BNPL space. Our read at the time was that any such movement by Cupertino would impact mass-market BNPL players more than niche-focused companies. Apple has a fintech base and broad IRL payment acceptance, making it a potentially strong competitor for BNPL services aimed at consumers; BNPL services targeted at particular industries or niches would likely see less competition from Apple.

From that landscape, let’s explore the Square-Afterpay deal. We want to know what Afterpay brings to Square in terms of revenue, growth and reach. We also want to do some math on the price Square is willing to pay for the company — and what that might tell us about the value of BNPL and fintech revenues more broadly. Then we’ll eyeball the numbers and try to decide if Square is overpaying for Afterpay.

As with most major deals these days, Square and Afterpay released an investor presentation detailing their argument in favor of their combination. Let’s dig through it.

Square is a two-part company. It has a large consumer business via Cash App, and it has a large business division that offers payments tech and other fintech services to corporate customers. Recall that Square is also building out banking services for its business customers and that Cash App also serves some banking and investing functionality for consumers.

Powered by WPeMatico

The payments space — amazingly — remains up for grabs for startups. Yes, dear reader, despite the success of Stripe, there seems to be a new payments startup virtually every other day. It’s a mess out there! The accelerated growth of e-commerce due to the pandemic means payments are now a booming space. And here comes another one, with a twist.

WhenThen has built a no-code payment operations platform that, they claim, streamlines the payment processes “of merchants of any kind”. It says its platform can autonomously orchestrate, monitor, improve and manage all customer payments and payments ops.

The startup’s opportunity has arisen because service providers across different verticals increasingly want to get into open banking and provide their own payment solutions and financial services.

Founded six months ago, WhenThen has now raised $6 million, backed by European VCs Stride and Cavalry.

The founders, Kirk Donohoe, Eamon Doyle and Dave Brown, are three former Mastercard Payment veterans.

Based out of Dublin, CEO Donohoe told me: “We see traditional businesses embracing e-comm, and e-comm merchants now operating multiple business models such as trade supply, marketplace, subscription, and more. There is no platform that makes it easy for such businesses to create and operate multiple payment flows to support multiple business models in one place — that’s where we step in.”

He added: “WhenThen is helping e-commerce digital platforms build advanced payment flows and payment automation, in minutes as opposed to months. When you start to integrate different payment methods, different payment gateways, how you want the payment to move from collection through to payout gets very, very complex. I’ve been doing this for over a decade now, as an entrepreneur building different businesses that had to accept, collect and pay payments.”

He said his founding team “had to build very complex payment flows for large merchants, airlines, hotels, issuers, and we just found it was ridiculous that you have to continue to do the same thing over and over again. So we decided to come up with WhenThen as a better way to be able to help you build those flows in minutes.”

Claude Ritter, managing partner at Cavalry, said: “Basic payment orchestration platforms have been around for some time, focusing mostly on maximizing payment acceptance by optimizing routing. WhenThen provides the first end-to-end payment flow platform to equip businesses with the opportunity to control every stage of the payment flow from payment intent to payout.”

WhenThen supports a wide range of popular payment providers such as Stripe, Braintree, Adyen, Authorize.net, Checkout.com, etc., and a variety of alternative and locally preferred payment methods such as Klarna Affirm, PayPal and BitPay.

“For brave merchants considering global reach and operating multiple business models concurrently, I believe choosing the right payment ops platform will become as important as choosing the right e-commerce platform. Building your entire e-comm experience tightly coupled to a single payment processor is a hard correction to make down the line — you need a payment flow platform like WhenThen”, added Fred Destin, founder of Stride.VC.

Powered by WPeMatico

With the right message, even a small startup can connect with established and emerging stars on TikTok, Instagram and YouTube who will promote your products and services — as long as your marketing team understands the influencer marketplace.

Creators have a wide variety of brands and revenue channels to choose from, but marketers who understand how to court these influencers can make inroads no matter the size of their budget. Although brand partnerships are still the top source of revenue for creators, many are starting to diversify.

If you’re in charge of marketing at an early-stage startup, this post explains how to connect with an influencer who authentically resonates with your brand and covers the basics of setting up a revenue-share structure that works for everyone.

Full Extra Crunch articles are only available to members

Use discount code ECFriday to save 20% off a one- or two-year subscription

Our upcoming TC Early Stage event is devoted to marketing and fundraising, so expect to see more articles than usual about growth marketing in the near future.

We also ran a post this week with tips for making the first marketing hire, and Managing Editor Eric Eldon spoke to growth leader Susan Su to get her thoughts about building remote marketing teams.

We’re off today to celebrate the Juneteenth holiday in the United States. I hope you have a safe and relaxing weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: ballyscanlon (opens in a new window) / Getty Images

The pandemic forced a reckoning about the way we work — and whether we want to keep working in the same way, with the same people, for the same company — and many are looking for something different on the other side.

Art Zeile, the CEO of DHI Group, notes this means it’s a great time for startups to recruit talent.

“While all startups are certainly not focused on being disruptive, they often rely on cutting-edge technology and processes to give their customers something truly new,” Zeile writes. “Many are trying to change the pattern in their particular industry. So, by definition, they generally have a really interesting mission or purpose that may be more appealing to tech professionals.”

Here are four considerations for high-growth company founders building their post-pandemic team.

Image Credits: Bryce Durbin

“Refraction AI calls itself the Goldilocks of robotic delivery,” Rebecca Bellan writes. “The Ann Arbor-based company … was founded by two University of Michigan professors who think delivery via full-size autonomous vehicles (AV) is not nearly as close as many promise, and sidewalk delivery comes with too many hassles and not enough payoff.

“Their ‘just right’ solution? Find a middle path, or rather, a bike path.”

Rebecca sat down with the company’s CEO to discuss his motivation to make “something that is useful to the general public.”

Image Credits: RichVintage (opens in a new window)/ Getty Images

What are investors looking for?

Founders often tie themselves in knots as they try to project qualities they hope investors are seeking. In reality, few entrepreneurs have the acting skills required to convince someone that they’re patient, dedicated or hard working.

Johan Brenner, general partner at Creandum, was an early backer of Klarna, Spotify and several other European startups. Over the last two decades, he’s identified five key traits shared by people who create billion-dollar companies.

“A true unicorn founder doesn’t need to have all of those capabilities on day one,” Brenner, writes “but they should already be thinking big while executing small and demonstrating that they understand how to scale a company.”

Image Credits: TechCrunch

EV sales are driving demand for services and startups that fulfill the new needs of drivers, charging station operators and others.

Evette Ellis and Ben Schippers took to the main stage at TC Sessions: Mobility 2021 to share how their companies capitalized on the new opportunities presented by the electric transportation revolution.

Image Credits: Alexandr Wang

Scale co-founder and CEO Alex Wang joined us at TechCrunch Sessions: Mobility 2021 to discuss his company’s role in the autonomous driving industry and how it’s changed in the five years since its founding.

Scale helps large and small AV players establish reliable “ground truth” through data annotation and management, and along the way, the standards for what that means have shifted as the industry matures.

Even if two algorithms in autonomous driving might be created more or less equal, their real-world performance could vary dramatically based on what they’re consuming in terms of input data. That’s where Scale’s value prop to the industry starts, and Wang explains why.

Image Credits: Getty Images / Vertigo3d

The prevailing post-pandemic edtech narrative, which predicted higher ed would be DOA as soon as everyone got their vaccine and took off for a gap year, might not be quite true.

Natasha Mascarenhas explores a new crop of edtech SaaS startups that function like guidance counselors, helping students with everything from study-abroad opportunities to swiping right on a captivating college (really!).

“Startups that help students navigate institutional bureaucracy so they can get more value out of their educational experience may become a growing focus for investors as consumer demand for virtual personalized learning increases,” she writes.

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie,

My co-founders and I launched a software startup in Iran a few years ago, and I’m happy to say it’s now thriving. We’d like to expand our company in California.

Now that President Joe Biden has eliminated the Muslim ban, is it possible to do that? Is the pandemic still standing in the way? Do you have any suggestions?

— Talented in Tehran

Image Credits: Rudzhan Nagiev (opens in a new window) / Getty Images

Chris Jackson, the vice president of client development at CompTrak, writes in a guest column that having a conversation about diversity, equity and inclusion initiatives and “agreeing on the need for equality doesn’t mean it will be achieved on an organizational scale.”

He lays out a data-driven proposal that brings in everyone from directors to HR to the talent acquisition team to get companies closer to actual equity — not just talking about it.

Image Credits: TechCrunch

Few people are more closely tapped into the innovations in the transportation space than investors.

They’re paying close attention to what startups and tech companies are doing to develop and commercialize autonomous vehicle technology, electrification, micromobility, robotics and so much more.

For TC Sessions: Mobility 2021, we talked to three VCs about everything from the pandemic to the most overlooked opportunities within the transportation space.

Image Credits: TechCrunch

Automakers’ interest in robotics is not a new phenomenon, of course: Robots and automation have long played a role in manufacturing and are both clearly central to their push into AVs.

But recently, many companies are going even deeper into the field, with plans to be involved in the wide spectrum of categories that robotics touch.

At TC Sessions: Mobility 2021, we spoke to a trio of experts at three major automakers about their companies’ unique approaches to robotics.

Image Credits: James D. Morgan/Getty Images

Apple’s location devices — called AirTags — have been out for more than a month now. The initial impressions were good, but as we concluded back in April: “It will be interesting to see these play out once AirTags are out getting lost in the wild.”

That’s exactly what our resident UX analyst, Peter Ramsey, has been doing for the last month — intentionally losing AirTags to test their user experience at the limits.

This Extra Crunch exclusive helps bridge the gap between Apple’s mistakes and how you can make meaningful changes to your product’s UX.

Image Credits: NanoStockk (opens in a new window) / Getty Images

Robotic process automation (RPA) is no longer in the early-adopter phase.

Though it requires buy-in from across the organization, contributor Kevin Buckley writes, it’s time to gather everyone around and get to work.

“Automating just basic workflow processes has resulted in such tremendous efficiency improvements and cost savings that businesses are adapting automation at scale and across the enterprise,” he writes.

Long story short: “Adapting business automation for the enterprise should be approached as a business solution that happens to require some technical support.”

Image Credits: TechCrunch

Mobility should be a right, but too often it’s a privilege. Can startups provide the technology and the systems necessary to help correct this injustice?

At our TC Sessions: Mobility 2021 event, we sat down with Revel CEO and co-founder Frank Reig, Remix CEO and co-founder Tiffany Chu, and community organizer, transportation consultant and lawyer Tamika L. Butler to discuss how mobility companies should think about equity, why incorporating it from the get-go will save money in the long run, and how they can partner with cities to expand accessible and sustainable mobility.

Image Credits: Carlin Ma / Madrona Venture Group/Brian Smale

Coda CEO Shishir Mehrotra and Madrona partner S. Somasegar joined Extra Crunch Live to go through Coda’s pitch doc (not deck. Doc) and stuck around for the ECL Pitch-off, where founders in the audience come “onstage” to pitch their products to our guests.

Extra Crunch Live takes place every Wednesday at 3 p.m. EDT/noon PDT. Anyone can hang out during the episode (which includes networking with other attendees), but access to past episodes is reserved exclusively for Extra Crunch members. Join here.

Powered by WPeMatico

About four years ago, social impact organization Norrsken Foundation launched a small program investing around €30 million in capital it had received from its wealthy patron, Klarna co-founder Niklas Adalberth.

Now, that initiative has become its own impact investment firm, Norrsken VC and, according to people familiar with the firm, is about to close on its first independent investment vehicle — a €125 million ($149) fund focused on investing in startups that are, as its website suggests, “solving the world’s biggest problems.”

Norrsken VC did not respond for a request for comment about the firm’s fundraising plans.

Already, the young firm has invested in companies that would be standouts among any venture capital portfolio. Norrsken VC is one of the early backers behind Northvolt, which just received a $14 billion order for its batteries for electric vehicles from Volkswagen.

Electrification is actually a big theme for the early-stage firm, which counts the electric plane technology developer, Heart Aerospace, and autonomous electric vehicle developer Einride, and the battery monitoring and data management startup, Nortical, among its other portfolio companies.

Einride scored another huge coup recently. TechCrunch reported that the company was close to closing on $75 million in new funding even as it explored a potential SPAC for its business.

Indeed, Norrsken Foundation’s work in investing presaged a surge in climate and sustainability-focused activity from both venture investors, public markets and entrepreneurs looking at how to aid in the transition from fossil fuels to renewable resources and other zero carbon sources of energy.

That thesis on energy consumption extends to other areas of the firm’s portfolio, including companies like the energy efficient data center designer and technology developer, Submer.

If electrification and efficiency are one area of focus in the climate fight, Norrsken has also made moves to combat waste and improve efficiency in the food chain, as well. It’s probably the largest area of focus for the firm’s current portfolio outside of electrification, and there appear to be some early winners emerging in that category.

Those range from startups focused on agriculture like WeFarm and Ignitia, to consumer waste in the food industry through investments in Olio, Matsmart and Whywaste.

Taken together the climate and sustainability thesis has been the largest and most opportune investment target, but healthcare and wellness are also within the firm’s investment mandate. Startups like Winningtemp are an interesting indication of the firm’s thesis. That startup provides ways to monitor and support employees’ mental health.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion. Use code “TCARTICLE at checkout to get 20% off tickets right here.

Powered by WPeMatico

Three years ago, we released the first edition of the Matrix Fintech Index. We believed then, as we do now, that fintech represents one of the most exciting major innovation cycles of this decade. In 2020, all the long-term trends forcing change in this sector continued and even accelerated.

The broad movement away from credit toward debit, particularly among younger consumers, represents one such macro shift. However, the pandemic also created new, unforeseen drivers. Among them, millennials decamped from their rentals in crowded cities to accelerate their first home purchases to the benefit of proptech companies and challenger mortgage players alike.

E-commerce saw an enormous acceleration in growth rates, furthering adoption of online payments platforms. Lastly, low interest rates and looming inflation helped pave the way for the price of Bitcoin to charge toward $30,000. In short, multiple tailwinds combined to produce a blockbuster year for the category.

In this year’s refresh of the Matrix Fintech Index, we’ll divide our attention into three parts. First, a look at the public stocks’ performance. Second, liquidity. Third, we highlight one major trend in the sector: Buy Now Pay Later, or BNPL.

For the fourth straight year, the publicly traded fintechs massively outperformed the incumbent financial services providers as well as every mainstream stock index. While the underlying performance of these companies was strong, the pandemic further bolstered results as consumers avoided appearing in-person for both shopping and banking. Instead, they sought — and found — digital alternatives.

For the fourth straight year, the publicly traded fintechs massively outperformed the incumbent financial services providers as well as every mainstream stock index.

Our own representation of the public fintechs’ performance is the Matrix Fintech Index — a market cap-weighted index that tracks the progress of a portfolio of 25 leading public fintech companies. The Matrix fintech Index rose 97% in 2020, compared to a 14% rise in the S&P 500 and a 10% drop for the incumbent financial service companies over the same time period.

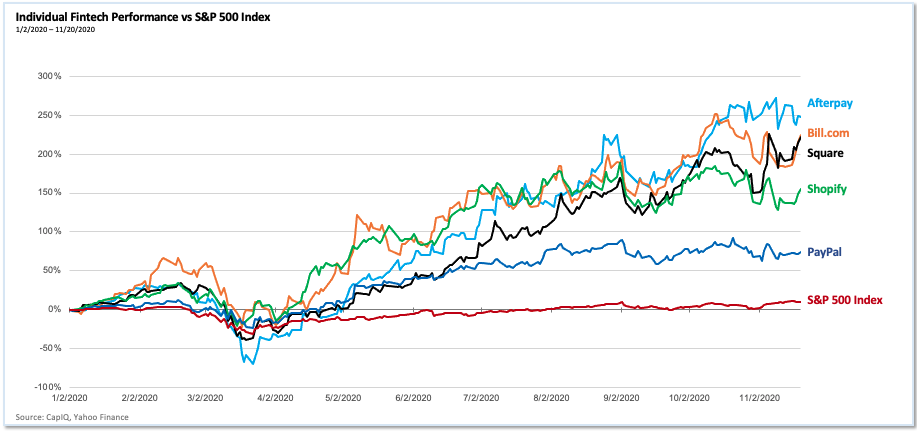

2020 performance of individual fintech companies vs. SPX Image Credits: CapiQ, Yahoo Finance

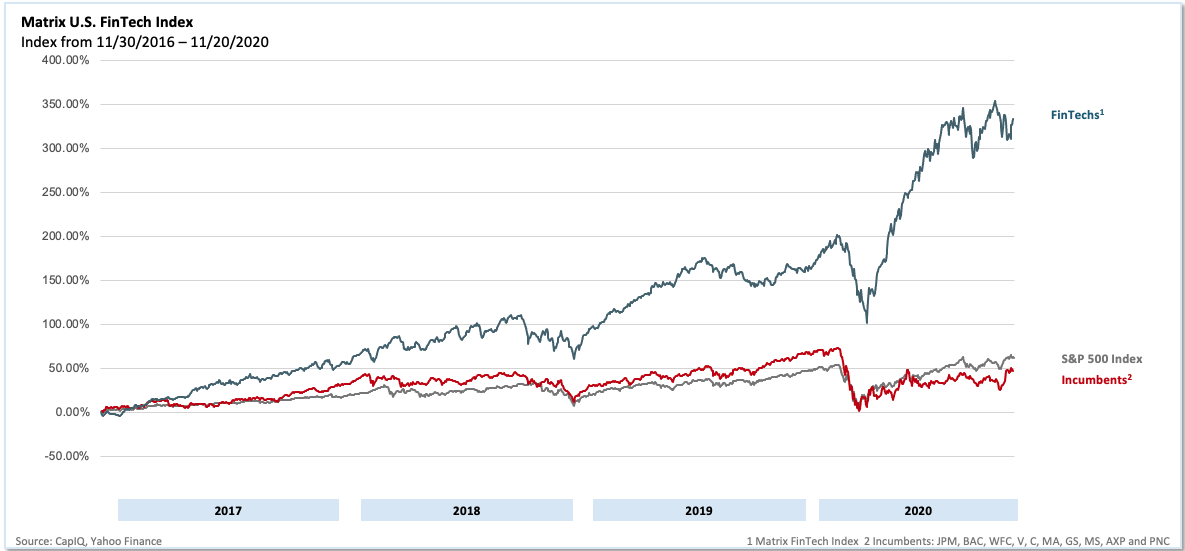

Matrix U.S. Fintech Index, 2016 -2020 Image Credits: CapiQ, Yahoo Finance

E-commerce undoubtedly stood out as a major driver. As a category, retail e-commerce grew 35% YoY as of Q3, propelling PayPal and Shopify to add over $160 billion of market capitalization over the year. For its part, PayPal in the third quarter signed up 15 million net new active accounts (its highest ever).

Powered by WPeMatico

Sebastian Siemiatkowski, the co-founder and CEO of Klarna — the Swedish fintech “buy now, pay later” sensation that is currently Europe’s most valuable private tech company — is dismissive of the suggestion that non U.S. companies should relocate to Silicon Valley if they really want to grow.

“We did hear that and I think it’s very poor advice,” he says. An overheated market for tech talent and the fickle nature of employees that are constantly job-hopping, he argues, make it harder to build a company for the long term.

Then he goes further.

“When I went to San Francisco for the first time about 10 years ago, [it] was a magical place. It was the early days of Facebook, there was an amazing vibe. When I go to San Francisco today, it’s changed to become, in my opinion, fairly cold.”

Siemiatkowski, a Swedish national and the son of two immigrants from Poland, is also sceptical of the “American dream.” In contrast to America, he points out how Sweden is among the most successful societies in the world from a social mobility perspective — referencing its free education and free health care, which sets up as many people as possible for success. But there is one caveat: he doesn’t think first-generation immigrants in Sweden do nearly as well as their children.

“We didn’t have a lot of money,” he tells me. “My father was driving a cab, he was unemployed for many years, even though he had basically a doctorate in agronomy. That’s kind of the unfortunate part of this, but that has obviously created a massive amount of hunger with me.”

As second generation success stories go, the rise of Klarna is up there with the best, even if it has already been 15 years in the making.

Backed by the likes of Sequoia, Silverlake, and Atomico, a new $650 million funding round in September gave the company a whopping $10.65 billion valuation — almost double the price achieved a year earlier, cementing its status as a poster child for Europe’s ability to build tech companies valued far above $1 billion. Siemiatkowski still owns an 8.1 percent stake.

Klarna is also, perhaps, even more mythical than a unicorn: a fintech that has been profitable nearly from the get-go. That only changed in 2019, when it decided to incur losses in favor of investing millions trying to conquer the U.S. market, choosing New York and L.A. over San Francisco for its American offices.

The company has been built on the concept of giving consumers a way to buy things online without having to pay for them upfront, and without resorting to a credit card. It does this both by offering online retailer integrations where Klarna appears as an option at check out, and through its own “shopping mall” app, where users can browse all the stores that let you pay with Klarna. On the back of this, the company hopes to foster a bigger financial relationship with its users as a fully-fledged bank.

If a bank is partly about corralling enough users on to your platform to pay money in and out, Klarna is well on its way. Today, the company boasts a registered customer base of 90 million, 11 million of which are in the U.S. In the last year alone, 21 million users were added globally. Klarna’s direct to consumer app, which sits alongside its 200,000 strong merchant point of sale integrations, has 14 million active users globally. Combined, Klarna is processing over 1 million transactions per day through its platform.

Image Credits: Klarna

This growth has continued apace as Klarna rides one macro trend and bucks another: Prompted by the pandemic, e-commerce has gone gangbusters, while, conversely, consumer credit as a whole has been in decline as people are paying down longer-term debt in record numbers. Even before COVID-19, Klarna and other buy now, pay later providers had been successfully picking up the slack created by a credit card market that, in some countries, has been steadily contracting.

Yet with a business model that generates the majority of its revenue by offering consumers short-term credit — and against a backdrop where the idea of easy credit and infinite consumption is increasingly criticised — the fintech giant is not without detractors.

When I mention Klarna to people who work in the European tech industry, the reaction tends to fall into one of three camps: those who reference the company’s “weird” above the line advertising and social media campaigns; those who use the service regularly and talk in terms of guilty pleasures; and those who are outright scornful of the impact on society they perceive Klarna to be making. And it’s true: You can’t help but be suspicious of something that gives consumers the feeling that they can spend money they might not have. And those “Smoooth” ads (below) certainly don’t offer much reassurance.

Delve a little deeper, however, and it becomes clear that the company’s business model can be misunderstood and that the arguments playing out in the media for and against buy now, pay later is only one part of the Klarna story.

In a wide-ranging interview, Siemiatkowski confronts criticisms head on, including that Klarna makes it too easy to get into debt, and that buy now, pay later needs to be regulated. We also discuss Klarna’s business model and the balancing act required to win over consumers and keep merchants onside.

We also learn how, under his watch and as the company began to scale, Klarna missed the next big opportunity in fintech, instead being usurped by Adyen and Stripe. Siemiatkowski also shares what’s next for the company as it ventures further into the world of retail banking after gaining a bank license in 2017.

And, told publicly for the first time, Siemiatkowski reveals how he once sought out PayPal co-founder Max Levchin as an advisor, only to learn a little later that he had started Affirm, one of Klarna’s most direct U.S. competitors and sometimes described by Europeans as a Klarna clone.

But first, let’s go back to the beginning.

Klarna’s first ever transaction took place at 11:06:40 am on April 10, 2005 at a Swedish bookshop called Pocketklubben, according to the abbreviated history published on the company’s website. However, what is made less explicit is that there was likely very little technology involved. The real innovation was a business one, with Klarna’s young and non-technical founders, Sebastian Siemiatkowski, Niklas Adalberth and Victor Jacobsso, taking an old idea and reconfiguring it for the burgeoning e-commerce industry.

By enabling customers that shopped online to be mailed an invoice with 30 days to pay, online shopping could be made easier and safer for consumers, which in turn helped increase sales for retailers.

“The invoicing company”

“When they started, they didn’t position themselves so much as a startup or as a tech company,” recalls Skype founder Niklas Zennström, whose venture capital firm Atomico would eventually become a Klarna investor in 2012. “People referred to them as the invoicing company.”

Today, Klarna is most certainly a tech company, employing 1,300 software engineers out of a staff of over 3,500. The company is now entirely cloud based and with various fully automated processes, from credit risk processing to algorithms in the Klarna shopping app to personalize content for individual consumers to AI/machine learning for 24 hour customer service.

Crucially, however, even this early and rudimentary version of what would become ‘buy now, pay later’ ticked two important boxes. Consumers, especially those who were distrusting of e-commerce, could be sure they’d receive goods before being charged, and if for any reason a product needed to be returned, customers wouldn’t have to wait weeks to be reimbursed as they hadn’t outlaid cash in the first place. Arguably both problems were already solved by credit cards, but in countries like Sweden, credit card take up was low, while the humble debit card doesn’t carry the same consumer protections as a credit card.

“The reason that we were able to launch it and be successful was because we were in a market where debit cards were much more prevalent than credit cards,” says Siemiatkowski. “And most people who have credit cards don’t reflect on the fact that if you have a debit card and you shop online, you face a number of struggles that a credit card holder does not.”

Those “struggles” include tying up your own money for the time it takes to return an item and process a refund. In contrast, when you spend on a credit card, the merchant is effectively holding your credit card company’s money.

“If I am buying some items and feel a bit unsafe about the merchant I’m using, if there’s a credit card, I don’t feel like I’m risking my money. If it’s my salary money you’re actually holding as a merchant for three weeks while you’re processing the return, that’s a problem,” Siemiatkowski argues.

Instead, Klarna would step in and offer to pay the merchant up front while providing customers 30 days to settle their invoice. Later this would be extended to include installments as an option. In return for taking on all of the risk and promising to increase conversions, merchants would give the Swedish upstart a percentage cut of the transactions.

“They wanted to make it really simple by just putting in your name, your Social Security number, and then you can instantaneously get an option to get an invoice sent to you later on. So what it did was remove a lot of friction from buying,” says Zennström.

Meanwhile, the more retailers sold, the more revenue Klarna would generate, all without consumers having to be charged interest on what might otherwise be described as a short-term loan. Pitch perfect, you might think. However, in early 2005 and before the company was incorporated, the concept was stress-tested at a “Shark Tank”-style event held at the Stockholm School of Economics and attended by the King of Sweden. The judging panel, made up of prominent Swedish financiers, were not convinced and Klarna’s invoicing idea came last in the competition. Despite the loss, Siemiatkowski held on to feedback from an unknown member of the audience, who surmised that banks would never launch something similar. Siemiatkowski left undeterred.

Angel investment from a former Erlang Systems sales manager, Jane Walerud, followed and she put Klarna’s founders in contact with a team of developers who helped build the first version of the platform. However, it soon surfaced that there was a misunderstanding in relation to the equity promised and how it should be linked to a longer commitment to the project.

Reflects Siemiatkowski: “One of the drawbacks that we had at the company was that none of the three co-founders had any engineering background; we couldn’t code. We were connected to five engineers that by themselves were amazing engineers, but we had a slight misunderstanding. Their idea was that they were going to come in, build a prototype, ship it, and then leave for 37% of the equity. Our understanding was that they were going to come in, ship it, and if it started scaling they would stay with us and work for a longer period of time. This is the classic mistake that you do as a startup.”

Eventually, the original five engineers quit, leaving Siemiatkowski to manage something he didn’t understand. “We obviously hired a CTO, but I also needed to be able to evaluate his decision making and all of these things in order to be able to assess whether we had the right setup to achieve what we want to achieve,” he says.

Between 2006 and 2008, Klarna continued to grow as more people started shopping online. The company expanded beyond Sweden to neighboring Nordic countries Norway, Finland and Denmark, with a headcount that had reached 120 employees. Even though there were signs of growth, Siemiatkowski says it still took a long time to realise that if Klarna was ever going to be really successful, it needed to fully transform into a tech company.

“We were really good at sales, we were okay at marketing, [and] we were service oriented: we really delivered to our customers. But it wasn’t really that technology driven,” he concedes.

To attract the kind of tech talent required, Siemiatkowski decided he needed to woo a renowned tech investor. Further backing had come in 2007 from Swedish investment firm Investment AB Öresund, but by 2010 the Klarna CEO had two new targets in his sights: Niklas Zennström, the Swedish entrepreneur who had already achieved legend status back home after building and selling Skype, and Sequoia Capital, the Silicon Valley venture capital firm that had invested in Apple, Google and PayPal.

“Part of our thinking about how we make Klarna attractive for people with engineering backgrounds was to get an investor that really had the brand and could kind of put their mark on us and say, ‘this is a tech company,’” says Siemiatkowski.

There is every likelihood that Zennström’s Atomico would have joined Klarna’s cap table in 2010 if it weren’t for a single line of text published on the VC firm’s website, which read something like, “don’t contact us, we’ll contact you.” Europe’s startup ecosystem was still immature and what now seems like aloofness was probably nothing more than a crude way to deter cold pitches from non-venture type businesses. But whatever the intent, it would be another two years before the firm eventually had the opportunity to invest in Klarna at what was almost certainly a much higher valuation.

“That was our loss for being too arrogant,” says Zennström. “Clearly we didn’t pursue them, we didn’t discover them because we didn’t have them on our radar. When we got to know them [two years later], what we liked a lot as a firm was the pain point that they were addressing.

“E-commerce was a relatively low single digit penetration of all retail, but of course growing, and we have always believed that e-commerce is going to continue to grow and become bigger than physical retailers. We thought that if you can remove that friction of the payment, and offer people different payment methods, that’s a really big proposition.”

“I always tease Niklas about it,” admits Siemiatkowski. “They wanted to, you know, keep it exclusive and I get it. So we were like, ‘okay, we can’t get hold of them, so let’s talk to Sequoia instead.’”

However, cold calling Sequoia wasn’t going to cut it either, not only because the firm didn’t generally invest in Europe, but also by Siemiatkowski’s own admission, Klarna didn’t look much like a tech company at the time. Luckily, a mutual contact got wind that Sequoia was on the lookout for interesting companies in the region and Klarna’s name was promptly thrown into the mix.

“Chris [Olsen], who was working at Sequoia at the time, called me, [but] I had this idea that I needed to be hard to catch. So I decided to not call back for three days, which was a very nervous time where I was just sitting on my hands not doing anything,” he said. “It was like, I don’t want to look like I’m too interested in this. Eventually, after three days, I call back and we did an exclusive deal with them, which I don’t recommend companies do.”

In hindsight, the Klarna CEO advises that it’s always smarter to foster competition in a round. As the only show in town, Sequoia invested at a $100 million valuation. “They bought 25 percent of the company and that was kind of it,” he says.

Siemiatkowski believes a company is made up of three things.

The first he calls internal momentum: “How fast are we moving as an organisation? How good are the decisions we are taking? How much are we avoiding [company] politics? How much of a true meritocracy are we?”

The second is profit and loss.

And the third is valuation. In a small company these three things are closely correlated in time, he says, “so if you have great internal momentum, you will instantly see it in your P&L, and then you will instantly see that hopefully in your company valuation as well.”

But in a large company, because of its size, the challenge is that they start to become disconnected. “They’re obviously in the long term always 100% correlated, but in the short term, they can vary a lot,” cautions Siemiatkowski.

Unsurprisingly, fueled by Sequoia’s cash, Klarna continued to grow in 2010, ending the year with $54 million in annual revenue, an increase of 80%. In December 2011, General Atlantic and DST would invest $155 million in a round that gave Klarna the coveted status of a unicorn.

Siemiatkowski says, compared to the company’s subsequent $5.5 billion and $10.65 billion valuations, this is the one that put him under the most self-scrutiny.

“In just one and a half years, we went from $100 million to a $1 billion. And then I felt the pressure,” he tells me. “I felt like we made it such a competitive round because we wanted to compensate for what we saw partially as a mistake with Sequoia that we kind of went too far the other way.”

Klarna finally took Atomico’s money in 2012, and within two years had grown to over 1,000 employees. Along with multiple offices around the globe, the company moved to bigger headquarters in Stockholm and expanded to the U.K. with an office in central London. Yet, somewhere along the way, Siemiatkowski says Klarna had lost internal momentum.

“As the company scaled and we started adding more markets and growing fast, for me as CEO and co-founder, I found that very difficult,” he admits. “As long as we were up to 100 people, I found it easier, I understood how to talk to people, how to get things done, how to develop new products or features and so forth. It was all much less complex, and then we started approaching a couple of hundred people and I felt more and more lost in all of that.

“It was difficult, and at the same point of time, we still had a lot of success because we had built this product that worked really well and there was a lot of momentum coming solely from the product itself.”

Siemiatkowski says that most startups don’t recognize that “once you get the snowball rolling, you can actually do quite a lot of stupid things, and the snowball will continue rolling.”

The Klarna CEO doesn’t say it, but one of those “stupid things” came in 2012 when the startup faced a backlash in its home country. Instead of sending payment instructions in the post, the company had switched to email without considering that messages might go to spam or simply remain unread. This saw customers unintentionally defaulting and then being chased for payment, leading to accusations in the media that Klarna was tricking people so it could generate more revenue through late fees.

Powered by WPeMatico