Jeremy Liew

Auto Added by WPeMatico

Auto Added by WPeMatico

When “Law & Order” ended its 20-year run in 2010, it had already cemented its place as one of the longest-running television dramas in history. Its success was a testament to the enduring popularity of a good mystery.

Mining that same well of a demand for whodunnits, a roughly one-year-old Los Angeles-based startup called Solve has raised $20 million in financing to update the genre for a new generation of media consumers.

Its eponymously titled social media programming, available on Instagram and Snap, has managed to nab roughly 30 million interactions over the year-and-a-half that it distributed its productions. Now the company is launching a true crime podcast on the iHeartMedia and Apple platforms to tap into another potentially high-growth market.

Solve began as a series developed within the mobile-focused entertainment studio, Vertical Networks. Helmed by Tom Wright and financed by Elisabeth Murdoch (through her Freelands Ventures fund, which Wright also managed) and Snap, the company was one of the early entrants to raise cash as a production studio for mobile content. But it was far from the only studio to see money in mobile-first entertainment. All of the major internet-age media companies had their own mobile strategies.

Murdoch eventually replaced Wright (so that he could work on spinning up Solve as an independent entity) and sold Vertical Networks two months ago to the online media startup, Whistle, for an undisclosed amount.

“I spent a year looking deep, deep, deep into audience behavioral data on Snap and Facebook,” Wright says. “The DNA of what I thought [audience] sensibilities was leading towards was this format.”

As Vertical Networks was winding down, Solve was spinning up with help from Lightspeed Venture Partners, Upfront Ventures and Advancit Capital.

“We’ve seen incredibly popular crime mystery shows across media, including podcasts like Serial and Dirty John, TV shows like Making a Murderer and Law & Order, and movies like The Usual Suspects and Gone Girl,” said Jeremy Liew, partner at Lightspeed Venture Partners, in a statement. “Games have attained a first class status as media but we’ve yet to see a crime mystery format game achieve the same success, and Solve is going to right that wrong.”

The gamification element that’s made Solve’s episodes resonate with mobile audiences on social platforms will be a small part of the initial series, says Wright, with plans to expand the interactive elements going forward.

Produced in partnership with SALT audio, whose previous work includes “Blackout” and “Carrier” and iHeartMedia, the 10-episode series uses the same “ripped from the headlines” storytelling for its 30-minute broadcasts and offers listeners clues in leaked audio files, voicemails, courtroom testimony and other evidence to try to guess the killer.

For now, Solve is content to be a studio producing ad-supported media for platforms like Apple, Snap, Facebook, iHeartMedia and other distributors, according to Wright. It’s a different path than studios like Quibi, which is creating its own streaming service dedicated to mobile storytelling and backed by many of the major Hollywood studios.

The current pace of production means that Solve is making 18 original episodes per month. For the 40-year-old Wright, Solve represents a fourth foray into the world of startups. And while he’s not a fan of the crime or mystery genre himself, Wright said that the data around engagement was too compelling to not try to launch a business around it.

“The Internet has changed how we interact with the world from taxis to news to shopping. We believe that Solve can fundamentally change how we interact with narrative video storytelling,” said Mark Suster, managing partner, Upfront Ventures, in a statement. “When we heard Tom’s vision for short-form video that you not only watch but also must ‘solve‘, we knew that it had enormous potential.”

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week, I wrote about Stripe’s grand plans. Before that, I noted Peloton’s secret weapons.

Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets. If you don’t subscribe to Startups Weekly yet, you can do that here.

The best companies are built by people who have personally experienced the problem they’re attempting to solve. Lauren Jonas, the founder and chief executive officer of Part & Parcel, is intimately familiar with the struggles faced by the women she’s building for.

San Francisco-based Part & Parcel is a plus-sized clothing and shoe startup providing dimensional sizing to women across the U.S. The company operates a bit differently than your standard direct-to-consumer business by seeking to include the women who wear and evangelize the Part & Parcel designs by giving them a cut of their sales.

Here’s how it works: Ambassadors sign up to receive signature styles from Part & Parcel, which they then share and sell to women in their network. Ultimately, the sellers are eligible to receive up to 30% of the profit per sale. The out-of-the-box model, which might remind you somewhat of Mary Kay or Tupperware’s business strategy, is meant to encourage a sense of community and usher in a new era in which plus-sized women can facilitate other plus-sized women’s access to great clothes.

“I bought a brown men’s polyester suit and wore it to an interview,” Jonas, an early employee at Poshmark and the long-time author of the popular blog, ‘The Pear Shape,’ tells TechCrunch. “I was that kid wearing a men’s suit.”

Clothing tailored to plus-sized women has long been missing from the retail market. Increasingly, however, new brands are building thriving businesses by catering precisely to the historically forgotten demographic. Dia&Co., for example, raised another $70 million in venture capital funding last fall from Sequoia and USV. And Walmart recently acquired another brand in the space, ELOQUII, for an undisclosed amount. Part & Parcel, for its part, has raised $4 million in seed funding in a round led by Lightspeed Venture Partners’ Jeremy Liew.

The startup launched earlier this year in Anchorage, “a clothing desert,” and has since grown its network to include women in several other underserved markets. Given her own history struggling to find a fitted woman’s suit, Jonas launched her line with structured pieces, including suits and blouses — though the startup’s biggest success yet, she says, has been its boots, which come in three different calf width options.

“Seventy percent of women in this country are plus-sized,” Jonas said. “I’m bringing plus out of the dark corner of the department store.”

Image: Bryce Durbin / TechCrunch

TechCrunch’s Megan Rose Dickey published a highly anticipated deep dive on the state of sex tech this week. The piece provides new data on funding in sex tech and wellness companies, analysis on sex tech startup’s battle for public advertising and responses from industry leaders on how we can destigmatize sex with technology. Here’s a short passage from the story:

Cindy Gallop sees a market opportunity in every type of business obstacle she encounters. That’s why All The Sky will also seek to invest in startups that tackle the infrastructural tools needed to fuel sextech, like payments, hosting providers and e-commerce sites.

“I want to fund the sextech ecosystem to maintain and sustain a portfolio for All the Skies, to create a bloody huge sextech ecosystem and three, to monopolistically build out the ecosystem to be a multi-trillion-dollar market,” Gallop says.

I swung by Contrary Capital‘s Demo Day this week, in which a number of startups gave a 4- to 5-minute pitch. Next on my list is Alchemist‘s Demo Day in Menlo Park. The accelerator welcomes enterprise startups for a six-month program focused on early customer adoption, company development and mentorship.

Also on my radar is Females To The Front. The event began this week in Palm Springs and if I were based in SoCal, I would have swung by. Led by Amy Margolis, the event is said to be the largest gathering of female cannabis founders and funders to date. Here’s how the group describes the event: “Females to the Front Retreat will mix immersive and hands-on workshops, pitch training, investment deck preparation and business skill set education with investor meetings and plenty of shared meals, pool time, yoga, connections, rest and rejuvenation. Every workshop is built to directly engage attendees instead of powerpoint and panels. Be prepared to return home inspired, engaged and with so many more tools in your toolbox.”

For the record, I don’t advertise events in my newsletter just wanted to give props to this one because it’s a great development for the cannabis tech ecosystem.

We are just weeks away from our flagship conference, TechCrunch Disrupt San Francisco. We have dozens of amazing speakers lined up. In addition to taking in the great line-up of speakers, ticket holders can roam around Startup Alley to catch the more than 1,000 companies showcasing their products and technologies. And, of course, you’ll get the opportunity to watch the Startup Battlefield competition live. Past competitors include Dropbox, Cloudflare and Mint… You never know which future unicorn will compete next.

You can take a look at the full agenda here. And if you still need convincing, here’s five reasons to attend this year’s conference from our COO himself.

This week, the lovely Alex Wilhelm, editor-in-chief of Crunchbase News, and I gathered to discuss a number of topics including WeWork’s IPO and Uber’s attempts to bypass a new law meant to protect gig workers. Listen here.

Powered by WPeMatico

This week’s banishment of host Scott Rogowsky was merely a symptom of the ongoing struggle to decide who will lead HQ Trivia. According to multiple sources, over half of the startup’s staff signed an internal petition to depose CEO Rus Yusupov who they saw as mismanaging the company. But Yusupov then fired three core supporters of the mutiny, leading to a downward spiral of morale that mirrors HQ’s plummeting App Store rank.

TechCrunch spoke to multiple sources familiar with HQ Trivia’s internal troubles to piece together how the live video mobile game went from blockbuster to nearly bust. Two sources said HQ recently only had around $6 million in the bank but was burning over $1 million per month, meaning its runway could be dwindling. But its early investors are reluctant to hand Yusupov any more cash. “

Employees petitioned to remove HQ Trivia’s CEO Rus Yusupov

HQ reimagined gaming and mobile entertainment with the launch of its 12-question trivia game in August 2017 where players all competed live in twice-daily shows with anyone who got all the answers right split a cash jackpot. The games felt urgent since you could only participate at designated times, fun to play against friends or strangers, and winning carried a significance no single-player or non-stop online game could match.

When TechCrunch wrote the first coverage of HQ Trivia in October 2017, it had just 3500 concurrent players. But by January it had climbed to the #3 game and #6 overall app in the App Store, and grown to 2.38 million players by March. Quickly, copycats from China and Facebook entered the market. But they all lacked HQ’s secret weapon — its plucky host comedian Scott Rogowsky. Affectionately awarded nicknames like Quiz Daddy, Quiz Khalifa, Host Malone, and Trap Trebek from the “HQties” who played daily, he was the de facto face of the startup.

Yet HQ had some shaky foundations. Co-founder Colin Kroll, who’d also started Vine with Yusupov and sold it to Twitter, had been fired from Twitter after 18 months for being a bad manager, Recode reported. He’d also picked up a reputation of being creepy around female employees, as well as Vine stars, TechCrunch has learned. Rapid growth and an investigation by early HQ investor Jeremy Liew that found no egregious misconduct by Kroll paved the way for a $15 million investment. The round was led by Founders Fund’s Cyan Bannister, and it valued HQ at over $100 million.

Yusupov failed to translate that cash into sustained growth and product innovation. His public behavior had already raised flags. He yelled at a Daily Beast reporter after the outlet’s Taylor Lorenz interviewed Rogowsky without Yusupov’s approval, threatening to fire the host. “You’re putting Scott’s job in jeopardy. Is that what you want? . . . Please read me your story word for word,” Yusupov said. When he learned Rogowsky had expressed his preference for salad restaurant chain Sweetgreen, Yusupov shouted “He cannot say that! We do not have a brand deal with Sweetgreen! Under no circumstances can he say that.” The next day, Yusupov falsely claimed he’d never threatened Rogowsky’s job.

With HQ’s bank account full, sources say Yusupov was extremely slow to make decisions, allowing HQ to stagnate. The novelty of playing trivia for money via phone has begun to wear off, and people increasingly ignored HQ’s push notifications to join its next game. But beyond bringing in some guest hosts and the option to buy a second chance after a wrong answer, HQ ceased to evolve. HQ fell to the #196 game on iOS and the #585 overall app as concurrent players waned.

![]()

That’s when things started to get a bit Game Of Thrones.

Liew pushed for HQ to swap Kroll into the CEO spot in September 2018 while moving Yusupov to Chief Creative Officer, which was confirmed despite an HR complaint against Kroll for aggressive management. However, three sources tell TechCrunch that Yusupov pushed that HQ employee to file the complaint against Kroll. As the WSJ reported after Kroll’s death, that employee later left the startup because they felt that they’d been exploited. “There was definitely what felt like manipulation there, and that’s also why that employee resigned from the company.” one source said. Another source said that staffer “believed Rus used their unhappiness about work to use them as a pawn in his CEO war and not because Rus actually cared about resolving things.”

Cyan of Founders Fund stepped down from HQ’s board after the decision to swap out Yusupov due to her firm’s reputation of keeping founders in control, Recode’s Kurt Wagner reported. Sources say that despite Kroll’s reputation, the staff believed in him. “Colin loved HQ and was dedicated to all the employees more than Rus. Rus cares about Rus. Colin cared about the content” a source tells me.

Three sources say that in a desperate ploy to retain power and prevent Kroll’s rise, Yusupov suggested Rogowsky, a comedian with no tech or management experience, be made CEO of HQ Trivia. He even suggested the company film a reality show about Rogowsky taking over. That idea was quickly shot down as preposterous.

“It was a very personal desperation tactic not to have Colin be CEO. It was not a professionally thought-out idea” a source tells me, though another said it was always hard to tell if Yusupov’s crazy ideas were jokes. Both Yusupov and HQ Trivia declined to respond to multiple requests for comment, but we’ll update if we hear back.

HQ Trivia co-founder Colin Kroll passed away in December

Then tragedy struck in December. Kroll, then CEO, was found dead in his apartment from a drug overdose. Employees were distraught over what would happen next. “Colin’s plan was to ship fast, and get new things out there” a source says, noting that Kroll had pushed for the release of HQ’s first new game type HQ Words modeled after Wheel Of Fortune. “He wasn’t perfect but in the time he was in charge, the ship started to turn, but when Rus took over again it was like the 9 months where we did nothing.”

By February 2019, HQ’s staff was fed up. Two sources confirm that 20 of the roughly 35 employees signed a letter asking the board to remove Yusupov and establish a new CEO. With HQ’s download rate continuing to sink, they feared he’d run the startup into the ground. One source suggested Yusupov might rather have seen the whole startup come crashing down with the blame placed on the product than have it come to light that he played a large hand in the fall. The tone of the letter, which was never formally delivered but sources believe the board knew of, wasn’t accusatory but a plea for transparency about the company’s future and the staff’s job security.

At a hastily convened all-hands meeting in late February, HQ investor Liew told the company his fund Lightspeed would support a search for a new CEO to replace Yusupov, and provide that new CEO with funding for 18 more months of runway. Liew told the staff he would step down from the board once that CEO was found, but the search continues and so Liew remains on HQ’s board.

“Mostly everyone was on Jeremy’s side as no one wanted to work under Rus. Jeremy wasn’t trying to screw him over the way Rus would screw other people over. He just wanted to do what was right, getting behind what everyone wanted” a source said of Liew.

Instead, HQ’s board moved forward with instituting a new executive decision-making committee composed of Yusupov, HQ’s head of production Nick Gallo, and VP of engineering Ben Sheats. Yusupov would remain interim CEO, and he continued to cling to power and there’s been little transparency about the CEO replacement process. Until a new CEO is found, HQ must subsist on its existing funds. The staff is “always worried about running out of runway” and are given vague answers when they ask leadership about how much money is left.

On March 1st, the committee emerged from a meeting and fired three employees who had spearheaded the petition and been vocal about Yusupov’s failings.

One who wasn’t fired was Rogowsky, despite sources saying at one point he’d tried to organize the staff to go on strike. Other employees had been cautious about standing up to Yusupov. “Everyone was terrified of retaliation. Their fears have totally been validated” a source explains. Engineers and other staffers with strong employment prospects began to drain out of the company. Those left were just trying to hold onto their jobs. Without inspiring leadership or a strategy to reverse user shrinkage, recruiting replacements would prove difficult.

Yusupov remains on the board, along with Tinder CEO Elie Seidman who Yusupov appointed to his additional common seat. Liew retains his seat until the new CEO is found and given that seat. And Kroll’s seat appears to have gone to Lightspeed partner Merci Victoria Grace. Lightspeed and Cyan of Founders Fund declined to respond to requests for comment.

Tensions at HQ and a desire to diversify his prospects led Rogowsky to pick up a side gig hosting baseball talk show ChangeUp on the DAZN network, TMZ reported this week. He’d hoped to continue hosting HQ during its big weekend contests. But tensions with Yusupov and the CEO’s desire for the host to remain exclusively at HQ led negotiations to sour causing Rogowsky to leave the startup entirely. TechCrunch was first to report that he’s been replaced by former HQ guest host Matt Richards, who Yusupov bluntly told me Friday had polled higher than Rogowsky in a SurveyMonkey survey of HQ’s top players.

In tweets, Rogowsky revealed that that “Sadly, it won’t be possible for me to continue hosting HQ concurrently as I had hoped” noting, “I wasn’t given the courtesy of a farewell show.” Finding a way to preserve Rogowsky’s ties to HQ likely would have been best for the startup. TechCrunch had raised the concern a year ago that unless Rogowsky was properly locked in with an adequate equity vesting schedule at HQ, he could leave. Or worse, he could be poached by Facebook, Snapchat, or YouTube to host an HQ competitor.

“Rus is a visionary but not a good leader. He is extremely manipulative in an unproductive way. He’s a dude who just cares a lot about his reputation” a source noted. “A lot of the negative sentiment amongst staff is the belief that he cares more about his reputation than the company itself.”

HQ’s next attempt to revive growth appears to be HQ Editor’s Picks, is described as “a new live show on your phone where our host shows funny viral videos and you decide on who gets paid.” Finally it seems willing to embrace the potential of interactive live video entertainment outside of trivia and puzzles. HQ Editor’s Picks will face an uphill battle, since HQ dropped out of the top 1500 iOS apps last month, according to App Annie. Sensor Tower estimates that HQ saw just 8 percent as many downloads in March 2019 as March 2018.

After the loss of its spirit animal Rogowsky, the employees’ chosen leader Kroll, the supervision of veteran investor Cyan, and its product momentum, tough questions are what remain for HQ Trivia. The company’s struggles have paralyzed its progress towards finding a new viral mechanic or game format that attracts users. While HQ Words is fun, it’s too similar to its trivia competition to change the startup’s trajectory. And all of the in-fighting could scare off any talent hoping to turn HQ around. Unfortunately, securing an extra life for the game will take a more than a $3.99 in-app purchase.

Powered by WPeMatico

Young founders who want to start companies while still in school have an increasing number of resources to tap into that exist just for them. Students that want to learn how to build companies can apply to an increasing number of fast-track programs that allow them to gain valuable early stage operating experience. The energy around student entrepreneurship today is incredible. I’ve been immersed in this community as an investor and adviser for some time now, and to say the least, I’m continually blown away by what the next generation of innovators are dreaming up (from Analytical Space’s global data relay service for satellites to Brooklinen’s reinvention of the luxury bed).

Bill Gates in 1973

First, let’s look at student founders and why they’re important. Student entrepreneurs have long been an important foundation of the startup ecosystem. Many students wrestle with how best to learn while in school —some students learn best through lectures, while more entrepreneurial students like author Julian Docks find it best to leave the classroom altogether and build a business instead.

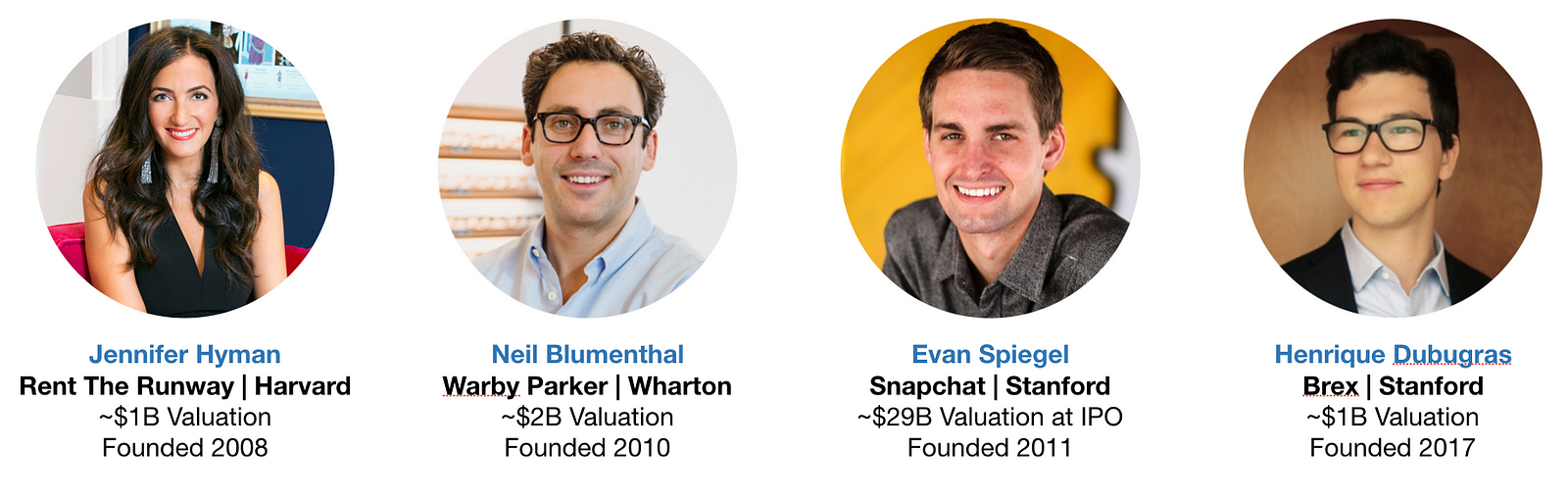

Indeed, some of our most iconic founders are Microsoft’s Bill Gates and Facebook’s Mark Zuckerberg, both student entrepreneurs who launched their startups at Harvard and then dropped out to build their companies into major tech giants. A sample of the current generation of marquee companies founded on college campuses include Snap at Stanford ($29B valuation at IPO), Warby Parker at Wharton (~$2B valuation), Rent The Runway at HBS (~$1B valuation), and Brex at Stanford (~$1B valuation).

Some of today’s most celebrated tech leaders built their first ventures while in school — even if some student startups fail, the critical first-time founder experience is an invaluable education in how to build great companies. Perhaps the best example of this that I could find is Drew Houston at Dropbox (~$9B valuation at IPO), who previously founded an edtech startup at MIT that, in his words, provided a: “great introduction to the wild world of starting companies.”

Student founders are everywhere, but the highest concentration of venture-backed student founders can be found at just 5 universities. Based on venture fund portfolio data from the last six years, Harvard, Stanford, MIT, UPenn, and UC Berkeley have produced the highest number of student-founded companies that went on to raise $1 million or more in seed capital. Some prospective students will even enroll in a university specifically for its reputation of churning out great entrepreneurs. This is not to say that great companies are not being built out of other universities, nor does it mean students can’t find resources outside a select number of schools. As you can see later in this essay, there are a number of new ways students all around the country can tap into the startup ecosystem. For further reading, PitchBook produces an excellent report each year that tracks where all entrepreneurs earned their undergraduate degrees.

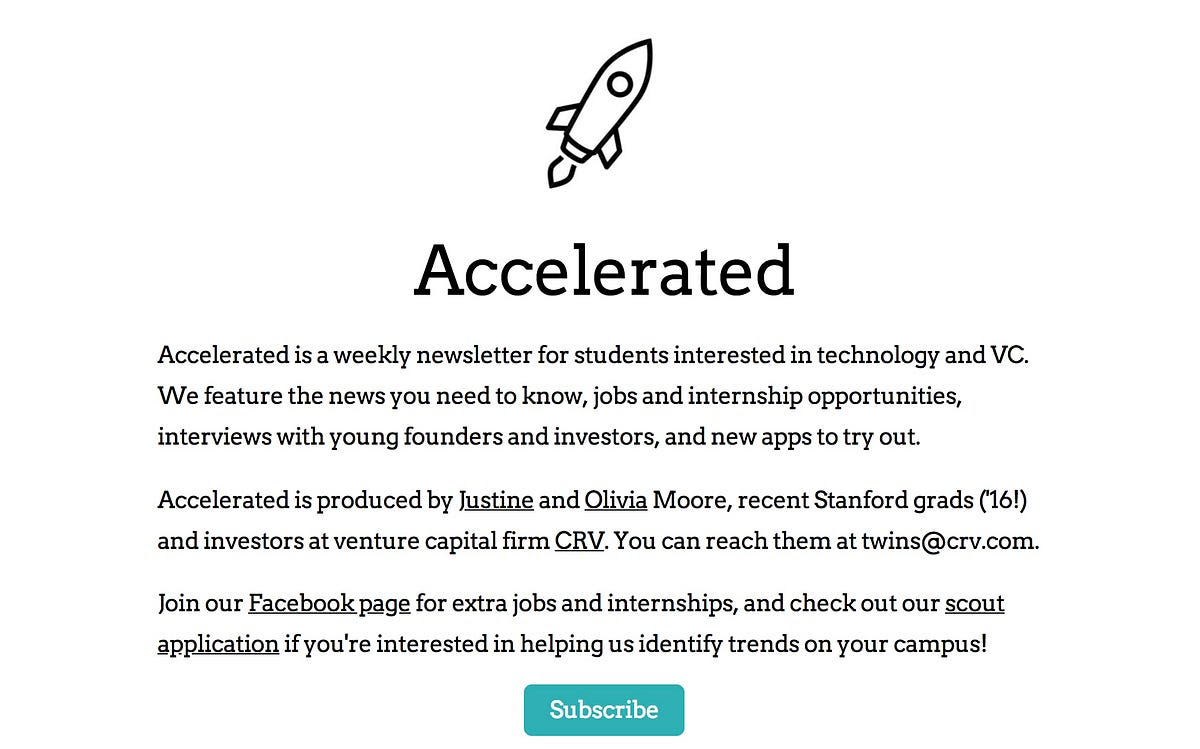

Student founders have a number of new media resources to turn to. New email newsletters focused on student entrepreneurship like Justine and Olivia Moore’s Accelerated and Kyle Robertson’s StartU offer new channels for young founders to reach large audiences. Justine and Olivia, the minds behind Accelerated, have a lot of street cred— they launched Stanford’s on-campus incubator Cardinal Ventures before landing as investors at CRV.

StartU goes above and beyond to be a resource to founders they profile by helping to connect them with investors (they’re active at 12 universities), and run a podcast hosted by their Editor-in-Chief Johnny Hammond that is top notch. My bet is that traditional media will point a larger spotlight at student entrepreneurship going forward.

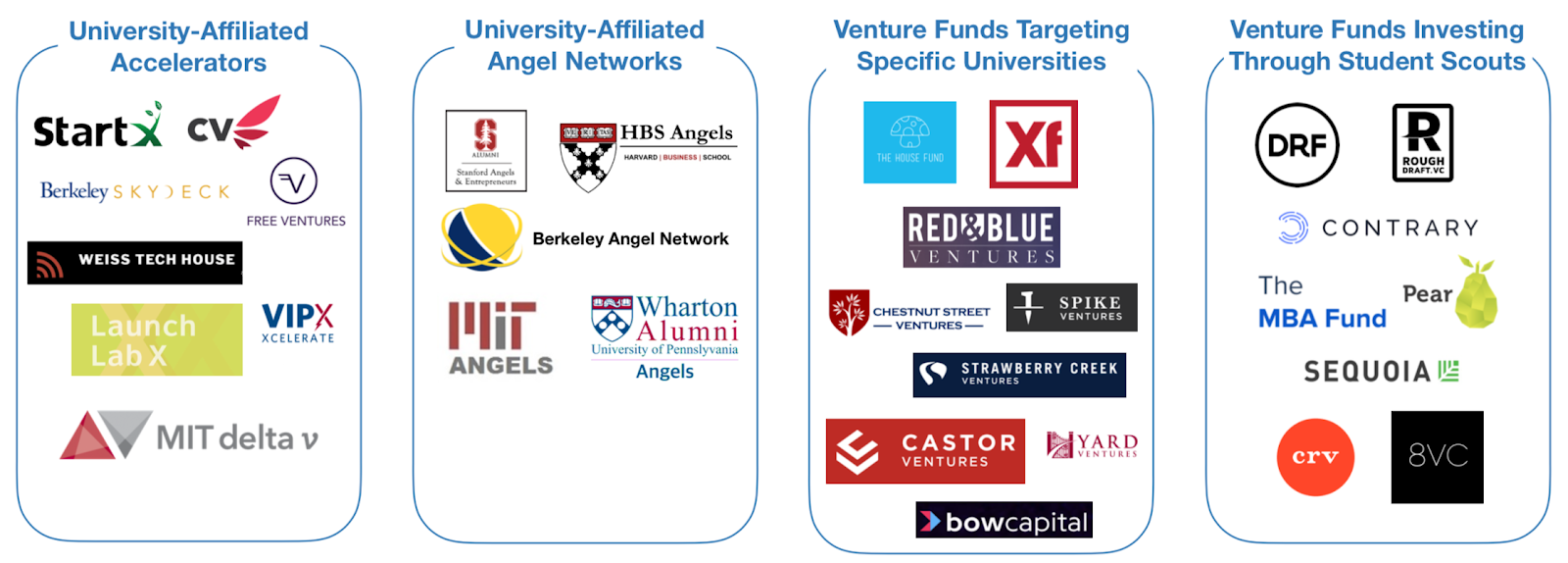

New pools of capital are also available that are specifically for student founders. There are four categories that I call special attention to:

While it is difficult to estimate exactly how much capital has been deployed by each, there is no denying that there has been an explosion in the number of programs that address the pre-seed phase. A sample of the programs available at the Top 5 universities listed above are in the graphic below — listing every resource at every university would be difficult as there are so many.

One alumni-centric fund to highlight is the Alumni Ventures Group, which pools LP capital from alumni at specific universities, then launches individual venture funds that invest in founders connected to those universities (e.g. students, alumni, professors, etc.). Through this model, they’ve deployed more than $200M per year! Another highlight has been student scout programs — which vary in the degree of autonomy and capital invested — but essentially empower students to identify and fund high-potential student-founded companies for their parent venture funds. On campuses with a large concentration of student founders, it is not uncommon to find student scouts from as many as 12 different venture funds actively sourcing deals (as is made clear from David Tao’s analysis at UC Berkeley).

Investment Team at Rough Draft Ventures

In my opinion, the two institutions that have the most expansive line of sight into the student entrepreneurship landscape are First Round’s Dorm Room Fund and General Catalyst’s Rough Draft Ventures. Since 2012, these two funds have operated a nationwide network of student scouts that have invested $20K — $25K checks into companies founded by student entrepreneurs at 40+ universities. “Scout” is a loose term and doesn’t do it justice — the student investors at these two funds are almost entirely autonomous, have built their own platform services to support portfolio companies, and have launched programs to incubate companies built by female founders and founders of color. Another student-run fund worth noting that has reach beyond a single region is Contrary Capital, which raised $2.2M last year. They do a particularly great job of reaching founders at a diverse set of schools — their network of student scouts are active at 45 universities and have spoken with 3,000 founders per year since getting started. Contrary is also testing out what they describe as a “YC for university-based founders”. In their first cohort, 100% of their companies raised a pre-seed round after Contrary’s demo day. Another even more recently launched organization is The MBA Fund, which caters to founders from the business schools at Harvard, Wharton, and Stanford. While super exciting, these two funds only launched very recently and manage portfolios that are not large enough for analysis just yet.

Over the last few months, I’ve collected and cross-referenced publicly available data from both Dorm Room Fund and Rough Draft Ventures to assess the state of student entrepreneurship in the United States. Companies were pulled from each fund’s portfolio page, then checked against Crunchbase for amount raised, accelerator participation, and other metrics. If you’d like to sift through the data yourself, feel free to ping me — my email can be found at the end of this article. To be clear, this does not represent the full scope of investment activity at either fund — many companies in the portfolios of both funds remain confidential and unlisted for good reasons (e.g. startups working in stealth). In fact, the In addition, data for early stage companies is notoriously variable in quality, even with Crunchbase. You should read these insights as directional only, given the debatable confidence interval. Still, the data is still interesting and give good indicators for the health of student entrepreneurship today.

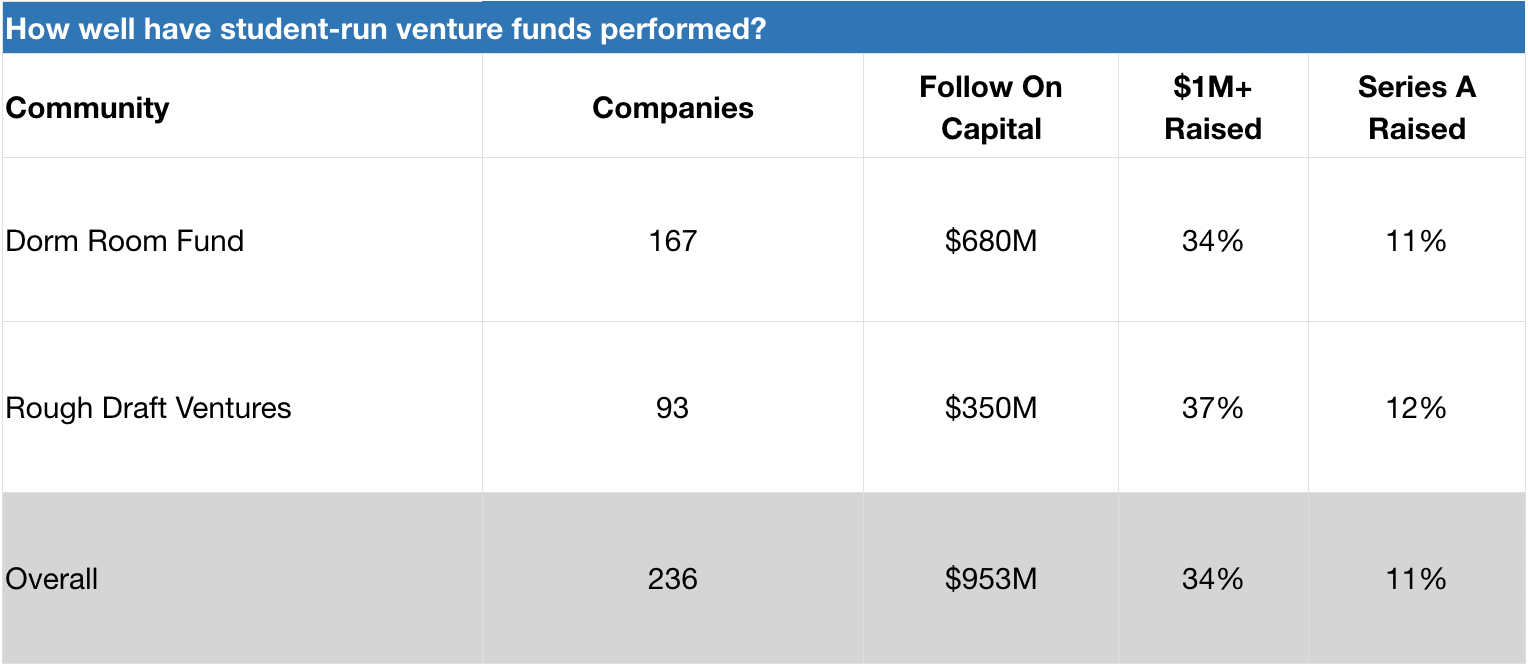

Dorm Room Fund and Rough Draft Ventures have invested in 230+ student-founded companies that have gone on to raise nearly $1 billion in follow on capital. These funds have invested in a diverse range of companies, from govtech (e.g. mark43, raised $77M+ and FiscalNote, raised $50M+) to space tech (e.g. Capella Space, raised ~$34M). Several portfolio companies have had successful exits, such as crypto startup Distributed Systems (acquired by Coinbase) and social networking startup tbh (acquired by Facebook). While it is too early to evaluate the success of these funds on a returns basis (both were launched just 6 years ago), we can get a sense of success by evaluating the rates by which portfolio companies raise additional capital. Taken together, 34% of DRF and RDV companies in our data set have raised $1 million or more in seed capital. For a rough comparison, CB Insights cites that 40% of YC companies and 48% of Techstars companies successfully raise follow on capital (defined as anything above $750K). Certainly within the ballpark!

Dorm Room Fund and Rough Draft Ventures companies in our data set have an 11–12% rate of survivorship to Series A. As a benchmark, a previous partner at Y Combinator shared that 20% of their accelerator companies raise Series A capital (YC declined to share the official figure, but it’s likely a stat that is increasing given their new Series A support programs. For further reading, check out YC’s reflection on what they’ve learned about helping their companies raise Series A funding). In any case, DRF and RDV’s numbers should be taken with a grain of salt, as the average age of their portfolio companies is very low and raising Series A rounds generally takes time. Ultimately, it is clear that DRF and RDV are active in the earlier (and riskier) phases of the startup journey.

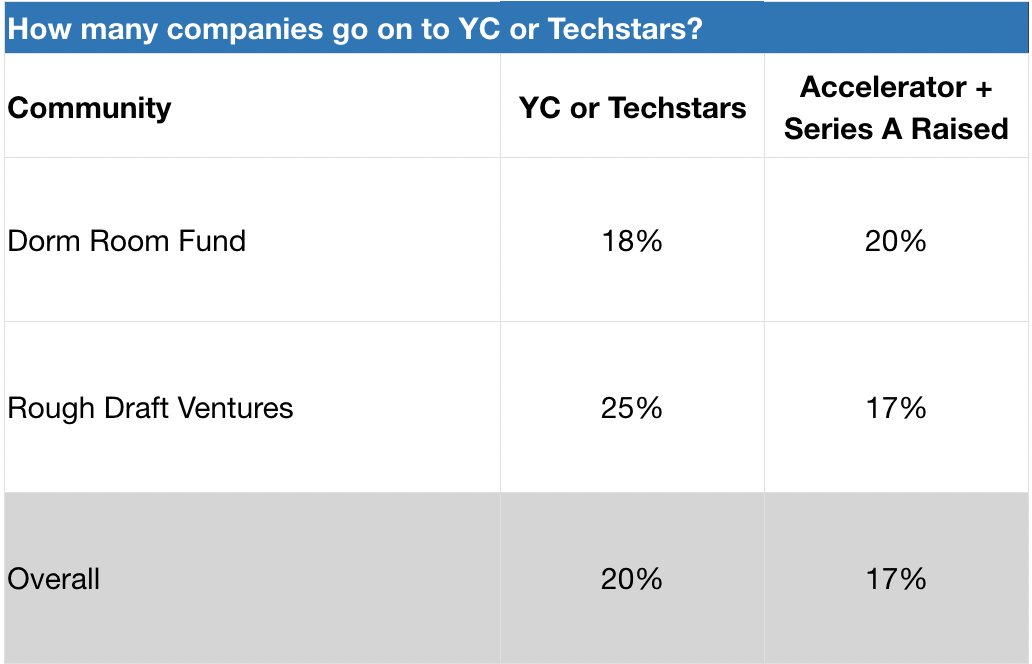

Dorm Room Fund and Rough Draft Ventures send 18–25% of their portfolio companies to Y Combinator or Techstars. Given YC’s 1.5% acceptance rate as reported in Fortune, this is quite significant! Internally, these two funds offer founders an opportunity to participate in mock interviews with YC and Techstars alumni, as well as tap into their communities for peer support (e.g. advice on pitch decks and application content). As a result, Dorm Room Fund and Rough Draft Ventures regularly send cohorts of founders to these prestigious accelerator programs. Based on our data set, 17–20% of DRF and RDV companies that attend one of these accelerators end up raising Series A venture financing.

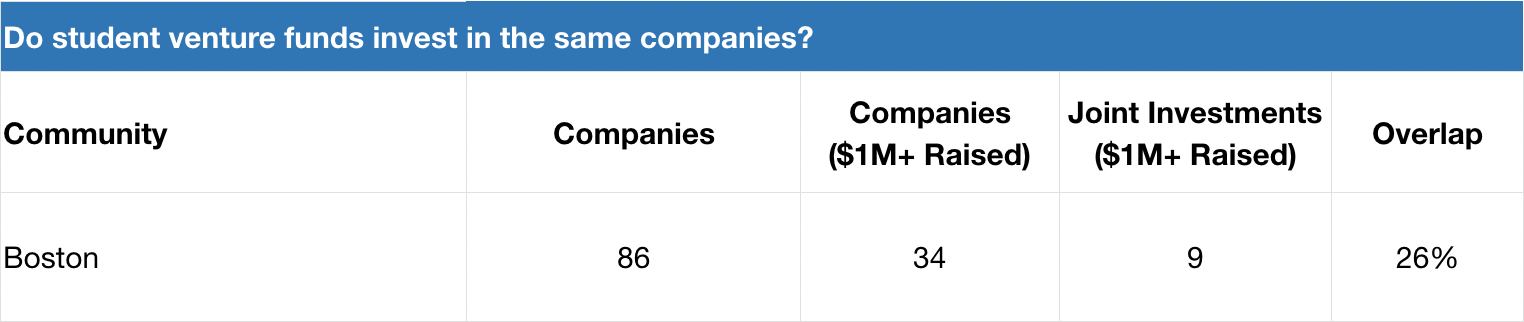

Dorm Room Fund and Rough Draft Ventures don’t invest in the same companies. When we take a deeper look at one specific ecosystem where these two funds have been equally active over the last several years — Boston — we actually see that the degree of investment overlap for companies that have raised $1M+ seed rounds sits at 26%. This suggests that these funds are either a) seeing different dealflow or b) have widely different investment decision-making.

Dorm Room Fund and Rough Draft Ventures should not just be measured by a returns-basis today, as it’s too early. I hypothesize that DRF and RDV are actually encouraging more entrepreneurial activity in the ecosystem (more students decide to start companies while in school) as well as improving long-term founder outcomes amongst students they touch (portfolio founders build bigger and more successful companies later in their careers). As more students start companies, there’s likely a positive feedback loop where there’s increasing peer pressure to start a company or lean on friends for founder support (e.g. feedback, advice, etc).Both of these subjects warrant additional study, but it’s likely too early to conduct these analyses today.

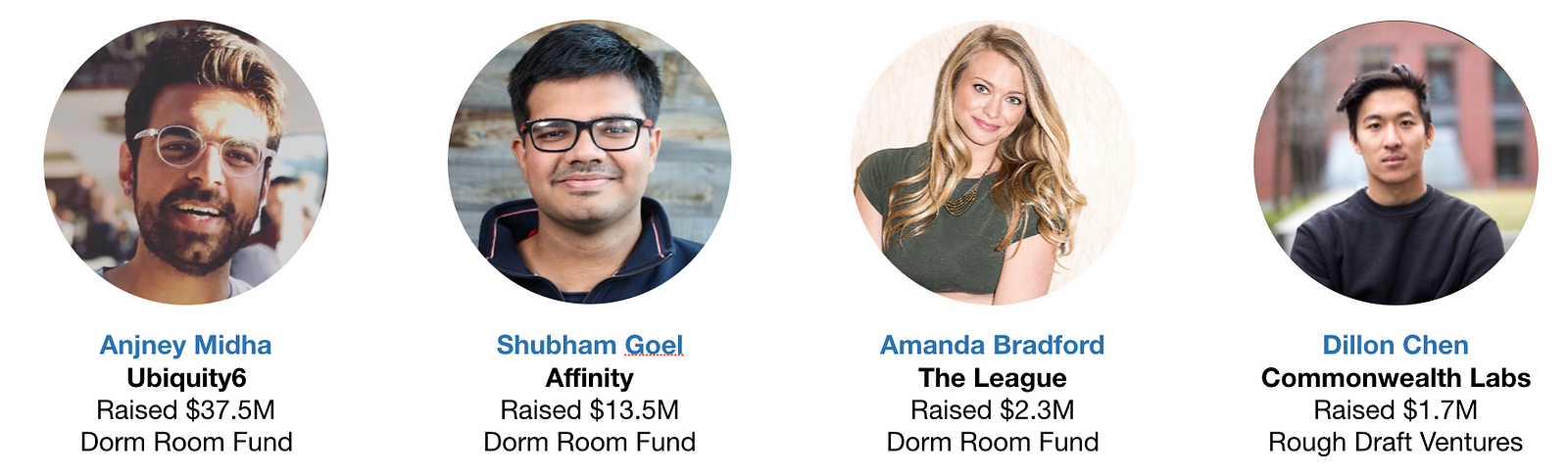

Dorm Room Fund and Rough Draft Ventures have impressive alumni that you will want to track. 1 in 4 alumni partners are founders, and 29% of these founder alumni have raised $1M+ seed rounds for their companies. These include Anjney Midha’s augmented reality startup Ubiquity6 (raised $37M+), Shubham Goel’s investor-focused CRM startup Affinity (raised $13M+), Bruno Faviero’s AI security software startup Synapse (raised $6M+), Amanda Bradford’s dating app The League (raised $2M+), and Dillon Chen’s blockchain startup Commonwealth Labs (raised $1.7M). It makes sense to me that alumni from these communities that decide to start companies have an advantage over their peers — they know what good companies look like and they can tap into powerful networks of young talent / experienced investors.

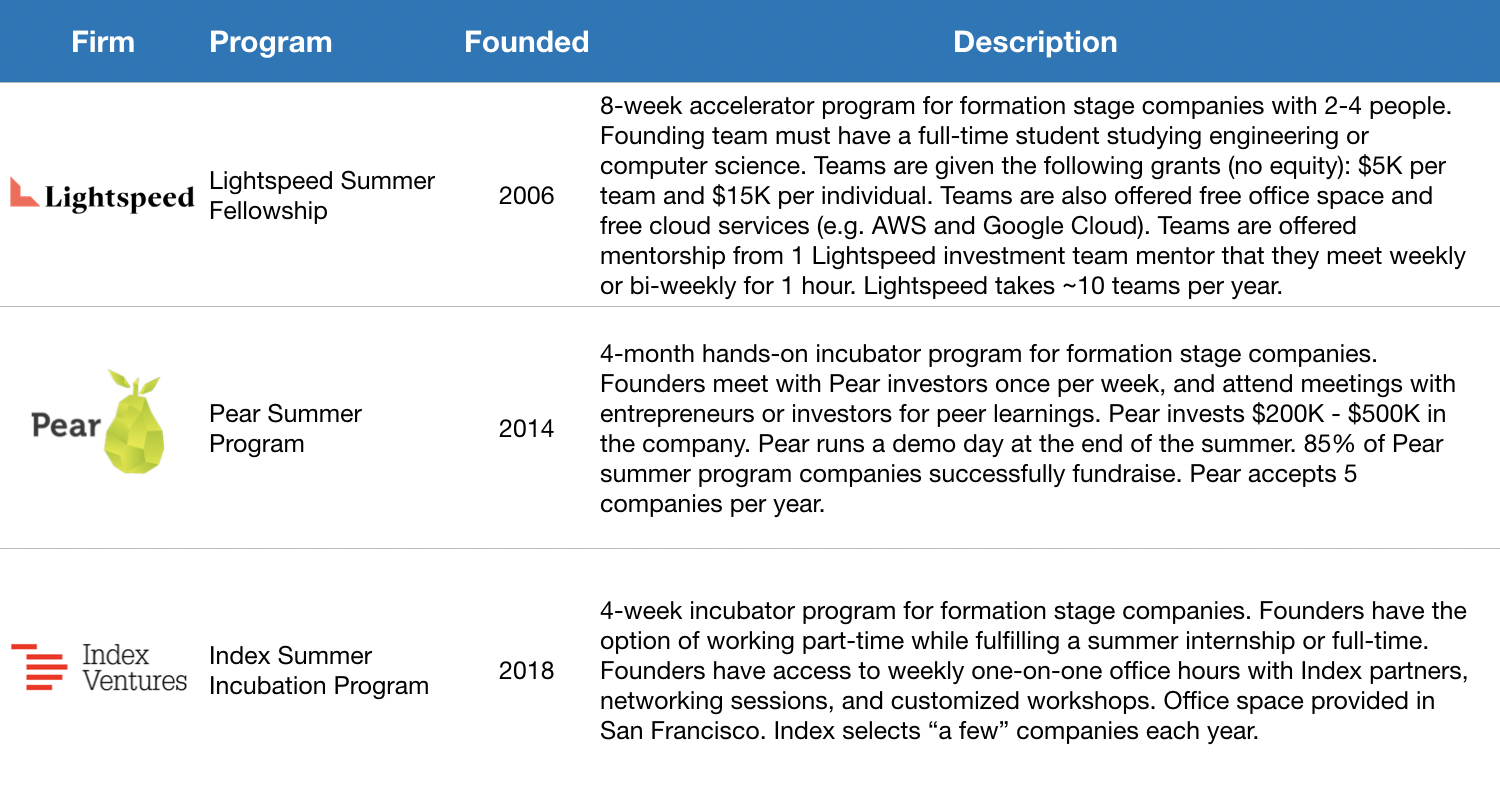

Beyond Dorm Room Fund and Rough Draft Ventures, some venture capital firms focus on incubation for student-founded startups. Credit should first be given to Lightspeed for producing the amazing Summer Fellows bootcamp experience for promising student founders — after all, Pinterest was built there! Jeremy Liew gives a good overview of the program through his sit-down interview with Afterbox’s Zack Banack. Based on a study they conducted last year, 40% of Lightspeed Summer Fellows alumni are currently active founders. Pear Ventures also has an impressive summer incubator program where 85% of its companies successfully complete a fundraise. Index Ventures is the latest to build an incubator program for student founders, and even accepts founders who want to work on an idea part-time while completing a summer internship.

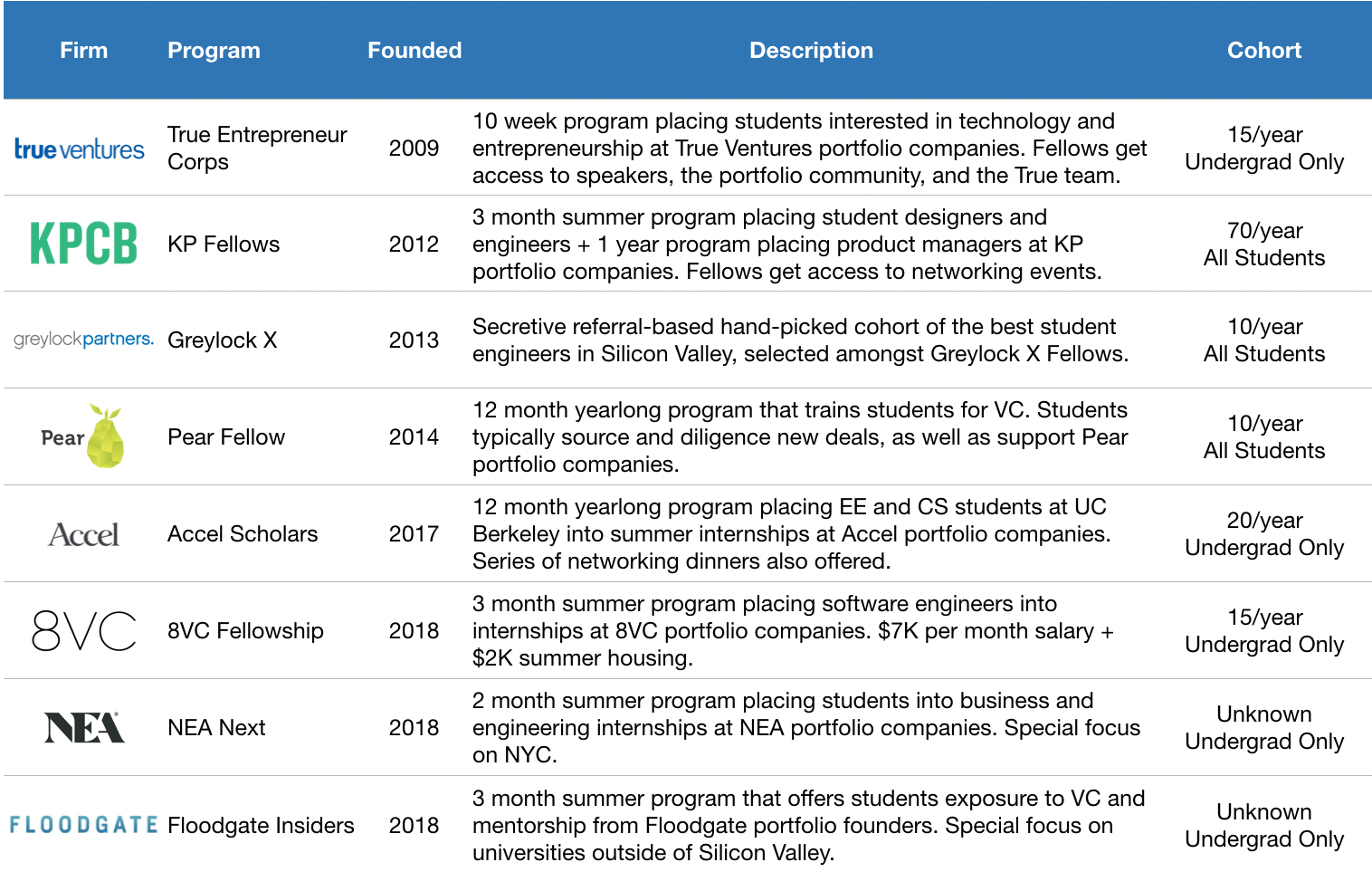

Let’s now look at students who want to join a startup before founding one. Venture funds have historically looked to tap students for talent, and are expanding the engagement lifecycle. The longest running programs include Kleiner Perkins’ class=”m_1196721721246259147gmail-markup–strong m_1196721721246259147gmail-markup–p-strong”> KP Fellows and True Ventures’ TEC Fellows, which focus on placing the next generation’s most promising product managers, engineers, and designers into the portfolio companies of their parent venture funds.

There’s also the secretive Greylock X, a referral-based hand-picked group of the best student engineers in Silicon Valley (among their impressive alumni are founders like Yasyf Mohamedali and Joe Kahn, the folks behind First Round-backed Karuna Health). As these programs have matured, these firms have recognized the long-run value of engaging the alumni of their programs.

More and more alumni are “coming back” to the parent funds as entrepreneurs, like KP Fellow Dylan Field of Figma (and is also hosting a KP Fellow, closing a full circle loop!). Based on their latest data, 10% of KP Fellows alumni are founders — that’s a lot given the fact that their community has grown to 500! This helps explain why Kleiner Perkins has created a structured path to receive $100K in seed funding to companies founded by KP Fellow alumni. It looks like venture funds are beginning to invest in student programs as part of their larger platform strategy, which can have a real impact over the long term (for further reading, see this analysis of platform strategy outcomes by USV’s Bethany Crystal).

KP Fellows in San Francisco

Venture funds are doubling down on student talent engagement — in just the last 18 months, 4 funds have launched student programs. It’s encouraging to see new funds follow in the footsteps of First Round, General Catalyst, Kleiner Perkins, Greylock, and Lightspeed. In 2017, Accel launched their Accel Scholars program to engage top talent at UC Berkeley and Stanford. In 2018, we saw 8VC Fellows, NEA Next, and Floodgate Insiders all launch, targeting elite universities outside of Silicon Valley. Y Combinator implemented Early Decision, which allows student founders to apply one batch early to help with academic scheduling. Most recently, at the start of 2019, First Round launched the Graduate Fund (staffed by Dorm Room Fund alumni) to invest in founders who are recent graduates or young alumni.

Given more time, I’d love to study the rates by which student founders start another company following investments from student scout funds, as well as whether or not they’re more successful in those ventures. In any case, this is an escalation in the number of venture funds that have started to get serious about engaging students — both for talent and dealflow.

Student entrepreneurship 2.0 is here. There are more structured paths to success for students interested in starting or joining a startup. Founders have more opportunities to garner press, seek advice, raise capital, and more. Venture funds are increasingly leveraging students to help improve the three F’s — finding, funding, and fixing. In my personal view, I believe it is becoming more and more important for venture funds to gain mindshare amongst the next generation of founders and operators early, while still in school.

I can’t wait to see what’s next for student entrepreneurship in 2019. If you’re interested in digging in deeper (I’m human — I’m sure I haven’t covered everything related to student entrepreneurship here) or learning more about how you can start or join a startup while still in school, shoot me a note at sxu@dormroomfund.com. A massive thanks to Phin Barnes, Rei Wang, Chauncey Hamilton, Peter Boyce, Natalie Bartlett, Denali Tietjen, Eric Tarczynski, Will Robbins, Jasmine Kriston, Alicia Lau, Johnny Hammond, Bruno Faviero, Athena Kan, Shohini Gupta, Alex Immerman, Albert Dong, Phillip Hua-Bon-Hoa, and Trevor Sookraj for your incredible encouragement, support, and insight during the writing of this essay.

Powered by WPeMatico