Italy

Auto Added by WPeMatico

Auto Added by WPeMatico

The UK has given up building a centralized coronavirus contacts-tracing app and will instead switch to a decentralized app architecture, the BBC has reported. This suggests its any future app will be capable of plugging into the joint ‘exposure notification’ API which has been developed in recent weeks by Apple and Google.

The UK’s decision to abandon a bespoke app architecture comes more than a month after ministers had been reported to be eyeing such a switch. They went on to award a contract to an IT supplier to develop a decentralized tracing app in parallel as a backup — while continuing to test the centralized app, which is called NHS COVID-19.

At the same time, a number of European countries have now successfully launched contracts-tracing apps with a decentralized app architecture that’s able to plug into the ‘Gapple’ API — including Denmark, Germany, Italy, Latvia and Switzerland. Several more such apps remain in testing. While EU Member States just agreed on a technical framework to enable cross-border interoperability of apps based on the same architecture.

Germany — which launched the decentralized ‘Corona Warning App’ this week — announced its software had been downloaded 6.5M times in the first 24 hours. The country had initially appeared to favor a centralized approach but switched to a decentralized model back in April in the face of pushback from privacy and security experts.

The UK’s NHS COVID-19 app, meanwhile, has not progressed past field tests, after facing a plethora of technical barriers and privacy challenges — as a direct consequence of the government’s decision to opt for a proprietary system which uploads proximity data to a central server, rather than processing exposure notifications locally on device.

Apple and Google’s API, which is being used by all Europe’s decentralized apps, does not support centralized app architectures — meaning the UK app faced technical hurdles related to accessing Bluetooth in the background. The centralized choice also raised big questions around cross-border interoperability, as we’ve explained before. Questions had also been raised over the risk of mission creep and a lack of transparency and legal certainty over what would be done with people’s data.

So the UK’s move to abandon the approach and adopt a decentralized model is hardly surprising — although the time it’s taken the government to arrive at the obvious conclusion does raise some major questions over its competence at handling technology projects.

Michael Veale, a lecturer in digital rights and regulation at UCL — who has been involved in the development of the DP3T decentralized contacts-tracing standard, which influenced Apple and Google’s choice of API — welcomed the UK’s decision to ditch a centralized app architecture but questioned why the government has wasted so much time.

“This is a welcome, if a heavily and unnecessarily delayed, move by NHSX,” Veale told TechCrunch. “The Google -Apple system in a way is home-grown: Originating with research at a large consortium of universities led by Switzerland and including UCL in the UK. NHSX has no end of options and no reasonable excuse to not get the app out quickly now. Germany and Switzerland both have high quality open source code that can be easily adapted. The NHS England app will now be compatible with Northern Ireland, the Republic of Ireland, and also the many destinations for holidaymakers in and out of the UK.”

Perhaps unsurprisingly, UK ministers are now heavily de-emphasizing the importance of having an app in the fight against the coronavirus at all.

The Department for Health and Social Care’s, Lord Bethell, told the Science and Technology Committee yesterday the app will not now be ready until the winter. “We’re seeking to get something going for the winter, but it isn’t a priority for us,” he said.

Yet the centralized version of the NHS COVID-19 app has been in testing in a limited geographical pilot on the Isle of Wight since early May — and up until the middle of last month health minister, Matt Hancock, had said it would be rolled out nationally in mid May.

Of course that timeframe came and went without launch. And now the prospect of the UK having an app at all is being booted right into the back end of the year.

Compare and contrast that with government messaging at its daily coronavirus briefings back in May — when Hancock made “download the app” one of the key slogans — and the word ‘omnishambles‘ springs to mind…

NHSX relayed our request for comment on the switch to a decentralized system and the new timeframe for an app launch to the Department of Health and Social Care (DHSC) — but the department had not responded to us at the time of publication.

Earlier this week the BBC reported that a former Apple executive, Simon Thompson, was taking charge of the delayed app project — while the two lead managers, the NHSX’s Matthew Gould and Geraint Lewis — were reported to be stepping back.

Back in April, Gould told the Science and Technology Committee the app would “technically” be ready to launch in 2-3 weeks’ time, though he also said any national launch would depend on the preparedness of a wider government program of coronavirus testing and manual contacts tracing. He also emphasized the need for a major PR campaign to educate the public on downloading and using the app.

Government briefings to the press today have included suggestions that app testers on the Isle of Wight told it they were not comfortable receiving COVID-19 notifications via text message — and that the human touch of a phone call is preferred.

However none of the European countries that have already deployed contacts-tracing apps has promoted the software as a one-stop panacea for tackling COVID-19. Rather tracing apps are intended to supplement manual contacts-tracing methods — the latter involving the use of trained humans making phone calls to people who have been diagnosed with COVID-19 to ask who they might have been in contact with over the infectious period.

Even with major resource put into manual contacts-tracing, apps — which use Bluetooth signals to estimate proximity between smartphone users in order to calculate virus expose risk — could still play an important role by, for example, being able to trace strangers who are sat near an infected person on public transport.

Update: The DHSC has now issued a statement addressing reports of the switch of app architecture for the NHS COVID-19 app — in which it confirms, in between reams of blame-shifting spin, that it’s testing a new app that is able to plug into the Apple and Google API — and which it says it may go on to launch nationally, but without providing any time frame.

It also claims it’s working with Apple and Google to try to enhance how their technology estimates the distance between smartphone users.

“Through the systematic testing, a number of technical challenges were identified — including the reliability of detecting contacts on specific operating systems — which cannot be resolved in isolation with the app in its current form,” DHSC writes of the centralized NHS COVID-19 app.

“While it does not yet present a viable solution, at this stage an app based on the Google / Apple API appears most likely to address some of the specific limitations identified through our field testing. However, there is still more work to do on the Google / Apple solution which does not currently estimate distance in the way required.”

“Based on this, the focus of work will shift from the current app design and to work instead with Google and Apple to understand how using their solution can meet the specific needs of the public,” it adds.

We reached out to Apple and Google for comment. Apple declined to comment.

According to one source, the UK has been pressing for the tech giants’ API to include device model and RSSI info alongside the ephemeral IDs which devices that come into proximity exchange with each other — presumably to try to improve distance calculations via a better understanding of the specific hardware involved.

However introducing additional, fixed pieces of device-linked data would have the effect of undermining the privacy protections baked into the decentralized system — which uses ephemeral, rotating IDs in order to prevent third party tracking of app users. Any fixed data-points being exchanged would risk unpicking the whole anti-tracking approach.

Norway, another European country which opted for a centralized approach for coronavirus contacts tracing — but got an app launched in mid April — made the decision to suspend its operation this week, after an intervention by the national privacy watchdog. In that case the app was collecting both GPS and Bluetooth — posing a massive privacy risk. The watchdog warned the public health agency the tool was no longer a proportionate intervention — owing to what are now low levels of coronavirus risk in the country.

Powered by WPeMatico

Finland-based Swappie has closed a €35.8 million ($40.6M) Series B to expand into new markets in Europe. The ecommerce business refurbishes and resells used iPhones, taking care of the entire process from testing and repairing used handsets, to selling the refurbished devices via its own marketplace, with a 12-month warranty.

Local VC and private equity firm TESI is a new investor in the Series B, along with Lifeline Ventures, Reaktor Ventures and Inventure Investors, all of whom participated in Swappie’s 2019 Series A. The total raised to date since the business was founded in 2016 is $48M.

Right now Swappie operates in Finland, Sweden, Denmark and Italy. The new financing will be used to expand across Europe, beginning with launches in Germany, Ireland, Portugal and the Netherlands this summer.

It’s also eyeing expansion beyond Europe — so will be speccing out a broader roadmap for the future.

“The main focus of this round is to become the number one player in Europe. But also to explore opportunities outside Europe as well,” says CEO and co-founder Sami Marttinen. “That’s something we will be looking into but no concrete plans to announce at this point.

“There are still opportunities for our business model everywhere in the world. So it’s a matter of just building the roadmap — where to go next.”

Swappie’s Jiri Heinonen (CMO) and Sami Marttinen (CEO) (Photo credit: Swappie)

Swappie touts growing consumer demand in the region to buy refurbished phones, saying that from 2018 to 2019 revenues grew 4x, hitting $35M+ in net revenue in 2019. It’s also seeing demand continuing to grow this year — recording a 5x increase in net revenue growth in April and May 2020 vs the same period last year, despite the ongoing COVID-19 pandemic. Indeed, the trend of consumers shifting to buying more online looks to be a help for its online marketplace.

Commenting on Swappie’s Series B in a statement, Tony Nysten, Investment Manager at TESI, said: “We believe there is a huge growth opportunity for Swappie. The smartphone market in Europe is worth over €100BN but used or refurbished phones currently make up just over 10% of that and only one in four pre-owned phones are currently re-sold. Through its rapid growth to date, Swappie has proven its ability to not just grow market share within the refurbished market, but to expand the size of the category overall. The business has enormous potential.”

Swappie’s early choice of market focus included not only familiar turf in the Nordics — but Italy, in Southern Europe. The latter was chosen deliberately on account of it being a tough market for ecommerce, per Marttinen.

“In the really early days the reason why we went to Italy was because it was one of the toughest ecommerce markets in Europe — they have a really low ecommerce maturity index. It’s very different in terms of shopping behavior. You need to build another level of trust in that market. There are lots of unique traits like cash on delivery, things like that. So we knew that in order to really conquer the market globally — and to be able to deliver on our global ambitions we would need to enter as difficult markets as early in our journey as possible.

“These days we have a much more advanced playbook and market studies across Europe.”

Swappie describes itself as a ‘scale-up’ tech business on account of addressing the whole value chain, per Marttinen.

“We’ve done a lot there on the hardware side — when it comes to actually refurbishing the devices we can make them even stronger then the original devices in many cases. So that means we can go as deep as onto the motherboard level in the repairs. Then on the software side, of course, we’re making selling and distribution and everything else scalable. Making sure that the checking processes and all the processes in the factory are according to the latest standards,” he says.

“Because of being so focused in also building the processes and focusing on the quality so much, so actually we have been able to truly change the way people consume electronics,” he adds. “If you think about it from a local player perspective they are typically mostly competing for the people who are already buying used devices — whereas we are able to deliver on this market by having full control of the entire value chain, from buying to refurbishing, to selling the phones to consumers.

“Most of our customers are buying used or refurbished devices for the first time — so actually our biggest competitors are new smartphone retailers.”

The most popular iPhone model sold on Swappie’s marketplace last year was the iPhone 8, per Marttinen.

He won’t disclosed the exact number of iPhones Swappie has refurbished and sold at this point but he says it’s a six-figure number — aka ‘hundreds of thousands’.

The team chose to focus on iPhones to ensure they can deliver the highest quality device refurbishment, he says, while also benefiting from the relatively higher cost of Apple’s smartphone hardware vs Android devices. Though he doesn’t rule out expanding to offer another type of refurbished smartphone in future.

“The business is now growing really rapidly but what we noticed in the early days is that the new device prices had started to rise before we started this business so we have been very lucky with the timing,” he tells TechCrunch, noting that Swappie also benefitted from the plateauing into advancements between handset models in recent years, as the technology matured.

“If you can build trust into this business, and make sure that the phones function as well as new devices — and that you’re actually making the buying process as well as safe as buying a new phone — that way you can actually accelerate the growth of the market. So that’s what we have been really successful in. It’s kind of the key to being able to grow so quickly.”

“One main point there has been that because we refurbish every device ourselves in our own factory in Finland we can deliver to customers the highest quality devices under warranty for much less than the cost of a new phone and also be more environmentally friendly,” he adds.

While, in years past, there have been instances of iPhone users’ devices bricked after a repair by an unauthorized repair shop Marttinen says Swappie is using only original iPhone parts so has avoided such problems.

He also points to recent European Commission proposals for a pan-EU ‘right to repair’ for electronics which suggests device makers selling in the region will be required to respect repairability, rather than using software updates as a way to penalize consumers who seek to extend the lifespan of their current device.

Photo credit: Swappie

Swappie’s business also slots into a wider Commission mission to transition the EU to a circular economy, as part of the green deal announced by current president, Ursula von der Leyen — so it’s skating to where the puck is headed, if you like.

“It’s really good for the environment that the right to repair legislation has come forward in the past few years. That’s one very important point for us as well which was one of the reasons why we wanted to built microscope level repairs in our factories — so we wouldn’t have to scrap as many phones as you normally would,” Marttinen adds.

What can’t it repair? The proportion of iPhones which turn out to be truly unsalvageable via its processes is “extremely small“, he says. “We can actually do any repairs that are possible to do the phones so, basically, water damaged phones which have been at the bottom of the ocean — those are of course unrepairable. Or if the phone is bent too much or if the motherboard is completely ruined. But basically all the other faults we can repair.”

On the competitive front, he says Swappie’s main rival are retailers selling new iPhones — given it’s trying to woo iOS users away from buying a brand new iPhone. On the secondhand marketplace front Marttinen mentions reBuy as one of the main rival players in refurbishing and reselling electronics, though it does not focus on iPhones — offering a full range of devices, from wearables to smartphones and tablets, laptops, consoles and cameras.

Powered by WPeMatico

Google is giving the world a clearer glimpse of exactly how much it knows about people everywhere — using the coronavirus crisis as an opportunity to repackage its persistent tracking of where users go and what they do as a public good in the midst of a pandemic.

In a blog post today, the tech giant announced the publication of what it’s branding COVID-19 Community Mobility Reports, an in-house analysis of the much more granular location data it maps and tracks to fuel its ad-targeting, product development and wider commercial strategy to showcase aggregated changes in population movements around the world.

The coronavirus pandemic has generated a worldwide scramble for tools and data to inform government responses. In the EU, for example, the European Commission has been leaning on telcos to hand over anonymized and aggregated location data to model the spread of COVID-19.

Google’s data dump looks intended to dangle a similar idea of public policy utility while providing an eyeball-grabbing public snapshot of mobility shifts via data pulled off of its global user-base.

In terms of actual utility for policymakers, Google’s suggestions are pretty vague. The reports could help government and public health officials “understand changes in essential trips that can shape recommendations on business hours or inform delivery service offerings,” it writes.

“Similarly, persistent visits to transportation hubs might indicate the need to add additional buses or trains in order to allow people who need to travel room to spread out for social distancing,” it goes on. “Ultimately, understanding not only whether people are traveling, but also trends in destinations, can help officials design guidance to protect public health and essential needs of communities.”

The location data Google is making public is similarly fuzzy — to avoid inviting a privacy storm — with the company writing it’s using “the same world-class anonymization technology that we use in our products every day,” as it puts it.

“For these reports, we use differential privacy, which adds artificial noise to our datasets enabling high quality results without identifying any individual person,” Google writes. “The insights are created with aggregated, anonymized sets of data from users who have turned on the Location History setting, which is off by default.”

“In Google Maps, we use aggregated, anonymized data showing how busy certain types of places are—helping identify when a local business tends to be the most crowded. We have heard from public health officials that this same type of aggregated, anonymized data could be helpful as they make critical decisions to combat COVID-19,” it adds, tacitly linking an existing offering in Google Maps to a coronavirus-busting cause.

The reports consist of per country, or per state, downloads (with 131 countries covered initially), further broken down into regions/counties — with Google offering an analysis of how community mobility has changed vs a baseline average before COVID-19 arrived to change everything.

So, for example, a March 29 report for the whole of the U.S. shows a 47 percent drop in retail and recreation activity vs the pre-CV period; a 22% drop in grocery & pharmacy; and a 19% drop in visits to parks and beaches, per Google’s data.

While the same date report for California shows a considerably greater drop in the latter (down 38% compared to the regional baseline); and slightly bigger decreases in both retail and recreation activity (down 50%) and grocery & pharmacy (-24%).

Google says it’s using “aggregated, anonymized data to chart movement trends over time by geography, across different high-level categories of places such as retail and recreation, groceries and pharmacies, parks, transit stations, workplaces, and residential.” The trends are displayed over several weeks, with the most recent information representing 48-to-72 hours prior, it adds.

The company says it’s not publishing the “absolute number of visits” as a privacy step, adding: “To protect people’s privacy, no personally identifiable information, like an individual’s location, contacts or movement, is made available at any point.”

Google’s location mobility report for Italy, which remains the European country hardest hit by the virus, illustrates the extent of the change from lockdown measures applied to the population — with retail & recreation dropping 94% vs Google’s baseline; grocery & pharmacy down 85%; and a 90% drop in trips to parks and beaches.

The same report shows an 87% drop in activity at transit stations; a 63% drop in activity at workplaces; and an increase of almost a quarter (24%) of activity in residential locations — as many Italians stay at home instead of commuting to work.

It’s a similar story in Spain — another country hard-hit by COVID-19. Though Google’s data for France suggests instructions to stay-at-home may not be being quite as keenly observed by its users there, with only an 18% increase in activity at residential locations and a 56% drop in activity at workplaces. (Perhaps because the pandemic has so far had a less severe impact on France, although numbers of confirmed cases and deaths continue to rise across the region.)

While policymakers have been scrambling for data and tools to inform their responses to COVID-19, privacy experts and civil liberties campaigners have rushed to voice concerns about the impacts of such data-fueled efforts on individual rights, while also querying the wider utility of some of this tracking.

And yes, the disclaimer is very broad. I’d say, this is largely a PR move.

Apart from this, Google must be held accountable for its many other secondary data uses. And Google/Alphabet is far too powerful, which must be addressed at several levels, soon. https://t.co/oksJgQAPAY

— Wolfie Christl (@WolfieChristl) April 3, 2020

Contacts tracing is another area where apps are fast being touted as a potential solution to get the West out of economically crushing population lockdowns — opening up the possibility of people’s mobile devices becoming a tool to enforce lockdowns, as has happened in China.

“Large-scale collection of personal data can quickly lead to mass surveillance,” is the succinct warning of a trio of academics from London’s Imperial College’s Computational Privacy Group, who have compiled their privacy concerns vis-a-vis COVID-19 contacts tracing apps into a set of eight questions app developers should be asking.

Discussing Google’s release of mobile location data for a COVID-19 cause, the head of the group, Yves-Alexandre de Montjoye, gave a general thumbs up to the steps it’s taken to shrink privacy risks. Although he also called for Google to provide more detail about the technical processes it’s using in order that external researchers can better assess the robustness of the claimed privacy protections. Such scrutiny is of pressing importance with so much coronavirus-related data grabbing going on right now, he argues.

“It is all aggregated; they normalize to a specific set of dates; they threshold when there are too few people and on top of this they add noise to make — according to them — the data differentially private. So from a pure anonymization perspective it’s good work,” de Montjoye told TechCrunch, discussing the technical side of Google’s release of location data. “Those are three of the big ‘levers’ that you can use to limit risk. And I think it’s well done.”

“But — especially in times like this when there’s a lot of people using data — I think what we would have liked is more details. There’s a lot of assumptions on thresholding, on how do you apply differential privacy, right?… What kind of assumptions are you making?” he added, querying how much noise Google is adding to the data, for example. “It would be good to have a bit more detail on how they applied [differential privacy]… Especially in times like this it is good to be… overly transparent.”

While Google’s mobility data release might appear to overlap in purpose with the Commission’s call for EU telco metadata for COVID-19 tracking, de Montjoye points out there are likely to be key differences based on the different data sources.

“It’s always a trade off between the two,” he says. “It’s basically telco data would probably be less fine-grained, because GPS is much more precise spatially and you might have more data points per person per day with GPS than what you get with mobile phone but on the other hand the carrier/telco data is much more representative — it’s not only smartphone, and it’s not only people who have latitude on, it’s everyone in the country, including non smartphone.”

There may be country specific questions that could be better addressed by working with a local carrier, he also suggested. (The Commission has said it’s intending to have one carrier per EU Member State providing anonymized and aggregated metadata.)

On the topical question of whether location data can ever be truly anonymized, de Montjoye — an expert in data reidentification — gave a “yes and no” response, arguing that original location data is “probably really, really hard to anonymize”.

“Can you process this data and make the aggregate results anonymous? Probably, probably, probably yes — it always depends. But then it also means that the original data exists… Then it’s mostly a question of the controls you have in place to ensure the process that leads to generating those aggregates does not contain privacy risks,” he added.

Perhaps a bigger question related to Google’s location data dump is around the issue of legal consent to be tracking people in the first place.

While the tech giant claims the data is based on opt-ins to location tracking the company was fined $57M by France’s data watchdog last year for a lack of transparency over how it uses people’s data.

Then, earlier this year, the Irish Data Protection Commission (DPC) — now the lead privacy regulator for Google in Europe — confirmed a formal probe of the company’s location tracking activity, following a 2018 complaint by EU consumers groups which accuses Google of using manipulative tactics in order to keep tracking web users’ locations for ad-targeting purposes.

“The issues raised within the concerns relate to the legality of Google’s processing of location data and the transparency surrounding that processing,” said the DPC in a statement in February, announcing the investigation.

The legal questions hanging over Google’s consent to track people likely explains the repeat references in its blog post to people choosing to opt in and having the ability to clear their Location History via settings. (“Users who have Location History turned on can choose to turn the setting off at any time from their Google Account, and can always delete Location History data directly from their Timeline,” it writes in one example.)

In addition to offering up coronavirus mobility porn reports — which Google specifies it will continue to do throughout the crisis — the company says it’s collaborating with “select epidemiologists working on COVID-19 with updates to an existing aggregate, anonymized dataset that can be used to better understand and forecast the pandemic.”

“Data of this type has helped researchers look into predicting epidemics, plan urban and transit infrastructure, and understand people’s mobility and responses to conflict and natural disasters,” it adds.

Powered by WPeMatico

Vancouver-based mobility startup Damon Motorcycles has entered the EV arena with a preview of its first e-moto, the Hypersport Pro.

The seed-stage company had previously focused on creating digital safety technology — like its 360-degree radar detection system — to augment two-wheelers made by other manufacturers.

Damon has determined to create its own EV model designed to overcome common flaws it sees in existing motorcycle offerings.

“We are for the first time being black and white about the fact that we are a full-on producer and we have a motorcycle we’re going to unveil at CES,” Damon Motorcycle founder and CEO Jay Giraud told TechCrunch.

That machine is the fully electric Damon Hypersport Pro. The news is a pre-announcement ahead of the full January debut, so Giraud would not offer much in the way of core specs — such as price, range, charge-time and performance.

He was clear the motorcycle is meant to be a direct competitor to the latest e-motos released by Harley-Davidson and California-based venture Zero Motorcycles — and to the gas-motorcycle market overall.

“We’ve come at this and the motorcycle problem in a way that no other company has,” Giraud explained.

“We’re trying to change the industry by addressing the issues of safety and handling and comfort and the problems that have persisted with everyone in the industry, including all the e-moto companies today.”

Damon’s Hypersport Pro is designed around the company’s CoPilot system, which uses sensors, radar and cameras to detect and track moving objects around the motorcycle, including blind spots, and alert riders to danger.

Damon has also taken on the problem of one-size-fits-all in motorcycle design, integrating a system on its Hypersport Pro that allows for adjustable ergonomics. The startup’s debut model will allow riders to electronically shift the motorcycle’s windscreen, seat, footpegs and handlebars to accommodate for different positions and conditions — from more upright city riding to more aggressive high-speed runs.

Damon Motorcycles is taking pre-orders for its Hypersport Pro and will skip dealers, opting to use a direct-sales and service model similar to Tesla . The startup’s Vancouver facility is equipped to build 500 motorcycles a year, according to Giraud.

The company recently brought on Derek Dorresteyn, the former CTO of e-moto startup Alta, as its COO. Full specs of the Hypersport Pro will come next month at CES, but Giraud did offer a glimpse, saying it would be more competitive and more powerful than existing e-moto offerings.

The company recently brought on Derek Dorresteyn, the former CTO of e-moto startup Alta, as its COO. Full specs of the Hypersport Pro will come next month at CES, but Giraud did offer a glimpse, saying it would be more competitive and more powerful than existing e-moto offerings.

Harley-Davidson released its first e-motorcycle — the $29K LiveWire — in 2019 and California EV startup Zero Motorcycles launched its $19K SR/F, both in bids to go take e-motos mass-market. Aside from the price-gap, both have comparable charge times (about an hour), performance and range (around 100 miles for combined city and highway riding).

The U.S. motorcycle industry has been in pretty bad shape since the recession. New sales dropped by roughly 50% since 2008 — with sharp declines in ownership by everyone under 40 — and have never recovered.

Harley-Davidon’s EV pivot is likely to bring e-moto offerings from the other large gas manufacturers, such as Honda and Yamaha, which are also attempting to revive sales to younger riders.

Harley-Davidson’s LiveWire

With Damon’s pivot to e-moto production, the startup is not alone. Italy’s Energica is expanding distribution of its high-performance EVs in the U.S. Other competitors include e-moto startup Fuell, with plans to release its $10K, 150-mile range Flow in the near future.

Of course, there have already been some speed bumps and market attrition, with three e-moto startups — Alta Motors, Mission Motors and Brammo — forced to power down over the last several years.

So how does Damon Motors plan to succeed as a new entrant in a motorcycle market with stagnant new bikes sales and increased EV competition from established OEMs and startups?

“We have so many advantages the others don’t have and we’re leveraging everyone of their weaknesses,” founder Jay Giraud said. The company’s direct-sale model will lend to more competitive pricing and higher margins for R&D, he said.

Then there are what Damon Motorcycles sees as its Hypersport Pro’s purposely designed comparative advantages over existing manufacturers.

“You’re gonna love the horsepower and range and all that good stuff, but that’s not what makes Damon different from every one else,” explained Giraud.

“What’s different is that it’s a safer motorbike with the safety features and transforming ergonomics that will keep you from smashing into someone’s car,” he said.

Not crashing into other people’s cars is certainly a compelling feature to offer in a motorcycle. Time and sales will ultimately tell how Damon fares in the inevitable cycle of events — profitability, failure, acquisition — that will play out in the increasingly competitive e-moto space.

Powered by WPeMatico

Imagine a moving tower made of huge cement bricks weighing 35 metric tons. The movement of these massive blocks is powered by wind or solar power plants and is a way to store the energy those plants generate. Software controls the movement of the blocks automatically, responding to changes in power availability across an electric grid to charge and discharge the power that’s being generated.

The development of this technology is the culmination of years of work at Idealab, the Pasadena, Calif.-based startup incubator, and Energy Vault, the company it spun out to commercialize the technology, has just raised $110 million from SoftBank Vision Fund to take its next steps in the world.

Energy storage remains one of the largest obstacles to the large-scale rollout of renewable energy technologies on utility grids, but utilities, development agencies and private companies are investing billions to bring new energy storage capabilities to market as the technology to store energy improves.

The investment in Energy Vault is just one indicator of the massive market that investors see coming as power companies spend billions on renewables and storage. As The Wall Street Journal reported over the weekend, ScottishPower, the U.K.-based utility, is committing to spending $7.2 billion on renewable energy, grid upgrades and storage technologies between 2018 and 2022.

Meanwhile, out in the wilds of Utah, the American subsidiary of Japan’s Mitsubishi Hitachi Power Systems is working on a joint venture that would create the world’s largest clean energy storage facility. That 1 gigawatt storage would go a long way toward providing renewable power to the Western U.S. power grid and is going to be based on compressed air energy storage, large flow batteries, solid oxide fuel cells and renewable hydrogen storage.

“For 20 years, we’ve been reducing carbon emissions of the U.S. power grid using natural gas in combination with renewable power to replace retiring coal-fired power generation. In California and other states in the western United States, which will soon have retired all of their coal-fired power generation, we need the next step in decarbonization. Mixing natural gas and storage, and eventually using 100% renewable storage, is that next step,” said Paul Browning, president and CEO of MHPS Americas.

Energy Vault’s technology could also be used in these kinds of remote locations, according to chief executive Robert Piconi.

Energy Vault’s storage technology certainly isn’t going to be ubiquitous in highly populated areas, but the company’s towers of blocks can work well in remote locations and have a lower cost than chemical storage options, Piconi said.

“What you’re seeing there on some of the battery side is the need in the market for a mobile solution that isn’t tied to topography,” Piconi said. “We obviously aren’t putting these systems in urban areas or the middle of cities.”

For areas that need larger-scale storage that’s a bit more flexible there are storage solutions like Tesla’s new Megapack.

The Megapack comes fully assembled — including battery modules, bi-directional inverters, a thermal management system, an AC breaker and controls — and can store up to 3 megawatt-hours of energy with a 1.5 megawatt inverter capacity.

The Energy Vault storage system is made for much, much larger storage capacity. Each tower can store between 20 and 80 megawatt hours at a cost of 6 cents per kilowatt hour (on a levelized cost basis), according to Piconi.

The first facility that Energy Vault is developing is a 35 megawatt-hour system in Northern Italy, and there are other undisclosed contracts with an undisclosed number of customers on four continents, according to the company.

One place where Piconi sees particular applicability for Energy Vault’s technology is around desalination plants in places like sub-Saharan Africa or desert areas.

Backing Energy Vault’s new storage technology are a clutch of investors, including Neotribe Ventures, Cemex Ventures, Idealab and SoftBank.

Powered by WPeMatico

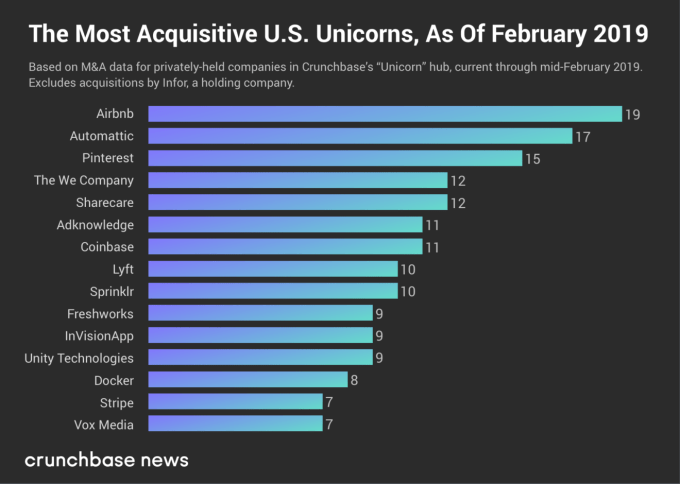

It takes a lot more than a good idea and the right timing to build a billion-dollar company. Talent, focus, operational effectiveness and a healthy dose of luck are all components of a successful tech startup. Many of the most successful (or, at least, highest-valued) tech unicorns today didn’t get there alone.

Mergers and acquisitions (M&A) can be a major growth vector for rapidly scaling, highly valued technology companies. It’s a topic that we’ve covered off and on since the very first post on Crunchbase News in March 2017. Nearly two years later, we wanted to revisit that first post because things move quickly, and there is a new crop of companies in the unicorn spotlight these days. Which ones are the most active in the M&A market these days?

Before displaying the U.S. unicorns with the most acquisitions to date, we first have to answer the question, “What is a unicorn?” The term is generally applied to venture-backed technology companies that have earned a valuation of $1 billion or more. Crunchbase tracks these companies in its Unicorns hub. The original definition of the term, first applied in a VC setting by Aileen Lee of Cowboy Ventures back in late 2011, specifies that unicorns were founded in or after 2003, following the first tech bubble. That’s the working definition we’ll be using here.

In the chart below, we display the number of known acquisitions made by U.S.-based unicorns that haven’t gone public or gotten acquired (yet). Keep in mind this is based on a snapshot of Crunchbase data, so the numbers and ranking may have changed by the time you read this. To maintain legibility and a reasonable size, we cut off the chart at companies that made seven or more acquisitions.

As one would expect, these rankings are somewhat different from the one we did two years ago. Several companies counted back in early March 2017 have since graduated to public markets or have been acquired.

Dropbox, which had acquired 23 companies at the time of our last analysis, went public weeks later and has since acquired two more companies (HelloSign for $230 million in late January 2019 and Verst for an undisclosed sum in November 2017) since doing so. SurveyMonkey, which went public in September 2018, made six known acquisitions before making its exit via IPO.

Which companies are still in the top ranks? Travel accommodations marketplace giant Airbnb jumped from number four to claim Dropbox’s vacancy as the most acquisitive private U.S. unicorn in the market. Airbnb made six more acquisitions since March 2017, most recently Danish event space and meeting venue marketplace Gaest.com. The still-pending deal was announced in January 2019.

WordPress developer and hosting company Automattic is still ranked number two. Automattic href=”https://www.crunchbase.com/acquisition/automattic-acquires-atavist–912abccd”>acquired one more company — digital publication platform Atavist — since we last profiled unicorn M&A. Open-source software containerization company Docker, photo-sharing and search site Pinterest, enterprise social media management company Sprinklr and venture-backed media company Vox Media remain, as well.

There are some notable newcomers in these rankings. We’ll focus on the most notable three: The We Company, Coinbase and Lyft. (Honorable mention goes to Stripe and Unity Technologies, which are also new to this list.)

The We Company (the holding entity for WeWork) has made 10 acquisitions over the past two years. Earlier this month, The We Company bought Euclid, a company that analyzes physical space utilization and tracks visitors using Wi-Fi fingerprinting. Other buyouts include Meetup (a story broken by Crunchbase News in November 2017) reportedly for $200 million. Also in late 2017, The We Company acquired coding and design training program Flatiron School, giving the company a permanent tenant in some of its commercial spaces.

In its bid to solidify its position as the dominant consumer cryptocurrency player, Coinbase has been on quite the M&A tear lately. The company recently announced its plans to acquire Neutrino, a blockchain analytics and intelligence platform company based in Italy. As we covered, Coinbase likely made the deal to improve its compliance efforts. In January, Coinbase acquired data analysis company Blockspring, also for an undisclosed sum. The crypto company’s other most notable deal to date was its April 2018 buyout of the bitcoin mining hardware turned cryptocurrency micro-transaction platform Earn.com, which Coinbase acquired for $120 million.

And finally, there’s Lyft, the more exclusively U.S.-focused ride-hailing and transportation service company. Lyft has made 10 known acquisitions since it was founded in 2012. Its latest M&A deal was urban bike service Motivate, which Lyft acquired in June 2018. Lyft’s principal rival, Uber, has acquired six companies at the time of writing. Uber bought a bike company of its own, JUMP Bikes, at a price of $200 million, a couple of months prior to Lyft’s Motivate purchase. Here too, the Lyft-Uber rivalry manifests in structural sameness. Fierce competition drove Uber and Lyft to raise money in lock-step with one another, and drove M&A strategy as well.

With long-term business success, it’s often a chicken-and-egg question. Is a company successful because of the startups it bought along the way? Or did it buy companies because it was successful and had an opening to expand? Oftentimes, it’s a little of both.

The unicorn companies that dominate the private funding landscape today (if not in the number of deals, then in dollar volume for sure) continue to raise money in the name of growth. Growth can come the old-fashioned way, by establishing a market position and expanding it. Or, in the name of rapid scaling and ostensibly maximizing investor returns, M&A provides a lateral route into new markets or a way to further entrench the status quo. We’ll see how that strategy pays off when these companies eventually find the exit door .

Powered by WPeMatico

We’re three weeks into January. We’ve recovered from our CES hangover and, hopefully, from the CES flu. We’ve started writing the correct year, 2019, not 2018.

Venture capitalists have gone full steam ahead with fundraising efforts, several startups have closed multi-hundred million dollar rounds, a virtual influencer raised equity funding and yet, all anyone wants to talk about is Slack’s new logo… As part of its public listing prep, Slack announced some changes to its branding this week, including a vaguely different looking logo. Considering the flack the $7 billion startup received instantaneously and accusations that the negative space in the logo resembled a swastika — Slack would’ve been better off leaving its original logo alone; alas…

On to more important matters.

Rubrik more than doubled its valuation

The data management startup raised a $261 million Series E funding at a $3.3 billion valuation, an increase from the $1.3 billion valuation it garnered with a previous round. In true unicorn form, Rubrik’s CEO told TechCrunch’s Ingrid Lunden it’s intentionally unprofitable: “Our goal is to build a long-term, iconic company, and so we want to become profitable but not at the cost of growth,” he said. “We are leading this market transformation while it continues to grow.”

Deal of the week: Knock gets $400M to take on Opendoor

Will 2019 be a banner year for real estate tech investment? As $4.65 billion was funneled into the space in 2018 across more than 350 deals and with high-flying startups attracting investors (Compass, Opendoor, Knock), the excitement is poised to continue. This week, Knock brought in $400 million at an undisclosed valuation to accelerate its national expansion. “We are trying to make it as easy to trade in your house as it is to trade in your car,” Knock CEO Sean Black told me.

While we’re on the subject of VCs’ favorite industries, TechCrunch cybersecurity reporter Zack Whittaker highlights some new data on venture investment in the industry. Strategic Cyber Ventures says more than $5.3 billion was funneled into companies focused on protecting networks, systems and data across the world, despite fewer deals done during the year. We can thank Tanium, CrowdStrike and Anchorfree’s massive deals for a good chunk of that activity.

Send me tips, suggestions and more to kate.clark@techcrunch.com or @KateClarkTweets.

I would be remiss not to highlight a slew of venture firms that made public their intent to raise new funds this week. Peter Thiel’s Valar Ventures filed to raise $350 million across two new funds and Redpoint Ventures set a $400 million target for two new China-focused funds. Meanwhile, Resolute Ventures closed on $75 million for its fourth early-stage fund, BlueRun Ventures nabbed $130 million for its sixth effort, Maverick Ventures announced a $382 million evergreen fund, First Round Capital introduced a new pre-seed fund that will target recent graduates, Techstars decided to double down on its corporate connections with the launch of a new venture studio and, last but not least, Lance Armstrong wrote his very first check as a VC out of his new fund, Next Ventures.

More money goes toward scooters

In case you were concerned there wasn’t enough VC investment in electric scooter startups, worry no more! Flash, a Berlin-based micro-mobility company, emerged from stealth this week with a whopping €55 million in Series A funding. Flash is already operating in Switzerland and Portugal, with plans to launch into France, Italy and Spain in 2019. Bird and Lime are in the process of raising $700 million between them, too, indicating the scooter funding extravaganza of 2018 will extend into 2019 — oh boy!

TechCrunch’s Josh Constine introduced readers to Squad this week, a screensharing app for social phone addicts.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase editor-in-chief Alex Wilhelm and I marveled at the dollars going into scooter startups, discussed Slack’s upcoming direct listing and debated how the government shutdown might impact the IPO market.

Powered by WPeMatico

Italy’s Autorità garante della concorrenza e del mercato, roughly equivalent to this America’s FTC, has fined Apple and Samsung a total of $15 million for the companies’ practice of forcing updates on consumers that may slow or break their devices. The amount may be a drop in the bucket, but it’s a signal that governments won’t always let this type of behavior fly.

The “unfair commercial practices” are described by the AGCM as follows:

The two companies have induced consumers – by insistently proposing to proceed with the download and also because of the significant information asymmetry of consumers vis-a-vis the producers – to install software updates that are not adequately supported by their devices, without adequately informing them, nor providing them an effective way to recover the full functionality of their devices.

Sounds about right!

In case you don’t remember, essentially Apple was pushing updates to iPhones last year that caused performance issues with older phones. Everyone took this as part of the usual conspiracy theory that Apple slows phones to get you to upgrade, but it turns out to have been more like a lack of testing before they shipped.

Samsung, for its part, was pushing Android Mashmallow updates to a number of its devices, but failed to consider that it would cause serious issues in Galaxy Note 4s — issues it then would charge to repair.

The issue here wasn’t the bad updates exactly, but the fact that consumers were pressured into accepting them, at cost to themselves. It would be one thing if the updates were simply made available and these issues addressed as they came up, but both companies “insistently suggested” that the updates be installed despite the problems.

In addition to this, Apple was found to have “not adequately informed consumers about some essential characteristics of lithium batteries, such as their average duration and deterioration factors, nor about the correct procedures to maintain, verify and replace batteries in order to preserve full functionality of devices.” That would be when Apple revealed to iPhone 6 owners that their batteries were not functioning correctly and that they’d have to pay for a replacement if they wanted full functionality. This information, the AGCM, suggests, ought to have been made plain from the beginning.

Samsung gets €5 million in fines and Apple gets €10 million. Those may not affect either company’s bottom line, but they are the maximum possible fines, so it’s symbolic as well. If a dozen other countries were to come to the same conclusion, the fines would really start to add up. Apple has already made some amends, but if it fell afoul of the law it still has to pay the price.

Powered by WPeMatico

Xiaomi gave Google’s well-intentioned but somewhat-stalled Android One project a major boost last year when it unveiled its first device under the program, Mi A1. That’s now joined by not one but two sequel devices, after the Chinese phone maker unveiled the Mi A2 and Mi A2 Lite at an event in Spain today.

Xiaomi in Spain? Yes, that’s right. International growth is a major part of the Xiaomi story now that it is a listed business, and Spain is one of a handful of countries in Europe where Xiaomi is aiming to make its mark. These two new A2 handsets are an early push and they’ll be available in over 40 countries, including Spain, France, Italy and 11 other European markets.

Both phones run on Android One — so none of Xiaomi’s iOS-inspired MIUI Android fork — and charge via type-C USB. The 5.99-inch A2 is the more premium option, sporting a Snapdragon 660 processor and 4GB or 6GB RAM with 32GB, 64GB or 128GB in storage. There’s a 20-megapixel front camera and dual 20-megapixel and 16-megapixel cameras on the rear. On-device storage ranges between 32GB, 64GB and 128GB.

The Mi A2 Lite is the more budget option that’s powered by a lesser Snapdragon 625 processor with 3GB or 4GB RAM, and 32GB or 64GB storage options. It comes with a smaller 5.84-inch display, there’s a 12- and 5-megapixel camera array on the reverse and a front-facing five-megapixel camera.

The A2 is priced from €249 to €279 ($291-$327) based on specs. The A2 Lite will sell for €179 or €229 ($210 or $268), against based on RAM and storage selection.

The 40 market availability mirrors the A1 launch last year, but on this occasion, Xiaomi has been busy preparing the ground in a number of countries, particularly in Europe. It has been in Spain for the past year, but it also launched local operations in France and Italy in May and tied up with CK Hutchison to sell phones in other parts of the continent via its 3 telecom business. While it isn’t operational in the U.S., Xiaomi has expanded into Mexico and it has set up partnerships with local retailers in dozens of other countries.

Xiaomi has been successful with its move into India, where it one of the top smartphone sellers, but it has not yet replicated that elsewhere outside of China so far.

China is, as you’d expect, the primary revenue market but Xiaomi is increasingly less dependent on its homeland. For 2017 sales, China represented 72 percent, but it had been 94 percent and 87 percent, respectively, in 2015 and 2016.

Powered by WPeMatico

Italian startup Freeda Media is raising a $10 million Series A round led by Alven Capital. U-Start and business angels are also participating in the round.

Freeda Media runs the popular Freeda Facebook page. With nearly 1.4 million likes, the page has an impressive reach. 24 million unique users see Freeda content every month in Italy, including 100 percent of millennial women who live in Italy. The company is also quite active on Instagram.

In other words, Freeda Media is a new media company that runs mostly on social media platforms. Many of the Facebook posts are short videos, social cuts with subtitles and quick interviews. Some posts link to Freeda’s own website for more traditional articles with text and photos. But there’s no front page per se.

With today’s funding round, the company plans to expand to other markets, starting with Spain. More interestingly, Freeda is still quite young as it took them 15 months to reach this level.

The company compares itself with other media brands for women, such as Elle, Teen Vogue, Vanity Fair, Cosmopolitan or Man Repeller. According to CrowdTangle, Freeda has a much higher engagement rate compared to its direct competitors.

Freeda Media’s business model is branded content and native advertising. But the startup is looking at other potential revenue streams. There’s clearly a risk of branded content overload for social-first media organizations. When you build a Facebook audience based on trust, your reputation can also quickly deteriorate and the algorithms can turn on you. So far, it doesn’t seem to be an issue.

Internationalization is going to be key to foster Freeda’s growth. If Freeda can replicate the same impressive numbers in multiple countries, the startup could end up convincing bigger advertisers and distributing more or less the same content in multiple countries.

Powered by WPeMatico